HDB upgrader — the Singaporean who has served their Minimum Occupation Period, built up equity in their flat, and now wants to step up to a private condo or a larger resale flat — is one of the most financially significant actors in Singapore’s property market. For many families, this is the single largest financial decision of their lives: timing it correctly can mean saving S$300,000 in ABSD; getting it wrong can mean paying that sum in full, in cash, within 14 days. This guide walks through every step, cost, rule, and strategy for the Singapore HDB upgrader in 2026.

Quick Answer — HDB upgrader essentials

- MOP requirement: You must complete the 5-year Minimum Occupation Period on your HDB flat before selling it or buying a private residential property.

- Three upgrade paths: Bigger HDB resale (no ABSD), Executive Condo EC (no ABSD, income ceiling S$16,000), or private condo (ABSD 20% if buying before selling).

- ABSD remission window: If you buy a private condo before selling your HDB, you pay ABSD 20% upfront — but IRAS will refund it if you sell your HDB within 6 months of the private OTP date.

- Financial pressure point: ABSD on a S$1.5M condo is S$300,000 cash — ring-fenced before the 14-day ABSD payment deadline.

- CPF accrued interest: Budget for the CPF principal + accrued interest refund on HDB sale — this reduces your immediate cash payout but returns money to your CPF OA.

- TDSR impact: Buying before selling your HDB means your HDB loan is still on your record for TDSR purposes — get the stress test done early.

Who Is the HDB Upgrader?

The HDB upgrader broadly refers to a Singapore household that currently owns an HDB flat (BTO or resale) and plans to move to a higher-value property — either a bigger or better-located HDB resale flat, an Executive Condominium (EC), or a private condominium or landed property. The upgrade motivation is typically a combination of changing family needs (growing household size, desire for better facilities), improved household income over time, and investment considerations (private property appreciates differently from HDB).

In 2026, upgrader demand remains a significant driver of both the HDB resale market and the new private launch market. The typical upgrader profile is a dual-income Singapore Citizen couple in their mid-30s to mid-40s, with a paid-down HDB flat carrying S$300,000–S$600,000 in equity, and combined income sufficient to pass the Total Debt Servicing Ratio (TDSR) stress test for a S$1.2M–S$2M condominium.

Step 1 — Check Your MOP Status

The Minimum Occupation Period (MOP) is the first gate every HDB upgrader must pass. You must have physically occupied your flat for the full MOP period before you can sell it on the open market or purchase a private residential property.

MOP durations in 2026 depend on flat classification. Standard BTO and resale HDB flats (both mature and non-mature estates) carry a 5-year MOP from the date the keys are collected. Plus and Prime classification flats introduced under the new framework carry a 10-year MOP. Executive Condominiums are HDB-administered at purchase and carry a 5-year MOP for resale; they are fully privatised after 10 years.

The MOP clock begins from the date of key collection (for BTO) or completion (for resale). It runs continuously regardless of whether you remain in the flat or rent it out (in some cases). Partial absence — such as working overseas — may pause the MOP clock, and you must reconfirm your MOP status with HDB before proceeding.

MOP Warning for Plus/Prime Flat Buyers: If you purchased a Plus or Prime classification BTO flat (launched from the August 2023 exercise onwards), your MOP is 10 years, not 5 years. Buyers who purchased these flats in 2023–2024 will not be able to upgrade to private property until 2033–2034 at the earliest. Factor this extended lock-up into your long-term planning.

