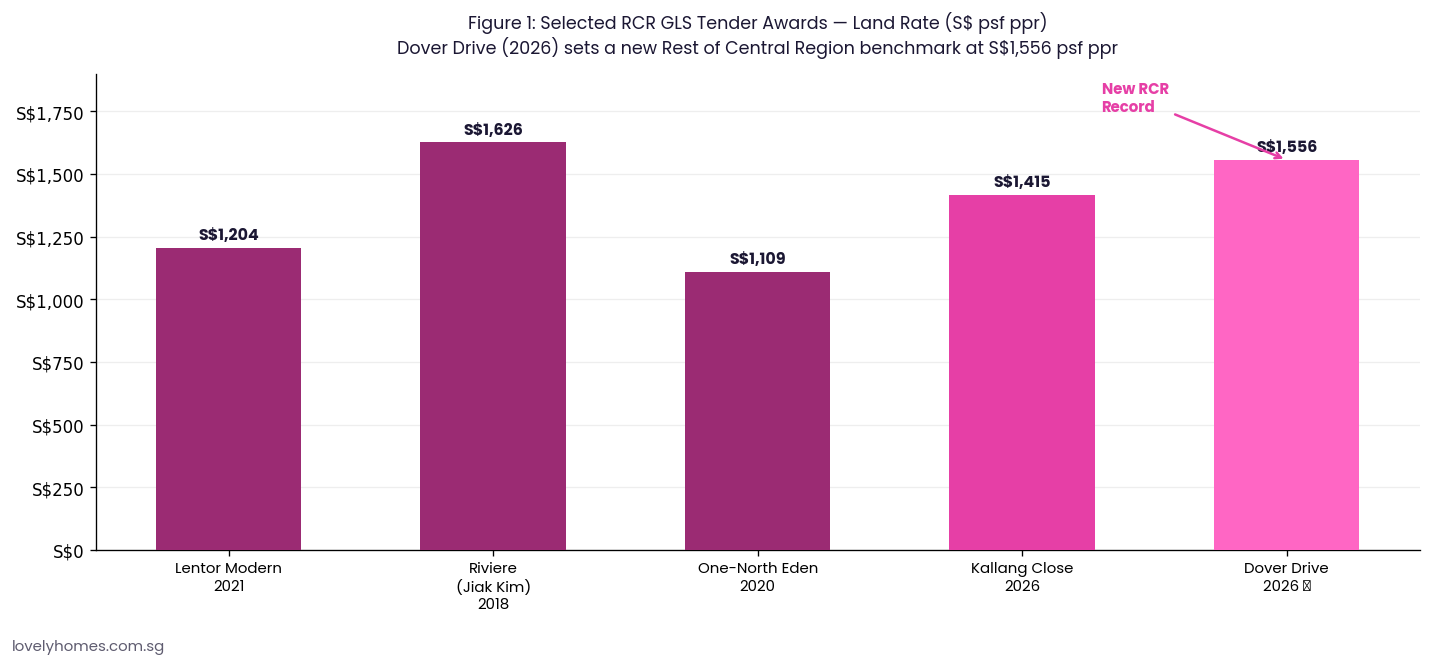

A joint venture comprising Forsea Holdings, Qingjian Realty, and Jianan Capital has set a new Rest of Central Region benchmark for Government Land Sales tender land rates, winning the Dover Drive GLS site with a top bid of S$951 million — equivalent to S$1,556 per square foot per plot ratio (psf ppr). The tender closed on 26 March 2026, drawing six bidders, with the Forsea-Qingjian-Jianan consortium’s offer exceeding the second-highest bid by approximately 8%. The result, confirmed by the Urban Redevelopment Authority, eclipses the previous RCR high and signals sustained developer confidence in Singapore’s mid-market residential sector despite elevated Additional Buyer’s Stamp Duty rates and rising construction costs.

