Quick Answer

- Foreigners (non-PR, non-SC) may purchase private residential property — condominiums, apartments, strata-titled units — in Singapore without restriction, subject to a 60% Additional Buyer’s Stamp Duty (ABSD) payable to IRAS.

- Foreigners cannot buy HDB flats (resale or BTO) and cannot buy landed residential property (houses, semi-detached, bungalows) without prior approval from the Singapore Land Authority (SLA), which is rarely granted.

- Executive Condominiums (ECs) become available to foreigners only after privatisation. For ECs from GLS sites tendered from 8 May 2026 onwards, privatisation occurs at 15 years from TOP; earlier ECs remain at 10 years.

- The 60% ABSD applies to the entire purchase price and must be paid within 14 days of exercising the Option to Purchase (OTP).

- Buyer’s Stamp Duty (BSD) is payable by all buyers regardless of nationality. On a S$2.5M purchase, BSD is approximately S$94,600.

- Foreigners can obtain a mortgage from Singapore-licensed banks. LTV limit is 75% for a first property loan with no existing housing loans, subject to Total Debt Servicing Ratio (TDSR) of 55%.

- Commercial and industrial property carries no ABSD — foreigners may purchase shophouses, office units, factories, and warehouses without the 60% surcharge.

- Nationals of the USA, Iceland, Liechtenstein, Norway, and Switzerland are exempt from ABSD on their first residential purchase under Free Trade Agreement commitments.

What Is the ABSD and Who Administers It?

The Additional Buyer’s Stamp Duty (ABSD) is a surcharge levied by the Inland Revenue Authority of Singapore (IRAS) on the purchase or acquisition of residential property in Singapore, on top of the standard Buyer’s Stamp Duty (BSD). Introduced in December 2011 as a demand-side cooling measure, the ABSD has been adjusted multiple times. The most significant recent change for foreigners was on 27 April 2023, when the rate was doubled from 30% to 60%.

The policy objective is explicit: ABSD prioritises home ownership for Singaporeans and ensures that property remains affordable for residents. Non-resident buyers must bear a substantial additional cost — and this is intentional. Singapore’s Ministry of National Development has consistently maintained that residential property is primarily for citizens, and the 60% rate is designed to reflect that priority firmly.

