Singapore First-Timer Home Buyer Complete Guide 2026: Grants, BTO vs Resale, HFE and Everything You Need

Buying your first home in Singapore is one of the biggest financial decisions you will ever make — and the government has designed a system that genuinely rewards first-timers. From priority balloting in the Build-To-Order (BTO) exercise to grants worth up to S$230,000 for resale flat buyers, first-timer status unlocks advantages that second-timers and investors cannot access. This guide covers everything from how HDB defines a first-timer to the full buying timeline, so you can make the right choice with confidence.

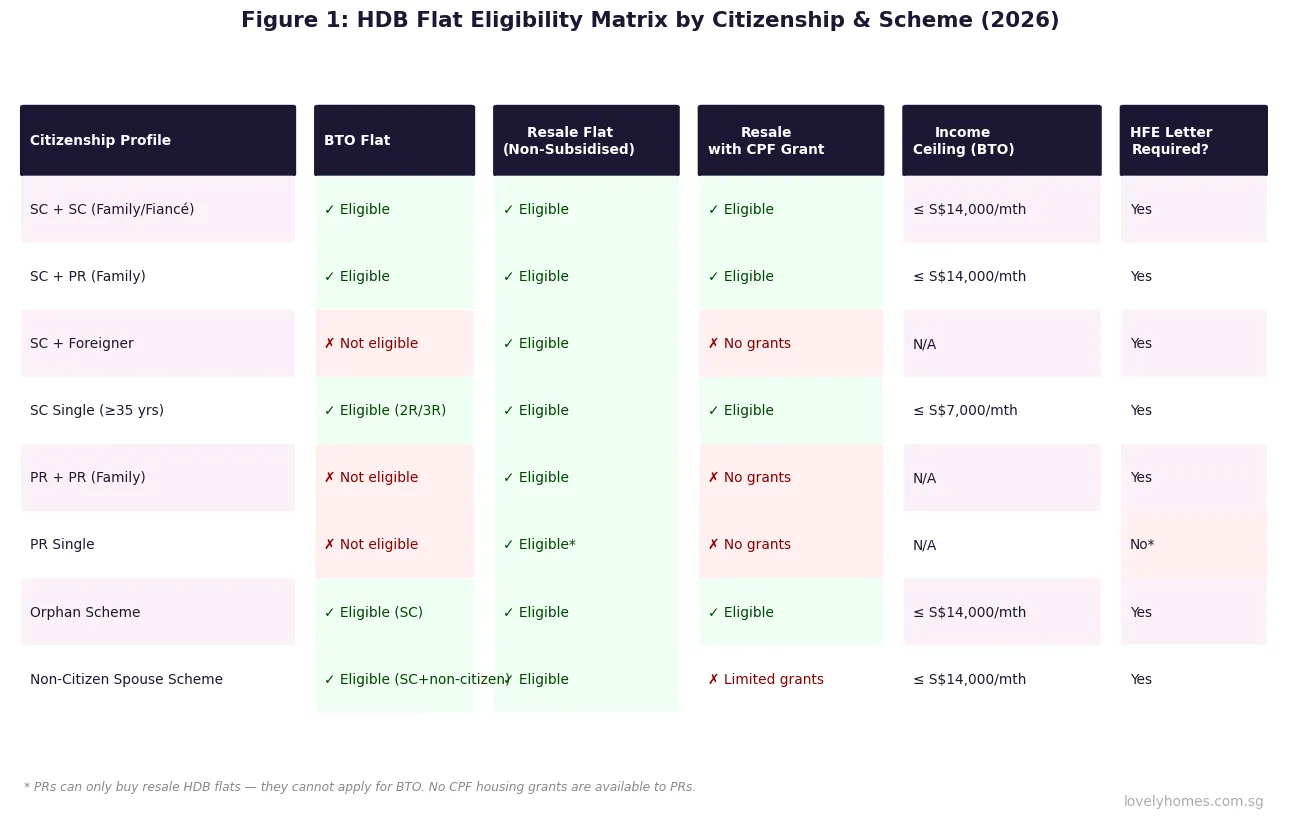

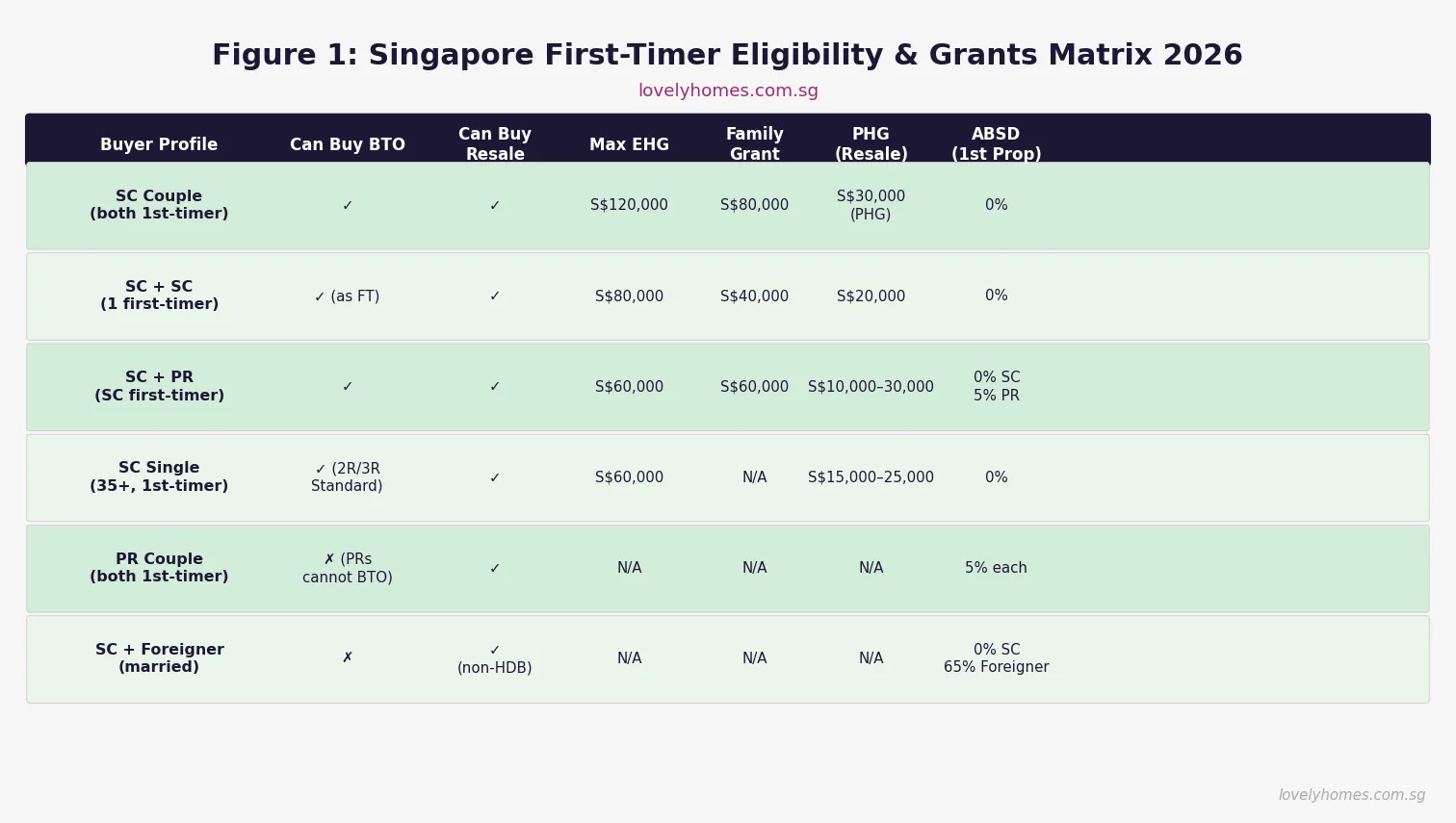

- First-timer status applies to Singapore Citizens (SC) and Permanent Residents (PR) who have never owned a subsidised HDB flat or private residential property in Singapore.

