Buying Property in Singapore as a Foreigner: Complete Guide 2026

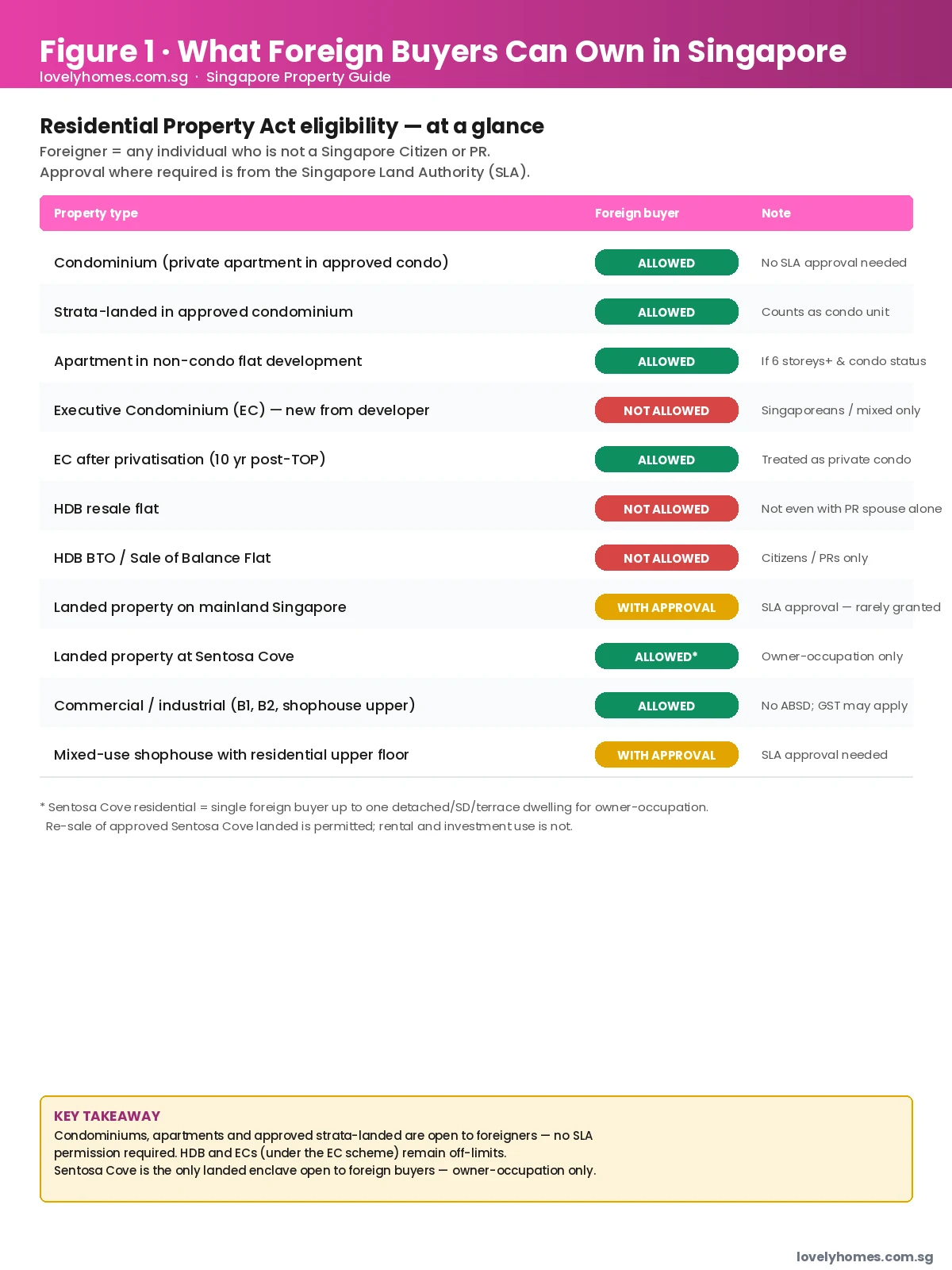

- Foreigners can freely buy private non-landed condominiums and apartments — no government approval required.

- Buying landed residential property requires Singapore Land Authority (SLA) approval, which is rarely granted to foreigners.

- Foreigners are not eligible to purchase HDB flats or new Executive Condominiums.

- Foreigners pay 65% Additional Buyer’s Stamp Duty (ABSD) on any residential purchase, on top of standard Buyer’s Stamp Duty.

