Figure 0: HDB Resale Levy Singapore 2026 — Complete Guide to Amounts, Exemptions and How It Works

Quick Answer — HDB Resale Levy at a Glance

The HDB Resale Levy is a payment required when a second-timer household buys a new subsidised HDB flat or an Executive Condominium (EC) unit after previously enjoying a housing subsidy.

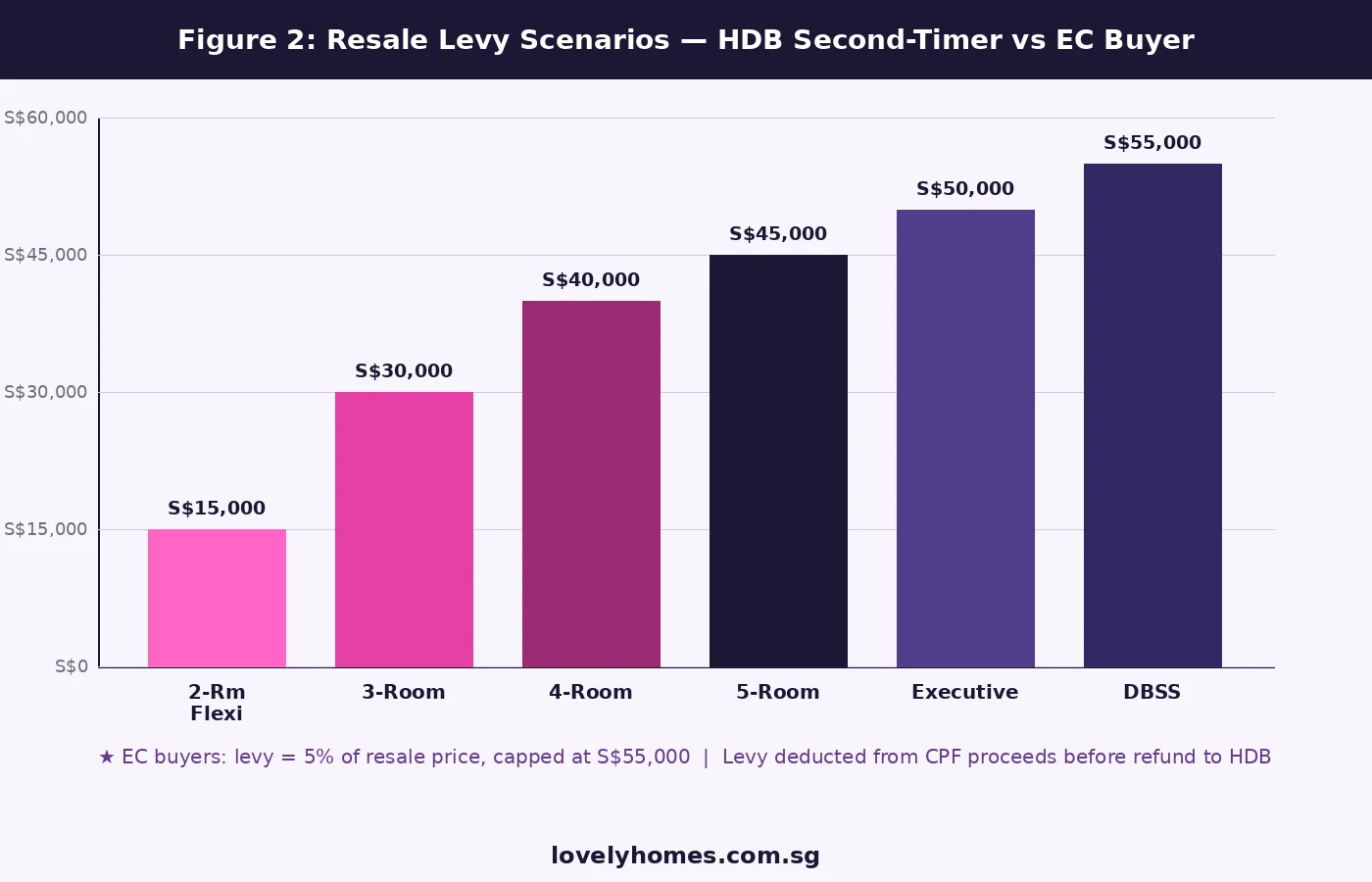

Levy amounts range from S$15,000 (for a 2-Room Flexi sold) to S$55,000 (for a DBSS flat sold), with EC buyers paying 5% of resale price (capped at S$55,000).

It is paid by deduction from the CPF refund when your first flat is sold — you do not write a cheque.

Exemptions apply if you bought your first flat on the resale market without any CPF Housing Grant, inherited the flat, or received it via a court order.

The levy does not apply when buying a private property — only a second subsidised HDB flat or EC triggers it.

Getting the levy wrong can delay your second flat booking and result in owing HDB cash if your CPF proceeds are insufficient.

From 3 March 2006, all levy amounts were fixed at the flat-type level — they are not a percentage of the first flat’s resale price (except for EC).

What Is the HDB Resale Levy?

The HDB Resale Levy is a subsidy recovery mechanism administered by the Housing & Development Board (HDB) under Singapore’s public housing framework. When the government provides a housing subsidy — such as the Central Provident Fund (CPF) Housing Grant, the Additional CPF Housing Grant (AHG), the Special CPF Housing Grant (SHG), or the Enhanced CPF Housing Grant (EHG) — it does so on the understanding that this benefit is tied to one subsidised flat per household. If that household later purchases a second subsidised flat or Executive Condominium unit, they are required to “return” a portion of the earlier subsidy benefit in the form of the resale levy.

The policy was introduced to ensure that public housing subsidies are targeted at households that genuinely need them and to maintain the long-term sustainability of Singapore’s public housing system. HDB administers the levy and collects it automatically at the point of sale of the first flat — it is not a separate bill sent to you but a deduction from your CPF Ordinary Account (OA) proceeds before they are refunded.

As at July 2026, the levy framework has remained stable since the flat-type rate schedule was fixed on 3 March 2006. Understanding it correctly is essential for any second-timer household planning to upgrade or right-size within the public housing system.

Figure 1: HDB Resale Levy Amounts by Flat Type Sold (2026). Fixed rates since 3 March 2006; EC applies a 5% rate with S$55,000 cap. Source: HDB Singapore.

Who Pays the HDB Resale Levy?

You are required to pay the resale levy if all three of the following conditions are met:

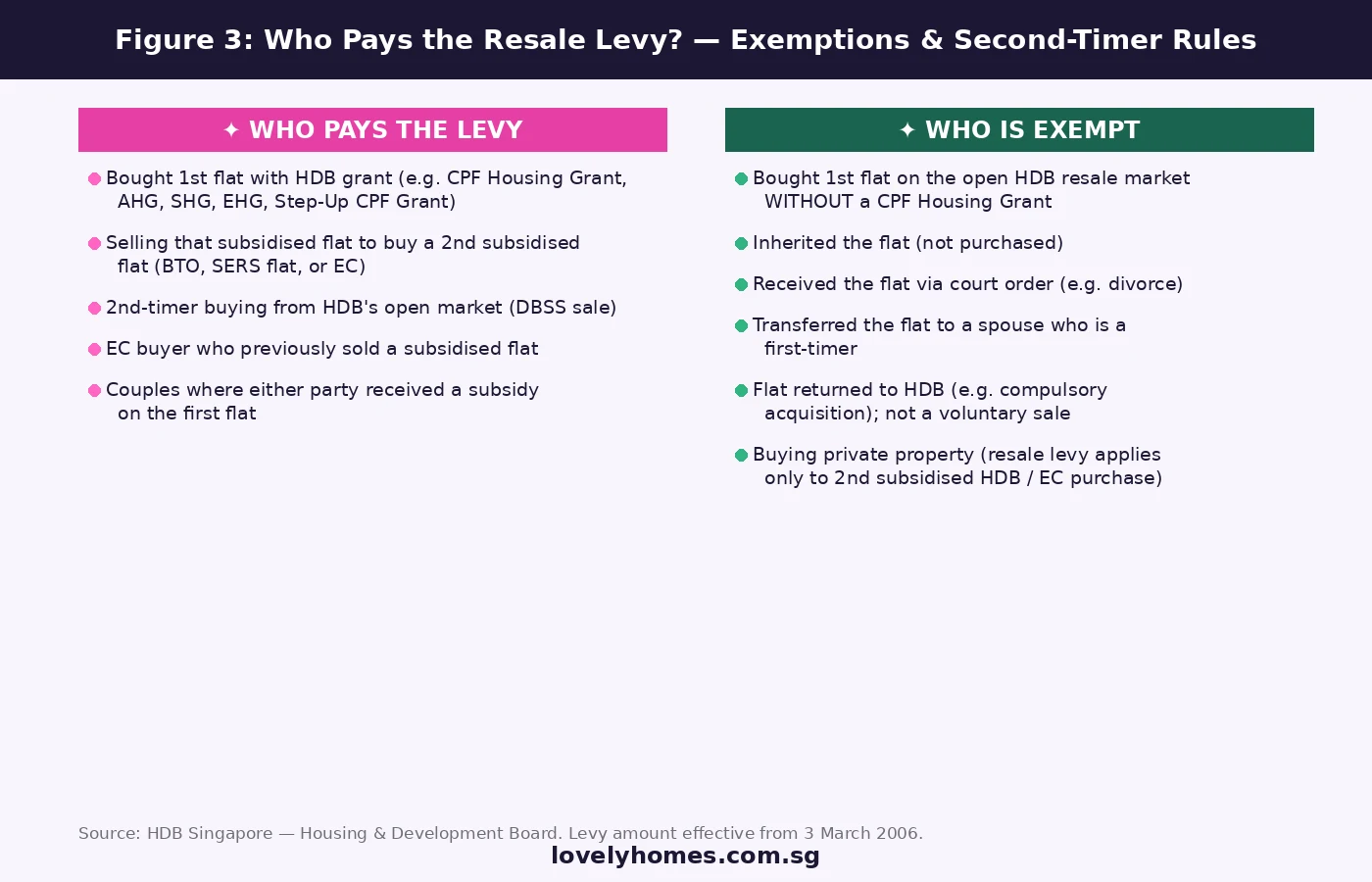

You (or your co-applicant, spouse, or essential occupier) previously purchased a subsidised HDB flat — meaning you received a CPF Housing Grant, AHG, SHG, EHG, Step-Up CPF Grant, or bought directly from HDB at a subsidised price in a Build-To-Order (BTO) or Selective En-bloc Redevelopment Scheme (SERS) exercise.

