Permanent Residency fundamentally changes a buyer’s property menu in Singapore — but not overnight. From day one, private property opens. HDB resale still waits three years. New HDB (BTO/Plus/Prime) and new ECs remain closed to PRs regardless of wait time.

This guide maps the PR property timeline, the full 2026 ABSD ladder for PR buyers, the most common mistakes PRs make when disposing of existing property, and the rules PRs should know before taking out a CPF loan. For the foreigner-side equivalent, see our foreigner property guide.

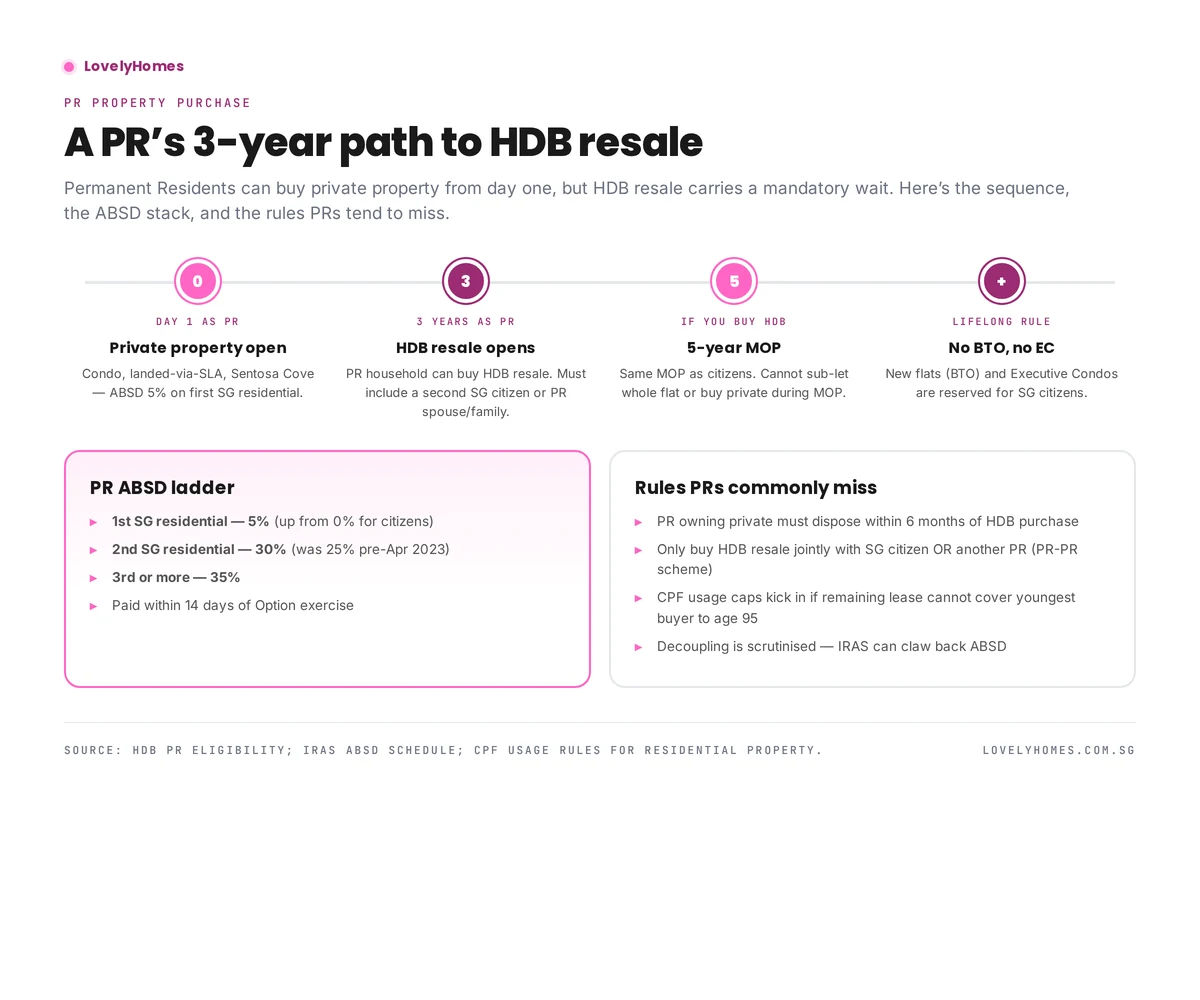

The PR property timeline

Day 1 as PR

Private condo, landed-via-LDAU, and Sentosa Cove landed open immediately. CPF usage opens once the PR has active OA/SA balances. LTV, TDSR and MSR frameworks are identical to citizens.

3 years as PR

HDB resale opens. A PR household must form a qualifying family nucleus — typically a PR applicant with a spouse (PR or SG citizen), or the PR-PR Scheme (both applicants PRs for at least 3 years).

5 years after HDB purchase (if you buy HDB)

Minimum Occupation Period. Same 5-year MOP as citizens. Cannot sub-let the entire flat, cannot buy private residential, cannot sell on the open market. See our MOP rules guide.

Lifetime rule

PRs cannot buy new BTO, new Plus, new Prime or new EC flats. These are reserved for SG citizens with a citizen spouse or fiancé(e). The only HDB route for PRs remains the resale market.

ABSD for PRs — the 2026 ladder

| Residential count | ABSD (PR) | Notes |

|---|---|---|

| 1st SG residential | 5% | Up from 0% that citizens pay |

| 2nd SG residential | 30% | Raised from 25% in Apr 2023 |

| 3rd or more | 35% | Raised from 30% in Apr 2023 |

ABSD is payable within 14 days of Option exercise, on top of BSD. If two PRs buy jointly, the ABSD is calculated on the highest-count profile among the buyers.

The HDB-specific rules PRs must follow

Dispose of private within 6 months

A PR who owns private residential (in Singapore or overseas) must dispose of it within 6 months of the HDB resale completion. This is usually the biggest surprise for incoming PR buyers — overseas apartments count.

