A conservation shophouse is one of roughly 7,200 gazetted heritage units that the Urban Redevelopment Authority (URA) protects under the Conservation Programme that began in 1989. The buildings are easy to recognise — narrow frontage, deep floor plate, ornate plasterwork or Peranakan tile facade, three or four storeys, and the famous five-foot way. The investment story is harder to read. Shophouses sit at an unusual intersection of three regulatory regimes — URA conservation guidelines, the Residential Property Act, and commercial-property stamp duty rules — and the rules around who can buy, what they can do with it, and how it is taxed depend almost entirely on the zoning of the unit.

Quick Answer

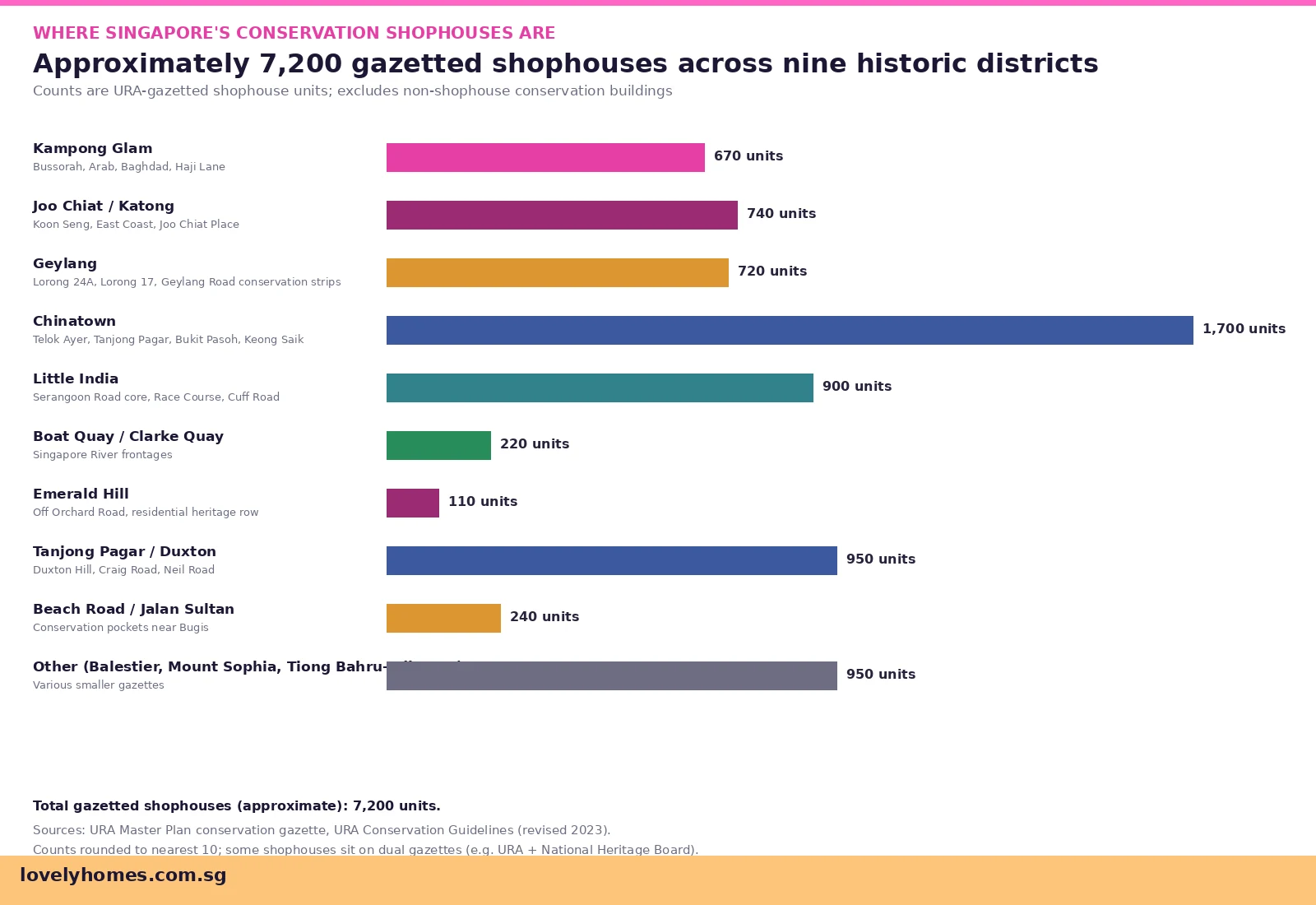

- ~7,200 gazetted shophouses across nine historic conservation districts including Chinatown, Tanjong Pagar, Joo Chiat, Kampong Glam and Little India.

