Most Singaporeans know that property is a favoured investment asset. What fewer realise is that they can access Singapore’s real estate returns without buying a physical unit, without paying Additional Buyer’s Stamp Duty (ABSD), and with as little as the price of a single share on the Singapore Exchange (SGX). Singapore Real Estate Investment Trusts — known as S-REITs — are listed vehicles that pool capital to own income-producing real estate, distribute the bulk of their rental income to unitholders, and trade like stocks on SGX. In 2026, with interest rates easing and cap rates compressing, S-REITs are once again attracting strong attention from retail and institutional investors alike.

Quick Answer — Singapore REITs Investment 2026

- What: Listed property investment vehicles traded on SGX; own commercial, industrial, retail, healthcare or hospitality properties

- Minimum investment: As low as S$1 per unit (or one lot = 100 units for standard board lots)

- Tax transparency: Singapore individuals pay no withholding tax on REIT distributions (subject to MAS rules)

- ABSD: Zero — REITs are securities, not direct property purchases

- Indicative yields: 5.2%–6.4% distribution yield depending on sector (2026)

- Leverage cap: 50% aggregate leverage ratio (MAS guidelines)

- Key risk: Interest rate sensitivity — REIT unit prices fell sharply when rates rose 2022–2024; recovering in 2026

- Best for: Investors wanting passive income, diversification, or property exposure without ABSD or large capital outlay

What Are S-REITs and How Do They Work?

A Real Estate Investment Trust is a collective investment scheme structured to own and operate income-producing real estate. In Singapore, REITs are regulated by the Monetary Authority of Singapore (MAS) under the Securities and Futures Act. To qualify for tax transparency treatment, a Singapore REIT must distribute at least 90% of its taxable income to unitholders each financial year. In return, MAS-regulated S-REITs pay no corporate tax on distributed income, and individual Singapore resident unitholders receive distributions free of withholding tax.

S-REITs raise capital by issuing units on SGX. They use this capital, plus debt (up to the 50% aggregate leverage cap), to acquire properties that generate rental income. A REIT Manager — a MAS-licensed entity — makes investment, financing, and asset management decisions on behalf of unitholders. Management fees (typically 0.3%–0.8% of assets under management per annum) reduce net distributions to unitholders.