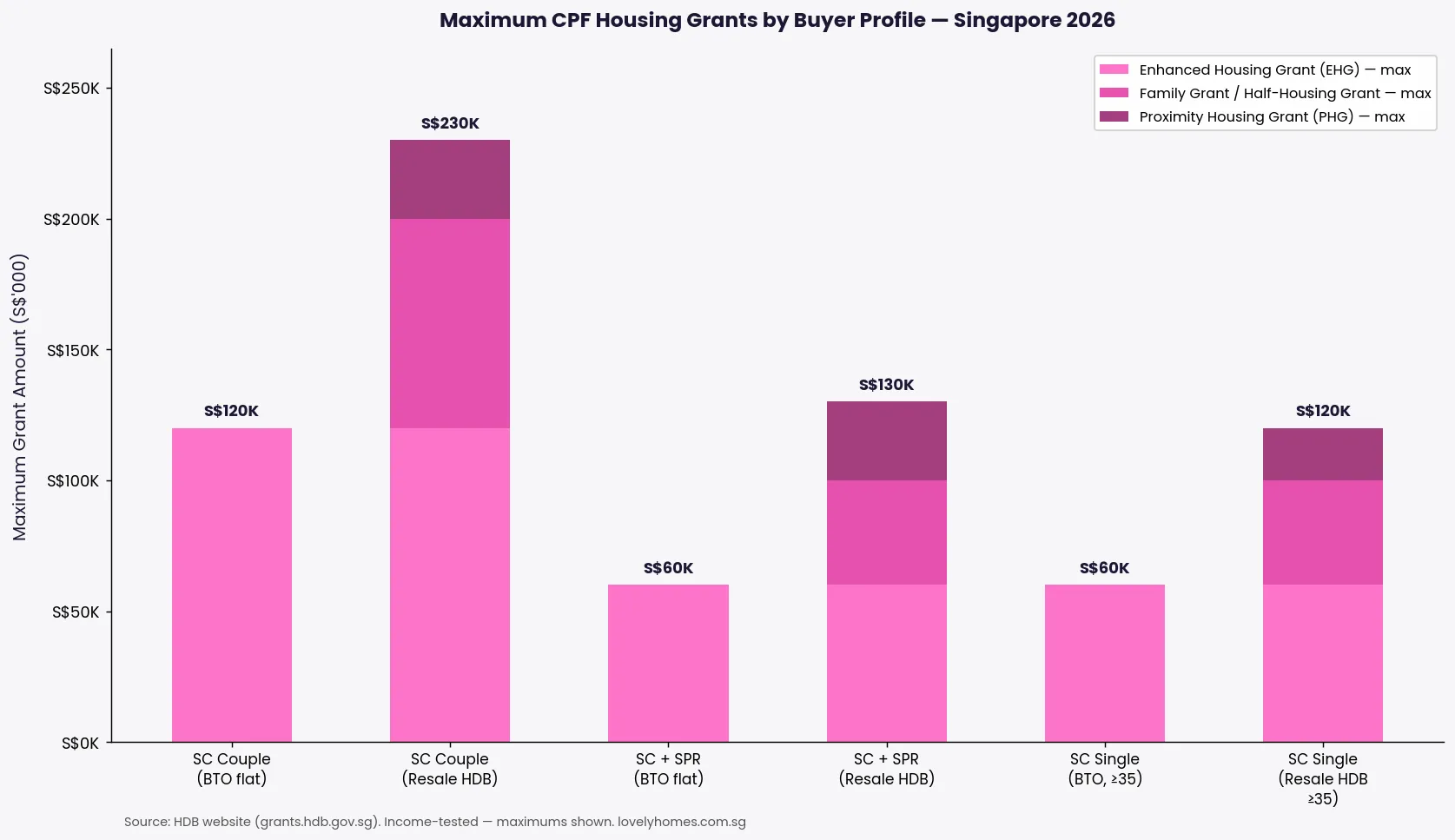

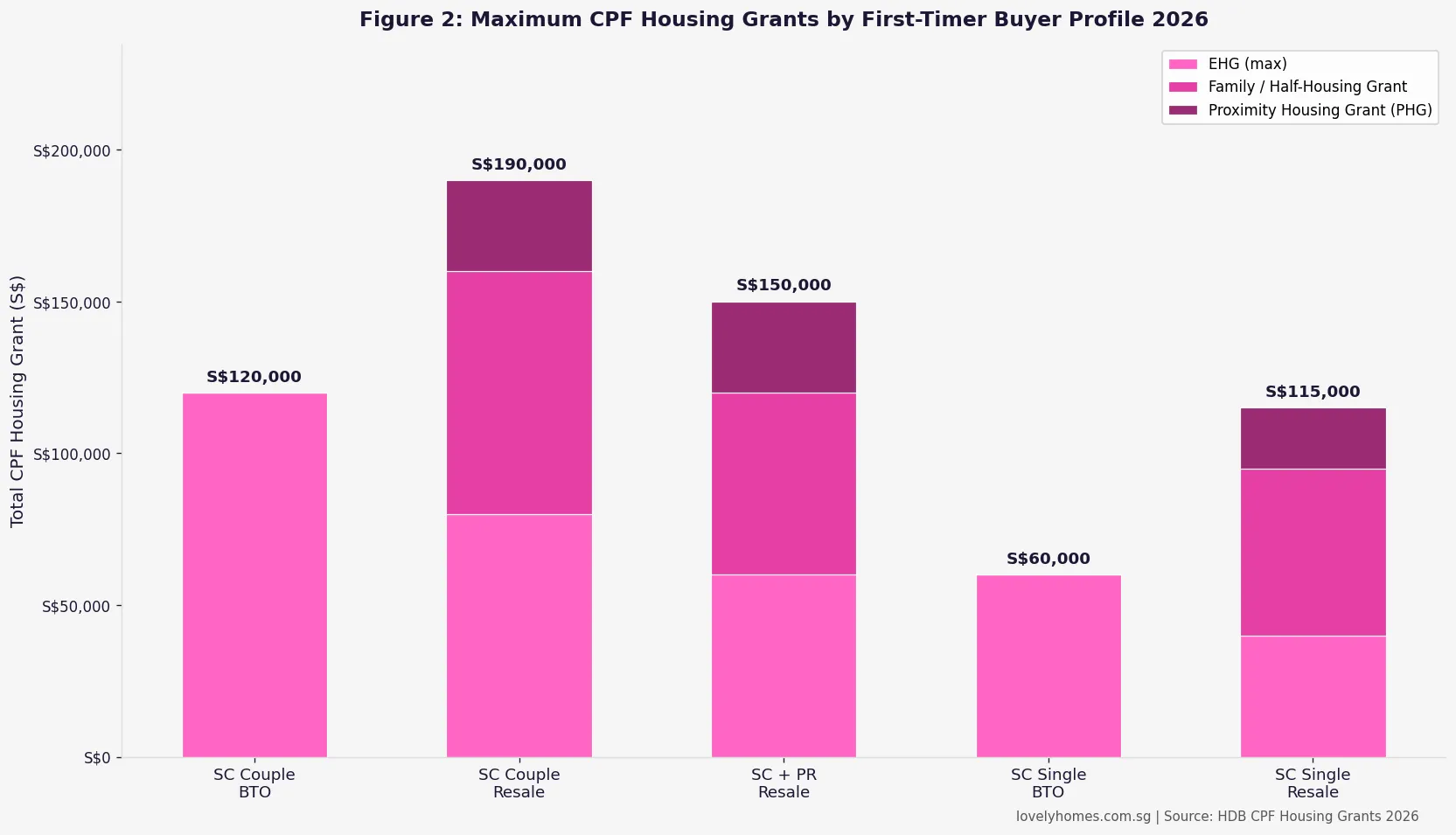

- CPF housing grants can total up to S$230,000 for SC couple buying an HDB resale flat (EHG + Family Grant + PHG combined).

- BTO priority balloting: first-timers get two ballot chances for every one chance given to second-timers.

- HDB Flat Eligibility (HFE) letter is mandatory before you can apply for any BTO or resale HDB flat — validity is 9 months.

- ABSD: SC buying first property pays 0% ABSD; PR pays 5%; foreigners pay 65%.

- MSR cap: monthly HDB/EC mortgage must not exceed 30% of gross monthly income.

