Singapore Prime District Property Guide 2026: D9, D10 and D11 Complete Buyer’s Guide

- Prime district refers to Districts 9, 10 and 11 — Singapore’s Core Central Region (CCR), covering Orchard, River Valley, Bukit Timah, Holland Village, Newton and Novena.

- Prices range from approximately S$2,200 to S$5,500 psf for non-landed condominiums; Good Class Bungalows (GCBs) in D10 can exceed S$3,500 psf or S$30–S$65M per plot.

- ABSD for foreigners buying in prime districts is 60% on residential property — making CCR far more expensive for non-Singapore Citizens than OCR or RCR alternatives.

- CCR price growth since 2018 is +40% (URA PPI), lagging OCR’s +73% — but CCR’s rental yields (2.5–3.8%) and tenant quality (expats, HNW individuals) remain superior.

- No ABSD exemption for prime districts specifically — buyer profile (SC, PR, foreigner) determines ABSD, not location.

- Bank loans only for prime condos above S$4M; TDSR 55% applies; most buyers will need 25–40% cash/CPF downpayment.

- Rental demand remains strong: D9/D10/D11 house the bulk of Singapore’s international community and senior expatriate workers.

What Are Singapore’s Prime Districts?

When property professionals and analysts refer to “prime” residential property in Singapore, they mean Districts 9, 10 and 11 — three postal districts that together constitute the Core Central Region (CCR) residential belt. Administered under Singapore’s Urban Redevelopment Authority (URA) planning framework, the CCR is distinguished by its central location, high land values, superior amenity density and a tenant pool dominated by international businesses, embassies and high-net-worth individuals.

District 9 covers Orchard Road, River Valley, Cairnhill, Killiney and the Somerset corridor — Singapore’s retail and entertainment spine. District 10 encompasses Bukit Timah, Holland Road, Holland Village, Balmoral, Tanglin and the Good Class Bungalow (GCB) enclave of Nassim Road and Dalvey Estate. District 11 spans Newton, Novena, Thomson, Moulmein and the Dunearn Road corridor — a quieter, hospital-cluster area with strong medical professional demand. Together, these three districts contain some of Singapore’s most prestigious addresses, and set the benchmark against which all other residential property is measured.

This guide covers what you need to know in 2026: current prices by type and district, URA price index trends, stamp duty calculations by buyer profile, financing constraints, rental dynamics, and a full worked example for a Singapore Citizen purchasing a S$3.5M D10 condominium.

District 9 — Orchard and River Valley: Singapore’s Glamour Belt

District 9 commands the highest non-landed residential values in Singapore outside of Sentosa Cove. The Orchard Road corridor — stretching from Tanglin Mall to Plaza Singapura — anchors the district’s commercial identity, while the River Valley residential enclave (along River Valley Road, Kim Seng Road and Great World City) offers a slightly less frantic but equally prestigious residential address. Key developments in D9 include the freehold Ardmore Park (Scotts Road, ~S$4,200–5,500 psf), Claymore Connect, Cairnhill 16, and newer launches such as Haus on Handy and Orchard Sophia.

As at Q1 2026, URA REALIS data shows median non-landed transacted prices in D9 at approximately S$3,100–3,800 psf for newer freehold units and S$2,400–2,900 psf for 999-year leasehold or older freehold stock. Rental yields in D9 average 2.8–3.6% gross, supported by demand from multinational executives, banking professionals and the region’s diplomatic community. Studio and 1-bedroom units (400–700 sqft) targeting single expatriates rent for S$5,500–9,000 per month; 3-bedroom units (1,200–1,600 sqft) command S$8,000–14,000 per month in prime D9 buildings.

District 10 — Bukit Timah and Holland Village: GCBs and the Green Corridor

District 10 is arguably Singapore’s most prestigious postal district by land value and per-plot price. The Good Class Bungalow (GCB) Areas — including Nassim Road, Dalvey Estate, Swettenham Road, Ford Avenue and Bin Tong Park — are restricted to Singapore Citizens and house some of Singapore’s wealthiest individuals. GCBs in D10 have transacted at S$3,000–9,000 psf on land area, with entire plots changing hands at S$15M–S$65M. Under URA rules, GCBs must have a minimum land area of 1,400 sqm; demolition and rebuild is common, driving construction activity even in established enclaves.

