Who can rent: Singapore citizens, permanent residents, and most foreigners holding valid work or long-term passes may rent a private condo unit. There is no separate approval required from HDB or URA for non-landed private property rentals.

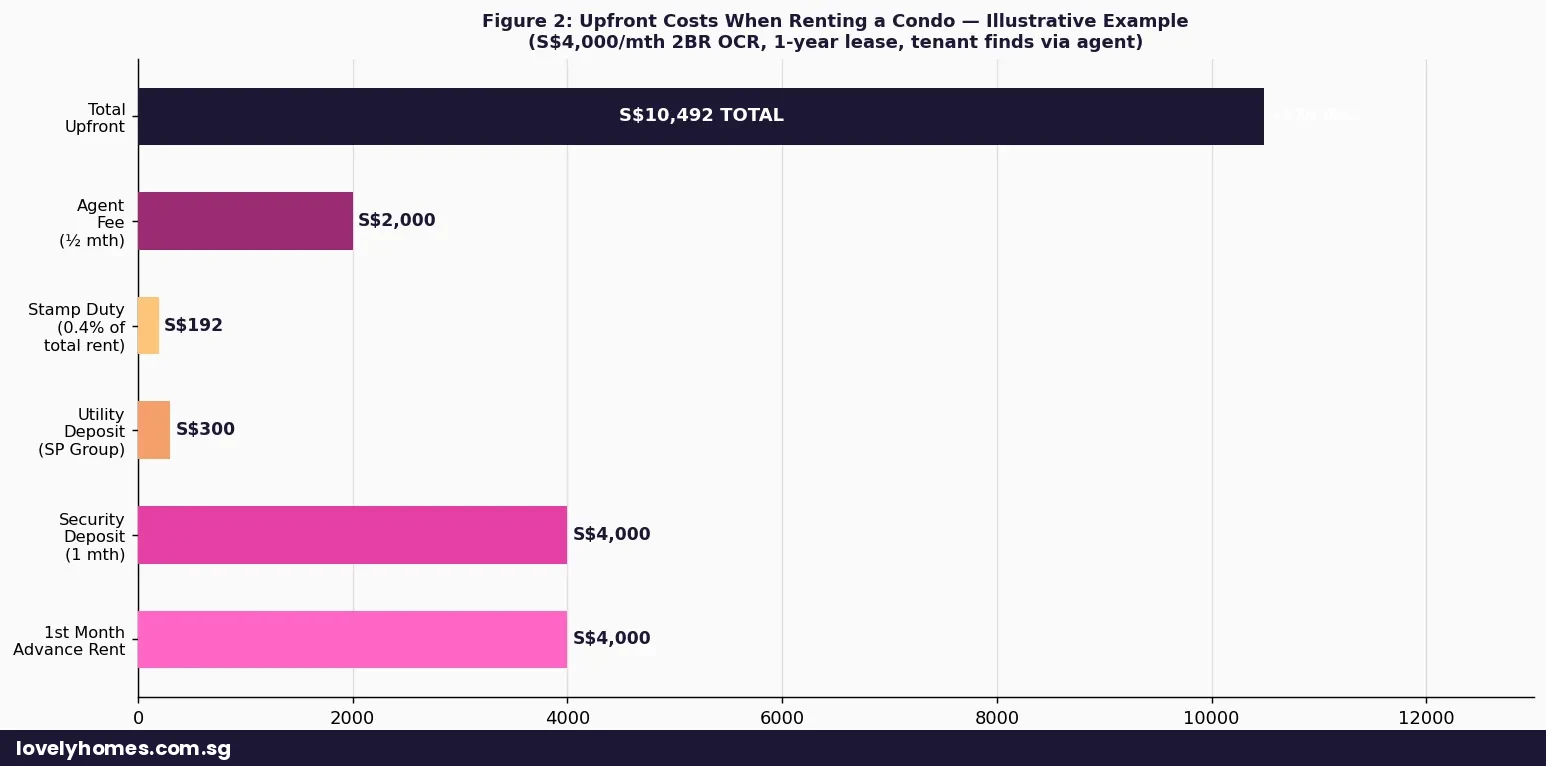

Typical upfront costs on a 1-year lease include the first month’s advance rent, a security deposit (typically one month’s rent for a 1-year lease), and stamp duty on the Tenancy Agreement.

Stamp duty on the lease is borne by the tenant and is approximately 0.4% of the total contract rent. A S$4,000/mth 1-year lease incurs approximately S$192 in stamp duty.

The Tenancy Agreement (TA) must be stamped with IRAS within 14 days of the date it was signed.

Lease durations are typically 1 or 2 years. 3-year leases exist but are less common for condos.

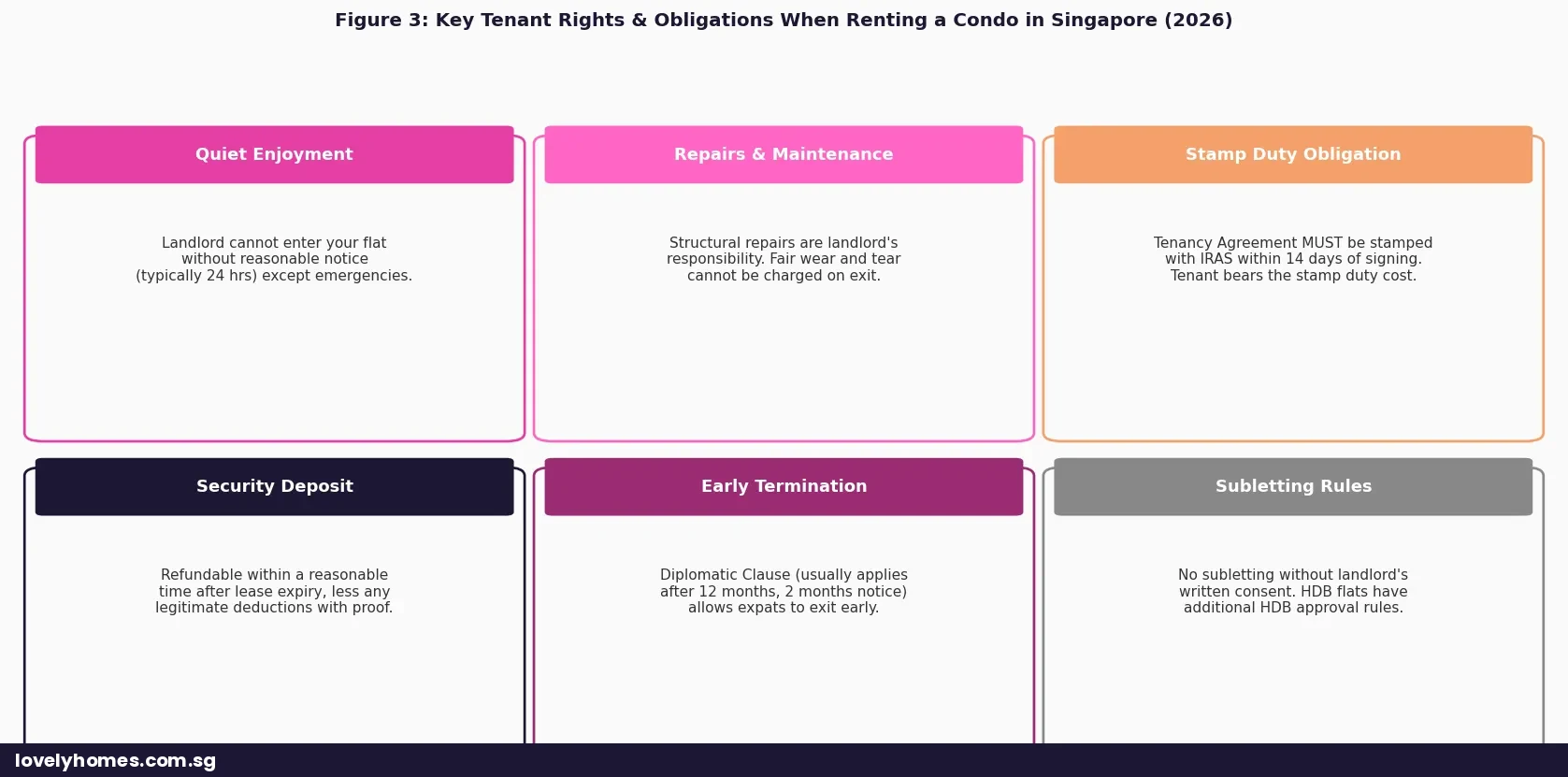

Diplomatic Clause: most landlords grant this for 2-year leases, allowing early termination (usually after 12 months) with 2 months’ notice — important for foreign tenants.

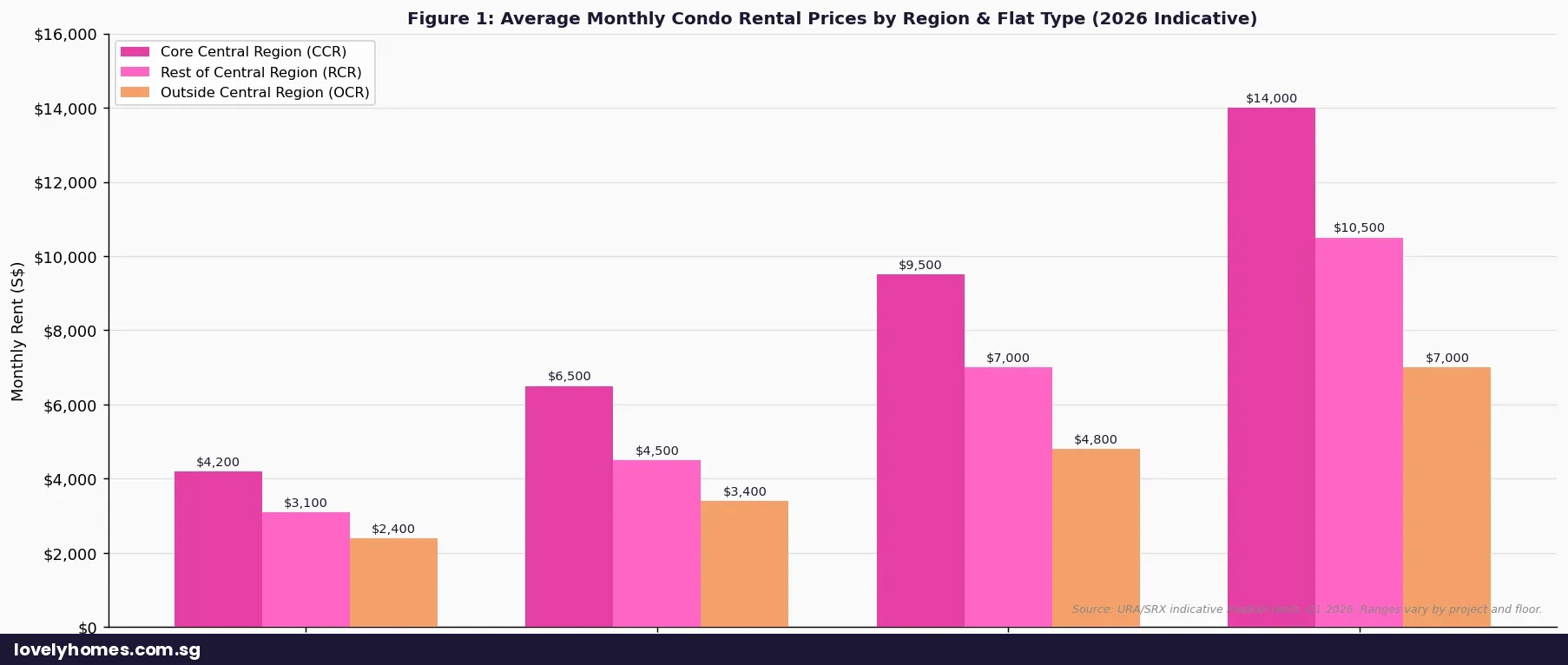

Rental prices in 2026 range from approximately S$2,400/mth for a studio in the Outside Central Region (OCR) to over S$14,000/mth for a 4-bedroom unit in the Core Central Region (CCR).

Property tax and maintenance fees are the landlord’s responsibility — not the tenant’s, unless otherwise agreed in the TA.

Singapore’s Condominium Rental Market in 2026

Singapore’s condo rental market is one of the most active in Asia. With a permanent resident and expatriate population generating sustained demand, and a growing professional class of Singaporeans choosing to rent rather than buy, private condominium rentals remain a key pillar of the residential property market. According to URA rental data, over 70,000 non-landed private residential rental transactions are registered annually in Singapore, the majority being condominiums.

Rental prices rose sharply between 2021 and 2023 as pandemic-era supply disruptions and surging demand from returning expatriates pushed rents to record highs. Since late 2023 and into 2024–2026, the market has moderated as a substantial pipeline of new completions — including major integrated developments and Build-To-Rent projects — has added supply. As at Q1 2026, URA’s condo rental index shows rents broadly stable, with pockets of softness in the OCR and selective strength in CCR luxury units.

Who Can Rent a Condo in Singapore?

