URA Launches Two New GLS Sites in May 2026: Berlayar Drive and New Upper Changi Road — 1,425 Homes in the Pipeline

- The Urban Redevelopment Authority (URA) launched two new residential Government Land Sales (GLS) sites in May 2026 — at Berlayar Drive (District 3, Bukit Merah) and New Upper Changi Road (District 16, Bedok).

- Berlayar Drive is a 271,929 sqft site with GPR 1.4, expected to yield ~415 homes; tender closes 4 August 2026.

- New Upper Changi Road is a larger 331,194 sqft site with GPR 2.8, potentially yielding ~1,010 homes — a future mega-development; tender closes 1 September 2026.

- Both sites are 99-year leasehold; no land price benchmark yet — developers submit sealed bids by the respective tender close dates.

- Berlayar Drive sits within the Greater Southern Waterfront (GSW) transformation corridor — one of Singapore’s most significant long-term urban rejuvenation projects.

- New Upper Changi Road is the first large OCR residential GLS site in Bedok since the Bayshore Drive parcel (Vela Bay, awarded 2025), bringing much-needed OCR supply to the eastern region.

- Together, both sites add 1,425 estimated units to the 1H 2026 GLS pipeline, contributing to MAS and URA’s stated goal of maintaining adequate private housing supply.

