HDB Loan vs Bank Loan Singapore 2026: Rates, LTV, Eligibility and Which Saves You More

📌 Quick Answer: HDB Loan vs Bank Loan Singapore 2026

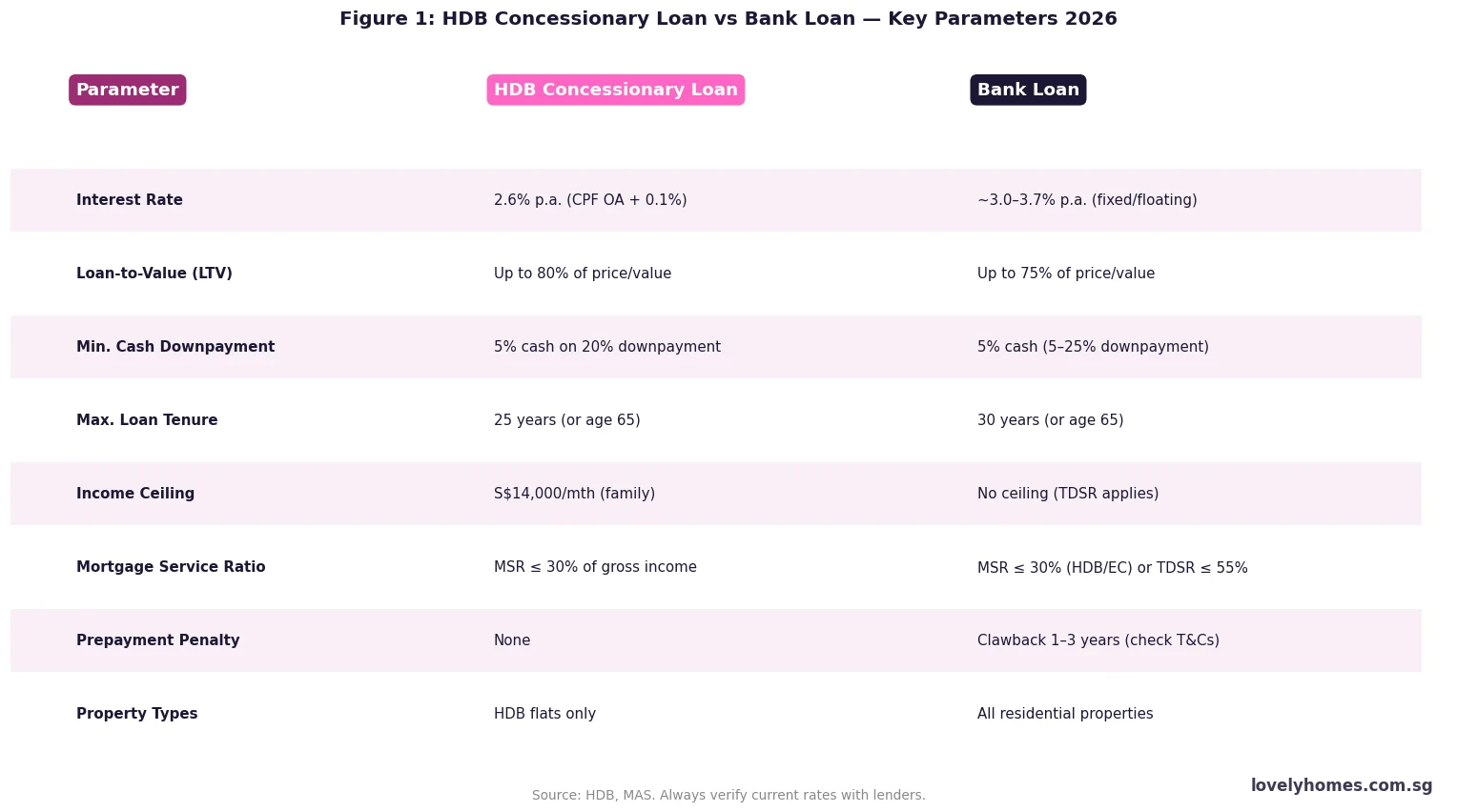

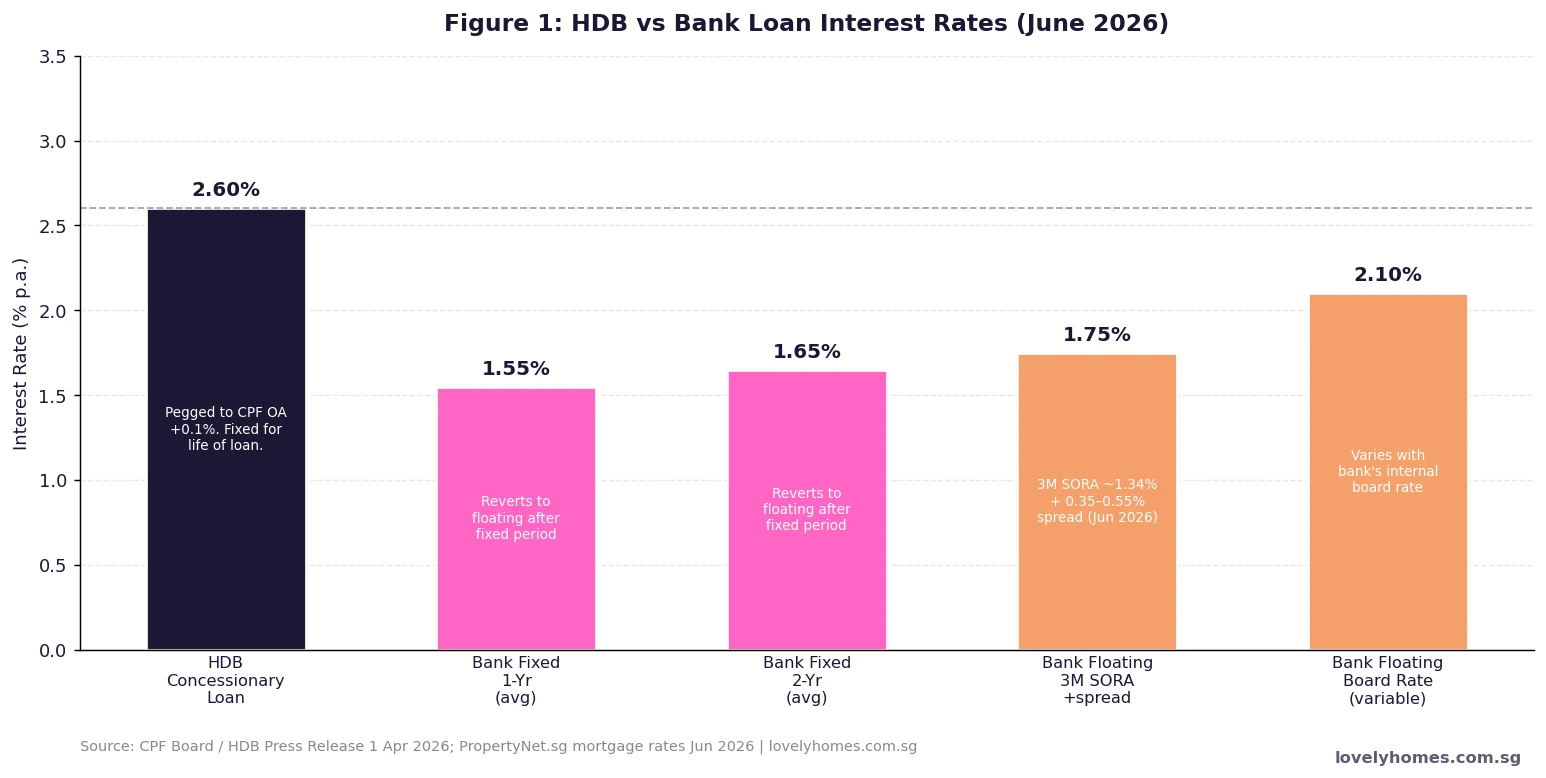

- HDB loan rate: 2.60% p.a. (fixed at CPF OA rate + 0.1% = 2.5% + 0.1%), unchanged from January to June 2026. Bank fixed rates are lower at 1.35%–1.65% for 1-year and 1.55%–1.80% for 2-year packages as at June 2026.

- LTV is now the same: Both HDB loans and bank loans offer up to 75% LTV for HDB flats following the August 2024 policy change (previously 80% for HDB loans). The minimum downpayment is 25% for both.

- Key difference — cash downpayment: With an HDB loan, the entire 25% downpayment can be paid from your CPF OA. With a bank loan, you must pay at least 5% in cash, with the remaining 20% from CPF OA.

- One-way door: You can switch from an HDB loan to a bank loan at any time. But once you are on a bank loan, you cannot switch back to the HDB concessionary loan.

- HDB loan eligibility: Subject to an income ceiling of S$14,000/mth (families) or S$7,000/mth (singles). Bank loans have no income ceiling but apply standard TDSR/MSR rules.

- Rate risk: The HDB rate is stable and rarely changes. Bank fixed rates revert to floating (SORA-based) after the fixed period — typically 1–3 years — meaning repayments can rise if SORA increases.

- Bottom line: Bank loans save on interest but require cash downpayment and carry rate risk. HDB loans offer stability and zero-cash downpayment but cost more in interest over the long run.

Every HDB flat buyer in Singapore must make one of the most consequential financing decisions of their lives: take the Housing & Development Board’s own concessionary loan, or borrow from a bank. The choice affects how much cash you need upfront, what you pay monthly for up to 25 years, and how exposed you are to interest rate fluctuations.

This guide explains both options in full — rates, LTV, eligibility, cashflow impact, and the one-way door rule — so you can make a fully informed decision before exercising your HDB Flat Eligibility (HFE) letter or signing a bank Letter of Offer. It also covers the role of the Mortgage Servicing Ratio (MSR) and Total Debt Servicing Ratio (TDSR), which govern how much either type of lender can lend you.

