HDB vs Condo Singapore 2026: Complete Comparison Guide

Quick Answer: HDB vs Condo in 2026 — Key Takeaways

- Cost gap is wide: a new 4-room BTO costs from S$350,000–S$500,000; an equivalent OCR condo easily costs S$900,000–S$1,200,000 — two to three times more upfront.

- Only Singapore Citizens can buy new HDB flats; Singapore Permanent Residents (SPRs) and foreigners are restricted to resale HDB (SPR only, with limitations) or private residential.

- ABSD applies to condos as a second property: a SC buying a second condo pays 20% ABSD on top of BSD; HDB upgraders face this fully.

- CPF can fund both, but the accrued interest rule means proceeds from selling an HDB flat are partially returned to CPF, reducing actual cash profit.

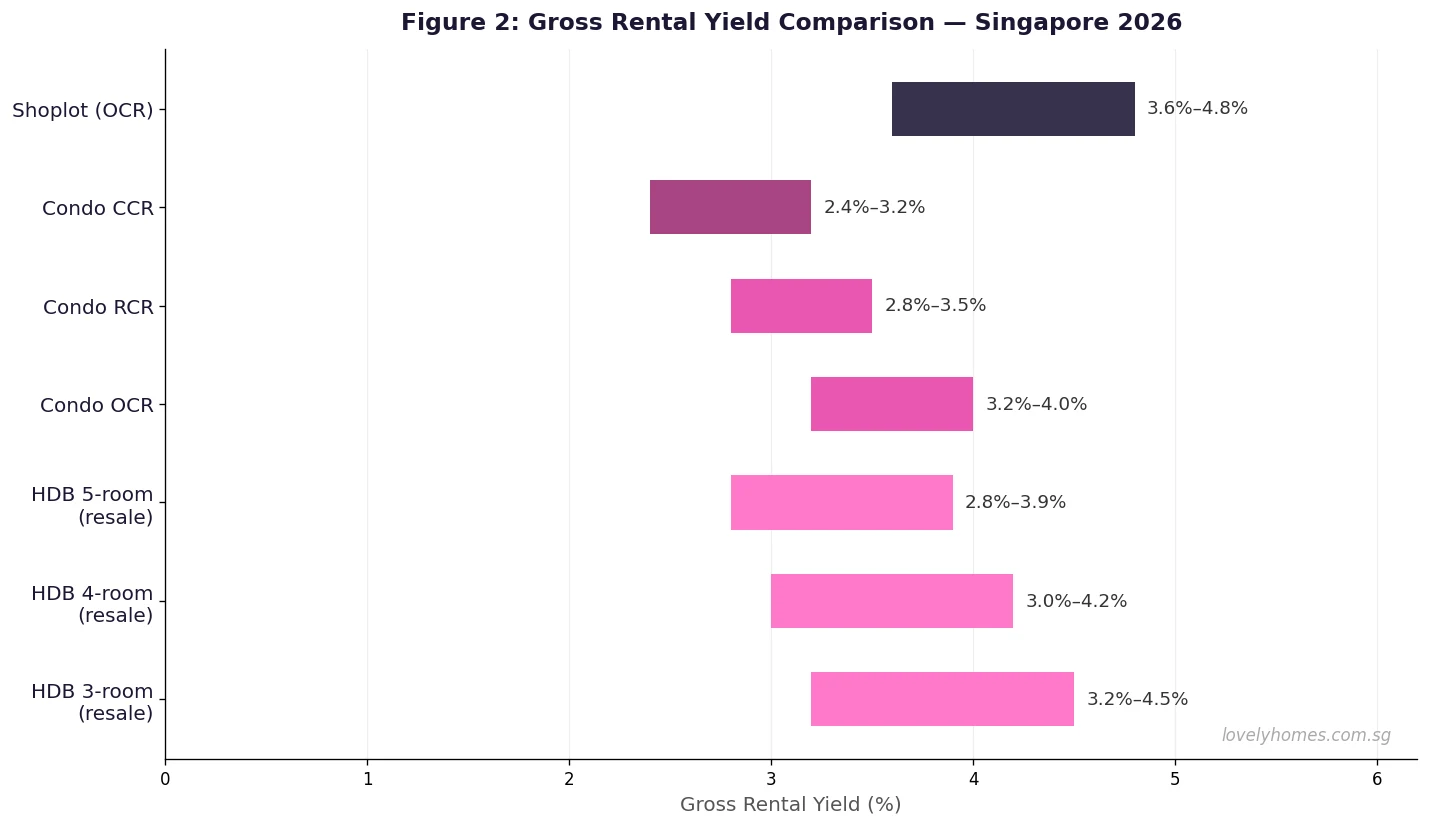

- Rental yield: HDB resale flats gross 3.0%–4.5%; OCR condos 3.2%–4.0%; the HDB advantage narrows significantly when considering non-owner-occupancy restrictions (10-year MOP rule for subletting applies).

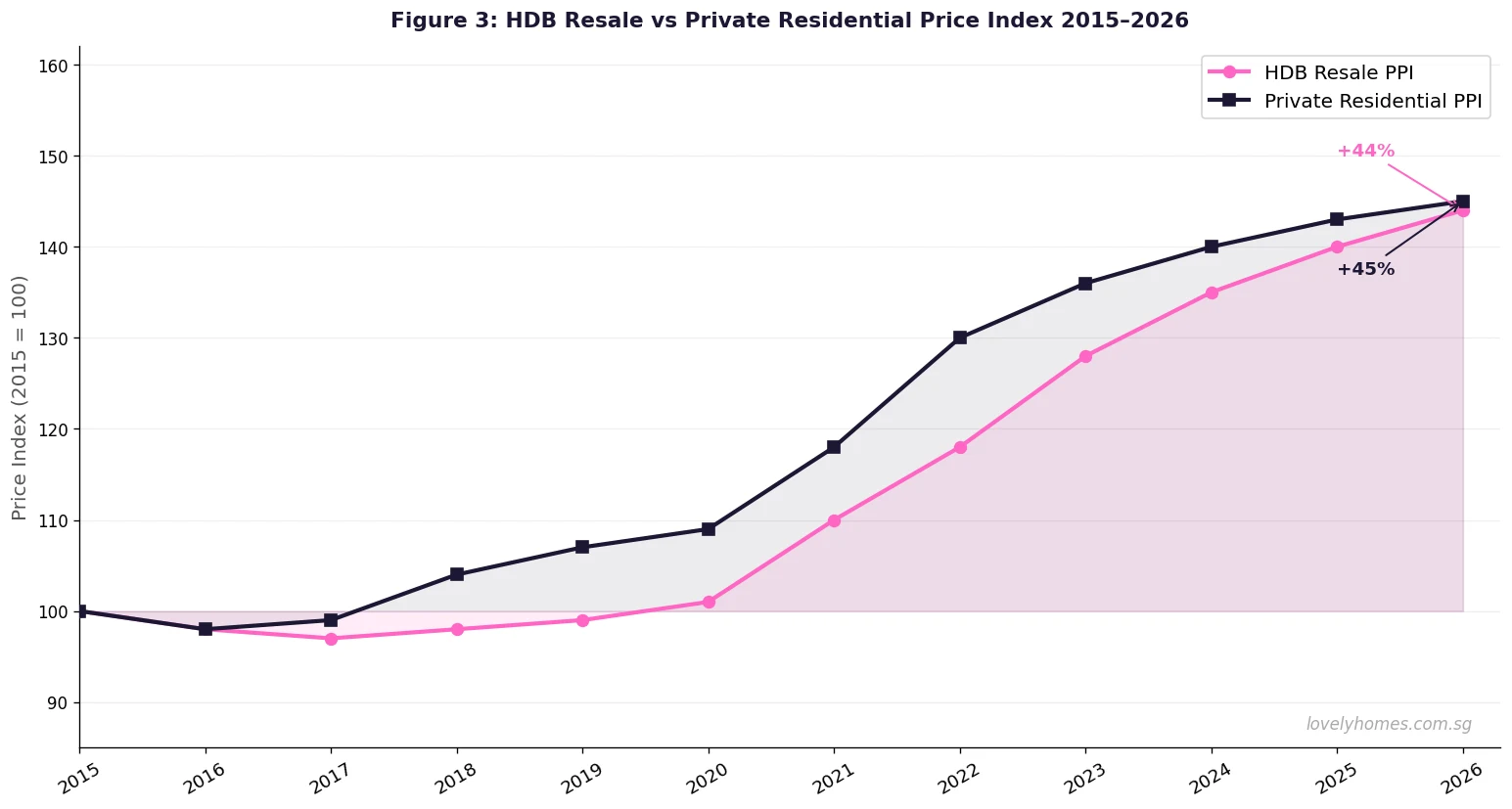

- Capital appreciation (2015–2026): HDB resale PPI is up approximately 44%; private residential PPI is up approximately 45% — broadly similar over a 10-year horizon.