Step 2 — Choose Your Upgrade Path

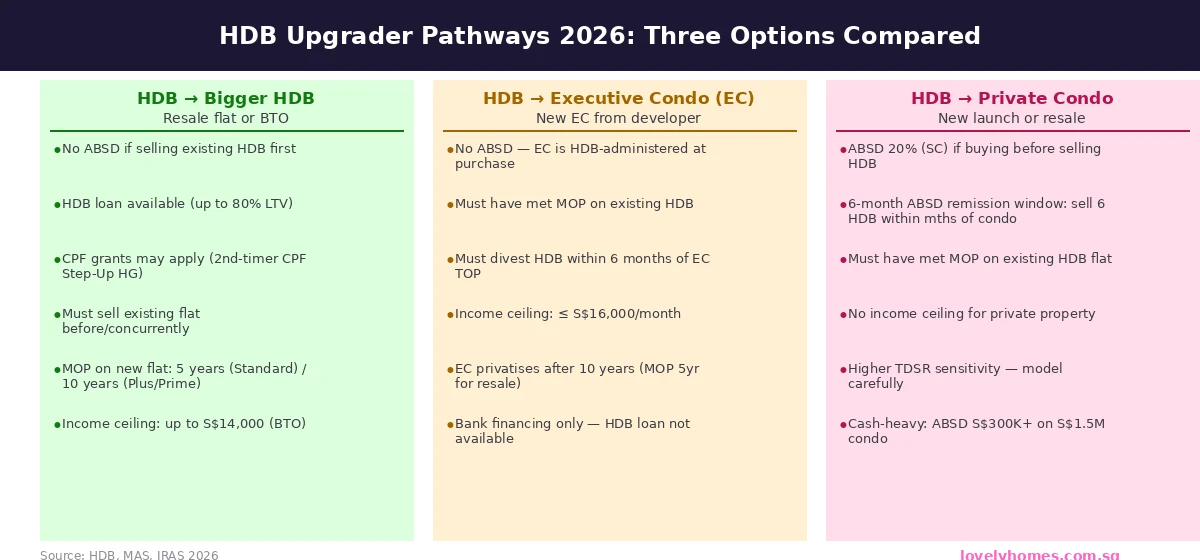

Once MOP is confirmed, you have three main upgrade paths. Each carries different ABSD treatment, financing rules, income restrictions, and flexibility.

Path A: Bigger HDB Resale Flat. The most financially conservative option. Upgrading from a 3-room to a 5-room or executive flat in a different estate carries no ABSD (you are not buying a second property — you are buying another HDB flat while selling the first). You can use an HDB housing loan (LTV 80%) and may qualify for the Step-Up CPF Housing Grant (up to S$15,000 for second-timers buying a 4-room or smaller resale flat). The downside is that HDB resale flats do not appreciate in the same way as private property and cannot be rented out without restriction.

Path B: Executive Condominium (EC). An EC sits between public and private housing. At launch, it is sold by a developer under HDB rules — meaning no ABSD at purchase (it is treated as a first-timer residential property). You must divest your existing HDB flat within 6 months of EC completion (TOP), otherwise penalties apply. The household income ceiling is S$16,000/month. After 5 years from TOP, you can sell on the open market to Singapore Citizens and PRs; after 10 years, it is fully privatised and can be sold to foreigners. Bank financing only — no HDB loan for EC.

