Singapore Property Tax Guide 2026: IRAS Annual Value, Owner-Occupied Rates and How to Pay

⚡ Quick Answer: Singapore Property Tax 2026

- Administered by: IRAS (Inland Revenue Authority of Singapore) — not URA, not HDB.

- Based on Annual Value (AV): Property tax is charged on the AV of your property — the estimated annual market rent — not on the purchase price or the outstanding mortgage.

- Two rate schedules: Owner-Occupied (OO) rates are significantly lower and progressive; Non-Owner-Occupied (NOO) rates are higher and apply to all investment properties, vacant units, and rented-out homes.

- HDB flats included: All property owners — HDB flat owners included — pay property tax. However, most HDB flats have low AVs and benefit from the 0% OO tier on the first S$8,000.

- Paid annually: IRAS issues property tax bills in January each year, payable by 31 January. GIRO instalments are available.

- AV is IRAS’s estimate: IRAS reviews AVs periodically based on market rental data. You may object to your AV if you believe it is too high.

- Commercial property: Non-residential property (offices, shops, industrial) is taxed at a flat 10% on AV — not the progressive residential schedule.

What Is Property Tax in Singapore?

Property tax is an annual tax levied by the Singapore Government on all property owners — whether the property is owner-occupied, rented out, or vacant. It is administered by the Inland Revenue Authority of Singapore (IRAS) under the Property Tax Act (Cap. 254). Property tax is distinct from income tax, stamp duty, and Goods and Services Tax, though all may apply to property-related transactions.

The key distinction that most buyers and owners misunderstand is that property tax is not a tax on rental income or on capital gains — it is a tax on the right to own a property in Singapore, computed against the property’s Annual Value (AV). It does not matter whether you are currently receiving rental income: if you own a property that sits empty, IRAS still levies property tax at the higher Non-Owner-Occupied (NOO) rate unless you have formally declared the property as your own residence.

Every property owner in Singapore — from the owner of a humble 2-room HDB flat to the holder of a Good Class Bungalow (GCB) in District 10 — receives a property tax bill from IRAS each January. For most HDB owner-occupiers, the annual bill is relatively modest. For high-value investment properties, it can run into tens of thousands of dollars.

Understanding property tax matters for several reasons: it affects the true cost of ownership, it influences net rental yield calculations, and it is a recurring holding cost that does not diminish with time the way a mortgage does.

What Is Annual Value (AV) and How Does IRAS Calculate It?

The Annual Value (AV) of a property is IRAS’s estimate of the gross annual rent the property would fetch if it were rented out on the open market for a year, exclusive of furniture and maintenance. This is not based on what you actually receive in rent (or what you would receive if you rented it out) — it is IRAS’s independent assessment of market rental value, derived from rental transaction data for comparable properties.

IRAS reviews AVs periodically — typically when there are significant changes in the rental market — and updates them to reflect current conditions. The 2022–2023 rental surge in Singapore, which pushed private condo rents up by 30–40% in some segments, triggered widespread AV reviews and upward revisions, which in turn increased property tax bills for many owners.

How IRAS Arrives at the AV

IRAS uses three main reference points when assessing AV: (1) actual rental transactions for comparable properties in the same area and building type, sourced from rental contracts stamped with IRAS; (2) URA rental statistics for private residential properties by district and property type; and (3) HDB rental data for public housing. For unique properties such as landed homes and GCBs, IRAS may use direct comparisons with known rental transactions for nearby similar properties.

If your property has never been rented — for example, you bought a new condo and moved in immediately — IRAS will estimate the AV by reference to rents achieved by comparable units in the same development or comparable developments nearby.

Owner-Occupied (OO) vs Non-Owner-Occupied (NOO)

The most important variable in your property tax calculation is whether the property is classified as owner-occupied. If you live in the property as your principal place of residence, you pay the lower, progressive OO rates. All other residential properties — rented out, left vacant, or used as a secondary home — are taxed at the higher NOO rates.

