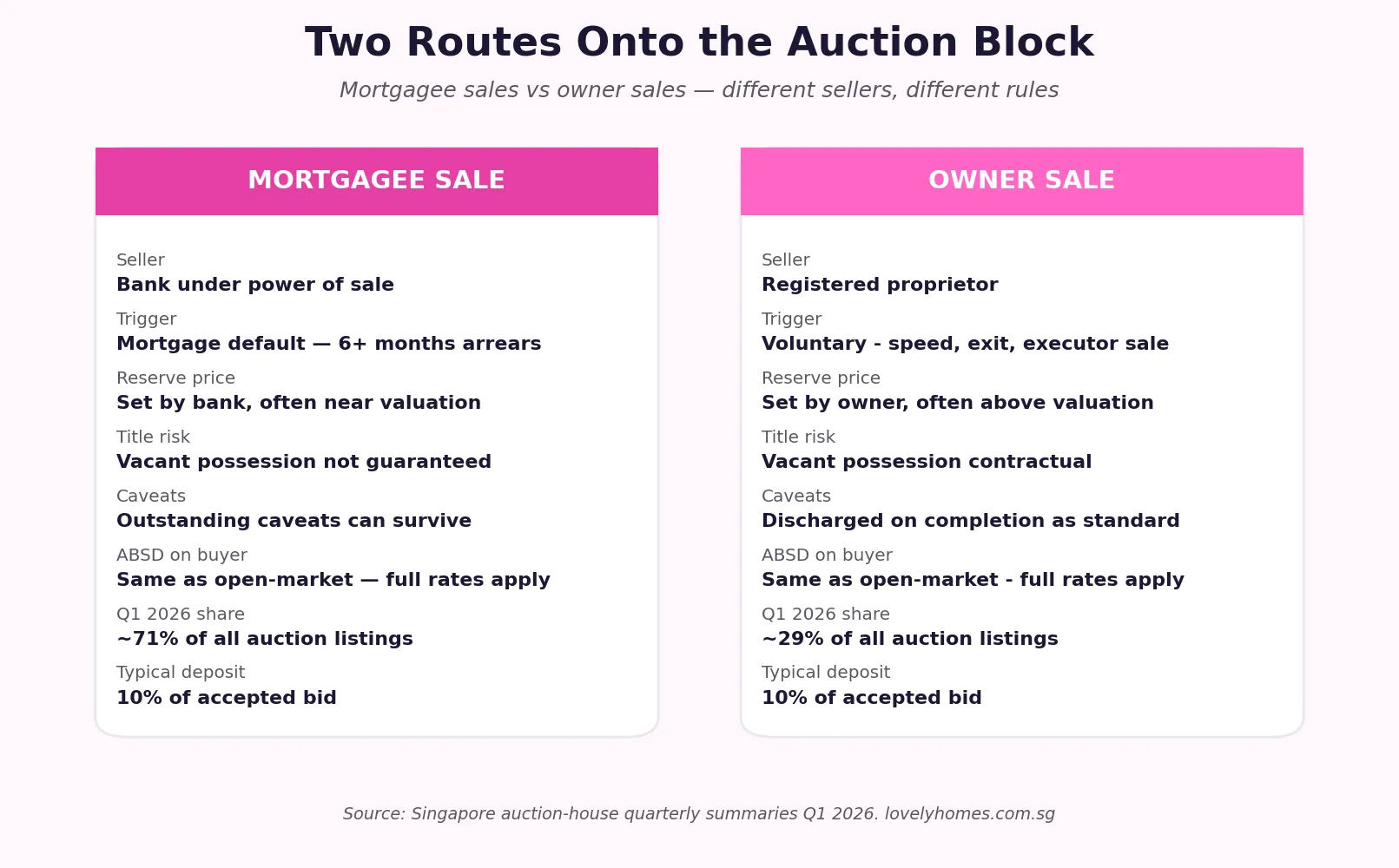

A property auction is the open public sale of a Singapore property under conditions printed in advance — a fixed reserve price, a published Conditions of Sale, a 10% deposit on the fall of the hammer, and a binding contract that crystallises the moment the highest bid is accepted. Most auction listings in Singapore are mortgagee sales — the seller is a bank exercising its power of sale after a defaulted mortgage, not the original homeowner. Mortgagee-sale auction listings jumped roughly 28.8% quarter-on-quarter in the first quarter of 2026, the sharpest single-quarter rise in five years, and industry research expects the climb to extend through the rest of the year. This guide walks through how the auction route actually works in Singapore in 2026, where the legal traps lie, what the 10% deposit really binds you to, and a worked S$1.95 million bid-and-completion example.