Interest Rates: HDB Loan vs Bank Loan (June 2026)

The interest rate difference is the single most scrutinised comparison between the two options. As at June 2026, the data is as follows.

The HDB Concessionary Rate

The HDB concessionary interest rate is pegged at 0.1% above the prevailing CPF Ordinary Account (OA) interest rate. The CPF OA rate has been at its floor of 2.5% p.a. continuously since 2009, making the HDB loan rate 2.60% p.a. The CPF Board reviews OA rates quarterly (in January, April, July, and October). The HDB and CPF Board confirmed on 29 March 2026 that the rate remains unchanged at 2.60% for the April–June 2026 quarter.

The HDB rate is therefore effectively fixed for most borrowers’ planning purposes — it has not changed in over 15 years. However, it is technically variable, and a CPF OA rate increase (which requires the prevailing 3-month average yields of 10-year SGS bonds and similar benchmarks to exceed 2.5%) would flow through to HDB loan repayments.

Bank Loan Rates (June 2026)

Bank loan rates in Singapore come in two main varieties: fixed-rate packages (where the rate is locked for 1–3 years, then reverts to a floating rate) and floating-rate packages (pegged to 3-month SORA or the bank’s internal board rate). As at June 2026, the range observed in the market is as follows. For fixed 1-year packages, rates range from approximately 1.35% to 1.65% p.a. For fixed 2-year packages, rates range from approximately 1.55% to 1.80% p.a. Floating SORA-based packages price at 3-month SORA (~1.34%) plus a spread of 0.35%–0.55%, resulting in effective rates of approximately 1.70%–1.90% p.a.

The critical caveat for bank fixed rates is that after the initial fixed period expires, the loan typically reverts to a floating rate — either SORA-based or the bank’s board rate — which is currently around 2.0%–2.5% p.a. Borrowers who take a 1-year fixed package at 1.45% should budget for a step-up to a floating rate when the fixed period ends, unless they refinance to another fixed package (which typically incurs legal and valuation fees of S$2,000–S$3,500).