- Condos offer facilities (pool, gym, function rooms, 24-hour security) that HDB blocks do not; this premium is priced in and reflected in maintenance fees of S$300–S$700/month.

- Decision rule of thumb: if your household income is below S$14,000/month, start with HDB (BTO or resale) to benefit from CPF grants and lower entry cost; graduate to private once equity has built up.

For most Singaporeans, the question is not simply “which is better?” — it is “which is right for me, right now?” The HDB vs condo decision shapes your finances, lifestyle and options for the next decade. This guide breaks down every dimension — purchase cost, ongoing fees, rental potential, capital growth, rules and restrictions — with real 2026 numbers so you can make an informed call.

The Financial Case: Upfront Costs Compared

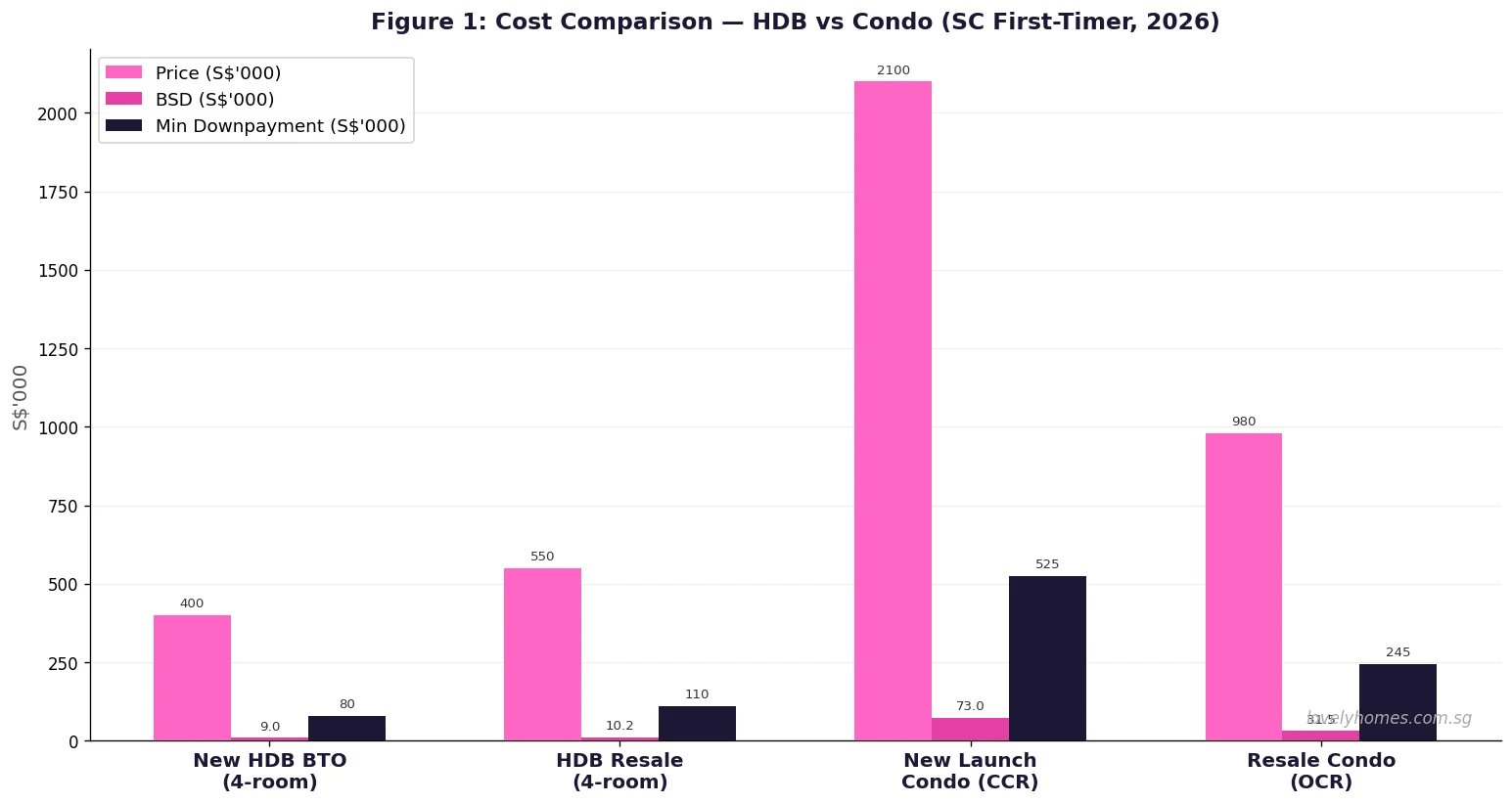

The starkest difference between HDB and private condominium ownership is the entry cost. A new HDB Build-To-Order (BTO) 4-room flat in a non-mature estate is priced from around S$350,000–S$500,000, subsidised by the Housing & Development Board (HDB) under the principle that public housing should remain affordable. An equivalent-sized (800–900 sqft) resale condominium in the Outside Central Region (OCR) typically changes hands at S$950,000–S$1,300,000 — roughly double to triple the cost.

This gap widens further once you account for BSD, legal fees, and the minimum downpayment. A first-timer Singapore Citizen (SC) buying a BTO flat pays no ABSD and a modest BSD of S$9,000–S$14,000 on an S$450,000 flat; the same buyer purchasing an S$1,000,000 condo pays BSD of S$32,600 and must stump up at least S$250,000 in cash or CPF as the 25% minimum downpayment (with at least 5% in cash if using a bank loan).

HDB grants add another layer of advantage for eligible buyers. A first-timer SC household with combined monthly income of S$9,000 qualifies for the Enhanced Housing Grant (EHG) of up to S$80,000 on a BTO flat, plus a Family Grant of S$50,000 on a resale HDB flat. These grants are non-repayable and come directly off the purchase price. No such grants exist for private property purchases.