URA Launches Two New Residential GLS Sites in May 2026

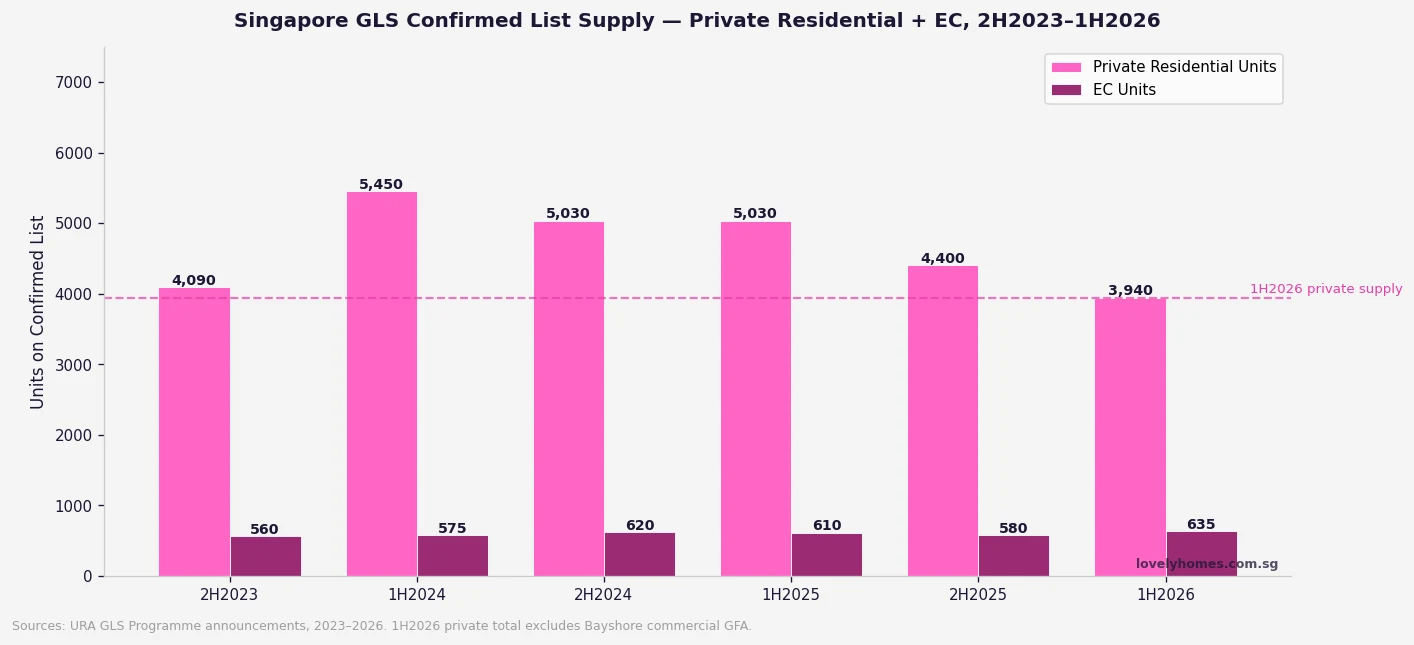

The Urban Redevelopment Authority (URA) released two residential sites for sale by public tender in May 2026 under the 1H 2026 Government Land Sales (GLS) programme — at Berlayar Drive in Bukit Merah and New Upper Changi Road in Bedok. The launch adds approximately 1,425 private homes to the confirmed list supply pipeline, reinforcing the government’s commitment to ensuring adequate housing supply as private residential prices continue to be closely monitored by both URA and the Monetary Authority of Singapore (MAS).

The two sites are markedly different in character. Berlayar Drive is a smaller, low-density waterfront parcel within the emerging Berlayar estate — part of the broader Greater Southern Waterfront transformation masterplan. New Upper Changi Road is a high-density OCR site that could become one of Singapore’s largest single condominium developments, with analysts projecting 1,000 or more units. Both sites will be sold by closed tender, with bids evaluated on the highest price basis subject to the technical conditions of tender.

Berlayar Drive — Waterfront Living at the Edge of the Greater Southern Waterfront

The Berlayar Drive site is located in the Bukit Merah planning area (District 3), adjacent to Telok Blangah MRT station on the Circle Line (CC29). The site forms part of the nascent Berlayar estate, a new residential precinct being carved out from the southern edges of Bukit Merah and Telok Blangah, with proximity to the Southern Ridges park connector system, Henderson Waves, and the Labrador Nature Reserve.

At 271,929 sqft with a gross plot ratio of 1.4, the Berlayar Drive site is notably low-density for a Singapore residential GLS parcel — reflecting URA’s planning intent to create a mid-rise, waterfront-adjacent neighbourhood rather than another high-rise tower cluster. The estimated 415 units would make this a boutique-to-mid-sized development, and the lower density is expected to attract premium pricing from developers given the site’s proximity to the Southern Waterfront and the overall scarcity of new residential supply in D3.

The Greater Southern Waterfront (GSW) masterplan — one of Singapore’s most ambitious urban transformation programmes — encompasses a 30km waterfront stretch from Pasir Panjang to Marina East, including the relocation of Tanjong Pagar Terminal (to Tuas by 2027), the repurposing of Pulau Brani, and the creation of new waterfront precincts at Keppel, Mount Faber, Berlayar, Labrador and Pasir Panjang. Berlayar Drive sits directly within this transformation zone. Industry analysts expect the developer to price land at S$1,300–1,600 psf ppr, reflecting the GSW premium, the D3 RCR location and the low-density advantage — which typically supports higher per-unit ASP.

New Upper Changi Road — Bedok’s Potential Mega-Development

The New Upper Changi Road site occupies a 331,194 sqft parcel in the Bedok planning area (District 16), a mature residential neighbourhood in Singapore’s eastern region. With a gross plot ratio of 2.8, the site could yield approximately 1,010 residential units — making it one of the largest GLS residential parcels on the 1H 2026 confirmed list. The nearest MRT station is Bedok (East-West Line), a major interchange point in D16 with established amenities including Bedok Mall, Bedok Interchange Hawker Centre, and bus interchange connectivity.

Bedok is a well-established mature estate, home to a large HDB population and a smaller but growing private condominium market. Notable recent transactions in D16 include units at Grandeur Park Residences (TOP 2019, ~S$1,600–2,000 psf) and Coco Palms (~S$1,400–1,700 psf). The New Upper Changi Road site’s OCR location means it will attract primarily HDB-upgrader buyers and Singapore Citizen first-time private buyers, for whom 0% ABSD applies on a first private property purchase. For these buyers, an OCR mass-market entry point (estimated launch price S$1,600–2,000 psf) represents an accessible entry into private property ownership in a mature, well-connected eastern district.

The mega-development scale — if fully realised at 1,010 units — carries both supply and marketing risk. Mega-developments require phased launches over 12–18 months to absorb market demand without undercutting their own prices. Developers who tender for this site will need deep marketing resources and a willingness to sustain a long selling campaign. The 2-year deadline from award to launch (under ABSD developer rules) adds urgency to the tender and project development timeline.