Quick Answer

- Two routes: mortgagee sale (bank as vendor under its power of sale) and owner sale (registered proprietor selling voluntarily). Mortgagee sales were ~71% of Q1 2026 listings.

- The hammer creates a binding contract the moment it falls. There is no cooling-off period, no Option to Purchase, no 14-day reflection window.

- Buyer pays a 10% deposit on the fall of the hammer — cashier’s order, payable to the vendor’s solicitor — and the auction memorandum is signed within the same hour.

- Buyer’s Stamp Duty (BSD), Additional Buyer’s Stamp Duty (ABSD) and any Lender’s Duty on Acquiring Units (LDAU) fall due to IRAS within 14 days of the contract — exactly as for a private-treaty sale.

- Standard completion: balance 90% in 12–14 weeks; failure to complete forfeits the 10% deposit and exposes the buyer to a damages claim if the property is re-auctioned at a lower price.

- Mortgagee sales are sold on an “as-is, where-is” basis. Vacant possession is not guaranteed in many mortgagee deals — squatters, holdover tenants, and pending caveats can survive completion.

- ABSD applies in full at the buyer’s profile rate. Citizens 60% on second property; PRs and entities tagged at higher rates. The auction route confers no stamp-duty discount.

Why Auctions Are Suddenly Busier in 2026

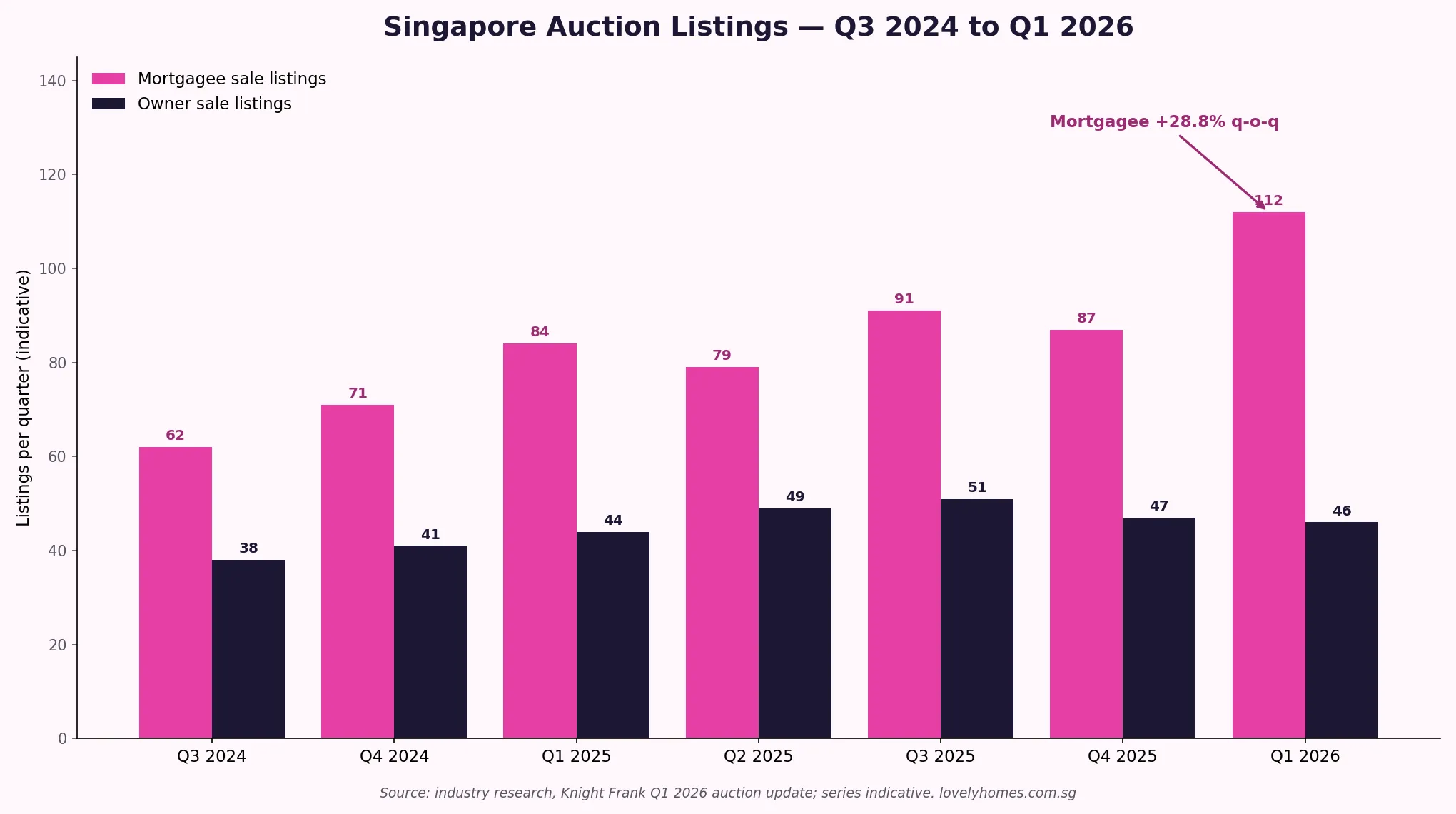

Auction activity is countercyclical. Through the strong 2021–2022 price run, mortgagee sales were rare — refinancing was easy, valuations had risen comfortably above purchase prices, and distressed sellers preferred the open market. Through 2024 and 2025, however, two forces pushed listings higher. The first was the lagged effect of the 2022–2024 rate rise: borrowers on three-year fixed packages from 2022 rolled onto materially higher floating rates in 2025, and households at the margin began missing instalments from the second half of 2024. The second was the 2024 wave of small commercial and shophouse defaults, particularly in F&B-heavy enclaves, which fed niche commercial lots into the auction calendar.