You subsequently sold that subsidised flat (or are in the process of doing so).

You are now applying to buy a second subsidised flat from HDB — either a new BTO flat, a SERS flat, a Design, Build and Sell Scheme (DBSS) unit, or an Executive Condominium (EC) unit from a developer.

The key point is that the levy applies to subsidised second-time purchases only. If your second property is a private condominium, a landed home, a resale HDB flat (from the open market), or any commercial property, no resale levy is chargeable. Many upgraders mistakenly believe the levy applies whenever they buy a second property — it does not. It is specifically a tax on accessing public subsidies a second time.

Couples and Joint Applications

For married couples and joint flat buyers, the resale levy status of either party is taken into account. If either the main applicant or the co-applicant previously received a housing subsidy, the levy is applicable to the household. This prevents a household from circumventing the levy simply by swapping the person listed as main applicant on the second purchase. The rule is designed to capture the household’s cumulative subsidy benefit, not merely the individual’s.

Singles

Singles purchasing under the Single Singapore Citizen (SSC) scheme — eligible for 2-Room Flexi BTO flats — are also subject to the levy if they previously benefited from a housing subsidy. As the levy amount for a 2-Room Flexi flat is S$15,000, it is still a meaningful cost for solo buyers planning to upsize.

HDB Resale Levy Amounts (2026)

The levy amount depends on the type of flat you previously sold. Since 3 March 2006, the rates have been fixed at the following flat-type level:

Flat Type Sold (First Flat)

Resale Levy Payable

Notes

2-Room Flexi

S$15,000

Applies to subsidised 2-Room Flexi BTO flats

3-Room

S$30,000

—

4-Room

S$40,000

Most common upgrader profile

5-Room

S$45,000

—

Executive Flat

S$50,000

HDB Executive flat (not EC)

DBSS Flat

S$55,000

Design, Build and Sell Scheme (discontinued)

EC (Executive Condominium)

5% of resale price

Capped at S$55,000; applies after the EC’s 5-year MOP when sold on the open market

One common source of confusion is that the levy is based on the type of flat you sold, not on its resale price. Whether you sold your 4-Room flat for S$500,000 or S$900,000, the levy is always S$40,000. The EC rule is the sole exception: there the levy is 5% of the EC’s resale price (i.e. the proceeds from selling the EC), subject to a maximum of S$55,000.

Figure 2: Resale Levy by Flat Type (2026). The levy is flat-based, not price-based — except for EC where it is 5% of resale price, capped at S$55,000. Source: HDB Singapore.

How and When Is the Resale Levy Paid?

The resale levy is settled automatically at the completion of the sale of your first flat. HDB deducts the levy amount from the CPF Ordinary Account (OA) refund you would otherwise receive when the flat sale is completed. You do not receive a separate invoice from HDB and you do not make a cash payment at any counter.

Here is how the sequence works:

Apply to buy second flat: When you apply for a BTO flat or EC as a second-timer, HDB identifies your levy status at the point of application.

HDB confirms levy payable: HDB notifies you of the levy amount in the appointment letter for your second flat booking.

First flat sold: On the day of the legal completion of your first flat sale, the CPF Board refunds your OA principal and accrued interest as usual — but before the refund is credited to you, HDB deducts the levy amount directly from those CPF proceeds.

Balance returned: The net CPF refund (after levy deduction) is credited to your OA account.

What If Your CPF Refund Is Less Than the Levy Amount?

This can happen in rare situations — for instance, if the outstanding HDB loan and CPF accrued interest together consume most of the sale proceeds. In such cases, the shortfall must be made up in cash. HDB will require you to pay the difference out-of-pocket before the second flat booking proceeds. This is one reason why financial planning ahead of an upgrade is important: always model your net CPF position against the levy amount before committing to a second BTO application.

Who Is Exempt from the HDB Resale Levy?

Not everyone who has previously owned an HDB flat will be required to pay the resale levy. Key exemptions include:

Resale flat purchased without a CPF Housing Grant: If you bought your first flat on the open HDB resale market and did not receive any CPF Housing Grant (Family Grant, Enhanced Housing Grant, Proximity Housing Grant, or any earlier-generation grant), you are not a “subsidised” flat owner for levy purposes. The levy reflects subsidy recovery — without a subsidy, there is nothing to recover.

Inherited flat: If the flat was left to you in a will or through intestacy, you did not receive a direct purchase subsidy, so the levy does not apply.

Court order transfer: Flats transferred to one party as part of a divorce settlement are generally exempt because the transfer is not a voluntary purchase attracting a subsidy.

Private property purchasers: The levy applies only when the second purchase is a subsidised BTO flat or EC. Upgraders to private property are not subject to the levy — though they face ABSD (Additional Buyer’s Stamp Duty) instead.

Flat returned to HDB involuntarily: If your first flat was compulsorily acquired by the government (e.g. for road widening or MRT works), this is not considered a voluntary sale and the levy is not triggered.

Figure 3: Who Pays vs Who Is Exempt — HDB Resale Levy 2026. Source: HDB Singapore.

Worked Example: The Tan Family’s Second BTO Application

Scenario

Mr and Mrs Tan (both Singapore Citizens) purchased a 4-Room BTO flat in Tampines in January 2019 at S$420,000, using a CPF Housing Grant of S$40,000. They have fulfilled the 5-year Minimum Occupation Period (MOP) and sell the flat in July 2026 for S$710,000.

They are applying for a new 5-Room BTO flat in Tengah at a subsidised price of S$620,000 — a second subsidised HDB purchase, making them second-timers.

The Tans’ second flat purchase proceeds normally. The S$40,000 levy is handled automatically by HDB and CPF Board; neither party needs to make a separate payment. The net cash received is S$197,000, which can go toward the downpayment and costs of the new flat.

Special Situations and Edge Cases

EC Owners Selling and Buying a Second BTO

If you bought an EC (fully privatised after 10 years) and now wish to purchase a new BTO flat, you are subject to the resale levy at 5% of the EC’s resale price, subject to a maximum of S$55,000. Because EC prices have risen significantly — many ECs in mature estates now resale at S$1.2M–S$1.8M — the effective levy is almost always the capped S$55,000. For example, an EC sold for S$1.4M would attract a levy of S$70,000 in the absence of the cap; the cap holds it at S$55,000.

SERS Flat Recipients

Households that received a replacement flat under the Selective En-bloc Redevelopment Scheme (SERS) are treated as having received a housing subsidy. If they subsequently wish to buy a second new flat from HDB or an EC, the levy applies based on the type of flat they were re-housed in.

Divorce and Reassignment of Flat Ownership

When a flat is transferred to a divorced spouse under a court order, that spouse is considered a second-timer if the transferred flat was a subsidised purchase. If they later apply for a new BTO flat, the levy will apply. Seeking early legal advice on how divorce asset division affects CPF and HDB subsidy status is advisable.

Concurrent Applications

Some second-timers apply for a BTO flat while still occupying their first flat. HDB allows this — but the levy is held in reserve and deducted at the point of the first flat’s sale completion. You must sell your first flat within 6 months of collecting the keys to the second (this is the standard condition for second-timers purchasing new flats).

Why the Resale Levy Matters for Your Upgrade Strategy

The resale levy is one of several interlocking costs that second-timer households must budget for when planning an upgrade within the public housing system. It is easy to overlook because it is deducted automatically from CPF, making it feel invisible — but it directly reduces the cash and CPF resources available for your second flat.

Consider the total cost of a 4-Room BTO upgrade: beyond the flat price itself, a second-timer household must account for the Buyer’s Stamp Duty (BSD) on the new flat, legal fees, potential income grant reductions (second-timers receive smaller EHG amounts than first-timers), renovation costs, and the S$40,000 resale levy. These costs collectively can reduce the effective CPF buffer you have on hand.

In contrast, upgrading to private property involves no resale levy — but attracts ABSD of 20% as a second property purchase (if you own the HDB flat at the time of buying private, and have not yet sold it). The ABSD on a S$1.5M private property would be S$300,000 — a very different magnitude. Households navigating this choice should consider the full cost picture of each route. Our ABSD Singapore 2026 Complete Guide and HDB Upgrader Guide 2026 cover the private-property upgrade path in detail.