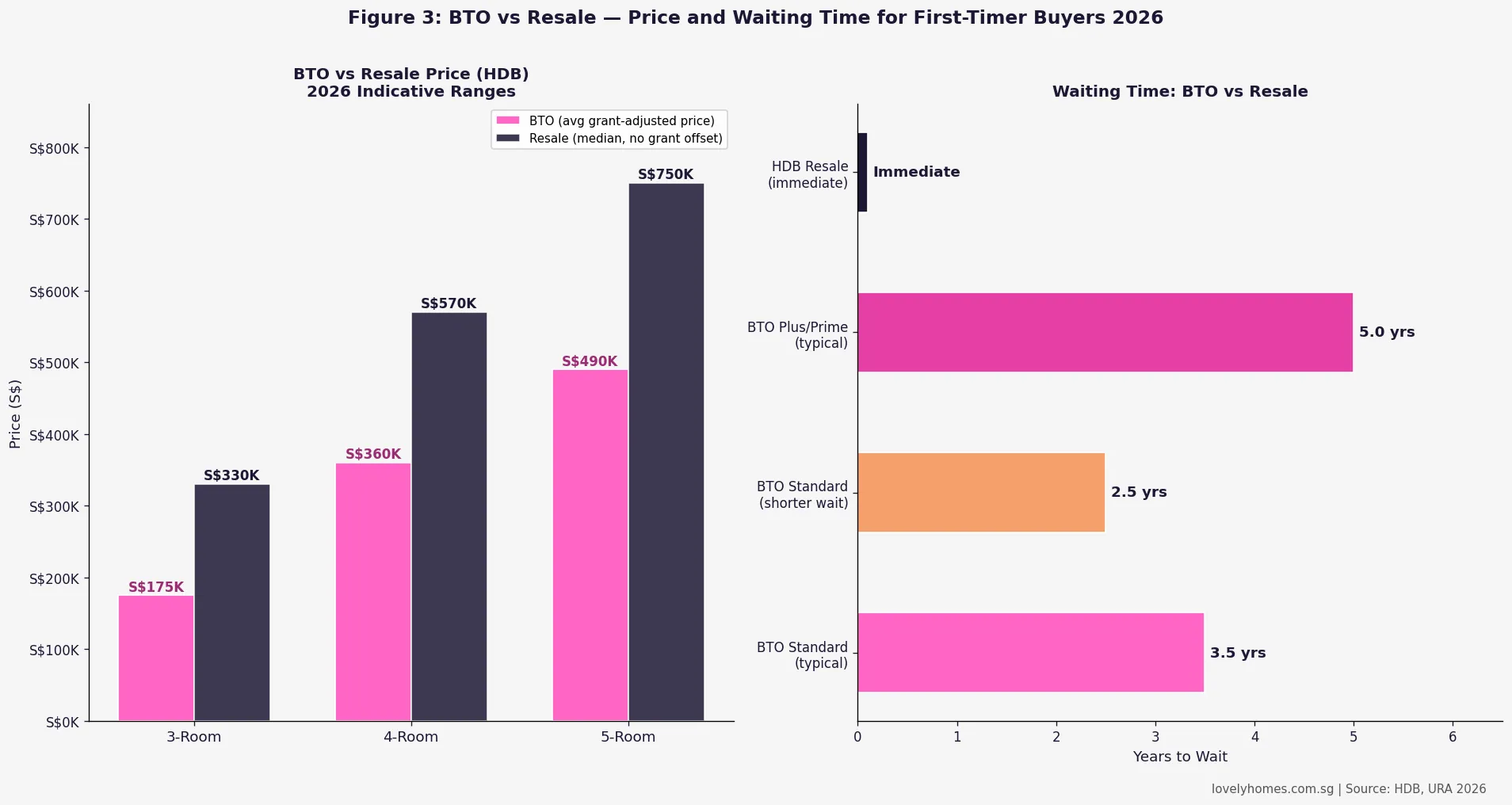

- BTO waiting time: 2.5–5 years for standard flats; resale is immediate.

- New classification (2024 onwards): BTO flats are now categorised Standard, Plus, or Prime — each with different resale restrictions and grant levels.

- MOP: standard flats require 5-year Minimum Occupation Period; Plus/Prime BTO and new ECs (from May 2026) require 10 years.

- BSD is payable by all buyers regardless of first-timer status — progressive from 1% to 6% on purchase price.

What Makes You a First-Timer in Singapore’s Property System?

HDB defines a first-timer applicant as someone who has not previously received a housing subsidy from HDB. Practically, you are a first-timer if all the following are true: you have never owned an HDB flat (purchased directly from HDB), you have not previously received an HDB grant, and you have not owned a private residential property in Singapore in the 30 months before your flat application (this 30-month rule applies to resale applications). If you co-own a private property overseas, it does not automatically disqualify you for HDB purposes, but you must divest any Singapore private property.

The key distinction is subsidised housing: inheriting an HDB flat from a deceased parent does not strip your first-timer status, provided you sell it within the required period. Similarly, owning a commercial property or industrial unit does not affect your HDB eligibility. HDB reassesses your status at the point of application, so the 30-month rule runs backwards from the date you submit your HFE application.