For non-landed condominiums, D10 offers a range from established projects such as One Holland Village Residences (Holland Village MRT, ~S$3,100–3,600 psf), Leedon Green (Farrer Road, S$2,600–3,000 psf freehold), The Grange (S$3,000–3,500 psf) and boutique developments along Bukit Timah Road. The recently awarded Holland Plain GLS site (Sim Lian, S$1,491 psf ppr, April 2026) is expected to launch in Q3–Q4 2027 at indicative prices of S$3,100–3,800 psf, reinforcing D10’s CCR premium.

Proximity to international schools — United World College of South East Asia (UWCSEA), Anglo-Chinese School (International) and Tanglin Trust School — makes D10 especially attractive for families with school-age children. This factor consistently underpins rental demand even during market downturns.

District 11 — Newton and Novena: Medical Hub and Quiet Prestige

District 11 occupies the northern edge of the CCR belt, anchored by the Novena medical cluster (Tan Tock Seng Hospital, Mount Elizabeth Novena, KK Women’s and Children’s Hospital) and the Thomson/Newton MRT interchange. It is quieter and less trophy-centric than D9/D10, making it attractive to medical professionals, senior expats and buyers seeking CCR addresses at a slight PSF discount relative to Orchard or Bukit Timah.

Key non-landed developments in D11 include Pullman Residences (Newton Road, ~S$3,000–3,400 psf), The Atelier (Makeway Avenue, ~S$2,400–2,900 psf), and older leasehold stock along Thomson Road and Balestier. The Thomson-East Coast Line’s Stage 4 (TEL4) with Novena, Newton and Stevens stations puts D11 on Singapore’s most comprehensive transit corridor. Gross rental yields for D11 condominiums average 2.5–3.2%, with studios at S$3,800–5,500/month and 3-bedrooms at S$7,000–11,000/month.

| District | Coverage Area | Non-Landed PSF Range (2026) | Landed / GCB | Avg Gross Yield | Key MRT Stations |

|---|---|---|---|---|---|

| D9 | Orchard, River Valley, Cairnhill, Somerset | S$2,400–S$5,500 psf | Limited (no GCB area) | 2.8–3.6% | Orchard, Somerset, Dhoby Ghaut (NSL/CCL/NEL) |

| D10 | Bukit Timah, Holland, Balmoral, Nassim, Tanglin | S$2,600–S$5,200 psf | GCBs: S$3,000–9,000 psf land; S$15M–S$65M/plot | 2.5–3.5% | Holland Village (CC21/TE17), Farrer Road (CC28), Stevens (DT10/TE11) |

| D11 | Newton, Novena, Thomson, Moulmein, Dunearn | S$2,200–S$4,800 psf | Semi-D / terrace: S$2,600–4,500 psf land | 2.5–3.2% | Newton (NSL/DTL), Novena (NSL), Thomson (TEL) |

CCR vs RCR vs OCR — Price Growth, Yield and What the Data Shows

A common question from buyers is why CCR — the premium region housing D9/D10/D11 — has recorded the lowest absolute price growth over the past eight years. URA’s Private Residential Property Price Index (rebased 2018=100) shows CCR at approximately 140 as at Q1 2026 (+40%), versus RCR at 149 (+49%) and OCR at 173 (+73%). The explanation lies in three structural factors.

First, CCR’s 2017–2019 base was already elevated. Before the 2018 cooling measures, CCR prices were at multi-year highs driven by foreign buyer demand and en bloc proceeds; the 60% ABSD imposed in April 2023 then sharply curtailed new foreign buyer activity, which had historically been a CCR price driver. Second, OCR’s strong growth was partly driven by the HDB upgrader cohort — Singapore Citizens paying zero ABSD on their first private purchase — who targeted affordable OCR mass market condos. CCR’s price floor (~S$2,000 psf) is already beyond many upgraders’ reach, narrowing the buyer pool. Third, the sheer volume of new OCR and RCR supply from government land sales in Tengah, Jurong, Woodlands and Punggol has compressed per-unit land cost for developers in those regions.