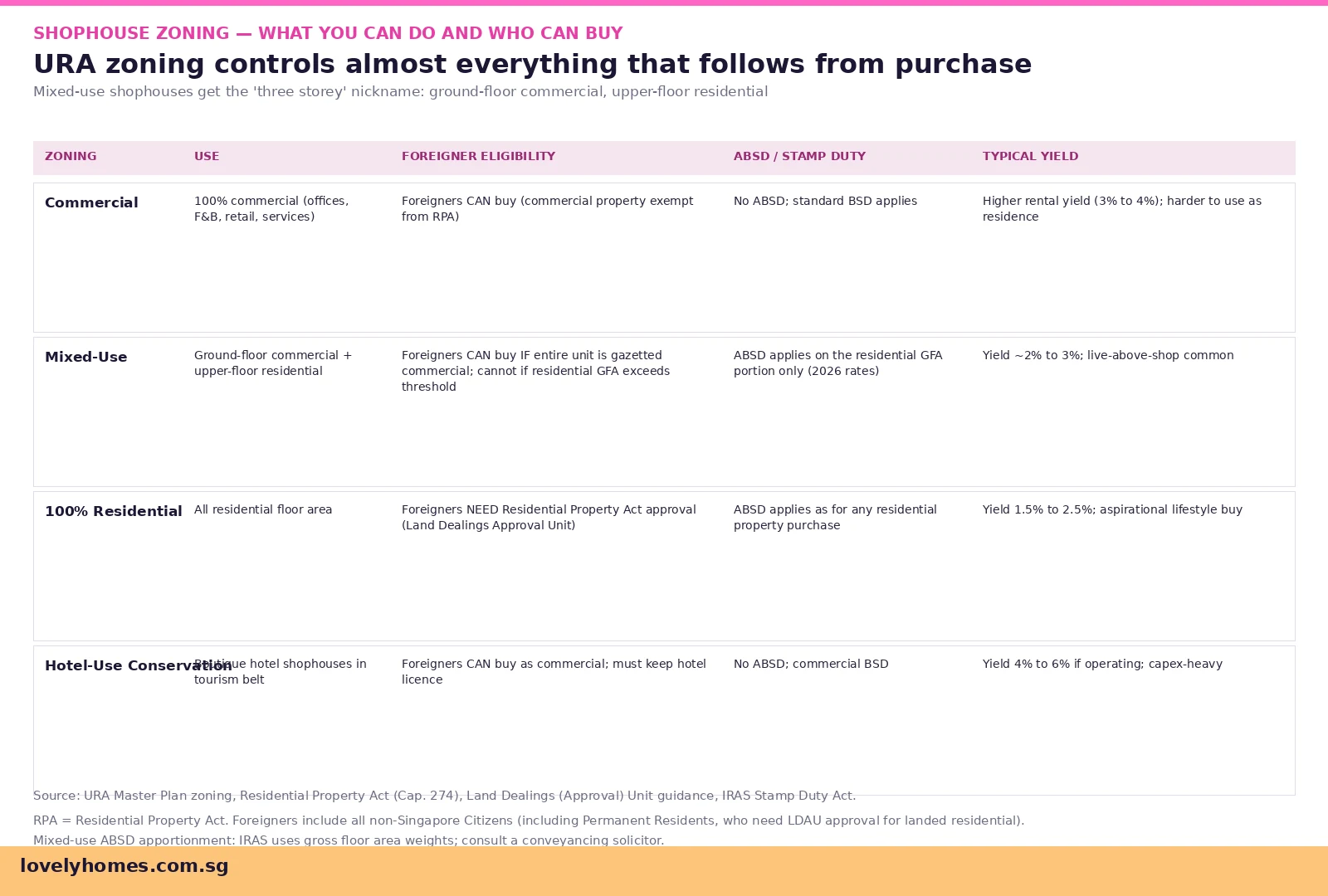

- Zoning is the single most important variable. Commercial-zoned shophouses can be bought by foreigners without ABSD or Residential Property Act approval. Residential-zoned shophouses require LDAU approval and attract ABSD.

- Mixed-use is the typical reality. Many shophouses are commercial on the ground floor and residential above; ABSD applies only on the residential gross floor area portion.

- Prime CBD shophouses traded at S$5,500 to S$8,000 psf in 2024-2025. The market cooled in 2025 after MAS and IRAS scrutiny on suspicious-buyer transactions; 2026 pricing has stabilised but transaction volume is roughly half of the 2023 peak.

- Restoration costs S$400 to S$1,000 psf. URA-permitted, heritage-compliant restoration is mandatory; non-compliant works can attract enforcement and fines under the Planning Act.

- Yields are modest. Residential shophouse yields run 1.5 to 2.5 percent; commercial yields 3 to 4 percent; boutique-hotel shophouses 4 to 6 percent (when operating).

- Financing is harder than condo lending. Commercial loans cap at 60 percent LTV with shorter tenors; residential mortgages still apply TDSR / MSR. Specialist lenders dominate the segment.

- The buyer pool is narrow. Family offices, ultra-high-net-worth individuals, and Family Trust structures are the main buyers; the segment is illiquid and capex-heavy.

The Backdrop — How Conservation Came About

