- HDB resale median prices (2026): 3-room S$440k · 4-room S$598k · 5-room S$885k · Executive S$1.12M

- Private condo: S$1,600–S$2,600 psf depending on age; AMO Residence (D26) achieved S$2,100–S$2,600 psf at launch

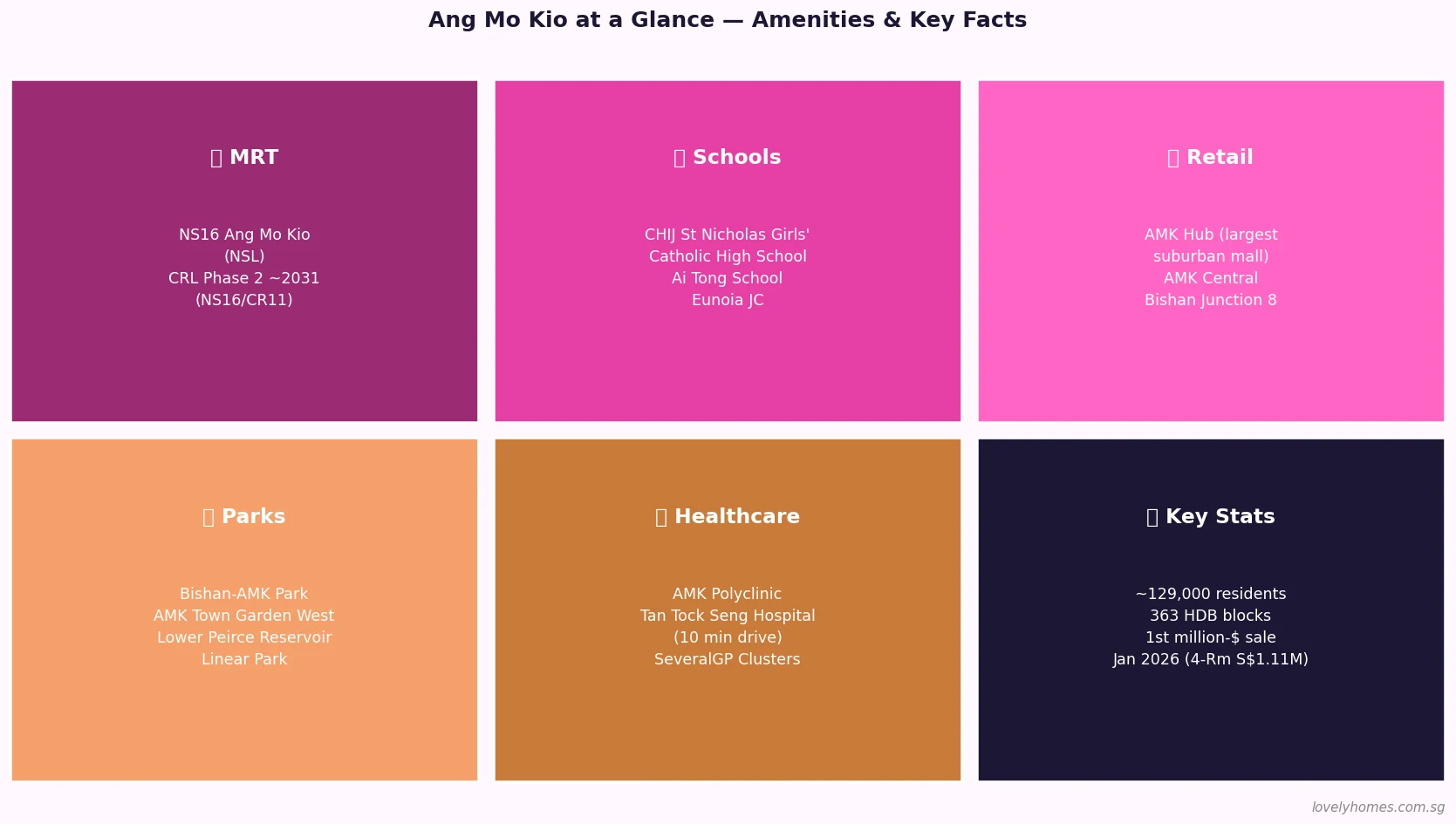

- MRT: Ang Mo Kio MRT (NS16, NSL) with Cross Island Line interchange planned ~2031 (NS16/CR11)