CPF Housing Grants: What First-Timers Can Claim

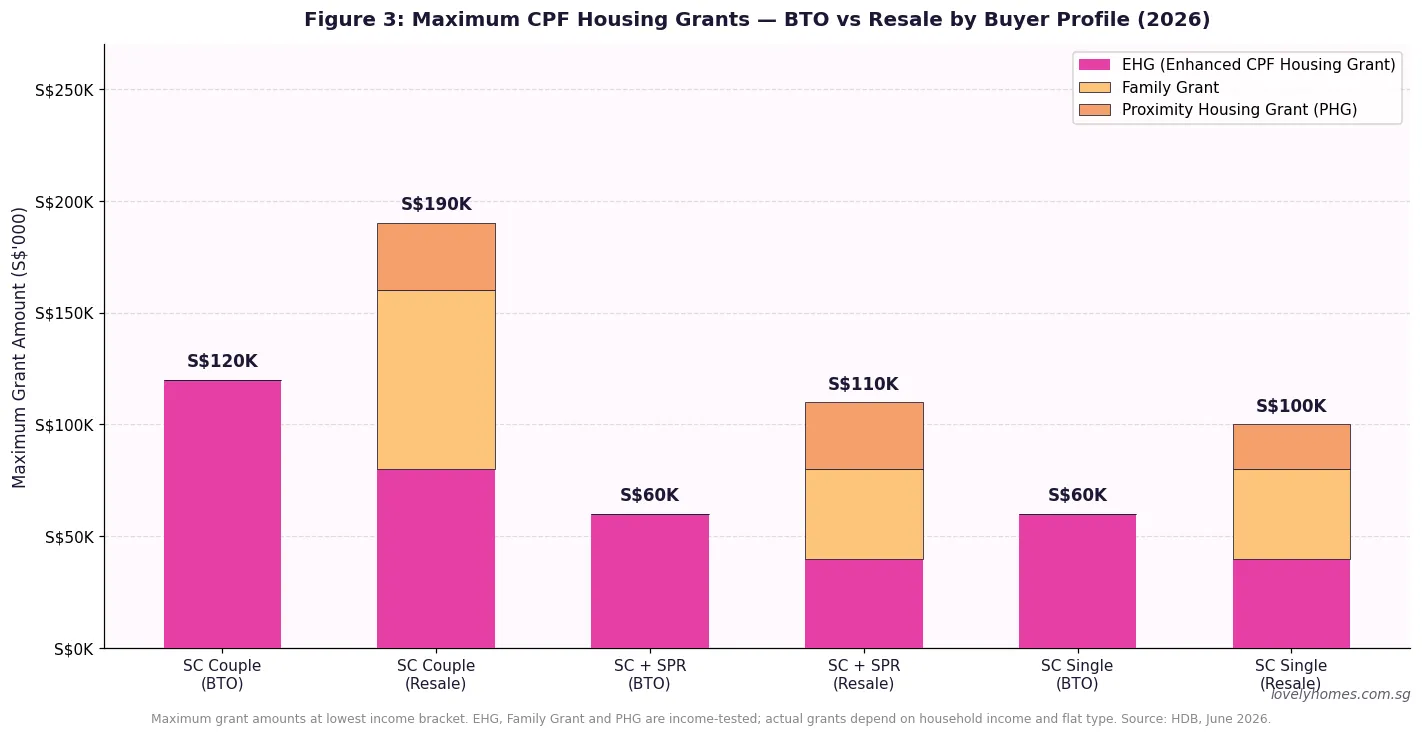

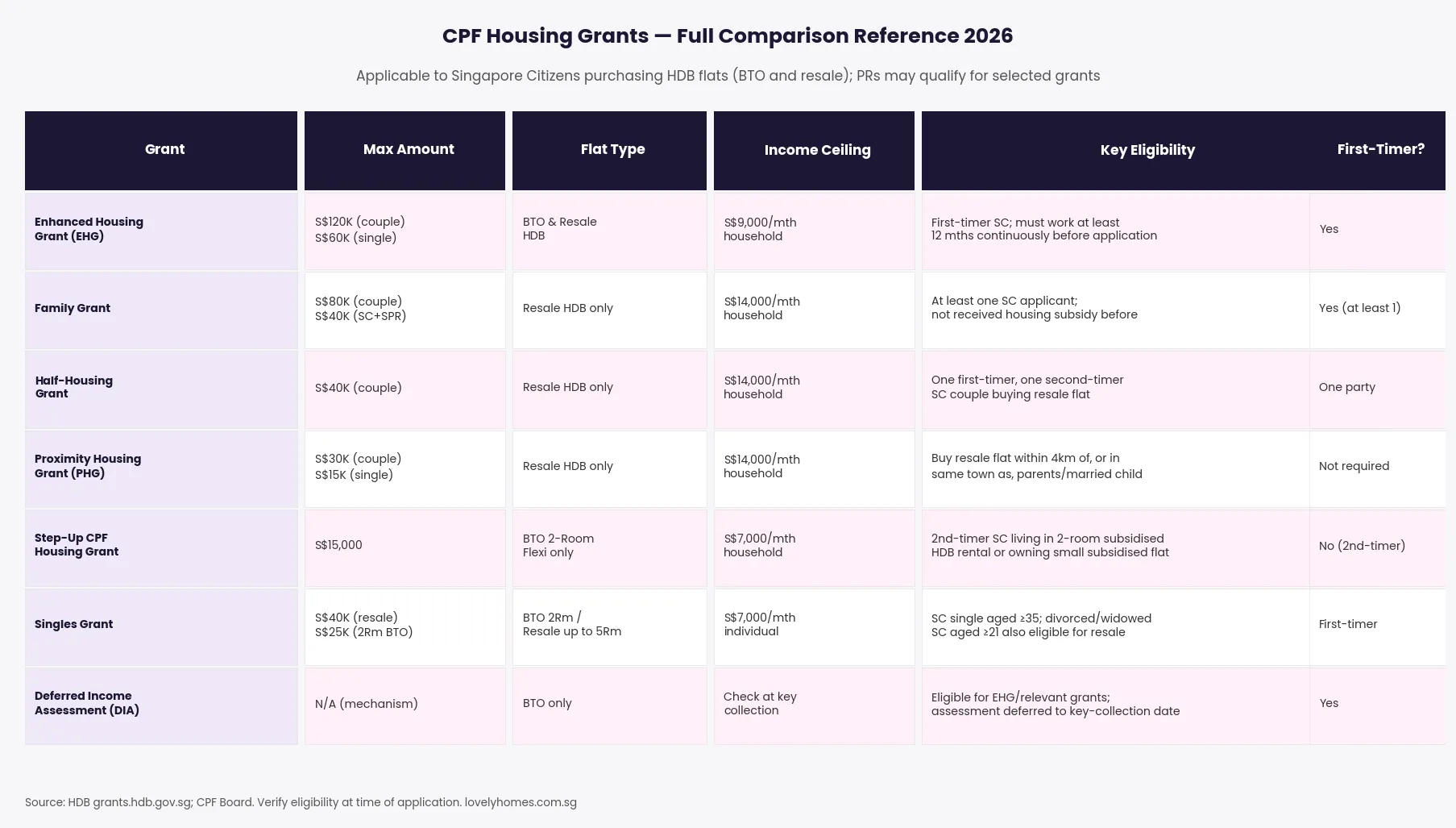

The CPF housing grant system is tiered and means-tested. Higher grants are available to buyers with lower household incomes, with most grants phasing out at S$9,000 per month for couples. All grants are disbursed as CPF Ordinary Account (OA) credits — they reduce the cash you need for the purchase, but they accumulate accrued interest at 2.5% per annum that must be refunded to CPF when you sell.