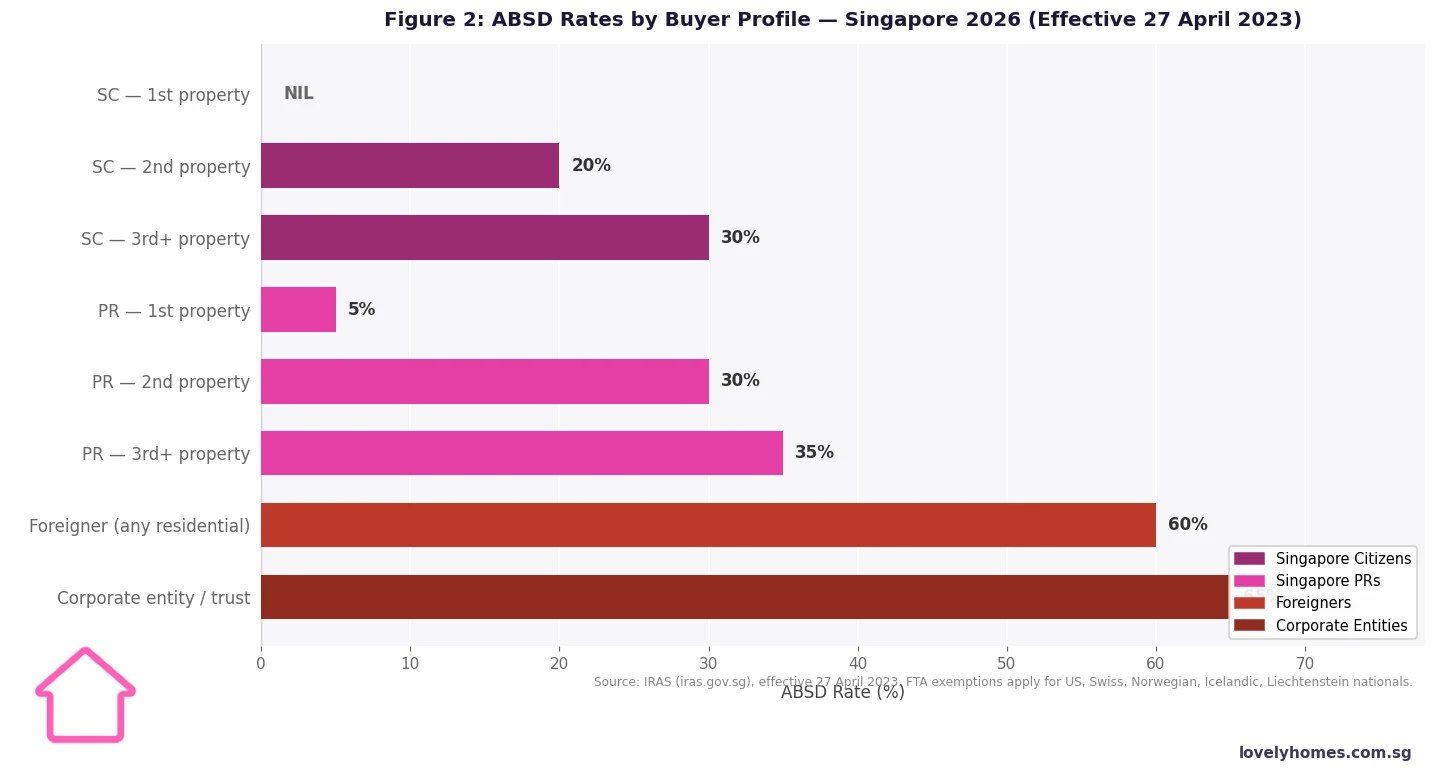

ABSD Rates by Buyer Profile (Effective 27 April 2023)

ABSD is charged on the higher of the purchase price or the property’s market value. The table below shows the current rates, administered by IRAS, for residential property in Singapore:

| Buyer Profile | 1st Property | 2nd Property | 3rd+ Property |

|---|---|---|---|

| Singapore Citizen | 0% | 20% | 30% |

| Singapore Permanent Resident (PR) | 5% | 30% | 35% |

| Foreigner (non-PR, non-SC) | 60% — flat rate, regardless of how many properties held in Singapore | ||

| Corporate entity / trust | 65% — flat rate on residential property | ||

Source: IRAS, effective 27 April 2023. FTA exemptions apply for nationals of the USA, Switzerland, Iceland, Liechtenstein, and Norway.

Free Trade Agreement (FTA) Exemptions

Under Singapore’s FTA commitments, nationals of the USA, Iceland, Liechtenstein, Norway, and Switzerland are treated on par with Singapore Citizens for ABSD on their first residential property purchase. This means a US national buying their first Singapore condo pays 0% ABSD. On second and subsequent purchases, the SC schedule applies. The exemption is for individuals only; US-incorporated companies do not benefit. IRAS requires passport proof of nationality when claiming the FTA exemption.

What Foreigners Can Buy — and Cannot Buy

Permitted (60% ABSD where residential): Private condominiums, private apartments, strata-titled units, SOHO units with residential classification. ECs after privatisation (15 years from TOP for new GLS-launched ECs from 8 May 2026; 10 years for earlier ECs). Sentosa Cove landed property. Commercial shophouses, strata office units, retail units, industrial factories, warehouses — all without residential ABSD.

Not permitted without special approval: Landed residential property outside Sentosa Cove (houses, semi-detached, bungalows, terraced houses). The SLA may grant approval under the Residential Property Act in exceptional circumstances, but approvals are rare.

Strictly prohibited: HDB flats (both new BTO and resale). HDB housing is reserved for Singapore citizens and permanent residents under the Housing and Development Act. ECs during their MOP and privatisation period are also off-limits to foreigners.

Buyer’s Stamp Duty (BSD) — Payable by Everyone

BSD is levied by IRAS on every property purchase in Singapore, regardless of nationality. For residential property, the tiered rates are: 1% on the first S$180,000; 2% on the next S$180,000; 3% on the next S$640,000; 4% on the next S$500,000; 5% on the next S$1,500,000; and 6% on amounts above S$3,000,000. On a S$2.5M purchase, total BSD = S$94,600.

| Purchase Price Tier | BSD Rate | BSD on This Tier |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 (up to S$360,000) | 2% | S$3,600 |

| Next S$640,000 (up to S$1,000,000) | 3% | S$19,200 |

| Next S$500,000 (up to S$1,500,000) | 4% | S$20,000 |

| Next S$1,500,000 (up to S$3,000,000) | 5% | Up to S$75,000 |

| Remainder above S$3,000,000 | 6% | Variable |

Sellers’ Stamp Duty (SSD) — The Anti-Flip Tax

SSD is administered by IRAS and applies to all sellers who dispose of residential property within three years of purchase, regardless of nationality. The rates are: 12% within 1 year; 8% within 2 years; 4% within 3 years; nil thereafter. For a foreigner who has paid 60% ABSD, an SSD liability on a short-term resale would be a severe additional burden. Foreign buyers must plan for a meaningful long-term holding horizon.