- Top schools: CHIJ St Nicholas Girls’ School, Catholic High School, Ai Tong School, Eunoia Junior College, Nanyang Polytechnic

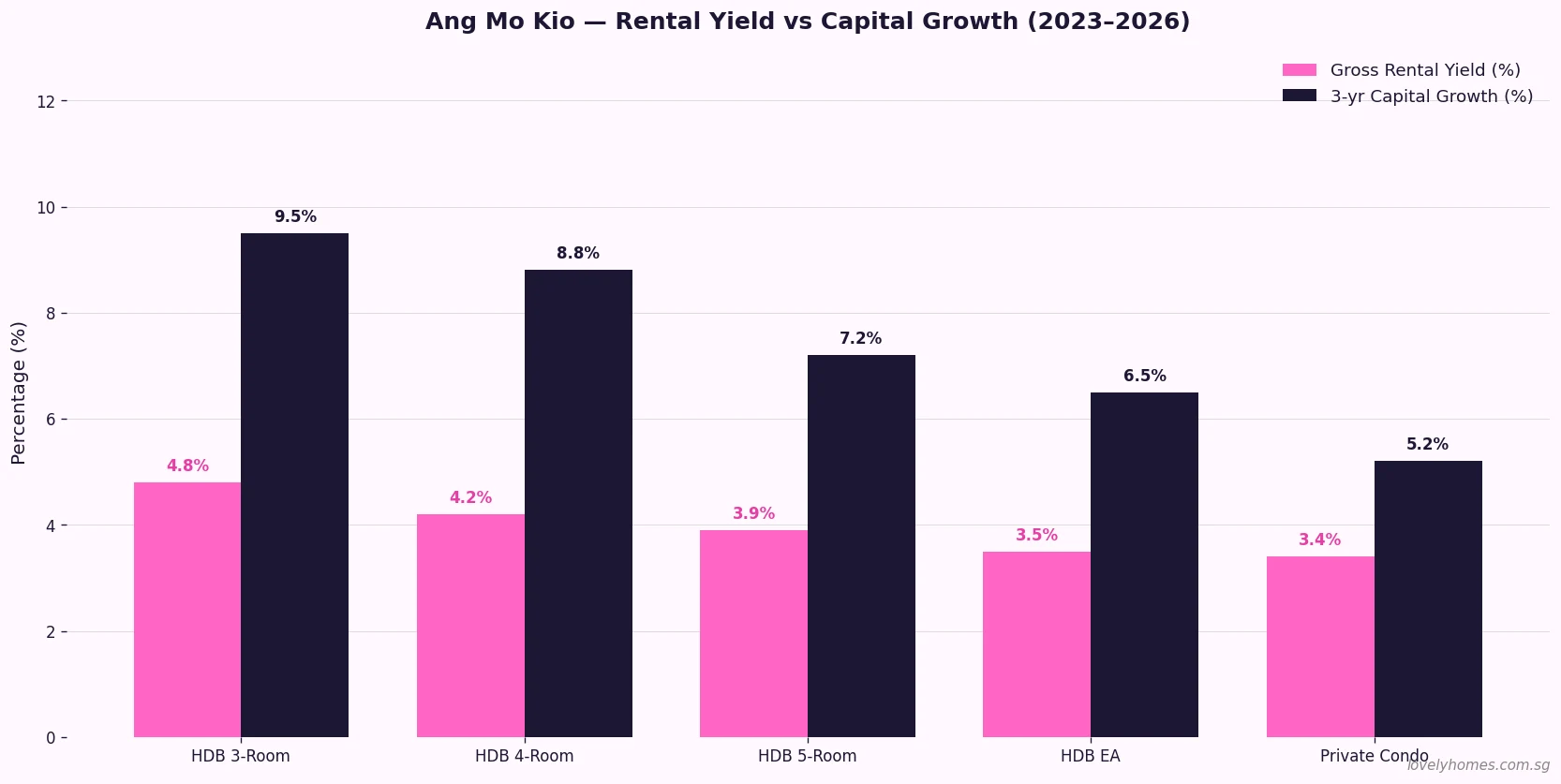

- Gross rental yield: HDB 3-room ~4.8% · 5-room ~3.9% · private condo ~3.4%

- June 2026 BTO: Two Plus-class projects launching in AMK (~1,050 units combined)