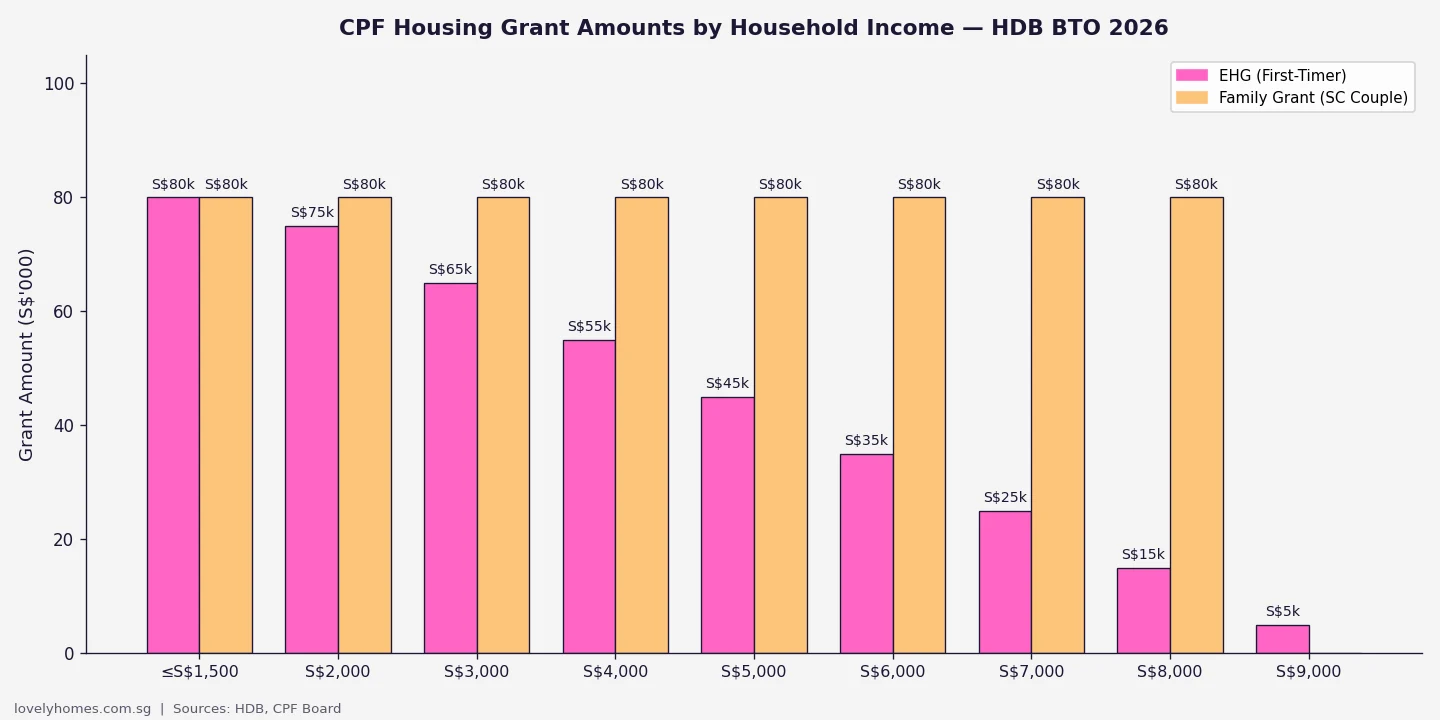

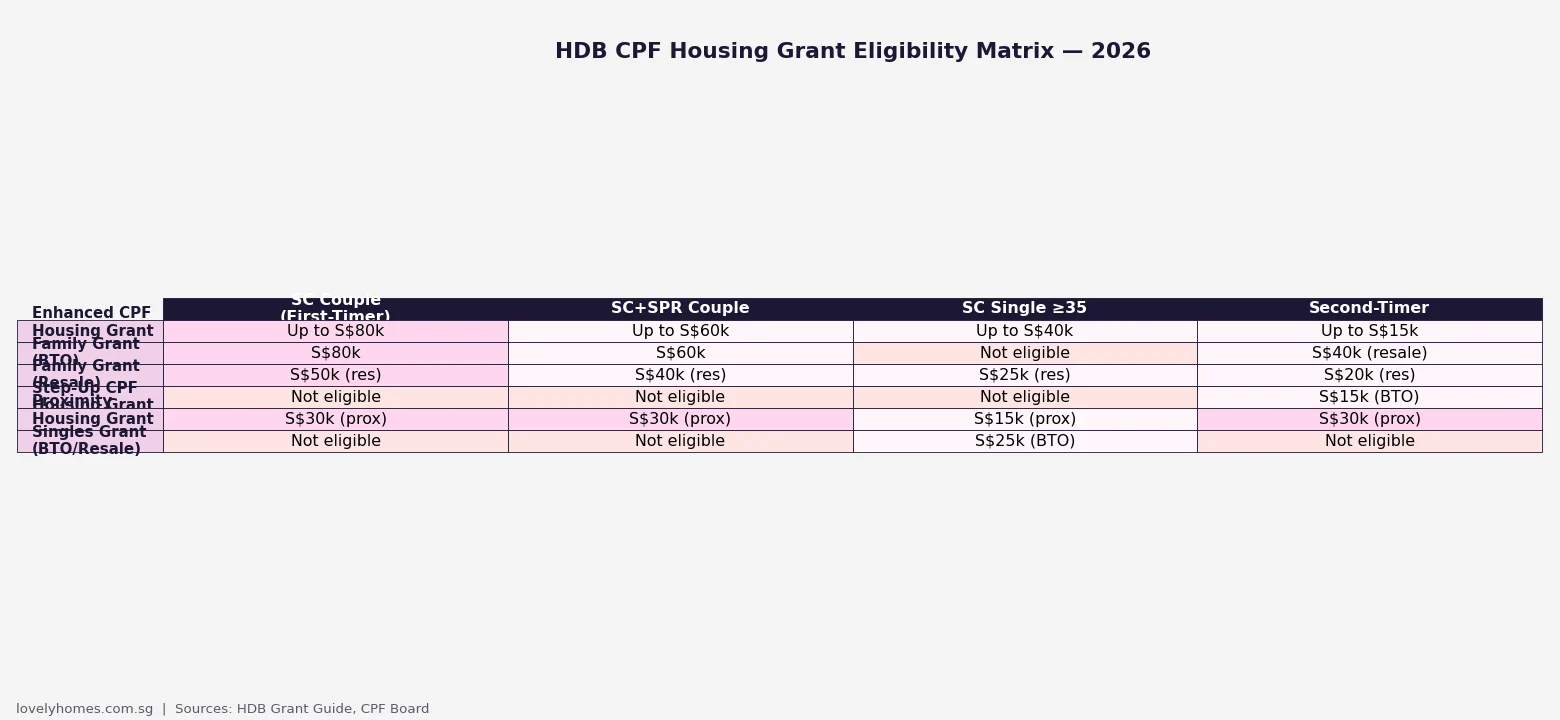

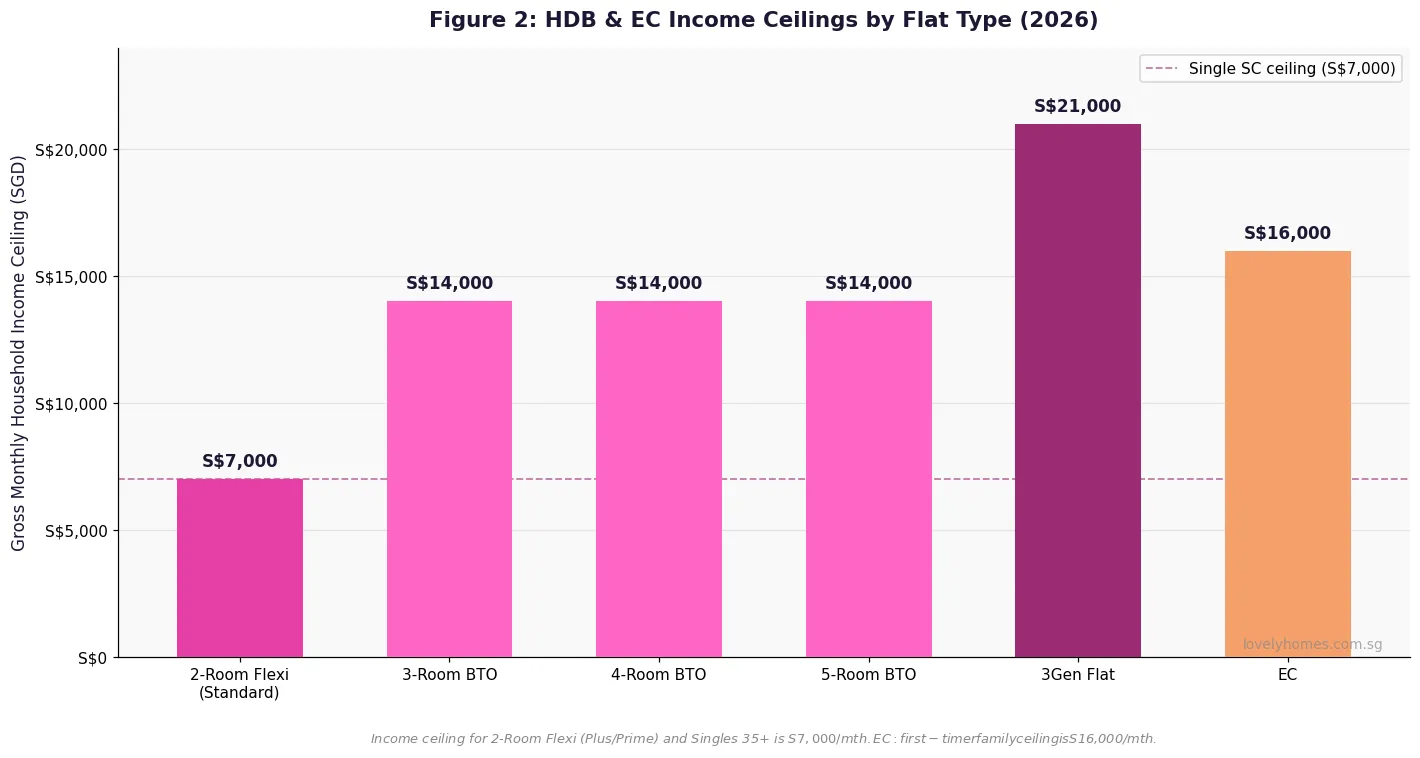

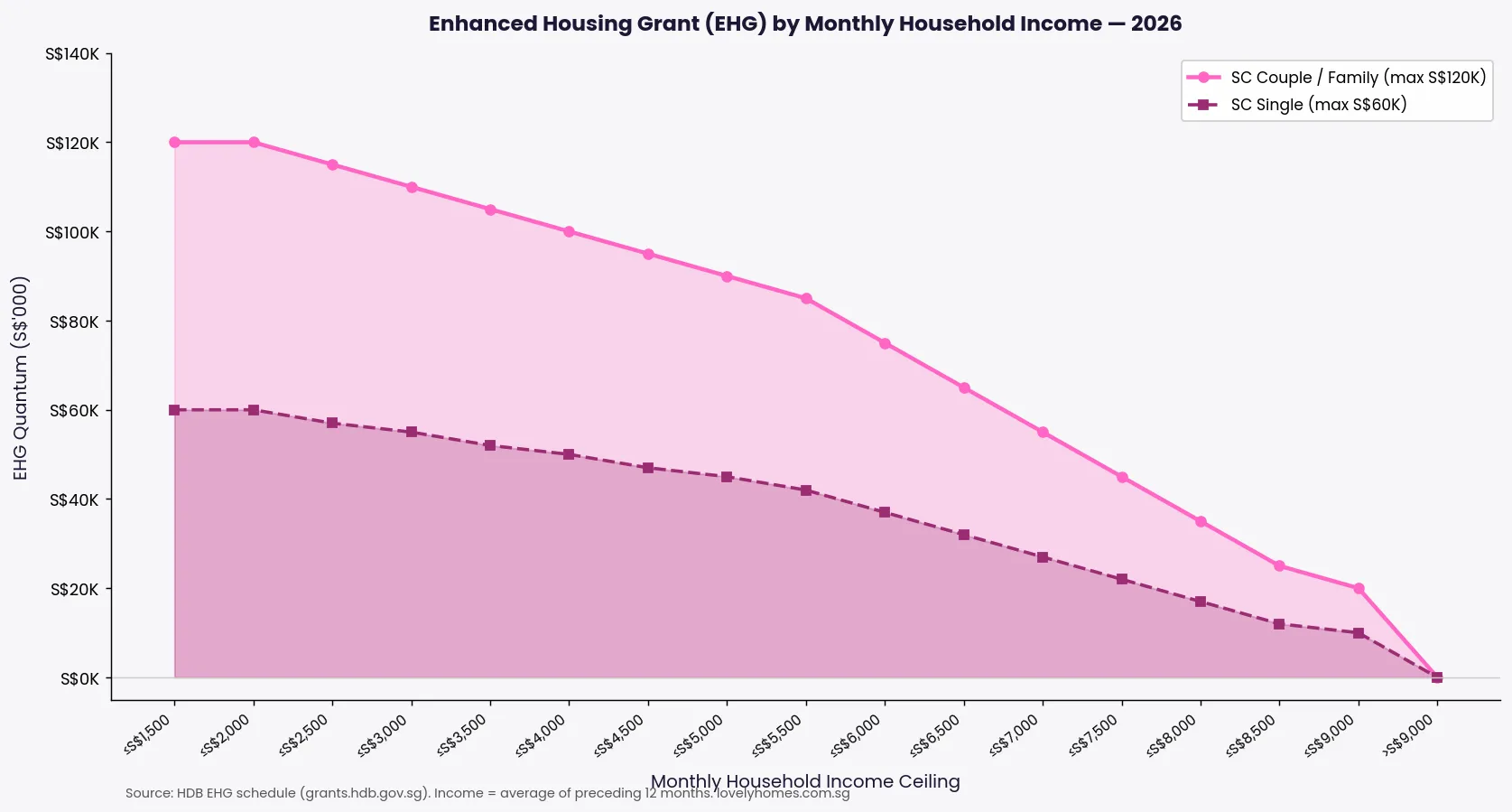

Enhanced CPF Housing Grant (EHG) is the most generous and the most means-tested. For SC couples buying a BTO, EHG ranges from S$5,000 (income S$8,501–S$9,000) up to S$120,000 (income ≤S$1,500). For SC couples buying resale, the EHG is capped at S$80,000 (income ≤S$1,500). Singles aged 35 and above can claim up to S$60,000 for BTO and S$40,000 for resale. The EHG requires that at least one buyer is buying a flat with a remaining lease that can cover the youngest buyer until age 95.

Family Grant applies to resale flats only and is a flat amount: S$80,000 for SC couples, S$60,000 for SC + SPR couples. There is no income ceiling for the Family Grant itself, but the EHG already tapers to zero above S$9,000 household income, so high-income buyers effectively claim only the Family Grant.

Proximity Housing Grant (PHG) rewards buyers who choose a resale flat within 4 km of their parents or children, or who buy in the same town. Amounts range from S$10,000 (living within 4 km of parents) to S$30,000 (living with parents in the same flat). PHG is available to SC buyers only.

Half-Housing Grant: where one buyer is a first-timer and the other is a second-timer, the first-timer can still claim half the Family Grant — S$40,000 for SC + SC, S$30,000 for SC + SPR — on a resale flat purchase.

