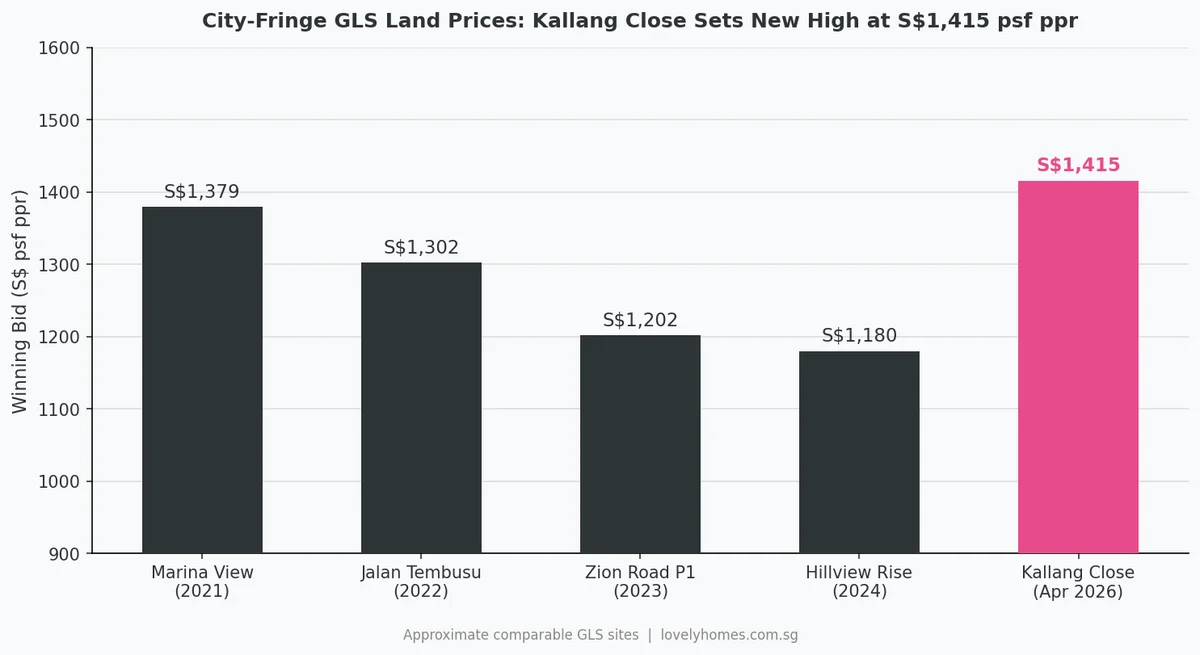

Quick Answer: The GLS tender for Kallang Close closed on 7 April 2026. A joint venture between Frasers Property and Mitsubishi Estate submitted the winning bid of S$610.75 million (S$1,415 psf ppr), the highest psf ppr for a city-fringe residential GLS site in recent years. The site can yield approximately 470 homes and will be the first private residential development in the Kallang Close industrial enclave in 12 years.

