Quick Answer — Foreign Property Investment from Singapore (2026)

- Singapore Citizens and PRs CAN buy overseas property, but ABSD still applies on their Singapore-side property count — buying a Malaysia condo counts as a second property if you already own a Singapore home.

- CPF Ordinary Account funds cannot be used for overseas property. All payments must be in cash or via a Singapore bank loan.

- Rental income from overseas property is taxable in Singapore under IRAS rules, even if the income is not remitted to Singapore.

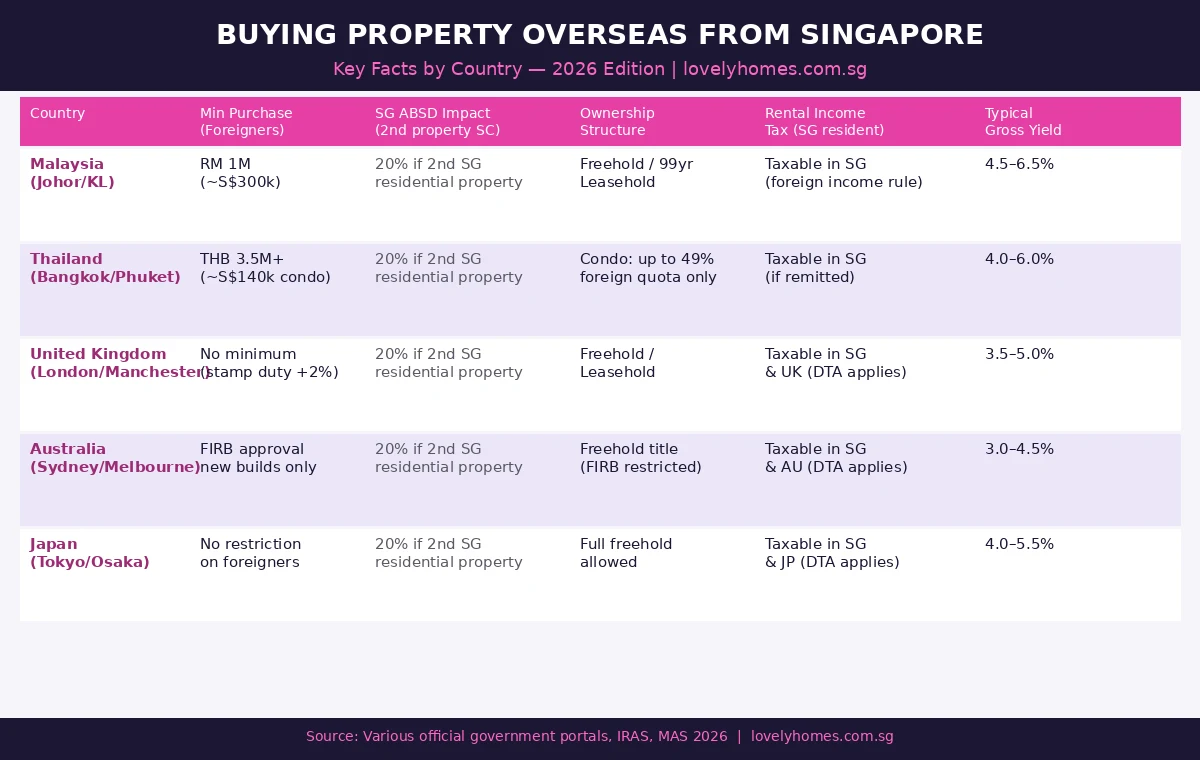

- Popular destinations for Singapore investors: Malaysia (Johor, KL), Thailand (Bangkok, Phuket), UK (London, Manchester), Australia (Sydney, Melbourne), Japan (Tokyo, Osaka).

- Malaysia offers the lowest entry price (from RM 1 million for foreigners); Japan has no foreign ownership restrictions; Australia restricts foreigners to new builds only.