Singapore began gazetting buildings under the Conservation Master Plan in 1989. The motivation was a recognition that the country had quietly demolished much of its pre-war urban fabric in the development push of the 1960s, 70s and 80s. The first batch of conservation buildings included blocks in Chinatown, Tanjong Pagar, Boat Quay and Kampong Glam. Over the next three decades the gazette expanded to include Joo Chiat, Geylang, Little India, Emerald Hill and pockets along Beach Road, Bukit Pasoh, Balestier and Tiong Bahru’s earliest pre-war stock.

The legal mechanism is straightforward. Once a building is gazetted under the Planning Act and listed in the URA’s conservation portfolio, the owner must obtain URA approval before any external alteration, addition or demolition. The interior is more flexible — owners can refit floor plates, add lifts, and re-plan internal partitions, but the facade, party walls, roof line, five-foot way colonnade and any specific feature called out in the conservation guidelines (timber stairs, decorative tiles, original plaster mouldings) must be preserved.

Zoning — The Variable That Drives Everything

Whether a foreigner can buy a particular shophouse, whether ABSD applies, what financing is available and what the unit can be used for all flow from the URA Master Plan zoning. The four common configurations:

100 percent commercial. The whole unit is gazetted commercial — typically the entire ground-floor and upper-floor envelope. These are the shophouses that foreigners and family offices have flocked to since the late 2010s, because the Residential Property Act does not apply, no ABSD is payable on purchase, and the asset can be held in a corporate or trust structure with relative ease. Acceptable uses include offices, F&B, retail, professional services and (sometimes) hotel-use under a separate licence.