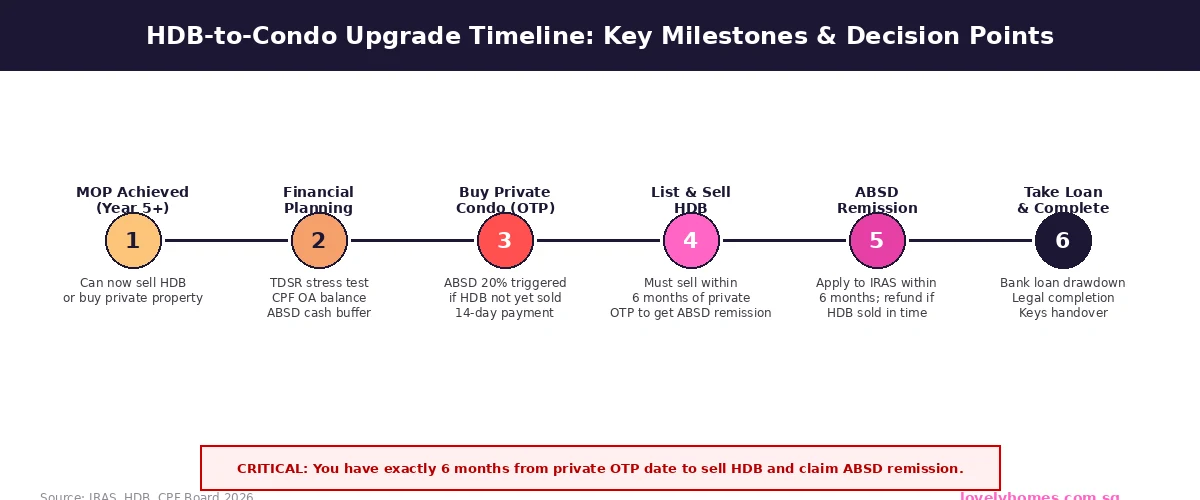

Path C: Private Condominium or Landed Property. The most expensive and financially demanding path. If you buy a private property before selling your HDB flat, you are technically holding two residential properties simultaneously — triggering ABSD of 20% for Singapore Citizens. You have two sub-options: sell your HDB first (safer, no ABSD, but you need interim accommodation), or buy first and claim the ABSD remission by selling within the 6-month window.

The ABSD Remission Strategy — Buy First, Sell Later

The most common upgrader strategy for those targeting private property is the “buy first, sell later” approach using the ABSD remission for married couples (where at least one spouse is a Singapore Citizen). Under this framework:

- You sign the OTP for the private property and pay ABSD 20% (for SC) within 14 days of OTP date — in cash.

- You simultaneously list and market your HDB flat for sale.

- You must complete the sale of your HDB flat within 6 months of the private property OTP date (not completion date).

- Within 6 months of HDB sale completion (and within the original 6-month window), you file for the ABSD remission with IRAS.

- If approved, IRAS refunds the full ABSD paid, with no interest (i.e., you have effectively loaned the Government S$300,000 interest-free for up to 6–12 months).

The risk is liquidity: you need S$300,000+ in ready cash to pay the ABSD at the 14-day deadline. If you cannot sell your HDB within 6 months — due to market conditions, a slow transaction, or a buyer who defaults — the ABSD is not refunded. Some upgraders bridge the gap with a bridging loan, but these are expensive (typically prime + 1–2%) and have their own TDSR implications.

Summary: Upgrade Path Comparison at a Glance

| Factor | Bigger HDB Resale | Executive Condo (EC) | Private Condo |

|---|---|---|---|

| ABSD | None (HDB-to-HDB, sell first) | None at purchase | 20% SC if buying before selling HDB; refundable if HDB sold within 6 months |

| Financing | HDB loan (80% LTV) or bank | Bank loan only | Bank loan only |

| Income Ceiling | None for resale; S$14,000 for BTO | S$16,000/month | None |

| MOP to Sell New Property | 5 years (10 for Plus/Prime) | 5 years (privatised at 10 years) | No MOP (private property) |

| CPF OA Usable? | Yes (HDB and bank loans) | Yes (bank loan) | Yes (up to Valuation Limit) |

| Rental Flexibility | Restricted — HDB rules apply | Restricted pre-privatisation | Full rental freedom |

| Typical Price Range | S$350K–S$800K | S$900K–S$1.6M | S$1.2M–S$3M+ |

Financial Planning for the Upgrade

Beyond the ABSD, upgraders must plan for a cluster of costs that come together at roughly the same time. A disciplined approach models each of the following:

CPF accrued interest on HDB sale proceeds: Your CPF principal withdrawn for the HDB flat, plus 2.5% p.a. compounded interest for every year you held it, must be refunded to your CPF OA from the HDB sale proceeds. On a S$350,000 CPF withdrawal held for 8 years, accrued interest is approximately S$78,000 — meaning S$428,000 goes back to CPF, not to your cash pocket (though it is available for the condo purchase).