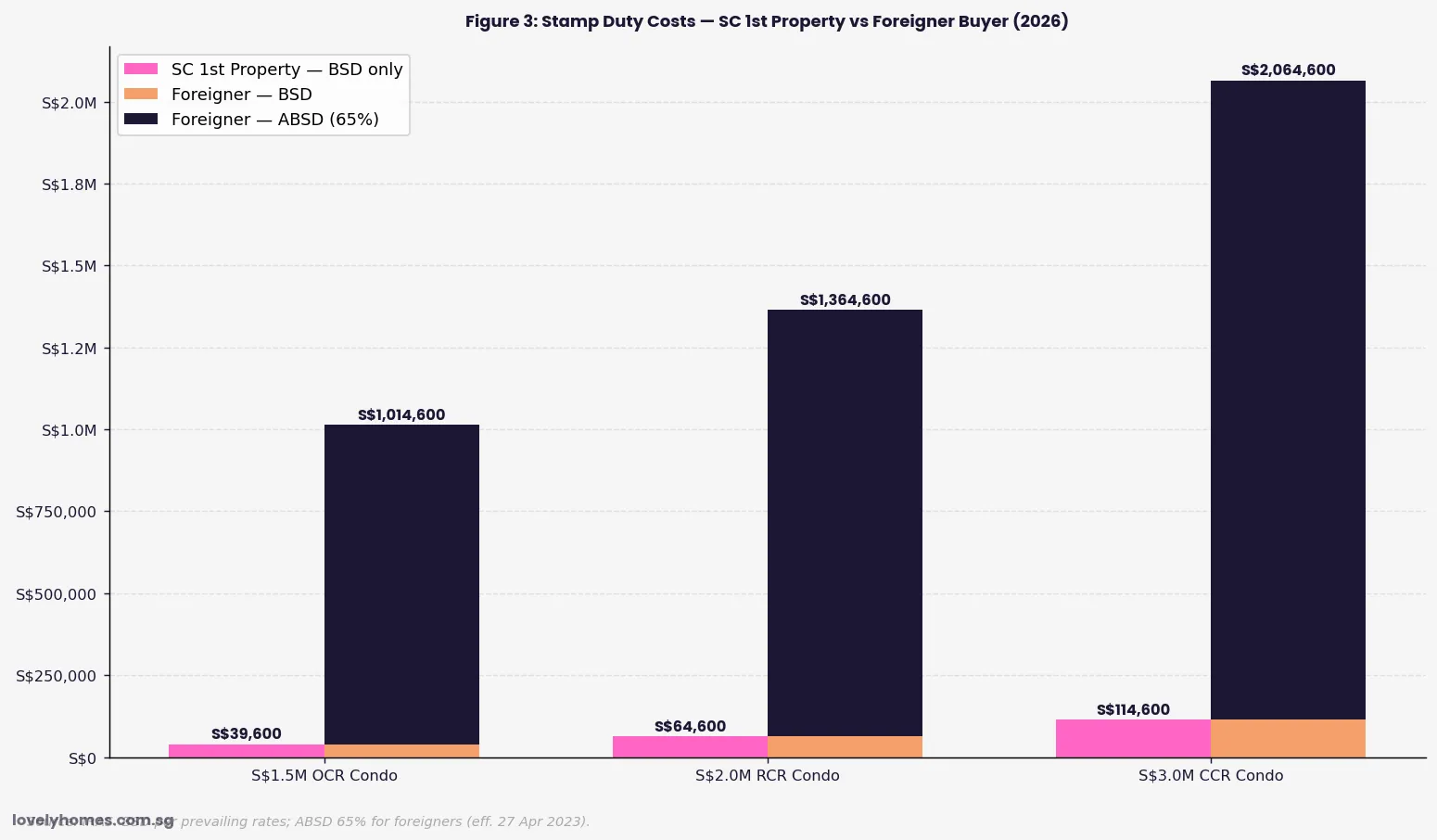

- On a S$1.5 million condo, a foreigner pays approximately S$1.01 million in stamp duties — versus S$39,600 for a SC buying their first property.

- Commercial and industrial properties are open to all buyers with no ABSD.

- Foreigners can obtain Singapore bank mortgages; HDB loans are unavailable to non-citizens.

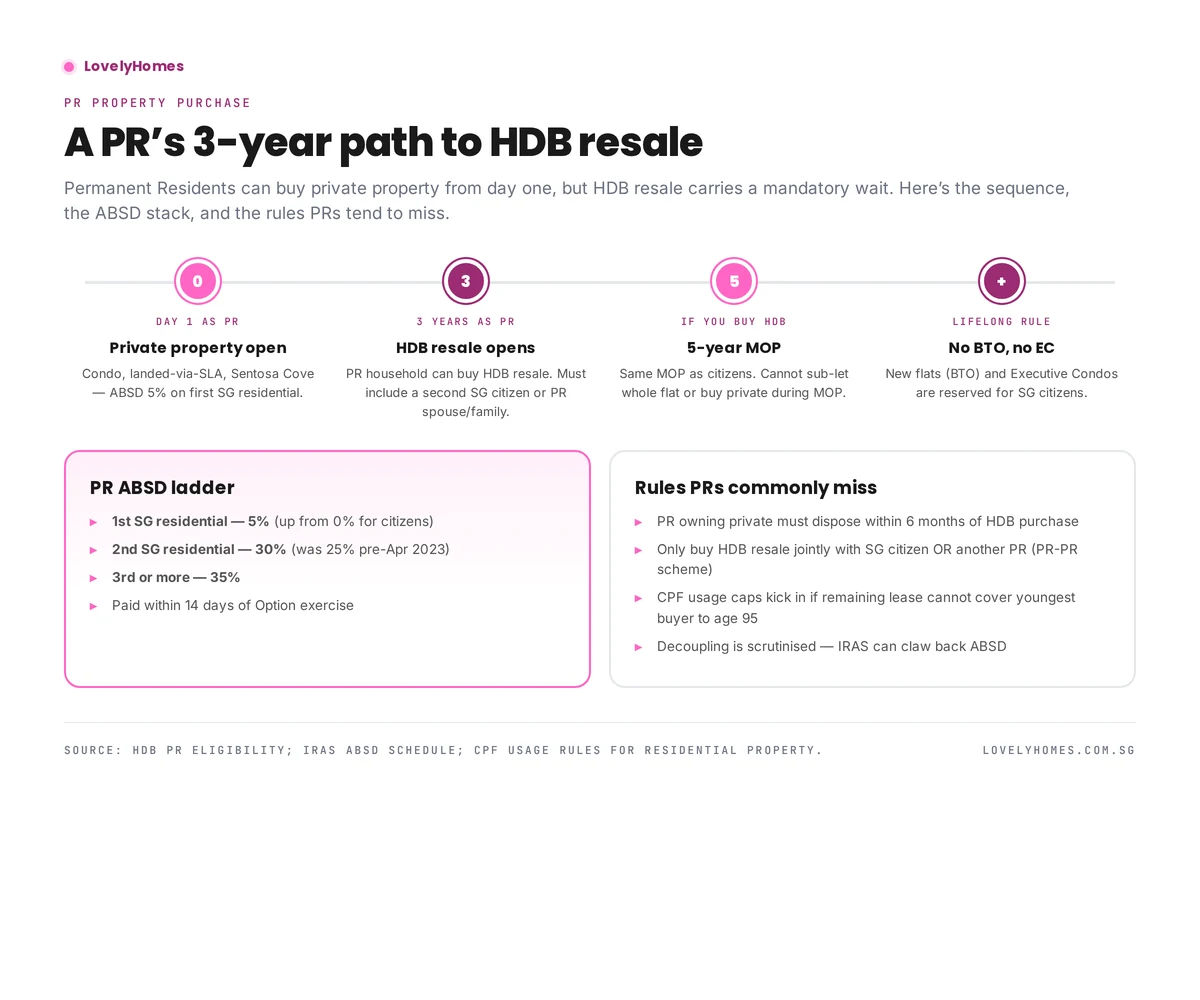

- Permanent Residents (SPRs) pay 5% ABSD on a first residential purchase and are eligible to buy HDB resale flats under specified conditions.

Who Is a “Foreigner” Under Singapore Property Law?

Under the Residential Property Act (Cap. 274), a foreigner is any person who is not a Singapore Citizen (SC) or a Singapore Permanent Resident (SPR). This definition covers expatriates on Employment Passes, Dependant Passes, Long-Term Visit Passes, and individuals with no Singapore residency status. Companies, limited liability partnerships, and discretionary trusts are classified as entities and attract the highest stamp duty rates.