However, CCR’s lower capital growth must be read alongside rental dynamics. CCR’s tenant pool — primarily multinational corporations on housing allowances, and high-net-worth individuals — tends to sustain rental demand through economic cycles better than mass-market OCR. During the 2022–2023 rental surge, CCR rents climbed 30–40% in absolute terms, narrowing the yield disadvantage versus OCR.

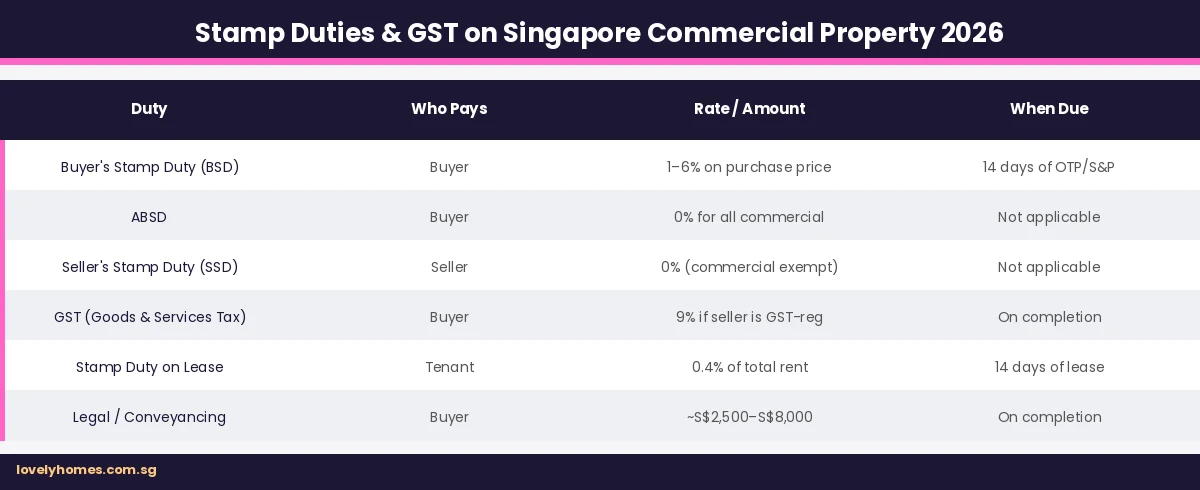

Stamp Duty and Total Acquisition Cost in Prime Districts

Buying in the prime districts involves the same stamp duty framework applied across all Singapore residential property — Buyer’s Stamp Duty (BSD) administered by the Inland Revenue Authority of Singapore (IRAS) and Additional Buyer’s Stamp Duty (ABSD) at rates set by the Ministry of Finance. No premium or surcharge exists simply because a property is in D9/D10/D11; however, the higher absolute prices mean BSD dollars are substantially larger.

BSD rates effective from 15 February 2023: 1% on first S$180,000; 2% on next S$180,000; 3% on next S$640,000; 4% on next S$500,000; 5% on next S$1.5M; 6% on any balance above S$3M. For a S$5M prime district condominium, BSD alone is S$234,600.