Any person with a legal right to reside in Singapore may rent a private condominium unit. This includes Singapore citizens, permanent residents, Employment Pass holders, S Pass holders, Dependent Pass holders, and Long-Term Visit Pass holders. There is no application to HDB or the Urban Redevelopment Authority (URA) required for non-landed private property rentals — the agreement is directly between landlord and tenant, governed by general contract law and the Residential Tenancies Act framework.

However, landlords are obligated under the Residential Property Act and Immigration Act rules to verify that all tenants hold valid passes allowing them to reside in Singapore. Tourist visa holders may not enter into a rental agreement. Short-term rentals of less than three months are prohibited under URA’s short-term accommodation rules (which also restrict Airbnb-style platforms for private residential units).

Rental Prices by Region and Flat Type (2026)

Figure 1: Average Monthly Condo Rental Prices by Region and Flat Type — Indicative Q1 2026 (Source: URA/SRX median data)

Singapore’s condo rental prices differ substantially across the three planning regions. The Core Central Region (CCR) — comprising Districts 1–4, 9, 10, 11 and Sentosa Cove — commands premium rents driven by proximity to the Central Business District, prestigious schools, and international amenities. The Rest of Central Region (RCR) offers a middle ground, with maturing townships such as Queenstown, Bishan, and Toa Payoh appealing to both expatriates and local professionals. The Outside Central Region (OCR) spans the suburban heartlands from Jurong to Tampines, Woodlands to Pasir Ris, offering the most accessible rental entry points.

Flat Type

CCR (Monthly S$)

RCR (Monthly S$)

OCR (Monthly S$)

Studio / 1-Bedroom

S$3,500–S$6,000

S$2,800–S$3,800

S$2,200–S$3,000

2-Bedroom

S$5,000–S$9,000

S$3,800–S$5,500

S$3,000–S$4,200

3-Bedroom

S$8,000–S$14,000

S$5,500–S$8,500

S$4,200–S$6,000

4-Bedroom / Penthouse

S$12,000–S$25,000+

S$8,500–S$13,000

S$6,000–S$10,000

Table 1: Indicative monthly condo rental ranges by region and flat type, as at Q1 2026. Actual rents vary by project, floor, furnishing, and lease tenure. Source: URA rental caveats and SRX median data.

The Condo Rental Process: Step-by-Step

Renting a condominium in Singapore follows a relatively standard process. Unlike buying a property, there is no government portal or pre-approval required — the process is market-driven, though stamp duty obligations and pass verification requirements are mandatory.

Define your budget and requirements: determine your affordable monthly rent (typically no more than 30–40% of net take-home income), preferred region, flat type, and preferred MRT or school proximity.

Search and viewings: search listings on property portals or engage a salesperson. Note that landlords and tenants typically each engage their own representative, with fees negotiated case by case — typically one month’s rent for a 1-year lease paid by the tenant, or co-broking arrangements.

Letter of Intent (LOI) / Offer to Lease: once you identify a unit, submit a Letter of Intent with your proposed rental terms, key money (typically one to two weeks’ rent), and requested lease commencement date. The landlord may accept, reject, or counter.

Tenancy Agreement (TA): upon acceptance, the TA is drafted (typically by the landlord’s salesperson). Review it carefully — key clauses include rent amount, lease period, security deposit, Diplomatic Clause, permitted use, and maintenance responsibilities. Seek legal advice for any non-standard terms.

Sign and stamp: both parties sign the TA. The tenant pays the first month’s advance rent and the security deposit upon signing. The TA must be stamped with IRAS within 14 days of the signing date. Stamp duty is payable by the tenant.

Move-in inventory check: conduct a joint inspection with the landlord on or before the lease commencement date. Document all existing defects in writing and by photographs — this protects both parties on the security deposit at the end of the tenancy.

Upfront Costs When Renting a Condo

Figure 2: Upfront Costs When Renting a Condo — Illustrative for a S$4,000/mth 2BR OCR 1-Year Lease (2026)

The security deposit is typically one month’s rent for a 1-year lease or two months’ rent for a 2-year lease. This deposit is held by the landlord (or sometimes in escrow) and refunded within a reasonable time after the tenancy ends, less any justified deductions for rent arrears or damages beyond fair wear and tear.

0.4% of the average annual rent for leases with a fixed term (simplified computation: 0.4% × total rent for leases up to 4 years).

For a 1-year lease at S$4,000/mth: total rent = S$48,000; stamp duty = S$48,000 × 0.4% = S$192.

For a 2-year lease at S$4,500/mth: total rent = S$108,000; stamp duty = S$108,000 × 0.4% = S$432.

Stamp duty is payable by the tenant, though this is occasionally negotiated otherwise in the TA.

Failure to stamp within 14 days incurs a late penalty (initially S$10, then escalating).

The TA must be stamped via the IRAS myStamp portal or at any IRAS service centre. Many salespersons handle this on behalf of their clients, but the legal obligation remains with the tenant unless the TA specifies otherwise.

Key Clauses to Check in Your Tenancy Agreement

The TA is a legally binding contract. Clauses worth scrutinising carefully include:

Diplomatic Clause: allows early termination after a minimum period (usually 12 months for a 2-year lease) with 2 months’ written notice. Essential for foreign tenants whose employment situation may change. Not standard on all leases — negotiate before signing.

Landlord’s access: the landlord should only enter the unit with reasonable advance notice (24 hours is customary) except in emergencies. Any clause allowing entry without notice should be queried or struck out.

Maintenance responsibilities: the TA typically requires the tenant to be responsible for minor maintenance (e.g., replacing light bulbs, unblocking drains) while the landlord covers structural and major appliance repairs. Clarify what constitutes “fair wear and tear”.

Air-conditioner servicing: standard practice is quarterly servicing at the tenant’s cost. This is often stated explicitly in the TA and is a reasonable tenant obligation.

Subletting: subletting the entire unit without the landlord’s written consent is generally prohibited. If you require the right to sublet individual rooms, negotiate this explicitly.

Handover condition: confirm the exact condition in which the unit must be returned (e.g., professionally cleaned, walls repainted).

Figure 3: Key Tenant Rights and Obligations in Singapore Condo Rentals (2026)

Worked Example: James Rents a 2BR OCR Condo

James is a British national on an Employment Pass, earning S$8,500/mth. He wants to rent a 2-bedroom unit in the OCR (Jurong East area) on a 2-year lease.

Agreed rent: S$3,500/mth for a 2BR 840 sqft unit at a leasehold condo 8 minutes’ walk from Jurong East MRT.

Lease period: 1 July 2026 to 30 June 2028 (2 years), with Diplomatic Clause from 1 July 2027 (12 months + 2 months’ notice).

Stamp duty: total rent = 24 × S$3,500 = S$84,000; stamp duty = S$84,000 × 0.4% = S$336 (stamped by salesperson via IRAS within 14 days).

Agent fee (co-broke): S$3,500 × 1 = S$3,500 (1 month’s rent, split between landlord’s and tenant’s representatives on co-broking basis; tenant’s representative absorbed by landlord in this example).

Total upfront outlay for James: S$7,000 (deposit) + S$3,500 (1st month) + S$336 (stamp duty) = S$10,836.

Monthly on-going: S$3,500 rent + quarterly air-con servicing ~S$80 + SP Group utilities (metered) ~S$200/mth estimated = approximately S$3,780/mth all-in.

Rental as % of income: S$3,500 / S$8,500 = 41.2% — on the higher end of affordability benchmarks, but manageable given no CPF obligations for EP holders.

What This Means for You

Renting a condo in Singapore is one of the most transparent and well-regulated rental experiences in Asia. The stamp duty obligation, while modest (0.4%), ensures leases are formally registered. The emphasis on written TAs and inventory checks protects both parties. The Diplomatic Clause — while not legally mandated — is widely accepted practice and critically important for expatriates.

From a cost perspective, 2026 represents a more balanced rental market than the peak of 2022–2023. Tenants have more negotiating power on lease terms, furniture packages, and rent-free periods than they did two years ago. Vacancy rates have risen in several OCR and newer RCR developments as completions accelerate, meaning landlords in these pockets are more willing to negotiate. The CCR luxury segment, however, remains tight — driven by sustained demand from financial sector and tech-sector professionals.

What Might Come Next

Singapore’s rental market in the medium term (2026–2028) faces two countervailing forces. On the supply side, a significant pipeline of private residential completions — approximately 8,000–10,000 units per year through 2027 according to URA’s construction data — should continue to exert moderating pressure on rents, particularly in the OCR and new RCR townships. On the demand side, Singapore’s continued attractiveness as a regional business hub and the government’s restrained foreign manpower policies mean rental demand from pass holders is unlikely to collapse.

Regulatory watch: MAS and URA are studying the residential tenancies framework, including possible standardisation of TA templates and security deposit handling. A formal Residential Tenancies Act — modelled on frameworks in Hong Kong or Australia — has been discussed but not yet enacted as at mid-2026. Any such legislation would likely strengthen tenant protections around deposit refunds and repair obligations, which are currently governed primarily by contract terms rather than statute.

Frequently Asked Questions

Can I negotiate on condo rental price in 2026?

Yes, and more so than in 2022–2023. With a softer rental market across the OCR and parts of the RCR, landlords are more flexible on headline rent, rent-free fit-out periods (1–2 weeks free rent at the start of the lease to allow for minor touch-ups), furniture packages, and minor TA terms. In the CCR luxury segment, negotiating room is narrower but still exists for high-quality tenants with strong employment credentials. Always make any rent concession explicit in the TA — verbal assurances are not enforceable.

What happens to my security deposit if the landlord sells the property during my lease?

Your Tenancy Agreement is binding on successors in title — a new owner takes the property subject to your existing lease. The security deposit should be transferred to the new owner at completion of the sale. However, this transfer is the landlord’s legal obligation, not yours. If the new owner denies holding your deposit, you may have a claim against the original landlord. It is therefore prudent to keep a stamped copy of the TA and your payment receipt for the deposit for the full duration of the tenancy. Some tenants negotiate for the deposit to be held in a separate account.

Can foreigners buy or rent a condo in Singapore?

Foreigners can freely rent any private condominium unit in Singapore, provided they hold a valid pass allowing them to reside here. Purchasing a private condominium (non-landed) is also legally permitted for foreigners, though the Additional Buyer’s Stamp Duty (ABSD) of 65% on the purchase price applies to all foreign buyers as at July 2026. There are no ownership restrictions on non-landed private residential property (condominiums and apartments) for foreigners — restrictions apply only to landed property (which requires SLA approval) and HDB flats (which foreigners cannot purchase). For a full breakdown of ABSD rates, see our ABSD Singapore 2026 Complete Guide.

What is a “break clause” or “diplomatic clause” and who benefits from it?

A Diplomatic Clause (also called a break clause) is a contractual provision in the TA that allows the tenant to terminate the lease early, typically after the first 12 months of a 24-month lease, by giving 2 months’ written notice. On termination under the Diplomatic Clause, the tenant forfeits no deposit and pays only rent up to the notice period. The clause exists to protect foreign tenants who may need to relocate due to job changes or repatriation at short notice. Most Singapore landlords accept the Diplomatic Clause for 2-year leases, particularly when renting to corporate-sponsored expatriate tenants. For 1-year leases, early termination is more complex as there is no standard clause — tenants seeking to break a 1-year lease typically negotiate a settlement with the landlord, often involving partial deposit forfeiture.

Is the tenant required to pay property tax or maintenance fees (MCST fees)?

No. Property tax (payable to IRAS) and MCST maintenance fees (payable to the condo’s Management Corporation Strata Title) are the landlord’s responsibility, not the tenant’s. These costs are factored into the landlord’s rental pricing decision but are not directly charged to or payable by the tenant, unless the TA explicitly (and unusually) states otherwise. You should confirm this in your TA. Conversely, the tenant is typically responsible for all utility costs (electricity, water, gas via SP Group), internet, and parking charges.

What should I do if the landlord refuses to return my security deposit?

If the landlord has deducted all or part of your deposit after the lease ends and you dispute the deductions, the first step is written communication — formally requesting an itemised breakdown of deductions with supporting receipts or quotes. If this fails, Singapore offers several avenues for resolution: the Community Disputes Resolution Tribunal (CDRT) handles disputes between neighbours; for financial claims below S$30,000, the Small Claims Tribunal (SCT) is a fast and inexpensive route to adjudication. Alternatively, Singapore Mediation Centre (SMC) offers pre-litigation mediation. As at 2026, there is no dedicated tenancy dispute tribunal in Singapore (unlike Hong Kong’s Lands Tribunal), which is why clear inventory documentation at move-in and move-out is critical.

This article is published by LovelyHomes Editorial Team for general informational purposes only and does not constitute legal, financial, or property advice. Rental prices cited are indicative market ranges as at Q1 2026 and will vary by project, floor, furnishing level, and individual negotiation. Stamp duty obligations are administered by the Inland Revenue Authority of Singapore (IRAS). Tenancy law is governed by Singapore’s Residential Property Act, the Stamp Duties Act, and general contract law. Readers should refer to official URA, IRAS, and Ministry of Law publications for the most current regulations, and obtain independent legal advice before signing any Tenancy Agreement. Pass validity requirements for foreign tenants are governed by the Immigration and Checkpoints Authority (ICA) and the Ministry of Manpower (MOM).