The rules governing foreign property ownership span three legislative frameworks: the Residential Property Act (administered by the Singapore Land Authority), the Stamp Duties Act (enforced by IRAS), and the Housing and Development Act (HDB). Understanding all three is essential before committing to any purchase in Singapore.

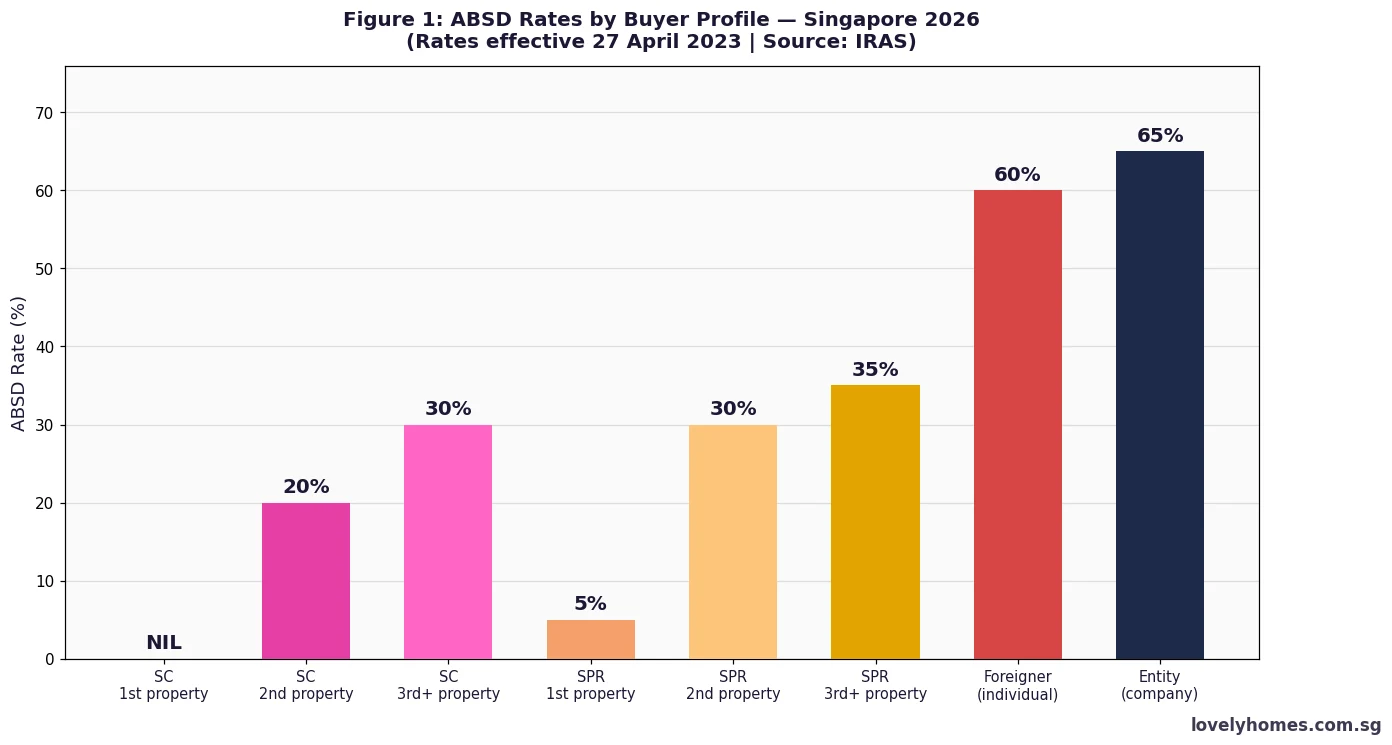

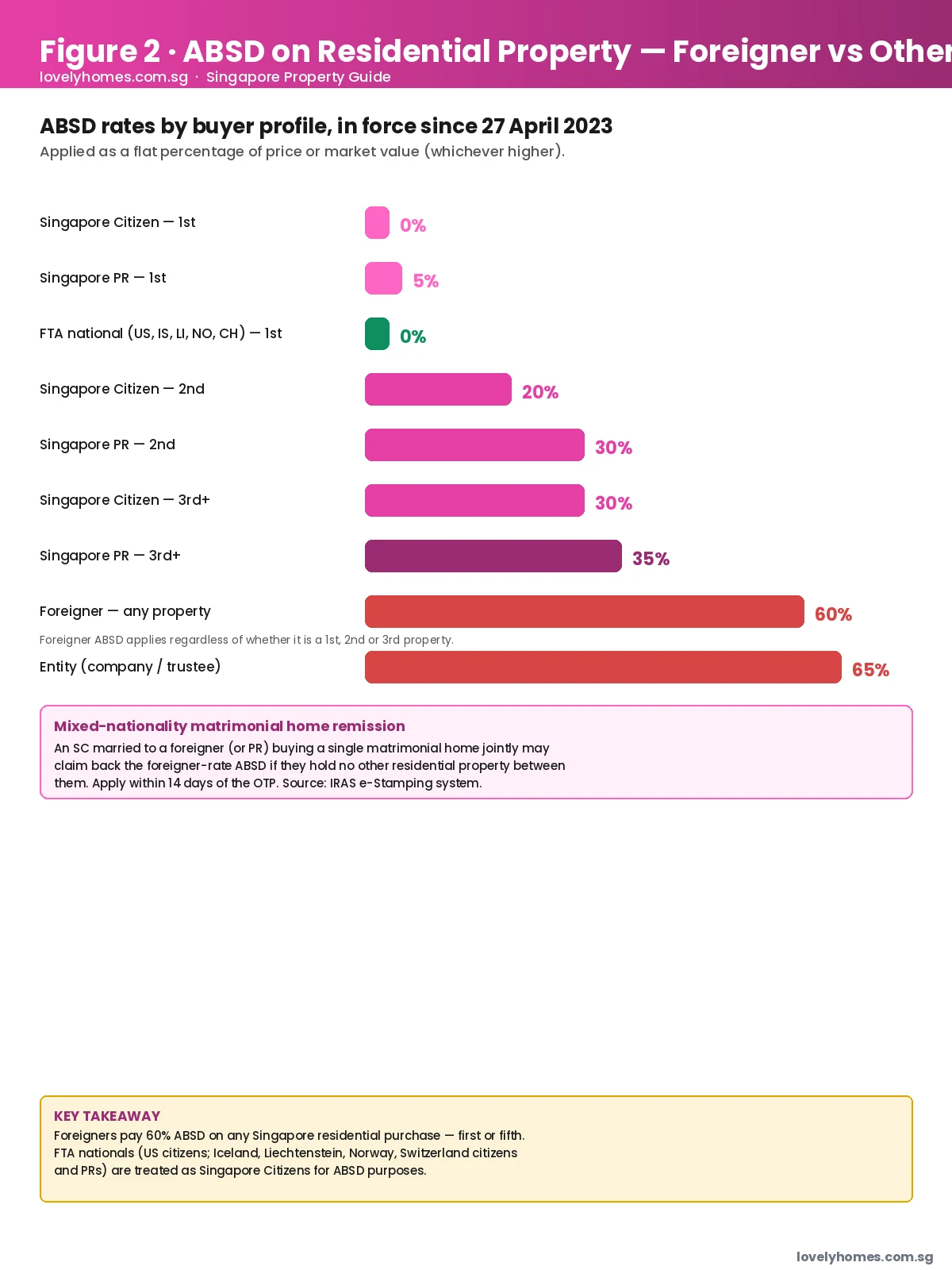

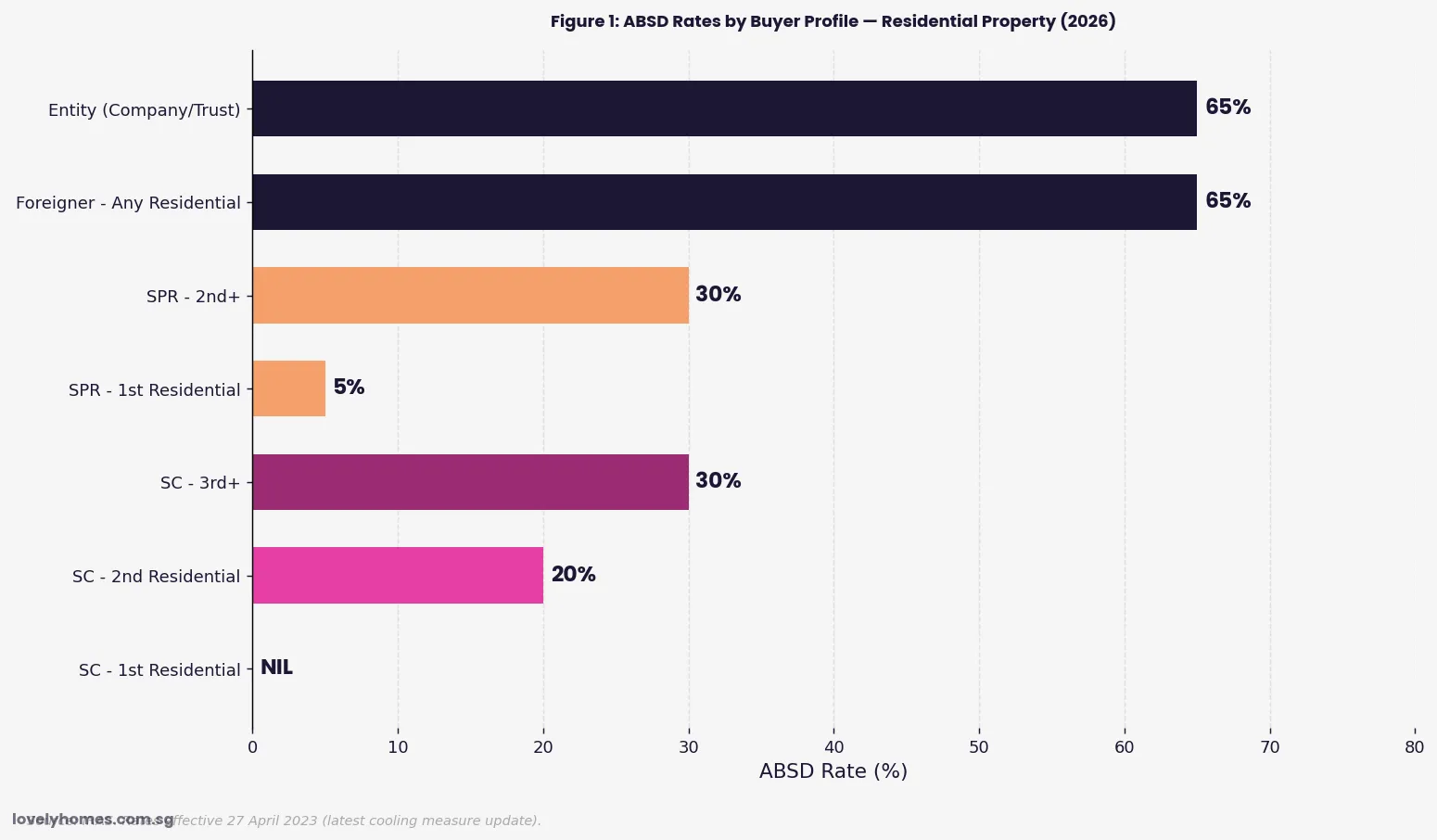

ABSD Rates in 2026: The True Cost of Buying

The Additional Buyer’s Stamp Duty (ABSD) is levied on top of the standard Buyer’s Stamp Duty (BSD). For foreigners, the rate is 65% of the purchase price — introduced in the April 2023 cooling measures package and unchanged as at 8 July 2026. This rate applies to every residential purchase regardless of whether it is the foreigner’s first or subsequent property in Singapore.

Buyer’s Stamp Duty (BSD) applies to all buyers. It is calculated on a tiered basis: 1% on the first S$180,000; 2% on the next S$180,000; 3% on the next S$640,000; 4% on the next S$500,000; 5% on the next S$1,500,000; and 6% on any amount exceeding S$3,000,000. For a S$1.5 million property, BSD amounts to S$39,600.

| Buyer Profile | 1st Residential Purchase | 2nd Purchase | 3rd+ Purchase |

|---|---|---|---|

| Singapore Citizen (SC) | 0% | 20% | 30% |

| Singapore PR (SPR) | 5% | 30% | 30% |

| Foreigner (non-SC/SPR) | 65% | 65% | 65% |

| Entity (company/trust/LLP) | 65% | 65% | 65% |

ABSD remission for married couples: Where one spouse is SC and the other is a foreigner, the couple may apply for ABSD remission under the Married Couples (Joint Purchase) scheme when purchasing their first joint residential property. This is not automatic — a formal application to IRAS is required and specific conditions must be met. Professional legal advice is essential in these situations.