Frequently Asked Questions — HDB Resale Levy 2026

Q1. Can I avoid the resale levy by selling my flat before applying for the BTO?

No. Your levy status is determined by your subsidy history, not by the sequence of sale and purchase. Whether you sell before or after booking the BTO flat, the levy still applies because you previously received a CPF Housing Grant. Selling early may give you more CPF OA funds to draw on, but it does not remove the levy obligation.

Q2. My spouse is a first-timer. Does the household still pay the levy?

Yes. HDB assesses the household as a unit. If either the main applicant or co-applicant has previously received a housing subsidy, the entire household is classified as a second-timer for levy purposes. There is no mechanism to apply as a “first-timer” household if one party is a second-timer. However, in this situation, the household may be eligible for a reduced levy in some cases — consult HDB directly for your specific profile.

Q3. Is the resale levy the same as the CPF accrued interest I must return?

No — these are two completely different obligations. CPF accrued interest (at 2.5% p.a.) is the amount you owe your own CPF account for the OA savings you withdrew to pay for the flat. It is returned to your OA upon sale — you are repaying yourself. The resale levy, in contrast, is paid to HDB as a subsidy recovery charge. Both deductions happen at the point of sale, but they serve entirely different purposes and go to different places.

Q4. Can I use CPF to pay the resale levy, or must it come from cash?

The levy is deducted automatically from the CPF OA refund you receive when your first flat is sold. You do not need to arrange a separate cash payment unless your CPF refund is insufficient to cover the levy — in which case HDB will require the shortfall in cash before releasing the booking fee for your new flat. Always check your estimated CPF refund against the applicable levy amount before committing to a second BTO booking.

Q5. Does the resale levy apply if I buy an EC as a first-time EC buyer but sold an earlier subsidised flat?

Yes. If you are buying an EC and you previously sold a subsidised HDB flat, the resale levy is payable. The EC levy is the higher of: 5% of the resale price of your sold flat or (if you are selling a non-EC subsidised flat) the flat-type levy amount — unless you are selling the EC itself, in which case it is 5% of the EC’s resale price (capped S$55,000). HDB’s levy assessment letter, issued before your EC booking, will specify the exact amount applicable to your situation.

Q6. Has the HDB resale levy changed recently? Will it increase?

The flat-type levy rates have been unchanged since 3 March 2006. As at July 2026, there has been no announcement by HDB or the Ministry of National Development (MND) of any impending change to the levy framework. Given that BTO prices have risen considerably since 2006, some analysts have speculated that a levy increase is overdue — but this is speculative. Decisions on the levy are policy matters resting with MND. Monitor HDB press releases and MND Budget announcements for any changes.

Q7. What happens if I cannot sell my first flat in time to pay the levy before the second flat completion?

Second-timers purchasing a new HDB flat must generally sell their existing flat within 6 months of collecting the keys to the new flat. If you have not sold your first flat by the time you need to complete the purchase of the new flat, HDB may defer key collection or require you to arrange an interim cash payment for the levy amount. Contact HDB directly if your sale is delayed — they may grant a time extension in genuine cases, but this is not guaranteed and is assessed case by case.

Disclaimer: The information in this article is intended for general educational purposes only. HDB policies, levy amounts, and eligibility rules can change. Always verify current requirements directly with the Housing & Development Board (HDB), the CPF Board, and the Ministry of National Development (MND). This article does not constitute financial, legal, or property advice. Consult a licensed property agent (CEA-registered), a qualified financial adviser, or a solicitor for advice specific to your situation.

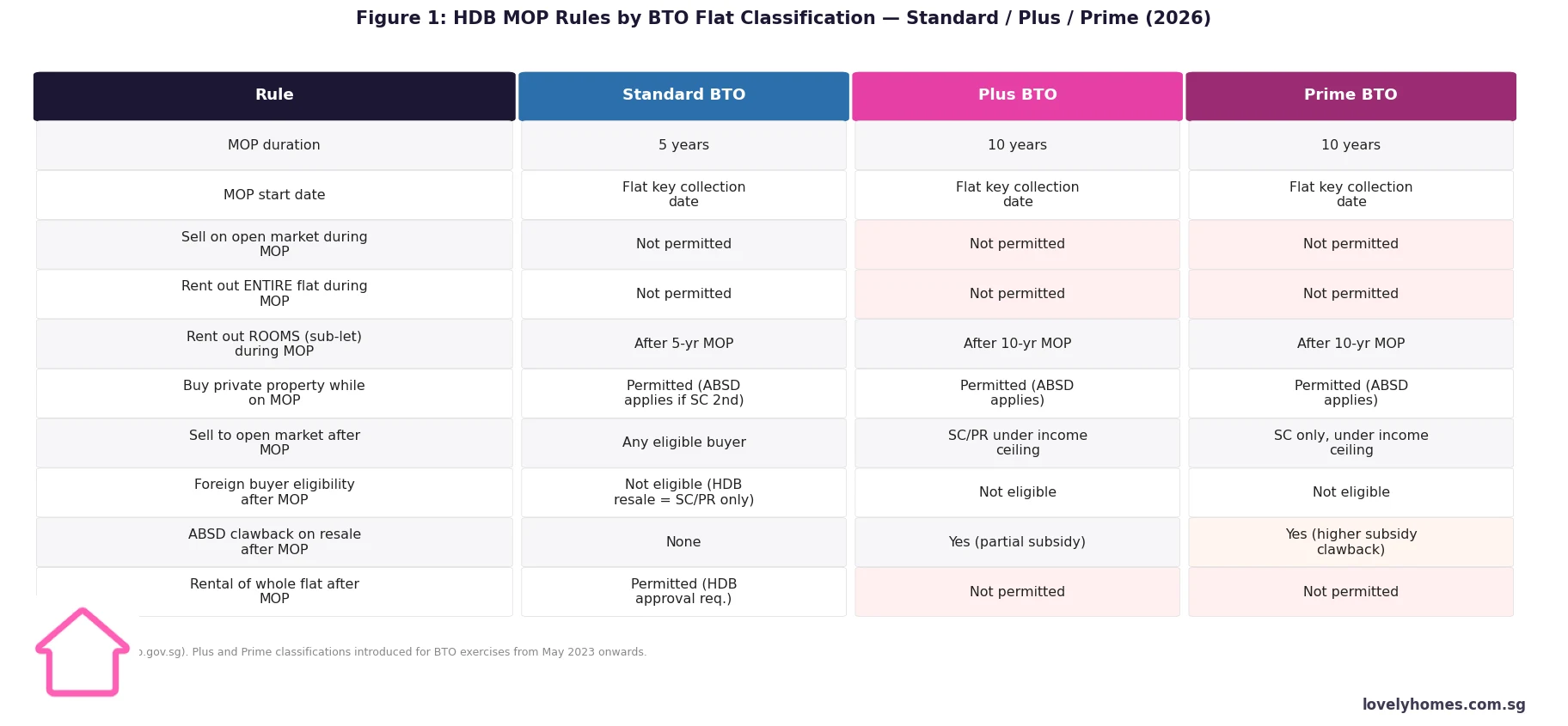

The HDB Minimum Occupation Period (MOP) is the mandatory period you must physically occupy your HDB flat before you can sell it on the open market, rent out the entire flat, or purchase a second private residential property without incurring the full ABSD burden. MOP is administered by HDB (Housing and Development Board).

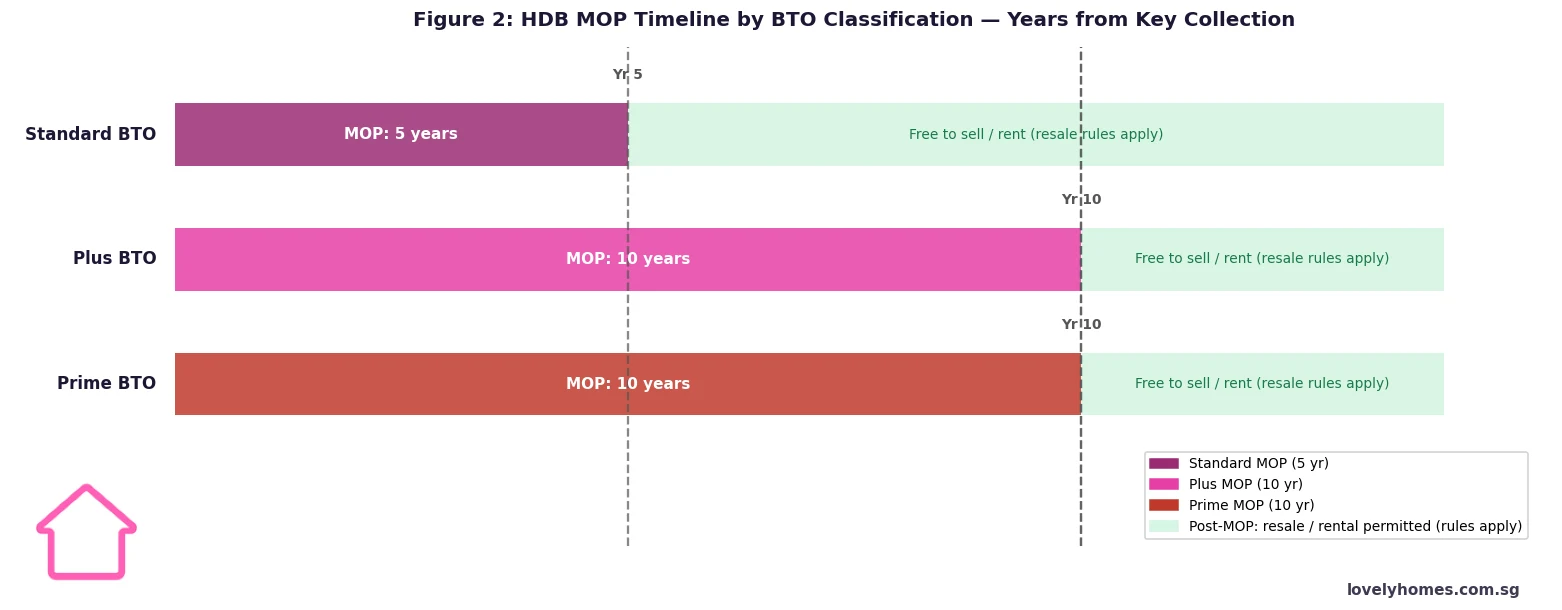

For Standard BTO flats, the MOP is 5 years from the date of key collection. For Plus and Prime BTO flats (introduced for BTO exercises from May 2023), the MOP is 10 years.

