Singapore Mortgage Refinancing Guide 2026: When to Refinance, How Much You Save

Quick Answer: Singapore Mortgage Refinancing 2026 — Key Takeaways

- Refinancing replaces your existing home loan with a new one from a different bank, typically to secure a lower interest rate; repricing keeps the same bank but renegotiates the rate.

- The best time to refinance is when your lock-in period expires — usually 2–3 years after taking the loan. Refinancing within the lock-in incurs a break cost of typically 1.5% of the outstanding loan amount.

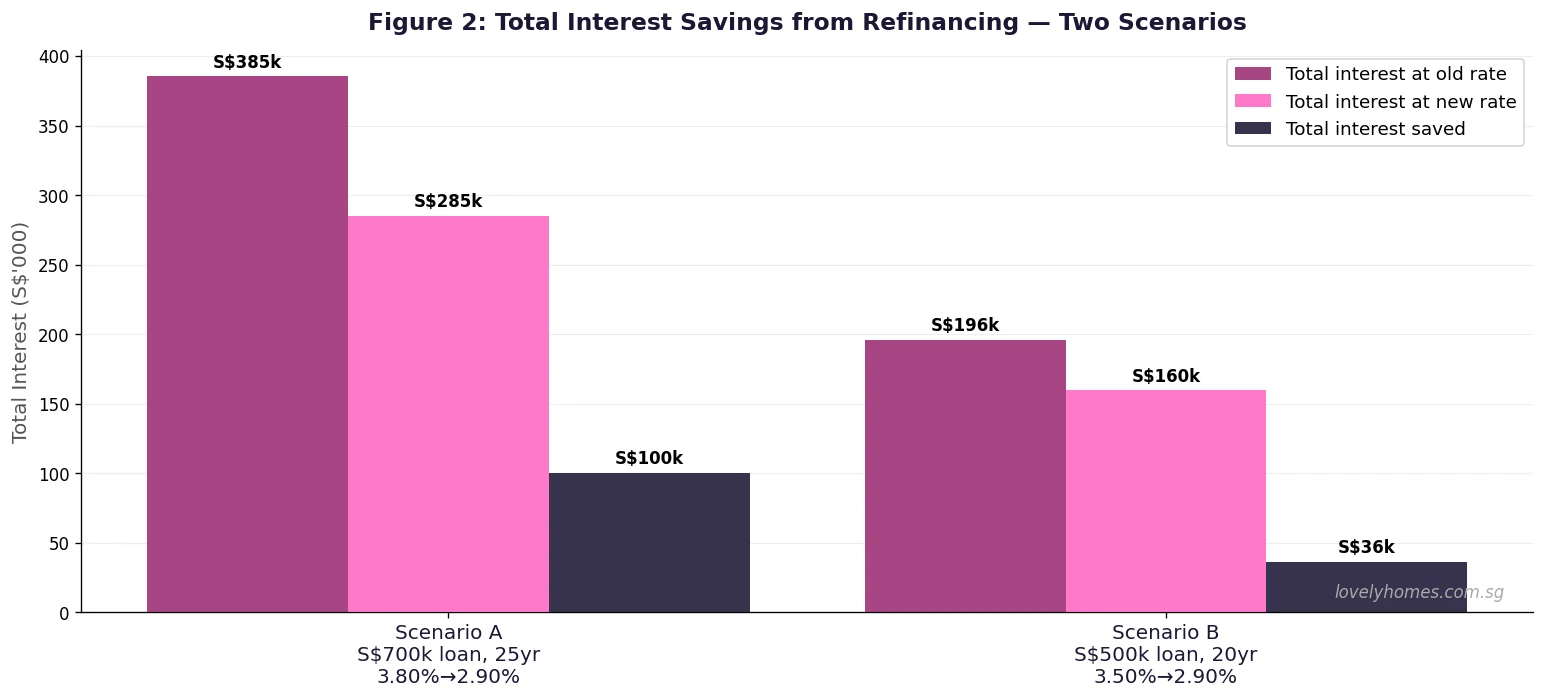

- Typical savings in 2026: a borrower refinancing a S$700,000 loan from 3.80% (a 2024-vintage fixed rate) to 2.90% (current refinance rate) saves approximately S$78,000 in total interest over 25 years, or around S$260/month.