Quick Answer — Dover Drive GLS at a Glance

- Winner: Forsea Holdings, Qingjian Realty and Jianan Capital JV

- Winning bid: S$951 million / S$1,556 psf ppr — new RCR record

- Site: Dover Drive, Bukit Timah Turf City precinct, ~19,041 sqm, 99-year leasehold

- Yield: approximately 330 residential units and 1,400 sqm of commercial space

- Location: District 10, within 500m of Sixth Avenue MRT (Downtown Line)

- Estimated launch price: industry analysts project S$2,800–3,100 psf for the future development

- Previous RCR GLS benchmark: Kallang Close at S$1,415 psf ppr (7 April 2026)

- Context: Bukit Timah Turf City is a major URA Master Plan 2025 precinct transforming the site of the former horse-racing turf city into a new residential neighbourhood

The Dover Drive Site: Location and Planning Context

The Dover Drive GLS site sits within the Bukit Timah Turf City precinct — a large-scale urban transformation project that the Urban Redevelopment Authority unveiled in Draft Master Plan 2025 consultations as a model for car-lite, transit-oriented residential development. The precinct occupies the site of the former Singapore Turf Club racing grounds in the Bukit Timah corridor, and the URA has earmarked it for a mix of private residential, retail, and community uses connected by a green pedestrian spine. The Dover Drive parcel is the first residential GLS site to be tendered from this precinct, making it a landmark bid not just for its price but for the signal it sends about developer and market confidence in the entire transformation zone.

The site is approximately 400 metres from Sixth Avenue MRT station on the Downtown Line (DTL), and approximately 1.1 kilometres from the King Albert Park MRT. The immediate neighbourhood is characterised by D10 landed housing estates and older low-density condominiums; the arrival of a new high-density residential development will be a significant change in the character of the streetscape. The 330-unit yield, spread across a 19,041 sqm site at a 2.8 plot ratio, implies a mid-rise or high-rise configuration suited to the premium nature of the D10 location.

Why S$1,556 psf ppr Is a Record — and What It Means

The RCR land rate record matters because it directly constrains the launch price of the future development. Developers typically need to achieve a residential selling price equivalent to approximately 1.5–1.8 times the land rate (after accounting for construction costs, development charges, interest carry, and profit margin) to achieve a viable return. At S$1,556 psf ppr, the arithmetic points to a launch price of approximately S$2,800–3,100 psf — which would make the future Dover Drive development the most expensive new launch in the Rest of Central Region to date, eclipsing current RCR benchmarks set by projects like Riviere (Jiak Kim Street, by Frasers) at S$2,500–2,700 psf.

For buyers already in the market, the Dover Drive result is a read-through signal: it implies that new launches in the broader RCR — particularly near Sixth Avenue, Holland Village, and the Bukit Timah corridor — will be repriced at higher launch PSFs to maintain developer returns relative to elevated land costs. Resale condos in the immediate catchment (Sixth Avenue, Nexus, One Holland Village) are likely to experience upward valuation pressure as the future Dover Drive development sets new comparable prices.

The Developer Consortium: Forsea, Qingjian, Jianan

Forsea Holdings is the Singapore development arm of Far East Consortium International, a Hong Kong-listed conglomerate with hospitality and residential development assets across Asia, the United Kingdom, and Australia. Qingjian Realty is the Singapore subsidiary of Qingjian Group, a major Chinese state-owned construction conglomerate that has been active in Singapore’s EC and private residential market since the 2010s — notable prior projects include Bellewoods EC and Jadescape. Jianan Capital is a Chinese-backed investment vehicle that has participated in recent Singapore GLS tenders. The consortium structure — a combination of Hong Kong regional capital, mainland Chinese construction expertise, and Singapore market knowledge — reflects the continuing interest of overseas capital in Singapore’s relatively stable and transparent property market despite the foreign buyer ABSD headwind at the consumer level.