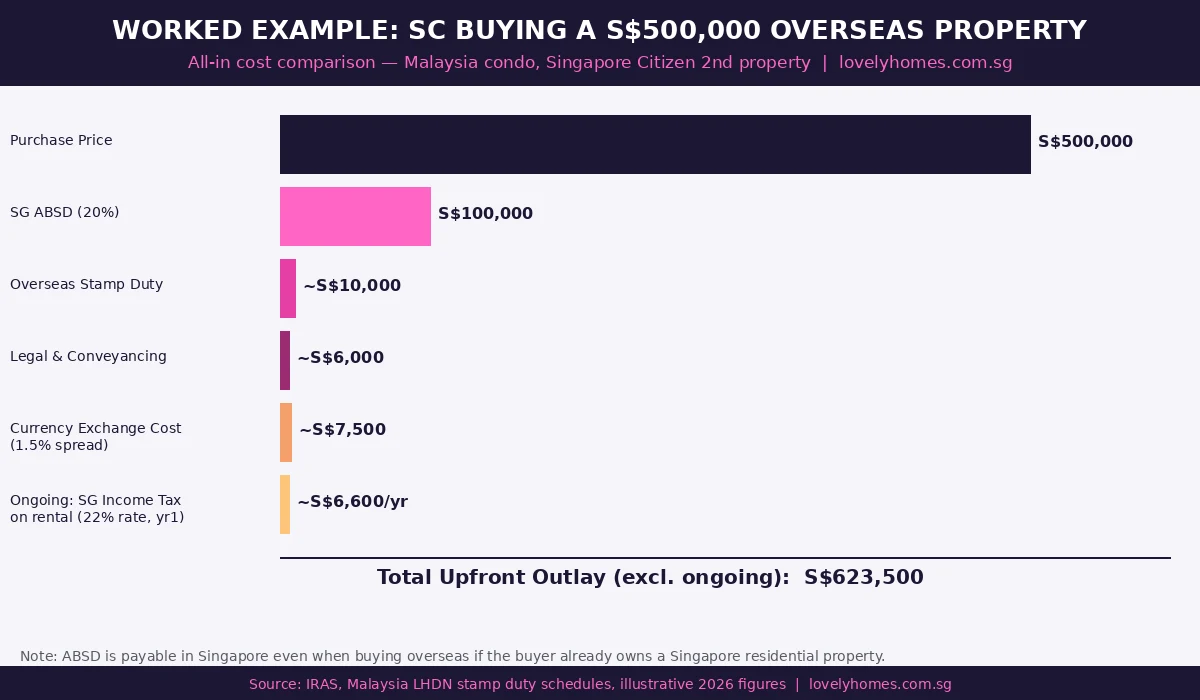

- A Singapore Citizen buying a S$500,000 overseas property as a second property faces total upfront costs exceeding S$623,000 once ABSD, stamp duties, legal fees and currency costs are included.

- Double Taxation Agreements (DTAs) with UK, Australia and Japan reduce the risk of being taxed twice on rental income.

For many Singapore investors, the appeal of overseas property is clear: lower entry prices, higher gross yields, and the ability to diversify a portfolio beyond the Singapore market. A freehold Tokyo apartment at S$250,000, a Johor Bahru condo at RM 800,000 (~S$240,000), or a Manchester studio at £120,000 (~S$210,000) look attractive when Singapore OCR condos routinely trade above S$1.5 million.

But overseas property investing from Singapore is far more complicated than buying locally. The Additional Buyer’s Stamp Duty (ABSD) that applies to a second Singapore property also applies to your Singapore property count — your overseas purchase does not “reset” your ABSD obligations. You cannot use CPF. Rental income is taxable here regardless of where it is earned. And legal frameworks, title structures, and foreign ownership rules vary enormously from country to country.

This guide walks through every major destination market, the Singapore tax and regulatory considerations, how to structure an overseas purchase, and the full cost mathematics — so you can make an informed decision.

1. Does ABSD Apply When You Buy Overseas Property?

This is the most commonly misunderstood question in overseas property investing. The answer: ABSD does not apply to the overseas property itself (that would be a foreign transaction outside Singapore’s jurisdiction), but it applies to any future Singapore property purchase you make, because your overseas residential property counts towards your Singapore property tally for ABSD purposes.

Specifically, the IRAS and SLA count all residential properties owned globally when determining your ABSD rate on a Singapore purchase. If you own a Malaysia condo and then buy a Singapore condo, you pay 20% ABSD as a Singapore Citizen (2nd property rate), not 0%. Your overseas property is not exempted from the count.