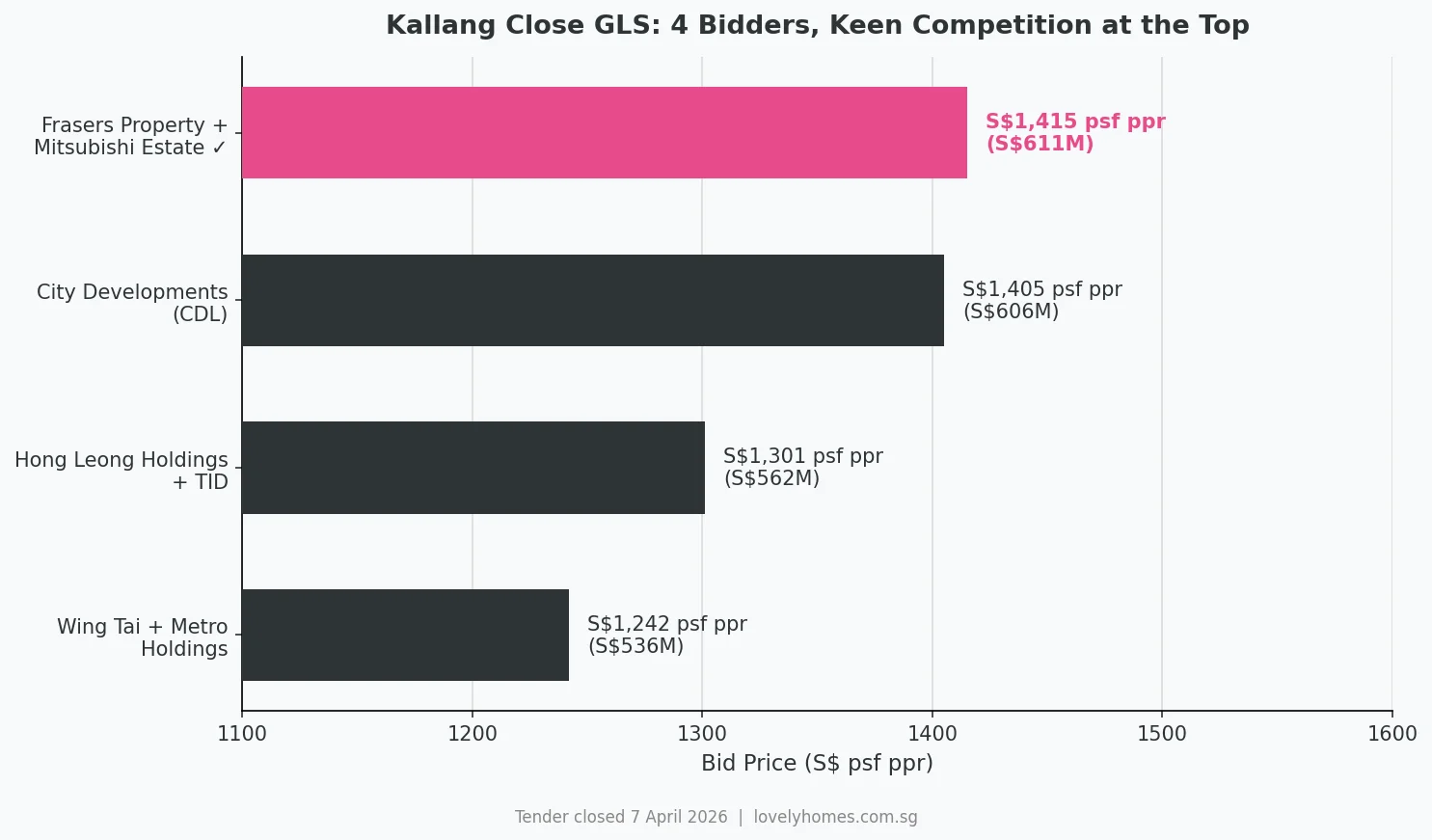

The government land sale (GLS) tender for the Kallang Close residential site closed on 7 April 2026 with four bids — and a result that underscores sustained developer confidence in city-fringe locations, even amid a broader market that posted its lowest transaction volume since Q2 2020.

The winning consortium, a joint venture between Frasers Property Singapore and Mitsubishi Estate, submitted a bid of S$610.75 million (S$1,415 per square foot per plot ratio) — just S$4.35 million, or 0.7%, above second-placed City Developments Ltd. The paper-thin margin between first and second illustrates how keenly both bidders valued the site, and gives a clear signal of where institutional capital believes city-fringe launch prices can go.