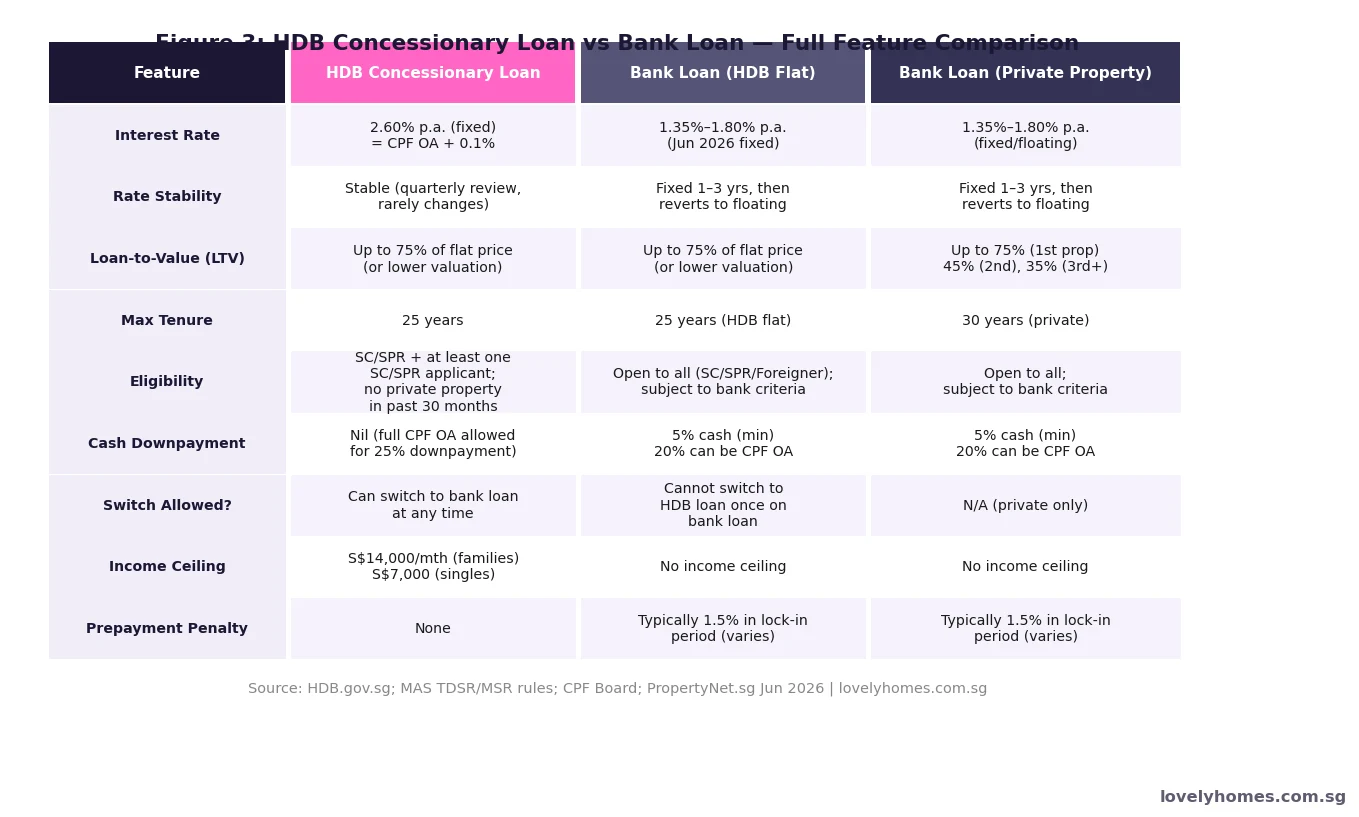

Loan-to-Value and Downpayment Requirements

One of the most important practical differences between the two loan types is the cash component of the downpayment. Since August 2024, both HDB loans and bank loans have the same LTV cap of 75% for HDB flats. However, the source of the downpayment differs significantly.

| Item | HDB Concessionary Loan | Bank Loan (HDB flat) |

|---|---|---|

| Loan-to-Value (LTV) | Up to 75% | Up to 75% |

| Minimum downpayment | 25% of purchase price | 25% of purchase price |

| Minimum cash downpayment | Nil (full CPF OA allowed) | 5% cash required |

| Balance of downpayment | 25% from CPF OA | 20% from CPF OA |

| Max tenure (HDB flat) | 25 years | 25 years |

| Max tenure (private) | N/A | 30 years |

For a flat priced at S$500,000, the HDB loan borrower can fund the entire S$125,000 downpayment from CPF OA savings — requiring zero cash at exercise. The bank loan borrower must bring S$25,000 in cash (5%), with the remaining S$100,000 from CPF OA. For first-time buyers with limited liquid savings but substantial CPF OA balances, this distinction can be decisive.