The reverse does not apply: buying an overseas property when you already own a Singapore property does not trigger Singapore ABSD on the overseas transaction. But it does mean any future Singapore purchase will be at a higher ABSD rate. For a comprehensive breakdown of ABSD rates and the remission regime, see our ABSD Singapore 2026 Complete Guide.

2. CPF Rules: No Overseas Exemption

The CPF Board’s position is unambiguous: CPF Ordinary Account (OA) savings may not be used for the purchase of properties situated outside Singapore. This rule applies regardless of whether you are buying in Malaysia, Australia, or anywhere else. There is no appeal pathway or ministerial exemption for private individuals.

This has significant financial implications. Unlike a Singapore private property purchase — where CPF OA can fund the down payment and ongoing monthly instalments — an overseas purchase requires:

- A full cash down payment (typically 10–30% depending on the country and lender).

- Either a cash mortgage with a Singapore bank (subject to their overseas property lending policies) or a local overseas mortgage in the destination country.

- All ongoing instalments paid in cash or via bank debit — no CPF top-ups.

Singapore banks (DBS, OCBC, UOB) do offer overseas property loans for selected markets (primarily Malaysia, UK, Australia and some ASEAN countries), but the loan-to-value (LTV) ceiling is typically 60–70% for overseas properties, lower than the 75% available for Singapore private homes. The Singapore home loan comparison guide explains local LTV and TDSR rules in detail — overseas loans follow different parameters.

One related point: if you later sell the overseas property and repatriate the proceeds to Singapore, those funds are generally free from Singapore capital gains tax (Singapore does not levy CGT on most investment property disposals). Our Capital Gains and Rental Tax guide covers the full picture.

3. Rental Income from Overseas Property: Taxable in Singapore

Many investors assume that because the rental income is earned abroad and kept in a foreign bank account, it is not taxable in Singapore. This assumption is incorrect.

Under IRAS rules, a Singapore tax resident is taxable on income derived from overseas property if:

- The income is received in Singapore (remitted), or

- From 1 January 2024 onwards, the income is derived from a foreign property held for investment purposes — even if not remitted, under the expanded foreign-sourced income rules that took effect for investment income.

In practice, this means rental income from your Malaysia condo, Thai apartment, or UK flat is likely taxable in Singapore at your marginal income tax rate. For a Singapore tax resident earning a combined income of S$120,000 per year plus S$30,000 in overseas rental income, that rental income could be taxed at 11.5%–15% depending on the total income tier.

However, Double Taxation Agreements (DTAs) between Singapore and several countries allow you to offset taxes already paid abroad against your Singapore liability. Singapore has DTAs with Australia, the UK, Japan, and numerous ASEAN countries. The DTA generally provides relief so you are not fully double-taxed — you pay the higher of the two countries’ rates, not both in full.

Crucially, Singapore has no DTA with Thailand, which means rental income from Thailand may be subject to both Thai withholding tax and Singapore income tax without the same credit offset. Investors should seek advice from a Singapore-registered tax consultant before investing in Thailand property specifically for rental purposes.

4. Country-by-Country Guide

Malaysia (Most Popular Destination)

Malaysia remains the top overseas market for Singapore investors, driven by geographic proximity, a shared cultural context, Ringgit-SGD familiarity, and relatively low entry prices. The minimum purchase price for foreigners was raised to RM 1 million in most states (Johor: RM 1 million; KL: varies by zone; Penang: RM 1 million on the island).

Key considerations: foreign ownership is allowed in most property categories except agricultural and Malay Reserved Land; the MM2H visa programme provides a long-stay option for investors; property appreciation in Johor (especially Iskandar Malaysia) has been boosted by the Johor-Singapore Special Economic Zone (JS-SEZ) announced in 2024 and ongoing infrastructure investment. Stamp duty in Malaysia for buyers is approximately 1–3% on a tiered basis.