- Investment catalyst: CRL Phase 2 station (NS16/CR11) planned; 13,480-unit national MOP wave boosting resale supply

- Best for: Families prioritising elite schools, upgraders with HDB equity, and long-hold investors banking on CRL uplift

Ang Mo Kio — or AMK as it is universally called — is one of Singapore’s oldest and most self-contained Housing Development Board (HDB) towns. Built out from the 1970s under the Urban Redevelopment Authority (URA) and HDB’s ambitious resettlement programme, the town is today home to roughly 129,000 residents across 363 HDB blocks, a sprawling AMK Hub mall, and one of Singapore’s most storied school corridors. For buyers in 2026 the town presents a notable paradox: property prices that remain meaningfully below the premium of Bishan or Toa Payoh, yet access to schools, green space, and infrastructure that rivals any mature estate on the island.

This guide covers everything you need to know about buying, renting, or investing in Ang Mo Kio property in 2026 — HDB resale and BTO options, private condominiums, rental yields, the June 2026 BTO launch, and the longer-term investment case anchored by the forthcoming Cross Island Line interchange.

Ang Mo Kio Property Market Overview

AMK sits in URA Planning Area D20 — a mature, predominantly public-housing district bookended by Bishan to the south and Yishun/Lower Seletar Reservoir to the north. The HDB resale market recorded roughly 827 transactions in the twelve months to March 2026, with the overall median resale price at S$500,000. The estate’s first million-dollar 4-room flat transacted in January 2026 at S$1.11 million — a milestone that underscores the structural upward drift in AMK values even as the national HDB Resale Price Index dipped 0.1% in Q1 2026 per HDB’s official data.

HDB Resale Market — Prices, Trends and What Drives Them

AMK’s HDB resale market is deep and liquid. The town’s large stock of 3-room flats (the most traded type, accounting for roughly 444 of the town’s annual transactions) keeps entry prices accessible for first-timers. At a median of S$440,000 for a 3-room flat, AMK sits competitively against comparable mature estates such as Toa Payoh (S$475,000) and Serangoon (S$465,000), while offering comparable commute times to the city via the North-South Line.

The 4-room market — median S$598,000 — is where most upgrader activity is concentrated. Blocks in the Ang Mo Kio Court and Avenue 3 cluster command a premium given proximity to CHIJ St Nicholas Girls’ School (1-km radius for priority Phase 2B registration), and it was an Avenue 10 4-room unit that became the estate’s first million-dollar resale transaction in January 2026. The 5-room and Executive markets (medians S$885,000 and S$1.12M respectively) are thinner but attracting growing interest from HDB-to-HDB upgraders who have booked proceeds from Bishan or Ang Mo Kio Avenue 1 mature blocks.

Private Condominium Market

Private residential supply within AMK town proper is limited, which is structurally supportive of prices. The most representative benchmark is AMO Residence (99-year leasehold, launched 2022 by UOL Group), which achieved an average of approximately S$2,110 psf at launch and has sustained resale values in the S$2,050–S$2,200 psf range through Q1 2026. Older condominiums — such as The Calrose and Grandeur 8 — trade between S$1,450 and S$1,700 psf, providing a wider entry range for buyers who are less sensitive to remaining lease.

For investors, the private condo market in AMK competes primarily against Bishan and Thomson given similar school proximity; prices at Thomson Road typically command a 15–20% premium for comparable units. This relative discount, combined with the anticipated Cross Island Line (CRL Phase 2) station at Ang Mo Kio (~2031 expected opening), makes AMK private condos an interesting medium-term hold for yield-and-growth buyers.