The Minimum Occupation Period (MOP) is the trade-off: HDB flat owners must live in the flat for five years (ten years for Prime and Plus classification flats since August 2024) before selling or renting out the entire flat. Condo owners face no MOP restriction — they can sell or rent from day one, subject only to Seller’s Stamp Duty (SSD) if selling within three years.

Ongoing Costs: Monthly Commitments

Purchase price is only the beginning. The true cost of ownership includes monthly mortgage repayments, MCST maintenance fees (condos), conservancy and service charges (HDB), property tax, fire insurance and — for condos — sinking fund contributions.

For a 4-room HDB resale flat at S$560,000, the monthly mortgage on an HDB concessionary loan (2.60% per annum, 25 years, 80% loan) is approximately S$2,040. Monthly Service & Conservancy Charges (S&CC) for a 4-room flat average S$60–S$80 per month. Property tax for an owner-occupied HDB flat is effectively zero for most flat values, as the Annual Value (AV) is low and owner-occupier rates are 0% on the first S$8,000 AV.

For a 3-bedroom condo at S$1,200,000 (OCR), the monthly mortgage on a bank loan (3.50% fixed for two years, 75% LTV, 25 years) is approximately S$4,498. On top of this, MCST monthly fees typically range from S$350 to S$700 depending on the development’s facilities and share value. Property tax for a S$1,200,000 condo is roughly S$2,400–S$3,000 per year (owner-occupier rate on the estimated AV).

Over a 25-year holding period, the total interest cost is another S$180,000–S$300,000 for HDB borrowers versus S$300,000–S$550,000 for condo borrowers — a function of both the higher principal and higher interest rates on bank loans.

Rental Yield and Investment Returns

A common misconception is that condos automatically deliver higher rental yields. In Singapore, rental yields are a function of entry price, not just rental income — and since HDB flats are bought at subsidised prices, their yield on cost is frequently competitive with, or even superior to, condos.