During the MOP, you cannot sell the flat, rent out the entire unit, or transfer ownership. You can, however, rent out individual rooms with HDB approval, and you may purchase private property (subject to ABSD).

After the MOP, Standard flat owners may sell to any eligible HDB buyer (SC or SPR). Plus flat owners must sell to SC or SPR buyers whose household income is within the prevailing income ceiling. Prime flat owners may only sell to Singapore Citizens whose household income is within the income ceiling.

Whole-flat rental after MOP is permitted for Standard flats (subject to HDB approval). It is not permitted at any time for Plus or Prime flats.

A subsidy clawback applies when Plus and Prime flats are sold on the open market — HDB recovers a portion of the housing grant and pricing subsidy. The clawback amount is higher for Prime flats.

The MOP clock starts from the date of key collection — not the date of BTO application, booking fee payment, or Temporary Occupation Permit (TOP). A flat collected in June 2024 has its Standard MOP expiry in June 2029.

What Is the MOP and Who Administers It?

The Minimum Occupation Period (MOP) is a statutory requirement under the Housing and Development Act, administered by the Housing and Development Board (HDB). It requires owners of HDB flats to physically occupy their flat for a minimum period before certain rights become available — primarily the right to sell on the open market, rent out the entire unit, or purchase a second private residential property.

The MOP exists for two complementary policy reasons. First, it ensures that subsidised HDB flats are used as genuine owner-occupied homes rather than short-term investment instruments. Second, it moderates the supply of resale HDB flats that enter the market at any one time, which helps to stabilise resale prices. The requirement has been part of Singapore’s public housing policy for decades, and HDB enforces it through its ownership records, which are cross-referenced against the buyer’s NRIC address for SC/SPR buyers.

Figure 1: HDB MOP Rules by BTO Classification — Standard, Plus and Prime (2026) | Source: HDB

Standard, Plus and Prime: The Three BTO Classifications

From the May 2023 BTO exercise onwards, HDB classifies all new BTO flats into one of three tiers based on location and subsidy level. This classification directly determines MOP length, post-MOP resale eligibility, rental rights, and subsidy clawback:

Standard flats are located in non-central, typically suburban estates (such as Tengah, Woodlands, Sembawang, and Punggol). They carry the lowest subsidies relative to market value and have the most permissive rules: 5-year MOP, resale to any eligible SC/SPR buyer, and whole-flat rental allowed after MOP with HDB approval.

Plus flats are located near transport nodes or commercial hubs, in estates that would otherwise be too pricey for first-timer buyers without additional subsidy. They come with a 10-year MOP, resale restricted to SC/SPR buyers within the prevailing income ceiling, and no whole-flat rental at any time.

Prime flats are located in the choicest sites — city-fringe, waterfront, or mature central estates like Kallang, Toa Payoh, and Marina South — where HDB provides the heaviest subsidies. They carry a 10-year MOP, SC-only resale (SPR buyers are ineligible), income ceiling restrictions, no whole-flat rental at any time, and the highest clawback rate.

Buyers are told which classification a flat falls under at the time of BTO application. The classification is permanently attached to the flat and does not change over time, even after resale. A Prime flat remains a Prime flat in every subsequent transaction.

Figure 2: HDB MOP Timeline by BTO Classification — Years from Key Collection (Singapore 2026)

What You Can and Cannot Do During the MOP

The MOP does not mean you are locked away from all activity — it specifically restricts disposal and whole-unit rental. The table below summarises key permitted and prohibited actions:

Activity

During MOP

After MOP (Standard)

After MOP (Plus/Prime)

Sell flat on open market

Not permitted

Permitted (SC/SPR buyers)

SC/PR (Plus); SC only (Prime); income ceiling applies

Rent out entire flat

Not permitted

Permitted (HDB approval)

Not permitted (ever)

Rent out rooms (sub-let)

Not permitted during MOP

Permitted (HDB approval)

Permitted (HDB approval)

Buy private property

Permitted (ABSD applies if SC 2nd property: 20%)

Permitted

Permitted

Transfer ownership (gift / divorce / death)

HDB approval case-by-case

Yes

Yes (subject to Plus/Prime resale rules)

Renovate / alter the flat

Permitted (HDB renovation permit)

Permitted

Permitted

Buying Private Property During the MOP

One of the most common questions from HDB flat owners is whether they can buy a private condominium before their MOP is up. The answer is yes — you are allowed to purchase private residential property in Singapore while your MOP is running. However, there are important financial consequences to consider.

If you are a Singapore Citizen owning an HDB flat (which counts as your first residential property) and you buy a private condo during the MOP, you are buying a second property. This means you pay 20% ABSD on the private property purchase. If you are an SPR, your second-property ABSD is 30%. The HDB flat itself remains subject to the MOP and cannot be sold until the MOP expires.

This means you will be servicing two housing loans simultaneously until the HDB can be sold — which requires careful TDSR planning. The TDSR cap of 55% applies across all outstanding loans. HDB loans (from HDB directly) and bank loans on HDB flats are both counted in TDSR. If the combined debt servicing ratio exceeds 55% when adding the private mortgage, financing for the private property may be declined.

What Happens When You Sell After the MOP

Once the MOP is fulfilled, the key restrictions are lifted — but resale rules still apply, especially for Plus and Prime flats:

Standard flats: May be sold to any eligible HDB resale buyer — SC or SPR, subject to standard HDB eligibility criteria (Ethnic Integration Policy quotas, family nucleus requirements, etc.). No income ceiling on the buyer.

Plus flats: May only be sold to buyers whose household income does not exceed the prevailing income ceiling (currently S$14,000/month for families, S$7,000 for singles). SPR buyers are eligible. A subsidy clawback is deducted from the sale proceeds on the first open-market resale.

Prime flats: May only be sold to Singapore Citizen buyers (SPR buyers are not eligible) whose household income does not exceed the income ceiling. The subsidy clawback rate is higher than for Plus flats and is also deducted from the first open-market resale proceeds.

The subsidy clawback is calculated as a percentage of the resale price (or market value, whichever is higher) and is paid to HDB at the point of resale. HDB has not publicly released a fixed clawback percentage table; the exact rate is determined and communicated at the time of application. This is intended to recover some of the subsidy advantage enjoyed by Plus/Prime buyers while still allowing them a fair profit on genuine capital appreciation.

The MOP and CPF Accrued Interest

When you sell an HDB flat after the MOP, any CPF funds used to purchase the flat (including the option fee, downpayment, and monthly mortgage instalments paid from your CPF Ordinary Account) must be refunded to your CPF accounts — along with accrued interest at the CPF OA interest rate (currently 2.5% per annum). This accrued interest represents what your CPF savings would have earned had they not been used for housing. On a long MOP (10 years), accrued interest can be substantial and reduces the net cash proceeds from the sale.