Amenities, Connectivity and Schools

Ang Mo Kio MRT Station (NS16) sits on the North-South Line (NSL), providing direct access to Orchard Road in approximately 18 minutes and to Raffles Place in 25 minutes. Bishan Station (NS17) is one stop south — useful for connecting to the Circle Line. The transformative addition will be the Cross Island Line (CRL) Phase 2 station at Ang Mo Kio, designated NS16/CR11, expected to open around 2031. When operational, AMK will become a two-line interchange; historically, new interchange status has driven 8–15% appreciation in surrounding HDB resale values within the two years preceding opening.

The school landscape is AMK’s most compelling selling point for family buyers. Within a practical commute of the town sit CHIJ St Nicholas Girls’ School (independent school, 1-km bubble covers AMK), Catholic High School (independent, highly sought-after secondary), Ai Tong School (popular primary with strong ballot demand), Anderson Secondary School, and Eunoia Junior College. At the tertiary level, Nanyang Polytechnic occupies the northern edge of the estate — its presence supports rental demand from students, a structural tailwind for investors in 4-room and 5-room HDB units offering individual room rentals.

Retail is anchored by AMK Hub, one of Singapore’s largest suburban malls with over 200 tenants and direct MRT-level connectivity. Green space is abundant: Bishan-Ang Mo Kio Park — one of Singapore’s largest urban parks at 62 hectares — runs along the Kallang River, offering cycling, kayaking, and active recreation. Lower Peirce Reservoir and its nature trails are within 15 minutes. Healthcare is served by AMK Polyclinic, with Tan Tock Seng Hospital approximately 10 minutes away by car.

Rental Market and Investment Yields

AMK offers a structurally solid rental market driven by three demand segments: international and local professionals priced out of Bishan and Toa Payoh; Nanyang Polytechnic students and lecturers seeking room rentals; and families seeking proximity to the CHIJ–Catholic High school corridor. Gross rental yields in 2026 range from approximately 4.8% for a 3-room HDB to 3.4% for a private condo, with net yields (after property tax and maintenance) typically 0.8–1.2 percentage points lower.

Three-room HDB units generate the highest yields on a gross basis, reflecting their lower entry price relative to monthly rents (S$1,700–S$2,200 per month for a whole-unit rental in 2026). Five-room units in the S$880,000–S$940,000 range can achieve S$2,800–S$3,200 per month, delivering a gross yield of approximately 3.9% — still meaningfully above the 3.4% available from a private condo. For investors subject to 20% ABSD on a second residential property, the after-ABSD yield compression needs to be factored into the decision: at 20% ABSD, a S$900,000 HDB resale purchase carries an additional S$180,000 tax burden, reducing the five-year total return by roughly 3 percentage points compared with an ABSD-free first purchase.

Ang Mo Kio Property Summary (2026)

| Property Type | Median / Avg Price | Approx PSF | Gross Rental Yield | Best For |

|---|---|---|---|---|

| HDB 3-Room | S$440,000 | ~S$485/psf | ~4.8% | First-timers, singles (35+) |

| HDB 4-Room | S$598,000 | ~S$570/psf | ~4.2% | Young families, school-proximity buyers |

| HDB 5-Room | S$885,000 | ~S$610/psf | ~3.9% | Growing families, multi-gen households |

| HDB Executive | S$1,119,000 | ~S$595/psf | ~3.5% | Families requiring extra space |

| Private Condo (older) | S$1,450–S$1,700 psf | — | ~3.6% | Private upgraders on tighter budgets |

| Private Condo (AMO Residence) | S$2,050–S$2,200 psf | — | ~3.2% | Long-hold CRL play, school-zone investors |

Worked Example — HDB Upgrader in Ang Mo Kio

Mr and Mrs Lim are a Singapore Citizen couple in their mid-thirties. They purchased a 4-room BTO flat in AMK in 2019 for S$385,000. Their Minimum Occupation Period (MOP) cleared in October 2024. They are now considering selling and buying a 5-room resale flat within AMK to remain in the CHIJ St Nicholas Girls’ School proximity zone for their daughter.

