HDB Resale Levy Singapore 2026: Complete Guide for Second-Timer Flat Buyers

- The HDB Resale Levy applies when a second-timer household buys a new BTO flat or a new Executive Condominium (EC) from a developer after previously enjoying a housing subsidy.

- Levy amounts range from S$15,000 (2-Room Flexi) to S$55,000 (Multi-Generation flat), based on the flat type you are selling.

- The levy does not apply if you buy a resale HDB flat on the open market, or if you buy private property.

- Payment comes from your sale proceeds (CPF refund + cash). If proceeds fall short, you must top up in cash.

- The policy ensures those who already benefited from a large housing subsidy pay back a portion before receiving a second round of public housing support.

- If your previous subsidised home was an Executive Condo (EC), the levy is calculated differently: 15% of your net EC resale proceeds, subject to a minimum of S$15,000.

- Singles under the Single Singapore Citizen (SSC) scheme or Joint Singles Scheme may also be subject to the levy if buying a second subsidised flat.

What Is the HDB Resale Levy?

The HDB Resale Levy is a financial charge levied by the Housing and Development Board (HDB) on households who apply to purchase a second new subsidised flat — either a Build-to-Order (BTO) flat or a new Executive Condominium (EC) sold directly by a developer — after having previously benefited from a public housing subsidy.

The policy exists to uphold the principle of equity in Singapore’s public housing system. New BTO flats and ECs are sold at prices significantly below open-market value, a subsidy funded by taxpayers. HDB’s view is that once a household has enjoyed this advantage, they should not receive the same full quantum of subsidy a second time without contributing back to the system. The resale levy is that contribution.

Introduced in its current fixed-amount form for households that sold their first subsidised flat on or after 3 March 2006, the levy has remained a cornerstone of Singapore’s housing mobility framework. HDB administers the levy directly, collecting it at the point when the second subsidised flat purchase is completed.

Who Has to Pay the HDB Resale Levy?

The levy applies specifically to second-timer households. HDB classifies a household as a second-timer when at least one applicant has previously:

- Received a housing subsidy from HDB — including the Enhanced CPF Housing Grant (EHG), the Central Provident Fund Housing Grant (CPF-HG), the Special CPF Housing Grant (SHG), or any earlier-generation grant — when buying a resale flat; or

- Bought a new BTO, Build-to-Order Sales of Balance Flats (SBF), or EC flat directly from a developer.

If you are a first-timer — meaning you have never previously bought an HDB flat or EC, and have not received a CPF housing grant for a resale purchase — you do not pay the resale levy on your first BTO or EC purchase, regardless of price or flat type.

The levy also applies to Singles buying under the Single Singapore Citizen (SSC) scheme who have previously owned a subsidised flat, and to non-citizen spouses in joint applications where the Singapore Citizen applicant is a second-timer.