Monthly Repayment Comparison

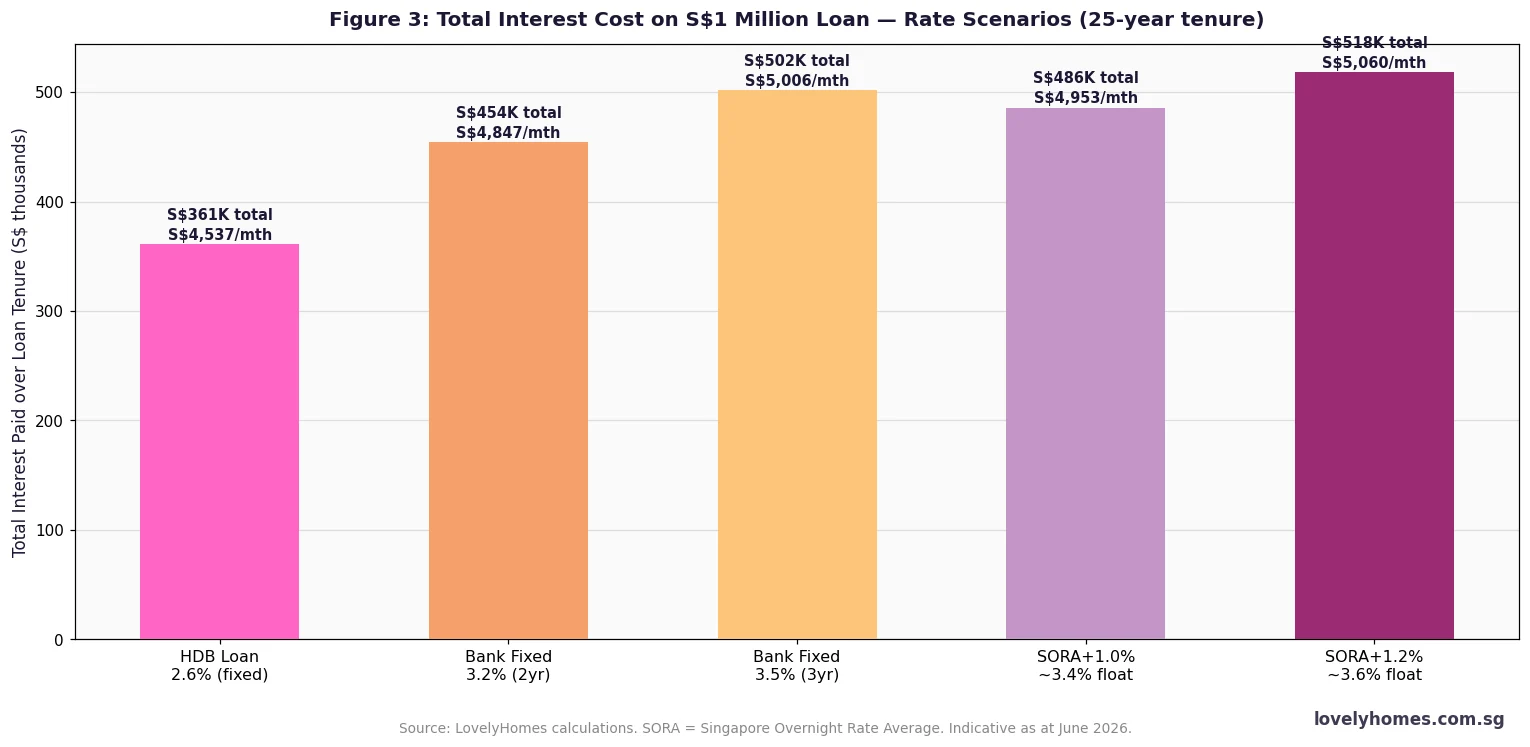

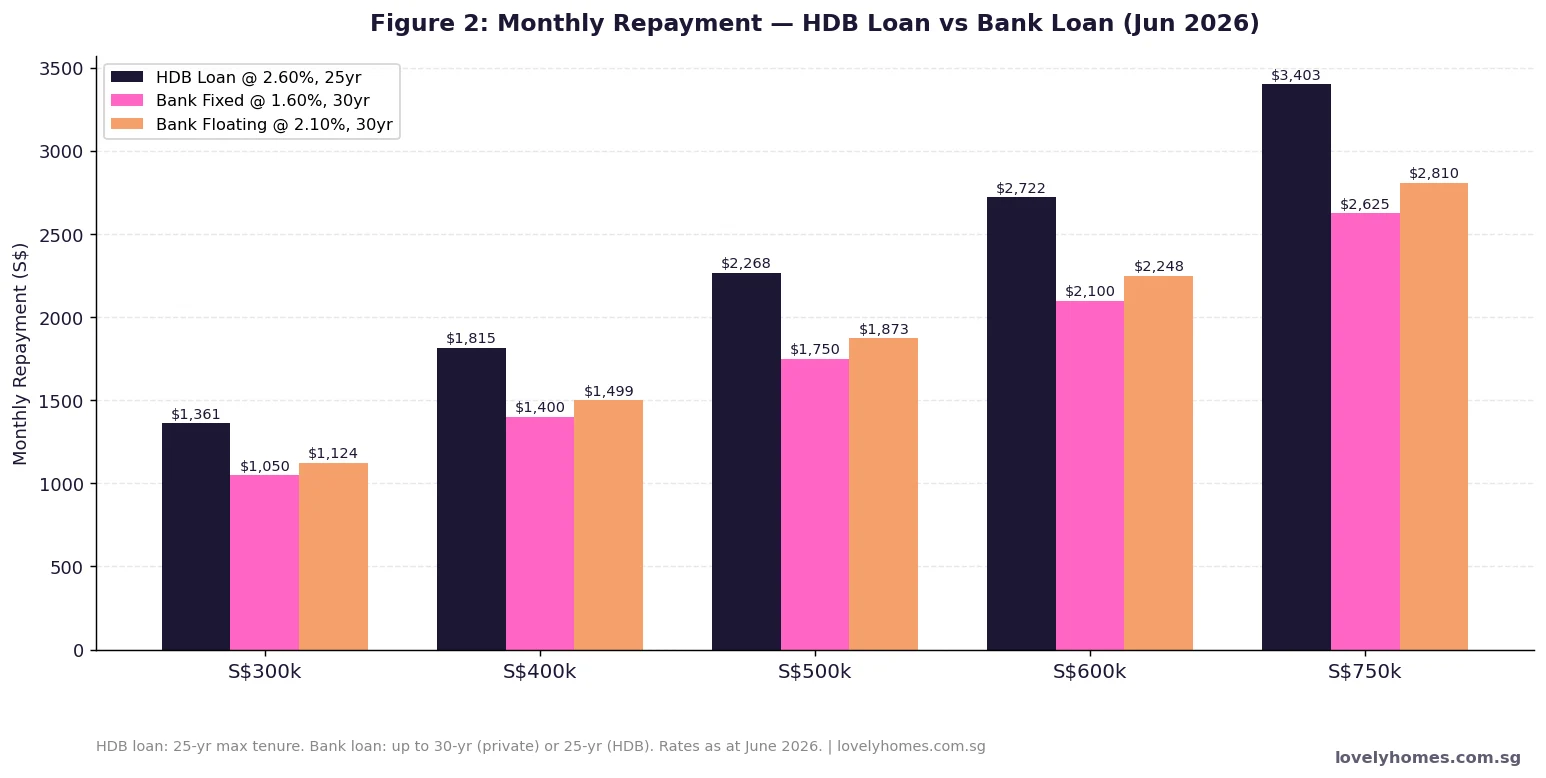

Despite the higher HDB rate, the impact on monthly repayments is less dramatic than many buyers expect, because the HDB loan uses a shorter maximum tenure of 25 years while bank loans for HDB flats are also capped at 25 years.

At a S$500,000 loan, the HDB borrower at 2.60% over 25 years pays approximately S$2,260/mth. The bank borrower at 1.60% over 25 years pays approximately S$2,020/mth — a saving of S$240/mth, or S$2,880/year. Over the full 25-year tenure, this compounds to a total interest saving of approximately S$34,000–S$40,000. However, if the bank rate reverts to 2.50% floating after the initial fixed period, the saving shrinks substantially. The total interest difference over 25 years narrows to S$5,000–S$12,000 depending on the rate path taken by SORA.

Eligibility: Who Can Take an HDB Loan?

Not all buyers can choose between the two options — the HDB concessionary loan has eligibility criteria that bank loans do not.