By the first quarter of 2026, mortgagee-sale auction listings had jumped roughly 28.8% quarter-on-quarter — Knight Frank’s Q1 auction-market update flagged the figure and noted that the climb is expected to continue through 2026 even as benchmark rates ease. The composition is also shifting: prime-district condominium units in Districts 9, 10 and 11 made up a larger share of Q1 2026 mortgagee listings than in any quarter of 2025, reflecting strain among investor-borrowers who funded second-home purchases on tight cash flow.

Mortgagee Sale: How the Bank Actually Sells

The legal foundation of a mortgagee sale in Singapore is the power of sale conferred on the lender under the mortgage instrument and the Conveyancing and Law of Property Act 1886. Banks invoke that power only after a documented default — typically six months or more of unpaid instalments — and after issuing a formal demand letter and a Letter of Demand under section 75 of the Act. The borrower is given a final window, usually 30 days, to remedy the default. If the arrears are not cleared, the bank instructs an auctioneer, agrees a reserve price benchmarked to the lender’s panel valuation, and lists the property at the next scheduled public auction.

The bank’s duty is narrow but real. It must obtain the “true market value” of the property — meaning the reserve cannot be set artificially low simply to clear the loan. If the property is sold materially below value and the borrower can prove a breach of that duty, the borrower retains a residual claim against the bank. In practice Singapore reserve prices on mortgagee sales are set within 5–10% of the lender’s valuer’s market estimate.

The mortgagee sale extinguishes the bank’s mortgage on completion. The buyer takes title free of that charge — but not necessarily free of other caveats, such as a second-mortgage caveat held by another financial institution, a maintenance charge from a management corporation, or a CPF charge against the borrower’s withdrawal. Ascertaining the full encumbrance position is the responsibility of the buyer’s solicitor before the auction; once the hammer falls there is no scope to renegotiate.