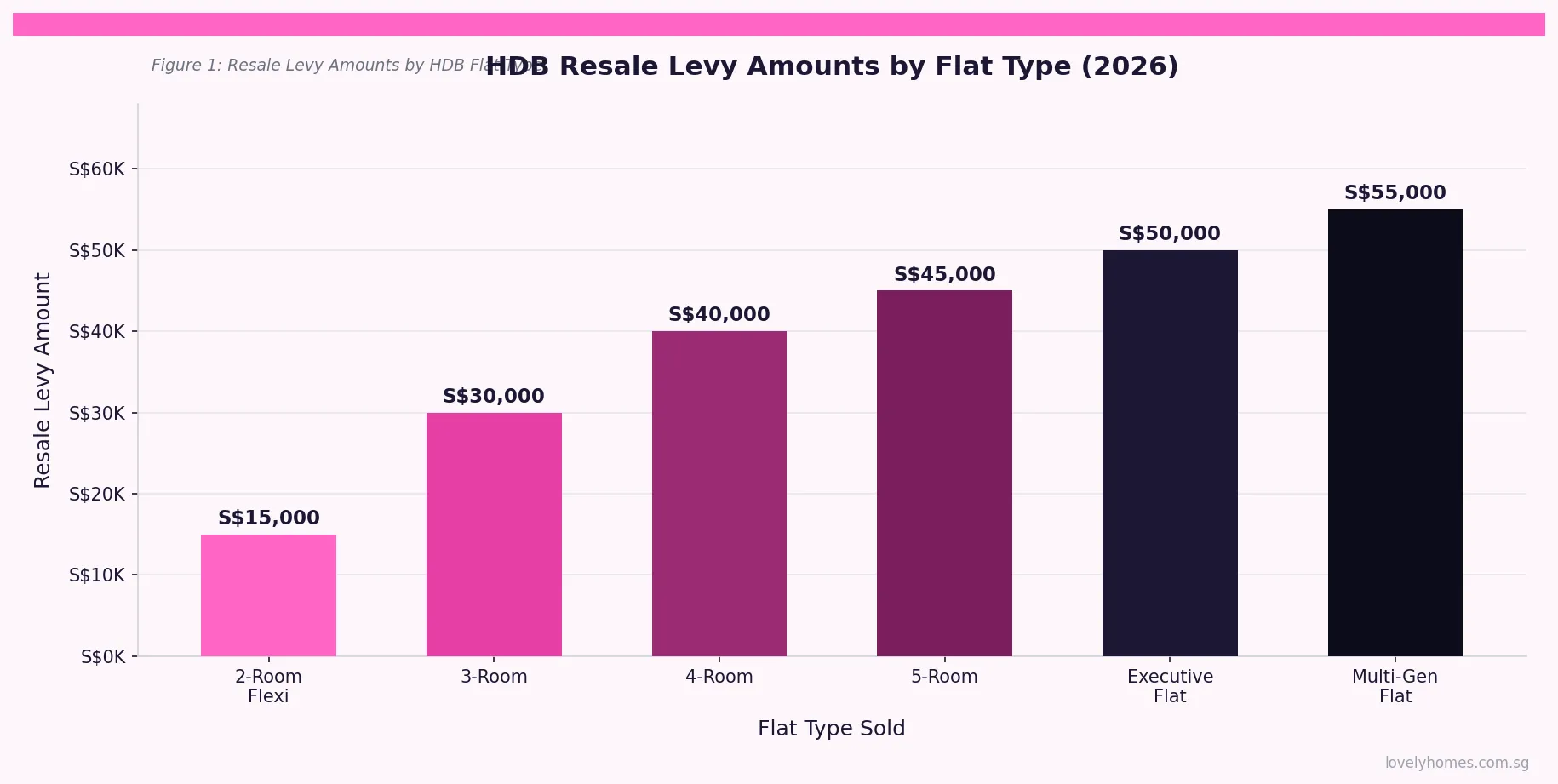

Resale Levy Amounts by Flat Type (2026)

The levy is fixed and based on the type of HDB flat you are selling, not on the purchase price of your next flat. This table shows the 2026 schedule:

| Flat Type Sold | Resale Levy (Fixed) | Notes |

|---|---|---|

| 2-Room Flexi | S$15,000 | Lowest levy; applies to Type 1 and Type 2 2-room flats |

| 3-Room | S$30,000 | Applies to 3-room BTO and resale-with-grant flats sold |

| 4-Room | S$40,000 | Most common flat type; levy payable on proceeds |

| 5-Room | S$45,000 | Includes 5-room improved and 5-room model A flats |

| Executive Flat | S$50,000 | Applies to executive maisonettes and executive apartments |

| Multi-Generation (Multi-Gen) Flat | S$55,000 | Highest fixed levy; Multi-Gen flats are rare and targeted at three-generation families |

| DBSS Flat | By flat type equivalent | A DBSS 4-room incurs S$40,000; 5-room incurs S$45,000 |

| Executive Condominium (EC) | 15% of net resale proceeds (min. S$15,000) | Only applies if you previously bought an EC directly from a developer and are now buying a new BTO/EC |

Key point on DBSS flats: Design, Build and Sell Scheme (DBSS) flats are treated equivalently to standard HDB flats of the same flat type for levy purposes. The levy on a 4-room DBSS flat sold is S$40,000 — the same as a standard 4-room HDB.

Key point on ECs: Executive Condominiums sold before their 5-year Minimum Occupation Period (MOP) are treated differently. If you sold your EC at the 5-year MOP mark (when it is still classified as an HDB property for resale purposes) and wish to buy another subsidised flat, your levy is calculated at 15% of the net resale price of the EC, not a fixed sum. The minimum levy is S$15,000.

When Does the Resale Levy Apply?

The trigger for the levy is narrow and precise: it applies only when a second-timer household purchases a new subsidised flat from HDB directly (BTO or SBF exercise) or a new EC from a developer. It does not apply in any of the following scenarios:

- Buying a resale HDB flat on the open market — even if you are a second-timer, no levy is charged when you buy a resale flat (though you will also receive no EHG or CPF housing grants).

- Buying private property — the levy is exclusively a feature of the subsidised public housing system.