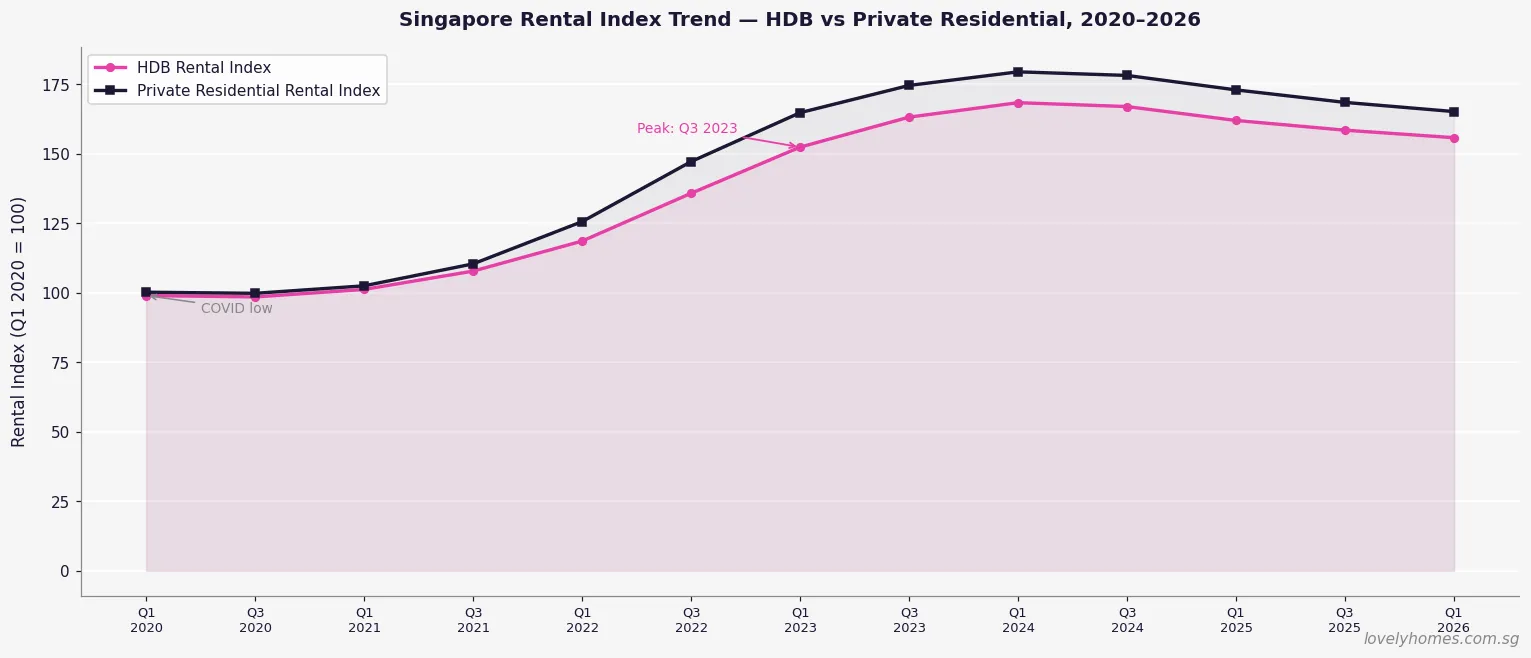

Singapore’s private residential rental index rose 0.3% in Q1 2026 (URA), recovering from a 0.5% dip in Q4 2025, but remains below the 2023 peak.

HDB rental index eased 0.1% in Q1 2026, continuing a gradual softening from the 2023 high after two years of elevated rents.

Median rents in Q1 2026: HDB 4-room S$2,600/mth, condominium 2-bedroom S$3,600/mth (OCR), condominium 3-bedroom S$5,200/mth.

Gross rental yields remain attractive for HDB (4.7–5.6%) compared with private condominiums in Core Central Region (CCR) (2.6%).

Rising supply from 2024–2025 completions is the dominant dampener; landlords must price competitively in 2026.

Demand drivers: foreign professional workforce (Employment Pass/S Pass holders), expat families on education visas, and domestic upgraders waiting for new homes to complete.

Short-term rentals (fewer than 3 months) remain prohibited for residential properties in Singapore under URA regulations.

Landlords must declare rental income on their annual income tax returns to IRAS; allowable deductions include mortgage interest, property tax, and maintenance fees.

Understanding Singapore’s Rental Market

Singapore’s residential rental market is one of Asia’s most closely watched — shaped by a unique interplay of government-controlled HDB supply, private condominium completions, immigration policy, and one of the highest proportions of home ownership in the world (approximately 89%). Unlike many global cities, Singapore’s rental sector is comparatively small: most residents own their HDB flats. The rental pool is disproportionately driven by the expatriate workforce and a domestic segment of upgraders temporarily between properties.

The Urban Redevelopment Authority (URA) tracks the Private Residential Rental Index quarterly; HDB separately tracks the HDB Rental Index. Both indices are released alongside quarterly real estate statistics — the primary authoritative source for rental market data. The Q1 2026 URA statistics confirmed that private rental growth has moderated after the exceptional surge of 2021–2023, when the market rose over 50% from its COVID-era trough on the back of a supply drought and surging foreign workforce arrivals.

Rental Index Trend: 2020–2026

The rental cycle of this decade is one of the most dramatic in Singapore’s property history. From a base of approximately 100 in early 2020, the HDB Rental Index rose to a peak of approximately 163 by mid-2023 before softening. Private residential rents peaked near 175 in mid-2023. As at Q1 2026, both indices have retreated — the HDB index to approximately 156, the private residential index to approximately 165 — representing a correction of roughly 4–6% from peak.

Figure 1: Singapore HDB and Private Residential Rental Index trend, Q1 2020 – Q1 2026 (Q1 2020 = 100). Sources: URA, HDB quarterly real estate statistics.

The correction has been driven primarily by supply normalisation — a wave of private condominium completions in 2024–2025 (including several large integrated developments) added significant rental stock to the market, while post-COVID foreign workforce growth moderated as global companies trimmed headcount in 2024–2025. Nevertheless, rents remain approximately 55% higher in absolute terms than pre-COVID levels for most property types.

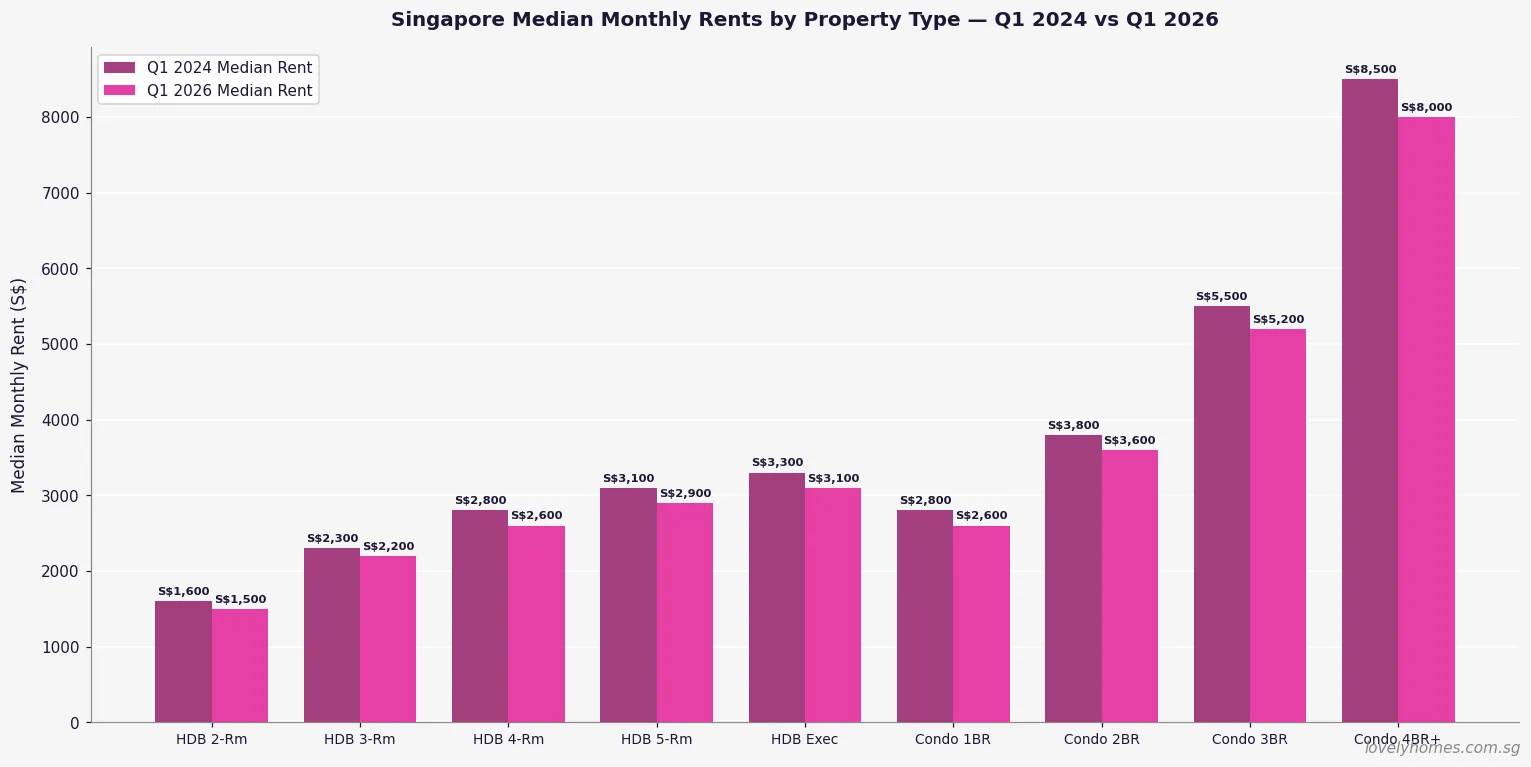

Median Monthly Rents by Property Type, Q1 2026

Industry figures from Q1 2026 show median monthly rents across property types as follows. HDB room types continue to offer the most accessible entry point for tenants, while Core Central Region (CCR) condominiums command a substantial premium reflecting proximity to the CBD and top international schools.

Figure 2: Singapore median monthly rents Q1 2024 vs Q1 2026 by property type. All figures are indicative medians; individual transacted rents vary by location, floor, condition, and furnishing.

Key observations from the Q1 2026 data: HDB 3-room rents have eased from approximately S$2,300/mth in Q1 2024 to approximately S$2,200/mth, a modest 4.3% decline. Private condominium 3-bedroom rents have softened more noticeably from approximately S$5,500/mth to S$5,200/mth (−5.5%). Executive flat rents remain relatively sticky at approximately S$3,100/mth, reflecting persistently high demand from larger families displaced from the HDB resale market by the 15-month wait.

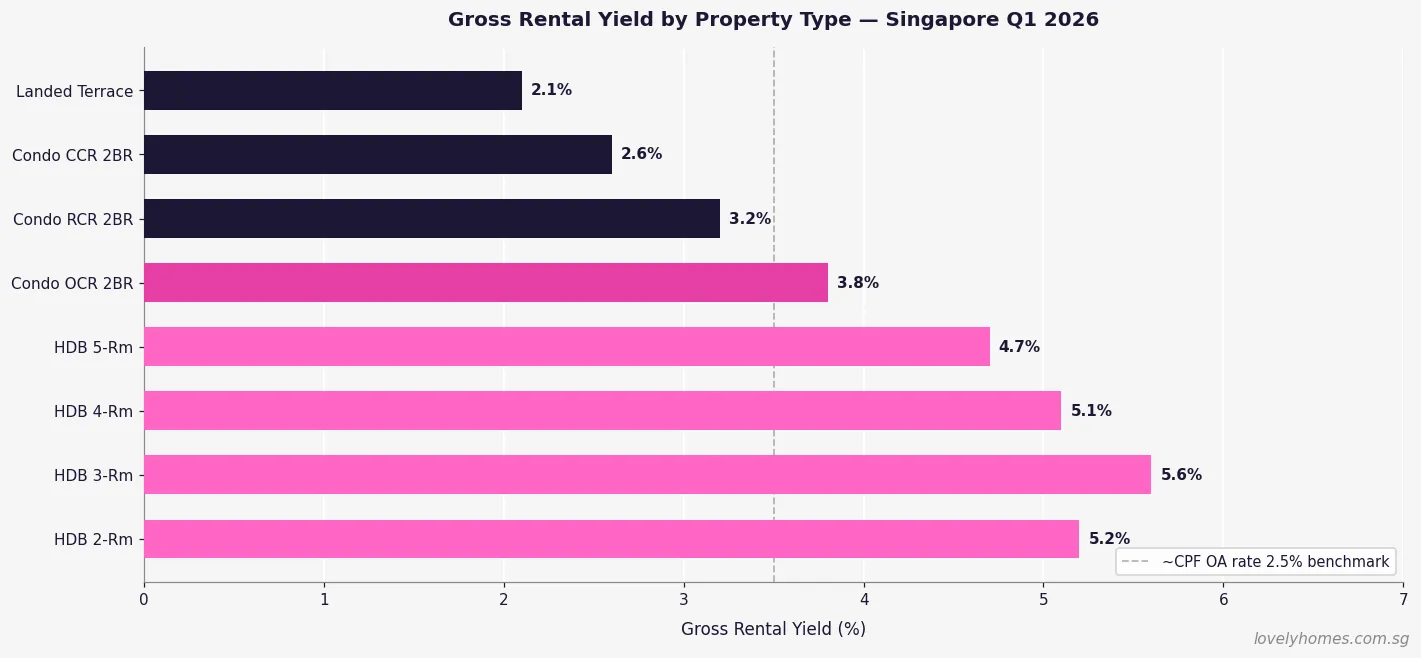

Gross Rental Yields by Property Type

Gross rental yield is calculated as annual rent divided by market value. In Singapore’s context, it is an imperfect but useful comparator — particularly when set against the CPF Ordinary Account rate of 2.5% p.a. and typical bank mortgage rates of 3.0–3.7% p.a. in 2026. Properties yielding below the mortgage rate require careful cash flow modelling; properties yielding above 4.5% can generate positive carry even at current financing costs.