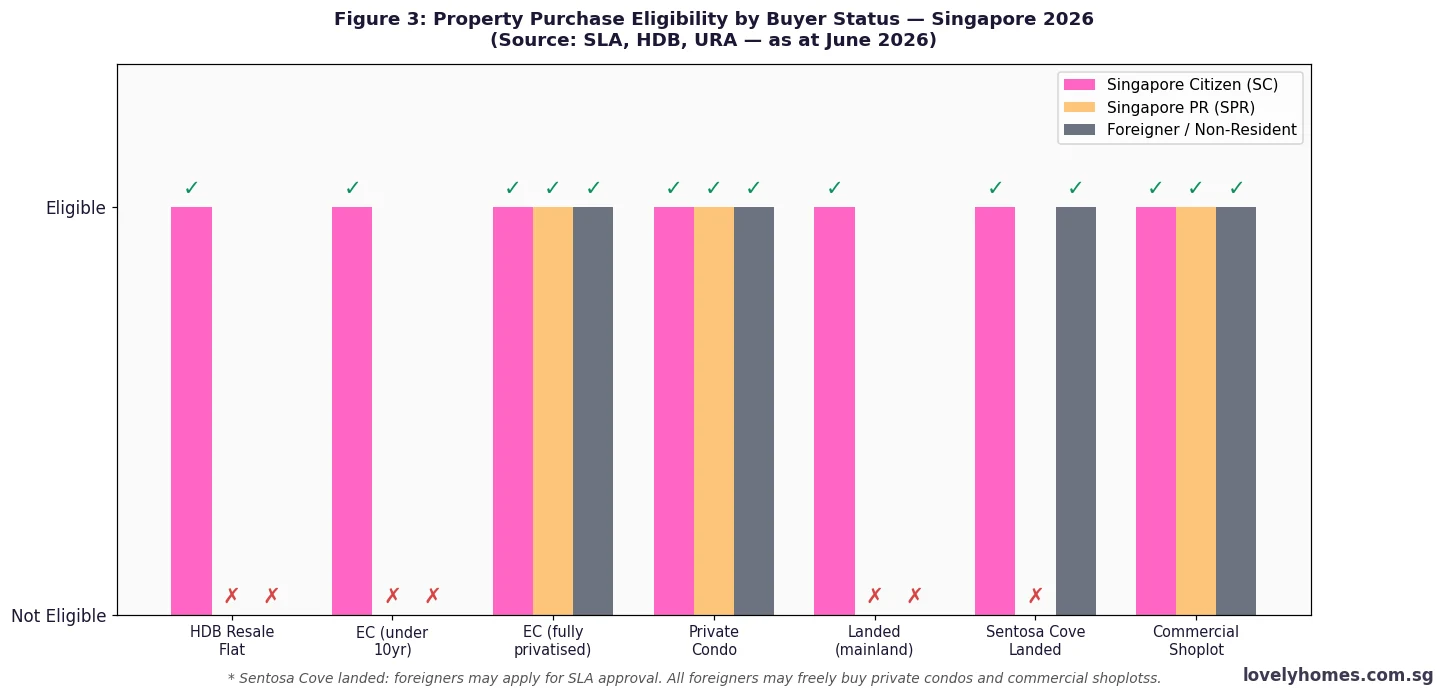

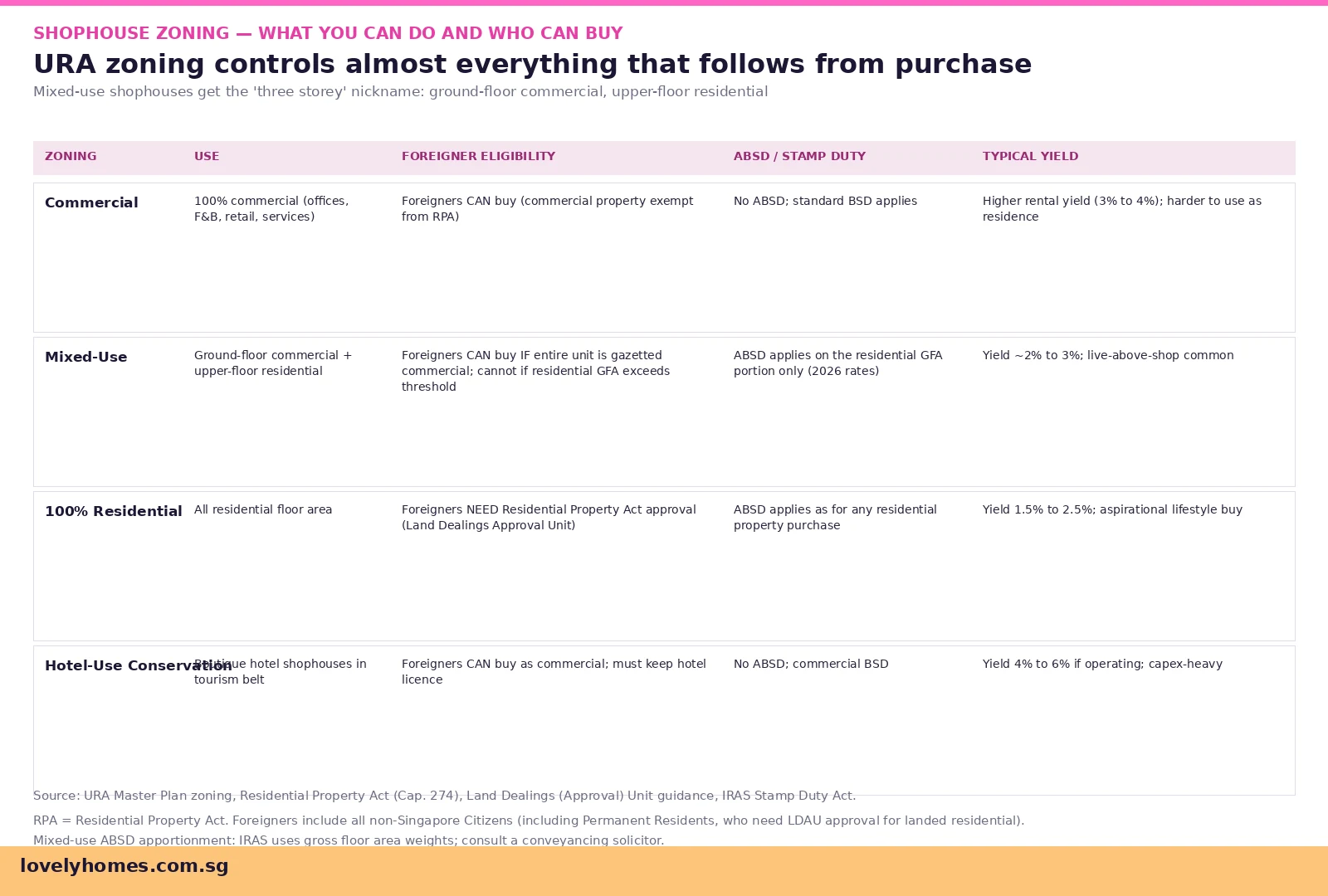

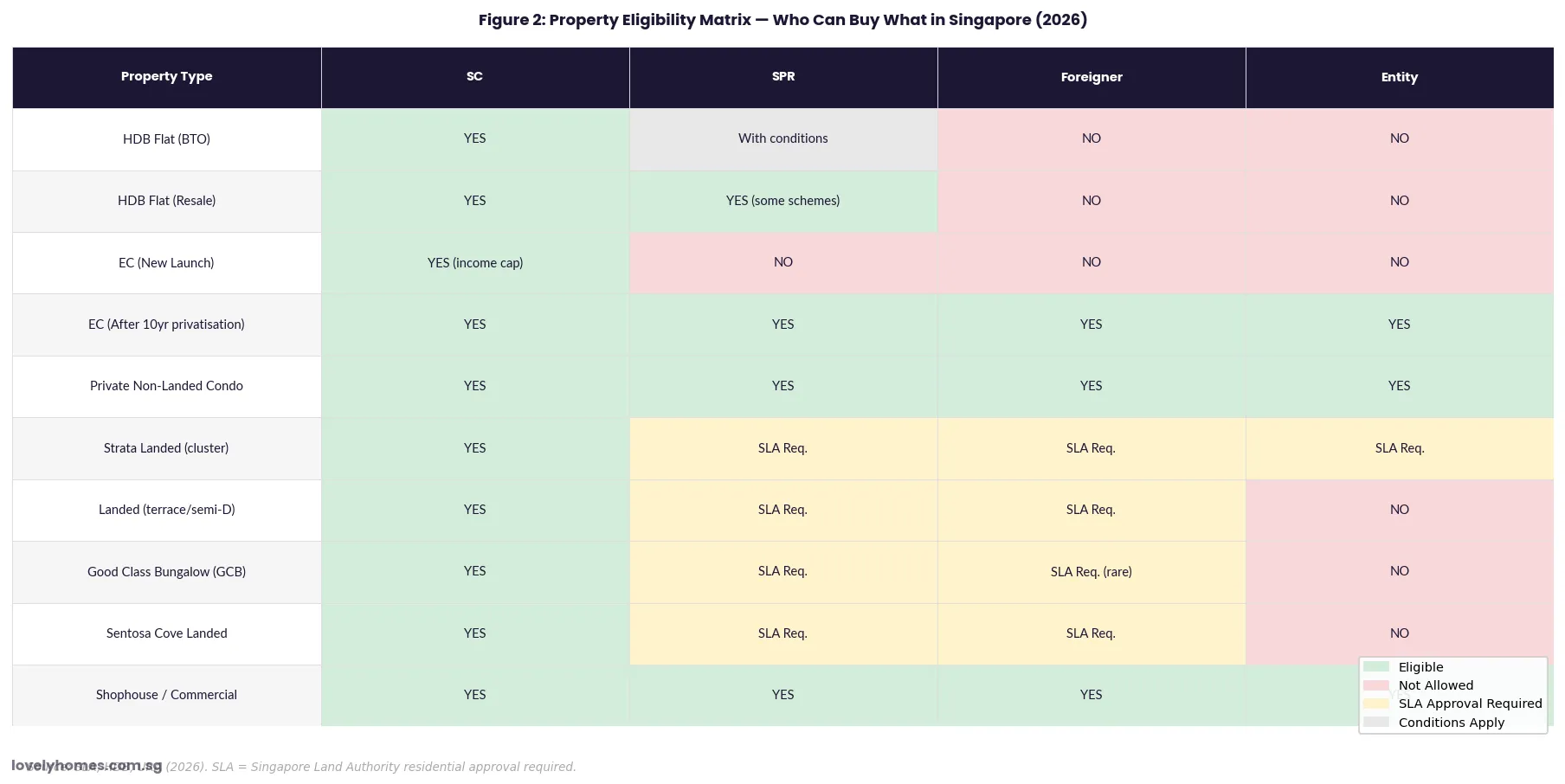

What Can Foreigners Buy? Full Eligibility Matrix

The range of property types available to foreigners varies significantly depending on the asset class and whether government approval is required.

Private non-landed condominiums and apartments are the most accessible asset class. No approval is required; only BSD and ABSD must be paid. Foreigners buy freely across all districts — OCR (Outside Central Region), RCR (Rest of Central Region), and CCR (Core Central Region).

Landed residential properties — terrace houses, semi-detached, bungalows, and Good Class Bungalows (GCBs) — are restricted under the Residential Property Act. Foreigners must apply to the SLA before purchasing. Approvals are rarely granted and limited to individuals who have made exceptional economic contributions to Singapore. Sentosa Cove is the one area where SLA approvals for foreigners are more regularly forthcoming, consistent with the original planning intent for the island enclave.

HDB flats are off-limits to foreigners entirely. Only Singapore Citizens may buy new BTO or open-booking HDB flats. SPRs are eligible for HDB resale flats under the Public Scheme but must form a family nucleus with another SC or SPR.

Executive Condominiums (ECs) during the new-launch and restricted resale period (first 10 years) are not available to foreigners. After full privatisation at the 10-year mark, ECs trade as regular private property and are purchasable by all nationalities.

Commercial and industrial property — shophouses, offices, retail strata units, industrial units — carry no ABSD and no nationality restriction. These are a common entry point for foreign investors seeking Singapore real estate exposure without the full residential stamp duty burden.

