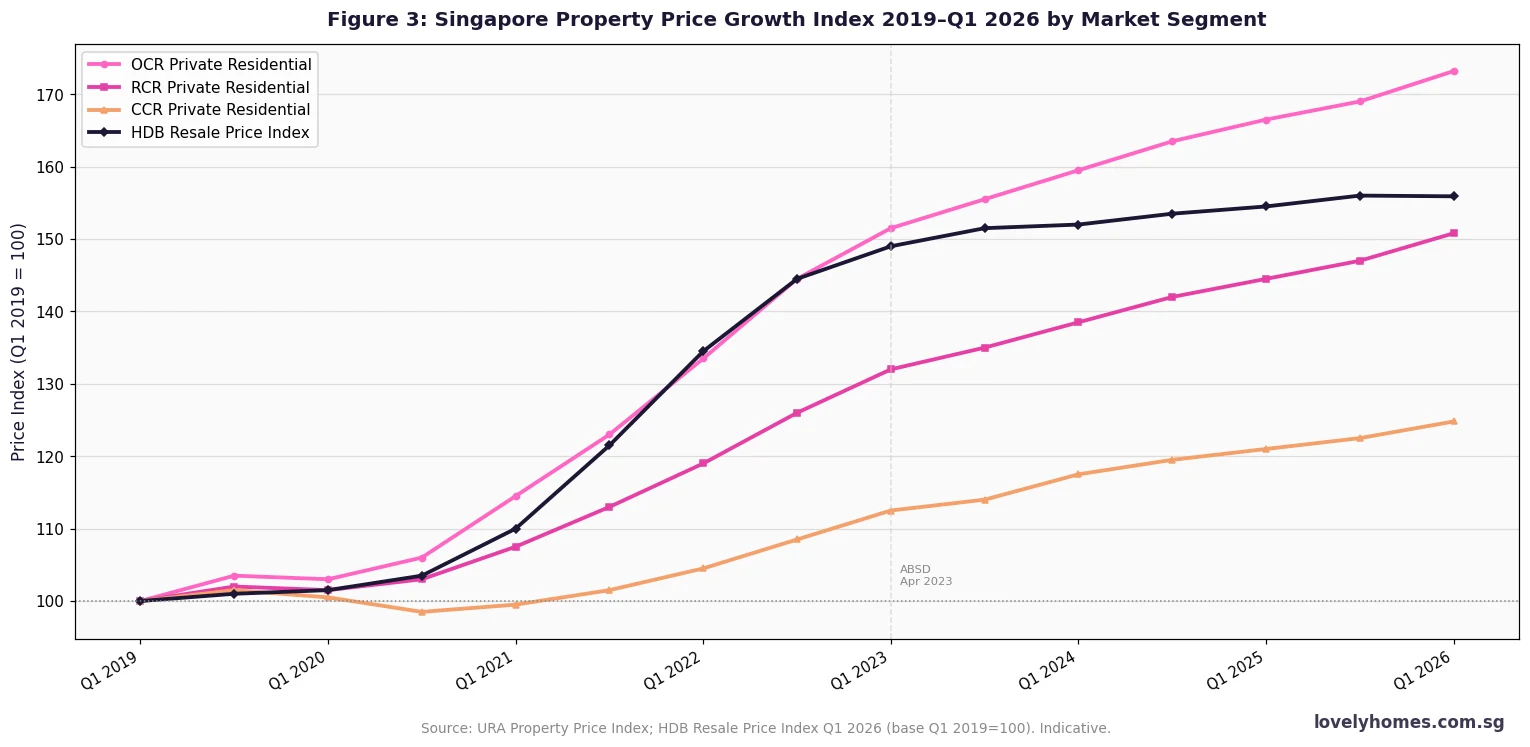

Price growth: OCR private residential prices rose +2.2% in Q1 2026; RCR +1.6%; CCR -0.3%; HDB resale -0.1% — a stabilising market post-2023 cooling measures.

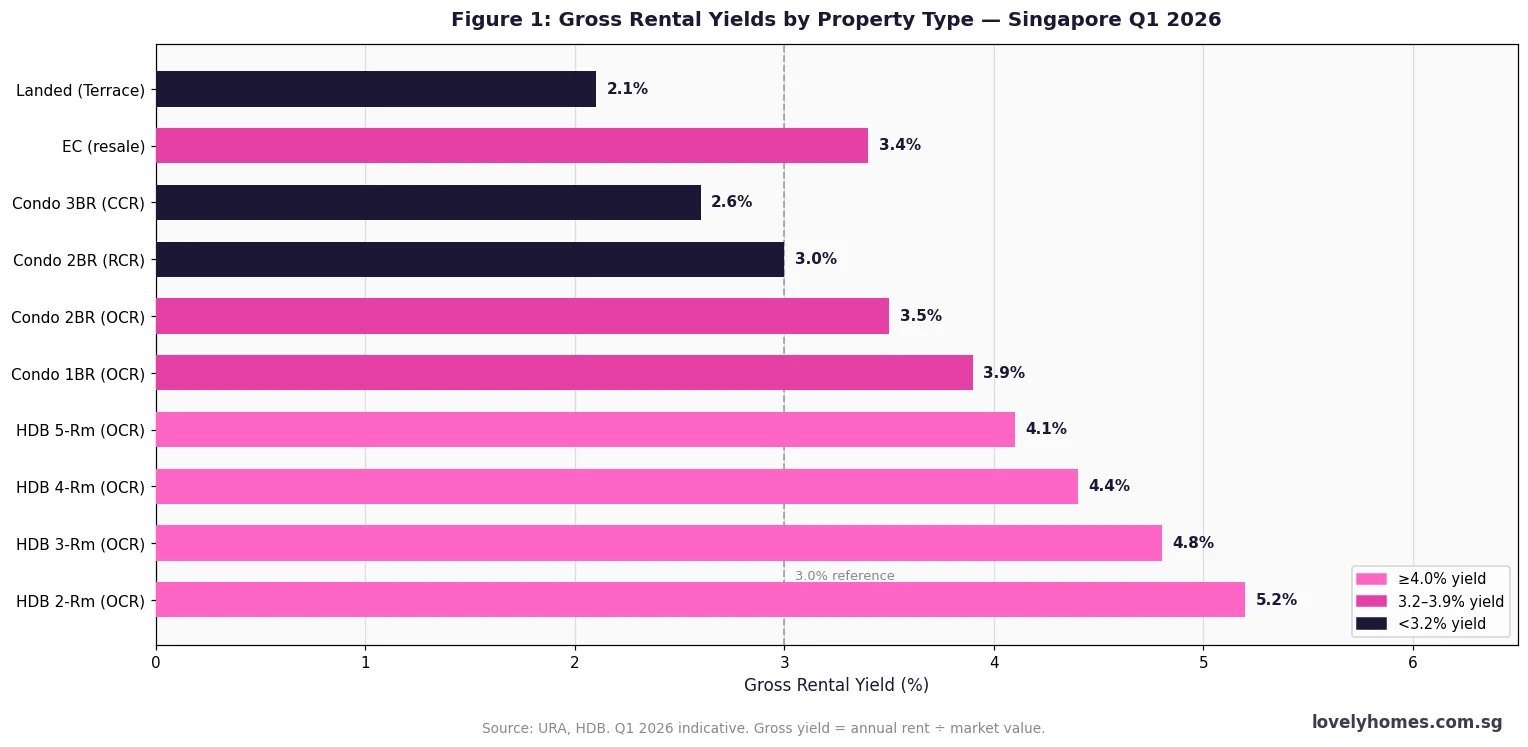

Rental yields: HDB flats generate the highest gross yields at 4.1–5.2%; OCR condos 3.5–3.9%; CCR condos 2.5–2.8%.

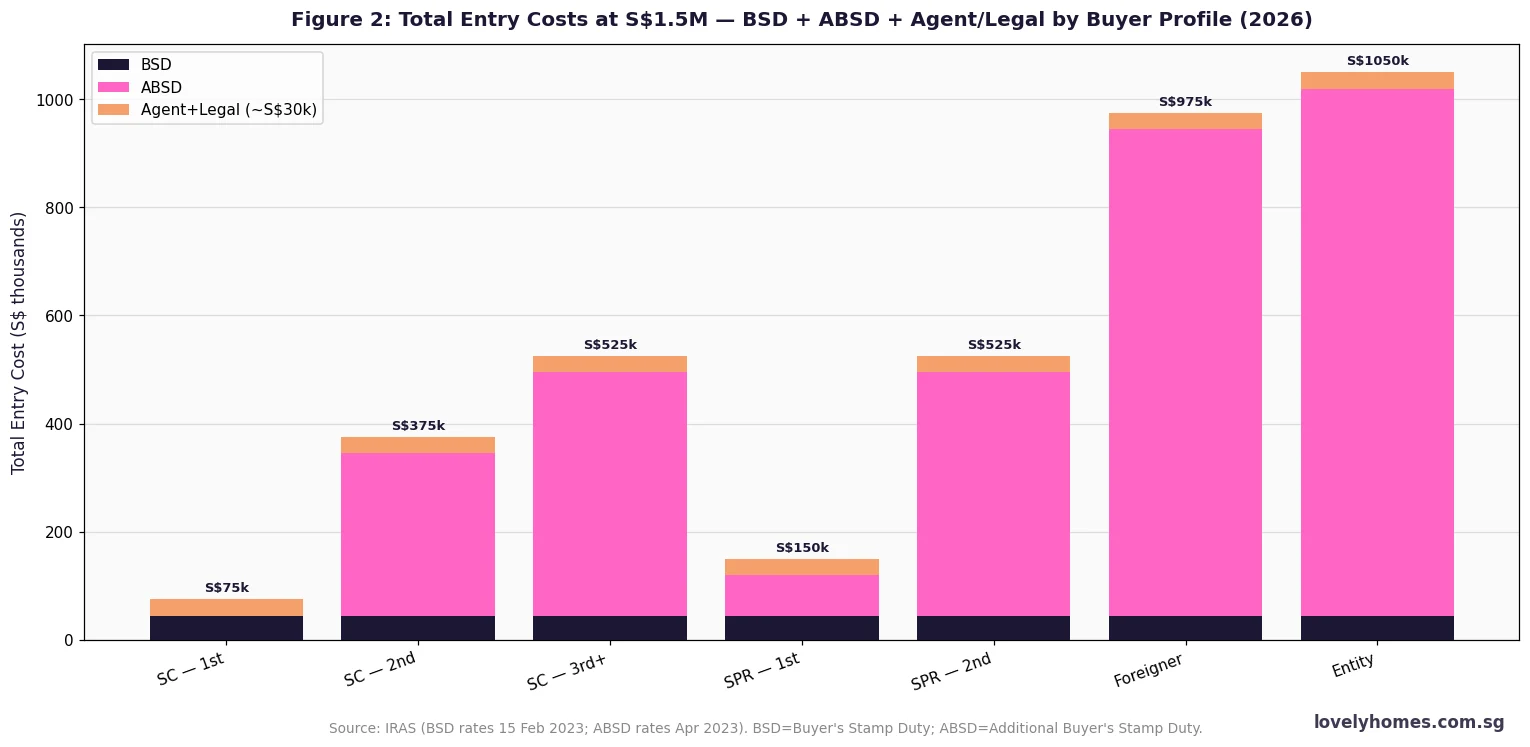

ABSD is the single biggest cost variable: Singapore Citizens pay 0% on their first property and 20% on the second; foreigners pay 60%. ABSD must factor into every ROI calculation.