Only one property may be declared OO. If you own two residential properties, one must be NOO. You notify IRAS of your OO status by filing an OO declaration; failure to do so defaults the property to the NOO rate. If your circumstances change — for example, you move out and rent the property — you must update IRAS within 30 days.

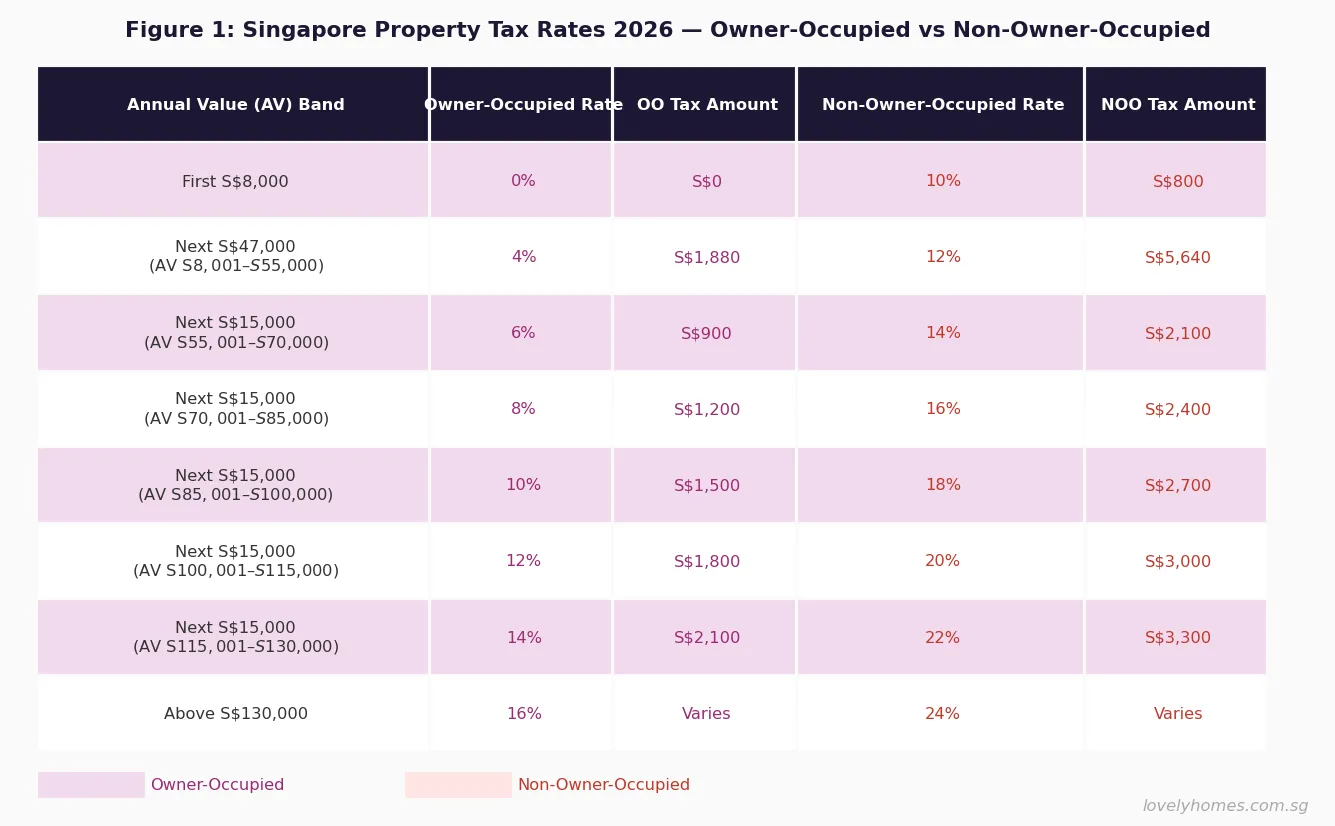

Singapore Property Tax Rates 2026

Singapore uses a progressive property tax rate system for residential property. As the AV increases, higher tiers of AV are taxed at higher rates. The OO schedule is significantly more generous than the NOO schedule, reflecting the Government’s intent to support owner-occupiers while taxing investment and rental properties more heavily.