TDSR with two loans: If you buy the condo before selling your HDB, both your HDB loan instalment and the projected condo loan instalment are counted in your TDSR. On a combined income of S$15,000/month, the 55% TDSR cap allows maximum total monthly debt obligations of S$8,250. If your HDB instalment is S$1,500 and the projected condo instalment is S$5,800, your combined TDSR is 48.7% — within limits. Lenders will also stress-test the condo loan at a higher rate (currently 4%), so run this calculation carefully.

6-month bridging period cash buffer: Between paying the private property ABSD, the downpayment, and waiting for the HDB sale to complete and CPF refund to process, upgraders need a substantial cash buffer. Industry guidance suggests setting aside at least 12 months of combined mortgage payments plus the full ABSD amount as liquid savings before signing the private OTP.

Worked Example: The Lim Family’s Upgrade

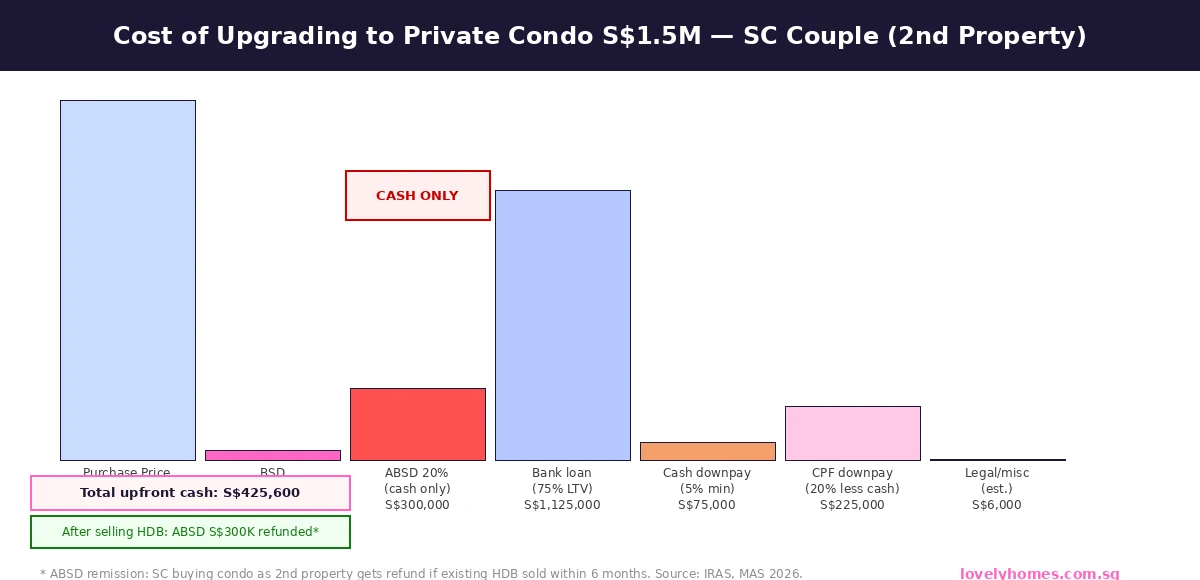

Profile: Mr and Mrs Lim, SC couple, combined income S$14,500/month. Own a 4-room Punggol BTO flat (keys August 2020), CPF OA balance: Mr S$182,000, Mrs S$145,000. Cash savings: S$380,000. Target: OCR 3-bedroom condo at S$1.55M.