- Transaction costs are modest: legal fees run S$1,800–S$3,000; valuation fees S$300–S$600; some banks offer full legal subsidy packages for refinancers.

- SORA-pegged floating rates (Singapore Overnight Rate Average) offer potential savings when rates fall but expose you to upward repricing; fixed rates provide certainty for 2–3 years.

- CPF OA funds can service the new loan, but the CPF accrued interest rule means any CPF monies used must be repaid (with accrued interest at 2.5% p.a.) on eventual sale.

- Total Debt Servicing Ratio (TDSR) still applies at refinancing — you must prove the new monthly repayment stays within 55% of your gross monthly income.

- Process timeline: from application to completion is typically 4–8 weeks; allow 3 months before lock-in expiry to start comparing packages.

In Singapore’s rate environment of 2024–2026, tens of thousands of homeowners took out fixed-rate mortgages at 3.50%–4.00% when the US Federal Reserve was tightening monetary policy. As those lock-in periods approach their two-year anniversary, refinancing has moved from a niche financial exercise to a mainstream priority. This guide explains exactly when to refinance, how to calculate whether it is worth it, what the process looks like and what to watch out for.

Refinancing vs Repricing: What Is the Difference?

These two terms are often conflated, but they involve distinct processes with different cost structures:

Refinancing means taking out a new home loan from a different bank to repay your existing loan. The new bank’s solicitors handle the discharge of the old mortgage and registration of the new one. You bear legal costs (S$1,800–S$3,000), valuation fees (S$300–S$600), and potentially a break cost if you exit before the lock-in period ends. Many banks offer legal subsidy packages that rebate S$1,800–S$2,500 to offset these costs for loans above a certain quantum.

Repricing means renegotiating your interest rate with your existing bank without changing lenders. The bank may offer this as a retention offer when your lock-in approaches expiry. Repricing is simpler and cheaper (typically S$200–S$800 in administration fees), but the rate offered is often not as competitive as what a new lender will offer to win your business. The trade-off is convenience versus maximum savings.

When Should You Refinance?

The single most important factor is the lock-in period. Most Singapore bank home loans carry a lock-in of 2–3 years, during which refinancing or full redemption triggers a penalty — typically 1.5% of the outstanding loan amount. On a S$700,000 outstanding balance, that is a S$10,500 penalty. You should almost never refinance within the lock-in unless the rate savings are dramatic and you have a very long holding horizon.

Outside the lock-in, refinancing is worth pursuing if the new rate is at least 0.50% lower than your current all-in rate. Below that threshold, the transaction costs (legal fees, valuation, time) may not justify the exercise unless your loan quantum is very large. The breakeven analysis in the next section provides the full framework.

Other triggers that make refinancing particularly timely:

- Your property has appreciated significantly, improving your Loan-to-Value (LTV) ratio and qualifying you for a lower rate tier.

- Your income has increased, qualifying you for a larger loan or improving your TDSR buffer, allowing you to reduce the loan tenure and total interest.

- Interest rates in the market have fallen materially (as has been occurring in Singapore in 2025–2026 as the Fed easing cycle feeds through to SORA and fixed-rate offerings).

- You want to switch from a floating-rate package (with rate uncertainty) to a fixed-rate package for budget certainty.

How Much Can You Save? The Breakeven Calculation

The refinancing decision is fundamentally a breakeven analysis: total savings from a lower rate versus total cost of switching. Here is the framework:

Step 1 — Calculate monthly repayment saving:

Monthly saving = [Old monthly payment] − [New monthly payment]