Note: The rates below represent the progressive schedule as applied to residential property. Always verify the current year’s exact rates with IRAS at iras.gov.sg, as rates are subject to revision.

| Annual Value Band | OO Rate (%) | OO Tax on Band | NOO Rate (%) | NOO Tax on Band |

|---|---|---|---|---|

| First S$8,000 | 0% | S$0 | 10% | S$800 |

| Next S$47,000 (AV S$8,001–S$55,000) | 4% | S$1,880 | 12% | S$5,640 |

| Next S$15,000 (AV S$55,001–S$70,000) | 6% | S$900 | 14% | S$2,100 |

| Next S$15,000 (AV S$70,001–S$85,000) | 8% | S$1,200 | 16% | S$2,400 |

| Next S$15,000 (AV S$85,001–S$100,000) | 10% | S$1,500 | 18% | S$2,700 |

| Next S$15,000 (AV S$100,001–S$115,000) | 12% | S$1,800 | 20% | S$3,000 |

| Next S$15,000 (AV S$115,001–S$130,000) | 14% | S$2,100 | 22% | S$3,300 |

| Above S$130,000 | 16% | Proportional | 24% | Proportional |

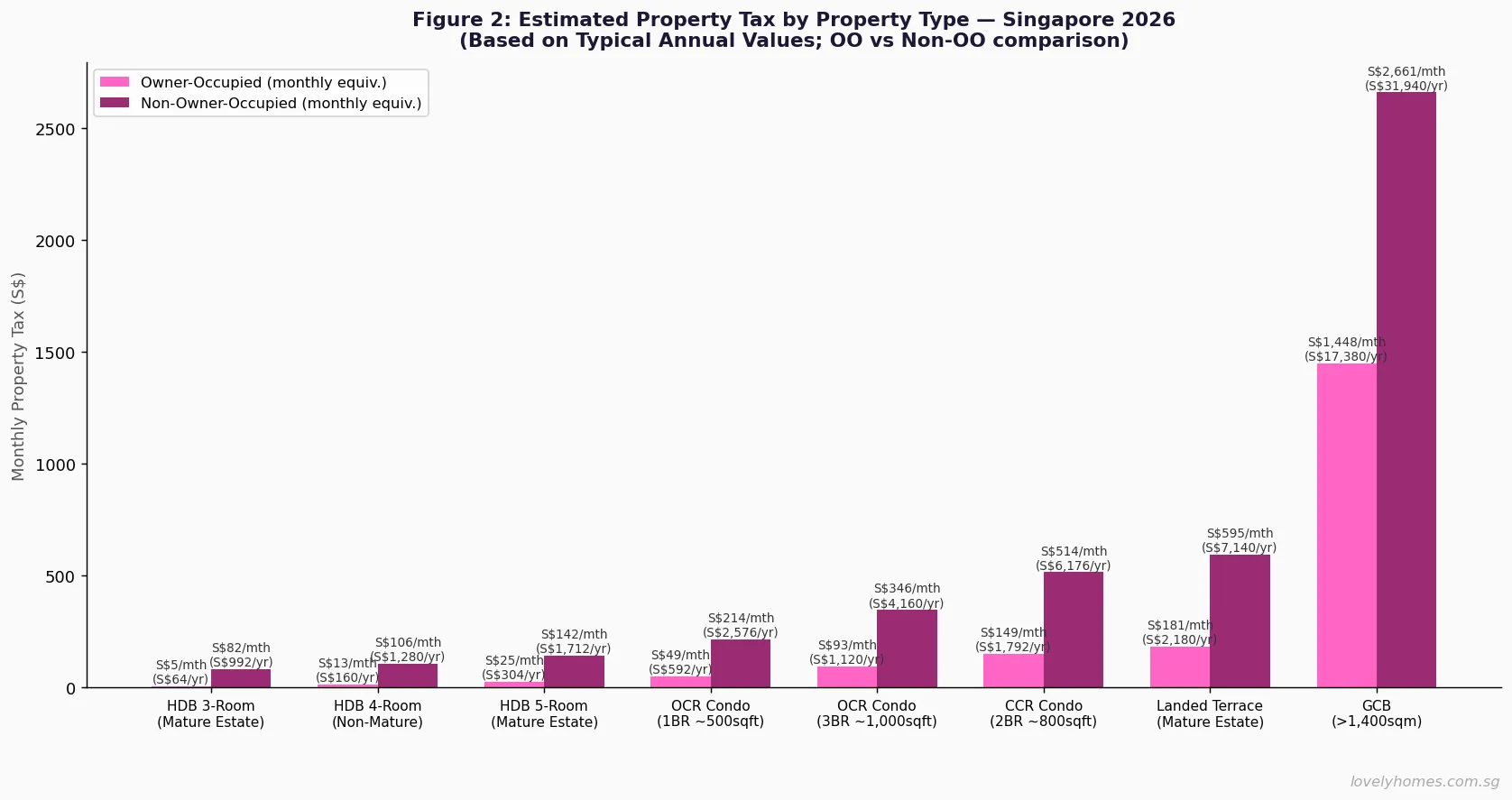

The progressive structure means you do not pay the top rate on your entire AV — only on the portion that falls within each band. An HDB 4-room flat with a typical AV of S$12,000 pays 0% on the first S$8,000 and 4% on the remaining S$4,000, totalling S$160 per year in property tax if owner-occupied — less than S$14 per month.

How to Check Your Property’s Annual Value

IRAS publishes each property’s AV in the annual property tax bill sent each January. You can also check your AV anytime via the IRAS myTax Portal at mytax.iras.gov.sg — log in with your Singpass and navigate to “Property Tax” to view the current AV, rate applied, and tax amount for any property you own.

The AV is not the same as the purchase price, the valuation for bank loan purposes, or the market value of the property. It is specifically the rental-equivalent estimate. As a rough rule of thumb, the AV of private residential property is often around 2.5–4.0% of market value, reflecting rental yields in the broader market. For a condo valued at S$1.5 million yielding 3.2% gross, the AV would be approximately S$48,000.