Owner Sale: Auctions as a Speed Tool

The second route is the owner sale — a voluntary auction by the registered proprietor. Owners use the auction route for three reasons. First, speed: an auction marketed for two weeks delivers a binding contract in a single afternoon, against the multi-week dance of options, exercise and conveyancing in a private-treaty sale. Second, price discovery: when the property is unusual (a freehold conservation shophouse, an estate-administered Good Class Bungalow, a subdivided strata mix) and there is no obvious comparable, an auction extracts the highest bidder rather than the highest opening offer. Third, process discipline: estate executors, divorce-mandated sales and corporate liquidations face fiduciary duties to obtain market value, and a public-auction record is the cleanest defensible audit trail.

Owner sales are typically sharper on title quality. The owner remains in possession until completion and contracts to deliver vacant possession on legal completion — that is the usual position for a private-treaty sale and it carries through to the owner’s auction. Caveats are routinely discharged on completion using the sale proceeds. The buyer faces fewer “legacy” risks than on a mortgagee lot.

The Auction-Day Mechanic

Singapore auctions follow a near-uniform script. The auctioneer reads the lot description, calls a starting price (usually 5–10% below the reserve), and accepts ascending bids in fixed increments — typically S$10,000 for residential lots under S$2 million, S$50,000 above that. Bids in the room are visible; absentee written bids are submitted to the auctioneer on a sealed form before the lot is called. Online and telephone bidding are now standard at every major Singapore auction house since 2021. The reserve is undisclosed but the lot is withdrawn if no bid clears it.

When the highest bid clears the reserve and three calls fail to produce a higher bid, the hammer falls. The successful bidder produces a 10% cashier’s order on the spot — issued in advance to the auctioneer’s instruction — and signs the auction memorandum. That memorandum, attaching the printed Conditions of Sale, becomes the executed Sale and Purchase Agreement. From that moment the buyer is locked in: no cooling-off, no inspection contingency, no financing contingency.

The 10% Deposit and Forfeiture

The 10% deposit is more than earnest money — it is liquidated damages. If the buyer fails to complete on the contractual completion date (typically 12–14 weeks after the hammer), the vendor is entitled to forfeit the deposit absolutely under the Conditions of Sale. There is no notion of partial forfeiture; the entire 10% is lost. If the property is later re-auctioned at a price below the original bid, the defaulting buyer is liable for the shortfall as further damages — including the costs of the re-auction.

This is the single highest-risk feature of the auction route. A buyer who cannot complete because financing fell through (the bank’s loan amount was lower than expected once a fresh valuation came in below the bid), or because vacant possession proved harder than expected, has no escape. The 10% deposit on a S$2 million lot is S$200,000 of cash. That cash is gone.

Stamp Duties on the Auction Buyer

Auction purchases attract the same stamp-duty regime as private-treaty purchases — there is no auction-route discount. Buyer’s Stamp Duty applies on a sliding scale up to 6% on the slab above S$3 million for residential property. Additional Buyer’s Stamp Duty applies at the buyer’s profile rate: 0% for a Singapore Citizen first home, 20% on a Citizen second home, 30% on a third or subsequent home; 5% for a Permanent Resident first home, 30% on second; 60% for foreigners; 65% for entities; with a 35% LDAU surcharge for housing-developer entities. Stamp duty falls due to IRAS within 14 days of the contract date, which for an auction is the date the hammer falls.

Buyers planning an auction bid should compute the all-in cost — bid price plus BSD plus ABSD plus typical S$2,500 of legal cost plus 10% deposit financing — before raising the paddle. A foreigner bidding S$2 million on a residential lot pays S$1.2 million in ABSD on top, taking the all-in cost beyond S$3.25 million.

Q1 2026 Listings — Where Volume Came From

The Q1 2026 climb in mortgagee-sale listings was concentrated in three property classes. Strata-titled commercial units — small office and retail lots in mixed-use buildings — accounted for the largest single increment, reflecting accumulated rental softness from the 2024 supply wave. Prime-district condominiums in Districts 9, 10 and 11 made the second-largest contribution, particularly two-bedroom and three-bedroom investment units bought between 2018 and 2021 with high LTV. Suburban executive condominiums and freehold landed terraces in Districts 13, 15 and 19 made up the third stream, mostly owner-occupier defaults rather than investor-driven listings. Owner-sale listings were broadly flat across the same period — the rise in auction volume was overwhelmingly distress-driven, not voluntary.