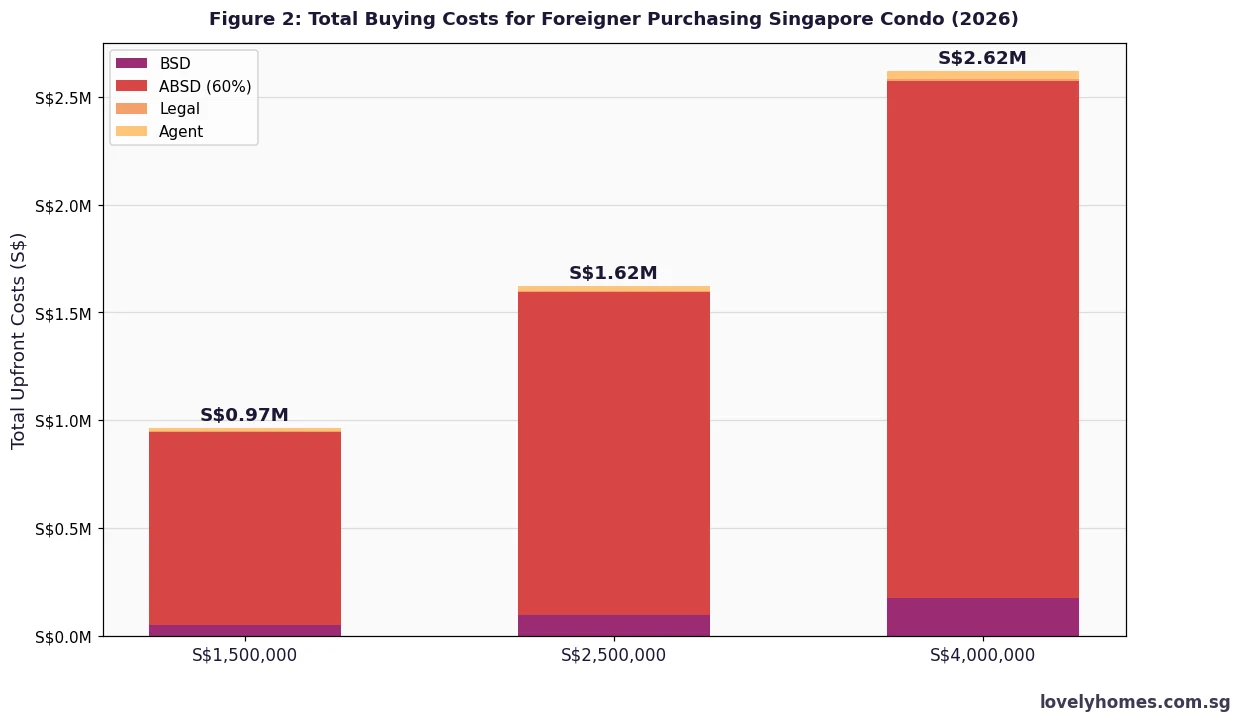

Stamp Duty Costs: SC First Property vs Foreigner

The financial difference between a Singapore Citizen buying their first property and a foreigner buying the same property is dramatic. The chart below illustrates the stamp duty gap across three common price points.

Financing: What Mortgages Are Available to Foreign Buyers?

Foreigners may apply for bank mortgage loans from Singapore-licensed financial institutions. The Total Debt Servicing Ratio (TDSR) framework, administered by the Monetary Authority of Singapore (MAS), caps total monthly debt obligations at 55% of gross monthly income. The Loan-to-Value (LTV) limit for a first property loan is 75%. HDB loans are unavailable to foreigners.

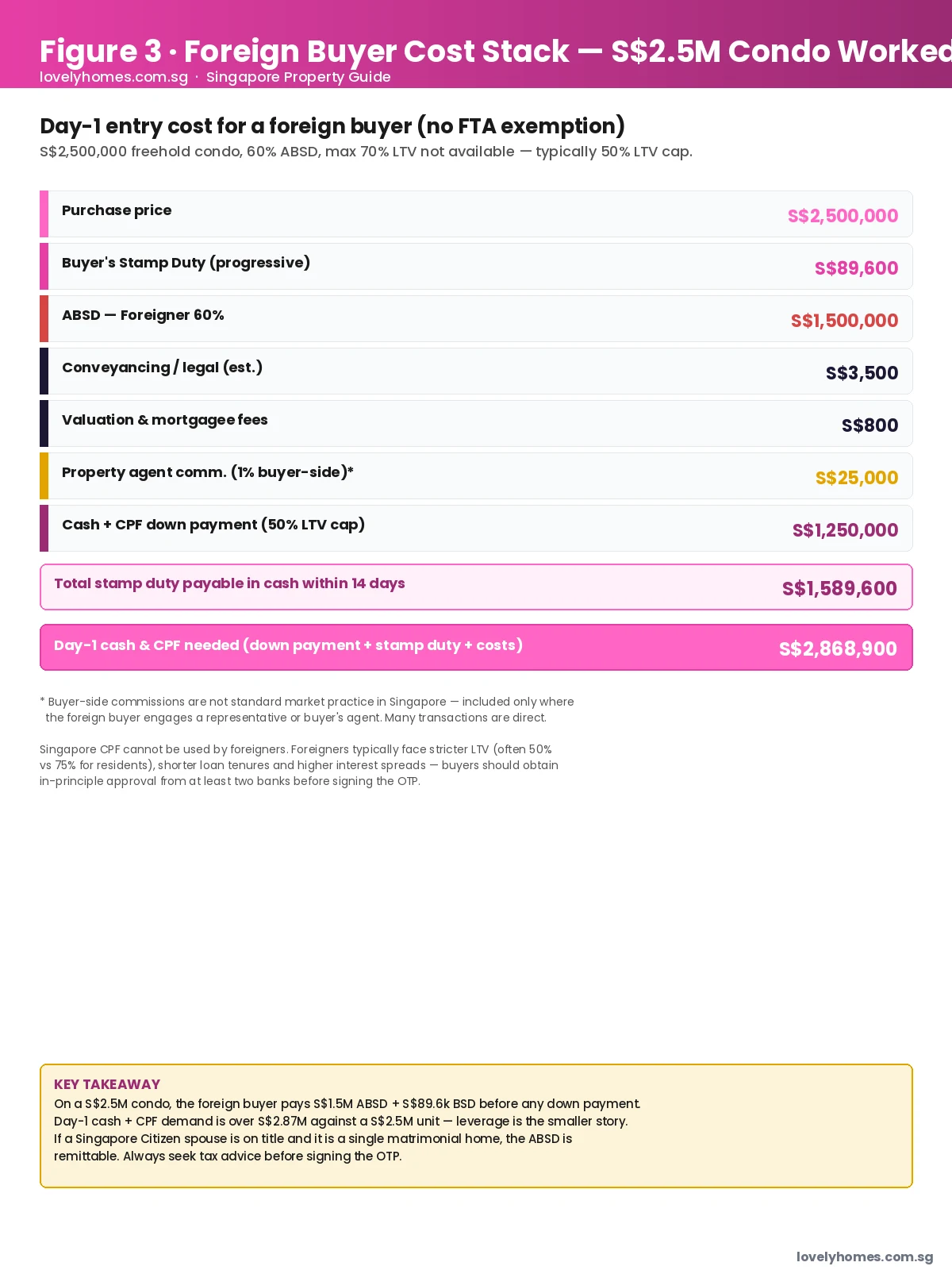

A foreigner buying a S$2 million condo must fund: 25% downpayment (S$500,000) + ABSD 65% (S$1,300,000) + BSD (S$64,600) + legal fees (~S$15,000) = approximately S$1,879,600 in cash. The S$1,500,000 bank loan (75% LTV) at 2.90% for 30 years would cost approximately S$6,274 per month — requiring gross monthly income of at least S$11,408 to satisfy TDSR.