Investment Properties and the Non-Owner-Occupied Rate

For property investors, the NOO property tax rate is a significant recurring cost that must be factored into yield calculations. On a private condo with an AV of S$40,000 — consistent with a mid-tier OCR 2-bedroom unit — the annual property tax at the NOO schedule amounts to approximately S$4,640 per year. On an AV of S$60,000 (a larger OCR or mid-CCR unit), the annual NOO tax rises to approximately S$8,040.

This cost is tax-deductible against rental income for income tax purposes if the property is genuinely rented out and declared as rental income under IRAS’s income tax framework. Investors should factor property tax, maintenance fees, sinking fund contributions, insurance, and depreciation into their true net yield calculations — gross rental yield does not reflect these holding costs.

If you own two or more residential properties, your second property will always be taxed at the NOO rate regardless of whether it is rented out. There is no provision to designate a second property as OO. Planning the sequence of property ownership — particularly for HDB upgraders moving to private property — requires careful thought about the tax implications of continuing to hold the HDB while buying private.

How to Pay Your Singapore Property Tax

IRAS issues property tax bills in January each year, covering the period from 1 January to 31 December. Payment is due by 31 January. Late payment attracts a 5% penalty on the outstanding amount, and further penalties may apply for continued non-payment.

Payment methods accepted by IRAS include: GIRO (the recommended method — set up once and IRAS auto-debits monthly instalments or annually); PayNow (via Singpass, referencing the IRAS tax reference); internet banking (using IRAS’s provided bill reference); and AXS stations for cash payments. CPF cannot be used to pay property tax — it must be paid in cash.