Thailand (High Yield, Restricted Title)

Thailand offers some of the highest gross yields in Southeast Asia (4–6% in Bangkok, 5–8% in Phuket for short-term rental), but foreign ownership is restricted to condominium units in buildings where foreigners hold no more than 49% of total floor area. Foreigners cannot own land; villa purchases must be structured through long-term leasehold arrangements (30+30+30 years) or a Thai company, both of which carry legal risk.

The Thailand Elite Visa (now restructured as the Privilege Entry Visa) provides long-stay access. Thai rental income is subject to withholding tax at 15% for non-residents. As noted, Singapore has no DTA with Thailand.

United Kingdom (Established Market, High Transaction Costs)

The UK remains popular for its transparent legal system, deep rental market, and English-language familiarity. Foreign buyers pay an additional 2% Stamp Duty Land Tax (SDLT) surcharge on top of the standard rates, plus the non-resident SDLT surcharge introduced in 2021. On a £500,000 (≈S$860,000) London flat, total SDLT for a non-UK-resident buyer can reach £37,500 (≈S$64,500). UK rental income is taxed in the UK at 20% basic rate (or higher) for non-UK residents under the Non-Resident Landlord scheme; the UK–Singapore DTA then reduces your Singapore liability accordingly.

Australia (New-Builds Only for Foreigners)

The Foreign Investment Review Board (FIRB) restricts foreign buyers (non-Australian residents) to purchasing new residential property or vacant land only — existing dwellings are off-limits. FIRB approval fees start from A$14,100 (≈S$13,000) for properties up to A$1 million. Australian states levy additional foreign buyer surcharges on stamp duty (e.g., 8% in Victoria, 8% in NSW). Australian rental income is taxable in Australia; the Australia–Singapore DTA provides relief against double Singapore taxation.

Japan (No Restrictions, Unique Risks)

Japan is unique: foreigners may purchase property freely, including freehold land. Tokyo and Osaka condominiums can be acquired for S$250,000–S$600,000 with gross yields of 4–5.5% in central districts. However, Japan carries distinct risks: a declining population in regional areas; earthquake risk; high property management costs (10–15% of rental income typically charged by local management firms); and Japan’s inheritance tax, which applies to assets held in Japan by non-residents at rates up to 55%. Legal and notarial processes are entirely in Japanese, requiring a bilingual agent and solicitor.

5. Financing Your Overseas Purchase

As noted, CPF cannot be used. Your financing options are:

| Financing Route | Pros | Cons |

|---|---|---|

| Singapore bank overseas loan (DBS, OCBC, UOB) | SGD-denominated; familiar process; no currency mismatch on loan repayment | LTV typically 60–70%; limited to selected markets; stricter eligibility for overseas collateral |

| Local overseas mortgage | Higher LTV often available; local currency reduces exchange risk for rental income offset | Foreign legal process; language barrier; may require local credit history; exchange risk on SGD repayment |

| Cash purchase | No interest cost; fastest completion; no TDSR or MSR concerns | Locks up significant capital; higher opportunity cost; no leverage amplification |

| CPF Investment Scheme (CPFIS) via equity | Indirectly access property-linked returns via S-REITs using CPFIS-OA | Not actual property ownership; lower yield than direct property; market risk |

For Singapore-bank overseas loans, the Total Debt Servicing Ratio (TDSR) of 55% still applies to the borrower’s Singapore income and total obligations. An overseas property mortgage counts towards your TDSR, potentially limiting your ability to finance a future Singapore property purchase.

6. Structuring the Purchase: Direct vs. Corporate Ownership

Some investors purchase overseas property through a Singapore holding company or a foreign special-purpose vehicle (SPV). Corporate ownership can offer certain advantages — limiting personal liability, facilitating estate planning, and potentially accessing business deductions — but also carries significant downsides:

- Corporate stamp duty surcharges apply in many countries (e.g., Malaysia’s RPGT applies differently to companies; UK imposes a 15% SDLT surcharge on “dwellings purchased by certain non-natural persons”).

- Increased ongoing compliance costs: annual returns, corporate tax filings, audit requirements.

- Banks are generally less willing to extend mortgage financing to SPVs, especially for residential property.

For most individual Singapore investors purchasing one or two overseas properties, direct personal ownership remains the most straightforward structure. Corporate ownership is worth exploring only when the portfolio exceeds 3–5 properties or when estate planning complexity demands it.

