Singapore Home Loan Refinancing Guide 2026: When to Switch, What It Costs and How Much You Save

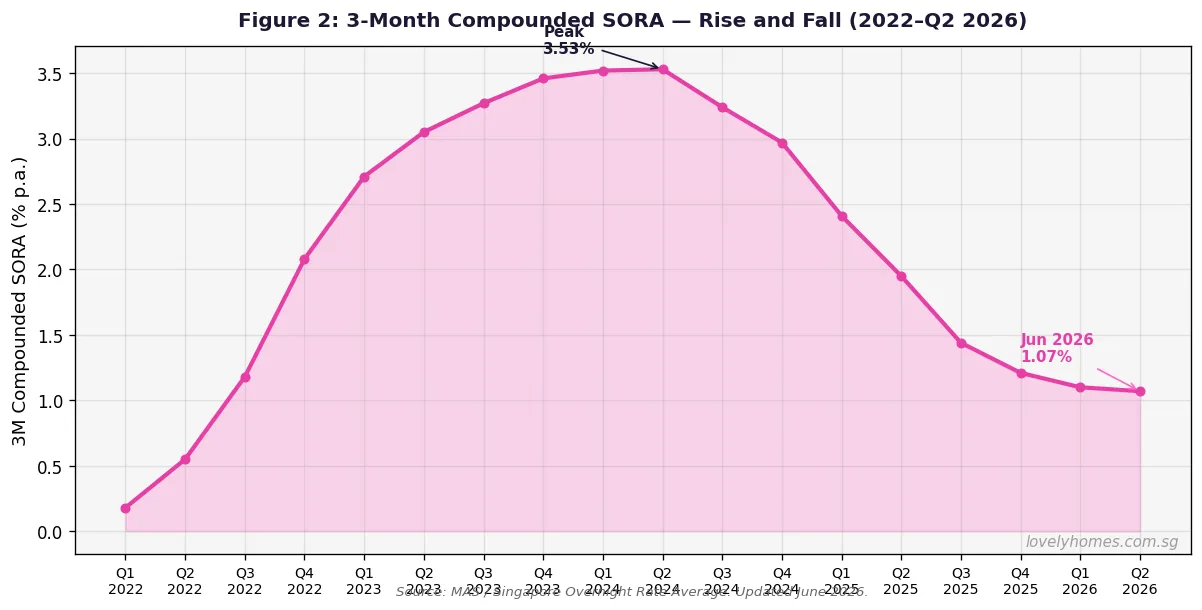

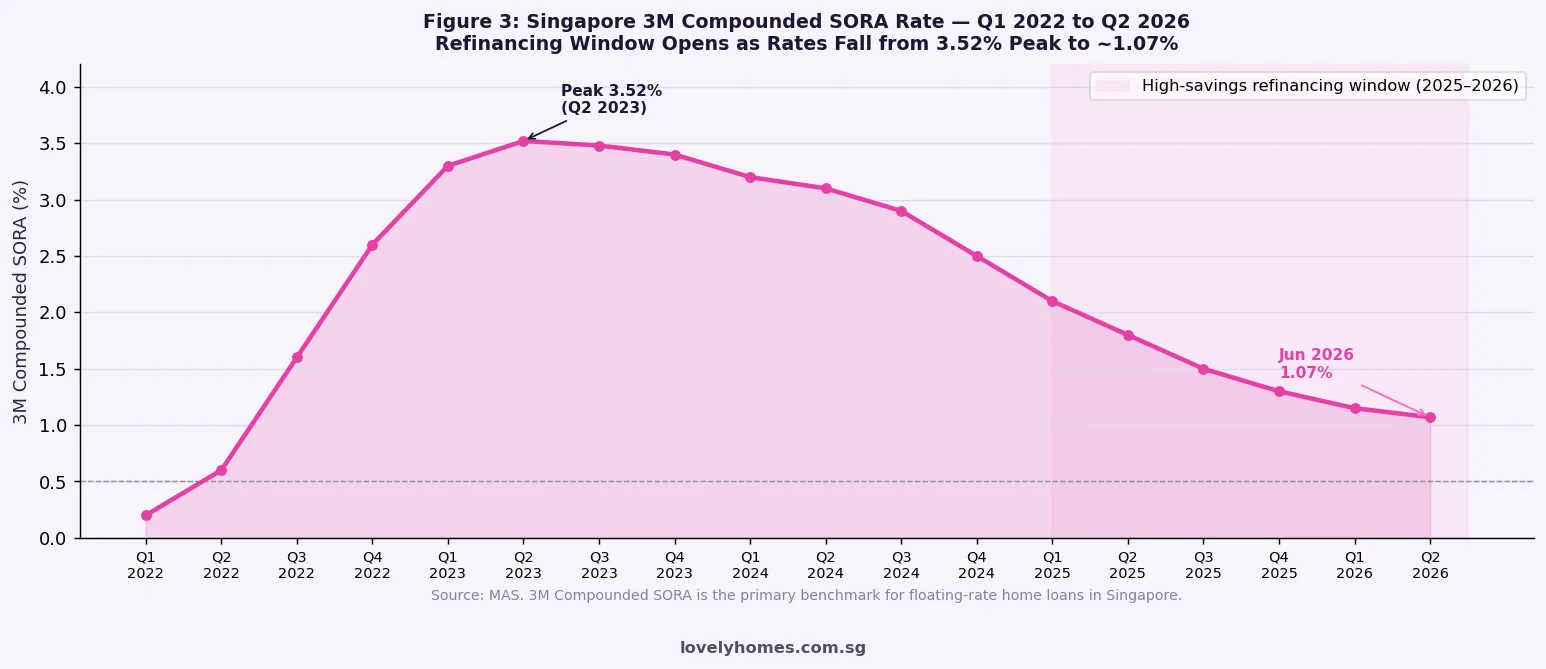

As the 3-month compounded SORA rate settles near 1.07% in June 2026 — down from its 3.52% peak in Q2 2023 — Singapore homeowners sitting on 2021–2023 vintage floating-rate loans are staring at potential savings of S$400–S$1,000 per month simply by switching lenders. This guide explains exactly when refinancing makes sense, what it costs, and how to calculate your break-even in under five minutes.