Mixed-use. Ground floor commercial, upper floors residential — the original design intent of most pre-war shophouses, where the merchant lived above the shop. ABSD here is apportioned on gross floor area: the residential portion is treated as residential property, the commercial portion is exempt. Foreigners can buy if the entire unit is gazetted commercial-overlay, but cannot if the residential GFA exceeds the threshold without LDAU approval.

100 percent residential. The shophouse is entirely zoned for residential use. This is the rarest profile in the prime CBD belt but more common in Joo Chiat / Katong and Emerald Hill. Foreigners need approval from the Land Dealings (Approval) Unit under the Residential Property Act, and ABSD applies as for any residential acquisition. Residential mortgage rules including TDSR and MSR apply.

Hotel-use conservation. A small subset, mostly along Tanjong Pagar / Duxton, Bukit Pasoh and Kampong Glam, where a shophouse cluster has been redeveloped or licensed for boutique hotel operation. Buyer profile is hospitality investors; financing is through specialist lenders.

Pricing — From the 2023 Peak to the 2026 Stabilisation

Shophouse pricing peaked in 2023, when prime CBD units changed hands at S$7,000 to S$9,500 psf and total transaction volume hit roughly S$2.0 billion across the year. The 2024 cycle saw a noticeable cooling — partly because the highest-end deals moved offshore as buyers digested the 2023 ABSD hike on residential property, partly because financing tightened with elevated US rates, and significantly because the Monetary Authority of Singapore and the Inland Revenue Authority of Singapore opened scrutiny of suspicious shophouse transactions involving complex offshore vehicles. The 2024 money-laundering case that froze hundreds of millions of dollars of Singapore property included shophouses in the affected portfolio.

By 2026, prime CBD shophouse pricing has stabilised at S$5,500 to S$8,000 psf depending on location and condition. Joo Chiat and Katong residential shophouses sit at S$3,000 to S$5,000 psf. Geylang and Little India fringe transactions can clear under S$2,800 psf. Transaction volume is approximately half the 2023 peak.

Summary — Conservation Shophouse Indicators, 2024 to 2026

| Year | Total Volume (S$ B) | Prime CBD psf | Joo Chiat / Katong psf | Notable |

|---|---|---|---|---|

| 2023 | ~S$2.0B | S$7,000-9,500 | S$3,200-5,500 | Peak cycle; family offices dominant. |

| 2024 | ~S$1.1B | S$6,200-8,500 | S$3,000-5,200 | Money-laundering investigation; scrutiny of offshore buyers. |

| 2025 | ~S$0.95B | S$5,800-7,800 | S$2,900-4,800 | Volume bottom; ‘cleaner’ deals as enhanced KYC took hold. |

| Q1 2026 | ~S$0.30B | S$5,500-8,000 | S$3,000-5,000 | Stabilised pricing; heritage-restored stock commanding ~10% premium. |

Sources: URA caveat data 2023-2026, EdgeProp transaction archives, MAS Financial Stability Review 2024 and 2025.

Restoration — The Hidden Capex

The headline transaction price never tells the full story. A shophouse acquired in fair-restored condition might need only S$200 to S$300 psf of refurbishment for tenant fit-out. A “shell” shophouse — original timber elements, weathered facade, dilapidated roof — typically requires S$700 to S$1,000 psf of restoration. The work is regulated. Owners must engage a qualified person, submit drawings to URA, secure conservation approval, and then secure separate Building & Construction Authority (BCA) permits for structural works. The timeline is typically 9 to 18 months from purchase to completion.

Common restoration line items include: facade repair and re-rendering (heritage plasterwork is irreplaceable; specialist applicators charge S$300 to S$500 psf of facade), timber roof and structural rafters, rear extension with URA approval (a critical floor-area lever), modern services (air-conditioning, new electricals, plumbing, fire-safety), interior reconfiguration (lifts can be inserted but must be free-standing within the conservation envelope), and party-wall and rainwater works.