BSD starts at 1% and rises progressively to 6% above S$3M. A S$1.5M condo incurs S$44,600 in BSD alone.

Financing: TDSR is capped at 55% of gross income; MSR at 30% for HDB and EC purchases. CPF OA can fund downpayment and mortgage instalments but accrues 2.5% interest payable on sale.

Capital appreciation: OCR private prices are up ~73% since Q1 2019; HDB resale up ~56%; CCR up ~25%.

Pipeline risk: total private residential pipeline stands at ~61,000 units as at Q1 2026 — elevated supply is a medium-term moderating factor.

Best entry strategies for most Singapore households: HDB resale (high yield, government grants available) → EC (medium yield, capital gains on privatisation) → OCR condo (growth play, TDSR-permitting).

What is Property Investment in Singapore?

Property investment in Singapore means acquiring residential or commercial real estate with the objective of generating rental income, capital appreciation, or both. Singapore’s property market is one of the most regulated in Asia — by design. The Urban Redevelopment Authority (URA) controls land supply through the Government Land Sales (GLS) programme; the Housing & Development Board (HDB) administers public housing policy; the Monetary Authority of Singapore (MAS) governs financing limits; and the Inland Revenue Authority of Singapore (IRAS) collects stamp duties.

This web of regulation is not accidental. Singapore uses property policy as a macro-prudential tool — adjusting ABSD rates, LTV caps, and supply releases to prevent asset-price bubbles and ensure housing remains accessible. For investors, understanding why each rule exists is as important as knowing the rates themselves, because policy changes (like the April 2023 ABSD hike to 60% for foreigners) can transform return profiles overnight.

This guide covers every dimension a Singapore property investor needs to understand in 2026: property types, buyer profiles, costs, financing, yields, price trends, and entry strategies — all benchmarked against current government data.

Singapore divides its residential market into three broad categories. The HDB market covers public housing flats, which house roughly 80% of Singapore’s resident population. HDB flats are sold by the government at subsidised prices via the Build-To-Order (BTO) scheme or on the open resale market. Singapore Citizens and Permanent Residents may own HDB flats under eligibility rules; foreigners may not. The executive condominium (EC) market is a hybrid tier — EC units are built by private developers on government land, initially subject to HDB eligibility rules, and progressively privatised after 5 years (partial privatisation) and 10 years (full privatisation), at which point foreigners may purchase them. The private property market includes condominiums, apartments, and landed houses, open to all buyer profiles subject to ABSD.

Geographically, URA divides Singapore into three market segments: the Core Central Region (CCR) — the prime districts 9, 10, 11 and Marina Bay — characterised by high absolute prices and lower yields but strong expat demand; the Rest of Central Region (RCR) — inner-ring districts like Queenstown, Toa Payoh, Bishan — offering a balance of capital upside and rental demand; and the Outside Central Region (OCR) — suburban estates like Tampines, Punggol, Jurong East, Woodlands — which offer the highest rental yields and the strongest capital growth over the past five years driven by HDB upgrader demand.

Figure 1: Gross rental yields by property type, Singapore Q1 2026. HDB flats continue to generate the highest gross yields at 4.1–5.2%. Source: URA, HDB.

Singapore Property Prices in 2026 — What the Data Says

URA’s Q1 2026 private residential price index recorded an overall increase of +0.9% quarter-on-quarter — a steady but measured pace following the April 2023 ABSD hike that cooled the market materially. By segment, OCR led at +2.2%, reflecting robust HDB upgrader demand for suburban condos; RCR rose +1.6%; while CCR dipped -0.3% as the 60% foreign buyer ABSD continued to suppress transaction volumes in the prime market. The landed residential segment eased -0.4%. HDB resale prices slipped -0.1% — the first quarterly dip after an unbroken run of increases since 2021 — which analysts attribute to increased BTO supply and the dampening effect of PLH and Plus-category resale restrictions.

On a five-year basis, the performance picture differs significantly by segment. OCR private prices are up approximately 73% since Q1 2019 (base year), driven by the work-from-home boom, pent-up upgrader demand, and the record-low supply of new OCR launches between 2020 and 2022. RCR has risen roughly 51%; CCR approximately 25%; and the HDB Resale Price Index approximately 56% over the same period — a remarkable run for public housing given its subsidised entry cost.

Buyer Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD)

Stamp duties are the single largest transaction cost in Singapore property and cannot be ignored in any investment analysis. Buyer’s Stamp Duty (BSD) applies to all property purchases regardless of buyer profile. It is progressive: 1% on the first S$180,000, 2% on the next S$180,000, 3% on the next S$640,000, 4% on the next S$500,000, 5% on the next S$1.5M, and 6% above S$3M (rates effective 15 February 2023). On a S$1.5M property, BSD amounts to S$44,600.

Additional Buyer’s Stamp Duty (ABSD) is the more consequential levy. Rates (effective April 2023) vary by buyer profile and property count: Singapore Citizens pay nil on their first property, 20% on their second, and 30% on their third or subsequent. Singapore Permanent Residents pay 5% on their first, 30% on the second. Foreigners pay a flat 60%; entities (companies) pay 65%. Certain FTA nationals (US, Swiss, and Icelandic/Liechtenstein/Norwegian nationals purchasing residential property) are treated the same as Singapore Citizens for ABSD on their first property under trade agreement provisions.

Figure 2: Total entry costs at S$1.5M including BSD, ABSD, and estimated agent/legal fees by buyer profile. Source: IRAS (BSD 15 Feb 2023; ABSD Apr 2023).

Financing: TDSR, MSR, LTV and CPF Rules

MAS introduced the Total Debt Servicing Ratio (TDSR) framework in June 2013 to prevent household over-leverage. Under TDSR, a borrower’s total monthly debt obligations — including the new property loan, car loans, personal loans, and credit card revolving debt — may not exceed 55% of gross monthly income. For married couples buying jointly, the household income can be combined but the same 55% cap applies to combined obligations. The Mortgage Servicing Ratio (MSR), which is more restrictive, limits monthly repayments on HDB flat loans and EC loans to 30% of gross monthly income.

Loan-to-Value (LTV) limits determine maximum loan quantum. For a first property with no outstanding housing loans, HDB concessionary loans allow up to 80% LTV (on purchase price or valuation, whichever is lower) with a minimum 5% cash downpayment. Bank loans for a first property are capped at 75% LTV, also with at least 5% in cash. For a second property, the LTV cap drops to 45% (with at least 25% cash for the downpayment). Third or subsequent properties: 35% LTV.

CPF Ordinary Account (OA) savings, earning a guaranteed 2.5% p.a., can be used for the property downpayment, monthly mortgage instalments, and stamp duties. However, the Valuation Limit (VL) caps total CPF use at the property’s lower of purchase price or market value, while the Withdrawal Limit (WL) — set at 120% of VL — represents the absolute ceiling if the property has at least 60 years of remaining lease. Any CPF drawn must be refunded with 2.5% accrued interest on eventual sale, which can meaningfully reduce net cash proceeds.

Summary: Key Investment Parameters at a Glance

Parameter

HDB Flat

Executive Condo (EC)

OCR Condo

CCR Condo

Typical price range

S$300k–S$900k

S$850k–S$1.4M

S$900k–S$2.5M

S$1.8M–S$6M+

Gross rental yield

4.1–5.2%

3.2–3.6%

3.4–3.9%

2.3–2.8%

5-year price growth

+8–12% (resale)

+12–18% (resale)

+15–25%

+8–14%

Foreign buyer eligible?

No

Only after 10 yrs

Yes (60% ABSD)

Yes (60% ABSD)

Max LTV (first property)

80% (HDB loan)

75% (bank loan)

75% (bank loan)

75% (bank loan)

Minimum occupation period

5 yrs (PLH/Plus: 10 yrs)

5 yrs before sale

No MOP

No MOP

Income ceiling

S$14,000/mth

S$16,000/mth

None (TDSR applies)

None (TDSR applies)

Capital gains tax

Nil

Nil

Nil (SSD may apply)

Nil (SSD may apply)

Worked Example: SC Household Upgrading from HDB to OCR Condo

Case Study — Mr & Mrs Ong, Singapore Citizens upgrading to a first private property

Household profile: Mr & Mrs Ong, both Singapore Citizens, joint gross income S$14,000/month. They own a 5-room HDB flat in Jurong East which has completed its 5-year MOP, currently valued at S$780,000 (outstanding HDB loan S$220,000; CPF used S$320,000 + S$43,000 accrued interest = S$363,000 total CPF refund on sale). Target: buy an OCR 2BR condo at S$1,350,000.

Step 1 — Sell HDB first: Sale proceeds S$780,000 − HDB loan redemption S$220,000 − CPF refund S$363,000 − agent commission 2% S$15,600 − legal S$2,500 = net cash ~S$178,900. After selling, their ABSD on the new private purchase is nil (first private property, SC). If they buy before selling and hold both simultaneously, the condo purchase would attract 20% ABSD = S$270,000 — avoidable by selling first (or using the SC married couple remission: buy first, sell HDB within 6 months).

Step 2 — Buy OCR condo S$1,350,000: BSD = S$37,400. Minimum cash downpayment = 5% × S$1,350,000 = S$67,500. Balance downpayment 20% total = S$270,000 (S$67,500 cash + S$202,500 CPF). Bank loan: 75% LTV = S$1,012,500 @ 3.0% p.a. 30 years → monthly instalment S$4,268. TDSR check: S$4,268 ÷ S$14,000 = 30.5% — well within 55% PASS. Total upfront cost: S$67,500 (5% cash down) + S$37,400 (BSD) + S$2,800 (legal) = S$107,700 cash. CPF deployed: S$202,500 (balance of 20% down). Net cash from HDB sale S$178,900 covers the full S$107,700 requirement with S$71,200 remaining.