Estimated sale proceeds (seller’s side): Their 4-room resale in Q1 2026 at the estate median of S$598,000, less outstanding HDB loan S$180,000, less CPF principal refund S$155,000, less CPF accrued interest at 2.5% p.a. over 6 years (~S$24,000), less conveyancing and agent fees (~S$13,000), leaves net cash proceeds of approximately S$226,000.

Buying a 5-room resale at S$880,000: BSD payable = [(1% × S$180k) + (2% × S$180k) + (3% × S$640k)] = S$1,800 + S$3,600 + S$19,200 = S$24,600. ABSD = 0% (SC buying first property after selling existing HDB). Down payment: 10% cash minimum (bank loan, 75% LTV) = S$88,000. Loan amount: S$660,000 at a 1.80% 2-year fixed rate → monthly instalment approximately S$2,820 per month. On a combined household income of S$12,000, TDSR = 23.5% — comfortably within the 55% ceiling.

This example illustrates that an AMK within-estate upgrade is very achievable for dual-income SC couples who have accumulated equity over a five-to-seven-year HDB ownership period, and that the school-zone premium built into AMK prices is well supported by continued family demand.

Why Ang Mo Kio Matters for Buyers in 2026

AMK is not a growth hotspot in the same way Tengah or Bayshore is — it lacks the blank-canvas narrative. But what it offers is arguably more valuable in an uncertain macro environment: depth, liquidity, and infrastructure. The town has bus interchanges, a polyclinic, AMK Hub, and one of the densest concentrations of top primary and secondary schools in any single planning area outside Buona Vista and Queenstown.

Three structurally sound reasons to consider AMK in 2026. First, the CRL interchange effect: historical precedent from Buona Vista (EW21/CC22) and Outram Park (EW16/NE3/TE17) shows that a new interchange station typically adds 8–15% to surrounding HDB resale values in the 24 months before opening. With NS16/CR11 targeted for ~2031, the repricing window is 2028–2031. Second, the June 2026 BTO factor: two new Plus-class BTO projects totalling approximately 1,050 units are launching in the second week of June 2026 — broad media coverage will drive resale enquiries from applicants who prefer immediate occupancy. Third, school proximity demand is structural: Singapore’s primary school registration framework creates permanent, ballot-driven demand for properties within 1-km of top schools.

What Might Come Next

Beyond the near-term CRL and BTO catalysts, URA’s Master Plan 2025 envisions the AMK town as a rejuvenated district-level commercial and leisure hub. Older industrial parcels along Ang Mo Kio Industrial Park are being progressively repositioned under White and Business Park zoning. The longer-term question is whether any GLS sites for private residential will be released within AMK town proper — currently private residential supply is entirely resale, which supports price stability but limits launch-driven price discovery.

On the HDB side, the national MOP supply wave (13,480 flats reaching MOP in 2026 nationally) includes AMK Avenue 1 and Avenue 6 BTO flats from 2019–2021 launches. Their entry into the resale market over 2026–2027 will moderately expand choice and may hold 4-room medians in the S$580,000–S$620,000 range before the CRL premium accrues. Patient buyers who watch for the first wave of post-MOP AMK listings stand to acquire at prices that will likely look attractive in retrospect by 2029–2031.

Frequently Asked Questions — Ang Mo Kio Property 2026

Is Ang Mo Kio a good place to buy property in 2026?

AMK is a strong choice for families prioritising school proximity (CHIJ St Nicholas, Catholic High, Ai Tong, Eunoia JC), and for medium-term investors positioning ahead of the Cross Island Line Phase 2 interchange (~2031). Prices remain moderate compared to Bishan and Toa Payoh for comparable estate profiles, and the deep resale market provides good liquidity at exit. The key near-term risk is the wave of post-MOP resales from 2019–2021 BTO cohorts, which may modestly increase supply in 2026–2027 and limit short-term capital appreciation. Buyers with a five-to-seven-year hold horizon are best positioned.