To qualify for an HDB loan in 2026, the borrower must meet the following requirements. The household gross monthly income must not exceed S$14,000 for families (including couples), or S$7,000 for singles applying under the Single Singapore Citizen or Joint Singles Scheme. At least one borrower must be a Singapore Citizen. The co-borrower (if any) must be a Singapore Citizen or Permanent Resident. The borrower must not have disposed of any private residential property in the 30 months immediately before the flat application — the HDB loan is intended for buyers who are in genuine need of public housing finance, not for investors cycling between private property and HDB. The flat being purchased must be an HDB flat (resale or BTO); HDB loans are not available for private condominium purchases.

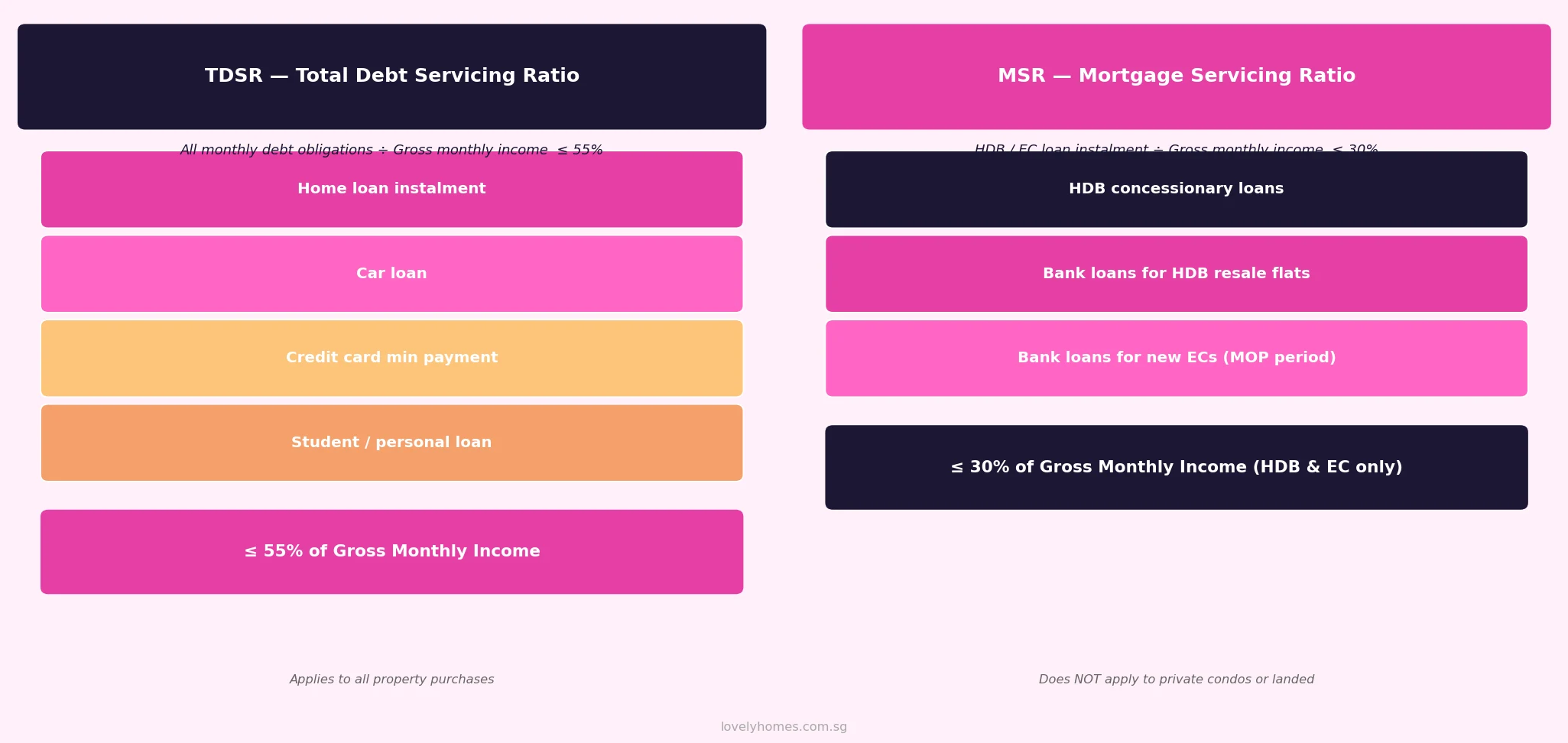

Bank loans have none of these eligibility restrictions — they are open to Singapore Citizens, SPRs, foreigners, companies, and buyers of any income level. The governing constraints for bank loans are the Mortgage Servicing Ratio (MSR) — capped at 30% of gross monthly income for HDB flat purchases — and the Total Debt Servicing Ratio (TDSR) — capped at 55% of gross monthly income for all property purchases.