Capital Appreciation: Singapore Property vs Other Asset Classes

Singapore residential property has compounded at an effective annualised rate of roughly 8–10% in OCR markets over the 2019–2026 period — broadly comparable to the Straits Times Index total return of around 6–8% annually, and notably lower than the Nasdaq’s run but with far lower volatility. The critical advantage of property is leverage: a S$270,000 equity stake (20% downpayment on a S$1.35M property) growing at 8% per annum generates capital on the full S$1.35M base, dramatically amplifying the equity return relative to unleveraged assets.

However, leverage cuts both ways. A 15–20% property price correction — comparable to the 2013–2017 period when prices fell roughly 12% following TDSR and cooling measures — would erode a 20% equity buffer significantly. Investors should stress-test their holdings against an interest rate spike (3M SORA remains at approximately 2.4% as at June 2026 but has ranged from 0.05% to 4.0% in the past five years) and against a 12–18 month vacancy period.

Figure 3: Singapore property price index by market segment, Q1 2019 to Q1 2026. OCR leads all segments with ~73% growth over the period. Source: URA, HDB.

Why Singapore Property Remains a Core Investment Asset

Three structural factors continue to underpin Singapore’s residential market. First, land scarcity: Singapore covers 733 km² and cannot expand its land mass materially beyond ongoing reclamation. The total stock of private residential units stands at roughly 365,000, with a pipeline of ~61,000 units as at Q1 2026. Government control of the GLS programme means supply is managed, not market-driven. Second, strong legal framework: Singapore’s property rights are among the most secure globally — clear title, transparent transactions, an independent judiciary, and efficient land registration through the Singapore Land Authority (SLA). Third, no capital gains tax: Singapore does not levy capital gains tax on property. The Seller’s Stamp Duty (SSD), which applies at 12%, 8%, or 4% for properties sold within 1, 2, or 3 years of purchase respectively, effectively discourages speculative flipping but leaves medium-to-long-term investors entirely unaffected.

Compared to peers in the region, Singapore’s regulatory environment is more transparent than Hong Kong or mainland China, and its legal protections are stronger than most ASEAN markets. For high-net-worth individuals and regional corporates, Singapore residential property serves as both a wealth store and a hedge against currency risk in Southeast Asia’s most stable monetary environment.

What Might Come Next: Outlook for H2 2026 and Beyond

Speculation follows, not government guidance. The 2H2026 Government Land Sales programme announced by URA in June 2026 includes nine Confirmed List sites capable of yielding approximately 4,745 residential units and 735 EC units, alongside the landmark Jurong Lake District white site. The sustained supply pipeline is expected to moderate price growth in the OCR to a 1–2% quarterly range through 2026. The Jurong Region Line opening in phases from approximately 2028 will likely catalyse a re-rating of Jurong, Tengah, and Choa Chu Kang OCR pricing, potentially delivering a 8–15% uplift to proximate properties based on historical MRT-opening precedents.

Interest rate trajectory remains the key macro variable. If 3M SORA retreats to the 1.5–2.0% range by late 2026 as some market observers anticipate, monthly servicing costs for SORA-pegged bank loans could fall materially, broadening the pool of TDSR-eligible buyers and supporting price momentum. Conversely, any renewed MAS tightening — whether via further ABSD increases or LTV reductions — could quickly dampen transaction volumes, as the April 2023 measures demonstrated.

Do Singapore Citizens pay any tax on capital gains from property?

No. Singapore does not levy a capital gains tax on residential property sales. However, the Seller’s Stamp Duty (SSD) applies if you sell within three years of purchase: 12% for sale within the first year, 8% within the second year, and 4% within the third year, calculated on the higher of the sale price or market value. Properties held for more than three years attract zero SSD. This means medium-to-long-term investors retain the full capital gain on sale, making Singapore’s tax environment highly favourable for property investment by global standards.

How does ABSD affect investment property returns?

ABSD fundamentally reshapes the return maths for all but first-time SC buyers. A Singapore Citizen purchasing a second property worth S$1.5M pays 20% ABSD = S$300,000 upfront. To break even on this cost alone — before financing and other expenses — the property must appreciate at least S$300,000 beyond the purchase price (roughly a 20% gross gain) before any net profit is realised. For SPR second-property buyers (30% ABSD) and foreigners (60% ABSD), the bar is even higher. This is precisely why many experienced property investors in Singapore prioritise holding their first property long-term and are extremely cautious about second purchases — the ABSD converts a 10% market gain into a near-breakeven outcome.

Can I use CPF to pay for investment property?

Yes, CPF Ordinary Account (OA) funds can be used for the downpayment and monthly mortgage instalments on a second or investment property. However, CPF usage for a second property is subject to the Valuation Limit (VL) and Withdrawal Limit (WL = 120% of VL), and critically — all CPF drawn must be refunded with 2.5% per annum accrued interest when the property is sold. This means long-holding-period investors will accumulate a substantial refund obligation that directly reduces net sale proceeds. If you have deployed S$400,000 in CPF over 15 years, your refund obligation at 2.5% compound could exceed S$590,000 — a significant deduction from the sale price.

What is the difference between OCR, RCR and CCR for investment purposes?

The three planning regions serve very different investor profiles. The CCR (Core Central Region — Districts 9, 10, 11, Downtown Core, Sentosa) offers prestige, expat rental demand, and freehold tenure, but yields are the lowest at 2.3–2.8% and price growth since 2019 has lagged at ~25%. The RCR (Rest of Central Region — inner suburbs like Queenstown, Toa Payoh, Bishan) offers a middle ground: yields of 3.0–3.5% and solid capital appreciation of ~51% since 2019. The OCR (Outside Central Region — Tampines, Jurong, Woodlands, Punggol) delivers the highest gross yields (3.4–3.9% for condos) and the strongest capital growth (~73% since 2019) driven by HDB upgrader demand. Most Singapore residents with a single investment property budget should look at OCR first.

Is it better to buy an HDB resale flat or a private condo as an investment?

For most Singapore Citizens and PRs within HDB eligibility criteria, HDB resale flats offer compelling investment characteristics: the highest gross rental yields in the market (4.1–5.2%), government grants for eligible buyers, an established tenant pool, and lower absolute entry costs that improve leverage efficiency. The key constraint is the 5-year Minimum Occupation Period (MOP) — 10 years for Plus and Prime flats — during which the flat cannot be rented out entirely and cannot be sold. Private condos offer no MOP, greater flexibility, and exposure to the private price index, but entry costs are significantly higher and yields are lower. For buyers who need immediate rental income and cannot lock up capital for five years, a private condo is the better choice. For patient investors willing to occupy first, HDB offers the most efficient risk-adjusted return in the Singapore market.

What is the Seller’s Stamp Duty (SSD) and when does it apply?

The Seller’s Stamp Duty (SSD) was introduced in February 2010 and last revised in January 2011 to its current three-tier structure. SSD applies to residential properties (and industrial properties, which have a separate regime) sold within three years of purchase. The rates are: 12% if sold within the 1st year of purchase, 8% within the 2nd year, and 4% within the 3rd year. SSD is computed on the higher of the sale price or market value at the date of sale. Inherited properties: SSD runs from the original purchase date of the deceased, not the date of inheritance. For most buy-and-hold investors, SSD is a non-issue, but it effectively eliminates profitable short-term flipping strategies for properties purchased at market rates.

Should I invest in residential property or Singapore REITs?

REITs (Real Estate Investment Trusts) listed on the Singapore Exchange (SGX) offer exposure to commercial, industrial, retail, and hospitality property without the ABSD, TDSR, MOP, and management burden of direct ownership. Singapore REIT distribution yields typically range from 5–7%, compared to 3–4% gross yields for direct residential investment. However, REITs are equity instruments subject to market sentiment volatility and do not carry the leverage benefit of direct property. For investors who cannot qualify for a second property loan under TDSR, or who have already exhausted CPF, REITs offer a capital-light alternative. Most sophisticated investors hold both: direct residential for leverage and capital gains, REITs for yield and liquidity.

Disclaimer: This article is for general educational and informational purposes only and does not constitute financial, investment, legal, or tax advice. Property prices, stamp duty rates, CPF rules, TDSR limits, and government policies are subject to change without notice. All figures and data are sourced from URA, HDB, MAS, IRAS, and CPF Board publications as at June 2026 and are indicative only. Readers should conduct their own due diligence and consult a licensed financial adviser, property agent registered with the Council for Estate Agencies (CEA), and a qualified lawyer or tax professional before making any property investment decision. Past price performance is not indicative of future results.

Quick Answer — Singapore Home Loans at a Glance (2026)

Two main options: HDB Concessionary Loan (2.6% p.a., LTV 80%) and Bank Loan (~3.0–3.7% p.a., LTV 75%).

MSR caps your HDB or EC loan instalment at 30% of gross income; TDSR caps all debt at 55% of income.

Bank loans require a minimum 5% cash downpayment; HDB loans require 5% cash on the 20% downpayment portion.

Floating-rate loans are pegged to SORA (Singapore Overnight Rate Average) — 3M SORA ~2.4% at June 2026.

A S$1 million loan at 3.5% over 25 years costs S$85,000 more in total interest than at 2.6%.

Lock-in periods of 1–3 years are standard on bank fixed-rate packages; exiting early triggers a clawback of ~1.5% of the outstanding loan.

Refinancing after the lock-in expires can save tens of thousands; always compare at least 3 banks’ packages.

What Is a Home Loan and Why Does the Structure Matter?

A home loan (or housing loan) is a secured credit facility from a lender — either the Housing and Development Board or a licensed bank — that allows you to finance the purchase of a residential property in Singapore. The property serves as collateral; if you default, the lender can repossess and sell it to recover the outstanding debt.

The structure matters because small differences in interest rate, tenure, and loan-to-value ratio compound dramatically over a 25–30-year horizon. A 0.9 percentage point difference (say, 2.6% vs 3.5%) on a S$600,000 HDB loan over 25 years translates to roughly S$51,000 in additional interest. That is not a minor detail. Beyond the rate, two Monetary Authority of Singapore (MAS) rules govern how much you can borrow: the Mortgage Servicing Ratio (MSR) for HDB and Executive Condominium (EC) purchases, and the Total Debt Servicing Ratio (TDSR) for all property loans.