Quick Answer: Home Loan Refinancing in Singapore 2026

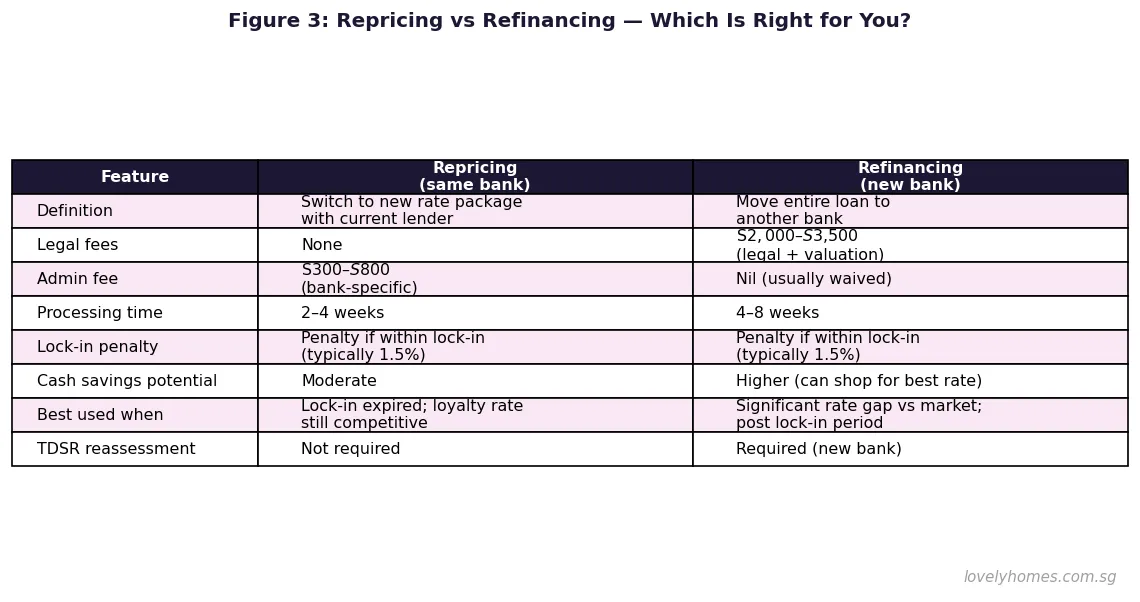

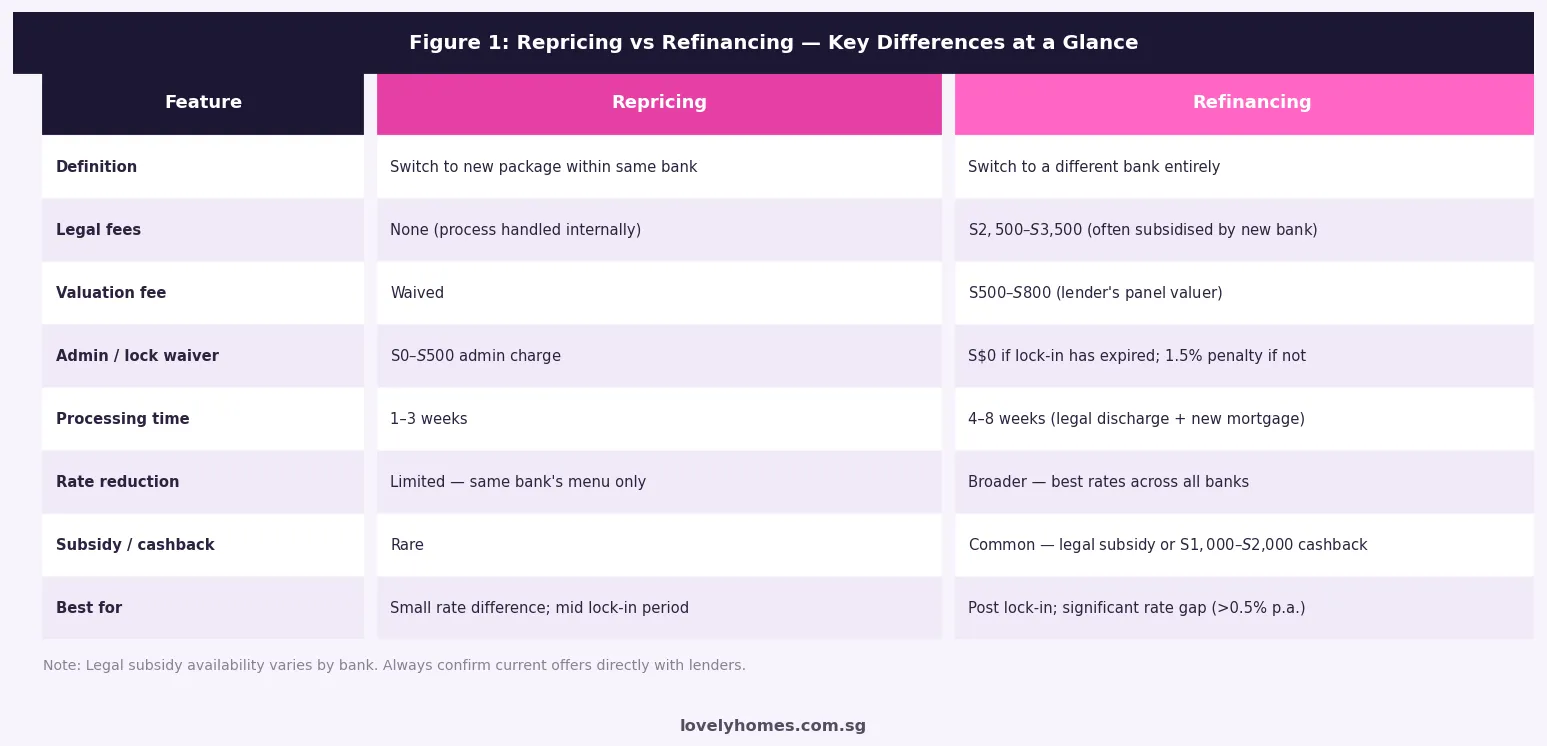

- Repricing = switching to a new package within your existing bank (no legal fees; limited rate reduction). Refinancing = switching to a new bank entirely (broader savings; legal costs of S$2,500–S$3,500, usually subsidised).