Full Feature Comparison Table

The One-Way Door Rule

Perhaps the most important strategic consideration is the one-way door: you can switch from an HDB loan to a bank loan at any time, but you cannot switch from a bank loan back to an HDB loan.

This asymmetry has significant implications. Buyers who start on an HDB loan preserve optionality — if bank rates fall materially (as they did in 2021–2023 and again in 2025–2026 as the SORA rate cycle eased), they can refinance to a bank loan at the more favourable rate. Buyers who start on a bank loan, by contrast, are permanently locked out of the HDB concessionary rate. This means that if bank rates were to rise significantly (as they did in 2022–2023 when 3M SORA peaked above 3.8%), a bank loan borrower who refinanced cannot fall back to the HDB rate as a safety net.

Given that bank rates are currently at or near their cyclical lows as at June 2026, the relative attractiveness of a bank loan is greatest at present. But starting on a bank loan is an irreversible choice — buyers with lower risk tolerance or less financial flexibility may prefer to start on the HDB loan and refinance later if rates remain favourable.

Worked Example: S$550,000 Resale 4-Room HDB

Mr and Mrs Goh are SC joint buyers, gross household income S$9,000/mth. They are purchasing a resale 4-room HDB flat in Bedok for S$550,000. They have CPF OA savings totalling S$130,000 between them and liquid cash savings of S$80,000.

Option A — HDB Concessionary Loan:

Loan amount (75% LTV): S$412,500

Downpayment: S$137,500 (all from CPF OA — no cash required)

Monthly repayment @ 2.60%, 25yr: S$1,862/mth

MSR check: S$1,862 / S$9,000 = 20.7% ✅ (under 30% cap)

Cash preserved: S$80,000

Total interest over 25yr: ~S$148,500

Option B — Bank Loan (1.60% fixed 2-yr, then SORA ~2.10% thereafter):

Loan amount (75% LTV): S$412,500

Downpayment: S$137,500 (5% cash = S$27,500 + CPF OA S$110,000)

Monthly repayment @ 1.60%, 25yr: S$1,675/mth (fixed period)

Monthly repayment after fixed period @ 2.10%: S$1,784/mth (illustrative)

MSR check: S$1,784 / S$9,000 = 19.8% ✅

Cash required upfront: S$27,500 (leaves S$52,500 liquid)

Total interest over 25yr (blended at ~2.10%): ~S$132,000 — saving ~S$16,500 vs HDB loan over full tenure

Decision: The bank loan saves approximately S$16,500 in total interest over 25 years (assuming the blended rate stays around 2.10%). However, the Gohs must commit S$27,500 in cash now, reducing their emergency fund. Given their stable employment and comfortable MSR headroom, they might reasonably prefer the bank loan. If either spouse expected a career break or job change, the HDB loan’s nil-cash requirement and rate stability would be more prudent. The right answer depends on cashflow resilience, not just rate arithmetic.