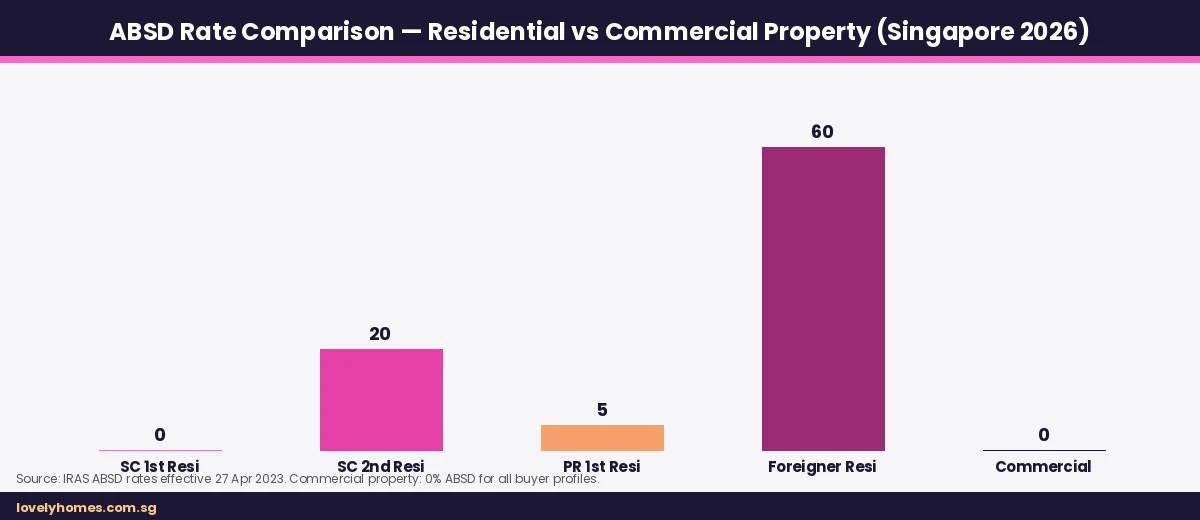

ABSD rates (as at 25 May 2026): Singapore Citizens purchasing a first residential property — 0%; second property — 20%; third and subsequent — 30%. Singapore Permanent Residents: first property — 5%; second — 30%; third+ — 35%. Foreigners (all residential property) — 60%. Entities — 65%. A German national buying a S$5M Orchard condominium therefore pays S$234,600 BSD + S$3,000,000 ABSD = S$3,234,600 in stamp duties — 65% of the purchase price — before any legal costs, renovation or financing.

Financing a Prime District Purchase — TDSR, LTV and Bank Loan Reality

All private condominium purchases in Singapore are subject to the Total Debt Servicing Ratio (TDSR) limit of 55% of gross monthly income, administered by the Monetary Authority of Singapore (MAS). At CCR price levels, this is often the binding constraint rather than the loan-to-value (LTV) cap.

For a S$3.5M condominium with a 75% LTV bank loan (S$2.625M) at 3.2% over 25 years, the monthly repayment is approximately S$12,748. A borrower would need minimum gross monthly income of S$23,178 to satisfy TDSR at 55%. Total upfront cash/CPF required (25% downpayment + 5% cash minimum + BSD S$154,600 + legal S$8,000–12,000) approximates S$1,050,000. This is the financial reality of prime district ownership and explains why many buyers are either existing asset-rich upgraders, HNW individuals, or institutional buyers.

CPF Ordinary Account (OA) savings may be used to pay the downpayment and monthly instalments for private property, subject to the Withdrawal Limit (WL) — 120% of the property’s Valuation Limit. For a S$3.5M valuation, the WL is S$4.2M; this effectively means CPF OA can fund the full loan until the borrower turns 55 or reaches the WL ceiling, whichever is earlier.

Worked Example: SC Couple Buying S$3.5M D10 Condominium

Mr and Mrs Goh are Singapore Citizens, both in their early 40s, with a joint gross monthly income of S$26,000. They currently own a HDB flat (MOP completed) which they plan to sell prior to completion of their private purchase, making this effectively their first private property (no ABSD applies as they will deregister ownership of the HDB).

Property: 3-bedroom, 1,249 sqft condominium in Holland Village (D10), purchase price S$3.5M. Freehold tenure.

BSD: 1% × S$180,000 (S$1,800) + 2% × S$180,000 (S$3,600) + 3% × S$640,000 (S$19,200) + 4% × S$500,000 (S$20,000) + 5% × S$2,000,000 (S$100,000) = S$144,600 BSD

ABSD: S$0 (SC, first private property after HDB sold)

Bank loan: 75% LTV = S$2,625,000 @ 3.00% fixed 2yr + floating thereafter, 25 years → S$12,474/month

TDSR check: S$12,474 / S$26,000 = 48.0% — within 55% TDSR limit. ✓

Upfront cash/CPF required: 25% downpayment S$875,000 (of which minimum 5% cash = S$175,000) + BSD S$144,600 + legal/disbursements est. S$10,500 + stamp certificate S$72 = approx. S$1,030,000 total

Note: If HDB is sold first (prior to private purchase completion), CPF OA refund and net sale proceeds can fund the downpayment and BSD — reducing the cash requirement substantially depending on outstanding HDB loan.