- Transferring ownership within the family — an intra-family transfer is not a new subsidised purchase and does not trigger the levy.

- First-timers — by definition, if you have not previously received a housing subsidy, the levy does not apply.

One nuance worth noting: if you buy a resale HDB flat with a CPF housing grant (making you a subsidised buyer of a resale flat), you become a second-timer for future subsidised flat purchases. Should you later apply for a BTO or new EC, the resale levy will apply at that stage, calculated on the flat you had originally bought with the grant.

How Is the Resale Levy Paid?

The levy is deducted from the proceeds of your flat sale. In practice, HDB coordinates the payment as part of the resale transaction. The sequence is:

- You agree to sell your existing flat and apply for a new BTO flat or EC concurrently.

- At the point of your existing flat’s resale completion, HDB retains the levy amount from the sale proceeds.

- The retained amount is credited to HDB’s account — it is not returned to your CPF Ordinary Account.

- If your sale proceeds (after CPF refund) are insufficient to cover the levy, you must make up the shortfall in cash.

Unlike CPF principal and accrued interest (which are refunded to your CPF OA and can be redeployed for the next flat), the resale levy is gone once deducted. It is a one-time levy and cannot be offset against BSD, legal fees, or any other cost of the new purchase.

There is no option to defer the levy or to split it across multiple payment dates. It must be settled in full at the point of sale completion of the existing flat. HDB does not currently offer any hardship waiver or instalment arrangement for the levy.