Types of S-REITs and Their Characteristics

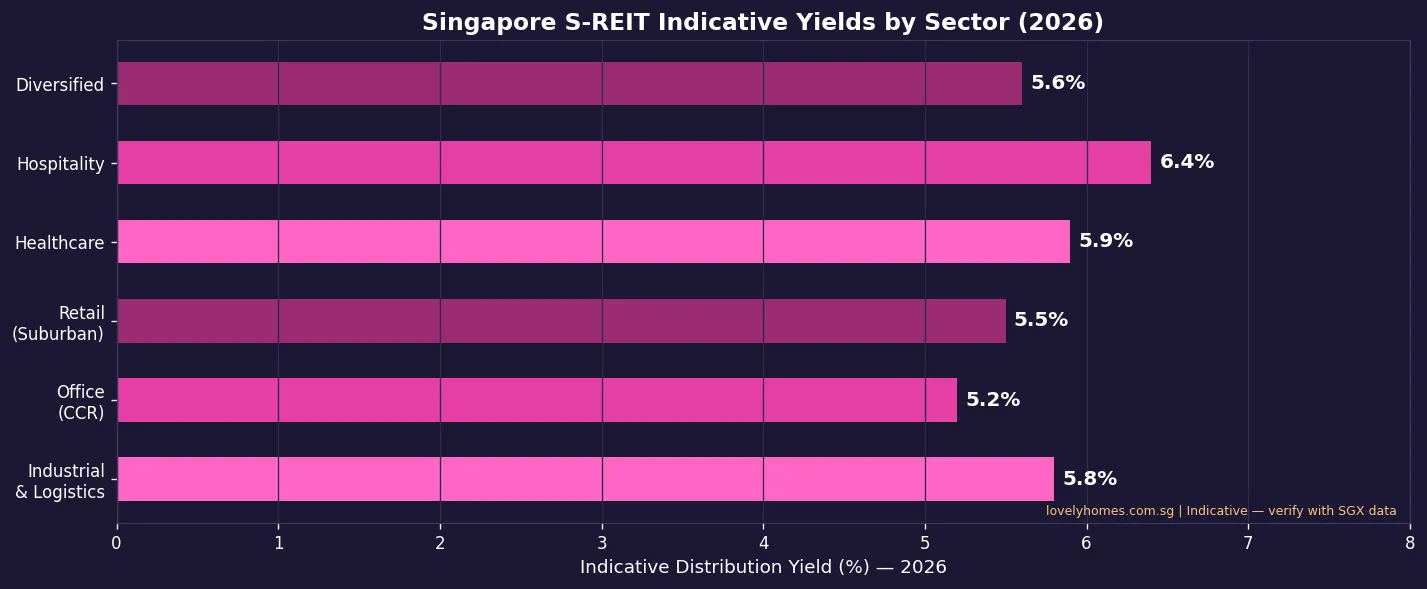

Singapore hosts one of Asia’s deepest REIT markets, with approximately 40 S-REITs and property trusts spanning several asset classes. Industrial and Logistics REITs own warehouses, data centres, and business parks with long leases (5–15 years) and strong demand from technology occupiers; indicative yields around 5.5%–6.0%. Office REITs own Grade A commercial buildings in the CBD; yields around 5.0%–5.5%. Retail REITs own shopping malls — suburban malls have proven resilient post-pandemic; yields around 5.3%–5.8%. Healthcare REITs own hospitals and nursing homes on long triple-net leases; yields around 5.5%–6.0%. Hospitality REITs own hotels and serviced residences; more volatile income but recovering with Singapore tourism; yields around 6.0%–6.5%. Diversified REITs own a mix of asset types, offering built-in diversification; yields around 5.3%–5.8%.