Site Factsheet

| Detail | Information |

|---|---|

| Address | Kallang Close, Singapore |

| District | D08 — Kallang / Whampoa |

| Site Area | Approximately 11,456 sq m (123,320 sq ft) |

| Plot Ratio | 3.5 |

| Maximum GFA | Approximately 40,107 sq m (431,611 sq ft) |

| Estimated Units | ~470 private residential homes |

| Tenure | 99-year leasehold (from date of award, Apr 2026) |

| Retail Component | Capped at 115 sq m GFA |

| Childcare Centre | Minimum 500 sq m GFA (mandatory) |

| Winning Bid | S$610.75 million (S$1,415 psf ppr) |

| Joint Venture | Frasers Property Singapore × Mitsubishi Estate |

| Tender Closed | 7 April 2026 |

The Four Bids: Near-Record Competition

| Rank | Bidder | Total Bid | S$ psf ppr |

|---|---|---|---|

| 1st (Winner) | Frasers Property + Mitsubishi Estate | S$610.75M | S$1,415 |

| 2nd | City Developments Ltd (CDL) | S$606.40M | S$1,405 |

| 3rd | Hong Leong Holdings + TID JV | ~S$561.5M | S$1,301 |

| 4th | Wing Tai Holdings + Metro Holdings | ~S$536.4M | S$1,242 |

The 0.7% gap between the top two bids is one of the narrowest in recent Singapore GLS tender history. CDL — which co-developed Norwood Grand in Woodlands with Frasers Property — was effectively beaten by its own partner on a different site. The spread between first and fourth bidders was 13.9%, indicating that all four consortia saw real value in the Kallang Close waterfront location, but had genuinely different views on achievable launch pricing and margins.

Why Kallang Close Commands a Premium

The site’s premium psf ppr reflects several structural advantages that are difficult to replicate in the GLS pipeline:

- Kallang River waterfront frontage. The site sits adjacent to the Kallang River, and the consortium has committed to delivering a publicly accessible riverfront promenade. Waterfront residential sites are rare in Singapore’s land-scarce market; comparable waterfront addresses — Robertson Quay, Marina Bay, Harbourfront — consistently command significant price premiums.

- First private homes in the precinct in 12 years. Kallang Close has been predominantly industrial. The last private residential development in the immediate vicinity launched over a decade ago. Buyers arriving at this project will be entering a precinct undergoing transformation, which historically has been a strong driver of early-adopter price appreciation.

- Dual MRT accessibility. Kallang MRT (East-West Line) and Bendemeer MRT (Downtown Line) are both within walking distance, giving future residents cross-island connectivity without transfers.

- Proximity to the city and Kallang planning transformation. The Kallang Area Master Plan envisions a sports and lifestyle precinct around the Singapore Sports Hub, Kallang Alive, and the future redevelopment of the National Stadium precinct. The broader area is also benefiting from the Geylang-to-Kallang urban renewal corridor.

- Retail and childcare anchors. The mandatory childcare centre (minimum 500 sq m) and capped retail (115 sq m) will add day-to-day amenity value for residents without creating oversupply of commercial space.

What Will Launch Pricing Look Like?

At a land cost of S$1,415 psf ppr, industry analysts have modelled potential launch prices in the S$2,800–3,100 psf range, depending on:

- Construction cost trajectory. Building costs in Singapore rose significantly in 2022–2024 and have moderated but remain elevated. A 99-year leasehold development on a 3.5 plot-ratio site with waterfront features and a childcare component will carry above-average construction costs.

- Positioning relative to comparable launches. Recent city-fringe new launches — Robertson Opus (D09, ~S$3,150–3,360 psf), UPPERHOUSE (D10, ~S$3,350 psf) — provide a ceiling benchmark. Kallang Close, while waterfront, is in D08 which has historically priced at a modest discount to D09/D10.

- Launch timing. The project is unlikely to launch before late 2027 or 2028, given the need for site clearing, design, and construction commencement. The market trajectory over the next 12–18 months will influence the eventual strategy.

A rough breakeven analysis, assuming a 20–22% developer margin over total project cost (land + construction + marketing), suggests a launch price of approximately S$2,900–3,100 psf is required for the project to pencil. Some analysts have modelled upside to S$3,300 psf if the waterfront premium commands a strong early take-up rate.

The Frasers × Mitsubishi Partnership

This is the first JV between Frasers Property Singapore and Mitsubishi Estate, Japan’s largest real estate company by market capitalisation. Frasers Property brings deep Singapore-market execution capability — it has developed One Canberra, Riverfront Residences, and North Park Residences, among others. Mitsubishi Estate brings global real estate expertise and balance sheet scale.

The partnership follows a trend of Japanese developers deepening their Singapore exposure: Sekisui House co-developed THE ORIE in Toa Payoh, MCL Land (a Jardine Matheson subsidiary with deep ties to the Japanese market) developed ELTA in Clementi alongside CSC Land. Japanese investors view Singapore freehold and 99-year leasehold assets as strategic long-term holdings with stable SGD returns.