Worked Example: Property Tax for an HDB and a Private Condo

Scenario A — Owner-Occupied HDB 4-Room Flat (Tampines, AV S$12,000)

Annual Value: S$12,000. Owner-Occupied declaration filed. Tax computation:

- First S$8,000 @ 0% = S$0

- Next S$4,000 @ 4% = S$160

- Total annual property tax: S$160 (approx. S$13 per month)

Scenario B — OCR Condo, 2BR, Owner-Occupied (AV S$30,000)

- First S$8,000 @ 0% = S$0

- Next S$22,000 @ 4% = S$880

- Total annual property tax: S$880 (approx. S$73 per month)

Scenario C — Same OCR Condo Rented Out (NOO Rate, AV S$30,000)

- First S$8,000 @ 10% = S$800

- Next S$22,000 @ 12% = S$2,640

- Total annual property tax: S$3,440 (approx. S$287 per month)

The difference between owner-occupied and non-owner-occupied on the same S$30,000 AV condo is S$2,560 per year — a meaningful recurring cost for investors. At a monthly rent of S$3,500, this property tax alone reduces the effective net monthly income by S$213 per month (before maintenance fees, income tax, and other costs).

Scenario D — CCR Condo Investment Property (AV S$60,000, NOO)

- First S$8,000 @ 10% = S$800

- Next S$47,000 @ 12% = S$5,640

- Next S$5,000 @ 14% = S$700

- Total annual property tax: S$7,140 (approx. S$595 per month)