Worked Example: A French National Buying a CCR Condo

Marc (French national, Employment Pass), purchasing 2BR CCR condo at S$2,800,000

BSD: S$1,800 + S$3,600 + S$19,200 + S$20,000 + S$65,000 = S$109,600

ABSD (65%): S$2,800,000 × 65% = S$1,820,000

Total stamp duties: S$1,929,600 (100% cash — no CPF available to foreigners)

Bank loan (75% LTV): S$2,100,000 at 2.90% p.a. over 30 years = ~S$8,772/month

TDSR check: Marc earns S$28,000/month — TDSR 31.3% PASS (well within 55%)

Total cash required at purchase: S$700,000 downpay + S$1,929,600 stamp duties + S$15,000 legal = approximately S$2,644,600

Break-even holding period: At 3% annual capital appreciation, the property must be held for approximately 15 years before stamp duty entry costs are fully recovered through price appreciation alone, assuming no rental income offset.

What This Means for You: Singapore as a High-Cost Foreign-Buyer Market

Singapore’s 65% foreigner ABSD is one of the highest residential entry taxes for non-citizen buyers among developed global cities. Hong Kong imposes a 30% Buyer’s Stamp Duty for non-permanent residents; Australia restricts foreigners largely to new-build supply; the United Kingdom levies a 2% surcharge. Singapore’s deliberate policy positioning prioritises citizen home ownership above foreign investment demand.

The practical result: foreign residential buyers in Singapore are predominantly high-net-worth individuals for whom the ABSD represents an acceptable cost of entry into a stable, transparent, and appreciating market. URA transaction data shows foreign buyer share of private residential transactions fell from approximately 4–5% before April 2023 to below 2% post-hike. Despite the cost, Singapore remains attractive for long-tenure expatriates and global wealth holders because of rule of law, no capital gains tax, SGD currency stability, and Asia-Pacific gateway positioning.

What Might Come Next

As at July 2026, the government has given no indication of relaxing the 65% foreigner ABSD. The MAS Financial Stability Review (November 2025) noted that price growth had moderated — the URA Private Property Price Index rose just 0.5% in Q2 2026 — reducing immediate policy pressure. However, the CCR segment rose 2.0% in Q2 2026, the strongest performance among any segment, which may attract renewed attention to foreign demand in luxury districts. Buyers should plan on the basis that the 65% rate will persist through at least 2027–2028 and factor this into their financial modelling from the outset.

Frequently Asked Questions

Can a foreigner use CPF to pay ABSD?

No. ABSD must be paid entirely in cash. Only Buyer’s Stamp Duty can be funded from CPF Ordinary Account savings — and only by SC and SPR holders who maintain CPF accounts. Foreigners have no CPF accounts and must pay all stamp duties in cash. This is a material liquidity consideration: on a S$2 million purchase, ABSD alone is S$1.3 million in cash, payable within 14 days of the Sale and Purchase Agreement date.

Can a foreigner and SC jointly buy property to reduce ABSD?

When a foreigner and SC purchase jointly, ABSD is assessed at the highest applicable rate — meaning the foreigner’s 65% applies to the full purchase price regardless of ownership proportions. There is one exception: legally married spouses (one SC, one foreigner) purchasing their first joint residential property may apply to IRAS for ABSD remission under the Married Couples scheme. This requires a formal application and is subject to eligibility conditions. Couples should seek qualified tax and legal advice before structuring any joint purchase.

How does the SLA approval process work for landed residential property?

The Singapore Land Authority processes applications from foreigners wishing to purchase restricted residential property under the Residential Property Act. Applicants submit supporting documents including employment history, tax contribution records, length of Singapore residency, and evidence of community ties. SLA considers economic contribution to Singapore as the primary criterion. Approval rates for non-Sentosa Cove landed property applications by foreigners are estimated to be below 30% by industry practitioners, and GCB approvals for foreigners are exceedingly rare. Sentosa Cove applications have a higher success rate given the original planning intent for that precinct. Processing typically takes 8 to 16 weeks.

Can foreigners buy commercial or industrial property without ABSD?

Yes. Commercial properties (shophouses, offices, retail units) and industrial properties (factories, warehouses, business parks) are not subject to ABSD or residential property restrictions. BSD is payable on the purchase price at the same tiered rates as for residential purchases. This makes commercial and industrial Singapore property a more accessible entry point for foreign investors seeking Singapore real estate exposure. However, mixed-use properties containing a residential component may be partially subject to residential rules — professional advice is essential.

Does a foreigner pay Seller’s Stamp Duty (SSD) when selling?

Seller’s Stamp Duty applies to all sellers regardless of nationality for properties sold within the holding period: 12% within 1 year, 8% within 2 years, 4% within 3 years, and nil thereafter. There is no capital gains tax in Singapore — profits from property sold after the SSD window are not taxable. For foreigners who have already paid 65% ABSD on entry, the implication is clear: a minimum 3-year hold is almost always essential to make any residential investment viable. Short-term flipping is economically punitive for foreign buyers in Singapore.

Can a foreigner rent out their Singapore property?

Yes, foreigners may rent out private residential property without restriction. Rental income from Singapore property earned by non-residents is subject to Singapore income tax at the flat non-resident rate of 24%, assessed on net rental income after deducting allowable expenses such as mortgage interest, agent fees, maintenance charges, fire insurance premiums, and a statutory depreciation allowance. Non-resident landlords must file an annual Singapore income tax return with IRAS. Property tax at the non-owner-occupied (investment) rate also applies annually, calculated on the Annual Value assessed by IRAS.

Are there restrictions on foreigners buying through a Singapore company?

Purchasing residential property through any entity — including Singapore-incorporated companies — attracts the entity ABSD rate of 65%, the same as the individual foreigner rate. There is no advantage in using an entity structure for residential purchases from a stamp duty perspective. For commercial and industrial property, entity structures carry no ABSD and are commonly used by foreign investors for operational or tax-planning reasons. Entities holding residential property also pay higher annual property tax at non-owner-occupied rates and cannot benefit from CPF mortgage financing.