| Holding Period | SSD Rate |

|---|---|

| Up to 1 year | 12% |

| 1 to 2 years | 8% |

| 2 to 3 years | 4% |

| More than 3 years | Nil |

Financing — LTV, TDSR, and Mortgage Options

Foreigners may borrow from Singapore-licensed banks subject to MAS macro-prudential rules identical to those applied to residents. The LTV limit is 75% for a first property loan with no existing housing loans (reducing to 55% for a second and 35% for a third). The TDSR cap is 55% of gross monthly income. Loan tenors run up to 35 years, typically reduced by age exceeding 65. Most major Singapore banks lend to foreigners — DBS, OCBC, UOB, Standard Chartered, and HSBC all do so, subject to enhanced documentation requirements including overseas income proof and a valid work pass or Long-Term Visit Pass.

The Buying Process — Step by Step

- Arrange in-principle approval: Approach at least two Singapore banks before making offers. Allow 5–10 working days.

- Engage a CEA-licensed agent: For new launches, no buyer commission is payable; for resale, co-broking arrangements vary.

- Option to Purchase (OTP): On resale, the seller grants an OTP valid for 21 days; a 1% option fee is paid. For new launches, a 5% booking fee is paid directly to the developer.

- Pay BSD and ABSD: Both due within 14 days of OTP exercise. On a S$2.5M purchase, this means wiring S$94,600 (BSD) + S$1,500,000 (ABSD) to IRAS — a total of S$1,594,600 within a fortnight of signing.

- Engage a conveyancing solicitor: A Singapore-qualified solicitor handles title searches, mortgage documentation, and lodgement with SLA’s eConveyancing portal.

- Completion: For resale, typically 8–12 weeks. For new launches, completion occurs at TOP/CSC, which may be 3–5 years away.

Worked Example: Mr David Harrington Buys a S$2.5M CCR Condo

Mr David Harrington, 42, is a British national on an Employment Pass earning S$25,000/month gross. He purchases a two-bedroom unit in District 9 at S$2,500,000, with no existing property loans in Singapore.

| Cost Item | Amount (SGD) | Notes |

|---|---|---|

| 25% downpayment (cash) | 625,000 | 75% LTV → loan of S$1,875,000 |

| Buyer’s Stamp Duty (BSD) | 94,600 | IRAS; payable within 14 days of OTP |

| ABSD (60% x S$2,500,000) | 1,500,000 | IRAS; payable within 14 days of OTP |

| Stamp duty on mortgage (0.4% x loan) | 7,500 | On S$1,875,000 loan amount |

| Legal / conveyancing fees (est.) | 3,500 | Singapore-licensed solicitor |

| Valuation fee (est.) | 600 | Required by lender |

| Total upfront cash required | 2,231,200 | Excluding ongoing mortgage payments |

Monthly mortgage at 3.30% p.a. over 20 years on S$1,875,000 ≈ S$10,633/month. TDSR check: S$10,633 ÷ 55% = S$19,333 minimum monthly gross income required. Mr Harrington’s S$25,000/month comfortably qualifies. However, stamp duties alone represent 63.8% of the purchase price — the property must appreciate significantly for the investment to make financial sense on a net basis.

What This Means for Foreign Buyers

Despite the 60% ABSD headline rate, Singapore continues to attract foreign buyers for structurally sound reasons. Singapore offers secure freehold and 99-year leasehold titles with one of the most transparent property title systems in Asia. There is no capital gains tax, no inheritance tax, and no wealth tax. The SGD has historically been stable and appreciating against most major currencies, and Singapore’s rule of law is consistently ranked among the best globally.

For high-net-worth buyers from jurisdictions with currency risk, political instability, or restricted capital mobility — particularly from certain parts of Southeast Asia, China, and the Middle East — paying 60% ABSD is the premium for a stable, internationally recognised store of value. For US nationals, who pay 0% ABSD on their first purchase thanks to the FTA, Singapore offers one of the most favourable entry points into any developed-market property system globally.