What This Means for the Broader Market

The Kallang Close result has several read-throughs for Singapore property market observers:

- Developer confidence in RCR/city-fringe pricing remains high. Despite Q1 2026 transaction volumes falling 39.7% QoQ, four major consortia competed vigorously for a single site. Developers are bidding for land they believe they can sell at S$2,900+ psf — a vote of confidence in demand fundamentals.

- CDL’s near-miss is notable. CDL bid aggressively at S$1,405 psf ppr — its second near-miss in recent GLS tenders. The developer appears determined to rebuild its Singapore residential pipeline following a period of relative inactivity.

- The GLS programme is working as a supply valve. The 1H 2026 GLS programme placed 9 sites on the Confirmed List. Kallang Close is the first to be awarded. The forthcoming sites at River Valley Green, Holland Plain, and Peck Hay Road will further test developer appetite in the CCR and RCR.

- Waterfront as a permanent premium. Both the Frasers–Mitsubishi bid and CDL’s second-place bid exceeded S$1,400 psf ppr for a site with river frontage. This reinforces that waterfront views in Singapore command a structural premium that survives cooling measures and interest-rate cycles.

Timeline and What to Watch

| Date / Period | Milestone |

|---|---|

| 7 April 2026 | GLS tender closed; Frasers × Mitsubishi named provisional winner |

| Q2/Q3 2026 | URA formally awards site; conveyance and commencement of site works |

| Late 2026 – 2027 | Architectural design, planning approval, showflat construction |

| 2027 – 2028 (est.) | Showflat preview; public launch (subject to market conditions) |

| 2030 – 2031 (est.) | Expected temporary occupation permit (TOP) based on 99-yr leasehold timeline |

Frequently Asked Questions

Who won the Kallang Close GLS tender?

A joint venture between Frasers Property Singapore and Mitsubishi Estate, with a bid of S$610.75 million (S$1,415 psf ppr). The tender closed on 7 April 2026.

How many units will the Kallang Close development have?

Approximately 470 private residential homes, based on the site’s GFA of approximately 431,611 sq ft at a plot ratio of 3.5.

What is the expected launch price for the Kallang Close condo?

Industry analysts estimate a launch price in the range of S$2,900–3,100 psf, reflecting the land cost, construction expenses, waterfront premium, and comparable city-fringe launches. The project is unlikely to launch before late 2027 or 2028.

Is the Kallang Close site freehold or leasehold?

99-year leasehold, from the date of site award in April 2026.

Which MRT stations are near Kallang Close?

Kallang MRT Station (East-West Line) and Bendemeer MRT Station (Downtown Line) are both within walking distance of the Kallang Close site.

Why is this site significant?

It will be the first private residential development in the predominantly industrial Kallang Close precinct in approximately 12 years. The site has Kallang River waterfront frontage and sits within the broader Kallang Area Master Plan transformation zone, including the Kallang Alive sports and leisure precinct.

When will the Kallang Close condo be completed?

Based on typical construction timelines for a 99-year leasehold project of this scale, the estimated target for a Temporary Occupation Permit (TOP) is approximately 2030–2031. The official construction schedule will be confirmed after the site is formally awarded and planning approval obtained.

Interested in the Kallang Close launch? Register for early updates.

Related Articles

- UPPERHOUSE at Orchard Boulevard — Luxury Living in District 10

- The Robertson Opus — Heritage District Luxury on River Valley Road

- One Marina Gardens — Marina South’s Landmark Integrated Development

- ELTA at Clementi Avenue 1 — Family Living in the West

- Freehold vs 99-Year Leasehold Singapore 2026: The Real Price of Time

- TDSR & MSR: How Much Can You Actually Borrow in Singapore 2026

This article is for general informational purposes only and does not constitute financial or investment advice. Property prices are projections based on analyst estimates at the time of writing; actual launch prices will depend on market conditions at the time of launch. All figures cited are based on publicly available GLS tender results and URA data as at 20 April 2026. No marketing agency is named in connection with this development.

0 Comments