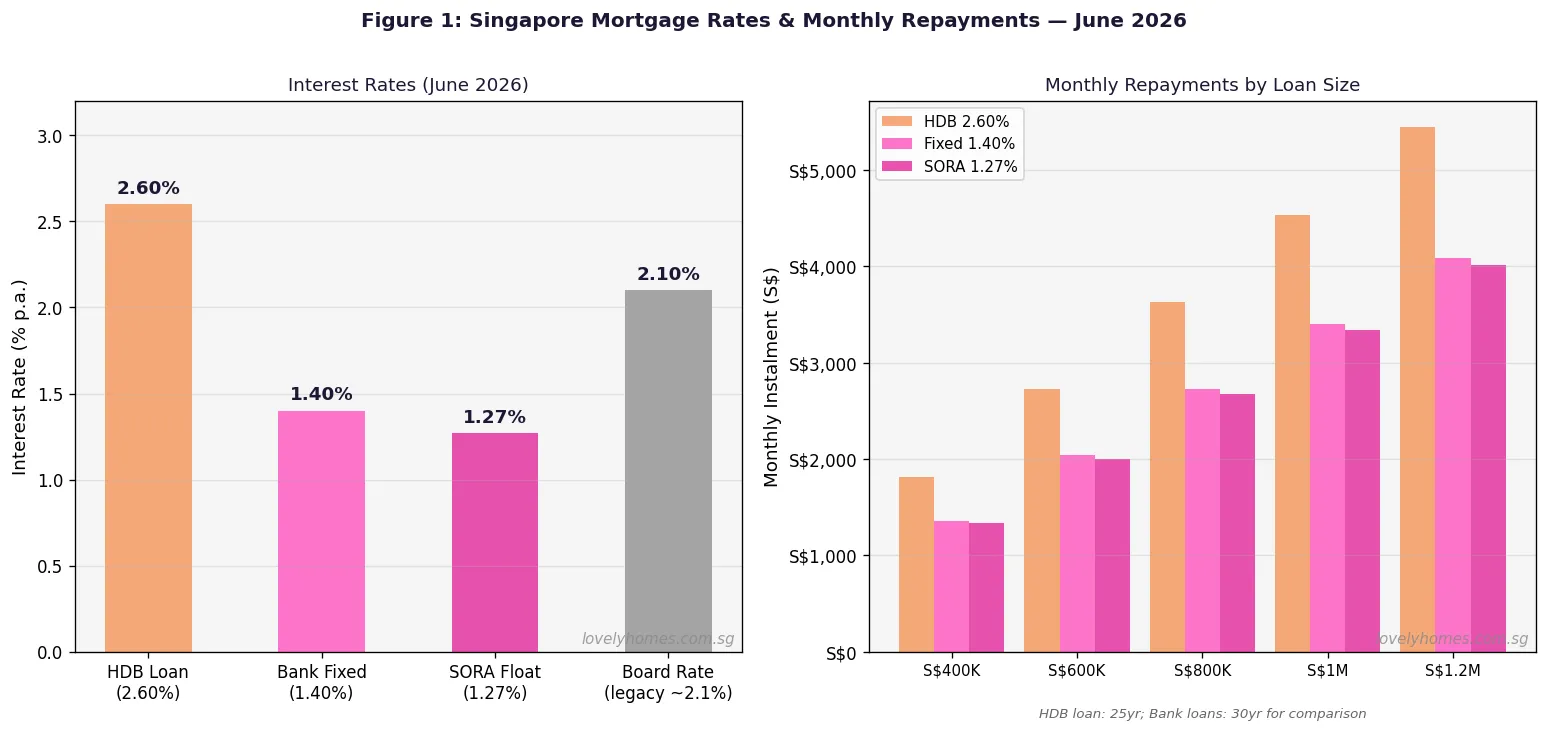

- Best fixed rate as at June 2026: approximately 1.55% p.a. (1-year) and 1.65% p.a. (2-year) for private property bank loans.

- SORA floating rate (3M compounded): ~1.07%, meaning all-in floating packages run at approximately 1.47–1.67% p.a. with typical spreads.

- Trigger rule of thumb: refinance if the rate differential exceeds 0.5 percentage points and savings over the lock-in period outweigh legal and valuation costs.

- Break-even formula: total refinancing cost ÷ monthly savings = months to break even. At S$800,000 outstanding loan, savings of ~S$800/mth and costs of ~S$3,000 breaks even in under 4 months.

- Lock-in trap: early redemption penalty is typically 1.5% of the outstanding loan; on S$800,000, that is S$12,000 — which often wipes out several years of savings.