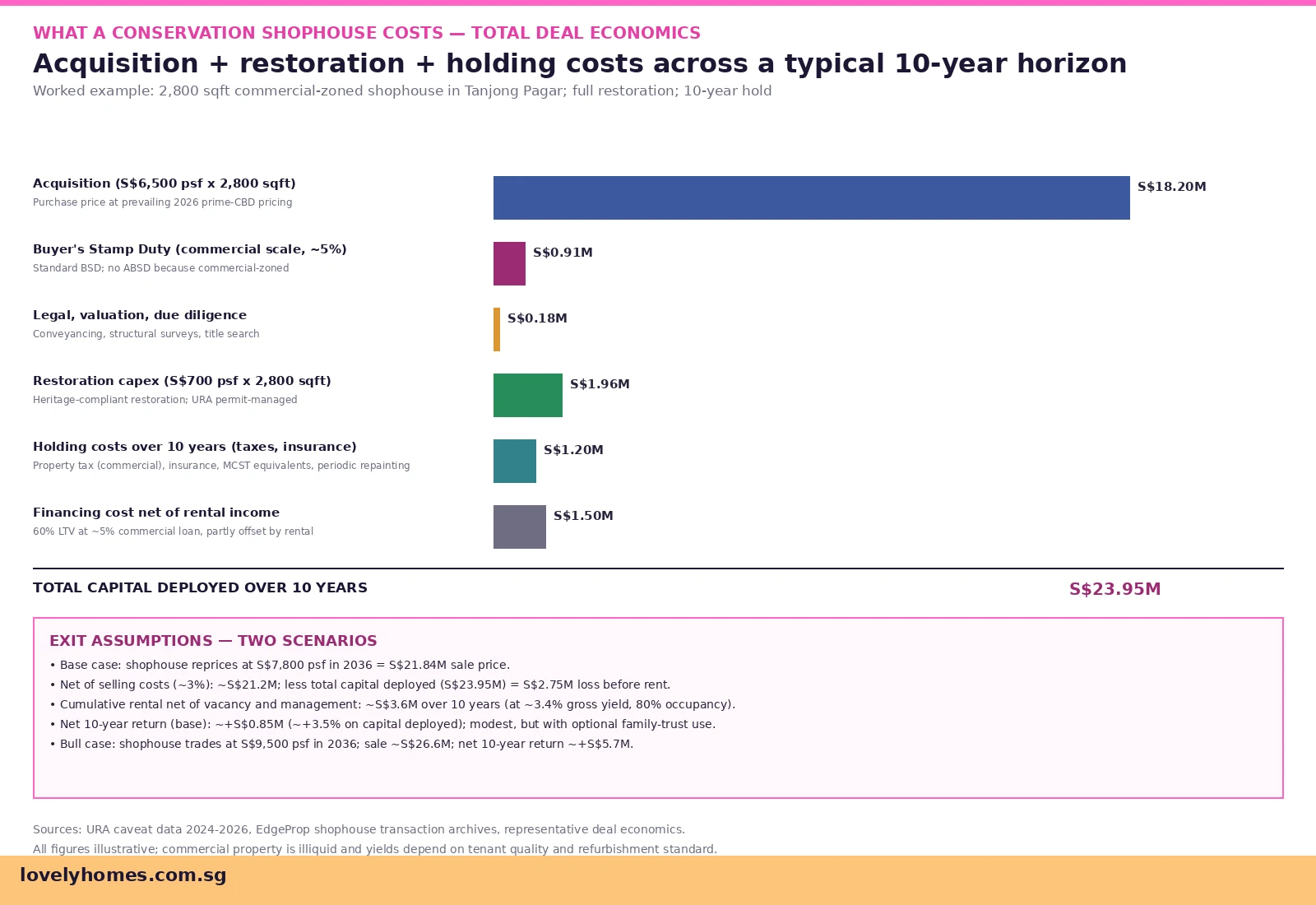

Worked Example — A 2,800 sqft Tanjong Pagar Commercial Shophouse

To make the deal economics tangible, take a hypothetical 2,800 square-foot, three-storey, commercial-zoned conservation shophouse in Tanjong Pagar. Assume acquisition in early 2026 at S$6,500 psf, a full heritage restoration over 12 months, and a 10-year hold thereafter.