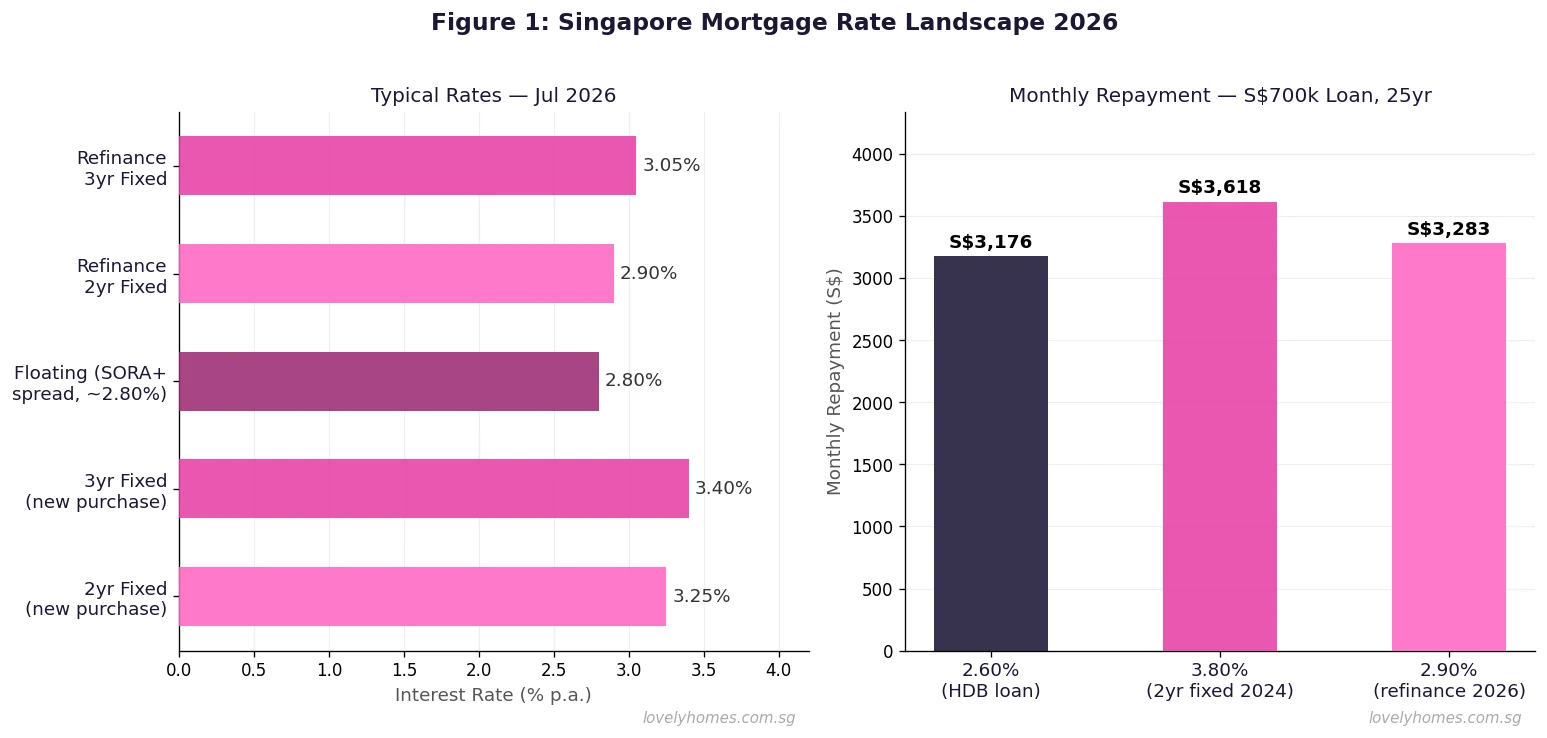

Example: Old rate 3.80%, new rate 2.90%, loan S$700,000, 25 years remaining.

Old payment: S$700,000 × 0.038/12 × (1+0.038/12)^300 / ((1+0.038/12)^300−1) = S$3,609/month

New payment: S$700,000 × 0.029/12 × (1+0.029/12)^300 / ((1+0.029/12)^300−1) = S$3,349/month

Monthly saving: S$260

Step 2 — Calculate total switching cost:

Legal fees: S$2,500 (conservatively; some banks subsidise S$1,800–S$2,500)

Valuation fee: S$500

Total cost: S$3,000 (or as low as S$700 if legal subsidy applies)

Step 3 — Calculate breakeven period:

Breakeven = Total cost ÷ Monthly saving = S$3,000 ÷ S$260 = approximately 11.5 months

With full legal subsidy: S$700 ÷ S$260 = approximately 2.7 months

If you plan to hold the property for more than 12 months after refinancing (virtually all owner-occupiers will), the refinancing exercise pays for itself many times over.