What the Two Sites Mean for the 1H 2026 Supply Programme

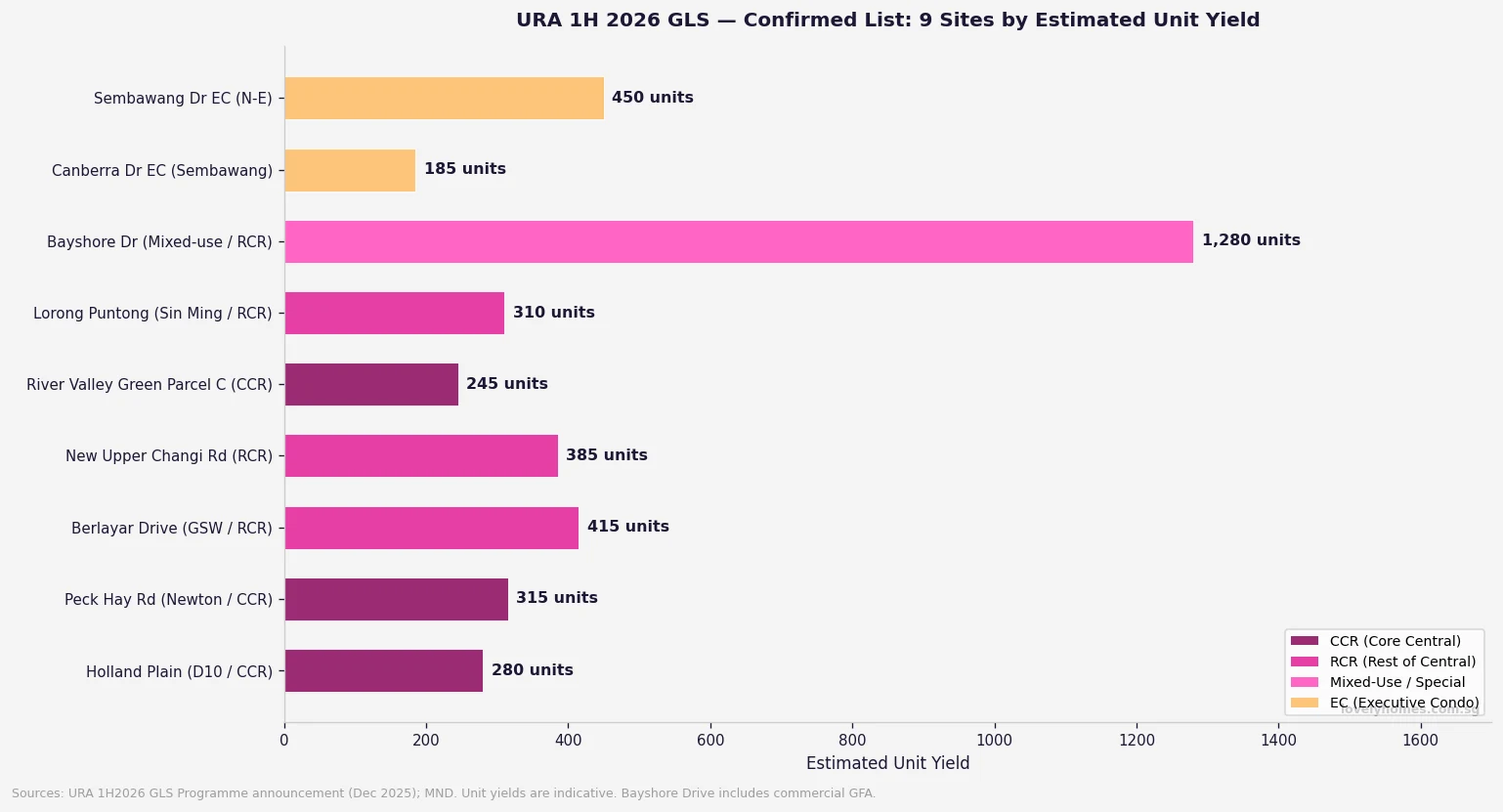

The URA’s 1H 2026 GLS confirmed list includes nine sites in total, with a combined estimated supply of approximately 5,050 private residential units. The two new sites — Berlayar Drive and New Upper Changi Road — account for 1,425 of these units, or roughly 28% of the confirmed list supply for the first half of 2026. Other sites on the confirmed list include Peck Hay Road (D9, ~350 units, tender closing 11 June 2026), River Valley Green Parcel C (D9, ~420 units, closing 18 June 2026), Dunearn Road (D11, ~325 units, already awarded), Holland Plain (D10, ~280 units, awarded to Sim Lian May 2026) and Kallang Close (D12, ~520 units, awarded to Frasers+Mitsubishi April 2026).

The geographic spread of the 1H 2026 sites — D3, D9, D10, D11, D12, D16 — reflects the URA’s deliberate intention to distribute supply across CCR, RCR and OCR markets. Including New Upper Changi Road (D16 OCR) ensures that affordable mass-market units are entering the pipeline, while the concentration of CCR sites (D9, D10, D11) addresses sustained high-end demand from upgraders and investors.

| Site | District | Region | Est. Units | Tender/Award Status | Land Price (psf ppr) |

|---|---|---|---|---|---|

| Holland Plain | D10 | CCR | ~280 | Awarded (May 2026, Sim Lian) | S$1,491 |

| Dunearn Road | D11 | CCR | ~325 | Awarded (Apr 2026) | S$1,250 (est.) |

| Kallang Close | D12 | RCR | ~520 | Awarded (Apr 2026, Frasers) | S$1,415 |

| Peck Hay Road | D9 | CCR | ~350 | Tender closes 11 Jun 2026 | TBD |

| River Valley Green C | D9 | CCR | ~420 | Tender closes 18 Jun 2026 | TBD |

| Berlayar Drive | D3 | RCR | ~415 | Tender closes 4 Aug 2026 | TBD |

| New Upper Changi Road | D16 | OCR | ~1,010 | Tender closes 1 Sep 2026 | TBD |

Buyer and Investor Implications

For prospective buyers, the Berlayar Drive and New Upper Changi Road sites represent future pipeline supply that is unlikely to launch before 2028 in both cases — developers typically require 18–24 months from award to project launch, with construction-to-TOP timelines of an additional 3–4 years. A buyer registering interest in a Berlayar Drive development today would likely see a launch preview in mid-to-late 2027, with TOP potentially in 2031–2032. New Upper Changi Road, being larger and more complex, may launch in late 2027 or 2028 depending on the developer’s phasing strategy.