Figure 3: Gross rental yield by property type, Singapore Q1 2026. Yields are gross — deduct mortgage interest, property tax, management fees, vacancy, and maintenance for net yield calculations.

HDB flats deliver the highest gross yields precisely because their prices are regulated and their transacted values remain significantly below equivalent private condominiums. A well-located 3-room HDB in Toa Payoh with a transacted rent of S$2,200/mth and a resale value of approximately S$470,000 generates a gross yield of approximately 5.6% — among the highest in Singapore’s residential market. However, HDB landlords face non-citizen quota constraints (8% or 11% per block/neighbourhood) and must comply with the Minimum Occupation Period (MOP) rules and HDB approval requirements. See our comprehensive HDB Rental Guide 2026 for full details.

Landlord Obligations and Legal Framework

Residential tenancies in Singapore are governed primarily by contract law — there is no Residential Tenancies Act equivalent to those in the United Kingdom or Australia. The standard Tenancy Agreement is a contractual document prepared by either party’s lawyer or the property agent. Key regulatory requirements for landlords include:

Stamp duty on tenancy agreements: The tenant is liable to pay stamp duty on the tenancy agreement via IRAS e-Stamping. The rate is 0.4% of the total rent for leases of 1–4 years; for leases exceeding 4 years, the rate is 4% of the average annual rent. In practice, landlords should confirm the stamp duty is paid within 14 days of signing, as IRAS treats it as a condition for the agreement to be legally admissible in court.

Short-term rental prohibition: URA regulations prohibit the use of private residential properties for accommodation for periods of fewer than 3 consecutive months. Platforms such as Airbnb, Agoda (short-stay listings), and similar are prohibited for residential properties. Violations carry fines of up to S$200,000 per offence.

HDB subletting rules: HDB flat owners who have completed their Minimum Occupation Period (MOP) may sublet their whole flat or individual bedrooms, subject to HDB approval, non-citizen quota compliance, and the maximum occupancy limits (8 persons per flat until 31 December 2026 under the current temporary relaxation).

Property tax: Landlords pay property tax at non-owner-occupier rates (typically 10–20% of the Annual Value for private properties, 10% for HDB), which is a deductible expense against rental income.

Rental income tax: Rental income is taxable as personal income in Singapore. Allowable deductions include mortgage interest, property tax, fire insurance premiums, maintenance fees, and depreciation of approved furniture at 20% per annum declining balance.

Summary: Singapore Rental Market at a Glance, 2026

Property Type

Typical Monthly Rent

Gross Yield

Key Tenant Profile

HDB 2-room

S$1,400–S$1,600

~5.2%

Singles, young couples

HDB 3-room

S$2,000–S$2,400

~5.6%

Small families, couples

HDB 4-room

S$2,400–S$2,800

~5.1%

Families, expat workers

HDB 5-room

S$2,600–S$3,200

~4.7%

Families, management expats

Condo 1-bedroom (OCR)

S$2,400–S$2,800

~3.8%

Young professionals

Condo 2-bedroom (OCR)

S$3,200–S$4,000

~3.8%

Couples, small families

Condo 2-bedroom (CCR)

S$4,500–S$6,500

~2.6%

Senior expat executives

Landed Terrace

S$6,000–S$10,000

~2.1%

High-net-worth families

Worked Example: Mr Rajan Buys a 3-Room HDB to Rent Out in Ang Mo Kio

Mr Rajan, a Singapore Citizen, purchased a 3-room HDB resale flat in Ang Mo Kio in August 2021 for S$450,000. His MOP completed in August 2026 and he immediately lists it for whole-flat rental while upgrading to a condominium. Key figures:

Purchase price: S$450,000 in August 2021.

MOP completion: August 2026 (5 years from key collection).

Estimated market rent (Q1 2026): S$2,100–S$2,300/mth for a well-maintained 3-room in Ang Mo Kio.

Monthly gross income: S$2,200/mth (midpoint).

Annual gross rent: S$26,400.

Gross yield: S$26,400 / S$450,000 = 5.9% (calculated on original purchase price; current AV-based valuation ~S$480,000 gives ~5.5%).

Property tax (non-owner-occupier): Annual Value approximately S$24,000; property tax approximately S$2,400/yr at 10%.

Mortgage interest (if outstanding loan S$150,000 at 2.6%): ~S$3,900/yr (deductible).

Net rental income (estimated): S$26,400 − S$2,400 (property tax) − S$3,900 (interest) − S$1,200 (maintenance, insurance) = approximately S$18,900/yr, taxable at Mr Rajan’s personal income rate.

Stamp duty on 12-month tenancy at S$2,200/mth: 0.4% × S$26,400 = S$105.60 (tenant’s liability but landlords confirm this is paid).

The non-citizen quota check (8% neighbourhood / 11% block) must be confirmed with HDB before signing the Tenancy Agreement. HDB approval is required for whole-flat rental; approval is typically granted within 3–5 business days via the HDB Resale Portal.

What Might Come Next for Singapore Rents

The 2026 rental market is characterised by a bifurcation: HDB rents are gradually softening as more MOP flats come onto the rental market and demand moderates, while premium private rents in the CCR are proving stickier, supported by a resilient pool of senior expatriate tenants who cannot or will not rent HDB. The key upside risk to the softening thesis is a reversal in Singapore’s technology and financial services hiring cycle — any rebound in Employment Pass issuances (which fell in 2024–2025 under tighter Fair Consideration Framework scrutiny) would tighten rental supply rapidly given the low vacancy rates in well-located projects. The key downside risk is continued elevated completions through 2026–2027 from the record launch years of 2021–2022, which will maintain supply pressure on mid-market condominiums.

For investors evaluating rental yield against price appreciation potential, the OCR condominium segment offers the most balanced risk-reward in 2026: gross yields of approximately 3.5–4.0% are competitive with bank deposit rates after factoring in leverage, while capital value upside from Jurong Lake District and Cross Island Line catalysts provides a medium-term appreciation thesis. See our Singapore Property Investment Guide 2026 for a full cross-asset comparison.

Frequently Asked Questions

Are Singapore rents going up or down in 2026?

Singapore’s rental market is in a gradual softening phase in 2026. According to URA Q1 2026 data, the private residential rental index rose 0.3% quarter-on-quarter — a marginal recovery after a 0.5% dip in Q4 2025 — but remains below the 2023 peak. HDB rents eased 0.1% in Q1 2026. The dominant factors are increased supply from 2024–2025 completions and moderating foreign workforce demand. Most market observers expect rents to remain broadly flat to slightly lower through 2026, with premium CCR properties proving more resilient than mass-market OCR condominiums and HDB flats.

Can I Airbnb my Singapore condo or HDB flat?

No. URA regulations prohibit the use of private residential properties for short-term accommodation of fewer than 3 consecutive months. This applies equally to condominiums, landed properties, and HDB flats. Listing a Singapore residential property on Airbnb, Agoda short-stay, or similar platforms is a regulatory offence carrying fines of up to S$200,000 per offence. HDB additionally prohibits subletting to short-term visitors regardless of platform. The minimum tenancy period for all residential properties in Singapore is 3 months.

Do I need to declare rental income to IRAS?

Yes. Rental income is taxable as personal income in Singapore and must be declared on your annual Income Tax return. IRAS requires landlords to report gross rent received, then deduct allowable expenses: mortgage interest (on the loan for the rented property), property tax paid, fire insurance premiums, cost of maintenance and repairs (but not capital improvements), management fees, and furniture depreciation at 20% per annum declining balance on approved items. Failure to declare rental income attracts penalties of up to 200% of the tax undercharged. See IRAS’s guide at iras.gov.sg for the current rental income declaration checklist.

What is the non-citizen quota for HDB rentals?

HDB imposes a Non-Citizen Quota (NCQ) to preserve the social mix of HDB estates. The quota limits the proportion of HDB flats in each block and neighbourhood that may be rented to non-Malaysia foreigners (i.e., all non-citizens who are not Malaysian citizens). The limits are 8% at the neighbourhood level and 11% at the block level. If either quota has been met, the landlord cannot rent to a non-Malaysian foreigner regardless of HDB approval status. Malaysia citizens are exempt from the NCQ. Singapore PRs count as citizens for NCQ purposes. Always check the NCQ status on the HDB website before signing any Tenancy Agreement with a foreign tenant.

What is a diplomatic clause in a tenancy agreement?

A diplomatic clause (or Diplomatic Break Clause) is a contractual provision that allows the tenant to terminate the tenancy early if they are relocated or transferred out of Singapore by their employer — typically with 2 months’ written notice after the first year of the lease. It is commonly requested by expatriate tenants and their employers. Landlords generally accept diplomatic clauses for premium properties where the tenant pool is predominantly expatriate. The clause should specify the minimum tenancy period before it can be activated (typically 12 months), the notice period, and whether any penalty or notice fee applies. If the tenant exercises the clause, they forgo the security deposit for the unused period — the exact mechanism is a matter of negotiation.

How is stamp duty on a tenancy agreement calculated?

Stamp duty on a Tenancy Agreement is calculated under the Stamp Duties Act (Cap. 312). For a lease of 1–4 years, the duty is 0.4% of the total rent payable over the tenancy period. For a lease exceeding 4 years, the duty is 4% of the average annual rent. Example: a 12-month lease at S$3,500/mth = total rent S$42,000; stamp duty = 0.4% × S$42,000 = S$168. Payment is due within 14 days of signing via the IRAS e-Stamping portal. The stamp duty is the tenant’s liability by default, but the Tenancy Agreement may specify otherwise. An unstamped tenancy agreement is inadmissible as evidence in court, though the tenancy itself remains contractually enforceable as between the parties.

What is a typical security deposit for a Singapore rental?

The market convention in Singapore is one month’s rent as security deposit for every year of tenancy — so a 1-year lease typically requires a 1-month deposit, and a 2-year lease requires a 2-month deposit. For leases with a diplomatic clause, landlords sometimes negotiate a 2-month deposit for a 1-year lease as additional security against early termination. There is no statutory cap on the security deposit amount in Singapore — it is entirely a matter of negotiation. The deposit should be held in a separate client account by the agent or returned directly to the landlord, and must be refunded within 14 days after the end of the tenancy (less any deductions for damage or unpaid rent, supported by receipts and a condition report).

Disclaimer: This article is intended for general informational purposes only and does not constitute legal, tax, or financial advice. Rental figures, yields, and index data cited are based on information available as at 7 June 2026 and are subject to change. Individual rental outcomes depend on property location, condition, furnishing level, and prevailing market conditions. Readers should consult a licensed Singapore real estate agent (CEA-registered), a Monetary Authority of Singapore (MAS) licensed financial adviser, and IRAS for personalised rental income tax guidance. Authoritative references: URA (ura.gov.sg), HDB (hdb.gov.sg), IRAS (iras.gov.sg), CEA (cea.gov.sg).

Singapore’s residential rental market entered 2026 after two years of adjustment. The extraordinary rental surge of 2022–2023 — when median rents rose by 30–40% driven by returning expatriates, supply disruptions, and a flood of en-bloc proceeds — has given way to a more measured environment. Vacancy rates across private residential properties averaged 7.6% at end-2025 (URA), reflecting a significant influx of completed units from the 2021–2023 pipeline.

Yet demand remains structurally healthy. Singapore’s open-economy model, its position as a regional headquarters hub, and a steady pipeline of work-permit and employment-pass holders keep rental absorption strong in the OCR and mature HDB heartland districts. For first-time landlords considering a buy-to-let strategy, and for tenants navigating a complex regulatory framework, understanding the rules administered by the Housing & Development Board (HDB), the Urban Redevelopment Authority (URA), and the Inland Revenue Authority of Singapore (IRAS) is essential.