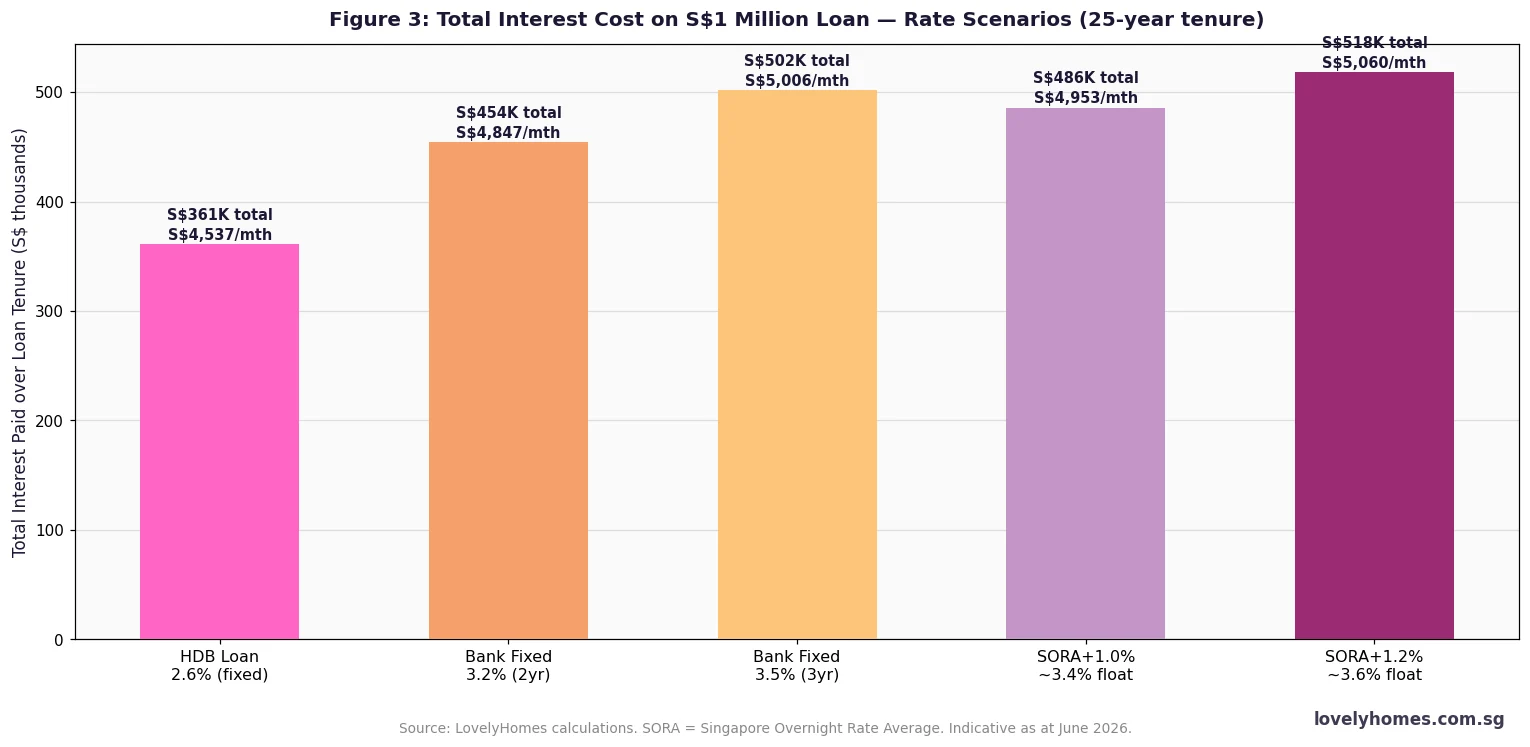

Choosing Between SORA Floating and Fixed Rate

Singapore bank mortgages are broadly offered in two flavours: floating rate (pegged to the Singapore Overnight Rate Average, or SORA, plus a spread) and fixed rate (a guaranteed rate for a defined period, usually 2–3 years).

As at July 2026, 3-month compounded SORA is approximately 2.35% per annum, and bank spreads on SORA packages run from 0.45% to 0.65%, giving an all-in floating rate of approximately 2.80%–3.00%. This is lower than most 2-year or 3-year fixed offerings (2.90%–3.40%). The floating rate appears attractive at current levels — but it will reprice every quarter as SORA moves, and there is no guarantee it stays below fixed rates in 2027–2028 if global rate pressures return.