- HDB homeowners: you may only switch from an HDB concessionary loan to a bank loan once — there is no return. Check MAS TDSR 55% and MSR 30% compliance before switching.

Repricing vs Refinancing: What Is the Difference?

These two terms are frequently confused, but they describe very different transactions with materially different cost profiles.

Repricing occurs within your existing bank. You notify your loan officer that you wish to move to a new rate package — say, from an expiring 2-year fixed package to a new 2-year fixed at the current prevailing rate. The bank assesses the request, may charge a small administration fee (typically S$0–S$500), and adjusts your loan terms. No lawyers are involved, no valuation is required, and the process is completed in 1–3 weeks. The limitation: you are confined to the rates that particular bank is willing to offer you.

Refinancing involves discharging your existing mortgage and registering a new mortgage with a different bank. This requires a conveyancing lawyer to handle the discharge and registration, a fresh valuation of the property, and completion of the new bank’s credit underwriting process. The reward: you have access to every bank’s current promotional rates, which often undercut what your existing bank is willing to reprice you to, and new banks routinely offer legal subsidies and cashback to attract refinancing clients.

When Does Refinancing Make Financial Sense?

Four conditions typically align to make refinancing worthwhile:

1. Your lock-in period has expired. Most Singapore bank loans carry a lock-in period of 2–3 years, during which early redemption attracts a penalty of around 1.5% of the outstanding loan amount. On an S$800,000 loan, this is S$12,000 — enough to negate several years of rate savings. Never refinance during the lock-in period unless the rate differential is extraordinary and you have run the full maths.

2. There is a rate differential of at least 0.5% p.a. Below 0.3%, the cost and administrative effort of refinancing rarely justify the switch. Between 0.3% and 0.5%, repricing within the same bank may deliver better net value. Above 0.5%, refinancing to a new bank is typically the superior option, especially if the new bank offers legal subsidies.

3. You have at least 3–5 years remaining on the loan. Refinancing costs are a one-time outlay recouped over the remaining loan term. If you plan to sell the property within 18–24 months, the break-even analysis may not support a refinancing.

4. The property valuation supports the Loan-to-Value ratio. Refinancing requires a fresh valuation. If property values have declined since purchase — or if you have an older property with a shorter remaining lease — the new bank may impose a lower LTV, requiring you to top up cash to reduce the loan quantum before the new mortgage can be registered.

Current Rates and Potential Savings (June 2026)