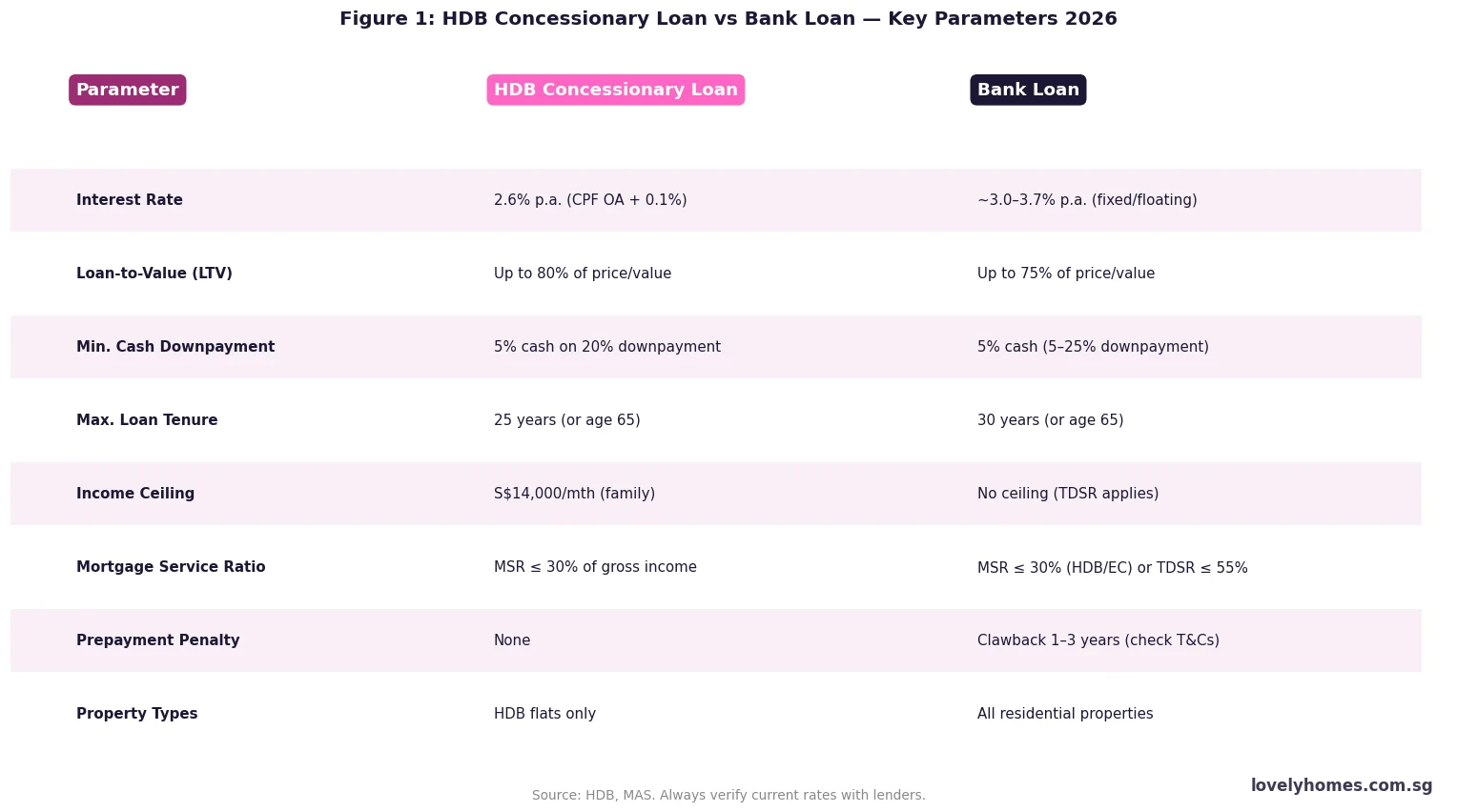

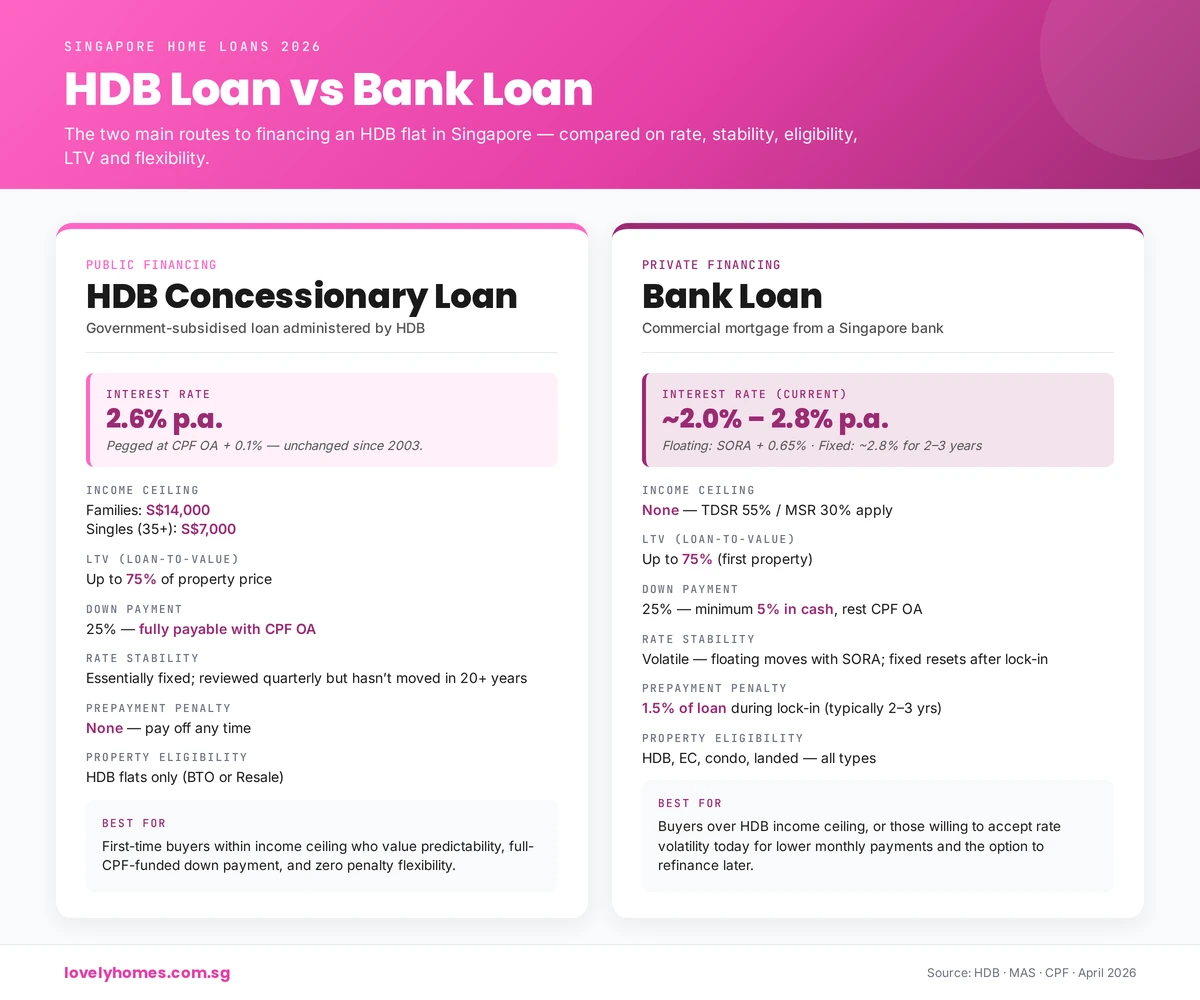

HDB Concessionary Loan vs Bank Loan — The Key Differences

Every Singapore home buyer faces the same first question: HDB loan or bank loan? Each has distinct advantages and constraints. The comparison below sets out the essential differences.

Figure 1: HDB Concessionary Loan vs Bank Loan — Key Parameters (2026). Source: HDB, MAS.

The HDB loan rate of 2.6% p.a. is fixed at 0.1% above the CPF Ordinary Account (OA) rate of 2.5%. It moves only if the CPF OA rate changes — which has not happened since July 1999. Bank loans fluctuate with market rates. At June 2026, the best 2-year fixed bank packages sit at approximately 3.0–3.2% p.a., while SORA-pegged floating packages range from SORA+0.75% to SORA+1.20% (3M SORA ~2.4%, implying ~3.15–3.60% all-in).

HDB Concessionary Loan — Eligibility and Key Rules

To qualify for the HDB loan, at least one buyer must be a Singapore Citizen; the household gross income must not exceed S$14,000 per month (families) or S$7,000 (singles); and no buyer may currently own or have disposed of private property in the 30 months before the flat application. You also need a valid HDB Flat Eligibility (HFE) letter — a mandatory pre-application document from HDB confirming your loan eligibility, CPF grant entitlement and maximum loan quantum (mandatory since May 2023, valid for 9 months).

The maximum loan under the HDB loan is 80% of the lower of the purchase price or valuation. On a S$700,000 flat that is S$560,000. The remaining 20% (S$140,000) is the downpayment — at least 5% (S$35,000) must be cash; the rest may come from CPF OA.

Bank Loans — LTV, Lock-in and SORA

Bank loans allow a longer maximum tenure (30 years vs 25 years), access to all property types, and — potentially — lower rates during low-rate periods. The trade-off is variability and the lock-in period. Most bank fixed rates carry a lock-in of 1–3 years, after which the loan reprices to a floating SORA-pegged rate. The Loan-to-Value (LTV) for a bank loan is 75% if you have no outstanding loans; 45% if you have one; 35% if two or more. SORA replaced SIBOR as the benchmark rate on 1 October 2024 following the MAS phase-out of SIBOR.