MOP check: Keys August 2020 → MOP satisfied August 2025 ✓

BSD on S$1.55M: S$46,600 (from CPF OA) ✓

ABSD (SC 2nd property): S$310,000 — must be paid in cash at OTP

Downpayment: Bank loan 75% LTV = S$1,162,500 loan. Remaining 25% = S$387,500. Min cash 5% = S$77,500. Balance from CPF = S$310,000

Cash required at OTP: ABSD S$310,000 + option fee 1% S$15,500 = S$325,500 cash within 14 days of OTP

TDSR check: Projected condo instalment at 3.5% over 25yr = S$5,802/mth. HDB instalment still on record: S$1,340/mth. Combined S$7,142/mth ÷ S$14,500 = 49.3% ✓ (under 55%)

HDB sale (6 months after OTP): Sold for S$760,000. CPF refund: S$319,000 (principal) + S$38,000 (accrued 5.5yr at 2.5%) = S$357,000 to CPF OA. Outstanding HDB loan: S$368,000. Net cash from HDB sale: S$760,000 − S$368,000 − S$357,000 (CPF) − S$8,000 (legal/misc) = S$27,000 net cash

ABSD remission: IRAS refunds S$310,000 ABSD within ~10 weeks of HDB sale completion ✓

Net position post-transaction: S$27,000 new cash + S$310,000 ABSD refund + S$357,000 new CPF OA balance → strong CPF position for condo loan repayments; minimal cash surplus (S$337,000 pre-condo closing costs from HDB cash + ABSD refund)

Common Mistakes HDB Upgraders Make

Forgetting ABSD is cash: The single most common error. Buyers who have set aside the full downpayment in CPF but do not have liquid cash for the ABSD face a crisis at the 14-day deadline. No lender will advance ABSD as part of the mortgage; no CPF withdrawal is permitted for ABSD.

Not accounting for the CPF refund: Many upgraders estimate their HDB “profit” as sale price minus outstanding loan, forgetting that a large CPF principal and accrued interest amount must first be returned to CPF. This can reduce cash-in-hand from the HDB sale by S$200,000–S$450,000 depending on how long the flat was owned and how much CPF was used.

Missing the 6-month window: If the HDB sale process hits delays — a buyer who withdraws, a bank valuation dispute, or an HDB resale application processing delay — the 6-month window can expire. Once it does, the ABSD is not refunded. Upgraders should list the HDB flat immediately after signing the private OTP, price it competitively, and have legal conveyancing engaged in parallel.

Underestimating TDSR exposure: Some upgraders are surprised when their bank pre-approval does not cover the desired loan quantum because the HDB loan is still reflected in their TDSR. Always get a fresh In-Principle Approval (IPA) with both loans in scope before signing the private OTP.

What Might Come Next for HDB Upgraders

Singapore’s cooling measures framework has not changed since April 2023, and upgrader ABSD at 20% represents the base cost of accessing private property while still holding an HDB flat. The Government has shown no appetite for relaxing this rate in the near term, given its explicit goal of moderating speculative demand from HDB-to-private upgraders. Any future relaxation would likely be preceded by a sustained period of flat or declining private property prices.

The emergence of Plus and Prime HDB classification flats, with 10-year MOPs and restrictions on renting out to non-family members, has already created a two-tier HDB resale market. Upgraders who purchased Plus or Prime flats in 2023–2024 face a much longer lock-up, and their upgrading flexibility will be significantly constrained until the early-to-mid 2030s. The long-term impact of this policy on upgrader dynamics is still playing out.

Frequently Asked Questions About HDB Upgrading

Do I have to sell my HDB flat before buying a private condo to avoid ABSD?

You do not have to sell first, but if you buy before selling, you will pay ABSD 20% (SC) or 30% (PR) upfront in cash. The ABSD remission framework allows you to claim a full refund if you sell your HDB within 6 months of signing the private OTP. The “sell first” approach avoids the ABSD cash outlay entirely but means you need temporary housing between HDB completion and condo handover (which can be 2–4 years for new launches). Most upgraders choose “buy first, sell within 6 months” to avoid the gap, provided they have sufficient cash for the ABSD.

Can I use my HDB flat’s rental income to help with the TDSR for the condo loan?