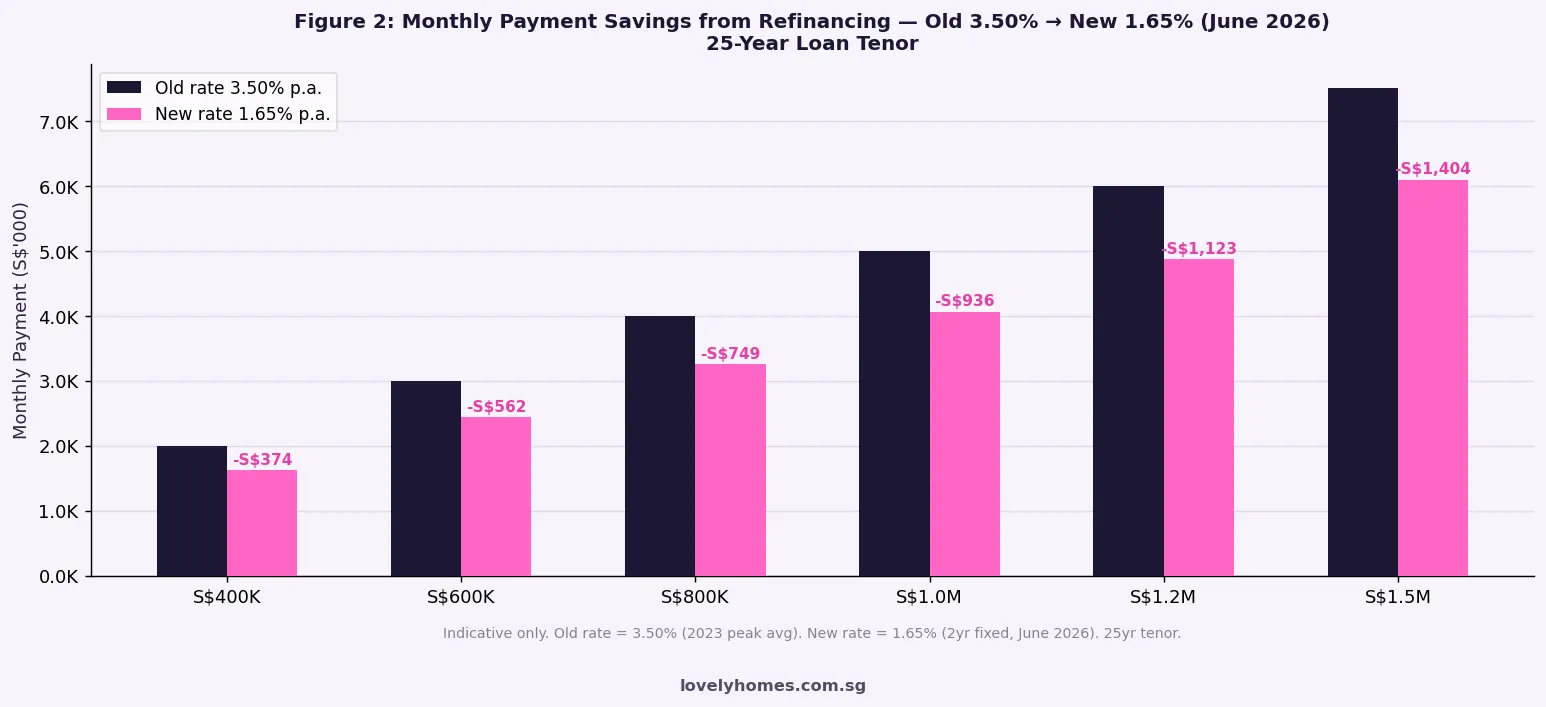

As at June 2026, the Monetary Authority of Singapore (MAS) publishes the 3-month compounded SORA at approximately 1.07%. Bank spreads on floating packages typically run at 0.40–0.60 percentage points above SORA, placing all-in floating rates at approximately 1.47–1.67% p.a. Fixed-rate packages for 1-year and 2-year lock-ins are offered at approximately 1.55% and 1.65% respectively by major Singapore lenders.

For homeowners who took 2-year or 3-year fixed packages in 2022–2023 at rates of 3.0–3.75% p.a. (many of which have now expired or will expire within the next 12 months), the savings opportunity is substantial. A borrower refinancing S$800,000 from 3.50% to 1.65% on a 25-year loan would reduce monthly repayments from approximately S$4,006 to S$3,212 — a saving of S$794 per month, or S$9,528 per year. Over a 2-year fixed period, that is S$19,056 in gross savings against legal and valuation costs of approximately S$3,000–S$4,000.

Step-by-Step: How to Refinance Your Singapore Home Loan

Step 1 — Check your lock-in expiry date. Review your existing loan letter or call your bank. Note the lock-in end date and the penalty rate (usually 1.5%) that applies if you redeem early.

Step 2 — Get competing quotes. Contact at least 3–4 banks or use a licensed mortgage broker to compare packages. Look at the all-in rate (not just the headline), the lock-in period, any clawback conditions on legal subsidies, and the cashback quantum.

Step 3 — Apply to the preferred bank. Submit your income documents (CPF contribution statements, last 3 months’ payslips or Notice of Assessment, existing loan statements). The new bank will run a fresh credit assessment and order a valuation of your property.

Step 4 — Instruct a conveyancing lawyer. The new bank will recommend panel solicitors. If the bank offers legal subsidy, this typically covers S$2,000–S$3,500 of the legal cost. You bear any shortfall.

Step 5 — Sign and complete. The lawyers handle the discharge of the existing mortgage and registration of the new mortgage with the Singapore Land Authority (SLA). Timeline: 4–8 weeks from application. Your first new payment is typically due the following month.

Break-even calculation: Divide total out-of-pocket cost (legal shortfall + valuation + any admin fees) by monthly savings. If break-even is under 12 months, refinancing is strongly justified on pure financial grounds.

HDB vs Private Property: Key Differences When Refinancing

HDB flat owners face an additional, irreversible consideration: the HDB concessionary loan. At 2.60% p.a. (pegged at CPF OA rate + 0.10%), the HDB loan has historically been competitive with bank loans in high-rate environments. In June 2026, however, bank fixed rates at 1.55–1.65% are substantially below the HDB loan rate.