Worked Example: A Foreigner Bid on a S$1.95 Million Mortgagee Lot

Mr Ravi, a Permanent Resident on his second residential property in Singapore, attends a major April 2026 auction. The lot is a 1,184 sq ft three-bedroom freehold condominium unit in District 15, listed under mortgagee sale by a major retail bank. The reserve, undisclosed, has been set at S$1,950,000 (~S$1,647 psf). The starting bid is S$1.85 million; the room runs the bid up in S$10,000 increments to S$1,960,000, where Mr Ravi’s S$1.97 million bid sees off a final telephone bidder. The hammer falls.

On the spot. Mr Ravi produces a S$197,000 cashier’s order — 10% of the bid — payable to the auction firm. He signs the auction memorandum and the printed Conditions of Sale. The contract is binding.

Within 14 days. Mr Ravi’s solicitor lodges and pays:

- Buyer’s Stamp Duty: ~S$70,000 (sliding scale to S$1.97M)

- ABSD at PR-second-home rate: 30% × S$1.97M = S$591,000

- Total stamp duties to IRAS: S$661,000

Weeks 1–4. Solicitor runs full title search at SLA, verifies discharge of the bank’s first mortgage on completion, and probes for any second-charge caveat or maintenance lien. Two outstanding maintenance arrears of S$11,400 are flagged from the management corporation; under the Conditions of Sale these survive completion and the buyer settles them as a post-completion debt to the MC.

Weeks 4–10. Mr Ravi finalises a refinance loan from a different bank at 1.65% fixed for 2 years, 75% LTV on his bid price. He receives the Letter of Offer at week 8. Critically, the new bank’s valuer puts indicative market value at S$1,920,000 — S$50,000 below the bid. The bank lends 75% of the lower of bid price and valuation, so the loan amount is S$1.44 million, not the S$1.4775 million Mr Ravi modelled. He has to top up S$37,500 in cash from the LTV gap, on top of the 25% he already had ready.

Week 14 — completion. Balance 90% (S$1.773 million) paid; legal completion at SLA. Mr Ravi takes vacant possession (the unit was already vacant — the previous borrower had moved out at default). All-in cost: bid S$1.97M + BSD S$70k + ABSD S$591k + legals S$3.5k + maintenance arrears top-up S$11.4k + cash gap S$37.5k = ~S$2.683 million. The “discount to market” once stamp duties are layered in is closer to 1% than the headline 5–10% reserve discount the auction was marketed at.

The Five Traps Newcomers Miss

| Trap | What goes wrong |

|---|---|

| Vacant possession not guaranteed | Mortgagee sales are “as-is, where-is”. Holdover tenants, family members in occupation, or squatters can survive completion; the buyer must apply for a writ of possession at extra cost and time. |

| Loan in principle is not loan certainty | A pre-auction LIP is not binding. The lender’s actual loan amount is determined post-bid, on a fresh valuation. If valuation comes in below bid, the LTV gap is the buyer’s cash problem, not the bank’s. |

| CPF release is slower than expected | CPF Board needs an executed S&P plus the new mortgage instrument before disbursing OA funds. On a 12-week auction completion, the CPF release usually arrives just-in-time; missed paperwork can push the buyer into late-completion penalties. |

| Outstanding caveats survive | A second-mortgage or judgment-debt caveat that isn’t the bank’s own first charge can ride through completion and become the buyer’s title problem to solve post-hand-over. |

| “Below valuation” can be illusion | The bank’s panel valuation is not the same as a buyer-side valuation. A reserve set at the bank’s number can sit above what an independent valuer signs off — and that is the number that drives loan size. |

Why This Matters

For most Singapore homeowners the auction route is simply not the right purchase channel — the binding-contract speed, the no-financing-contingency rule and the deposit forfeiture risk are unforgiving. For experienced investors with cash buffers, however, the auction calendar through 2026 is likely to widen the opportunity set: more mortgagee listings, in better postcodes, with reserves anchored to the lender’s valuation rather than seller aspiration. Anyone planning to bid should treat the auction not as a discount channel but as a different procurement mechanism with its own legal architecture and its own failure modes.