MSR and TDSR: The Regulatory Caps That Govern Both

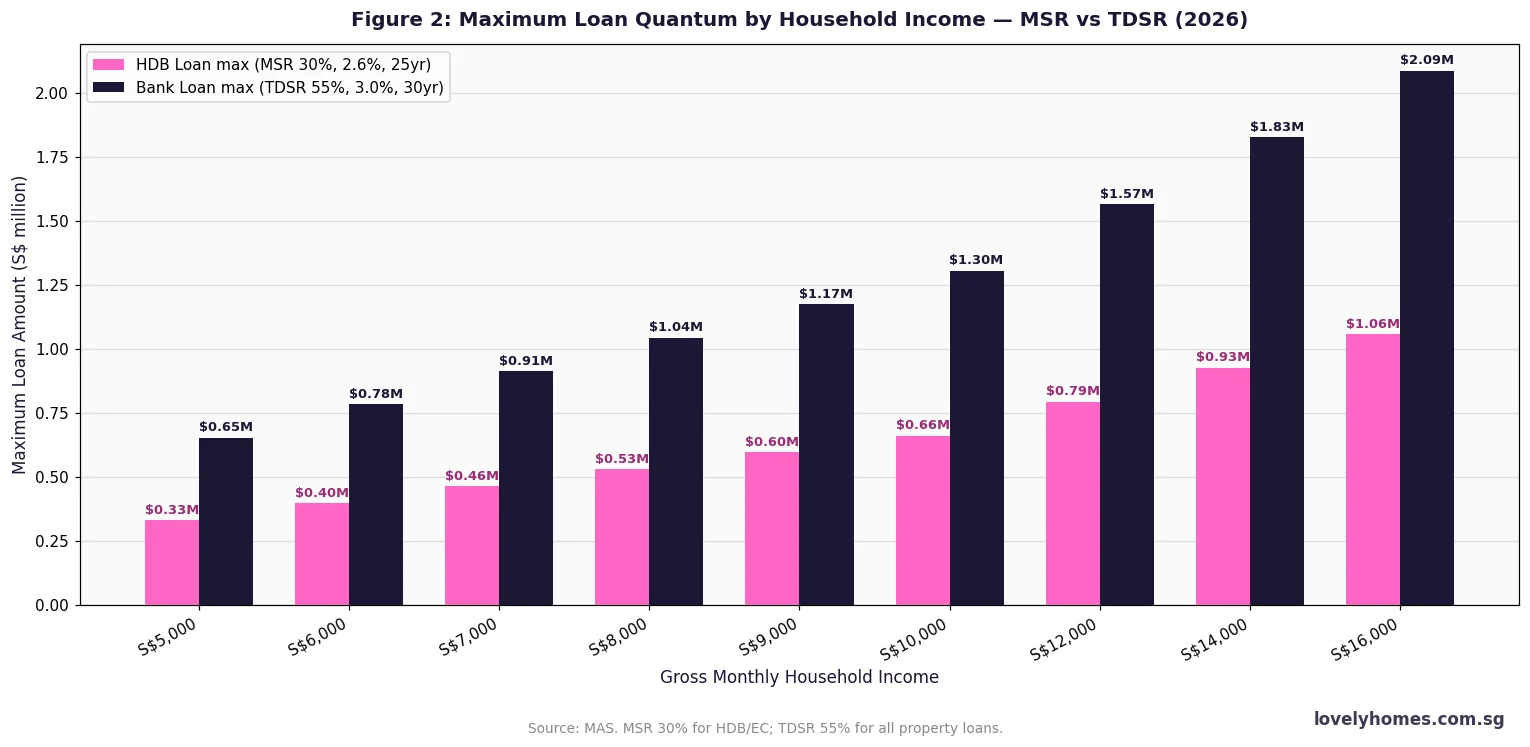

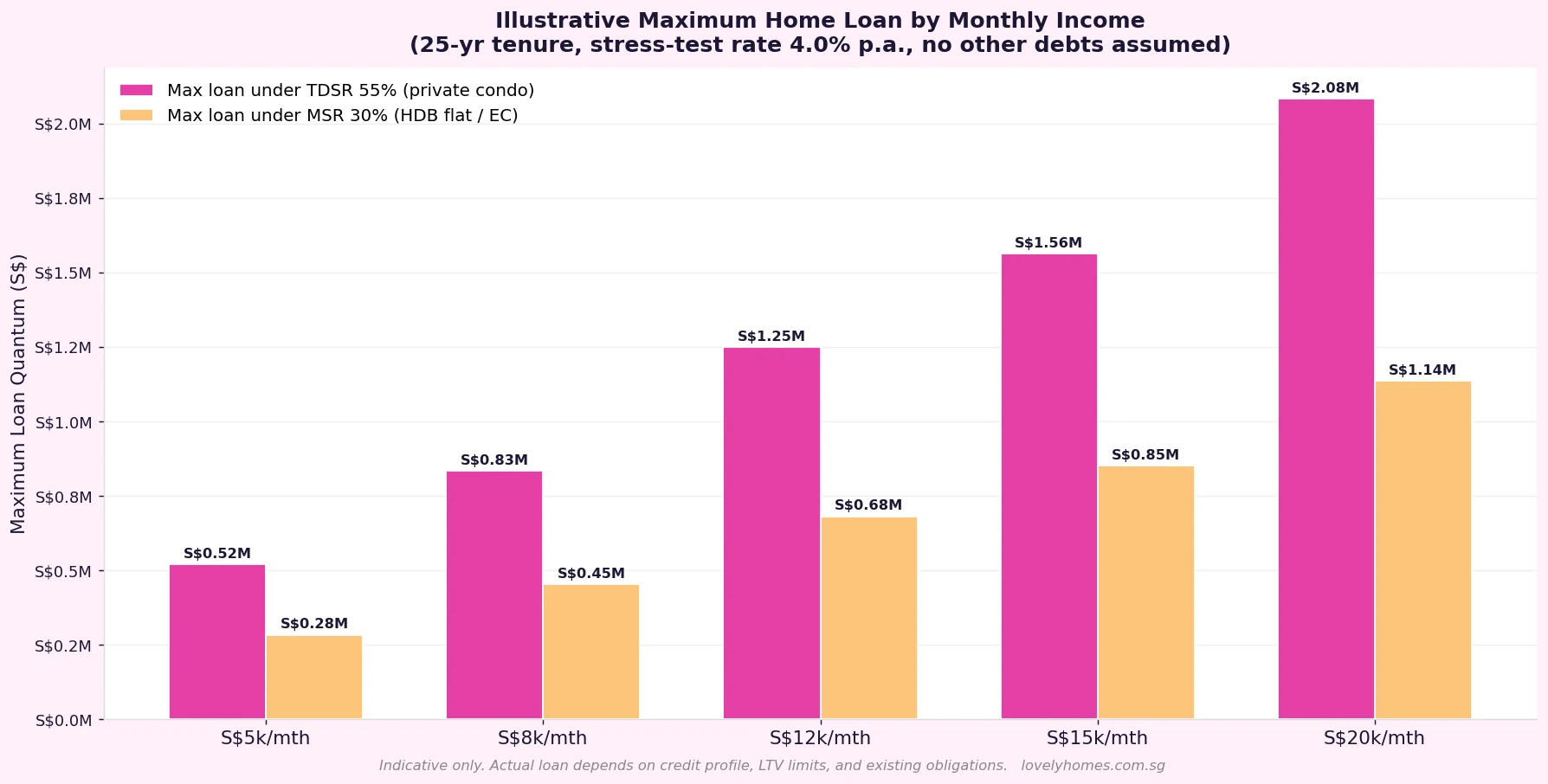

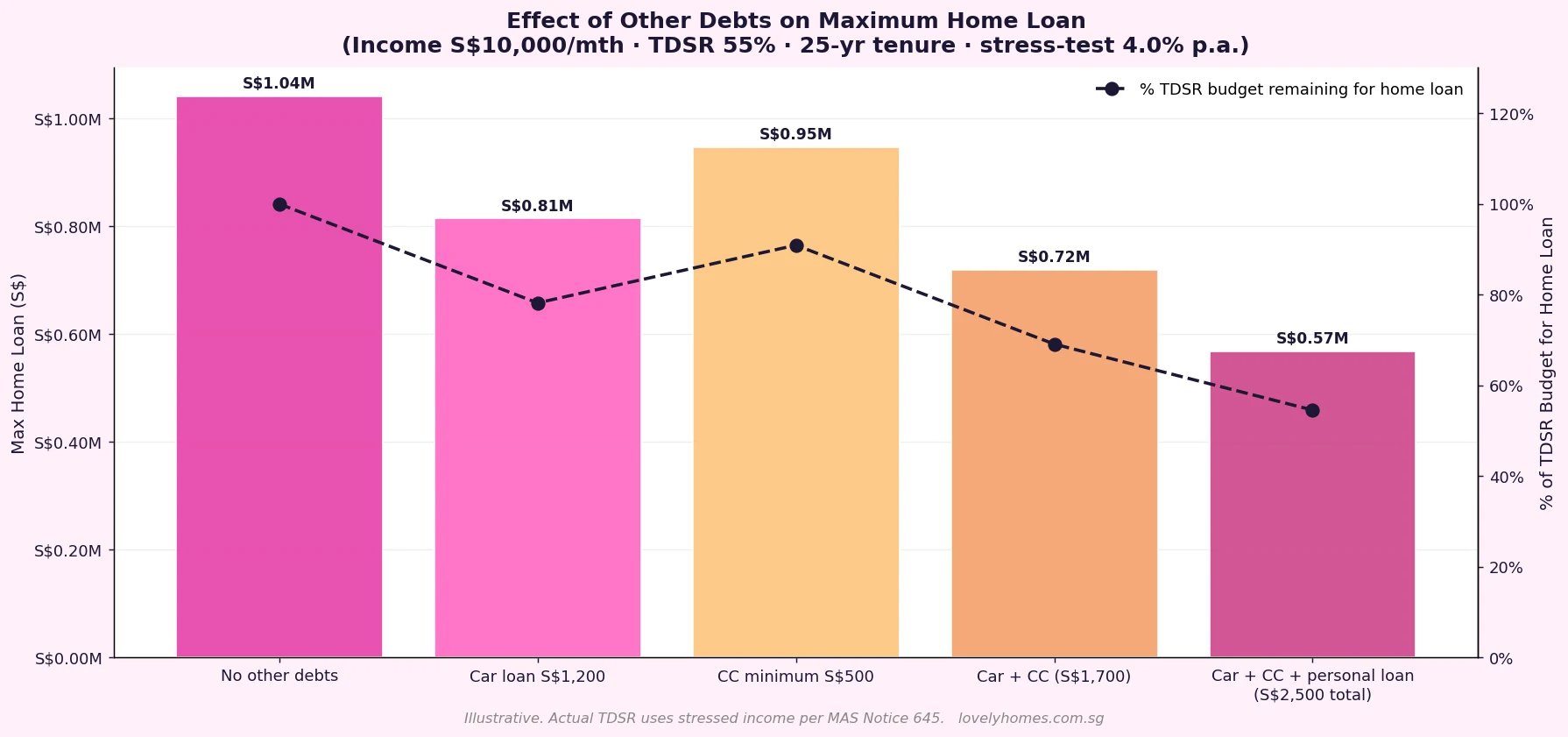

Regardless of whether you take an HDB or bank loan, your maximum loan quantum is limited by the Monetary Authority of Singapore’s (MAS) borrower stress-test rules. For HDB flat purchases, the MSR caps your monthly property loan repayments at 30% of gross monthly income. The TDSR caps total monthly debt repayments (including car loans, personal loans, credit card minimum payments, and all property loans) at 55% of gross monthly income.

Practically speaking, the MSR is the binding constraint for most HDB buyers. A couple earning S$8,000/mth can service a maximum monthly repayment of S$2,400 (30% MSR). At 2.60% over 25 years, this translates to a maximum loan of approximately S$510,000. At 1.60% over 25 years, the maximum loan is approximately S$572,000 — about 12% higher. The higher loan quantum available under a bank loan can sometimes allow a buyer to afford a higher-value flat.

Why This Matters: The Rate Cycle Context

As at June 2026, Singapore’s 3-month SORA has eased to approximately 1.34% p.a. from a peak of over 3.8% in late 2023, reflecting the US Federal Reserve’s rate-cutting cycle that began in late 2024. Bank fixed rates have consequently fallen to multi-year lows. This environment — low bank rates, stable HDB rate — makes the bank loan comparison particularly favourable relative to the 2022–2023 period, when SORA-based floating rates exceeded the HDB rate.