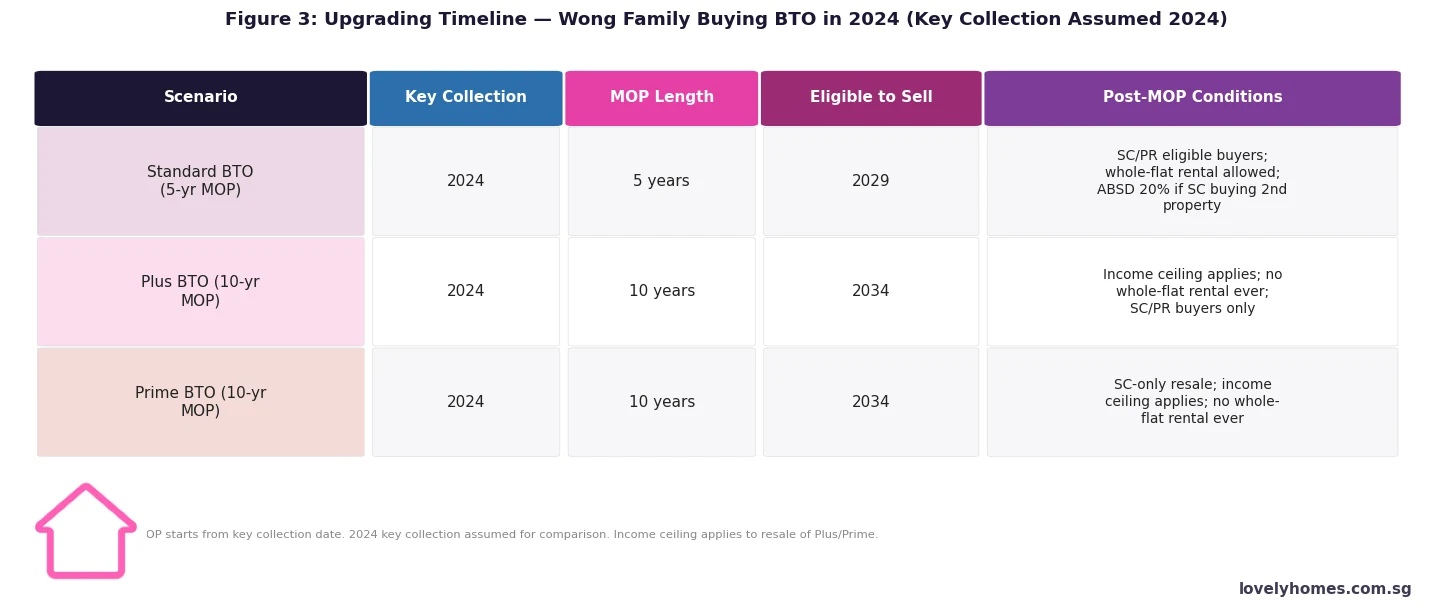

Worked Example: The Wong Family and the MOP Decision

Mr and Mrs Wong, both Singapore Citizens, purchase a 4-room BTO flat in Bishan (classified as a Plus flat) in June 2024. Key collection is in June 2024. Their household income is S$9,000/month. The purchase price is S$550,000.

Over the 10-year MOP, if the flat appreciates from S$550,000 to S$800,000 (a not unreasonable assumption for a Plus-classified Bishan flat), the Wongs would make a nominal gross gain of S$250,000. From this, HDB deducts the clawback (amount TBD at point of sale), plus CPF refund with accrued interest. On a S$550,000 purchase with 25% CPF downpayment (S$137,500) at 2.5% CPF OA rate over 10 years, accrued interest alone would be approximately S$38,700 — reducing net cash-in-hand from the sale. This is still a solid return, but buyers should model it carefully before factoring in the Plus flat subsidy as pure profit.

What This Means for HDB Buyers in 2026

The 10-year MOP for Plus and Prime flats is a significant commitment. A buyer collecting keys in 2026 cannot sell their Plus or Prime flat until 2036 at the earliest. Over that decade, Singapore’s property market will go through multiple cycles, interest rate shifts, and policy changes. Buyers who select Plus or Prime flats primarily because of the lower purchase price — and not because they genuinely intend to occupy the flat for 10 years — may find themselves in a difficult position if circumstances change (job relocation overseas, family expansion, divorce).

For those who do plan to stay, the Plus and Prime schemes deliver real value. A Prime flat in a central location at a subsidised price, occupied for 10 years with a no-rental restriction, is likely to appreciate meaningfully in absolute terms even after clawback. The restriction is the price of the subsidy.

What Might Come Next

The May 2023 introduction of Plus and Prime classifications represented a significant shift from the old Mature/Non-Mature estate binary. The April 2023 announcement also removed the ability of EC buyers to use the Deferred Payment Scheme from May 2026 — suggesting the government continues to tighten across all public and quasi-public housing tiers. Any further changes to MOP duration are unlikely in the near term given that the 10-year Plus/Prime MOP is relatively new and the government will want to assess its impact before adjusting. The resale income ceiling may, however, be revised upwards over time to track median income growth in Singapore.

When does the MOP start — from key collection or from BTO ballot application?

The MOP starts from the date of key collection — not the date of BTO application, not the ballot exercise date, and not the date you pay the option fee or sign the lease agreement. The key collection date is when you physically receive the keys to your flat and formally take possession. This date is recorded by HDB and serves as the MOP commencement date. For a Standard flat collected in July 2024, the MOP expires in July 2029. For a Plus or Prime flat collected in the same month, it expires in July 2034.

Can I rent out rooms in my HDB flat while the MOP is running?

No. During the MOP, you may not rent out any part of your flat — neither the entire unit nor individual rooms. Room rental (sub-letting) is only permitted after the MOP has been fulfilled and only with HDB’s prior written approval. After the MOP, Standard flat owners may rent out rooms or the entire flat (with HDB approval); Plus and Prime flat owners may rent out rooms after the MOP but may never rent out the entire flat under any circumstances.

What happens if I need to move overseas for work during the MOP?

If you need to work overseas temporarily, you must continue to maintain your HDB flat as your Singapore residence — meaning a family member must continue to reside in the flat, and you must return periodically. You cannot rent out the flat during the MOP even if you are overseas. If your overseas stint is long-term and the flat will genuinely be unoccupied, you should consult HDB directly. Abandoning the occupancy requirement during the MOP can result in HDB compulsorily acquiring the flat at a below-market price under the Housing and Development Act — a severe consequence that buyers should be aware of.

Can I buy a private condo while my HDB MOP is still running?

Yes. Purchasing a private residential property while your HDB MOP is outstanding is permitted. However, since your HDB flat counts as your first residential property, the private condo purchase is classified as a second property for ABSD purposes. A SC pays 20% ABSD on the private condo. An SPR pays 30%. You must also have the financial capacity to service both housing loans simultaneously and remain within the 55% TDSR cap. Many HDB owners choose to exercise this option a year or two before their MOP expires, so the HDB can be sold shortly after the MOP milestone — reducing the period of dual-loan exposure.

What is the subsidy clawback for Plus and Prime flats, and when is it paid?

The subsidy clawback for Plus and Prime flats is paid to HDB at the point of the first open-market resale (i.e., the first resale transaction after the MOP). It is deducted from the sale proceeds before any balance is paid to the seller. The clawback is calculated as a percentage of the resale price or market valuation (whichever is higher). HDB has not published a fixed percentage table publicly; the exact rate is communicated in the flat purchase document at the time of BTO booking and is specific to the flat’s classification and location. The clawback only applies to the first open-market resale — subsequent owners of a Plus or Prime flat do not face an additional clawback when they eventually sell.

Do MOP rules apply to HDB flats purchased on the open resale market?

Yes. When you purchase an HDB resale flat — whether Standard, Plus, or Prime — the MOP requirement applies afresh from the date you collect the keys. A Standard resale flat has a 5-year MOP from your key collection date; a Plus resale flat has a 10-year MOP; and a Prime resale flat has a 10-year MOP. The classification (Standard, Plus, Prime) of the flat follows it through all transactions. You cannot shorten the MOP on a resale flat because the previous owner already fulfilled their MOP.

Can an SPR buyer purchase a Plus or Prime HDB flat on the open resale market?

For Plus flats: yes, subject to the income ceiling (S$14,000/month household income) and standard SPR eligibility criteria. For Prime flats: no — Prime flats may only be resold to Singapore Citizens (not SPR). This restriction applies to every resale of a Prime flat in perpetuity, not just the first resale. SPR buyers wishing to purchase Plus flats must also form an eligible family nucleus (e.g., SC/SPR family or SPR household of two or more) to qualify under HDB’s resale eligibility framework.

Disclaimer: This article is for general information only and does not constitute legal or financial advice. HDB rules, MOP durations, clawback rates, and eligibility criteria are subject to change by HDB and the Ministry of National Development. Always verify the latest requirements at hdb.gov.sg and consult HDB directly or a licensed HDB resale agent for guidance specific to your situation. All figures and scenarios are illustrative and based on publicly available data as at 16 May 2026.