Summary Table: Dover Drive GLS Key Facts

| Parameter | Detail |

|---|---|

| Site address | Dover Drive, Bukit Timah Turf City, District 10 |

| Site area | ~19,041.6 sqm (~204,974 sqft) |

| Tenure | 99-year leasehold |

| Gross plot ratio | 2.8 (residential) + 1,400 sqm commercial |

| Estimated units | ~330 residential units |

| Winning bid | S$951 million (S$1,556 psf ppr) |

| Number of bids | 6 bids submitted |

| Developer | Forsea Holdings × Qingjian Realty × Jianan Capital JV |

| Nearest MRT | Sixth Avenue MRT (DTL), ~400m |

| Estimated launch psf | S$2,800–3,100 psf (analyst estimates; subject to market conditions) |

What This Means for Buyers and the Broader Market

The Dover Drive result arrives in a market context where URA’s Q1 2026 full statistics (released 25 April 2026) confirmed that private residential prices rose 0.9% quarter on quarter — healthy but below the 2021–2022 exuberance that triggered the April 2023 ABSD measures. Six bids is a reasonably competitive field, suggesting developers see long-run demand support in the D10 corridor sufficient to justify a S$951M land cost commitment. However, the sharp premium over the Kallang Close benchmark (itself set just three weeks before at S$1,415 psf ppr) indicates that specific site attributes — the Turf City transformation narrative, the D10 address, the Sixth Avenue MRT proximity — are being capitalised aggressively by the winning consortium.

For buyers monitoring the pipeline, the Dover Drive development is likely 3–4 years from launch (land award to launch typically takes 2–3 years for detailed planning, construction commencement, and preview preparation). It will not affect near-term new launch supply but will establish pricing anchors for the Bukit Timah Turf City precinct for future releases. The broader Turf City masterplan includes multiple residential, commercial, and community sites; the success of the Dover Drive tender is likely to encourage the URA to accelerate the release of subsequent Turf City parcels in the 2H2026 GLS programme.

Frequently Asked Questions

What is psf ppr and why does it matter for buyers?

PSF ppr stands for “per square foot per plot ratio” — it is the standard unit used to compare Government Land Sales tender prices across different sites that have different sizes and allowed development intensities. A site sold at S$1,556 psf ppr with a plot ratio of 2.8 implies a total development quantum that the developer must recoup through unit sales. For buyers, the psf ppr is the primary input to estimating the future launch price: developers typically need to price units at 1.5–1.8 times the land rate (plus development charges and construction costs) to make a viable return. A record psf ppr therefore almost always translates to a record launch price for the eventual development.

What will the new Dover Drive development be called and when will it launch?

As of April 2026, the development name has not been announced. The Forsea-Qingjian-Jianan consortium will need to complete detailed design, obtain regulatory approvals, and commence construction before a preview can be held. Based on the typical Singapore development timeline (land award to preview: approximately 2–3 years), the Dover Drive project is not expected to launch until 2028–2029 at the earliest. When it does launch, it will be marketed under the Turf City precinct identity that the URA has established for the broader development zone.

Does the Dover Drive result mean D10 property prices will rise?

The Dover Drive land sale is a leading indicator that suggests future new launch prices in the D10–D11 Bukit Timah corridor will be set at or above S$2,800–3,100 psf. For existing resale condos in the immediate catchment — particularly projects near Sixth Avenue, Shelford, and Farrer — this creates upward comparable pricing pressure when valuers and agents reference the forthcoming new launch as a benchmark. Whether this translates to immediate resale price increases depends on transaction volumes, seller motivation, and interest rate conditions, but historically the announcement of a high-price GLS award in a precinct has led to a 3–6% improvement in nearby resale asking prices within 6–12 months of the award.

Related Articles

- Kallang Close GLS: Frasers & Mitsubishi Estate S$610.8M Waterfront Condo 2026

- Singapore Private Property Q1 2026: Full URA Statistics

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Thomson-East Coast Line Property Guide Singapore 2026

- Singapore Landed Property Guide 2026: Types, Rules, Prices & Who Can Buy

Disclaimer

This article is based on publicly available information from the Urban Redevelopment Authority (URA) and industry sources. Estimated launch prices and yield figures are analyst projections and do not constitute investment advice. Property values may rise or fall. Consult a licensed property professional before making any property decision. ABSD and stamp duty rates are subject to change; verify with IRAS.

0 Comments