7. Six Key Risks You Must Manage

8. Worked Example: Mr Lee, SC, Buys a Johor Bahru Condo

Mr Lee (40, Singapore Citizen) already owns a S$900,000 Tampines HDB resale flat. He wants to buy a RM 1.2 million (~S$360,000 at RM 3.30/SGD) freehold condo in Iskandar Puteri, Johor Bahru, for rental income.

Singapore-side ABSD assessment: Mr Lee already owns one Singapore residential property. His JB condo counts as a residential property globally. If Mr Lee later purchases another Singapore property, ABSD is assessed at the 2nd (or 3rd) property rate at that time. The JB purchase itself does not trigger Singapore ABSD.

Total cost of the JB purchase:

- Purchase price: RM 1.2 million (S$363,636)

- Malaysia stamp duty (tiered): approximately RM 18,000 (S$5,455)

- Legal fees (Malaysia & Singapore solicitors): approximately S$8,000

- Currency conversion cost (1.5% spread): approximately S$5,450

- Down payment (30% LTV for overseas mortgage via Singapore bank): S$109,000 cash

- Bank arrangement fee: S$2,500

- Total out-of-pocket at purchase: approximately S$130,000 cash

Monthly rental income: RM 3,500/month (~S$1,061). Annual gross rental: ~S$12,730. Singapore gross rental yield: ~3.5% on S$363,636 price. After Malaysian property management fees (8%), net Malaysian income: ~S$11,700. IRAS assessment (Singapore resident, marginal rate assumed 9%): approximately S$1,053/yr in Singapore income tax on rental income.

What might change: If the Ringgit weakens by 10% against SGD (RM 3.30 → RM 3.63), Mr Lee’s rental income falls to ~S$964/month, reducing yield to ~3.2%. His S$363,636 property would now be valued at S$330,579 in SGD terms — a 9% capital loss without any change in Malaysian market price. Currency risk is the single largest unhedged variable in Malaysia property investing.

9. Comparison: Overseas Property vs. Singapore S-REIT

For investors with S$250,000–S$500,000 to deploy, the alternative to overseas physical property is a Singapore-listed Real Estate Investment Trust (S-REIT) with overseas exposure. Our S-REITs vs Property Investment guide covers this in detail, but the key trade-offs are:

- S-REITs offer immediate liquidity (SGX-listed; sell in minutes vs. 6–18 months for overseas property).

- S-REITs distribute at least 90% of taxable income as dividends; distributions to Singapore residents from qualifying REITs are exempt from Singapore income tax.

- Physical overseas property allows leverage (mortgage amplification), capital gain optionality, and tangible asset ownership.

- S-REITs offer diversified exposure across dozens of assets; physical property is concentrated in one unit, one building, one market.

10. What Might Come Next

Several trends are worth watching for Singapore overseas property investors in 2026 and beyond. The Johor-Singapore Special Economic Zone (JS-SEZ) is expected to accelerate infrastructure investment in Johor, potentially supporting JB property values as cross-border workers increase. In Australia, the FIRB rules have come under review as the Federal Government balances housing affordability concerns against foreign investment appetite — further restrictions on foreign buyers of new builds are possible. In the UK, the Renters’ Rights Act 2024 has introduced new landlord obligations that increase management complexity for overseas landlords letting to UK tenants.

From a Singapore tax perspective, IRAS continues to monitor overseas income reporting. Investors who have historically relied on the assumption that unrepatriated overseas rental income is non-taxable should review their position against IRAS’s published guidance on the expanded foreign-sourced income rules.

FAQ: Foreign Property Investment Singapore 2026

Does ABSD apply if I buy an overseas property?

ABSD does not apply to the overseas transaction itself — Singapore cannot levy stamp duty on a foreign property purchase. However, your overseas residential property is counted as part of your global residential property portfolio for ABSD purposes. This means any future Singapore residential property purchase you make will be assessed at the appropriate ABSD rate based on your total property count (including overseas properties). A Singapore Citizen who owns a Malaysia condo buying a Singapore condo pays 20% ABSD (2nd property rate).