Yes — but only if you have HDB’s approval to sublet the flat and you can provide documented rental income. Lenders typically apply a haircut of 30% to rental income when calculating TDSR (i.e., only 70% of gross rental income is counted as qualifying income). If your HDB flat generates S$2,500/month in verified rental income, S$1,750 may be added to your income base for TDSR purposes. Note that owner-occupiers on MOP cannot legally sublet their entire flat until MOP is completed, so this applies primarily to upgraders who have already completed MOP and chosen to rent out their HDB while purchasing a condo.

What happens if I fail to sell my HDB within 6 months and miss the ABSD remission?

If you do not sell your HDB within 6 months of the private OTP date, you forfeit the ABSD remission permanently. The S$300,000+ ABSD you paid in cash is retained by IRAS — it cannot be recovered. This is a catastrophic financial outcome for most households. To mitigate this risk: price your HDB competitively from day one, engage conveyancing lawyers for both transactions simultaneously, and do not accept a buyer for the HDB who requires more than 8–10 weeks to complete. If you are approaching the 5-month mark and the HDB has not sold, consider drastically reducing the asking price or seeking legal advice on options.

Is an EC a good upgrade target compared to a private condo?

An EC offers a unique value proposition: you buy at a price typically S$200,000–S$500,000 below a comparable private condo in the same location, with the same physical quality (developer-built to private standards). The trade-off is the HDB ownership conditions for the first 5–10 years — no subletting to foreigners, must divest HDB within 6 months of EC TOP, and income ceiling of S$16,000. For upgraders who meet the income ceiling and are comfortable with the constraints, ECs have historically outperformed many private condo segments in capital appreciation after privatisation at 10 years. However, ECs are only available as new launches — there is currently no resale EC from a developer; the secondary market is for existing privatised ECs sold by owners.

Can both spouses use their CPF OA for the condo purchase even if they are selling the HDB?

Yes. Once the HDB sale is completed, CPF refunds (principal + accrued interest) are credited back to each owner’s CPF OA in proportion to their respective CPF usage on the flat. Those refreshed CPF OA balances can then be applied to the condo purchase — for downpayment, monthly loan repayments, and BSD — subject to the condo’s own Valuation Limit. Many upgraders rely on this CPF “recycling” to fund a significant portion of the condo downpayment after the ABSD remission is returned to their bank account.

What is the Seller’s Stamp Duty (SSD) impact when upgrading?

Seller’s Stamp Duty applies to private residential properties sold within 3 years of purchase — at 12% (Year 1), 8% (Year 2), or 4% (Year 3). HDB flats are exempt from SSD. For most HDB upgraders, SSD is not relevant to the HDB sale (no SSD applies). SSD would only become relevant if you later sold the private condo within 3 years of purchase — which is an important consideration for upgraders who buy a new-launch condo that is still under construction. If market conditions deteriorate and you needed to exit quickly, SSD could cost S$180,000+ on a S$1.5M condo sold in Year 1.

Related Articles

- HDB MOP Singapore 2026: Complete Guide to Minimum Occupation Period

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore CPF for Property Guide 2026: Valuation Limits and Accrued Interest

- Singapore Stamp Duty Calculator 2026: BSD and ABSD Explained

- Singapore Condo Buying Process 2026: Step-by-Step from Offer to Keys

- Singapore Property Cooling Measures 2026: Complete Guide to ABSD, TDSR and LTV

Disclaimer: This article is for general informational purposes only and does not constitute financial, legal, or property advice. ABSD rates, MOP rules, CPF withdrawal limits, and TDSR/MSR parameters are set by the Government and may change. All figures reflect the framework as at 3 July 2026. Readers should verify current rules with HDB, IRAS, and CPF Board, and consult a licensed financial adviser and property solicitor before proceeding with any upgrade transaction. LovelyHomes does not provide financial, legal, or property advisory services.

0 Comments