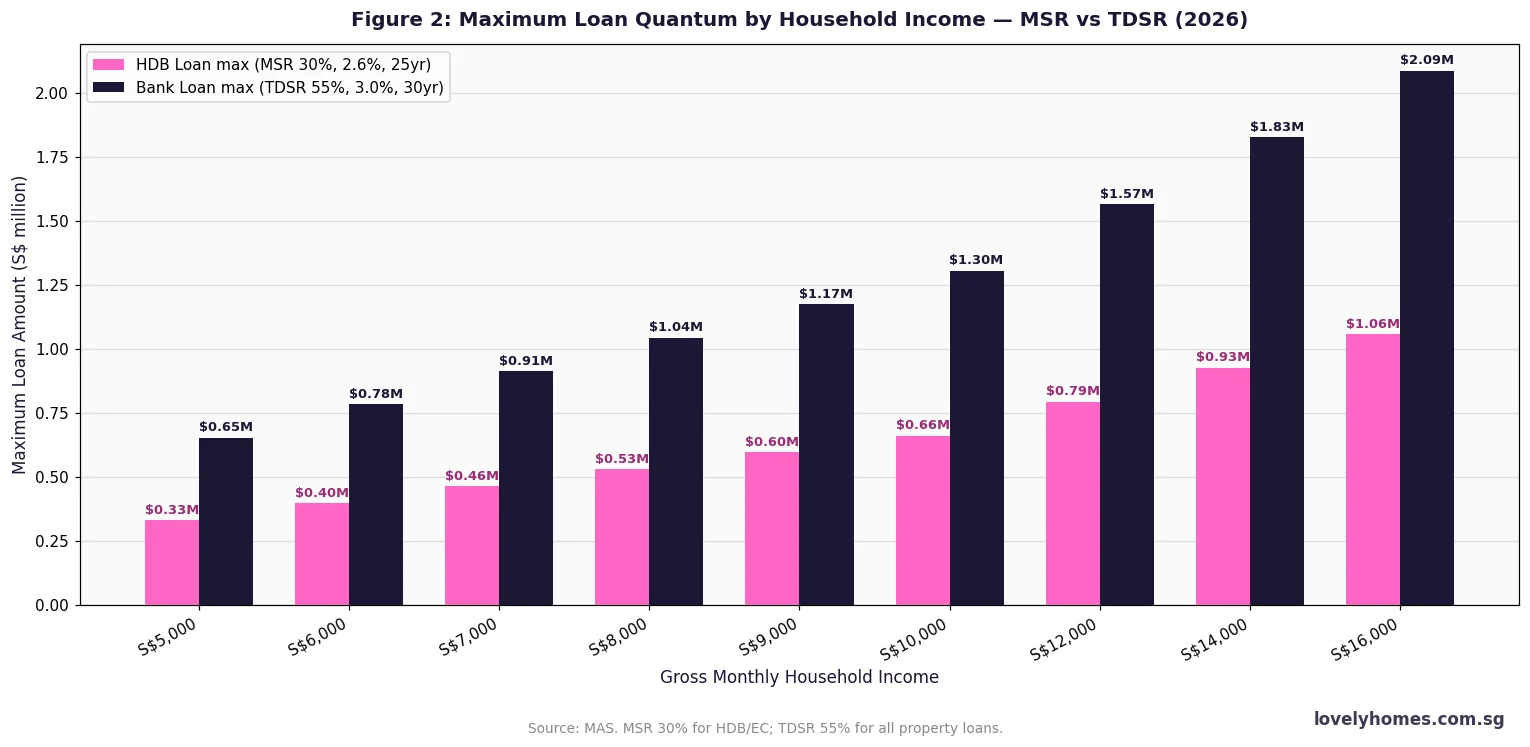

MSR and TDSR — How Much Can You Actually Borrow?

The MAS introduced the TDSR framework in June 2013 and has maintained it as the primary constraint on borrowing. For HDB and EC purchases, the MSR applies as a tighter cap.

TDSR ≤ 55%: Total monthly debt obligations — home loan plus all other debts — must not exceed 55% of gross monthly income.

MSR ≤ 30%: For HDB and EC purchases only — the monthly home loan repayment alone must not exceed 30% of gross monthly income.

Figure 2: Maximum Loan Quantum by Household Income — MSR (HDB/EC) vs TDSR (private property), 2026.

A household earning S$10,000 per month can borrow up to approximately S$826,000 on an HDB loan (MSR 30% at 2.6% p.a. over 25 years) or up to S$1,514,000 under TDSR on a bank loan for private property (55% at 3.0% p.a. over 30 years). The MSR is the binding constraint for HDB buyers; TDSR is the constraint for private property buyers.

Fixed Rate vs Floating Rate (SORA) — Which Is Better?

Fixed-rate packages offer certainty: the rate is locked for 2–3 years. After the lock-in, the loan reverts to a floating rate and you may reprice or refinance. Breaking the lock-in early triggers a clawback penalty of approximately 1.0–1.75% of the outstanding loan.

Floating-rate packages pegged to 3M compounded SORA move with the market. When rates fall, your instalment falls. When rates rise (as they did sharply in 2022–2023), your instalment rises. Floating packages currently sit at SORA + 0.75%–1.20%.

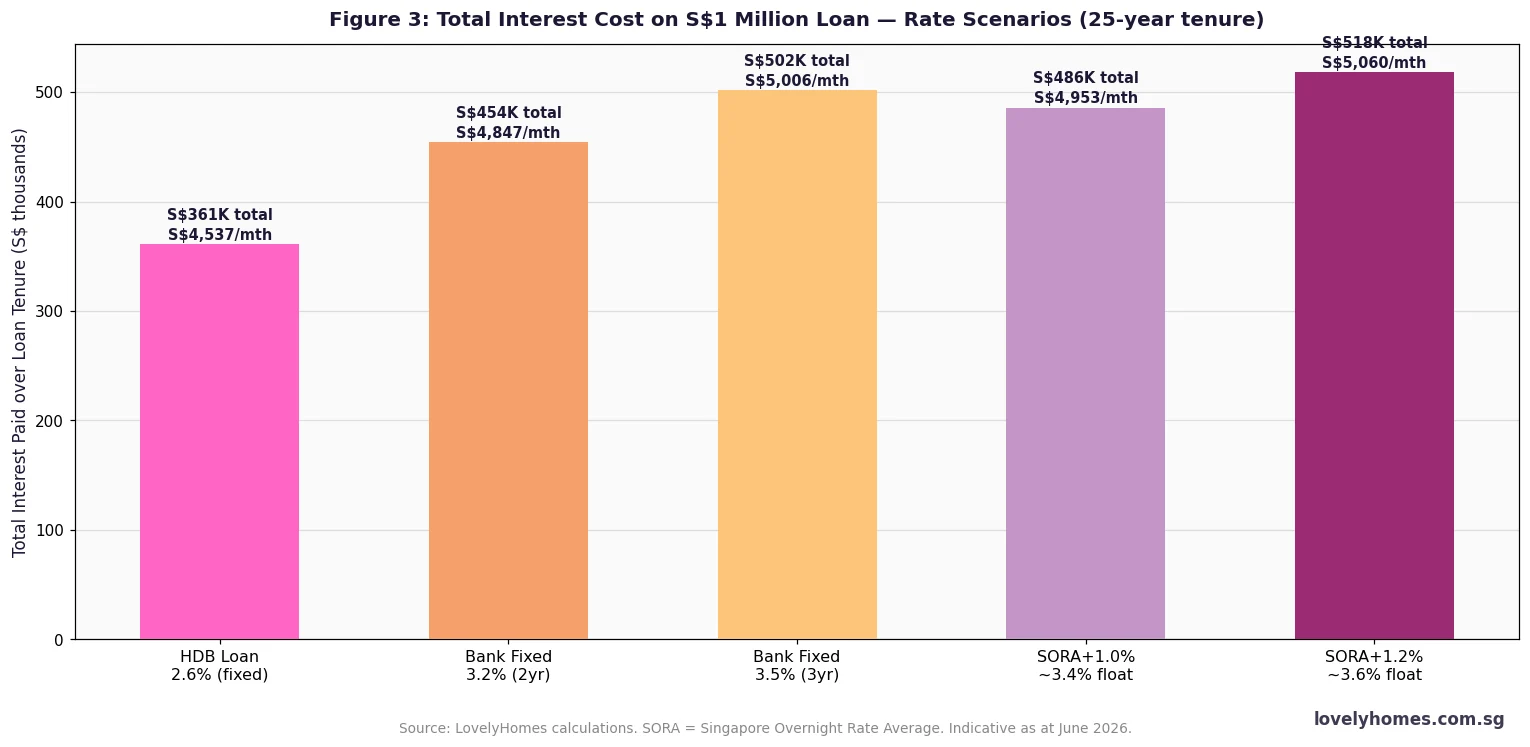

Figure 3: Total Interest Cost on S$1 Million Loan (25-year tenure) by Rate Scenario. Source: LovelyHomes calculations, indicative June 2026.

The chart shows the cost differential starkly. The HDB loan at 2.6% costs approximately S$377,000 in total interest over 25 years on a S$1 million loan. A bank fixed rate at 3.5% costs S$462,000 — a S$85,000 difference. For buyers of private property or ECs using bank financing, the choice between fixed and floating hinges on your rate outlook and risk tolerance.

CPF and Home Loan Financing

Most Singapore buyers use their CPF Ordinary Account (OA) to service instalments and fund the downpayment. The rules are set by the Central Provident Fund Board under the CPF Act (Cap 36). The key constraints are the Valuation Limit (VL) — the lower of price or valuation — and the Withdrawal Limit (WL), which is 120% of the VL. CPF OA can be used freely up to the VL; above the VL up to the WL only if you have set aside the Basic Retirement Sum (S$106,500 in 2026) in your CPF accounts.

A critical point: when you sell the property, you must refund to CPF the total principal withdrawn plus accrued interest at 2.5% p.a. This is not a penalty — it restores your retirement savings — but it reduces net cash proceeds from sale. See our CPF Property Withdrawal Limits 2026 guide for detail.

Summary Table — Singapore Home Loan Framework 2026

Parameter

HDB Concessionary Loan

Bank Loan (HDB/EC)

Bank Loan (Private)

Rate (Jun 2026)

2.6% p.a. fixed

~3.0–3.7% p.a.

~3.0–3.7% p.a.

Loan-to-Value

80%

75%

75%

MSR Cap

≤ 30%

≤ 30%

N/A

TDSR Cap

≤ 55%

≤ 55%

≤ 55%

Max Tenure

25 years (age 65)

30 years (age 65)

30 years (age 65)

Min Cash Down

5% of price

5% of price

5% of price

Lock-in / Clawback

None

1–3 yr clawback

1–3 yr clawback

Property Types

HDB flats only

HDB + EC

All types

Worked Example — Mr & Mrs Wong Buying Bishan 4-Room HDB Resale

Mr & Mrs Wong are a Singapore Citizen couple. Joint gross income: S$9,500 per month. They plan to purchase a 4-room HDB resale flat in Bishan at S$680,000. This is their first property. They hold S$90,000 combined CPF OA. They qualify for an Enhanced Housing Grant (EHG) of S$60,000 (income S$9,001–S$10,000) and a Proximity Housing Grant (PHG) of S$30,000 (parents within 4 km). Total housing grants: S$90,000.