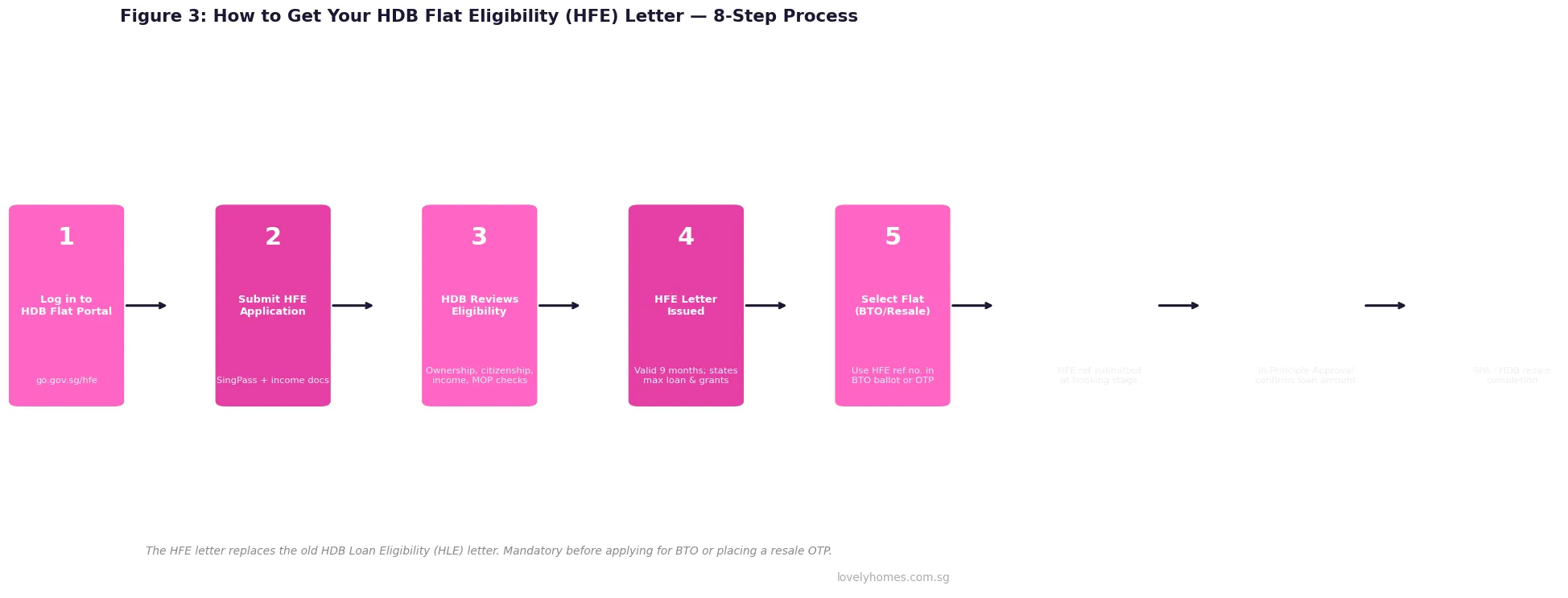

The HDB Flat Eligibility (HFE) Letter: Your First Step

Before you can ballot for a BTO or make an offer on an HDB resale flat, you must obtain an HFE letter from HDB. The HFE replaced the earlier Eligibility Letter (EL) in 2023 and now serves a dual purpose: it confirms your eligibility to purchase, and it indicates the CPF grants and HDB housing loan you may be entitled to. The HFE letter is valid for 9 months from its date of issue.

Applying for an HFE takes roughly 2–3 weeks. You submit an application through the HDB Flat Portal (homes.hdb.gov.sg), providing details of your household members, income documents, and ownership declaration. HDB pulls information from government databases — IRAS for income, SLA for property records — so you do not need to submit separate ownership declarations for most scenarios. If you plan to use an HDB loan, you receive a Loan Eligibility assessment alongside the HFE. If you prefer a bank loan, you should obtain an In-Principle Approval (IPA) from your chosen bank separately.

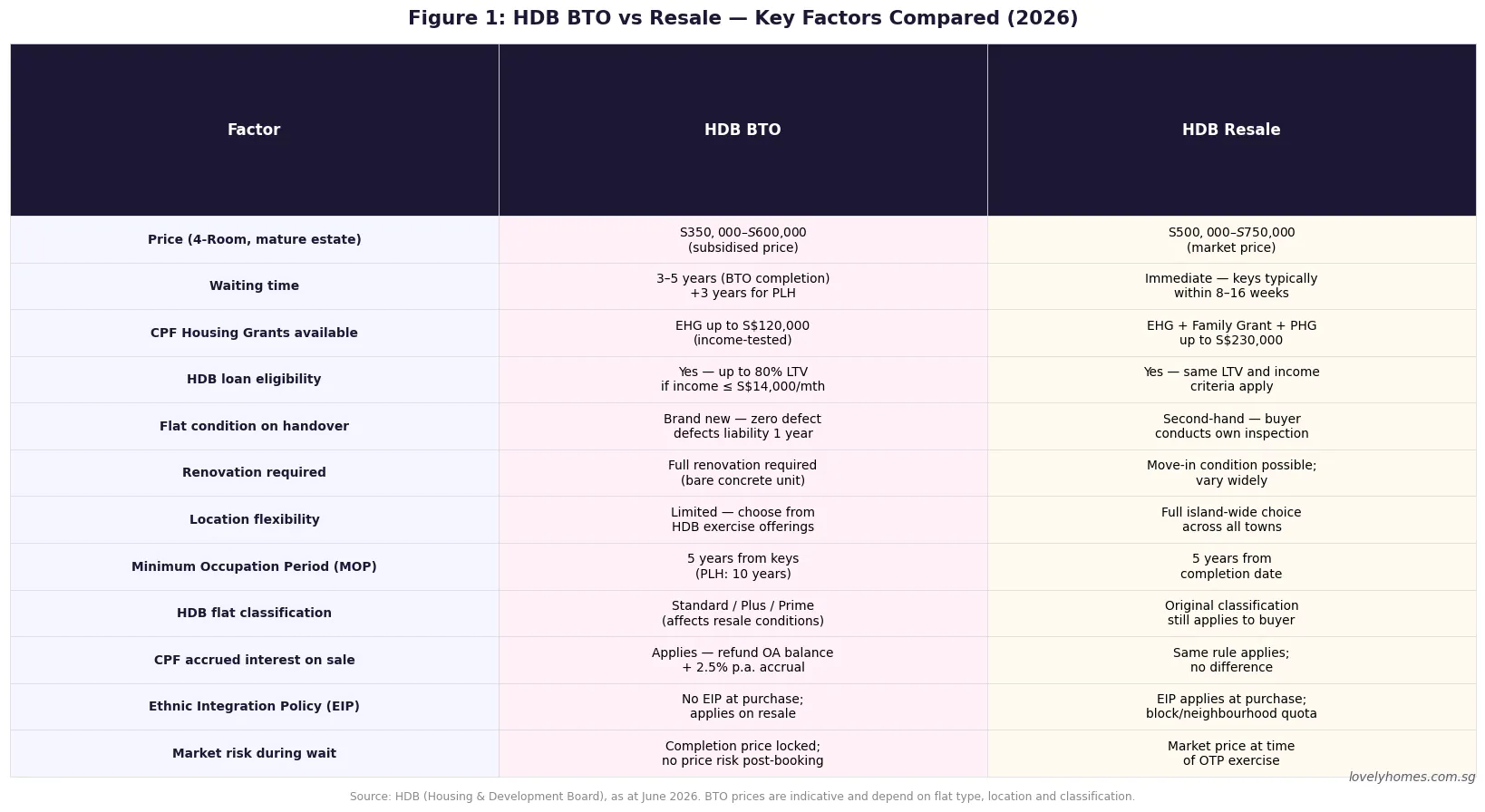

BTO vs Resale: The Core Decision for Every First-Timer

The most consequential decision for any first-timer is whether to buy a BTO flat or an HDB resale flat. This is not purely a financial decision — it involves trade-offs between price, location, waiting time, grant entitlements, and lifestyle.