HDB Flat Subletting Rules: What Every Landlord and Tenant Must Know

HDB flats are subsidised public housing built for owner-occupation, not investment. Subletting an entire HDB flat — or even individual rooms — is subject to a strict ruleset administered by the HDB under the Housing and Development Act.

Minimum Occupation Period (MOP)

Before a flat owner may sublet the entire flat, the property must have completed its 5-year Minimum Occupation Period (MOP) from the date of key collection. For flats purchased under the Prime Location Public Housing (PLH) or Plus classification introduced under HDB’s new classification system (effective BTO exercises from October 2023), the MOP is 10 years.

Room Rental (Subletting a bedroom)

Room-only subletting — where the owner continues to reside in the flat — is permitted before MOP, subject to occupancy cap rules. From 22 January 2026, the HDB and URA implemented a temporary relaxation of the occupancy cap to allow up to 8 unrelated persons in a flat or private residential property (up from the standard 6), applicable until 22 January 2028.

Key HDB subletting rules at a glance

Minimum tenancy term: 6 consecutive months per subletting period

Maximum subletting term: 3 years per application (renewable)

HDB subletting application must be made online at hdb.gov.sg before the subletting commences

Subtenants must be Singapore Citizens, Permanent Residents, or foreigners with a valid long-term pass (Employment Pass, S Pass, Dependent Pass, Long-Term Visit Pass)

Non-citizen (NR) subletting quota: no more than 8% of the HDB block may be sublet to non-Malaysian foreigners

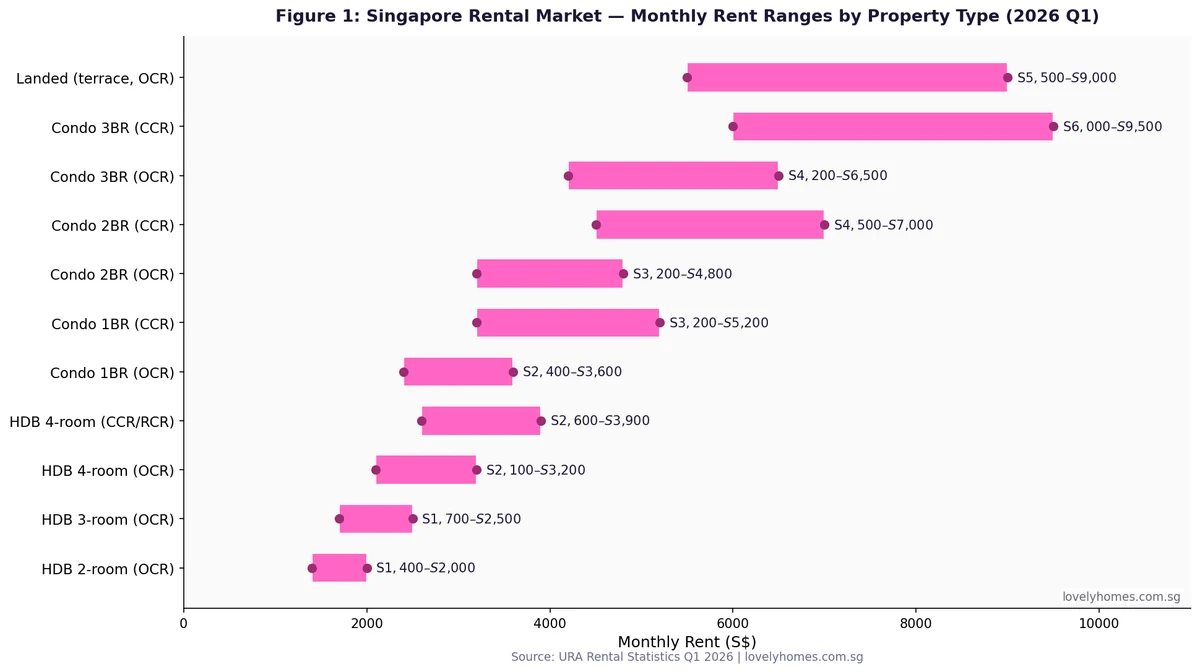

Figure 1: Singapore rental market — monthly rent ranges by property type and location, Q1 2026. Source: URA Rental Statistics.

Private Condo and Landed Property Rental Rules

Private residential properties — condominiums, apartments, and landed houses — are not subject to MOP restrictions. An investor who purchases a newly-launched private condo may sublet the entire unit immediately upon receiving the Temporary Occupation Permit (TOP), subject to two key rules administered by URA:

Minimum tenancy term: 3 consecutive months for private residential properties (compared to 6 months for HDB)

Occupancy cap: The standard cap is 6 unrelated persons per dwelling unit; the temporary relaxation to 8 persons applies through January 2028

Short-term rental prohibition: Platforms such as Airbnb and similar short-stay apps are prohibited for private residential properties in Singapore. Rental terms below 3 months are illegal and carry fines of up to S$5,000

Landed properties — terraced houses, semi-detached, and bungalows — follow private property rules (3-month minimum, no MOP). Foreign ownership of landed property is restricted under the Residential Property Act 1976, but foreigners may rent any landed home freely.

Rental Rates in 2026: What to Budget as a Tenant

Singapore’s rental market is priced according to property type, location (CCR/RCR/OCR), floor level, condition, and proximity to MRT stations. The data below reflects URA and HDB Rental Statistics for Q1 2026. All figures are monthly rents in Singapore dollars.

Property Type

Location

Typical Monthly Rent

Indicative PSF

HDB 2-room

OCR

S$1,400–S$2,000

S$3.0–S$4.2

HDB 3-room

OCR

S$1,700–S$2,500

S$2.8–S$3.8

HDB 4-room

OCR (mature)

S$2,100–S$3,200

S$2.6–S$3.5

HDB 4-room

CCR/RCR (Bishan, Toa Payoh)

S$2,600–S$3,900

S$3.2–S$4.2

Condo 1BR

OCR

S$2,400–S$3,600

S$4.2–S$5.5

Condo 1BR

CCR

S$3,200–S$5,200

S$5.5–S$8.0

Condo 2BR

OCR

S$3,200–S$4,800

S$3.8–S$5.2

Condo 2BR

CCR

S$4,500–S$7,000

S$5.8–S$8.5

Condo 3BR

OCR

S$4,200–S$6,500

S$3.5–S$5.0

Landed terrace

OCR

S$5,500–S$9,000

S$2.8–S$4.5

Stamp Duty on Tenancy Agreements

In Singapore, the tenant bears the cost of stamping the Tenancy Agreement (TA) via IRAS e-Stamp within 14 days of signing. The stamp duty rate is:

For leases of 4 years or less: S$4 for every S$250 (or part thereof) of the total rent payable over the term

For leases exceeding 4 years (or indefinite term): calculated on the higher of total rent or 4× annual rent, at the same rate

Example: A 2-year tenancy at S$3,500/month = S$84,000 total rent. Stamp duty = S$84,000 ÷ S$250 × S$4 = S$1,344. This must be paid via the IRAS e-Stamping portal at iras.gov.sg.

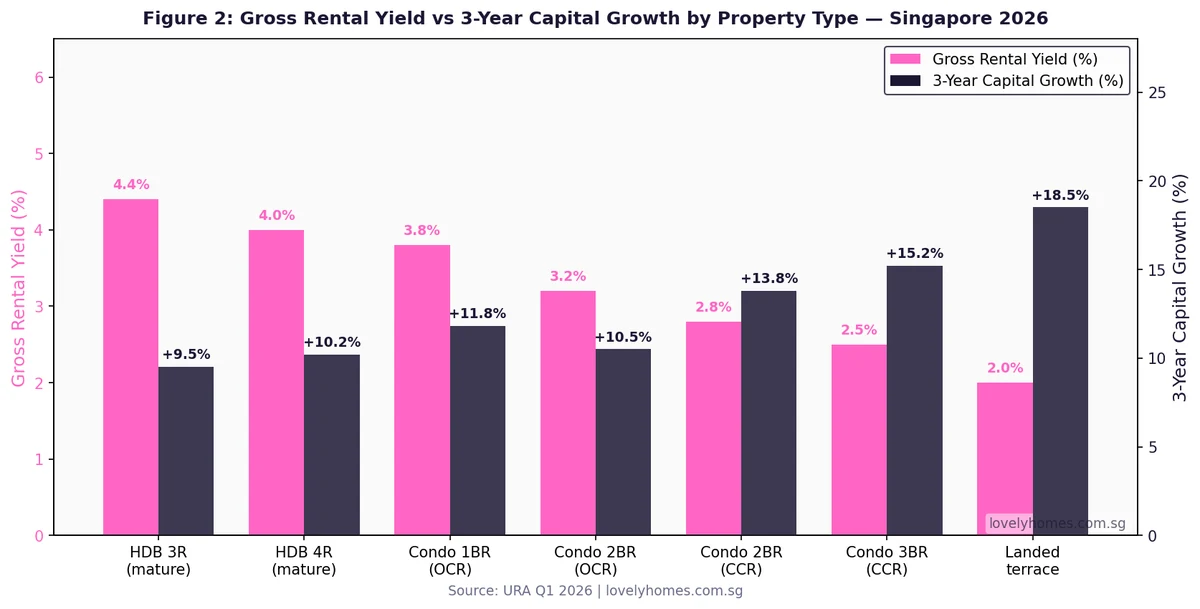

Rental Yield and Investment Performance

For property investors, gross rental yield is calculated as annual rent divided by purchase price. Singapore’s rental yields have compressed over the past decade as capital values outpaced rent growth, yet certain property types and locations still offer respectable returns — particularly HDB-adjacent OCR condos near MRT nodes and mature-town HDB resale flats after MOP.

Figure 2: Gross rental yield vs 3-year capital growth by property type — Singapore Q1 2026. Source: URA / lovelyhomes.com.sg research.

HDB resale flats offer the highest gross rental yields (4.0–4.4%) among mainstream property types, owing to relatively affordable purchase prices and sustained heartlander demand. Private condo yields are lower (2.5–3.8%), but the CCR segment benefits from stronger long-term capital growth — up to +15.2% over three years for CCR 3-bedroom units — driven by the irreplaceable land scarcity in Districts 9–11. Landed property yields are modest (2.0%) but capital growth is exceptional (+18.5%), reflecting the structural restriction on new landed supply in Singapore.

PSF Benchmarks and Vacancy Rates Across the Market

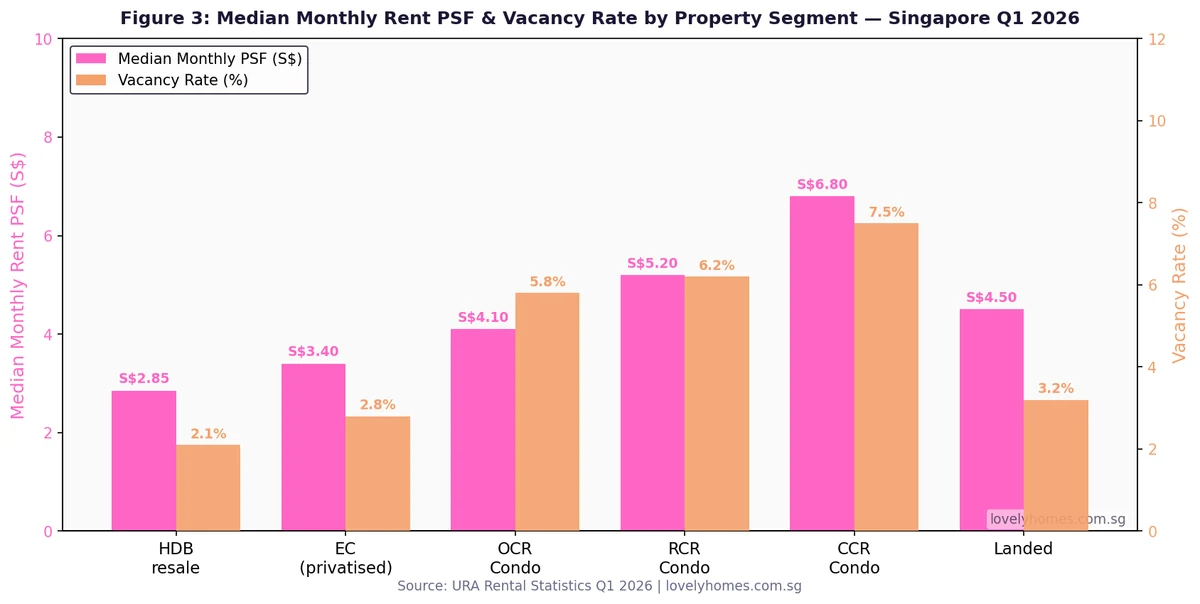

Analysing median monthly rent on a per-square-foot (PSF) basis allows meaningful comparison across property types of different sizes. URA’s Q1 2026 Rental Statistics show that CCR condos command the highest PSF (~S$6.80/sqft/month) but also carry the highest vacancy rates (~7.5%), reflecting the elevated supply completions in the prime districts. OCR condos are priced more keenly (~S$4.10 PSF) with lower vacancy (~5.8%).