What Might Come Next

The 60% ABSD rate for foreigners is unlikely to be reduced in the near term. Singapore’s government has consistently adjusted rates upward when demand has been firm, and the April 2023 doubling was a clear statement of direction. The EC policy changes of 8 May 2026 — extending MOP to 10 years and privatisation to 15 years, abolishing the Deferred Payment Scheme — further indicate a tightening trajectory. Foreign buyers should plan their acquisitions assuming the 60% rate will persist for the foreseeable future and structure their financial planning accordingly.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty (BSD) Singapore 2026: Rates, Calculation and Exemptions

- Stamp Duty Remissions Singapore 2026: ABSD Married Couple Refund Explained

- Private Condo Buying Process Singapore 2026: Step-by-Step Guide

- Singapore EC Cooling Measures May 2026: 10-Year MOP and End of DPS

- Home Loan Comparison Singapore 2026: Fixed vs Floating and TDSR Explained

- Singapore Property Market Outlook H2 2026: What to Watch

Frequently Asked Questions

Can a foreigner on an Employment Pass buy a condo in Singapore?

Yes. Holding an Employment Pass does not confer Singapore PR status, so the buyer is classified as a foreigner for ABSD purposes — meaning 60% ABSD applies. There is no minimum residency duration requirement to purchase private residential property. The buyer must satisfy the bank’s TDSR requirements using their Singapore employment income (fully counted) and any overseas income (subject to a bank haircut, typically around 30% on variable income).

Are there properties foreigners can buy without the 60% ABSD?

Yes. Commercial and industrial properties do not attract the residential ABSD. Strata office units, retail units, commercial shophouses, industrial factories, and warehouses can all be purchased by foreigners without the 60% surcharge. Many foreign investors therefore channel their Singapore property exposure through commercial assets or Singapore REITs listed on SGX, which provide property-linked returns without the ABSD burden.

Can a foreigner married to a Singapore Citizen pay lower ABSD?

Not directly on a joint purchase. If the property is purchased in the Singapore Citizen spouse’s name alone (sole ownership) and it is the SC’s first property, no ABSD is payable. However, if both names appear on the title, the foreigner’s inclusion triggers 60% ABSD. Many cross-nationality couples place the first property in the SC’s sole name. On subsequent purchases in joint names, ABSD at the SC second-property rate of 20% applies. Seek independent legal and tax advice before structuring ownership this way, as there are CPF, mortgage liability, and estate planning implications.

When exactly must the ABSD be paid?

ABSD must be paid within 14 days of the date on which the liability arises — typically the date of exercising the OTP or the date of the Sale and Purchase Agreement, whichever is earlier. Late payment attracts a 5% per annum penalty interest plus potential IRAS prosecution under the Stamp Duties Act. There is no grace period. The full ABSD amount must be available on or before the deadline, not merely committed in a loan facility.

Is ABSD refundable if the purchase falls through after the OTP is exercised?

Generally, no. Once the ABSD liability arises, it is payable regardless of whether the transaction completes. IRAS may consider a remission application in exceptional circumstances if a transaction is aborted, but this is not guaranteed. The ABSD Married Couple Remission — which allows one SC/PR spouse to sell their existing property within six months of a joint purchase and claim a refund — does not apply to foreigners. Always consult a licensed conveyancing solicitor before exercising any OTP if there is uncertainty about financing, as the ABSD liability is triggered on signing.

Can a foreigner buy a shophouse and occupy the upper residential floor?

This depends on the shophouse’s URA zoning and approved use. If the upper floors are classified as residential under the Residential Property Act, a foreigner cannot purchase without SLA approval (rarely granted). Some shophouses are zoned entirely commercial or approved for mixed use with the upper floors treated as non-residential. The correct approach is to check the URA Master Plan zoning and the specific approved use with a conveyancing solicitor before making any offer, as the legal classification is significant and not always obvious from the building’s physical appearance.

Does a foreigner pay ABSD on a privatised Executive Condominium?

Yes. Once an EC is privatised, it is treated as private residential property and all standard ABSD rules apply — including the 60% rate for foreigners. For ECs launched under GLS tenders from 8 May 2026, privatisation occurs at 15 years from TOP; earlier ECs privatise at 10 years from TOP. Buyers purchasing privatised ECs in the secondary market should verify the specific EC’s TOP date and calculate the privatisation milestone accordingly before making an offer.

Disclaimer: This article is for general information only and does not constitute legal, tax, or financial advice. Stamp duty rates, eligibility rules, and financing guidelines are subject to change by IRAS, MAS, HDB, SLA, and URA. Always verify current rates at iras.gov.sg and consult a licensed Singapore conveyancing solicitor, a CEA-registered real estate professional, and a licensed mortgage adviser before committing to any property transaction. All figures are illustrative based on publicly available data as at 16 May 2026.

0 Comments