How Singapore Property Tax Has Evolved — And Why It Matters

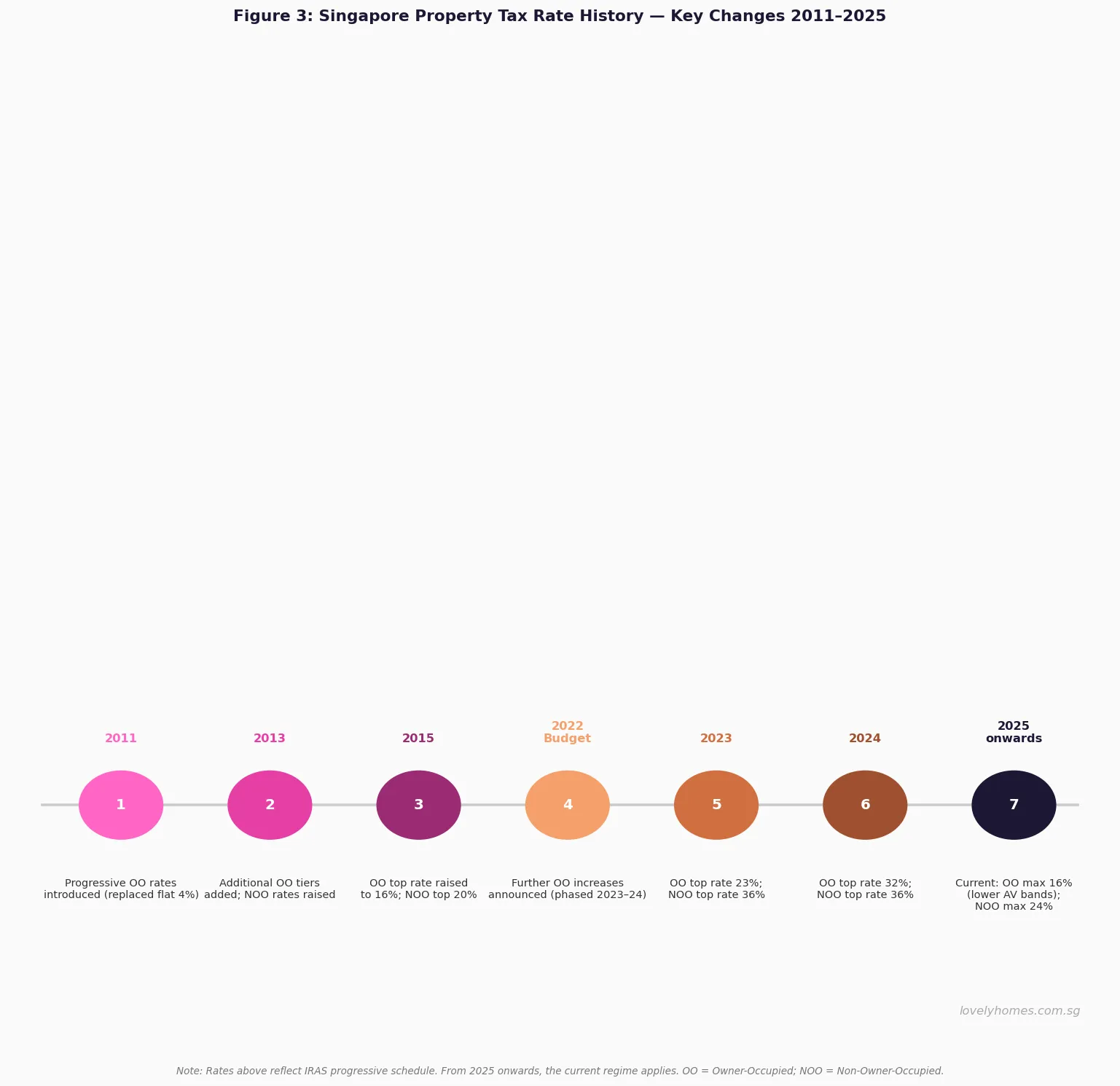

Singapore introduced progressive owner-occupied property tax rates in 2011, replacing a flat rate that had applied for decades. The shift reflected a recognition that a flat rate was regressive — owners of high-value properties in prime districts were paying the same percentage rate as HDB flat owners. The progressive structure effectively subsidises modest owner-occupiers while placing a heavier burden on high-value residential holdings.

The 2022 Budget took this further, announcing phased increases to property tax rates for higher-value residential property (both OO and NOO) effective from 2023 and 2024. The stated rationale was to make the property tax regime more progressive and to fund Singapore’s social expenditure needs. The changes had the most significant impact on owners of private property in the CCR and GCB areas, where AV levels frequently exceed S$100,000.

Compared internationally, Singapore’s property tax rates remain moderate. Hong Kong’s rates are typically 5% of assessable rent (a rate applied to actual rent, not an official AV). Australia’s state-based land taxes vary but are broadly comparable. The UK’s Council Tax is a flat charge by property band — arguably less progressive than Singapore’s AV-based system.

Property Tax Rebates and Reliefs

IRAS has periodically granted property tax rebates to help owner-occupiers manage their tax bills during periods of high AV or economic stress. The Government has in the past granted rebates to HDB flat owners, typically covering 20–60% of the OO property tax bill for HDB flats during COVID years and periods of elevated inflation. Similar rebates have been granted to commercial property owners during the same period.

As at July 2026, no general property tax rebate is in force for private residential property. HDB flat owners should check the most recent Budget Statement for any rebate applicable to the current year. IRAS publishes rebate details on its website alongside the annual property tax bill.

Objecting to Your Annual Value

If you believe IRAS has assessed an AV that is too high — perhaps because rental market conditions have deteriorated, your property has structural issues that depress its rentability, or IRAS has used an inappropriate comparable property — you may lodge an objection within 30 days of receiving the property tax notice. The objection process requires you to provide evidence of comparable rental transactions that support a lower AV.

IRAS will review the objection and may revise the AV, maintain it, or issue an explanation. If you disagree with IRAS’s determination after the objection, you may appeal to the Valuation Review Board (VRB), an independent tribunal. Note that property tax is still payable at the assessed amount pending the outcome of any objection — you are not entitled to withhold payment while an objection is being reviewed.

What Might Come Next for Singapore Property Tax

This section represents editorial analysis — not official guidance.