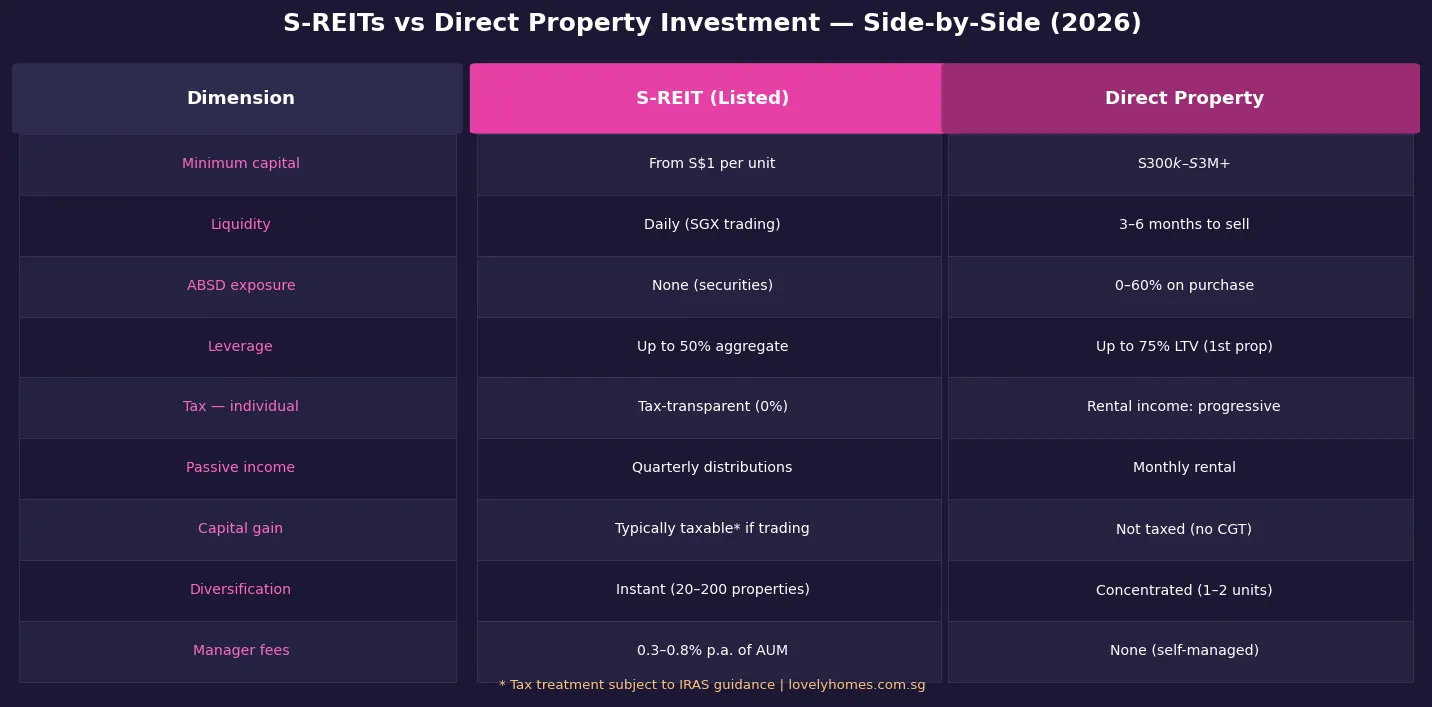

S-REITs vs Direct Property — The Critical Differences

The most significant advantage of S-REITs for Singapore residents is zero ABSD exposure. A Singapore Citizen buying a second residential property pays 20% ABSD on the entire purchase price — on a S$1.5 million condo, that is S$300,000 in ABSD before accounting for the regular Buyer’s Stamp Duty (BSD). Buying S$300,000 worth of a diversified S-REIT incurs no ABSD, no BSD, no conveyancing fees, and no mortgage-related costs.

Liquidity is another major difference. A direct property investment typically takes three to six months to sell, involves legal costs, agent commissions, and Seller’s Stamp Duty (SSD) if sold within three years. A REIT unit can be sold on SGX in seconds during market hours, and settlement occurs within two business days. The trade-off is stock market volatility: many quality S-REITs declined 20%–35% in unit price terms between 2022 and 2024 as the US Federal Reserve raised interest rates aggressively, even as their underlying properties continued generating stable rental income. In 2026, with SORA easing, S-REIT valuations have partially recovered.

Tax Treatment for Singapore Individual Investors

Singapore residents who are individuals receive S-REIT distributions free of withholding tax under the MAS tax transparency framework, provided the REIT distributes at least 90% of its income. This is one of the most favourable tax treatments for any income-generating investment in Singapore. By contrast, rental income from a directly owned investment property is taxed at the individual’s marginal income tax rate (up to 24% for income above S$1 million) after deducting allowable expenses. There is no Capital Gains Tax in Singapore, so gains on disposal of REIT units held for investment are generally not taxable — though IRAS may tax gains as income if the frequency and pattern of trading suggests a business of buying and selling REITs.

Key Facts: S-REIT Investment at a Glance

| Dimension | S-REIT (Listed) | Direct Property |

|---|---|---|

| Minimum capital | From S$1 per unit | S$300k–S$3M+ |

| Liquidity | Daily (SGX trading) | 3–6 months to sell |

| ABSD exposure | None (securities) | 0%–60% on purchase |

| Leverage | Up to 50% aggregate (MAS cap) | Up to 75% LTV (1st property) |

| Tax — individual | Tax-transparent (0% withholding) | Rental income: progressive rates |

| Indicative yield | 5.2%–6.4% (2026) | 2.5%–4.5% gross OCR (2026) |

| Diversification | Instant (20–200 properties) | Concentrated (1–2 units) |

| Manager fees | 0.3%–0.8% p.a. of AUM | None (self-managed) or agent fees |

Worked Example — Ms Chen Considers Her Options

Ms Chen is 38, a Singapore Citizen who already owns her HDB flat and has S$50,000 in investable savings. Option A — S-REIT: She invests S$50,000 in a diversified industrial S-REIT yielding 5.8% per annum. Annual distribution income: S$2,900. No ABSD, no BSD, no legal fees. Option B — Second Condo: She targets a S$1 million OCR condo as a second property. ABSD as a Singapore Citizen = 20% = S$200,000. BSD ≈ S$24,600. Total upfront stamp duties: S$224,600. Her S$50,000 would not even cover the stamp duties — she would need an additional S$174,600 just to clear the stamp duty obligation, plus the 25% down payment (S$250,000) and legal costs. For investors at Ms Chen’s capital level who already own one property, the REIT route offers immediate, tax-efficient property income with no stamp duty barrier.