Which MRT stations serve Ang Mo Kio?

Ang Mo Kio MRT (NS16) on the North-South Line is the primary station, located at AMK Avenue 8 adjacent to AMK Hub. It provides direct access to Orchard (6 stops, ~18 min) and City Hall (7 stops, ~22 min). Bishan MRT (NS17/CC15) is one stop south, serving as a Circle Line interchange. The Cross Island Line Phase 2 station at Ang Mo Kio (NS16/CR11) is expected around 2031, converting AMK MRT into a two-line interchange — a material infrastructure upgrade that should positively impact property values from approximately 2028 onwards.

What is the June 2026 BTO launch in Ang Mo Kio about?

HDB is launching two Plus-class BTO projects in Ang Mo Kio in the June 2026 sales exercise, offering approximately 1,050 units combined. Plus-class classification means a 10-year MOP, resale restricted to Singapore Citizens for the first transaction, and a subsidy clawback on resale proceeds. Indicative pricing is expected in the S$430,000–S$550,000 range for 4-room flats. The application window opens in the second week of June 2026. Full details are covered in the LovelyHomes June 2026 BTO Launch Guide.

How does Ang Mo Kio compare to Bishan and Toa Payoh for property investment?

All three are mature, NSL-served estates with strong school proximities, but AMK is priced meaningfully below both. Bishan 4-room HDB resale medians have consistently run 18–25% above AMK’s (roughly S$740,000 vs S$598,000 in early 2026). Toa Payoh medians are approximately 12–15% above AMK’s. For investors, AMK’s lower absolute entry price gives a higher gross yield and preserves more capital for deployment elsewhere. For owner-occupiers, the value proposition is highly favourable — comparable schools and amenities at a material discount.

Can first-time buyers get an HDB loan for an AMK resale flat?

Yes, provided they meet standard HDB loan eligibility criteria: Singapore Citizen or Permanent Resident, within the income ceiling (S$14,000 gross monthly for families, S$7,000 for singles), with a valid HDB Loan Eligibility (HLE) Letter. For a 4-room AMK resale at S$598,000, the maximum HDB loan (80% LTV) is S$478,400, with a minimum 2.5% cash outlay of S$14,950. At 2.6% over 25 years, monthly instalments are approximately S$2,159 — within the 30% Mortgage Servicing Ratio ceiling for a household earning S$8,600 per month. The Buyer’s Stamp Duty on S$598,000 is S$13,940.

What is the outlook for private condo prices in Ang Mo Kio?

Private residential supply in AMK town proper is limited, as there have been no new GLS launches within the core AMK planning area in recent years. AMO Residence (D26, TOP 2026) is the closest benchmark, with resale pricing broadly supported by strong rental demand and the anticipated CRL uplift. URA’s Q1 2026 data shows OCR non-landed prices rose 2.2% in the quarter — AMK private condos benefit from the same OCR demand dynamics. Industry research from Q2 2026 has cited AMK private condos as among the more compelling OCR plays for the 2026–2031 investment window, specifically on the basis of the CRL interchange premium and limited new supply pipeline.

Related Articles

- June 2026 BTO Launch: 6,900 Flats Across 5 Towns — Complete Buyer’s Guide

- HDB BTO Application and Ballot System Singapore 2026

- Tampines Neighbourhood Guide Singapore 2026

- Bedok Neighbourhood Guide Singapore 2026

- Pasir Ris Neighbourhood Guide Singapore 2026

- Upgrading from HDB to Private Property Singapore 2026

- HDB Grants Singapore 2026: EHG, CPF Housing Grant and More

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer: This article is provided for general information purposes only and does not constitute financial, investment, legal, or property advice. Property prices, rental yields, and policy details referenced are based on publicly available data from the Urban Redevelopment Authority (URA), Housing and Development Board (HDB), and industry research as at 18 May 2026, and may change without notice. Readers should conduct their own due diligence and consult licensed professionals — including a CEA-registered property agent, licensed bank or mortgage broker, and qualified legal counsel — before making any property transaction decision.

0 Comments