For investors tracking the pipeline, these two sites confirm that RCR (Berlayar, Kallang) and OCR (New Upper Changi Road) supply is building — which may moderate price growth in those segments beyond 2028 as completions arrive. The CCR, by contrast, has lighter confirmed list supply (Holland Plain and Dunearn Road are relatively small), which may support continued CCR price resilience through 2026–2027 even as OCR and RCR stock accumulates.

The worked example below illustrates what a buyer of a future Berlayar Drive unit might expect in acquisition costs, assuming an indicative launch price of S$2,200 psf for a 850 sqft 2-bedroom unit.

Worked example — Future Berlayar Drive 2-bedroom, est. S$1,870,000:

SC buyer (first private property, after selling HDB). BSD: 1%×S$180k (S$1,800) + 2%×S$180k (S$3,600) + 3%×S$640k (S$19,200) + 4%×S$500k (S$20,000) + 5%×S$370k (S$18,500) = S$63,100 BSD. ABSD: S$0. Bank loan 75% = S$1,402,500 @ 3.0% 25yr = S$6,649/month. TDSR: minimum income S$12,089/month required. Total upfront: S$467,500 downpayment + S$63,100 BSD + S$10,000 legal = est. S$540,600.

What Might Come Next

The immediate pipeline of tender closings is busy through Q3 2026: Peck Hay Road closes 11 June, River Valley Green Parcel C closes 18 June, Berlayar Drive closes 4 August, and New Upper Changi Road closes 1 September. Award announcements typically follow within 2–4 weeks of the tender close, at which point land price benchmarks will be set. If Peck Hay Road and River Valley Green (both D9 CCR) attract strong bids above S$1,500 psf ppr, it would signal continued developer appetite for CCR land despite the 60% foreigner ABSD headwind. If bids are soft (below S$1,200 psf ppr), it may indicate developer caution about CCR demand sustainability at current price levels. LovelyHomes will report on each tender award as results are released by URA.