Comparable markets offer useful perspective. In Australia, the Reserve Bank rate is 3.35% (June 2026), making equivalent fixed mortgages over 5.0% p.a. In Hong Kong, HIBOR-linked mortgages sit around 3.5%–4.0%. Singapore’s bank rates at 1.60%–1.80% fixed reflect the city-state’s position as a global financial centre with deep SGS bond markets — structural factors that have historically kept Singapore mortgage rates below comparable developed markets.

What Might Come Next

The MAS reviews TDSR/MSR thresholds periodically. There is no current indication of a change to the 30% MSR or 55% TDSR limits — they were last revised in September 2022, when the TDSR was lowered from 60% to 55%. However, if the Singapore property market were to overheat (the URA Private Residential Price Index rose 0.9% in Q1 2026, after several quarters of moderation), further macro-prudential tightening cannot be ruled out. On the CPF side, the OA rate is reviewed quarterly — sustained strong SGS yields could theoretically push the OA rate above 2.5%, which would raise the HDB loan rate. This has not occurred in over 15 years but is a tail risk worth monitoring.

Frequently Asked Questions

Can I use my CPF OA for the cash component of a bank loan downpayment?

What happens to my HDB loan if the CPF OA rate increases?

I took a bank loan. Can I switch back to the HDB loan if bank rates rise sharply?

Does taking an HDB loan affect my ability to buy a second property?

Can foreigners or SPRs take an HDB loan?

What is an HFE letter and do I need it before approaching a bank?

Is the MSR calculated on gross or net income?

Related Articles

Click anywhere outside to close