Figure 3: Median monthly rent PSF and vacancy rate by property segment — Singapore Q1 2026. Source: URA Rental Statistics.

Rental Income Tax for Landlords

Rental income is taxable in Singapore under the Income Tax Act. Landlords must declare gross rental receipts in their annual tax returns (Year of Assessment for the preceding calendar year). Allowable deductions reduce the taxable rental income:

Mortgage interest (for the period the property was rented out; capital repayments are not deductible)

Property tax paid on the rented property

Fire insurance premiums

Maintenance and repair costs (not capital improvements)

Agent commission (for securing the tenancy)

For individual landlords, the net rental income is added to total chargeable income and taxed at progressive rates (0–22% for residents in YA 2026). Non-resident landlords face a flat 24% withholding tax on gross rental income unless a lower treaty rate applies. IRAS cross-checks rental declarations against the HDB/URA subletting register, so non-disclosure carries significant risk.

Tenant Rights and Responsibilities in Singapore

Singapore does not have a dedicated Tenants’ Rights Act. Tenancy agreements are governed by general contract law and the Distress Act (Cap 84). However, several protections and obligations apply by convention and statute:

Security deposit: typically 1 month per year of tenancy (2 months for a 2-year lease). The landlord must return the deposit within 14 days of lease expiry, less documented deductions for damage beyond fair wear and tear

Good Faith Principle (HDB): HDB subletting landlords may not impose conditions on how subtenants use common areas of the flat

Quiet enjoyment: A tenant in possession cannot be evicted without court order once a TA is duly executed and stamped

Utilities: Tenants are solely responsible for utilities (SP Services) unless expressly stated in the TA

Dispute resolution: Landlord-tenant disputes may be referred to the Community Disputes Resolution Tribunals (CDRT) or Small Claims Tribunals (SCT) for claims under S$20,000

Worked Example: The Nguyens Rent and Invest in Singapore

Mr & Mrs Nguyen, Vietnamese nationals on Employment Passes, arrive in Singapore in June 2026. They have a monthly EP allowance of S$12,000 combined and wish to rent a 3-bedroom condo in the east (D15/D16 Marine Parade/Bedok corridor) for a 2-year lease.

Agent commission: Typically 1 month (half/half split with landlord) = S$2,600, usually borne by landlord for a 2-year lease from month 13 onwards per industry convention

Total upfront cash outlay by tenant: S$10,400 + S$5,200 + S$1,997 = S$17,597

Annual rental budget: S$5,200 × 12 = S$62,400 (51.7% of annual EP income — in the higher range, but Singapore’s 55% TDSR is a credit metric, not an expense-to-income rule for tenants)

Simultaneously, Mr & Mrs Nguyen consider whether to invest in a D16 OCR condo unit at S$1.65M. As foreigners, they would pay BSD S$51,800 + ABSD S$1,072,500 (65% of S$1.65M) = S$1,124,300 total stamp duty — effectively a 68% surcharge on the purchase price. ABSD for foreigners at 65% makes direct property investment by foreigners financially prohibitive in most cases; rental remains the rational choice for non-PR residents.

Why the Rental Market Matters for Property Investors

Singapore’s rental market is not a peripheral consideration — it directly influences property valuations, lending decisions, and investment returns. The MAS Total Debt Servicing Ratio (TDSR) framework allows a landlord to include up to 70% of verified rental income from existing investment properties when computing their debt-servicing capacity for new loan applications. This means a property generating S$4,000/month in verifiable rental income effectively allows the landlord to carry an additional S$2,800/month in debt obligations under TDSR calculations — a meaningful lever for portfolio expansion.

For owner-occupiers considering upgrading, rental yield is also an opportunity cost metric: if your HDB flat could generate S$3,000/month post-MOP but you remain in it rent-free, that S$3,000 is the implicit value of owner-occupation compared against renting out and renting elsewhere. The condo vs HDB upgrader analysis is informed significantly by this rental yield comparison.

What Might Come Next for Singapore Rentals

The near-term rental outlook points to continued moderation. The completion of large private condo projects in the OCR and RCR pipeline — particularly the Tengah, Bukit Timah, and Greater Southern Waterfront corridors — will keep vacancy elevated through 2026–2027. However, several countervailing forces support long-term demand: Singapore’s push to attract global business headquarters, the expanding one-north and JTC LaunchPad ecosystem, and the steady pace of permanent residence approvals all support rental absorption. If URA’s Q2 2026 data (expected July 2026) shows vacancy stabilising below 8%, that will be a positive signal for landlords. The HDB subletting market is likely to tighten further as the 2019–2021 BTO cohort approaches MOP in 2024–2026, releasing a new wave of HDB supply into the rental pool at precisely the moment private vacancy is also elevated. Tenants may benefit from negotiating power in this window.

Frequently Asked Questions

Can I rent out my HDB flat before completing the MOP?

You cannot sublet the entire HDB flat before completing the 5-year MOP (or 10-year MOP for PLH/Plus flats). However, you may sublet individual rooms — provided you continue to reside in the flat yourself. Room subletting does not require HDB approval, but the occupancy cap still applies (maximum 6 unrelated persons, or 8 during the temporary relaxation period through January 2028). Subletting the entire flat pre-MOP is a breach of the HDB terms and conditions and may result in compulsory acquisition of the flat by HDB.

What is the minimum tenancy period for a private condo in Singapore?

The minimum tenancy for a private residential property (including condominiums, apartments, and landed houses) in Singapore is 3 consecutive months, as set by URA regulations. Any lease shorter than 3 months is classified as short-term rental and is prohibited. For HDB flats, the minimum is 6 consecutive months. Short-stay platform listings (Airbnb-style) are illegal for all residential properties in Singapore and can result in fines of up to S$5,000 per offence.

Do I need to pay income tax on rental income in Singapore?

Yes. Rental income received by individuals is subject to income tax under the Income Tax Act (Cap 134). You must declare gross rental receipts in your annual income tax return. Allowable deductions include mortgage interest (not capital repayment), property tax, fire insurance premiums, maintenance and repair costs, and agent commission. The taxable net rental income is added to your other chargeable income and taxed at progressive rates (0–22% for residents in YA 2026; 24% flat for non-residents). IRAS cross-references HDB and URA subletting records, so undeclared rental income carries significant audit risk. You may file via myTax Portal at iras.gov.sg.

Who pays stamp duty on a Tenancy Agreement — landlord or tenant?

By convention and IRAS practice, the tenant bears the stamp duty on the Tenancy Agreement, unless the TA expressly states otherwise. The rate is S$4 per S$250 (or part thereof) of the total rent payable over the term (for leases up to 4 years). Stamp duty must be paid via IRAS e-Stamping within 14 days of signing the TA if signed in Singapore, or within 30 days if signed overseas. An unstamped TA is inadmissible in court as evidence, which is a significant risk if a landlord-tenant dispute later arises.

Can a foreigner rent a private condo or HDB flat in Singapore?

Foreigners may rent private residential properties (condominiums, apartments, landed houses) without restriction. However, foreigners may only rent HDB flats if they hold a valid long-term pass — specifically an Employment Pass, S Pass, Dependent Pass, or Long-Term Visit Pass. Tourist visa holders (SVP/STP) and short-term pass holders cannot legally rent an HDB flat. The HDB maintains a non-citizen (non-Malaysian foreigner) quota of 8% per HDB block — once that quota is reached, additional non-Malaysian foreigners cannot rent any flat in that block regardless of their pass type.

What security deposit is standard in Singapore rental agreements?

Singapore’s rental market follows the convention of 1 month’s deposit per year of tenancy — so a 1-year lease carries a 1-month deposit and a 2-year lease carries a 2-month deposit. This is not enshrined in statute but is industry standard enforced by the IRAS stamp-duty framework (which uses “gross rent” inclusive of any deposit payments). The landlord must return the full deposit within 14 days after the lease end date, less documented deductions for damage beyond normal fair wear and tear. Disputes over deposit deductions may be brought before the Small Claims Tribunal (SCT) for claims under S$20,000.

What happens if my landlord refuses to return my security deposit?

If a landlord unlawfully withholds a security deposit, the tenant may file a claim with the Small Claims Tribunal (SCT) for disputes involving sums up to S$20,000, or with the Community Disputes Resolution Tribunal (CDRT) if the dispute also involves neighbourly conduct. A stamped Tenancy Agreement is the primary piece of evidence; ensure you retain a signed copy and document the flat’s condition with photographs at both the start and end of the tenancy. The Consumer Association of Singapore (CASE) also provides mediation for tenancy disputes. Singapore’s courts have consistently upheld tenants’ rights to deposit recovery where the landlord cannot produce evidence of actual damage.

Disclaimer: The information in this guide is for general educational purposes only and does not constitute legal, tax, or financial advice. Rental rules, stamp duty rates, and HDB policies are subject to change by the relevant authorities — HDB, URA, IRAS, CPF Board, and MAS. Always verify current rules at the official government portals (hdb.gov.sg, ura.gov.sg, iras.gov.sg) and consult a licensed property agent or solicitor before entering into any tenancy or purchase transaction. LovelyHomes is an independent editorial platform and is not affiliated with any property agency.

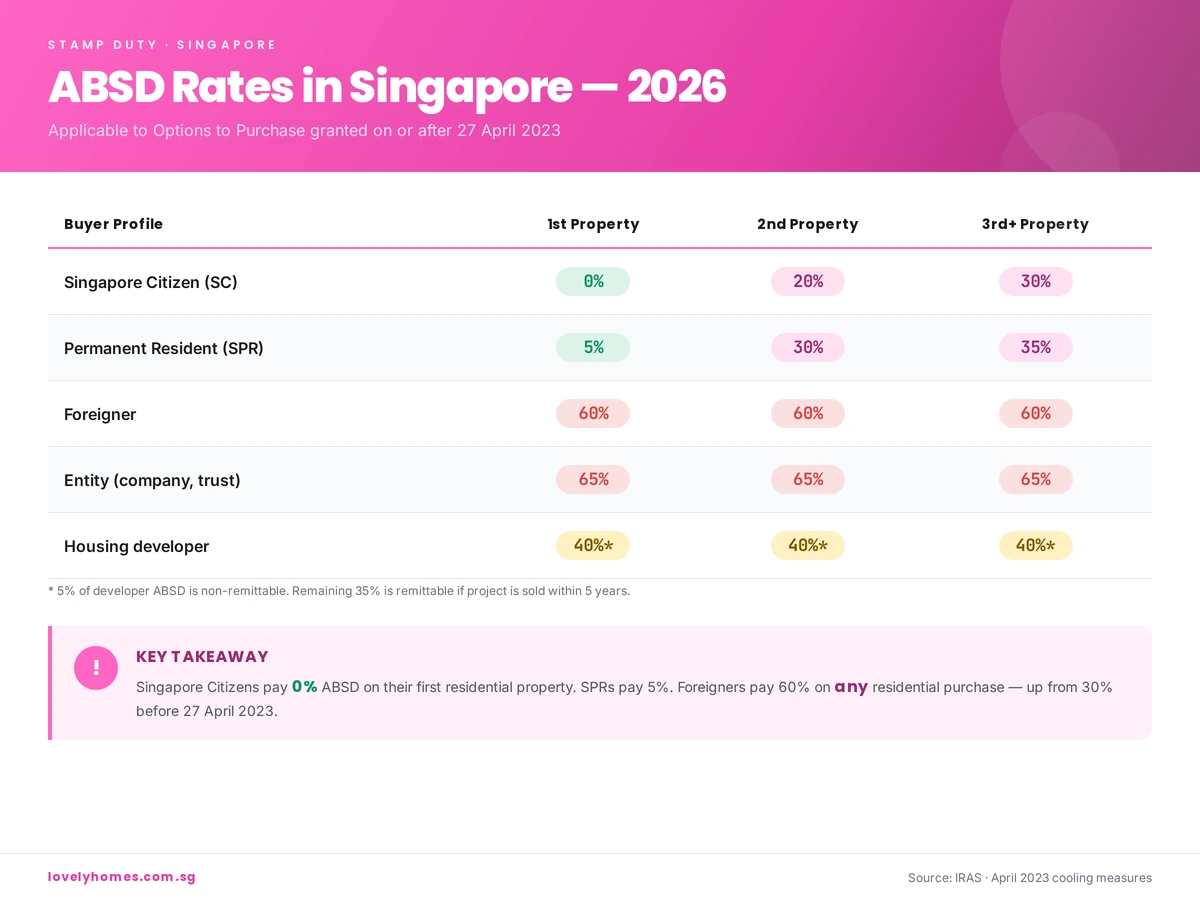

ABSD Singapore — short for Additional Buyer’s Stamp Duty — is the single largest upfront cost most buyers face when purchasing a second (or third, or fourth) residential property in Singapore. If you are buying as a foreigner, ABSD can add 60% of the purchase price to your cost. If you are a Singapore Citizen buying your second property, that figure is 20%. Get this number wrong in your budgeting, and you can very quickly wipe out years of planning.