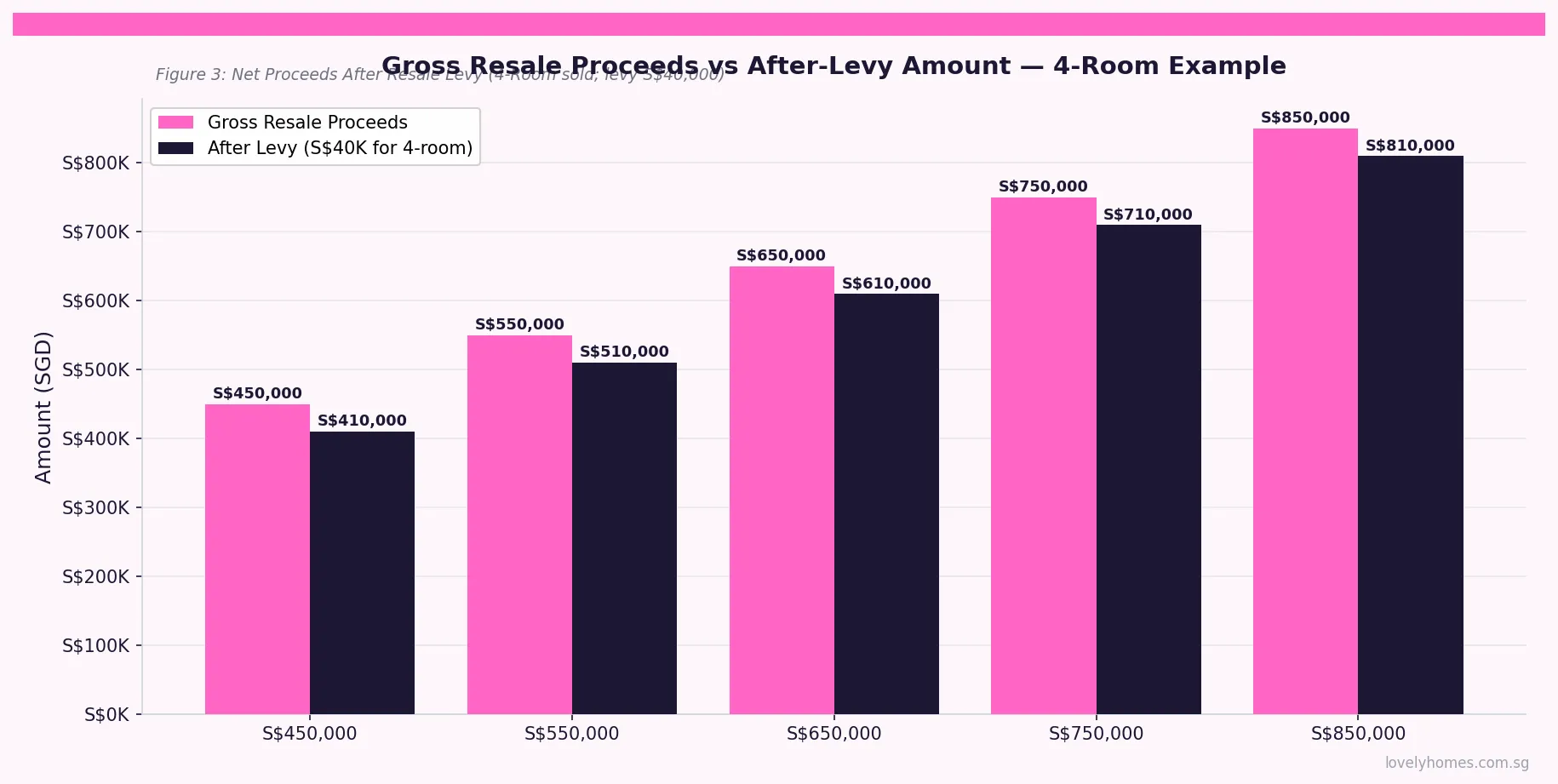

Net Proceeds After the Levy

Understanding your effective net proceeds after the levy is deducted helps with financial planning for your next purchase. The chart below illustrates how the S$40,000 levy on a 4-room flat affects gross sale proceeds at five common price points:

Critically, the levy reduces the pool of funds available for your CPF Ordinary Account refund and cash portion. If you are relying on the proceeds to fund the downpayment on a new BTO flat, factor the levy deduction in from the outset. A 4-room flat sold at S$550,000 effectively becomes S$510,000 in terms of what flows back to you and HDB.

Resale Levy vs HDB Grants: The Netting Question

A common question from second-timers is whether HDB grants can offset the resale levy. The short answer is no. Grants and the levy operate entirely separately:

- Second-timers who buy a new BTO flat receive reduced grants compared to first-timers. For example, a second-timer buying a new BTO flat under the Step-Up CPF Housing Grant may receive S$15,000 — far less than the S$80,000–S$120,000 available to first-timer families under the EHG.

- The resale levy is charged in addition to the reduced grant quantum. It is not deducted from any grant or factored into the BTO price.

- The combined effect is that second-timers face a higher effective cost of a new BTO purchase: less grant assistance AND an upfront levy payment.

This is the intended design. HDB’s rationale is that second-timers have already benefited significantly from the subsidised housing system and have had the opportunity to accumulate equity in their first flat. The reduced grants and levy together calibrate the subsidy quantum to reflect that prior benefit.

Worked Example: The Yip Family’s Resale Levy Calculation

Scenario: 4-Room Flat Sold, New 4-Room BTO Purchased

Mr and Mrs Yip, both Singapore Citizens, bought a 4-room BTO flat in Punggol in 2014 for S$390,000. They are now selling the flat (estimated market value S$610,000) and applying for a new 4-room BTO flat in Tengah under the Married Child Priority Scheme.

| Item | Amount |

|---|---|

| Gross resale price of Punggol 4-room flat | S$610,000 |

| CPF principal drawn + accrued interest (estimated) | S$320,000 (refunded to CPF OA) |

| Outstanding HDB mortgage balance | S$48,000 (repaid from proceeds) |

| HDB Resale Levy (4-room sold) | S$40,000 |

| Agent commission (1% + 9% GST) | S$6,649 |

| Legal fees (seller) | S$2,500 |

| Net cash proceeds to Mrs & Mr Yip | S$192,851 |

New Tengah BTO (4-room, estimated S$480,000 — Plus model):

| Item | Amount |

|---|---|

| BTO price | S$480,000 |

| Step-Up CPF Housing Grant (2nd-timer) | -S$15,000 |

| Net payable | S$465,000 |

| HDB loan (80% LTV, 2nd-timer eligible) | S$372,000 @2.60% 25yr = S$1,682/mth (MSR 18.7% of S$9,000/mth joint income) |

| Downpayment (20% — CPF OA) | S$93,000 from CPF OA refund |

| BSD (S$480,000) | S$8,700 |

| Legal fees (buyer) | S$2,500 |

| Remaining CPF OA balance after DP | S$227,000 (reserve for mortgage servicing) |

MSR check: S$1,682 / S$9,000 = 18.7% — within 30% MSR limit. TDSR not applicable (HDB loan). The S$40,000 resale levy is a sunk cost; Mr and Mrs Yip’s CPF OA reserve of S$227,000 provides strong mortgage cover for the Tengah BTO.

What This Means for Second-Timers Planning to Upgrade

The resale levy is best understood as a built-in “subsidy recapture” mechanism. For households who bought a 3-room or 4-room BTO flat in the 2010s and have watched flat values rise substantially — Tampines 4-rooms regularly changing hands above S$600,000 in 2025–2026 — the S$30,000–S$40,000 levy is relatively modest relative to the capital gain they have made. In such cases, the levy is unlikely to derail the upgrade path.