Purchase price: S$680,000

HDB Loan (80% LTV): S$544,000

Downpayment (20%): S$136,000 — CPF OA S$90,000 + cash S$46,000

The HDB loan is the clear choice here: the 2.6% fixed rate is materially cheaper than any bank offering in June 2026, the couple meets the S$14,000 income ceiling comfortably, and the S$90,000 grants significantly reduce the net outlay. Total cost of ownership over 25 years at 2.6%: approximately S$680,000 principal + S$200,000 interest + S$63,800 upfront costs = S$943,800 in total expenditure on a flat that, based on OCR HDB price growth of ~10% per year over the past 5 years, may be worth substantially more at resale.

Refinancing and Repricing — When and How

Repricing means switching to a new package with your existing bank; refinancing means moving to a new lender. Refinancing is generally more powerful but involves legal fees of S$1,800–S$3,500 and a valuation fee of S$200–S$500. Most banks offer cashback of S$1,800–S$2,000 to offset these costs. The optimal window to refinance is 3–6 months before your lock-in expires. Never refinance within the lock-in unless savings clearly outweigh the clawback penalty.

What to Watch in H2 2026

3M SORA has been stable at approximately 2.3–2.5% since early 2026 as global central banks paused tightening. The key variable remains the US Federal Reserve: any cut flows through to SORA within weeks. For buyers who value certainty, a 2-year fixed package now locks in June 2026 rates. For buyers expecting rates to fall over the next 12–18 months, a floating SORA package may deliver lower effective payments over the loan lifecycle. The prudent approach regardless: stress-test your affordability at a rate 1.5–2.0 percentage points above your current package rate.

Frequently Asked Questions

Can I switch from an HDB loan to a bank loan after purchasing?

Yes. You can refinance from the HDB loan to a bank loan at any time after the HDB loan is active — there is no lock-in or clawback on the HDB side. You will need a conveyancing lawyer to discharge the HDB mortgage and register the bank mortgage. Bank loans typically cover 75% LTV, so if your outstanding HDB loan balance is below 75% of the current valuation, it can be fully refinanced. Note: once you switch to a bank loan, you cannot switch back to the HDB loan.

What happens if SORA rises sharply on my floating-rate loan?

Floating-rate borrowers bear the full rate risk. A 1 percentage point rise in SORA increases the monthly instalment on a S$600,000 loan (30yr) by approximately S$300. MAS requires banks to stress-test borrowers at a floor of 3.5% or contractual rate plus 1%, whichever is higher — so your loan was approved assuming you can handle a rate rise. Budget a meaningful buffer above your starting instalment.

Can I use CPF to pay stamp duty?

BSD and ABSD must be paid in cash within 14 days of signing the OTP. After payment, you may apply for CPF reimbursement from your OA. The initial cash payment is mandatory. This is a common cash-flow surprise: on a S$680,000 HDB flat, BSD is approximately S$15,000 cash on top of the downpayment.

What is the difference between repricing and refinancing?

Repricing means switching packages with your current lender (processing fee S$0–S$800; limited to that bank’s offerings). Refinancing means moving to a new lender (legal fees S$1,800–S$3,500; access to the full market). Refinancing is generally more effective but involves more paperwork and a 1–3 month processing window. Cashbacks from new lenders typically offset legal costs.

Does my car loan or personal loan reduce how much I can borrow for a home?

Yes — under TDSR, all outstanding debt obligations count against your 55% cap. A car loan of S$1,200/month and personal loan of S$500/month on a S$10,000/month income household reduces the permissible home loan instalment to S$3,800/month (55% × S$10k − S$1,700). MAS allows a 30% haircut on variable income (bonuses, commissions) when computing TDSR.

Can a foreigner get a home loan in Singapore?

Yes — foreigners can obtain bank loans for Singapore private residential property. The HDB loan is available only to eligible Singapore Citizens and Permanent Residents buying HDB flats. Note that foreigners purchasing private residential property pay 60% ABSD as at 2026 — see our ABSD guide for the full rate table. Bank loans for foreigners follow the same LTV and TDSR framework, though some banks may apply slightly stricter income documentation requirements for non-residents.

Disclaimer: This guide is for general information only and does not constitute financial, legal, or mortgage advice. Interest rates, LTV limits, MSR, TDSR, and CPF rules are subject to change. Always verify current rates with your lender or mortgage broker, and consult a licensed financial adviser before making borrowing decisions. Official references: MAS, HDB, CPF Board, IRAS.

For most Singaporeans, purchasing a home represents the single largest financial commitment they will ever make. A typical S$500,000 home loan over 25 years will cost between S$180,000 and S$280,000 in interest alone—making the difference between an HDB concessionary loan (fixed at 2.6%) and a bank loan (pegged to SORA, pegged to 3M compounded SORA plus a bank spread) the difference between financial security and prolonged vulnerability to rate shocks. This 2026 guide walks you through both options, the figures that matter, and how to choose the right one for your circumstances.

Quick Answer

HDB Loan: 2.6% fixed for the loan’s life; rate stable; 75% max LTV; no surprises—but higher than current bank rates and you must be eligible (SC or PR, income ≤ S$14,000/month for families).

Bank Loan: Currently cheaper (1.5%–3.0% depending on fixed or floating); rate risk if SORA rises; 75% max LTV; fewer eligibility restrictions—but your monthly repayment could jump 20%+ if rates climb.

The HDB concessionary loan is Singapore’s most accessible home financing product. It is pegged to the CPF Ordinary Account (OA) interest rate plus 0.1%—a formula that has held since 1999. For 2026, the OA rate is 2.5%, making the HDB loan rate exactly 2.6% per annum, fixed for the life of the loan (or until you choose to refinance into a bank loan, at which point you cannot switch back).

HDB Loan: Eligibility

Citizenship: At least one owner must be a Singapore Citizen (SC). Permanent Residents (PRs) and foreigners cannot apply.

Income ceiling (monthly household): S$14,000 for families; S$7,000 for singles under the Young Single Scheme; S$21,000 for extended family schemes. These are hard ceilings—exceed them and you are ineligible, regardless of other factors.

Age: At least 21 at the time of the application.

Repayment by age 65: Loan tenure is 25 years maximum, or until you reach age 65, whichever is earlier.

HDB Loan: Key Terms

Term

HDB Loan

Interest Rate

2.6% p.a. (fixed; CPF OA + 0.1%)

Maximum LTV

75% (lowered from 80% on 20 Aug 2024)

Minimum Down Payment

25% (mix of cash & CPF OA; no mandatory cash minimum)

Maximum Tenure

25 years or age 65, whichever is earlier

MSR Cap

30% of gross monthly income

TDSR Cap

55% of gross monthly income

Rate Lock

Rate never increases; locked at 2.6% for life of loan

Early Repayment

No penalty; can pay down anytime using CPF or cash

Refinancing to Bank

Can refinance to bank loan (one-way; cannot switch back)

Example MSR Calculation: Your gross monthly household income is S$10,000. HDB MSR allows up to 30%, so your maximum monthly loan instalment is S$3,000. On a 2.6% 25-year loan, this translates to a maximum loan amount of roughly S$1,090,000 (before other debt).

Bank Loan: How It Works

Bank loans offer more flexibility than HDB loans but introduce interest-rate risk. Banks offer two primary structures: floating rates (pegged to SORA + spread) and fixed-rate packages (locked for 1–3 years, then typically floating). Check the current 3-month compounded SORA on the MAS domestic interest rates page. Banks typically add a spread of around 0.5%–1.0% on top. Fixed-rate packages range from 1.4% to 1.8% for 1–2-year locks.

Bank Loan: Eligibility

Citizenship: SCs, PRs, and even some foreigners can qualify (though foreigner terms are stricter, requiring higher down payments and lower LTV).

Income: No hard ceiling, but TDSR and MSR caps apply (see below).

Credit & Employment: Banks assess credit history, employment stability, and income verification.

Age: At least 21 at the time of application; typically loan must be repaid by age 60–75 (varies by bank).

Bank Loan: Key Terms

Term

Bank Loan (HDB)

Bank Loan (Condo)

Interest Rate (Floating)

3M SORA + 0.5–1.0% (current ~2.0%)

3M SORA + 0.5–1.0% (current ~2.0%)

Interest Rate (Fixed)

1.4%–1.8% for 1–2 yr lock

1.4%–1.8% for 1–2 yr lock

Maximum LTV (1st property)

75% (with 25-year tenure)

75% (with 30-year tenure)

LTV (2nd property outstanding)

45% max

45% max

Minimum Down Payment

25% (5% cash minimum; rest CPF or cash)

25% (5% cash minimum; rest CPF or cash)

Maximum Tenure

25 years (or to age 65)

30 years (or to age 65)

MSR Cap (HDB only)

30% of gross monthly income

N/A

TDSR Cap

55% of gross monthly income

55% of gross monthly income

Interest Rate Floor (TDSR calc)

3% (for calculation only)

4% (for calculation only)

Early Repayment Penalty

1.5% of outstanding balance (typically during lock-in; 2–3 yr lock-in standard)

1.5% of outstanding balance (typically during lock-in)

Rate Risk

After lock-in expires, rate floats; monthly payment can increase significantly

After lock-in expires, rate floats; monthly payment can increase significantly

Important TDSR Note: Banks use a minimum interest-rate floor when calculating whether you are eligible, even if the actual rate is lower. For HDB loans, the floor is 3%; for private property, it is 4%. So even if a bank offers you 2.0% floating, they assume 3%–4% when working out your TDSR, making the true affordability ceiling lower than the headline rate suggests.

Figure 1: The two main home-loan routes in Singapore — compared on rate, eligibility, LTV and flexibility.