This guide walks you through exactly how ABSD works in 2026 — who pays, how much, how it is calculated, what remissions are available, and the legitimate strategies property buyers use to manage it. All figures reflect the Government’s 27 April 2023 cooling measures, which remain the applicable framework. For the latest rates, always check the IRAS Additional Buyer’s Stamp Duty page.

Quick Answer — ABSD at a glance

Singapore Citizens: 0% on 1st property, 20% on 2nd, 30% on 3rd+

Singapore PRs: 5% / 30% / 35%

Foreigners: 60% on any residential property

Companies, trusts and other entities: 65%

ABSD is payable within 14 days of signing the Option to Purchase (OTP) or Sale & Purchase Agreement.

What is ABSD and Why Does It Exist?

ABSD is a transaction tax levied on the buyer when acquiring a residential property in Singapore. It sits on top of the regular Buyer’s Stamp Duty (BSD) that every buyer pays. Where BSD is progressive and maxes out at 6% for the portion of price above S$3 million, ABSD is a flat rate applied to the entire purchase price or market value (whichever is higher).

The tax was introduced in December 2011 as part of the Government’s suite of cooling measures — the tools Singapore uses to moderate speculative demand, manage affordability for owner-occupiers, and prevent the kind of runaway price inflation seen in other global cities. Because it targets second-and-subsequent-property buyers and non-citizens disproportionately, ABSD is the single most powerful lever in the cooling-measures toolbox. You can read more about the broader framework in our Property Cooling Measures section.

ABSD Rates in Singapore (2026)

The table below sets out the ABSD rates currently in force. Rates apply based on the profile of the buyer at the time the Option to Purchase (OTP) is granted.

ABSD rates by buyer profile — applicable to OTPs granted on or after 27 April 2023.

Buyer Profile

1st Residential Property

2nd Residential Property

3rd & Subsequent

Singapore Citizen (SC)

0%

20%

30%

Singapore Permanent Resident (SPR)

5%

30%

35%

Foreigner (non-PR individual)

60%

60%

60%

Entity (e.g. company, trustee for a trust)

65%

65%

65%

Housing developer

40%*

40%*

40%*

* 5% of a developer’s ABSD is non-remittable. The remaining 35% is remittable subject to conditions, including selling all units in a qualifying project within five years.

How ABSD is Calculated — A Worked Example

ABSD is applied to the higher of the purchase price or the market value of the property. It is not charged on a tiered basis — the full rate applies to the entire amount.

Example: A Singapore Citizen couple already owns their first home (a 4-room HDB flat). They decide to buy a S$2,000,000 resale condominium in District 15 as an upgrader investment. ABSD on the second property for a Singapore Citizen is 20%.

Purchase price: S$2,000,000

ABSD (20%): S$400,000

BSD (progressive, on S$2m): approximately S$64,600

Total stamp duty payable: S$464,600

That S$400,000 ABSD alone would consume most of the typical upgrader’s CPF and cash reserves. This is why many Singaporean couples take the ‘sell first, buy second’ upgrade route — selling the existing HDB or condo before buying the next home — which we cover later in this guide.

Who Pays ABSD? Exemptions and Special Cases

ABSD applies when you purchase an additional residential property. Commercial property, industrial property, and pure-land parcels are not within its scope. A property is counted toward your “property count” if:

You hold the title as a sole owner, joint tenant, or tenant-in-common;

You are a beneficial owner via a trust;

You are a beneficiary of an estate that holds residential property.

Properties not counted include: properties you merely reside in but do not own (e.g. as a tenant), inherited shares in a deceased estate within the administration period, and certain industrial/commercial units.

Executive Condominiums (ECs)

For new ECs bought directly from the developer during the minimum occupation period of the scheme, ABSD is not triggered because the buyer must commit to an owner-occupier arrangement. ABSD rules apply normally if an EC is purchased on the resale market after its 5-year MOP and 10-year privatisation milestones.

Free Trade Agreement (FTA) Nationals

Citizens and Permanent Residents of countries with which Singapore has an FTA extending National Treatment on stamp duty — namely Iceland, Liechtenstein, Norway, Switzerland, and United States citizens — are accorded the same ABSD treatment as Singapore Citizens. An eligible US citizen buying their first Singapore residential property therefore pays 0% ABSD, not 60%.

ABSD Remission Schemes — How to Get Some (or All) of It Back

Several remission schemes let qualifying buyers claim back part or all of the ABSD they initially pay. The big three to know are:

1. Married Couple Remission (Sale of First Residential Property)

If a Singapore Citizen (or mixed SC & SPR, SC & foreigner) couple buys a replacement home before selling their existing one, they can apply for ABSD remission provided they sell the first property within six months of the later of (a) the date of purchase of the replacement property, or (b) the TOP/CSC date if buying an uncompleted unit. This is effectively a “grace period” that allows upgraders to move without double-paying ABSD.

2. Mixed-Nationality Married Couples

An SC spouse married to a foreigner buying a matrimonial home jointly can enjoy SC rates (rather than foreigner rates) if the property will be used as their matrimonial home and conditions are met. Again, for a first joint home this means 0% ABSD.

3. Developer ABSD Remission

Licensed housing developers pay 40% ABSD upfront (5% non-remittable, 35% remittable) on land purchased for residential development. The 35% is remittable upon meeting development and sales conditions — typically completing the project and selling all units within 5 years.

Remissions must be applied for within strict timeframes (usually 14 days of the triggering event). We strongly recommend engaging a conveyancing lawyer who is experienced in stamp-duty remission applications before signing any OTP where remission will be relied upon.

ABSD vs BSD: What is the Difference?

Every property purchase in Singapore attracts Buyer’s Stamp Duty (BSD), which is a progressive tax on the purchase price:

1% on the first S$180,000

2% on the next S$180,000

3% on the next S$640,000

4% on the next S$500,000

5% on the next S$1,500,000

6% on the portion above S$3,000,000 (residential only)

BSD applies to every buyer; ABSD is the additional layer that may or may not apply depending on your citizenship status and property count. BSD and ABSD are payable together, within 14 days of signing the OTP.

The History of ABSD in Singapore (2011–2026)

Understanding how we arrived at today’s ABSD rates helps you anticipate where the Government may go next. The key milestones:

December 2011: ABSD introduced. Foreigners paid 10%; entities 10%; SPRs 3% on 2nd property; SCs 3% on 3rd+.

January 2013: First major hike. Foreigners to 15%, entities 15%, SPRs 5%/10%, SCs 7%/10% on 2nd/3rd.

July 2018: Rates raised again amid a reflating market. Foreigners to 20%, entities to 25%.

December 2021: Another round. Foreigners to 30%, entities to 35%, SPR 2nd property to 25%, SC 2nd to 17% / 3rd to 25%.

April 2023: The current regime. Foreigners doubled to 60%, entities to 65%, SPR 2nd to 30%, SC 2nd to 20%.

Each tightening has coincided with a period of accelerating private-residential price growth. For a full chronology including LTV, SSD and TDSR changes, see our comprehensive Property Cooling Measures archive.

How to Legally Minimise Your ABSD Bill

ABSD is not optional, but there are a handful of legitimate strategies buyers use to reduce the amount payable or to avoid triggering higher rates:

Sell first, then buy. For couples upgrading, timing the sale of your existing HDB or condo before the purchase of the next means you never hold two properties simultaneously and therefore pay 0% ABSD on the new first home (as an SC).

Use the matrimonial home remission. A mixed SC–foreigner couple buying their matrimonial home jointly enjoys SC rates if structured correctly.

Decouple responsibly. Where one spouse transfers their share of an existing property to the other, only the transferring spouse is freed to buy a second property as a “first” purchase. Decoupling has legal, CPF refund, and mortgage implications — always take specialist advice first.

Consider commercial or industrial property instead. Commercial and industrial properties do not attract ABSD. They have their own financing, GST, and tax considerations — but for investors focused on yield, they are worth analysing. See our Property Investment section for how commercial yields compare with residential.

Look offshore for second and third properties. Singaporeans investing in Malaysia (JB/Iskandar), Thailand, the UK, Australia, or Japan pay no ABSD to the Singapore Government for those purchases. Each destination has its own foreign-buyer regime, which we cover in our Foreign Property Investment guide.

Time your citizenship/PR application carefully. For families where PR or citizenship is in progress, the ABSD profile at the date the OTP is granted determines the rate. Moving the OTP date by a few weeks can, in edge cases, change the applicable rate by 15–25 percentage points.

Frequently Asked Questions

Is ABSD payable on the land value or the built-up value?

ABSD is calculated on the higher of the purchase price or the market value of the property at the time of acquisition. For new launches, this is typically the purchase price; for resale, IRAS may apply an independent market valuation.

When exactly is ABSD due?

Within 14 days from the date of the document triggering the duty — usually the signing of the Option to Purchase (for resale) or the Sale & Purchase Agreement (for new launches). Late payment attracts penalties.

Can CPF be used to pay ABSD?

No. ABSD (like BSD) cannot be paid from CPF directly at the point of purchase — it must be paid in cash. You can, however, apply for CPF reimbursement after the stamping is complete, drawing from your Ordinary Account against the purchase price.

Do I pay ABSD if I inherit a property?

No. A property acquired by way of inheritance is not a purchase and does not attract ABSD on the transfer itself. However, an inherited property does count toward your property count for future purchases.

I already own a commercial shophouse. Do I pay ABSD on my residential condo?

The residential-only count means commercial and industrial holdings are not included in your ABSD property count. If you are a Singapore Citizen buying your first residential property while owning commercial real estate, you still pay 0% ABSD.

How does ABSD affect an Executive Condominium purchase?

Buying a new EC from the developer under the EC scheme does not attract ABSD during the initial owner-occupation period. Once an EC is privatised (10 years after TOP) and traded on the open market, normal ABSD rules apply.

What to Do Next

ABSD changes how much house you can afford, how you time an upgrade, and sometimes whether a purchase makes sense at all. If you are weighing your options right now, we suggest three next steps:

If you are an upgrader, study our Upgrader Guide — the sequencing question (sell first vs buy first) is the single biggest lever for managing ABSD.

Review current market conditions in our Property News and Property Trends sections — if further cooling measures are telegraphed, timing your OTP becomes critical.

Looking at a specific development? Our detailed condo reviews — including One Marina Gardens, Arina East Residences, and our Aurea vs Chuan Park showdown — include the full ABSD-inclusive cost breakdown for various buyer profiles, so you can see the true entry cost before committing.

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. ABSD rates and remission rules change over time. Always verify the current position on the IRAS Stamp Duty page and consult a licensed conveyancing lawyer or tax specialist before acting on any property transaction.

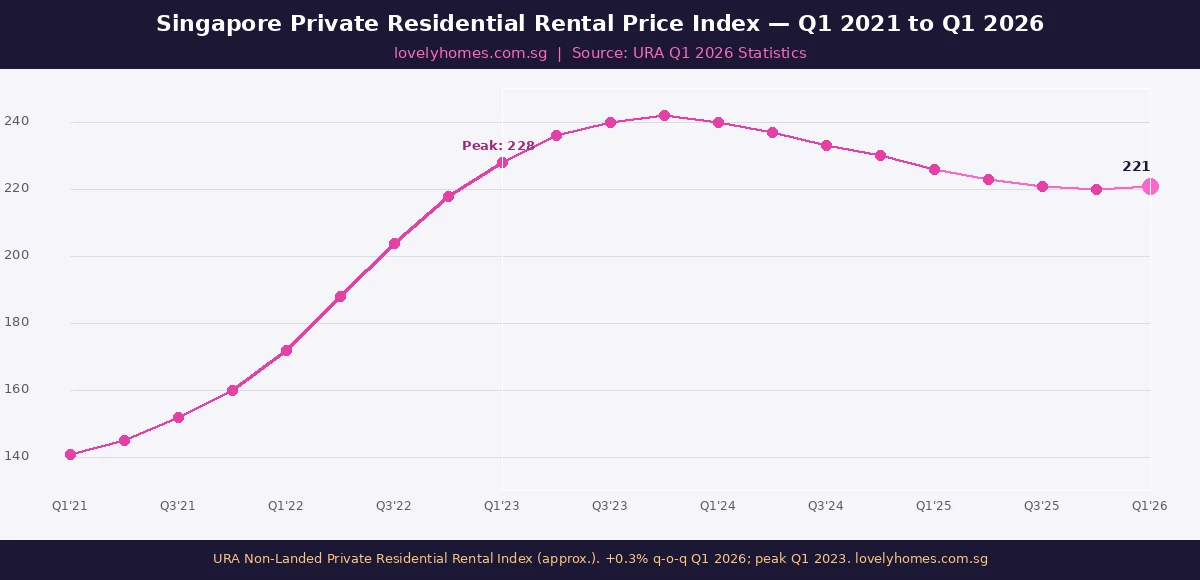

Rental index movement: URA’s non-landed private residential rental price index rose by +0.3% quarter-on-quarter in Q1 2026 — a near-stabilisation after 7 consecutive quarters of decline from the Q1 2023 peak.