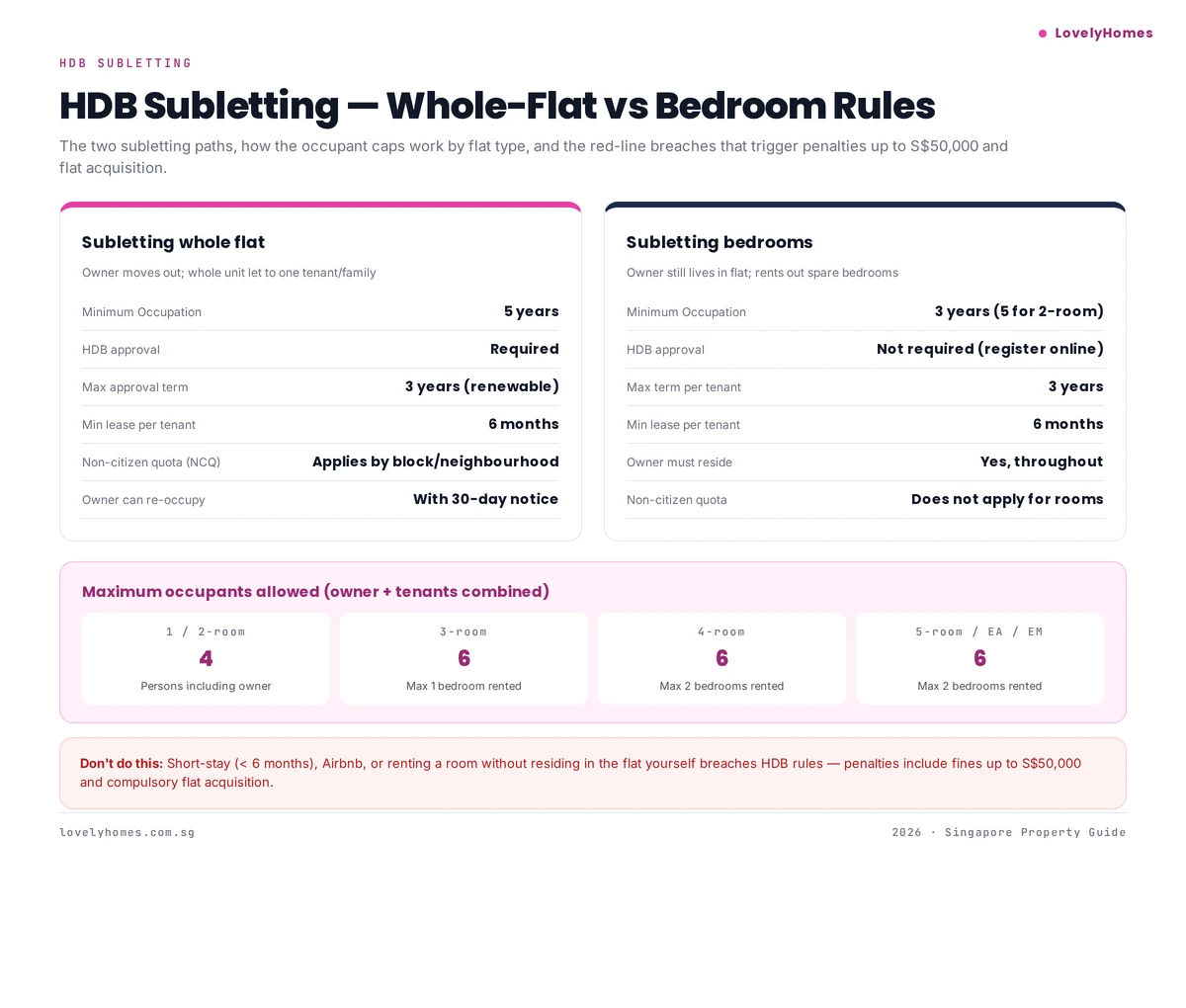

HDB owners can sublet whole flat after 5-year MOP (HDB approval required, max 3 years per approval, non-citizen quota applies) or sublet bedrooms after 3-year MOP (5 years for 2-room, no HDB approval needed but online registration required, owner must still live in the flat). Minimum lease is 6 months per tenant — no Airbnb, no short-stay. Breaches risk fines up to S$50,000 and compulsory flat acquisition.

HDB subletting is the single most rule-bound corner of the Singapore rental market. The policies exist because HDB is public housing, funded by subsidies and grants, and subletting concessions try to balance owner flexibility with social objectives (owner-occupation, ethnic integration, housing supply). The rules are enforced — HDB audits tenanted flats and compulsory acquisition is a real outcome for breaches.

This guide lays out the two subletting paths (whole flat vs bedrooms), the occupant caps, and the red lines you cannot cross.

For broader landlord obligations (licensing, tax, TA clauses), see our landlord’s guide. For more context on HDB rules generally, read our MOP rules guide.

Whole-flat vs bedroom subletting, occupant caps, and breach penalties

The two subletting paths at a glance

Rule

Whole-flat subletting

Bedroom subletting

MOP required

5 years (all flat types)

3 years (5 yrs for 2-room)

HDB approval

Required before tenancy

Register online; no approval needed

Owner must occupy

No — owner can live elsewhere

Yes — owner must still live in the flat

Max approval term

3 years per renewal

3 years per tenant

Min lease per tenant

6 months

6 months

Non-citizen quota

Applies (block + neighbourhood)

Does not apply

Ethnic quota (EIP/SPH)

Applies

Applies in certain cases

Whole-flat subletting in depth

Whole-flat subletting is allowed only after the full 5-year Minimum Occupation Period from key collection. Apply via HDB InfoWEB with:

Tenant’s NRIC/FIN and work/student/dependent pass

Proposed tenancy term and rent

S$20 non-refundable admin fee

Declaration of the owner’s temporary residential address

HDB typically approves within 2–3 weeks. The approval is valid for up to 3 years and can be renewed. Non-Citizen Quota (NCQ) may block some rentals if the block or neighbourhood has already reached its foreigner cap.

Bedroom subletting in depth

Bedroom subletting is simpler because the owner stays — HDB treats it more like house-sharing than a full rental. Register the tenant’s details on HDB InfoWEB within 7 days of the tenancy starting. No formal approval needed.

Key constraint: the occupant cap includes both the owner’s household and any subletted bedroom tenants.

Maximum occupants by flat type

Flat type

Max occupants

Max bedrooms rented

1-room / 2-room

4

1 bedroom

3-room

6

1 bedroom

4-room and above

6

2 bedrooms

Where the occupant cap used to be based on flat size, HDB moved to a hard cap of 6 persons in 2024 for most flat types to curb overcrowding and nuisance complaints.

What counts as a breach

Red-line breaches that trigger HDB enforcement:

Short-stay rentals under 6 months — includes Airbnb, Booking.com short lets, weekend stays, room-by-night.

Subletting the whole flat before MOP.

Subletting rooms before 3-year MOP, or 5-year for 2-room flats.

Subletting rooms without the owner residing in the flat.

Exceeding the occupant cap (even by one person).

Letting to tenants without a valid pass or to unauthorised nationalities.

Not registering bedroom subletting on HDB InfoWEB.

Accepting rental payments in cash without records (complicates dispute resolution and IRAS audits).

Penalties

HDB’s enforcement ladder, from lightest to most severe:

Written warning for minor paperwork lapses.

Financial penalty — fines up to S$50,000.

Compulsory acquisition of the flat for serious or repeated breaches. Owner receives compensation at HDB’s determined valuation — typically below market.

Debarment from buying another HDB flat or applying for HDB rental.

Frequently asked questions

Can I rent my HDB flat on Airbnb even if it’s for friends only?

No. The 6-month minimum lease rule applies regardless of who the tenant is. Any stay below 6 months is a breach, even if unpaid.

Can I sublet while I’m overseas for work?

Yes — this is a common use case for whole-flat subletting after MOP. You need HDB approval and must notify HDB of your overseas address. You can return any time.

Does bedroom subletting affect my PR sponsorship or home loan?

No direct effect on PR or citizenship applications. It may affect your TDSR if banks treat rental income as supplementary (they typically use 70–80% of the rent in TDSR calculations).

What’s the non-citizen quota?

HDB caps the percentage of non-Malaysian foreigners who can occupy flats in a block and neighbourhood. If your block has hit the cap, HDB will reject your subletting application until a spot opens up.

Disclaimer

This guide is for general information only. Singapore’s rental rules, HDB policies, and IRAS stamp duty rates change periodically. Always verify against the HDB, URA and IRAS websites before signing a lease or filing with IRAS. LovelyHomes is not a licensed property agent or tax adviser. For personalised advice, please engage a registered CEA agent or a qualified tax professional.

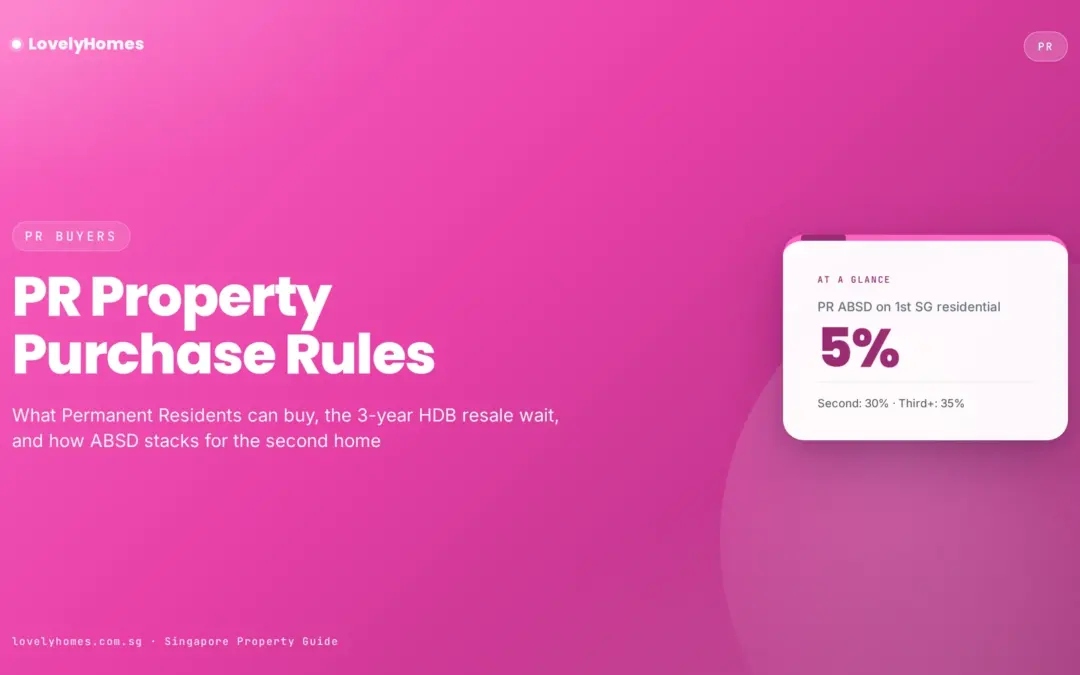

A Singapore Permanent Resident can buy private condos from day one of PR status, paying 5% ABSD on the first residential purchase (30% on second, 35% on third+). HDB resale flats open to PRs only after 3 years of PR status, and require a qualifying family nucleus. PRs cannot buy new BTO, Plus, Prime or EC flats. Landed property on the mainland needs LDAU approval. If you buy an HDB flat as a PR, MOP and subletting rules mirror citizens.