Frequently Asked Questions

When will the Berlayar Drive and New Upper Changi Road projects launch for sale?

Developer launches are typically 18–24 months after GLS award and subject to planning approvals. Given the Berlayar Drive tender closes 4 August 2026 and award follows approximately 3–4 weeks later, the earliest a developer could realistically launch a Berlayar Drive project would be Q1–Q2 2028, with New Upper Changi Road slightly later given its larger scale. Buyers should register interest directly with developers (via project marketing teams) once the tender is awarded and the developer is publicly known, typically in Q4 2026 for Berlayar Drive.

How does the Greater Southern Waterfront affect Berlayar Drive’s investment case?

The Greater Southern Waterfront (GSW) transformation is one of Singapore’s most significant long-term urban projects — it will eventually create new residential, commercial and recreational precincts across a 30km southern coastal corridor. In the near term (2026–2028), the primary catalyst for Berlayar Drive is proximity to the Southern Ridges, Telok Blangah MRT (CC29) and the nascent Berlayar estate identity rather than operational GSW amenities, which remain years away. Longer term (2030+), as Keppel Terminal land is repurposed and waterfront promenades connect Sentosa to Marina East, Berlayar Drive’s capital appreciation could benefit significantly. Buyers should view GSW as a long-horizon catalyst, not a near-term price driver.

Is the New Upper Changi Road site a good investment given its mega-development scale?

Mega-developments (1,000+ units) in Singapore carry specific risks and benefits. On the risk side: a large supply of similar units in one development creates internal price competition during resale, especially when multiple sellers list simultaneously post-MOP. On the benefit side: mega-developments attract developer marketing resources, typically feature comprehensive facilities, and benefit from economies of scale in management fees. For owner-occupiers in Bedok seeking a large community and established facilities, the New Upper Changi Road project may be highly attractive. For investors focused on rental or capital gain, smaller boutique developments in the same area may offer tighter supply dynamics post-TOP.

Who can buy these properties once they launch — are there foreign buyer restrictions?

Both sites are non-landed residential developments and may be purchased by Singapore Citizens, Permanent Residents and foreigners subject to the applicable stamp duties. Singapore Citizens buying their first private property pay BSD only (0% ABSD). PRs pay 5% ABSD on a first property. Foreigners pay 60% ABSD on all residential property. There are no additional restrictions specific to the Berlayar Drive or New Upper Changi Road locations beyond these standard rules. GCB areas and landed housing restrictions do not apply to apartment/condominium developments.

How do I track when developers register interest for Berlayar Drive and New Upper Changi Road?

Once a developer is awarded a GLS site, they typically announce a sales gallery opening and register-interest campaign within 6–12 months of award. LovelyHomes will publish updates as each tender is awarded. You can also monitor URA’s website (ura.gov.sg), the respective developer’s official website (once known), and property portals such as PropertyGuru and 99.co, which aggregate new launch previews. Alternatively, a CEA-registered property agent can notify you directly when the developer’s marketing team begins collecting expressions of interest.

Related Articles

- Jurong Lake District Property Outlook 2026: Singapore’s Next Commercial Hub

- Stamp Duty Calculator Singapore 2026: BSD and ABSD Complete Guide

- Holland Plain GLS 2026: Sim Lian Wins at S$1,491 psf ppr — D10 CCR Pricing and Investment Outlook

- Singapore Prime District Property Guide 2026: D9, D10 and D11 Complete Buyer’s Guide

- Singapore Developer Penalties 2026: New GLS Disqualification and Sales Suspension Framework

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer

This article is for general informational purposes only. All unit yield estimates are projections based on site area and GPR and actual development plans will be determined by the awarded developer subject to URA’s planning approval. Land price forecasts are market speculation and may differ materially from actual tender results. Nothing in this article constitutes investment or financial advice. Readers should conduct independent due diligence and consult licensed advisers before making any property decisions. Official information about these GLS sites is available at ura.gov.sg.