Side-by-Side Comparison: HDB vs Bank Loan

Factor

HDB Loan

Bank Loan

Interest Rate Type

Fixed (pegged to CPF OA)

Fixed (1–3 years) or Floating (SORA+)

Current 2026 Rate

2.6%

1.5%–1.8% (floating); 1.4%–1.8% (2yr fixed)

Maximum LTV (1st property)

75%

75% (HDB); 75% (Condo)

Min Cash Down

0% (full 25% can be CPF)

5% cash; remainder CPF or cash

Max Tenure

25 yrs or age 65

25 yrs (HDB) / 30 yrs (Condo), or age 65

MSR / TDSR

MSR 30%; TDSR 55%

TDSR 55% (no MSR for condo)

Rate Stability

Locked forever; never increases

Floating rate risk after lock-in; monthly payment can jump 20%+

Early Repayment Penalty

None

1.5% during lock-in (typically 2–3 yrs)

Switching Flexibility

Can refinance to bank (one-way; no switch-back)

Can refinance to another bank; cannot switch to HDB

Eligibility Ceiling

Income ceiling: S$14,000/mth (families); SC required

No income ceiling; open to PRs & some foreigners

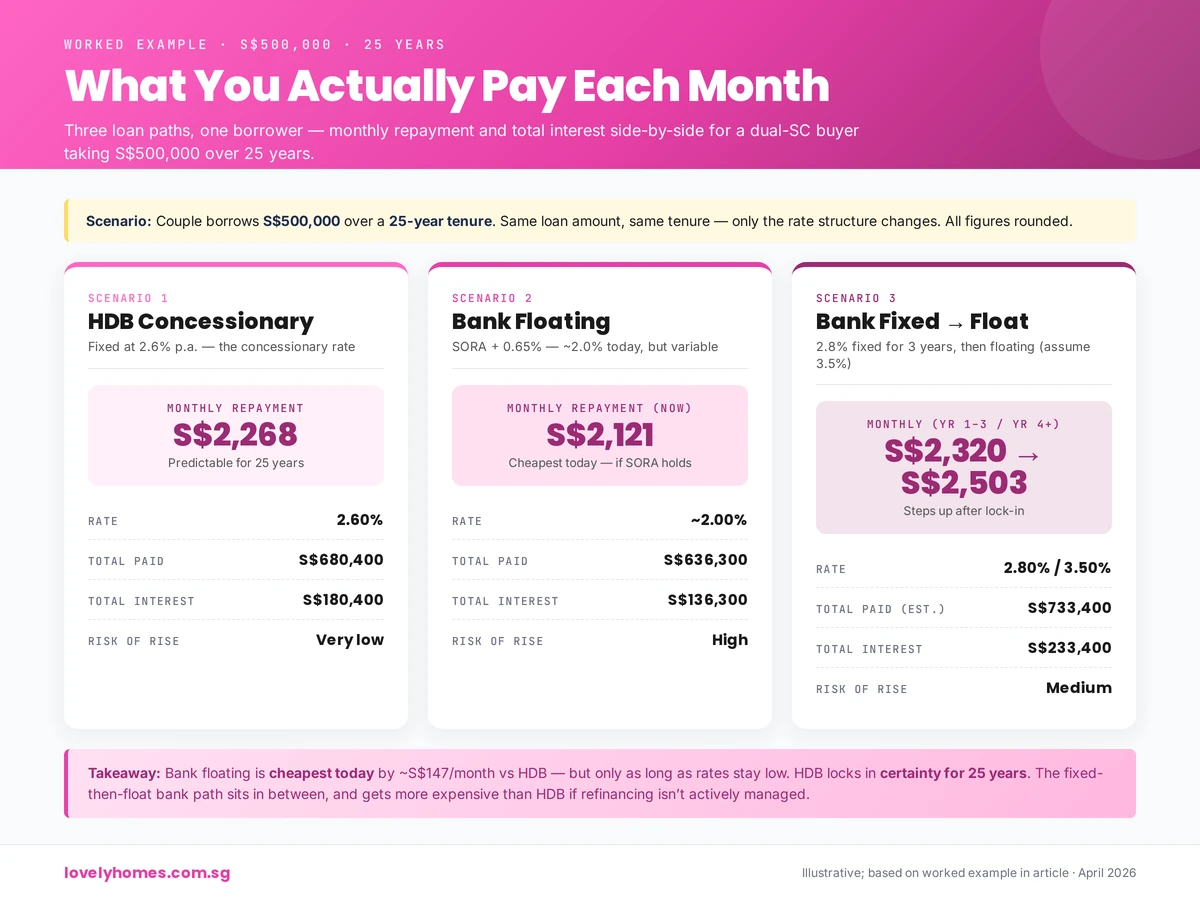

Figure 2: Three loan paths, same borrower — HDB S$2,268/mo; Bank floating S$2,121/mo; Bank fixed-to-floating S$2,320 → S$2,503/mo.

Worked Example: S$500,000 Loan, 25-Year Tenure

Let’s compare the true cost of an HDB loan versus two bank scenarios: a floating-rate loan and a fixed-then-floating loan.

Scenario 1: HDB Concessionary Loan at 2.6%

Loan Amount: S$500,000 Interest Rate: 2.6% p.a. (fixed for life) Tenure: 25 years (300 months) Monthly Instalment: S$2,269 Total Interest Paid: S$180,700 Total Amount Repaid: S$680,700

Scenario 2: Bank Floating Loan (SORA + 0.65%, Current ~2.0%)

Loan Amount: S$500,000 Interest Rate (Current): 2.0% p.a. (floating; SORA ~1.35% + 0.65% spread) Interest Rate (Assumption: Average over 25 yrs): 3.0% p.a. (to account for expected rate normalisation) Tenure: 25 years Monthly Instalment (at 2.0%): S$2,108 Monthly Instalment (at 3.0% average): S$2,372 Total Interest Paid (at 3.0% average): S$210,600 Total Amount Repaid: S$710,600 Life-of-Loan Difference vs HDB: +S$29,900 (approximately 3.5% higher total cost)

Note: The bank loan appears to save S$161/month initially, but that saving evaporates as rates normalise. Over the 25-year life, the HDB loan saves roughly S$30,000 despite starting at a higher rate.

Scenario 3: Bank Fixed (2.8%) for 3 Years, Then Floating (Assume 3.5%)

Years 1–3: 2.8% fixed

Monthly instalment: S$2,294

Years 4–25: 3.5% floating (after lock-in)

Recalculated instalment: S$2,506

Average Monthly Instalment: S$2,404 Total Interest Paid: S$221,200 Total Amount Repaid: S$721,200 Life-of-Loan Difference vs HDB: +S$40,500 Monthly Jump at Year 4: +S$212 (9% increase)

Key Insight: Even if you start with a bank loan at 2.0%–2.8%, the long-term cost edge of the HDB loan (at fixed 2.6%) becomes clear once you account for rate normalisation and the arithmetic of compound interest over 25 years. Moreover, the HDB loan offers psychological and budgetary peace of mind—your monthly repayment is guaranteed never to rise.

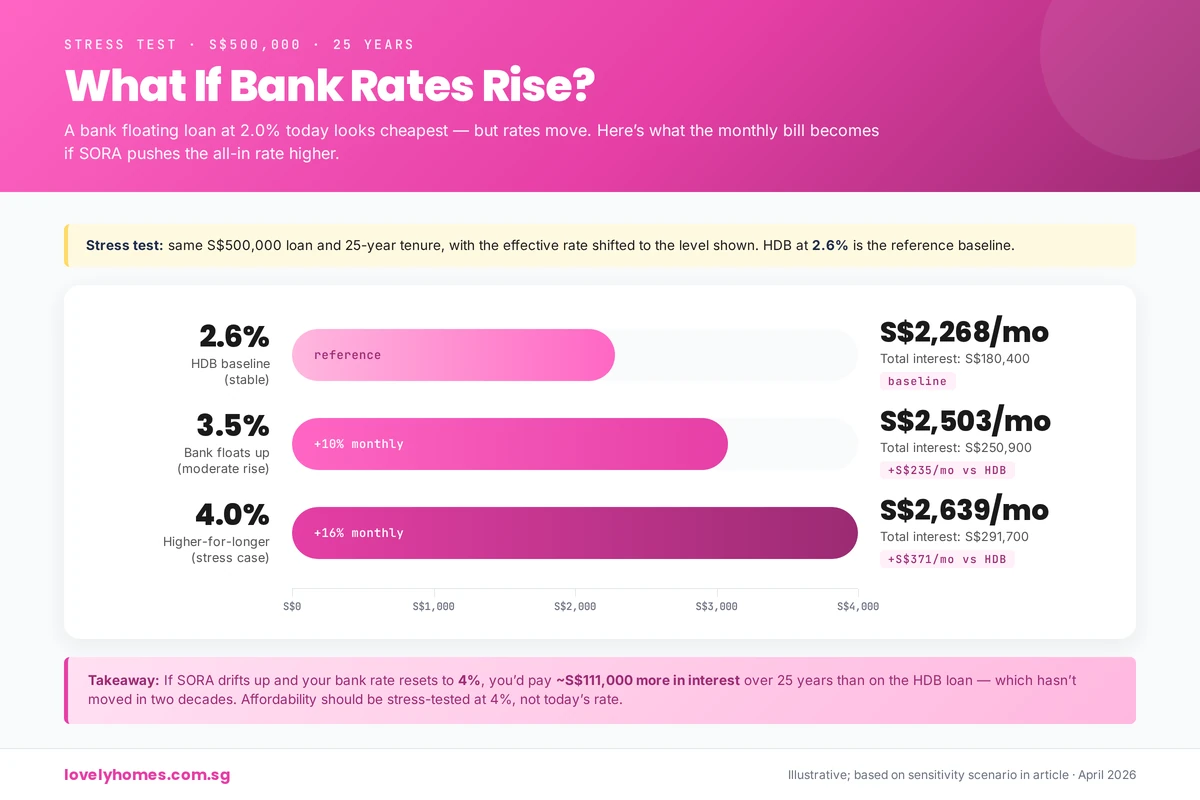

Sensitivity: What If Bank Rates Rise to 4.0%?

If 3M SORA drifts back toward 2.5% and bank spreads remain at 0.65%, a floating-rate loan would reset to approximately 3.15% base, but with TDSR floors at 4%, some borrowers would see repayments jump further. At a 4.0% effective rate:

S$500,000 loan, 25 years remaining (worst-case: rate shock in year 1): Monthly Instalment at 4.0%: S$2,639 vs HDB at 2.6%: S$2,269 Monthly Shock: +S$370 (+16.3%) Annual Impact: +S$4,440

For a household spending 30% of gross monthly income on the mortgage, a 16% rate shock could push TDSR above 55%, triggering a lender’s demand for early repayment or refinancing—a real risk during volatile rate environments.

Figure 3: Stress-tested at 2.6%, 3.5% and 4.0% — a rise to 4% adds ~S$111,000 in interest over 25 years vs the HDB baseline.

Which Should You Choose?

Choose HDB Loan If:

You are eligible (SC, income ≤ S$14,000/mth for families).