Annual context: Over the full year 2025, private residential rents fell approximately 6–8% from their 2023 peak, unwinding roughly a quarter of the surge recorded during 2022–2023.

Supply pipeline: URA’s April 2026 data release confirms approximately 55,800 private housing units (including ECs) in the pipeline for completion over the next several years — a large structural overhang on rents.

HDB rental market: HDB approved subletting of whole flat volumes declined year-on-year in Q1 2026, but the median HDB whole-unit rent remains robust at S$2,500–S$3,200 for 4–5 room flats.

Tenants: Overall negotiating position for tenants improved significantly compared to 2022–2023; vacancy rates for private condos in OCR rose to approximately 7–9% in Q1 2026.

Outlook: Analysts expect private rents to remain broadly flat or edge up 0–2% through 2026 as demand from returning expatriates and work-pass holders partially offsets the supply glut.

When URA released its Q1 2026 full private residential statistics on 24 April 2026, the headline private residential price index grabbed attention: a 0.9% quarter-on-quarter rise, revised sharply upward from the flash estimate of 0.3%. Less remarked upon — but equally significant for landlords, tenants and property investors — was the rental index, which edged up a modest 0.3% in Q1 2026 after seven straight quarters of decline from the market peak in early 2023.

This article provides a comprehensive analysis of the Singapore private rental market in Q1 2026: where rents are, how they got there, which segments and regions are stabilising or still under pressure, and what the large supply pipeline means for landlords and tenants through the remainder of 2026 and into 2027.

Figure 1: URA Non-Landed Private Residential Rental Price Index, Q1 2021–Q1 2026. Rents surged 62% from Q1 2021 to the Q1 2023 peak before declining steadily; Q1 2026 shows the first positive quarterly reading in seven quarters. Source: URA | lovelyhomes.com.sg

Context: The Rental Surge, the Correction, and the Stabilisation

Singapore’s private rental market experienced an extraordinary run between mid-2021 and early 2023. Multiple structural forces converged simultaneously: a pandemic-era construction backlog delayed completions by 12–24 months; returning expatriates and a surge in S-Pass and Employment Pass (EP) holders concentrated demand; and HDB flat owners waiting for their own BTO completions flooded the private rental market. The URA non-landed rental index rose approximately 62% from Q1 2021 to its Q1 2023 peak — an extraordinary appreciation that made Singapore one of the most expensive rental markets in Asia during that window.

From Q2 2023 onwards, the correction was gradual but persistent. Completions of projects deferred from 2021–2022 began hitting the market in waves. Work-pass holders rationalised accommodation costs as global tech hiring slowed. HDB BTO completions (delayed by the construction backlog) began accelerating in 2024, freeing up some demand. By Q4 2025, the private rental index had fallen approximately 7.5% from its peak — unwinding some, but not all, of the pandemic-era gains.

Q1 2026’s +0.3% reading is therefore significant as a directional signal: the rental market has not collapsed back to pre-pandemic levels (as some landlords feared) but has instead stabilised at a level roughly 50% above Q1 2021 values. Whether this represents a floor or merely a pause before further softening depends critically on how quickly the pipeline of 55,800 remaining units is absorbed.

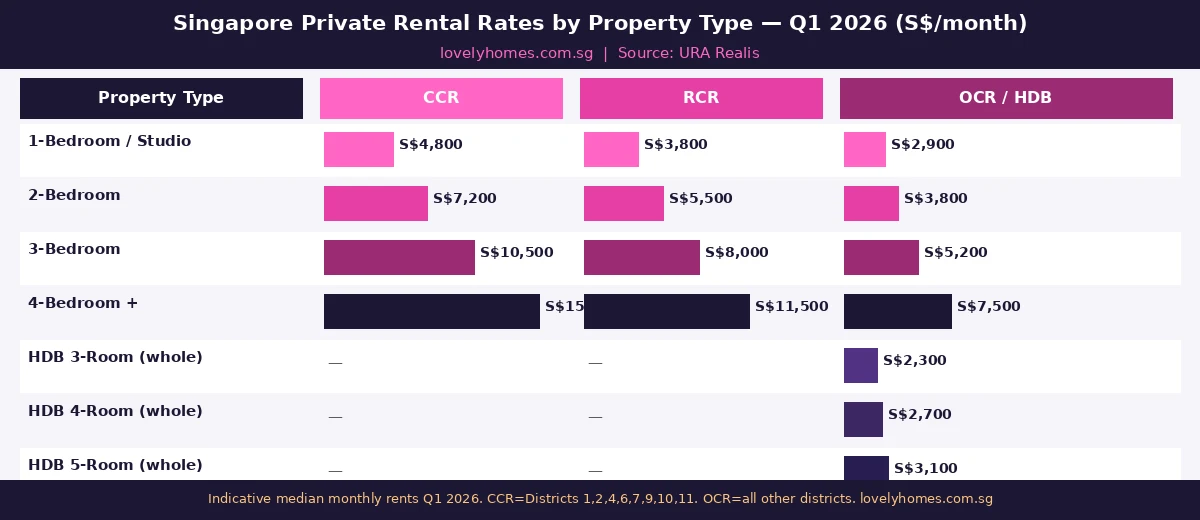

Rental Rates by Segment and Region: Where Is the Value?

Figure 2: Indicative median monthly rents by property type and URA market segment in Q1 2026. OCR represents the best value-for-money position for most tenant profiles. Source: URA Realis | lovelyhomes.com.sg

The rental market in Q1 2026 is highly segmented by both property type and location. The Core Central Region (CCR — Districts 1, 2, 4, 6, 7, 9, 10, 11) commands the highest rents, but has also seen the largest absolute corrections from its 2023 peak. A 2-bedroom CCR unit that rented for S$8,500–S$10,000 per month in early 2023 now transacts at approximately S$6,800–S$7,500. The Rest of Central Region (RCR) — mid-tier condos in Districts 3, 5, 8, 12–15, 20 — has proven more resilient, driven by domestic upgrader demand and relative affordability compared to CCR.

The Outside Central Region (OCR) is the segment showing the most rental stability in Q1 2026. Tenants priced out of CCR/RCR during the 2022–2023 boom have remained in the OCR, particularly in Tampines, Woodlands, Sengkang and Punggol, where rental yields for private condos remain approximately 3.0–3.5% on a gross basis. The Changi Business Park employment cluster in particular sustains demand for Tampines-area rentals from corporate tenants at rates of S$3,500–S$4,500 per month for a 2-bedroom unit.

Segment

Q1 2023 Median (2BR)

Q1 2026 Median (2BR)

Change

Vacancy Rate (est.)

CCR

~S$8,500

~S$7,200

−15%

~10–12%

RCR

~S$6,500

~S$5,500

−15%

~8–10%

OCR

~S$4,200

~S$3,800

−10%

~7–9%

The Supply Pipeline: 55,800 Units and What It Means

URA’s Q1 2026 statistics confirm a supply pipeline of approximately 55,800 private housing units (including executive condominiums) under construction or approved for construction. This is a substantial number relative to the annual new private housing completion rate of approximately 8,000–12,000 units per year in recent years. Spread across the 2026–2029 window, the pipeline represents approximately 4–7 years of average annual supply at historical absorption rates.

Not all of this supply will hit the rental market simultaneously. Owner-occupied units, units purchased as investment properties by buyers with long-term holding horizons, and units absorbed directly into owner-occupier demand (e.g., from HDB upgraders who sell their flat and move in) do not add to rental supply. In practice, analysts estimate that approximately 20–30% of new private completions in Singapore enter the rental market. On that basis, the pipeline implies approximately 11,000–17,000 additional rental units over the next 3–4 years — a meaningful but not overwhelming increment on a market of approximately 50,000–55,000 rental private residential units.

HDB Rental Market: A Different Dynamic

The HDB whole-unit rental market (subletting of HDB flats with HDB approval) operates differently from the private market. HDB restricts subletting to Singapore Citizens and PRs who are not concurrently buying another property, and enforces minimum subletting periods of 6 months. As a result, the HDB rental market is less volatile than private rentals. In Q1 2026, whole-unit HDB rentals showed modest quarterly softening, but the median whole-unit rent for a 4-room flat across Singapore remains approximately S$2,600–S$2,900 per month — still significantly above pre-pandemic levels of S$1,800–S$2,200. This provides a competitive floor under OCR private condo rents, since tenants choosing between a large well-located HDB flat and a smaller private studio will typically anchor their price comparison to HDB rental rates.

Worked Example: Tampines Investor — Rental Yield Recalculation Q1 2026

Mr Lim purchased a 2-bedroom private condo in Tampines in Q4 2021 for S$1,100,000. He rented it out in Q1 2023 at S$4,400 per month (gross yield 4.8%). By Q1 2026, the same unit rents for approximately S$3,800 per month as competition from new completions in the OCR has increased.

Current gross yield: (S$3,800 × 12) ÷ S$1,100,000 = 4.15%

Net yield (after property tax, maintenance, vacancy 2 mths/yr): approximately 2.8–3.1%

Capital appreciation since purchase: Q1 2026 OCR private condo resale value approximately S$1,370,000 — a gain of approximately S$270,000 (24.5% in 4.5 years)

Total return (rental + capital): approximately S$270,000 (capital) + S$190,000 (cumulative rent collected net of costs) = S$460,000 total return on S$1,100,000 — an annualised return of approximately 8.5%

This illustrates that even with the rental correction, the total return for investors who bought in 2021 and held through to 2026 has been strong, primarily driven by capital appreciation. The rental yield compression is real but manageable for investors with low leverage.

Outlook: Flat to Slightly Positive Rents Through 2026

The consensus view among Singapore property market analysts as of May 2026 is that private rents will remain broadly flat to marginally positive (0–2% growth) through the remainder of 2026. The key supporting factors are: modest improvement in global corporate hiring conditions; Singapore’s ongoing position as a preferred regional base for financial, technology and professional services firms; and the relative affordability of Singapore rentals compared to Hong Kong (which saw a 12–15% rental increase in 2025). The key headwinds remain the large supply pipeline and the stickiness of tenant habits formed during the correction (preference for smaller units, room rentals, or longer-term leases with break clauses).

For tenants, Q1 2026 is arguably the most tenant-friendly rental market Singapore has seen since 2020 — vacancy rates are elevated, landlords are willing to negotiate on fit-out allowances, and lease terms have become more flexible. For landlords and investors, the focus should shift to maintaining occupancy at competitive rents, minimising void periods and monitoring the pipeline of completions in their sub-market.

Frequently Asked Questions

Are Singapore private rents still falling in 2026?

The broad decline has largely stabilised. URA’s Q1 2026 data shows the non-landed private residential rental index rose +0.3% quarter-on-quarter — the first positive reading after seven consecutive quarterly declines from the Q1 2023 peak. However, the recovery is uneven: CCR and RCR rents are still 12–15% below their peak, while OCR rents have declined by a smaller 8–10% and are showing more stable trends. The large supply pipeline of 55,800 units means a sharp rental recovery is unlikely in 2026, but the worst of the correction appears to be behind us.

Which areas in Singapore have the best private rental yields in 2026?

In Q1 2026, the best gross rental yields for private condos are generally found in the OCR, particularly in employment-hub-adjacent towns: Tampines (near Changi Business Park), Woodlands (near Woodlands Regional Centre), Sengkang and Punggol (Seletar Aerospace/Punggol Digital District). Gross yields in these areas are approximately 3.2–4.0% for private condos, compared to 2.5–3.2% in CCR and 2.8–3.5% in RCR. HDB whole-unit rentals in mature OCR estates (Tampines, Bedok, Ang Mo Kio) can generate gross yields of 3.8–4.5% on a resale valuation basis, making them the highest-yielding mainstream residential asset class in Singapore.

Can a foreigner rent a private condo in Singapore?

Yes. Foreigners with valid immigration passes (Employment Pass, S-Pass, Dependent Pass, Long-Term Visit Pass or Student Pass) may rent private residential property in Singapore with no restriction. Foreigners may also rent HDB rooms (but not whole HDB flats unless the flat owner has obtained HDB approval for whole-unit subletting and the tenants meet HDB’s eligibility criteria). There is no cap on the rental amount or tenure for private condos, subject to the landlord’s minimum subletting period (most leases are 1–2 years). Short-term rentals of fewer than 3 months in private residential property are prohibited under the Planning Act and the Housing Agents Act.

Will Singapore rents rise or fall in the second half of 2026?

Most market analysts as of May 2026 expect Singapore private rents to remain broadly flat to slightly positive (0–2% growth) through the second half of 2026. The supply pipeline remains the dominant headwind — with approximately 55,800 private units under construction, completions will continue adding to available rental stock through 2027. However, demand from returning expatriates, regional hub activity and Singapore’s continued attractiveness as a base for financial and technology firms should partially offset supply pressure. The most likely scenario is rental stability with modest sequential gains in the OCR, and continued modest weakness in CCR luxury rentals where supply concentration is highest.

How does Singapore rental income get taxed?