However, the comparison is not straightforward. HDB flat owners face the five-year MOP restriction: you cannot rent out the entire flat during the MOP. After the MOP, you can sublet the whole flat with HDB’s approval (renewable every two or three years). Condo owners can rent out their unit immediately with no approval required. This flexibility premium is significant for investors who need early income.

For HDB upgraders buying a second property (a condo), ABSD applies at 20% for SCs — a substantial carry cost that compresses net returns. At S$1,200,000, ABSD of S$240,000 alone represents roughly 14 years of net rental income at S$18,000 per year. The breakeven horizon for an HDB upgrader buying an investment condo is therefore much longer than it appears at first glance.

Capital Appreciation: 2015–2026 in Data

Over the past decade, both HDB resale and private residential markets have delivered broadly similar capital appreciation. The HDB Resale Price Index (RPI) rose from a base of 100 in 2015 to approximately 144 by mid-2026 — a gain of around 44%. The URA Private Residential Property Price Index (PPI) moved from 100 to approximately 145 over the same period — a gain of about 45%.

The similarity masks important nuances. Private residential, particularly in the Core Central Region (CCR), outperformed in the 2021–2022 run-up, with some freehold D9/D10 developments gaining 25–35% in that window alone. HDB resale surged particularly in 2021–2023 as the pandemic-era demand for larger flats collided with restricted BTO supply, pushing mature estate 5-room flat prices above S$800,000 in some cases.

The key driver for private property appreciation is often freehold tenure and location within the CCR or RCR. A 999-year leasehold condo in Buona Vista has historically held its value better than a 60-year leasehold shoebox unit in an OCR new launch. HDB flats, by contrast, are all 99-year leasehold from the date the land was granted — and the lease decay effect becomes visible once the flat crosses 40 years, reducing bank loan quantum and CPF withdrawal eligibility.

Rules and Restrictions

Ownership eligibility is a fundamental constraint. HDB flats can only be owned by Singapore Citizens (BTO) or SCs/SPRs together (resale, with restrictions on ethnic composition under the Ethnic Integration Policy). Foreigners cannot own HDB flats at all. Private condominiums are open to all nationalities, though foreigners pay a punishing 60% ABSD on residential property purchases.

Subletting rules differ sharply. An HDB resale owner must wait for the MOP before subletting the entire flat; individual bedroom subletting is permitted during the MOP (maximum two non-Malaysian foreigners or six occupants). Condo owners can sublet their entire unit immediately, subject to a minimum rental period of three consecutive months (per URA rules since 2017). No renewal approval is required.

Redevelopment risk affects both. HDB estates are periodically redeveloped under SERS (Selective En-bloc Redevelopment Scheme) — owners are compensated at market value and offered replacement flats in the same or nearby precinct. For private condos, collective sales (en bloc) require 80% owner consent (90% for those less than ten years old) and full market pricing. En bloc payouts can be transformative for owners of older developments in prime locations.

Lifestyle Considerations

Condos typically offer facilities that HDB estates cannot match: swimming pools, gymnasiums, BBQ pavilions, function rooms, tennis courts and 24-hour concierge security. These amenities command a monthly maintenance fee but can significantly improve daily quality of life, particularly for families with young children or individuals who value recreational facilities within walking distance of home.

HDB towns are generally well-served by public transport, hawker centres, supermarkets and community clubs — the infrastructure of neighbourhood life is built into the planning template. Mature estates such as Toa Payoh, Tampines and Ang Mo Kio offer a richness of amenity that many suburban condos cannot match. For families prioritising proximity to good primary schools, both HDB and private addresses are relevant depending on the school’s 1 km radius — ownership type does not automatically determine school access.