Acquisition at S$6,500 x 2,800 = S$18.20 million. Buyer’s Stamp Duty on commercial property is roughly 5 percent at this price band — about S$910,000. Legal, valuation and due diligence add another S$180,000. Restoration at S$700 psf x 2,800 sqft = S$1.96 million.

Total capital deployed at end of restoration is approximately S$21.25 million. Add 10 years of holding costs (commercial property tax at 10 percent of annual value, building insurance, MCST equivalents on shared structures, intermittent maintenance) at an estimated S$120,000 per annum, or S$1.20 million over 10 years. Add net financing cost — a 60 percent loan-to-value commercial mortgage at 5 percent interest, partly offset by net rental income of about S$45,000 per month at 80 percent occupancy. The financing cost net of rent over 10 years is in the order of S$1.50 million.

Total capital deployed over the full 10-year horizon: S$23.95 million. If the shophouse reprices to S$7,800 psf in 2036 (a 20 percent capital appreciation over 10 years), the gross sale value is S$21.84 million; net of selling costs (~3 percent) it is roughly S$21.18 million. Cumulative net rental over the 10-year hold is about S$3.6 million. Net 10-year return is therefore approximately +S$0.85 million — a modest +3.5 percent on capital deployed. A bull case at S$9,500 psf in 2036 would return roughly +S$5.7 million on the same capital — a meaningful, if not dramatic, outcome.

Why This Matters for You

Three observations follow from the way the segment trades in 2026.

First, the foreigner-friendly route is real but narrowing. Commercial-zoned shophouses remain outside the Residential Property Act and free of ABSD, but enhanced KYC, source-of-funds verification, and beneficial-ownership disclosure now apply at much lower thresholds than five years ago. A foreign family office buying a S$15 million shophouse in 2026 will face significantly more documentation than in 2021. Buyers who cannot produce auditable wealth and tax-paid origins will struggle to clear the deal.

Second, restoration discipline separates winners from losers. The 10-year economics in the worked example are sensitive to restoration overrun, vacancy, and rental compression. Owners who engage experienced QPs, scope works tightly with URA early, and phase tenancy alignment can take meaningful capex out. Owners who treat the shophouse as a vanity project frequently overrun by 30 to 50 percent on restoration.

Third, the asset is illiquid and capex-heavy — a long-hold bet. The buyer pool is narrow, the holding obligations are real, and the realised return profile is more akin to a mid-cap commercial REIT than a residential investment property. Buyers seeking liquidity should look elsewhere; buyers prepared to hold for 10 to 20 years and treat the asset as a heritage-capital allocation tend to find the segment rewarding.

What Might Come Next

Two threads are worth tracking. URA has signalled a willingness to expand the conservation gazette to include early post-war stock — Tiong Bahru art-deco walk-ups beyond the existing pocket, mid-century low-rise blocks in Bukit Timah Road and Balestier — as a way of preserving Singapore’s later 20th-century heritage. Any expansion would create a fresh inventory of conservation properties, possibly under different zoning rules to the pre-war shophouse stock.

The second is government grant programmes for heritage restoration. URA’s Conservation Activation grants and the National Heritage Board Heritage Awards have already provided modest co-funding for exemplar restorations. Industry submissions to the 2025 Master Plan public consultation argued for a structured restoration grant system, capped per unit, with quality benchmarks. Whether the government adopts a formal grant-by-design programme will materially affect restoration economics for owner-occupiers and family trusts.

Frequently Asked Questions

Can a foreigner buy any shophouse without restrictions?