Permanent Residency fundamentally changes a buyer’s property menu in Singapore — but not overnight. From day one, private property opens. HDB resale still waits three years. New HDB (BTO/Plus/Prime) and new ECs remain closed to PRs regardless of wait time.

This guide maps the PR property timeline, the full 2026 ABSD ladder for PR buyers, the most common mistakes PRs make when disposing of existing property, and the rules PRs should know before taking out a CPF loan. For the foreigner-side equivalent, see our foreigner property guide.

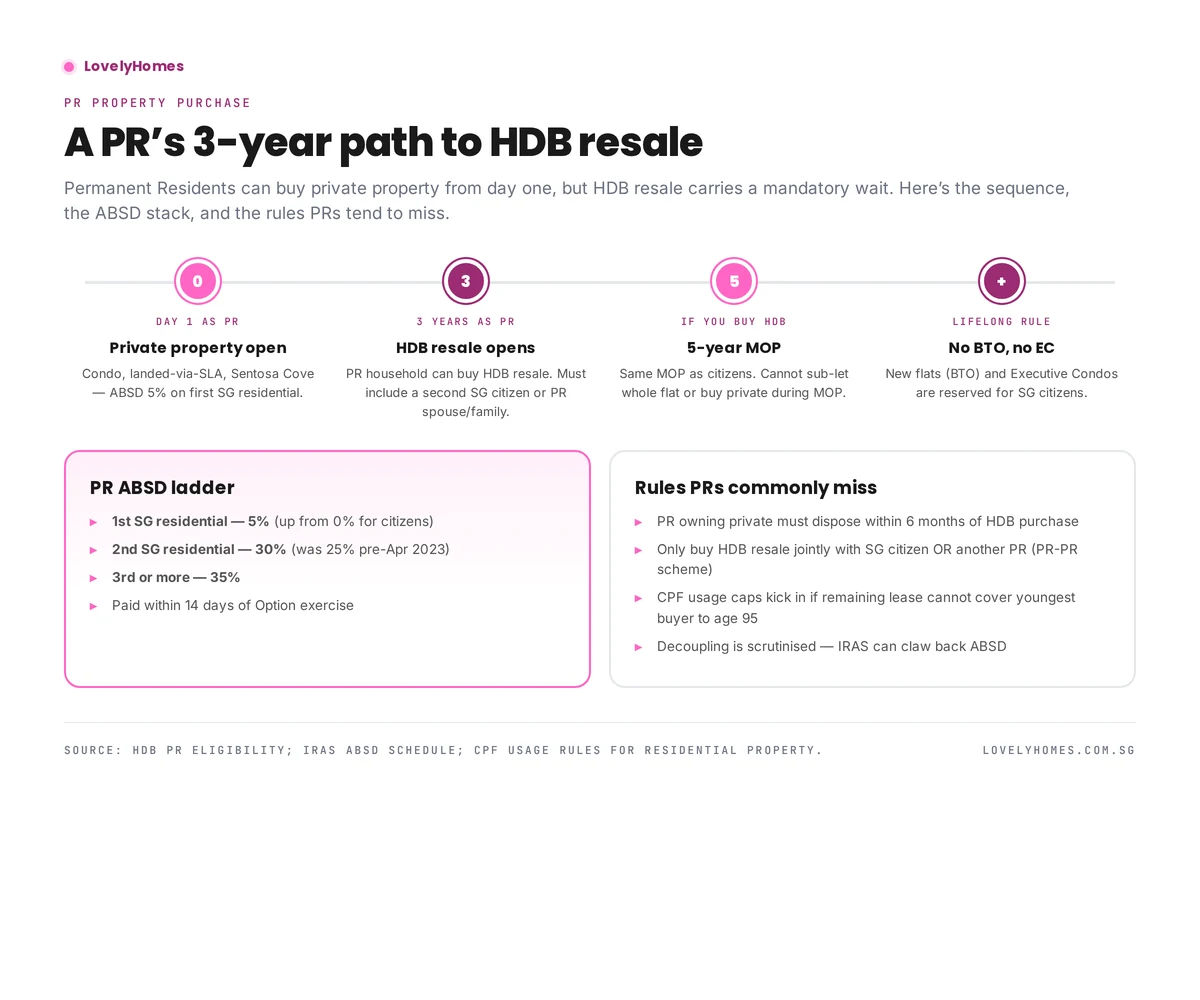

A PR’s 3-year path to HDB resale.

The PR property timeline

Day 1 as PR

Private condo, landed-via-LDAU, and Sentosa Cove landed open immediately. CPF usage opens once the PR has active OA/SA balances. LTV, TDSR and MSR frameworks are identical to citizens.

3 years as PR

HDB resale opens. A PR household must form a qualifying family nucleus — typically a PR applicant with a spouse (PR or SG citizen), or the PR-PR Scheme (both applicants PRs for at least 3 years).

5 years after HDB purchase (if you buy HDB)

Minimum Occupation Period. Same 5-year MOP as citizens. Cannot sub-let the entire flat, cannot buy private residential, cannot sell on the open market. See our MOP rules guide.

Lifetime rule

PRs cannot buy new BTO, new Plus, new Prime or new EC flats. These are reserved for SG citizens with a citizen spouse or fiancé(e). The only HDB route for PRs remains the resale market.

ABSD for PRs — the 2026 ladder

Residential count

ABSD (PR)

Notes

1st SG residential

5%

Up from 0% that citizens pay

2nd SG residential

30%

Raised from 25% in Apr 2023

3rd or more

35%

Raised from 30% in Apr 2023

ABSD is payable within 14 days of Option exercise, on top of BSD. If two PRs buy jointly, the ABSD is calculated on the highest-count profile among the buyers.

The HDB-specific rules PRs must follow

Dispose of private within 6 months

A PR who owns private residential (in Singapore or overseas) must dispose of it within 6 months of the HDB resale completion. This is usually the biggest surprise for incoming PR buyers — overseas apartments count.

CPF usage and the lease rule

CPF can fund the purchase only if remaining lease covers the youngest buyer to age 95. For older HDB stock this is a real constraint — see our CPF for property guide.

No grants (mostly)

Most HDB grants (EHG, Family Grant, Proximity Housing Grant) are reserved for SG-citizen first-timer households. A PR-PR couple does not qualify for EHG. However, a PR with an SG-citizen spouse may qualify under the standard first-timer framework — see our grants guide.

Landed and Sentosa Cove

PRs need LDAU approval under the Residential Property Act to buy landed on the mainland — rarely granted except for long-tenured PRs with strong local ties. Sentosa Cove landed is much more accessible: SLA approval is routinely granted for owner-occupation.

Common PR mistakes

Forgetting the 3-year HDB wait. Newly-minted PRs cannot buy HDB until year 3.

Holding overseas property while buying HDB. HDB will compel disposal within 6 months.

Attempting decoupling to reset ABSD. IRAS actively scrutinises PR decoupling post-2022 and may claw back ABSD. See our decoupling guide.

Using CPF on a lease-short flat. Always check the lease-to-95 calculator first.

Frequently asked questions

Can a PR buy an EC?

Not a brand new EC — that’s citizen-only. A PR can buy a privatised EC (post-10-year MOP + privatisation), because by then it is effectively private property.

Can two PRs buy HDB resale together?

Yes — under the PR-PR Scheme, both must have been PR for at least 3 years. Grants are not available.

What if I become a citizen after buying HDB as a PR?

The flat becomes a citizen-owned flat. Any remaining rules (MOP, subletting) still apply from the purchase date.

Does a PR pay the 60% foreigner ABSD?

No. PR status attracts the PR ladder (5% / 30% / 35%) — not the foreigner flat rate.

This guide is for general information only and is accurate as of April 2026. Singapore property rules, taxes and cooling measures change frequently — always verify current figures with URA, IRAS, HDB or a licensed professional before committing. LovelyHomes is not a financial, legal or tax advisor.

The Minimum Occupation Period (MOP) is the single most important HDB rule for any flat owner. It governs when you can sell, when you can rent out the whole unit, and even when you can buy a second property. This 2026 guide explains the 5-year standard rule, how the clock starts and when it can pause, the rare exceptions, and exactly what unlocks once MOP is fulfilled.

For the official rules, see the HDB MOP page. This article explains what those rules mean in practice.

Quick Answer — MOP in 60 Seconds

Standard MOP: 5 years from key collection — applies to most BTO, SBF, and resale flats.

Plus and Prime flats: 10 years MOP (introduced 2024).

Clock starts the day you legally take possession, not the day you apply or ballot.

Clock pauses when you are overseas for 6 months or more continuously.

Exceptions: divorce, death of spouse, financial hardship — case by case with HDB.

MOP unlocks the right to sell, rent the whole flat, and buy private property without disposing of the HDB.

The standard MOP is 5 years — the clock pauses for extended time overseas, and the consequences of breach are severe.

What Is MOP?

The Minimum Occupation Period is the number of years you must live in your HDB flat before you can sell it, rent it out as a whole unit, or use it to qualify for a second home purchase. It is HDB’s tool for ensuring public housing subsidies flow to people who actually need a home — not to speculators who buy and flip.