The AV review cycle and any further rate adjustments are the two main variables to watch. Given that rental market growth moderated through 2025 and into 2026 — with some segments seeing rents stabilise or soften — the next AV review cycle may result in downward revisions for certain property types and regions. This would be a modest relief for NOO property investors who have seen property tax bills rise significantly since 2022.

On the rate side, Singapore’s progressive property tax has achieved a reasonable degree of progressivity since the 2022 Budget changes. Further rate increases targeting ultra-high-AV properties (GCBs with AV > S$200,000) are a political possibility at future Budgets, consistent with the Government’s stated goal of distributing the tax burden more broadly across wealth brackets.

Frequently Asked Questions

Can I use CPF to pay my property tax?

No. Property tax must be paid in cash. CPF funds — including the Ordinary Account — cannot be used to pay IRAS property tax. This is a common point of confusion since CPF can be used for certain other property-related costs such as BSD, mortgage repayments (subject to limits), and HDB purchase price. If you are setting up GIRO for property tax, it must be linked to a bank account, not a CPF account.

Is property tax deductible as a rental expense?

Yes, if you rent out your property and declare the rental income to IRAS for income tax purposes, the property tax paid on that property is an allowable deduction against your rental income. You may deduct either the property tax actually paid, or take the default 15% deduction for deemed maintenance expenses (which includes property tax). You cannot claim both — choose whichever gives you the larger deduction. Consult a tax adviser for your specific situation.

My property is vacant — do I still pay property tax?

Yes. Property tax applies whether the property is occupied, rented out, or vacant. If the property is not your principal residence, it is taxed at the NOO rate even if nobody lives in it. There is no exemption for vacancy. This means owning a second property that is left empty carries both the opportunity cost of foregone rental income and the ongoing cost of NOO property tax, maintenance fees, and insurance.

When does IRAS review and change Annual Values?

IRAS reviews AVs on an ongoing basis, typically triggering a revision when market rents for comparable properties show a sustained movement of 10% or more from the current assessed AV. IRAS may review individual properties (for example, after a major renovation or a change in the property’s rentable area) or conduct broader sector-wide reviews when rental market conditions change materially. You will receive a notice from IRAS if your AV is revised, and you have 30 days to object if you disagree.

Does property tax apply to commercial shophouses?

Yes, but at a flat 10% rate on the AV, not the progressive residential schedule. Non-residential property — including commercial shophouses, offices, retail units, and industrial property — is taxed at this flat 10% rate. If a shophouse has a residential upper floor and commercial ground floor, IRAS apportions the AV between the two components and applies the residential rates (OO or NOO) to the residential portion and 10% to the commercial portion. This nuanced treatment is one reason shophouses are a structurally distinct investment category.

Do I need to pay property tax if I just bought a new launch condo that has not been completed?

Property tax begins accruing from the date the property is officially completed and issued a Temporary Occupation Permit (TOP) or Certificate of Statutory Completion (CSC). During the construction period, no property tax is levied. Once the TOP is issued, IRAS will assess the AV and begin charging property tax — typically at the OO rate if you declare it as your principal residence, or the NOO rate if you have not moved in or have another OO property. You do not need to do anything proactively; IRAS will write to you.

Related Articles on LovelyHomes

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Calculator 2026: BSD and ABSD Explained

- Singapore Private Property Buying Guide 2026

- Singapore CPF for Property Guide 2026

- Singapore Property Cooling Measures 2026

- Singapore Seller’s Stamp Duty (SSD) Guide 2026

- Singapore HDB Upgrader Guide 2026: Timing Your ABSD Remission

- Singapore Property Seller Complete Guide 2026

Disclaimer: The property tax rates and Annual Value figures cited in this article are illustrative and based on the progressive rate schedule as at mid-2026. Singapore property tax rates and thresholds are subject to change at each Budget. Always verify the current year’s exact rates and your property’s AV with IRAS at iras.gov.sg. This article is for general information only and does not constitute tax or legal advice. Consult a licensed tax adviser or property professional before making any decisions based on this information. Property values and rental markets fluctuate — figures cited are indicative only.