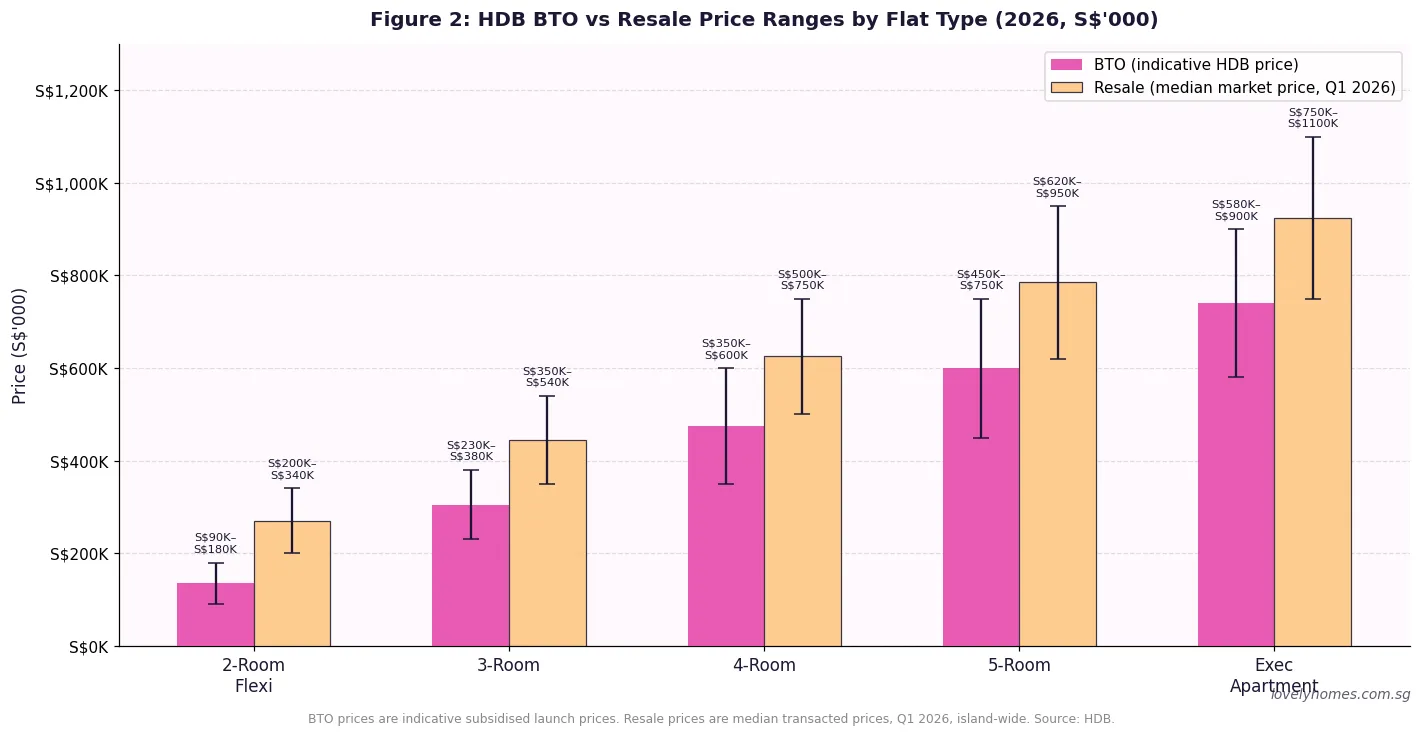

BTO flats are sold by HDB directly at subsidised prices — typically 20–40% below the equivalent resale transaction in the same estate. The trade-off is time: you ballot for a flat first, and you wait for it to be built, which takes 2.5–5 years from booking to key collection. In the meantime, you and your partner typically have to continue renting or living with family. BTO flats in Plus and Prime zones (central estates and highly sought-after areas) carry additional resale restrictions under the 2024 classification framework, including a 10-year MOP and a clawback of HDB subsidy on resale.

Resale flats are immediately available and offer greater locational flexibility — you can buy in virtually any HDB estate, at any floor level, and move in within 8–12 weeks of completing the transaction. They are more expensive than BTOs on a per-unit basis, but first-timers can use the full resale grant stack (EHG + Family Grant + PHG), which partially offsets the premium. Resale flats also come with a shorter remaining lease, which affects CPF withdrawal limits and future resale value — so buyers should check that the remaining lease covers the youngest buyer to age 95.

Financing Your First Home: LTV, MSR, TDSR and Choosing Your Loan

First-timer buyers have two loan options: an HDB Concessionary Loan or a bank loan. Understanding the constraints and advantages of each is critical, because the choice is largely irreversible — once you switch from an HDB loan to a bank loan, you cannot switch back.

HDB Concessionary Loan: available to SC buyers only (not PR-only households), with a combined household income cap of S$14,000 per month. The interest rate is pegged to the prevailing CPF OA rate plus 0.1%, currently 2.6% per annum. LTV ratio is 80%, and there is no cash down payment requirement beyond the minimum 20% top-up (which can be entirely from CPF). The monthly repayment must not exceed 30% of gross income (MSR rule).

Bank loans: available to all buyers. LTV is 75% for the first property, meaning a minimum 25% down payment (with at least 5% in cash and the remaining 20% from cash or CPF). Bank loan interest rates are tied to the Singapore Overnight Rate Average (SORA) — as of June 2026, the 3-month compounded SORA is approximately 1.07%, with typical bank packages for new HDB purchases ranging from 1.5% to 2.2% on floating-rate terms and 2.4%–2.7% on fixed-rate terms. Bank loans are subject to both MSR (30%) and TDSR (55%).

Stamp Duty for First-Timers

Buyer’s Stamp Duty (BSD) is payable on all property purchases in Singapore, without exception. It is calculated on the higher of the purchase price or the market value at a progressive rate: 1% on the first S$180,000, 2% on the next S$180,000, 3% on the next S$640,000, 4% on the next S$500,000, and 5%–6% on amounts above that. For a S$500,000 HDB resale flat, BSD is approximately S$9,600. For a S$650,000 flat, BSD is approximately S$14,400. BSD is payable within 14 days of signing the Option to Purchase and can be paid from your CPF OA.

Additional Buyer’s Stamp Duty (ABSD) for SC buyers purchasing their first property is 0% — no ABSD applies. PR buyers purchasing their first property pay 5% ABSD, and foreigners pay 65% on any residential property. The ABSD rates announced in the April 2023 cooling measures remain in effect as of June 2026.

Summary Table: First-Timer Home Buying at a Glance

| Topic | HDB BTO (First-Timer SC Couple) | HDB Resale (First-Timer SC Couple) |

|---|---|---|

| Max CPF Grants | Up to S$120,000 (EHG only) | Up to S$230,000 (EHG+FG+PHG) |

| Income Ceiling (loans/grants) | S$14,000/mth (HDB loan); S$9,000/mth for max EHG | Same; Family Grant has no separate income ceiling |

| Waiting Time | 2.5–5 years from ballot to keys | 8–12 weeks from OTP to keys |

| Loan Options | HDB (2.6%) or bank loan (SORA-based) | Same |

| Min Down Payment | 20% (all CPF; 5% cash if bank loan) | Same |

| BSD | Payable (from CPF OA) | Payable (from CPF OA) |

| ABSD (SC 1st property) | 0% | 0% |

| MOP (Standard) | 5 years from key collection | 5 years from key collection |

| MOP (Plus/Prime) | 10 years; subsidy clawback on resale | N/A (Plus/Prime applies to BTO only) |

| Ballot Priority | 2× chances vs second-timer | N/A (open market) |

Worked Example: First-Timer Couple Buying Their First HDB Flat

Mr and Mrs Ng are a Singapore Citizen couple. Both are first-timers aged 29. Their combined gross monthly income is S$7,800. They are considering two options: a 4-room BTO flat at a non-mature estate, or a 4-room resale flat in Tampines.