MOP is personal: it is the owner who must have occupied the flat for the period, not just anyone. If all listed owners have moved out within MOP (say, for overseas work), the clock pauses until at least one owner returns.

The 5-Year Standard

For most HDB flats — standard BTO, resale, SBF — the MOP is 5 years. This applies to:

All BTO flats except Plus and Prime

SBF (Sale of Balance Flats) purchases

Resale flats purchased on the open market

Executive Condominiums (for the EC-as-HDB period)

DBSS (Design, Build, Sell Scheme) flats

The 10-Year MOP: Plus and Prime Flats

Introduced in 2024, the revised BTO classification creates two new categories with extended MOP:

Plus flats

Plus flats are located in choice mature-estate areas that are not classified as “core central”. They have:

10-year MOP from key collection

Future-buyer income ceiling applied on resale (restricts buyer pool)

Subsidy clawback at resale computed by HDB

Prime flats

Prime flats are in genuinely core central locations (Tanjong Pagar, Queenstown, Rochor, etc.). They have all of the Plus restrictions, plus an even higher subsidy clawback at resale.

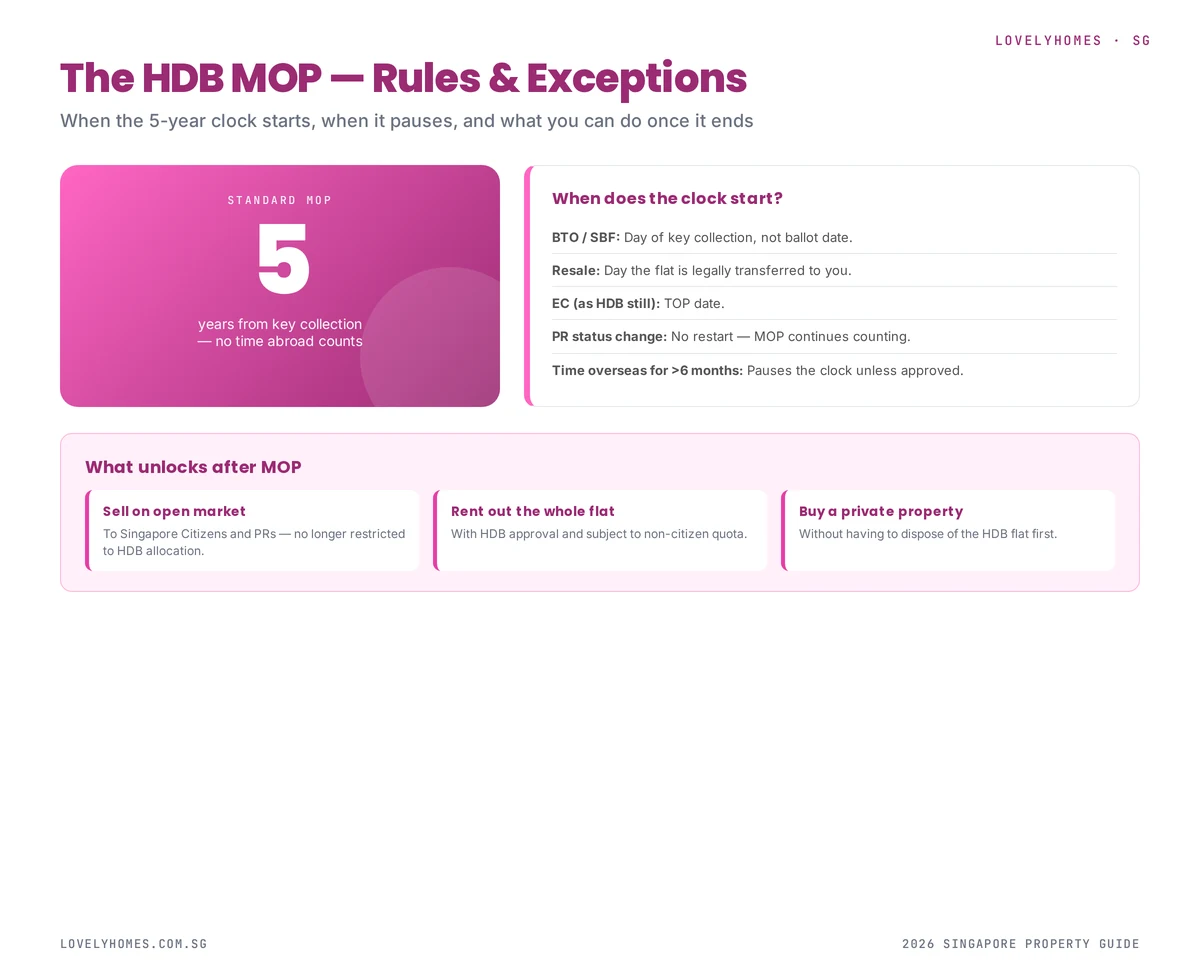

When Does the Clock Start?

The MOP clock starts on the day of key collection, not on:

The ballot date of your BTO application

The signing of the Lease Agreement

The purchase completion date (for resale, these are the same day)

The date you actually move in (if different from key collection)

You can verify the exact date on your HDB My Home record via Singpass. It is worth noting the date somewhere — the 5th anniversary is the earliest you can register Intent to Sell.

When Does the Clock Pause?

MOP is an occupation requirement. If no one who owns the flat is actually living in it for an extended period, the clock pauses. The standard trigger is 6 continuous months overseas by all listed owners.

How HDB tracks overseas status

Under the Income and Property Declaration required during resale applications, HDB cross-references ICA travel records. If your records show you were overseas for a year during MOP, your effective MOP date is pushed back by a year.

What counts as “overseas”

Overseas employment (with or without HDB approval)

Study overseas

Extended travel or sabbatical

Caring for family overseas

Short trips (weeks), business travel, holidays, and study leave that total less than 6 months per calendar year generally do not pause the clock.

Exceptions to the 5-Year Rule

HDB permits early disposal in a narrow set of circumstances:

1. Divorce

If the owners divorce within MOP, HDB may approve early disposal if neither party can afford to keep the flat. Ownership can also be transferred to one party under a court order.

2. Death of a spouse or co-owner

Surviving owner(s) can retain the flat without breach. If the surviving household falls below the minimum family nucleus requirement, HDB may require the flat to be sold.

3. Severe financial hardship

Documented financial distress (bankruptcy, serious illness, prolonged unemployment) may qualify for early disposal. Case-by-case with HDB’s Financial Assistance team.

4. Change in family circumstances

Marriage resulting in ineligibility under the original scheme, or purchase of a new flat under a scheme that requires disposal of the existing flat, may qualify.

What Unlocks Once MOP Is Fulfilled

1. Sell on the open market

You can register Intent to Sell and market the flat to Singapore Citizens and PRs (subject to the block’s EIP cap).

2. Rent out the whole flat

Previously you could only rent individual rooms while occupying the flat. After MOP, with HDB approval, you can rent the entire unit. Subletting quota rules (e.g. 1 non-citizen cap for non-Malaysian foreigners) still apply.

3. Buy private property without disposal

Before MOP, if you wanted to buy a private property, you would need to dispose of the HDB within 6 months of TOP of the new property. After MOP, you can hold both — subject to ABSD and TDSR implications. See our ABSD guide.

4. Apply for a second BTO or resale

Post-MOP, if you sell the original flat, you can re-enter the BTO / resale market as a second-timer buyer (with reduced grant eligibility but still eligible).

Consequences of Breaching MOP

Breaching MOP is treated seriously by HDB. Possible consequences include:

Compulsory acquisition of the flat at HDB’s administered price — typically below market value.

Financial penalty equivalent to the subsidy or concessionary loan received.

Banning from future HDB purchases for a period of years.

Referral for prosecution in cases of fraudulent misrepresentation (e.g. fake tenancy agreements).

The most common accidental breach is renting out the whole flat before MOP. If you must be overseas during MOP, sublet only individual rooms with HDB approval.

MOP and Your Financial Planning

Knowing your exact MOP date lets you plan key life decisions:

Upgrading to a condo? Target MOP + condo launch cycle for maximum CPF refund and minimum ABSD complexity.

Moving for work? Understand how overseas time pauses the clock so you don’t miss MOP by years.

Family expansion? Post-MOP flexibility (sell, rent, or buy additional property) enables better choices.

Rental income? Model the income stream against the HDB subletting quota rules.

FAQ — HDB MOP 2026

What is the shortest possible MOP?

5 years for standard flats. Plus and Prime flats are 10 years. There is no way to reduce the MOP shorter than these limits through any scheme.

Does becoming a PR after buying restart my MOP?

No. Citizenship status changes do not restart the MOP clock. The 5 years begin from key collection regardless.

Can I count time spent at my parents’ house toward MOP?

No. MOP requires occupation of your specific flat. Time spent elsewhere, even with family, does not count.

Does the MOP transfer to a new co-owner I add later?

Adding an owner does not restart the clock, but the added owner’s MOP is measured from the date they become an owner. This matters if they intend to use MOP completion for their own eligibility (e.g. to apply for a second property).

Can I sell the flat through a private sale after MOP, to avoid HDB involvement?

No. All HDB flat transactions must go through HDB’s resale process. Private sales of HDB flats outside the HDB framework are not permitted.

Disclaimer: This is general information, not legal advice. HDB evaluates MOP edge cases on a case-by-case basis — if your situation is unusual, contact HDB directly before making any plans.