CPF usage and the lease rule

CPF can fund the purchase only if remaining lease covers the youngest buyer to age 95. For older HDB stock this is a real constraint — see our CPF for property guide.

No grants (mostly)

Most HDB grants (EHG, Family Grant, Proximity Housing Grant) are reserved for SG-citizen first-timer households. A PR-PR couple does not qualify for EHG. However, a PR with an SG-citizen spouse may qualify under the standard first-timer framework — see our grants guide.

Landed and Sentosa Cove

PRs need LDAU approval under the Residential Property Act to buy landed on the mainland — rarely granted except for long-tenured PRs with strong local ties. Sentosa Cove landed is much more accessible: SLA approval is routinely granted for owner-occupation.

Common PR mistakes

- Forgetting the 3-year HDB wait. Newly-minted PRs cannot buy HDB until year 3.

- Holding overseas property while buying HDB. HDB will compel disposal within 6 months.

- Attempting decoupling to reset ABSD. IRAS actively scrutinises PR decoupling post-2022 and may claw back ABSD. See our decoupling guide.

- Using CPF on a lease-short flat. Always check the lease-to-95 calculator first.

Frequently asked questions

Can a PR buy an EC?

Not a brand new EC — that’s citizen-only. A PR can buy a privatised EC (post-10-year MOP + privatisation), because by then it is effectively private property.

Can two PRs buy HDB resale together?

Yes — under the PR-PR Scheme, both must have been PR for at least 3 years. Grants are not available.

What if I become a citizen after buying HDB as a PR?

The flat becomes a citizen-owned flat. Any remaining rules (MOP, subletting) still apply from the purchase date.

Does a PR pay the 60% foreigner ABSD?

No. PR status attracts the PR ladder (5% / 30% / 35%) — not the foreigner flat rate.

This guide is for general information only and is accurate as of April 2026. Singapore property rules, taxes and cooling measures change frequently — always verify current figures with URA, IRAS, HDB or a licensed professional before committing. LovelyHomes is not a financial, legal or tax advisor.

0 Comments