For borrowers who:

- Have a tight monthly budget and cannot absorb rate increases → choose fixed rate (2–3 years).

- Expect to sell within 2 years (and want no lock-in) → choose a floating package with no lock-in.

- Are refinancing opportunistically and comfortable with rate uncertainty → floating SORA may deliver better outcomes if rates continue declining.

Many borrowers opt for a hybrid: fixed rate for 2 years to lock in current savings, then assess the rate environment at the next repricing/refinancing window.

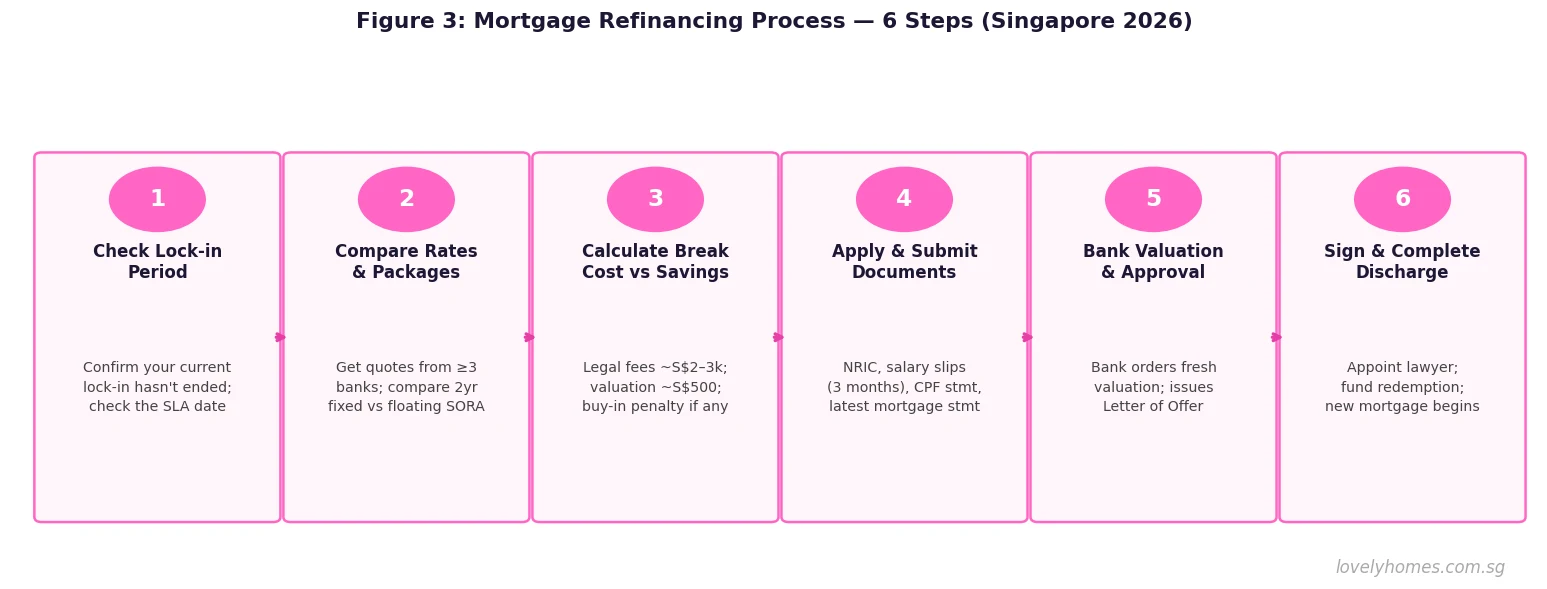

The 6-Step Refinancing Process

The process works as follows in more detail:

Step 1 — Check lock-in period: review your current Letter of Offer (LOO) or contact your bank. Note the exact lock-in expiry date. If lock-in ends in 3 months or less, start immediately.

Step 2 — Compare packages from ≥3 banks: use mortgage brokers or direct bank websites. Compare: all-in rate, lock-in period, legal subsidy quantum, clawback conditions (most banks claw back subsidies if you refinance again within 3 years), late payment penalties.

Step 3 — Calculate break-even: use the formula above. Factor in any legal subsidy. Confirm the new bank’s loan quantum by checking your LTV (outstanding loan vs current valuation).