What Might Come Next

Three signals will tell you where the 2026 auction year is heading. First, watch the quarterly mortgagee-listings count reported by the major Singapore auction houses — Q2 2026 figures, due in July, will confirm whether Q1’s 28.8% rise is the start of a multi-quarter trend or a one-off catch-up. Second, track average winning-bid spread to reserve: a tight spread (winning bid 0–3% above reserve) signals weak buyer pool; a wider spread (5–10%) signals contested bidding and stronger market psychology. Third, monitor commercial vs residential mix: a continued tilt toward strata commercial and shophouse lots would suggest that 2026 distress is corporate and small-business, not household, and that residential auction risk stays bounded.

Frequently Asked Questions

Can I attend a Singapore property auction without bidding?

Yes. Public auctions are open to attend; you can register as a non-bidder simply to observe. Most major Singapore auctions are also live-streamed online, and recordings of past auctions are sometimes posted by the auction house. Attending two or three auctions before raising your own paddle is the cheapest education there is on how the room actually behaves under bidding pressure.

Can I bid online or by phone?

Yes. Every major Singapore auction house since 2021 supports online bidding, telephone bidding, and absentee bid forms. Pre-registration is required, including identity verification and proof of funds. The auctioneer reads remote bids into the room as they come in; a remote bidder who wins still has to deliver a 10% cashier’s order to the auctioneer within hours of the hammer.

Is there any cooling-off period after the hammer falls?

No. Auctions are expressly excluded from the Sale of Commercial Properties Act / Housing Developers Act cooling-off framework. The contract created by the auction memorandum is binding from the moment of execution. There is no 14-day Holding Period, no 3-day reflection window. This is the single most important difference between auction and private-treaty purchase.

Do I pay ABSD if I buy at auction?

Yes. The auction route confers no stamp-duty discount whatsoever. BSD applies on the sliding scale to the bid price, and ABSD applies at the buyer’s profile rate — 0%/20%/30% for Citizens by property count, 5%/30% for PRs, 60% for foreigners, 65% for entities. Both fall due to IRAS within 14 days of the auction date.

What happens if my financing falls through after I win the bid?

The 10% deposit is forfeited. If the property is re-auctioned at a lower price, the defaulting buyer is also liable for the shortfall plus the costs of the re-auction. There is no financing contingency in the auction Conditions of Sale. Bidders should secure a Letter of Offer or at minimum an in-principle approval before bidding, and should bid at a level the LIP supports — not a level that depends on a higher post-bid valuation.

Are there auctions for HDB flats?

HDB resale flats are not sold at public auction in Singapore. HDB resale transactions must go through HDB’s own resale portal and require the seller to be the registered owner. Mortgagee-sale auctions therefore concern only private property — condominiums, apartments, executive condominiums (post-privatisation), landed homes, strata commercial and shophouse lots. Where an HDB flat enters a forced-sale scenario, HDB itself supervises the sale through its resale process rather than via a third-party auction house.

Do reserve prices change during an auction calendar?

Frequently. If a lot fails to sell at the published reserve in one auction round, the auctioneer will discuss a revised reserve with the vendor before the next round. Mortgagee sales typically see reserve cuts of 2–5% per failed round, capped by the bank’s duty to obtain market value. Owner-sale reserves are more elastic — the owner may withdraw the lot entirely if bidding is weak. Tracking a lot through two or three rounds is a routine technique among experienced auction investors.

Related Articles

- ABSD Singapore Complete Guide 2026

- Buyer’s Stamp Duty Singapore 2026

- Conveyancing Process Singapore 2026

- Refinancing Home Loan Singapore 2026

- Foreigner Property Buyer Singapore 2026

- Property Inheritance Singapore 2026

Disclaimer

This article is editorial commentary for general information only and does not constitute legal, financial, or stamp-duty advice. Auction Conditions of Sale, reserve prices and bidding procedures vary by auction house and by lot; always read the printed Conditions of Sale issued for the specific lot before bidding. Consult IRAS at iras.gov.sg for the prevailing BSD, ABSD and LDAU rates and the 14-day stamping deadline; consult SLA at sla.gov.sg for INLIS title-search and caveat information; consult MAS at mas.gov.sg for the prevailing TDSR cap and stress-rate; and engage a qualified solicitor familiar with auction conveyancing before raising a paddle.

0 Comments