Why Prime District Property Matters — And Who It’s Really For

Singapore’s prime districts serve a structural role that goes beyond trophy ownership. D9/D10/D11 house the bulk of Singapore’s Grade A residential rental stock, which in turn supports the country’s ability to attract and retain senior multinational executives and wealthy international residents. The URA’s planning intent — preserving D9/D10/D11 as high-density, high-quality residential-commercial precincts — means future supply in these districts is constrained. GLS confirmed sites for CCR in the 1H 2026 GLS programme include only the Holland Plain site and Morrison Lane; there are no large-scale new CCR parcels equivalent to the OCR mega-projects in Jurong or Tengah.

For Singapore Citizens, prime districts offer a first-property opportunity with zero ABSD — but the entry price is S$2,200–3,000 psf minimum, meaning even a 1-bedroom unit costs S$1.2M–S$1.8M. The majority of SC buyers in D9/D10/D11 are upgraders from larger HDB flats or smaller private properties, with existing property equity supporting the jump. Permanent Residents face a 5% ABSD on their first purchase — a material S$60,000–S$150,000 cost on typical D9/D10/D11 units — which tends to push PR buyers toward the upper end of the mass market (D5, D15, D18) instead.

For foreign investors, the 60% ABSD remains prohibitive at CCR prices. A S$5M D9 unit now costs a foreign buyer S$8M all-in before financing. However, some ultra-HNW foreigners continue to purchase in D9/D10/D11 for estate planning, long-term Singapore residency or family lifestyle reasons, viewing the ABSD as a sunk cost against a generational asset. GCB purchases (freehold, D10) remain SC-only under the Residential Property Act, 1976.

What Might Come Next — Prime District Outlook H2 2026

Several factors may influence CCR pricing in the second half of 2026. First, the Federal Reserve rate path: MAS’s exchange rate-based monetary policy means SORA follows USD rate expectations; if the Fed begins cutting rates in late 2026, Singapore bank mortgage rates will ease, potentially unlocking additional buyer demand at current CCR price levels. Second, the Holland Plain GLS launch by Sim Lian (~Q3–Q4 2027) will set a new CCR price benchmark — market consensus is S$3,100–3,800 psf — and if it sells strongly, it may catalyse price momentum across surrounding D10 projects. Third, any changes to ABSD rates (currently at political equilibrium following April 2023 increases) are unlikely in the near term; the government has signalled ABSD as a demand management tool, not a revenue measure, and will only adjust in response to material price overheating.

The wild card for D10 specifically is the GCB market: GCB transactions in 2025 totalled 57 deals (S$2.1B) — near the historical average — and the market remains thin but liquid for the right plots. Any loosening of ABSD for SC buyers on their second property (currently 20%) would disproportionately benefit CCR, as SC upgraders are the largest buyer cohort for S$3M–S$5M prime district condominiums.

Frequently Asked Questions — Singapore Prime District Property 2026

Can foreigners buy property in D9, D10 or D11?

Yes, foreigners may purchase non-landed residential property (condominiums and apartments) in D9, D10 and D11 without restriction — but they must pay the 60% Additional Buyer’s Stamp Duty (ABSD) introduced in April 2023. Foreigners may not purchase landed residential property (including Good Class Bungalows) anywhere in Singapore without specific approval from the Singapore Land Authority (SLA), which is rarely granted outside of Sentosa Cove. Certain nationalities (US citizens, nationals of Iceland, Liechtenstein, Norway and Switzerland) benefit from FTA arrangements and pay 0% ABSD on their first residential property purchase, subject to compliance with the relevant free trade agreement terms.

What is the minimum price I should expect for a D9 or D10 condominium in 2026?

As at Q1–Q2 2026, the practical entry point for a studio or 1-bedroom unit in District 9 (Orchard/River Valley) is approximately S$1.4M–S$1.8M, reflecting unit sizes of 400–650 sqft at S$2,600–3,000 psf. In District 10 (Holland Village precinct), 1-bedrooms in newer developments (post-2020 TOP) begin at S$1.5M–S$2.2M. Larger 2-bedroom units (750–950 sqft) typically start at S$2.5M–S$3.5M across D9/D10/D11. Freehold units carry a 10–20% price premium over 99-year leasehold equivalents in the same location.