The levy becomes more financially significant in two scenarios: (a) where the flat was held for a shorter period and appreciation is limited, or (b) where the household plans to buy a new EC priced at the upper end of the income ceiling — here, the reduced grant quantum combined with the levy can meaningfully increase the cash component required at completion.

From a policy perspective, Singapore’s resale levy is notably lighter than comparable mechanisms in other high-density housing markets. Hong Kong’s Home Ownership Scheme imposes resale restrictions rather than monetary levies; Taiwan’s affordable housing schemes cap resale gains outright. Singapore’s fixed-levy approach offers transparency and predictability — households know their exact levy exposure from the moment they decide to sell.

What Might Come Next

The following is editorial speculation based on observed policy trends and should not be relied upon for financial decisions.

HDB has not adjusted the fixed resale levy amounts since the current schedule took effect in 2006. Given that resale flat prices have increased substantially over the past two decades — the HDB Resale Price Index rose from a base of 100 in 1998 to approximately 183 in early 2026 — there is a reasonable argument that the S$15,000–S$55,000 range represents a declining proportion of the subsidy value enjoyed by second-timers.

Industry observers have periodically suggested that HDB may consider indexing levy amounts to flat values or the RPI. A levy pegged at, say, 7%–8% of the median resale price of the flat type sold would automatically adjust over time. Whether HDB will move in this direction is unknown; any change would likely be accompanied by an extended transition period given the direct impact on household finances.

Frequently Asked Questions

I’m selling a 4-room flat but buying a 3-room BTO. Does the levy depend on what I buy or what I sell?

The levy is calculated based on the flat type you are selling, not the flat type you are buying. If you sell a 4-room flat, you pay S$40,000 regardless of whether you buy a 2-room, 3-room, or 5-room BTO next. The type of your next flat does not affect the levy amount.

My spouse is a first-timer but I am a second-timer. Do we pay the resale levy?

Yes. In a joint application, if any one applicant is classified as a second-timer, the household is treated as a second-timer application and the resale levy applies. The levy is calculated on the flat type sold by the second-timer applicant. This is a common scenario for couples where one partner previously owned a subsidised flat before the marriage.

Can I use CPF Ordinary Account funds to pay the resale levy?

No. The resale levy is not a property purchase cost that HDB allows to be paid from CPF. It is deducted from the proceeds of the sale of your existing flat — which includes CPF funds refunded from that sale — but the levy itself flows out of those proceeds before they are returned to your CPF OA. The practical effect is that the levy reduces the CPF amount credited back to your OA, and any shortfall must be topped up in cash. You cannot make a direct CPF OA withdrawal specifically for the levy.

Does the resale levy apply if I sell my HDB flat to buy a private condo?

No. The resale levy only applies when you are purchasing a new subsidised flat (BTO, SBF, or new EC from a developer). If you sell your HDB flat and purchase a private condominium, no resale levy is charged. You may, however, incur ABSD if you own or co-own any other residential property at the time of the private property purchase. The levy and ABSD are separate instruments with separate triggers.

What happens if my resale proceeds are not enough to cover the levy?

If the net proceeds from your flat sale (after repaying the HDB mortgage and refunding CPF principal + accrued interest to your CPF OA) are insufficient to cover the levy, you must pay the shortfall in cash before the resale transaction can be completed. HDB will not approve the new flat application until the levy is settled in full. There is no waiver, reduction, or instalment scheme for the levy, even in cases of genuine financial hardship.

I sold my 4-room flat in 2004. Does the current levy schedule apply to me?

No. The fixed-levy schedule described in this guide applies only to households who sold their first subsidised flat on or after 3 March 2006. If you sold your first subsidised flat before that date, the earlier levy framework applies, which was based on a percentage of the resale price (15% for 3-room and above). If you are uncertain which regime applies to you, contact HDB directly with your transaction details.

My previous flat was a DBSS flat I bought from a developer. Do I pay the levy?

Yes, if the DBSS flat was purchased directly from a developer under HDB’s Design, Build and Sell Scheme, you are considered to have purchased a subsidised flat. When you sell the DBSS flat and apply for a new BTO or EC, the resale levy applies based on the flat type of the DBSS flat sold. A 4-room DBSS attracts S$40,000; a 5-room DBSS attracts S$45,000. The levy is the same as for a standard HDB flat of the equivalent type.