No. Only commercial-zoned shophouses can be bought by foreigners without prior approval under the Residential Property Act. Mixed-use shophouses with significant residential gross floor area, and 100 percent residential shophouses, require approval from the Land Dealings (Approval) Unit. Foreigners include all non-Singapore Citizens, including Permanent Residents.

Does ABSD apply to a commercial-zoned shophouse?

No. Additional Buyer’s Stamp Duty is a residential-property tax. A wholly commercial-zoned shophouse attracts only standard Buyer’s Stamp Duty on a commercial scale. For mixed-use shophouses, ABSD applies only on the residential floor area portion, apportioned by IRAS using gross floor area weights. A conveyancing solicitor and IRAS confirmation should be obtained before exchange.

What can I change about a conservation shophouse?

Almost everything internal — floor plates, internal walls, services, lifts, layouts — subject to BCA structural and fire-safety approvals. Almost nothing external without URA approval. The facade, five-foot way colonnade, roof line, party walls, and any specific element called out in the conservation guidelines (decorative tiles, plasterwork, timber elements) must be preserved or restored under a qualified person’s stewardship. Even paint colour can be regulated in some districts.

What kind of yield should I expect?

It depends on use and location. Commercial-zoned shophouses leased to F&B or office tenants typically return 3 to 4 percent gross. Mixed-use yields are 2 to 3 percent. Residential-zoned shophouses are 1.5 to 2.5 percent. Boutique-hotel shophouses can return 4 to 6 percent when operating, but face significant capex obligations and operational risk.

How is a shophouse financed?

Commercial shophouses are typically financed at 60 percent loan-to-value through commercial mortgages with 15 to 20-year tenors. Residential-zoned shophouses use residential mortgages subject to TDSR (55 percent) and MSR where applicable. Specialist lenders dominate the heritage-property segment because valuations require unusual expertise (heritage condition, restoration backlog, lease profile). Cash-buyer transactions are common at the top end.

Are conservation shophouses a good investment for a first-time buyer?

Generally no. The asset is illiquid, capex-heavy, requires specialist financing, and rewards a long hold of 10 to 20 years. A first-time investor with ordinary capital is better served by a smaller, liquid residential or commercial unit. Shophouses tend to suit family offices, Family Trust structures, ultra-high-net-worth individuals, and dedicated heritage investors who can underwrite the restoration risk and the holding obligations.

What did the 2024 money-laundering case mean for the segment?

Several conservation shophouses were among the assets frozen in the 2024 case where multiple foreign nationals were charged in connection with a S$3 billion money-laundering investigation. The fallout was twofold: enhanced KYC at banks and conveyancing firms, and an MAS-led tightening of source-of-funds documentation for any property transaction over a defined threshold. The segment has not been blacklisted, but it now operates under closer scrutiny for cross-border buyers.

Related Articles

- Foreign Buyer Guide Singapore 2026: Eligibility, ABSD, Sentosa Cove and Financing

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty Singapore 2026: Rates, Worked Examples and How to Calculate

- Freehold vs 99-Year Leasehold Singapore 2026: The Tenure Question Buyers Keep Asking

- Singapore Landed Property Guide 2026: Types, Rules, Prices and Who Can Buy

- Singapore Property Valuation 2026: How Banks Decide Your Home’s Worth

Disclaimer

This article is general information for Singapore property buyers and not legal, tax, valuation or planning advice. URA conservation guidelines, the Residential Property Act, ABSD apportionment, and commercial-property tax treatment are subject to change. Always verify current rules at the official Urban Redevelopment Authority portal (ura.gov.sg), the Inland Revenue Authority of Singapore (iras.gov.sg), and the Land Dealings (Approval) Unit (sla.gov.sg) before making any acquisition decision. For complex situations (cross-border buyers, family-trust structures, hospitality use), seek advice from a licensed conservation architect, conveyancing solicitor and tax advisor.

0 Comments