Crucially, the switch from an HDB loan to a bank loan is one-way. Once you refinance out of the HDB concessionary loan, you cannot return to it. You must also have a minimum 5% cash downpayment available when refinancing, since HDB allows 0% cash downpayment but banks require 5% cash (with the balance in cash or CPF). Additionally, the HDB Mortgage Servicing Ratio (MSR) of 30% of gross monthly income continues to apply — the bank will stress-test your repayments at 4% per annum.

Private property homeowners do not face the one-way constraint and have more flexibility in switching between floating and fixed packages. However, they are subject to the Monetary Authority of Singapore’s (MAS) Total Debt Servicing Ratio (TDSR) cap of 55% of gross monthly income. A borrower refinancing must demonstrate that all monthly debt obligations (including the new mortgage) do not exceed 55% of gross income at a stressed rate of 4%.

Summary Table: Refinancing at a Glance

| Parameter | Typical Value / Rule | Source |

|---|---|---|

| Best fixed rate (Jun 2026) — 2yr | ~1.65% p.a. | Bank market, MAS |

| 3M Compounded SORA (Jun 2026) | ~1.07% | MAS |

| Floating all-in rate (SORA + spread) | ~1.47–1.67% p.a. | Bank market |

| Early redemption penalty (lock-in) | 1.5% of outstanding loan | Bank standard |

| Legal fees (refinancing) | S$2,500–S$3,500 (often subsidised) | Conveyancing practice |

| Valuation fee | S$500–S$800 | Panel valuers |

| HDB loan → bank loan | One-way; cannot revert | HDB rules |

| TDSR stress test rate | 4% p.a. | MAS Notice 645 |

| MSR limit (HDB) | 30% of gross monthly income | MAS / HDB |

| Typical break-even period | 3–6 months (post lock-in, large loan) | LovelyHomes calculation |

Worked Example: The Ng Family Refinance Their Queenstown Condo

Scenario: SC couple with an expiring 3-year fixed package

Property: 3BR resale condo in Queenstown (D3), purchased in 2022 at S$1,950,000. Outstanding loan: S$1,200,000 with 22 years remaining.

Current rate: 3.40% p.a. fixed (2022 vintage, lock-in expired June 2026).

Current monthly payment: S$7,188 (estimated for S$1.2M at 3.40%, 22yr).

Refinancing option chosen: 2-year fixed package at 1.65% p.a. with a major Singapore bank. Bank offers full legal subsidy up to S$3,200 and S$1,000 cashback.

New monthly payment: S$6,119 (S$1.2M at 1.65%, 22yr).

Monthly saving: S$1,069.

Out-of-pocket cost: Valuation S$750 + admin S$200 = S$950 (legal fully subsidised). Cashback offsets the residual: net cost S$0, net cashback S$50 surplus.

Annual saving: S$12,828. Over the 2-year fixed period: S$25,656 in gross savings against near-zero cost.

TDSR check: Combined gross income S$18,500/mth. New monthly payment S$6,119. TDSR = 6,119 / 18,500 = 33.1% — well below the 55% MAS cap. PASS.

Conclusion: The Ngs should refinance immediately. At the current rate differential of 1.75 percentage points, every month they delay costs approximately S$1,069 in avoidable interest.

Why Now May Be the Best Window to Refinance

The SORA rate trajectory from 2022 to 2026 describes one of the most compressed monetary tightening-and-easing cycles in Singapore’s modern history. Rates rose from near-zero in Q1 2022 to a peak of 3.52% in Q2 2023, then declined steadily as the US Federal Reserve pivoted and MAS maintained a policy of modest Singapore Dollar appreciation. By Q2 2026, 3M SORA stands at approximately 1.07% — its lowest level since early 2022.

For homeowners whose fixed packages are expiring in H2 2026 or H1 2027, this is the optimal re-locking window. Fixed rates at 1.55–1.65% represent historically low absolute levels for Singapore dollar mortgages, and locking in for 2–3 years insulates borrowers from any future rate volatility while the MAS recalibrates policy stance in response to global conditions.