Step 4 — Apply and submit documents: typically required — NRIC/passport, last 3 months’ payslips, last 2 years’ NOA or CPF annual statement (for self-employed), last 3 months’ CPF transaction history, latest mortgage statement, title deed or SLA record search. Processing time: 2–3 weeks.

Step 5 — Valuation and Letter of Offer: the new bank orders a valuation (S$300–S$600; usually paid by borrower). On approval, a formal LOO is issued. Read all conditions carefully — especially the lock-in, penalty clauses and clawback on subsidies.

Step 6 — Legal completion: appoint a solicitor (often from the bank’s panel to qualify for subsidy). The solicitor handles mortgage discharge from old bank and registration of new charge. The process takes 2–4 weeks from LOO acceptance. On completion, the old loan is fully redeemed and the new mortgage commences.

Summary: When Refinancing Makes Sense

| Situation | Refinance? | Reason |

|---|---|---|

| Lock-in expired, rate gap ≥0.50% | Yes | Savings clear the transaction cost in <12 months |

| Lock-in expired, rate gap <0.25% | No / Reprice only | Transaction costs may outweigh savings on small loans |

| Within lock-in, penalty 1.5% | No | Break cost typically exceeds 3–5 years of rate savings |

| Property value up significantly | Yes, if lock-in expired | Better LTV unlocks lower rate tier |

| Planning to sell within 12 months | No | Insufficient time to recover transaction costs |

| Want certainty vs. floating rate | Switch to fixed | Budget certainty has value beyond raw rate comparison |

| Want maximum saving now | Floating SORA package | SORA ~2.80% is below fixed rates as at July 2026 |

Worked Example: The Tan Household Refinancing Decision

Mr and Mrs Tan are Singapore Citizens who purchased a D15 condominium in March 2024 at S$1,450,000. They took a S$1,087,500 (75% LTV) bank loan at a 2-year fixed rate of 3.80% per annum. Their lock-in expires in March 2026 (which has now passed). Their outstanding balance as at July 2026 is approximately S$1,040,000 with 23 years remaining.

Current monthly payment: S$1,040,000 @3.80%, 23 years = S$5,730/month

Proposed refinance rate: 2-year fixed at 2.90% from Bank B

New monthly payment: S$1,040,000 @2.90%, 23 years = S$5,323/month

Monthly saving: S$407

Annual saving: S$4,884

Transaction costs:

Legal fees: S$2,800 (solicitors for discharge and new mortgage)

Valuation: S$500

Legal subsidy from Bank B: S$2,000

Net out-of-pocket cost: S$1,300

Breakeven: S$1,300 ÷ S$407/month = 3.2 months

Total interest saving over 23 years (rough estimate): S$112,000

Verdict: Refinancing is strongly justified. The Tan household breaks even in just over 3 months, and with Bank B’s legal subsidy absorbing most of the switching cost, the exercise is essentially self-funding within a quarter. Their combined TDSR at S$5,323/month on S$18,000 combined income is 29.6% — well within the 55% cap.

What Might Come Next

Singapore mortgage rates are tied to global monetary conditions via SORA, which tracks the US Federal Reserve’s policy rate with a lag. If the Fed continues its easing cycle into 2027 — as futures markets tentatively suggest — SORA could drift lower, making floating-rate packages increasingly attractive. However, the US election cycle, inflation trajectory and any geopolitical disruptions could reverse this direction quickly.

For 2026 specifically, the window of opportunity for borrowers with 2024-vintage fixed loans at 3.50%–4.00% approaching lock-in expiry is now open. Industry data suggests Singapore mortgage refinancing volumes in Q1–Q2 2026 have exceeded 2023 levels as a result. Borrowers who act in 2026 are capturing a rate environment that is materially better than two years ago; those who wait may find rates have either risen again or the best packages are no longer available.

What is the difference between a lock-in period and a clawback period?

Can I refinance an HDB loan to a bank loan?

Does TDSR apply when refinancing?

How do I know if my property has appreciated enough to get a better rate?

What documents do I need to refinance a Singapore home loan?

Can I use CPF to pay off the legal fees when refinancing?

Is there a minimum loan amount to refinance in Singapore?

Click anywhere to close