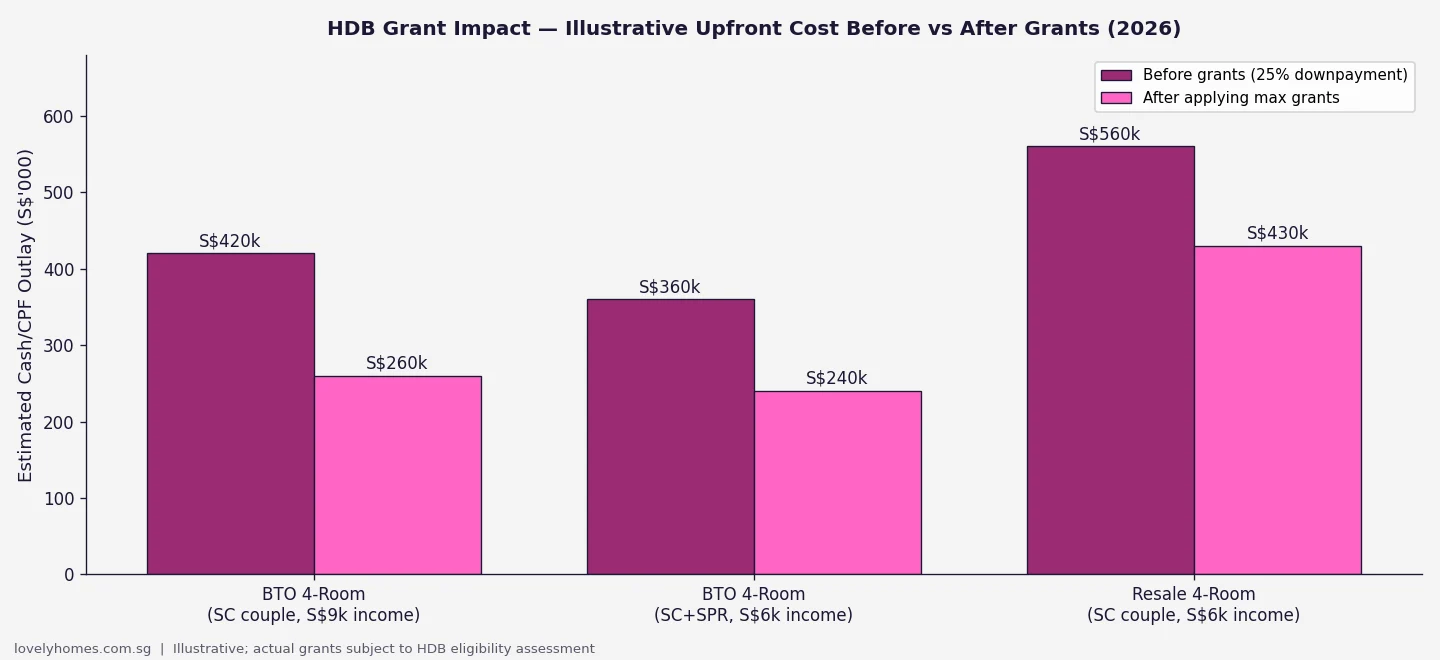

Option A — BTO (non-mature estate, 4-room): Indicative price S$380,000. EHG entitlement at S$7,800/mth income: approximately S$45,000 (income bracket S$7,501–S$8,000, couple BTO). Effective price after EHG: S$335,000. HDB loan at 80% LTV: S$268,000. Monthly repayment at 2.6% over 25 years: S$1,218/mth — MSR = 15.6%, well within the 30% cap. BSD on S$380,000: S$7,100 (payable from CPF). Cash required: essentially S$0 if CPF OA balance is sufficient (S$67,000 down payment + BSD from CPF). Waiting time: approximately 3.5 years.

Option B — Resale (Tampines, 4-room, ~25 years remaining lease): Price S$620,000. Grant entitlement: EHG S$45,000 + Family Grant S$80,000 + PHG S$10,000 (living within 4 km of parents) = S$135,000 total grants. Effective cost after grants: S$485,000 cash/CPF. HDB loan at 80% LTV: S$496,000 (on purchase price; capped to MSR: at S$7,800/mth income, MSR cap S$2,340/mth, loan tenure 25yr @ 2.6% → max loan S$515,000 — CLEAR). Monthly repayment: approximately S$2,250/mth — MSR 28.8% PASS. BSD: S$13,800 from CPF. Cash outlay: S$800 (OTP exercise fee) + legal fees ~S$2,500. Move-in: approximately 10 weeks from OTP.

Decision: Option A is S$240,000 cheaper in sticker price but requires a 3.5-year wait. Option B is immediately available and offers full grant stacking. At S$7,800/mth combined income, both options are financially feasible. The couple should weigh the rental cost during the BTO wait period (estimated S$80,000–S$100,000 over 3.5 years if renting privately) against the S$240,000 BTO price advantage.

What First-Timers Often Get Wrong

The most common mistake is treating the HFE letter as a mere formality — in fact, it is the document that locks in your grant entitlement. Applying for an HFE too early (income changes between HFE and purchase can reduce grants) or too late (HFE takes 2–3 weeks, which can cause you to miss an OTP deadline) both have real financial consequences. A second common error is underestimating CPF accrued interest: every dollar of CPF and grants deployed for the property accumulates 2.5% interest annually, which must be refunded to CPF upon sale. On a S$300,000 CPF drawdown over 10 years, that refund obligation reaches approximately S$85,000 — significantly reducing net cash in hand at sale. Third, first-timers sometimes overlook the BSD timing difference between BTO (payable on exercise of the Sale and Purchase Agreement, typically several years after ballot) and resale (payable within 14 days of signing the OTP) — a BTO purchase technically defers the BSD cash outflow.

What Might Come Next

Industry observers note that the new Standard/Plus/Prime BTO classification, introduced in 2024, is still bedding in. The October 2026 BTO exercise is expected to offer approximately 7,970 flats across Bedok, Geylang, Sembawang, Tengah, Toa Payoh, and Yishun — providing first-timer couples with options across multiple towns. The Bedok Bayshore sites (adjacent to Bayshore MRT) are being watched closely as the first BTO flats in a new waterfront neighbourhood. Policy observers have also been monitoring whether HDB will adjust the EHG income bands as Singapore’s median household income continues to rise, though no changes have been announced as of June 2026. The 15-month Wait-Out Period (WOP) for private property owners who wish to purchase an HDB resale flat — introduced in September 2022 — remains in place, adding a structural floor to HDB resale demand as upgraders are prevented from buying immediately.

Frequently Asked Questions

Can I apply for a BTO as a first-timer if I currently live in a private property?

Yes, provided you are an SC citizen and have never previously purchased a subsidised HDB flat. However, if you (or your spouse) currently own a private residential property in Singapore, you must dispose of it within 6 months of receiving the keys to your BTO flat. Overseas private property does not disqualify you. The 30-month Look-Back Period applies to resale HDB flat applications, not BTO ballot applications — so private property owners can ballot for a BTO flat while still holding their private property, as long as they sell it after receiving keys.

My spouse is a second-timer. Do we still get first-timer benefits?

You are treated as an “essential occupier + first-timer” family unit. For BTO balloting, you get first-timer ballot priority (2 chances). For grants, you can still claim the EHG based on your individual first-timer status. For resale, you can claim the Half-Housing Grant (half the Family Grant amount) rather than the full Family Grant. Your spouse’s second-timer status does not eliminate your personal grant eligibility, but it does reduce the total grant quantum compared to an all-first-timer couple.

How long does the HFE letter application take, and when should I apply?

The HFE letter typically takes 2–3 weeks to process from the date of submission. You should apply before — not after — you identify a flat. For BTO applicants, apply at least 3 weeks before the BTO launch window opens. For resale buyers, apply before you start your flat search, since an OTP seller may ask you to exercise within 14–21 days, and you need your HFE confirmed before you can proceed to the resale portal. The HFE is valid for 9 months; if it expires, you must reapply.

Can I use CPF to pay for the Option to Purchase (OTP) fee and BSD?

No — the OTP option fee (S$500–S$1,000) and the OTP exercise fee (1% of purchase price) must be paid in cash. BSD, however, can be paid from your CPF OA once the Option to Purchase is exercised. Your solicitor will process the CPF withdrawal for BSD after the OTP is exercised and the conveyancing process begins. Cash payments made before CPF is available cannot be reclaimed from CPF later.

What is the Deferred Income Assessment (DIA) and does it affect my grants?

The Deferred Income Assessment (DIA) allows eligible first-timer couples who are full-time students, National Service (NS) personnel, or freelancers with irregular income to defer their income declaration until key collection, when the EHG quantum is then assessed. This prevents buyers from being penalised during a temporarily low-income phase. The DIA is not automatic — you must declare eligibility at the HFE application stage. If your income rises significantly between application and key collection, your EHG may be lower than expected.

What is the Minimum Occupation Period (MOP) and what can I do during it?

The MOP is the minimum period you must live in an HDB flat before you can sell it on the open market. For standard HDB flats purchased from HDB (BTO), the MOP is 5 years from the date you collect your keys. For Plus classification BTO flats, the MOP is 10 years. During the MOP, you cannot rent out the entire flat (you can rent out individual bedrooms, subject to HDB approval and quota rules). You also cannot purchase a private residential property in Singapore until the MOP is cleared, unless you are buying it to upgrade and will sell the HDB flat within 6 months.

How much cash do I actually need to buy my first HDB flat?

For an HDB loan (no bank loan), the minimum cash required is remarkably low. The 20% down payment can come entirely from CPF OA. BSD is payable from CPF. Legal fees (~S$2,000–S$3,000) are payable in cash. The OTP option fee (S$500–S$1,000) and exercise fee (1%) are in cash, but these are modest. Total cash outlay for a S$500,000 BTO with HDB loan and S$80,000 CPF balance: approximately S$6,000–S$8,000 in cash (legal fees + OTP fees). For a bank loan, the minimum 5% cash down payment on S$500,000 is S$25,000 — the largest single cash item.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore CPF Property Usage Guide 2026: OA Withdrawal, Accrued Interest and Retirement Sum Rules

- Singapore HDB Flat Eligibility Guide 2026: HFE Check, Income Ceilings and What Qualifies You

- Singapore HDB CPF Housing Grant Guide 2026: EHG, Family Grant, PHG and More

- HDB BTO vs Resale Flat 2026: Complete Comparison

- Singapore Property Financing Guide 2026: LTV, TDSR, MSR and HDB vs Bank Loan

- Singapore Buyer’s Stamp Duty (BSD) Guide 2026

Disclaimer

This article is for general information only and does not constitute financial, legal, or conveyancing advice. Grant amounts, income ceilings, LTV ratios, and stamp duty rates are subject to change by HDB, IRAS, and MAS at any time. All figures quoted are as of June 2026. Readers should verify all information with official sources — HDB (www.hdb.gov.sg), IRAS (www.iras.gov.sg), MAS (www.mas.gov.sg), and CPF Board (www.cpf.gov.sg) — before making any property purchase decision. For complex situations involving second-timer spouses, foreign co-buyers, or inherited properties, consult a licensed conveyancing lawyer.