Can I use CPF to buy an overseas property?

No. The CPF Board does not permit the use of CPF Ordinary Account savings for any property located outside Singapore. This applies to the down payment, legal fees, stamp duties, and all ongoing mortgage instalments. The only way CPF could be indirectly involved is through CPFIS (CPF Investment Scheme), which permits investment in certain unit trusts and REITs — but this is not direct property ownership. For overseas property, you must use cash or a bank loan.

Is rental income from an overseas property taxable in Singapore?

Yes. IRAS taxes Singapore tax residents on overseas rental income, including income that is not remitted to Singapore. The expanded foreign-sourced income rules that took effect from 1 January 2024 mean investment income (including rental income from foreign property) is taxable on an arising basis for Singapore residents. Double Taxation Agreements with countries such as the UK, Australia, and Japan reduce the risk of being fully taxed twice, but you cannot assume the income escapes Singapore tax entirely. Keep good records of foreign taxes paid to claim the DTA credit.

Can foreigners buy freehold land in Thailand or Australia?

No on both counts. In Thailand, foreigners cannot own freehold land. They can own a condominium unit (subject to the 49% foreign quota per building) on a freehold basis, but any villa or house must be structured via long-term leasehold or a Thai company — both carry legal risks. In Australia, the Foreign Investment Review Board (FIRB) restricts non-resident foreigners to purchasing new residential dwellings or vacant land only; purchasing existing established homes is not permitted. FIRB approval fees and state-level foreign buyer surcharges add significantly to the acquisition cost.

What is the minimum budget to buy property in Malaysia as a Singaporean?

Most Malaysian states have set a minimum purchase price of RM 1 million (approximately S$300,000–S$310,000 at current exchange rates) for foreign buyers. This applies to Johor Bahru and Kuala Lumpur. Penang island properties have a similar RM 1 million threshold for foreigners purchasing in certain zones. Some states have lower thresholds for commercial properties or in specific approved zones. You should verify the current threshold with a Malaysia-licensed solicitor before proceeding, as state-level rules can change.

Does an overseas property affect my eligibility for HDB housing in Singapore?

Yes, potentially. Under HDB rules, Singapore Citizens and PRs applying for HDB flats (BTO, SBF, or resale) must satisfy eligibility conditions including the Non-Concurrent Ownership rule. Owning an overseas residential property may affect your eligibility status or first-timer classification, depending on the HDB scheme. Specifically, if you own or have an interest in any private property (which HDB treats as including overseas private residential properties in some schemes), a waiting period or eligibility restriction may apply. Confirm with HDB directly before applying if you have an overseas property interest.

What professional advice do I need before buying overseas?

At minimum, you should engage: a Singapore-licensed conveyancing solicitor familiar with overseas property transactions; a qualified accountant or tax adviser with IRAS expertise in overseas income rules and applicable DTA provisions; a licensed solicitor or notary in the destination country; and a reputable property manager in the overseas market. For markets like Japan or Thailand, a bilingual agent is essential. Avoid relying solely on the developer’s appointed solicitor, as their interests are aligned with the vendor.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Rental Yield Singapore 2026: Gross, Net and Location-Adjusted Yields

- Capital Gains and Rental Income Tax Singapore 2026

- Singapore REITs vs Direct Property Investment 2026

- TDSR Singapore 2026: How the 55% Cap and 4.0% Stress Test Work

- Home Loan Comparison Singapore 2026: HDB Loan, Fixed vs Floating and SORA

- CPF Accrued Interest and Property Sales Singapore 2026

- Conservation Shophouses Singapore 2026: Buying, Restoring and Investing

Disclaimer

This article is for general informational purposes only and does not constitute financial, tax, legal, or investment advice. Overseas property investment involves significant risks including but not limited to currency risk, legal title risk, and changes to foreign ownership regulations. Singapore and overseas tax laws change periodically — always verify current rules with IRAS (iras.gov.sg), the CPF Board (cpf.gov.sg), and the regulatory authorities in the destination country. Consult a Singapore-licensed solicitor and a qualified tax professional before proceeding with any overseas property transaction. LovelyHomes.com.sg does not endorse any specific overseas property or developer.

0 Comments