What Might Come Next for Singapore Mortgage Rates

Forecasting interest rates with precision is notoriously difficult, and homeowners should treat any interest rate outlook as a probabilistic scenario rather than a point prediction. That said, market pricing as at June 2026 suggests that 3M compounded SORA is expected to remain broadly stable in the 0.9–1.2% range through end-2026, with a modest rise toward 1.4–1.6% by end-2027 if global growth recovers and the US Federal Reserve pivots toward a less accommodative stance.

For Singapore homeowners, this implies that the current fixed-rate window at 1.55–1.65% — if locked in for 2 years — provides reasonable downside protection even if SORA nudges higher in 2027. Floating-rate borrowers would face upward rate exposure if that scenario materialises. Whether to fix or float depends on individual risk tolerance, loan quantum, and holding horizon, and the decision should be reviewed with a licensed financial adviser or mortgage broker.

MAS continues to monitor household debt levels through the TDSR framework and has not signalled any near-term changes to the 55% cap or the 4% stress-test assumption. The framework has proven effective in preventing excessive leverage, and its parameters are unlikely to change in a benign rate environment.

FAQ: Singapore Home Loan Refinancing

Can I refinance if I bought my property under the Deferred Payment Scheme (DPS)?

Under the Deferred Payment Scheme for new launches, the full mortgage typically kicks in only at TOP. Before TOP, you may be on a bridging or construction loan. Refinancing in the conventional sense (full mortgage switch) generally becomes available and practical once the property reaches TOP and you draw down the full loan amount. If your DPS loan has a lock-in clause that extends post-TOP, check the penalty terms before refinancing. Most new launch mortgages with post-TOP lock-ins of 2 years will be eligible for refinancing in the 24 months following TOP.

What is a legal subsidy, and is it a clawback if I refinance again within 3 years?

When a bank offers a legal subsidy to attract a refinancing client, it is essentially paying part of your conveyancing costs as an acquisition incentive. Most legal subsidies come with a clawback clause: if you refinance again before a specified period — typically 2–3 years — you are required to repay all or part of the subsidy. This creates a de facto lock-in even when the loan package itself does not have a formal lock-in. Always read the letter of offer and mortgage terms carefully for clawback conditions before accepting a legal subsidy.

Does refinancing affect my credit score or TDSR?

A refinancing application triggers a credit enquiry, which may temporarily affect your credit score under the CBS (Credit Bureau Singapore) system. Multiple applications within a short period can have a compounding effect, so it is advisable to narrow your shortlist before formally applying. TDSR is reassessed at refinancing, which is important for borrowers whose income has changed since the original loan. If your income has fallen — or if you have taken on additional debt obligations — you may find that fewer banks are willing to offer a refinancing, or that the eligible loan quantum has reduced.

Can I use CPF OA savings to pay the outstanding loan before refinancing to reduce the principal?

Yes. If you have CPF OA savings that have not yet been applied to the property (i.e., beyond the Valuation Limit or Basic Retirement Sum considerations), you may use CPF OA to partially redeem the loan principal. However, any CPF OA funds used for the property are subject to the CPF accrued interest rule: when you eventually sell, you must refund the CPF principal plus accrued interest at 2.5% per annum back to your CPF OA. Reducing your loan principal before refinancing may improve your LTV ratio and help you access better rate tiers at the new bank.

Is there any restriction on refinancing if my property has a short remaining lease?

Yes. Banks apply progressively stricter LTV limits as a leasehold property’s remaining lease shortens. Under MAS guidelines, if the remaining lease at the point of loan maturity is less than 20 years, the maximum LTV is significantly reduced. For properties where the remaining lease + loan tenure falls below 35 years, some banks impose additional haircuts or decline refinancing entirely. HDB-loaned homeowners with shorter-lease flats face the same constraints when switching to a bank loan. If your flat has 50 or fewer years of lease remaining, assess the LTV implications carefully before initiating a refinancing application.

What documents do I need to prepare for a refinancing application?

Standard documentation for a Singapore home loan refinancing includes: your NRIC or passport, the existing mortgage loan statement (showing outstanding balance and monthly payment), the last 6 months’ CPF contribution statement, your last 3 months’ payslips (or last 2 years’ NOA if self-employed), the property’s title deed reference (your conveyancing lawyer can retrieve this), and — if the property is rented out — the tenancy agreement and rental income records. Processing time is typically 2–4 weeks for employed applicants with straightforward income profiles.

Click anywhere outside to close