Rate stability is a priority. You plan to stay in the home for 15+ years and want zero uncertainty about future payments.

You are risk-averse or budget-conscious. Your household income is tight, and a 10%–16% payment jump would strain your finances.

You value the psychological benefit of a locked rate and a simpler loan structure.

You expect rates to rise. If SORA normalises to 2.5%+ (and spreads remain), HDB’s 2.6% becomes increasingly competitive.

Choose Bank Loan If:

You exceed HDB income ceilings (e.g. dual-income household exceeding S$14,000/mth) or are a PR/foreigner.

You are comfortable with rate risk and have sufficient financial buffers to absorb a 10%–20% payment increase.

You plan to sell or refinance within 5–10 years. Lower initial rates and longer maximum tenures (30 years for condos) offer flexibility.

You believe rates will stay low. If you expect SORA averages well below 2.6% over the life of your loan, a floating bank loan saves vs the HDB concessionary rate. If it averages above 2.6%, HDB is cheaper.

You want to refinance easily. Bank loans can be refinanced to another bank mid-term; HDB loans, once converted to a bank, cannot be converted back.

You own a condo or landed property. Bank loans offer longer tenures (30 years) and higher potential LTV; HDB loans only apply to HDB flats and ECs.

Refinancing: When and Why to Switch

The option to refinance exists at any point in your loan journey. Understanding when and why to refinance is crucial to optimising your loan cost.

HDB to Bank Refinance

If you currently hold an HDB loan at 2.6%, you can refinance to a bank loan. This is a one-way decision—once you switch to a bank, you cannot switch back. Refinancing makes sense if:

Bank rates fall significantly below 2.6% and are locked in for an extended term (5+ years).

You exceed HDB’s income ceiling due to a salary increase and want to increase your loan amount.

You are refinancing to raise cash (e.g. home equity release) against your property.

Give HDB three months’ written notice of your intention to refinance. HDB will calculate the outstanding balance and any adjustment due to CPF contributions.

Bank to Bank Refinance (or HDB → Bank)

If you hold a bank loan, you can refinance to another bank or (once) to HDB, depending on your eligibility. Refinancing makes sense if:

Your current fixed-rate lock-in is about to expire and rates have fallen; refinance before the jump.

Another bank offers 0.3%–0.5% lower rates or a longer fixed-rate tenure.

You want to consolidate multiple loans or restructure your debt.

Typical lock-in periods: 2–3 years. Early repayment within the lock-in incurs a 1.5% penalty on the outstanding balance. After lock-in, partial or full repayments are fee-free.

Lock-In Mechanics

Most bank home loans come with a lock-in clause that penalises early repayment during the initial fixed-rate period. The lock-in typically lasts 2–3 years. Here’s what you need to know:

Lock-in Period: Typically 2–3 years from the date of drawdown.

Early Repayment Penalty: 1.5% of the outstanding loan balance if you repay (or refinance) before lock-in expires.

After Lock-In: You can repay in full or in part without penalty. You can refinance to another bank.

Fixed-Rate Lock vs Lock-In: Do not confuse the fixed-rate period (e.g. 2.8% for 2 years) with the lock-in period. A 2-year fixed rate typically comes with a 2–3-year lock-in penalty clause.

Frequently Asked Questions

1. Can I switch from HDB to bank and back?

No. Refinancing from HDB to bank is one-way. Once you switch to a bank loan, you cannot return to HDB financing. Choose carefully before making the switch. If you are considering it, ensure bank rates are significantly lower and locked in for at least 5 years to justify the irreversibility.

2. What happens if I miss an HDB or bank loan payment?

Missing a payment triggers late fees and can damage your credit score, making future refinancing more expensive. For HDB loans, persistent defaults can lead to legal action and, in extreme cases, repossession of the flat. For bank loans, the consequences are similar. Both lenders are empowered to initiate enforcement proceedings if you default for more than three months. Contact your lender immediately if you foresee difficulties; many offer restructuring or deferment options for borrowers facing temporary hardship.

3. Can I use CPF to pay my mortgage?

Yes. You can use CPF Ordinary Account (OA) funds to pay both HDB and bank home loan monthly instalments, subject to:

Your CPF OA balance must be sufficient to cover the instalment.

CPF will automatically deduct the monthly instalment from your OA if you have set up standing instructions.

If your CPF OA is insufficient, you must pay the balance in cash.

You cannot use your CPF Medisave Account (MA) or Special Account (SA) for loan repayment.

After loan maturity, CPF regulations allow you to retain a minimum sum in your Retirement Account (RA) for healthcare and longevity protection; excess funds can be withdrawn.

4. What is SORA, and why does it matter?

SORA stands for Singapore Overnight Rate Average. It is the interest rate at which banks lend to each other overnight in the Singapore money market, published daily by the Monetary Authority of Singapore (MAS). Most bank home loans in Singapore are now pegged to 3-Month Compounded SORA (reviewed quarterly) rather than the older SIBOR benchmark.

Why it matters: Your bank loan interest rate is typically SORA + a bank spread (e.g. 0.65%). As SORA fluctuates, your loan rate (and monthly payment) fluctuates. Historically 3M SORA has moved widely — from well under 1% in 2020–2021, rising above 3% through 2023–2024, and moderating thereafter. Always check the latest rate on the MAS website before committing to a package. Understanding SORA trends helps you forecast your likely repayment path.

5. How does the interest-rate floor affect my loan amount?

When calculating whether you qualify for a loan (TDSR test), banks assume a minimum interest rate, even if the offered rate is lower. For HDB loans, the floor is 3%; for private property, it is 4%. This means:

If a bank offers you 2.0% floating but applies a 4% floor for TDSR calculation, you are approved based on 4% affordability, not 2%.

If your income is S$10,000/month and TDSR is 55%, your maximum total debt repayment is S$5,500/month.

At a 4% rate (the TDSR floor), a S$500,000 loan over 25 years costs ~S$2,639/month.

Even though the actual rate might be 2.0%, the lender approves you at 4% to protect against future rate rises.

This floor is a safeguard for lenders and borrowers alike, preventing over-leverage in a low-rate environment.

6. Can I take a joint loan with a family member?

Yes. Both HDB and bank loans can be taken jointly (e.g. spouse, parent, or adult child). Joint applicants must:

Both be on the property title (either as joint tenants or tenants-in-common).

Both pass the eligibility checks (citizenship, age, credit, income).

Both be liable for the loan; if one co-borrower defaults, the lender can pursue either or both.

Agree on the split of ownership (50:50 is common; other splits are possible but more complex for tax and CPF purposes).

Joint borrowing increases the combined household income for TDSR/MSR purposes, often allowing a larger loan. However, both parties remain responsible if the other defaults.

7. Is a fixed or floating rate better?

There is no universally correct answer; it depends on your risk appetite and rate outlook.

Fixed Rate (1–3 years): Choose if you want certainty and believe rates will rise. Lock-in at the lowest rate available (currently 1.4%–1.8% for 1–2 years). After lock-in expires, you will refinance or face a floating rate, so you are not truly “locked” for 25 years.

Floating (SORA+): Choose if you believe rates will stay low and you can afford a 20%–30% payment increase. Currently, floating rates are lower than fixed (around 1.5%–2.0% all-in vs 1.4%–1.8% fixed), so you pay a rate-stability premium if you lock in.

In 2026, most experts recommend a 2-year fixed rate as a compromise: you get near-current rates locked in for two years, and then you can reassess when the lock-in expires.

Summary: Making Your Decision

Choosing between an HDB loan and a bank loan is ultimately a question of values: stability vs savings, predictability vs flexibility. The HDB loan offers peace of mind and long-term cost protection but requires eligibility. The bank loan offers potential short-term savings and flexibility but introduces rate risk. Work through the decision tree below to clarify your path:

Start here: Are you a Singapore Citizen with household income ≤ S$14,000/month (families)?

Yes: You can access the HDB loan. Proceed to the next question.

No: You must use a bank loan. Skip to bank-loan considerations below.

Next: Is rate stability your top priority, or are you comfortable with rate risk?

Rate stability: Choose HDB. You cannot beat a fixed 2.6% rate that will not rise for 25 years.

Comfortable with risk: Compare HDB (2.6%) with current bank rates (floating 1.5%–2.0%; fixed 1.4%–1.8%). If bank rates are <2.2% and locked in for 5+ years, bank may be worthwhile. If rates are expected to rise to 3%+, HDB’s 2.6% becomes increasingly attractive.

For bank-loan applicants: What is your holding timeline?

Short term (5–10 years): Floating or short fixed-rate packages (1–2 years) are fine; refinance or sell before rate shock.

Long term (15+ years): Lock in a fixed rate (2.8%–3.0%) for as long as possible (5+ years if available). The certainty is worth 0.3%–0.5% in extra rate cost.

Key Takeaways

HDB loans are fixed at 2.6% (pegged to CPF OA + 0.1%). This rate will not increase for the life of the loan—a powerful advantage in a rising-rate environment.

Bank loans are currently cheaper (1.5%–2.0% floating; 1.4%–1.8% fixed for 1–2 years) but introduce rate risk. After lock-in expires (typically 2–3 years), your payment can jump 10%–30%.

Over a 25-year life, an HDB loan typically costs S$30,000–S$40,000 less than a bank loan that averages 3.0% over the tenor, even though it starts at a higher rate.

Eligibility is the first gatekeeper. If you are a SC with income ≤ S$14,000/month, HDB is an option; otherwise, you must use a bank.

Refinancing is possible but irreversible. HDB → bank is one-way; bank → bank is flexible. Plan before you switch.

Rate floors and TDSR caps mean that your true affordability is often lower than headline rates suggest. Always ask your lender what rate floor they use in their TDSR calculation.

In 2026, the optimal strategy for most Singaporeans is: (1) if HDB-eligible, take the HDB loan unless bank rates are locked below 2.2% for 5+ years; (2) if bank-eligible only, lock in a 2-year fixed rate at 1.4%–1.8% as a bridge, then reassess when lock-in expires.

This guide is for general information only and does not constitute legal, tax, or financial advice. Interest rates, LTV limits, MSR/TDSR caps, and eligibility rules change frequently. Always verify current figures with HDB (hdb.gov.sg), MAS (mas.gov.sg), and your bank before committing to a loan package. For complex situations—mixed-nationality couples, self-employed income, or refinancing decisions—consult a licensed mortgage advisor or conveyancing lawyer. CPF rules, tax treatment, and grant eligibility have edge cases; always verify your specific situation with the relevant authority.