Summary Comparison Table

| Factor | New HDB BTO (4-room) | HDB Resale (4-room) | New Launch Condo (OCR) | Resale Condo (OCR) |

|---|---|---|---|---|

| Typical price range | S$350k–S$500k | S$450k–S$750k | S$900k–S$1.4M | S$850k–S$1.3M |

| Who can buy | SC only (family/single ≥35) | SC + SPR (family nucleus) | All nationalities | All nationalities |

| ABSD (SC 1st property) | Nil | Nil | Nil | Nil |

| ABSD (SC 2nd property) | N/A (can’t buy BTO if owns private) | 20% (if owns private) | 20% | 20% |

| CPF grants available | Up to S$120,000 (EHG + others) | Up to S$130,000 (EHG + FG + PHG) | None | None |

| MOP / subletting restriction | 5 years (Prime/Plus: 10 years) | 5 years from completion | None — rent immediately | None — rent immediately |

| Gross rental yield (2026) | N/A (MOP applies) | 3.0%–4.5% | 3.2%–4.0% (OCR) | 3.2%–4.0% (OCR) |

| Monthly maintenance | S&CC: ~S$65/month | S&CC: ~S$65/month | MCST: S$350–S$700/month | MCST: S$350–S$700/month |

| Tenure | 99-year leasehold | 99-year leasehold (residual) | 99-year or freehold | 99-year or freehold |

| En bloc potential | SERS (government-initiated) | SERS (government-initiated) | Collective sale (80% consent) | Collective sale (80% consent) |

Worked Example: The Lim Family Decision

Mr and Mrs Lim are a Singapore Citizen couple, aged 32, with a combined monthly income of S$9,200. They are first-time buyers and must decide between a resale HDB 4-room flat in Tampines at S$560,000 and a resale 3-bedroom condo in Pasir Ris at S$1,050,000.

Option A — HDB Resale 4-room at S$560,000:

- Enhanced Housing Grant (EHG): S$55,000 (income S$9,200/month)

- Family Grant: S$50,000 (buying resale from non-related seller)

- Total grants: S$105,000

- Effective purchase price net of grants: S$455,000

- BSD on S$560,000: S$11,400

- HDB loan at 80%: S$448,000 @2.60% per annum, 25 years → S$2,030/month

- MSR check: S$2,030 ÷ S$9,200 = 22.1% — well within 30% cap. PASS

- Monthly S&CC: ~S$65

- Total monthly housing cost: approximately S$2,095

Option B — Condo resale at S$1,050,000:

- BSD: S$33,900 (no grants)

- ABSD: S$0 (first property for SC)

- Bank loan at 75%: S$787,500 @3.50% fixed, 25 years → S$3,940/month

- Minimum cash downpayment (5%): S$52,500 cash

- TDSR check: S$3,940 ÷ S$9,200 = 42.8% — within 55% TDSR. PASS

- Monthly MCST fees: approximately S$450

- Total monthly housing cost: approximately S$4,390

Verdict: Option A leaves S$2,295/month more in monthly cash flow — that is S$27,540 per year, or roughly S$275,000 over 10 years that can be redeployed into investments, education or a future upgrade to private property. For the Lim family at their income level, the HDB route captures S$105,000 in grants, stays well within the Mortgage Servicing Ratio (MSR) limit, and preserves significant financial flexibility.

What Might Come Next

The gap between HDB and private property prices is a live policy concern for the government. The August 2024 classification of BTO flats into Prime, Plus and Standard tiers — with differentiated MOP and subsidy recovery rules — signals that HDB will continue to be the primary vehicle for owner-occupier housing, while private property is positioned as a step-up or investment option for those who have built equity.

Cooling measures, including the current ABSD framework (20% for SCs on their second property), are explicitly designed to deter HDB upgraders from treating condo investment as a wealth-building short-cut. Whether the 20% rate will be adjusted in the near term is speculative; the Ministry of Finance (MOF) has consistently stated that measures will remain “calibrated” to prevent property from becoming a speculative asset class.

For buyers who are watching the market, the coming quarters offer one potential catalyst: the URA Q2 2026 full data release (expected 24 July 2026) will show whether the +0.5% QoQ private residential price gain in Q2 reflects stabilisation or early softening. HDB resale volumes have remained resilient at around 6,000–7,000 transactions per quarter, suggesting continued strong end-user demand regardless of investment sentiment.

Is it better to buy HDB or condo as a first-time buyer in Singapore?

Can I buy both an HDB flat and a condo at the same time?

Do HDB flats appreciate as well as condos?

What are the ABSD implications when upgrading from HDB to condo?

Can foreigners buy HDB flats in Singapore?

What is the difference in monthly costs between HDB and condo ownership?

Should I wait for BTO or buy HDB resale?

Click anywhere to close