Why This Matters — REITs as a Portfolio Complement

Singapore has actively developed the S-REIT market since the first REIT listed on SGX in 2002. Today, Singapore is the third-largest REIT market in Asia by market capitalisation. For retail investors, S-REITs provide access to institutional-quality properties — prime CBD office towers, logistics parks, hospitals, and data centres — that would otherwise be entirely out of reach. A S$5,000 investment in a well-managed industrial REIT gives proportional exposure to a portfolio of properties worth hundreds of millions of dollars, managed by professionals and audited to MAS standards.

What Might Come Next

In 2026, the REIT market is benefiting from a gradual easing in SORA rates. As the 3-month compounded SORA trends lower from its 2024 peak, financing costs for S-REITs ease and the distribution yield spread above the risk-free rate widens, making S-REITs more attractive relative to fixed deposits and Singapore Government Securities (SGS bonds). Investors should monitor SORA trajectory, MAS interest rate guidance, and individual REIT occupancy rates and lease expiry profiles. Always check the latest REIT financial statements on SGX before deploying capital.

Frequently Asked Questions

Do I pay ABSD when buying S-REIT units?

No. ABSD applies to purchases of residential property. S-REIT units are securities — not direct property ownership — and are bought and sold on SGX in the same manner as shares. There is no Buyer’s Stamp Duty, no ABSD, and no conveyancing process. The only transaction cost is brokerage commission (typically 0.05%–0.28% per trade on standard Singapore platforms).

How often do S-REITs pay distributions?

Most Singapore REITs distribute income quarterly, though some distribute semi-annually. The distribution is declared per unit (in cents per unit) and paid to unitholders on the register as at the ex-dividend date, received in your brokerage account within a few weeks of the payment date. Check each REIT’s investor relations page for its historical distribution per unit (DPU) track record.

Can I use CPF to invest in S-REITs?

Yes, subject to the CPF Investment Scheme (CPFIS). You can invest CPF OA savings in approved S-REITs listed on SGX under CPFIS-OA. You may invest up to 35% of your investable savings (OA balance above S$20,000) in stocks and REITs under CPFIS. Note that the 2.5% OA interest rate is the opportunity cost benchmark — if your REIT does not beat 2.5% on a total-return basis, leaving the money in your OA would have been better.

What are the key risks of investing in S-REITs?

Key risks include: (1) Interest rate risk — rising rates increase REIT borrowing costs and make their yields less attractive relative to bonds. (2) Occupancy/tenant risk — if key tenants vacate or become insolvent, rental income falls. (3) Currency risk — many S-REITs own properties overseas (Australia, Japan, Europe, US); income is earned in foreign currencies and translated back to SGD. (4) Rights issue dilution — to fund acquisitions, REITs frequently issue new units at a discount. (5) Manager quality risk — poor capital allocation erodes long-term value. Diversifying across multiple REITs and asset classes mitigates several of these risks.

Is S-REIT income taxable for Singapore residents?

Distributions from S-REITs to Singapore individual residents are generally exempt from withholding tax under MAS’s tax transparency framework. You receive distributions gross, with no tax deducted at source, and generally do not declare them as taxable income on your personal tax return. Capital gains from selling REIT units are also generally not taxable for investors. Non-residents and entities are subject to withholding tax on distributions. Verify your specific position with a tax adviser, as IRAS guidance may evolve.

What is the MAS 50% leverage cap and why does it matter?

MAS requires Singapore REITs to maintain an aggregate leverage ratio (total debt divided by total assets) of no more than 50%. REITs meeting an interest coverage ratio (ICR) of at least 2.5× can access the upper 50% limit; others are capped at 45%. This protects unitholders from excessive debt risk. When evaluating a REIT, check its reported leverage ratio and ICR trend in its financial statements — these are disclosed quarterly.

How do I start investing in S-REITs?

Open a brokerage account with a SGX-licensed broker (DBS Vickers, OCBC Securities, UOB Kay Hian, Moomoo, Tiger Brokers, or Interactive Brokers). Fund it with SGD. Search for SGX-listed REITs on the broker’s platform — filter by sector, yield, and market capitalisation. Standard board lots are 100 units. Research each REIT’s annual report, distribution history, and investor presentation before investing. The SGX REITs and Property Trusts section is the authoritative listing of all Singapore-listed vehicles.

Related Articles

0 Comments