Is District 11 (Novena/Newton) cheaper than D9 and D10?

Generally yes — District 11 trades at a modest discount to D9 and D10, typically 8–15% lower in PSF terms for comparable unit types and age. This reflects D11’s less glamorous address (no Orchard Road, no Bukit Timah enclave), slightly longer walk to amenities in some sub-areas, and a more varied building quality mix. However, D11 still falls firmly within the CCR premium tier, and buildings adjacent to the Newton MRT interchange or Novena medical cluster command strong rents from medical professionals. The Thomson-East Coast Line (TEL) has added transit value to D11, partly closing the gap with D9/D10.

Are prime district properties good for rental investment in 2026?

Prime district properties offer lower gross yields (2.5–3.8%) than OCR mass market condos (3.5–5.0%), but the tenant profile is fundamentally different. CCR tenants are predominantly corporate-let expatriates and HNW individuals, who pay on time, cause less wear, and often renew for multi-year terms. Net yield after property tax (10–20% IRAS non-owner-occupier rate on Annual Value), maintenance fees (typically S$500–900/month for prime condos), and occasional vacancy can narrow to 1.8–2.8% net. For yield maximisation, OCR wins; for capital preservation, tenant quality and long-term asset liquidity, CCR prime districts remain the preferred institutional choice.

What is a Good Class Bungalow (GCB) and can I buy one in D10?

A Good Class Bungalow (GCB) is a landed residential property within one of 39 designated GCB Areas gazetted by the URA. GCBs must have a minimum land area of 1,400 sqm and are restricted to Singapore Citizens only — permanent residents and foreigners may not own GCBs without specific SLA approval, which is not granted in GCB Areas. District 10 hosts several of Singapore’s most exclusive GCB Areas, including Nassim Road, Dalvey Estate, Swettenham Road, Ford Avenue and Leedon Park. As at 2026, GCB asking prices range from S$20M (smaller, older rebuilds) to over S$60M for large freehold plots on Nassim Road.

Will cooling measures on prime districts ever be lifted?

The government has not signalled any plans to reduce the 60% ABSD for foreigners or the 20% ABSD for SC second-property buyers, both of which disproportionately affect prime district demand. The April 2023 ABSD increases were explicitly designed to cool the high-end residential market following a sustained post-pandemic surge. Any easing would most likely be incremental and targeted (e.g., reducing SC second-property ABSD from 20% to 15%, or adjusting PR rates), rather than wholesale removal. Buyers should plan on current ABSD rates remaining in place through at least 2027.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Foreigners Buying Property in Singapore 2026: ABSD Rates, Eligibility and Cost Guide

- Stamp Duty Calculator Singapore 2026: BSD and ABSD Complete Guide

- Singapore Landed Property Buying Guide 2026: Terrace, Semi-D, Bungalow and GCB

- Rental Yield vs Capital Gain Singapore 2026: The Property Investor’s Decision Framework

- Holland Plain GLS 2026: Sim Lian Wins at S$1,491 psf ppr — D10 CCR Pricing and Investment Outlook

- Singapore Home Loan Interest Rates 2026: SORA vs Fixed Rate Complete Guide

Disclaimer

This article is for general informational and educational purposes only. Property prices, stamp duty rates, MAS financing rules, URA planning guidelines and CPF policies are subject to change; readers should verify all figures with official sources including the Urban Redevelopment Authority (ura.gov.sg), Inland Revenue Authority of Singapore (iras.gov.sg), Monetary Authority of Singapore (mas.gov.sg), CPF Board (cpf.gov.sg) and Singapore Land Authority (sla.gov.sg). Nothing in this article constitutes financial, legal, tax or investment advice. Before purchasing any property, consult a licensed financial adviser, a practising lawyer and a CEA-registered property agent. LovelyHomes publishes this content in good faith but accepts no liability for decisions made in reliance on the information presented.