Click image or press Esc to close

Quick Answer: Bishan Neighbourhood at a Glance

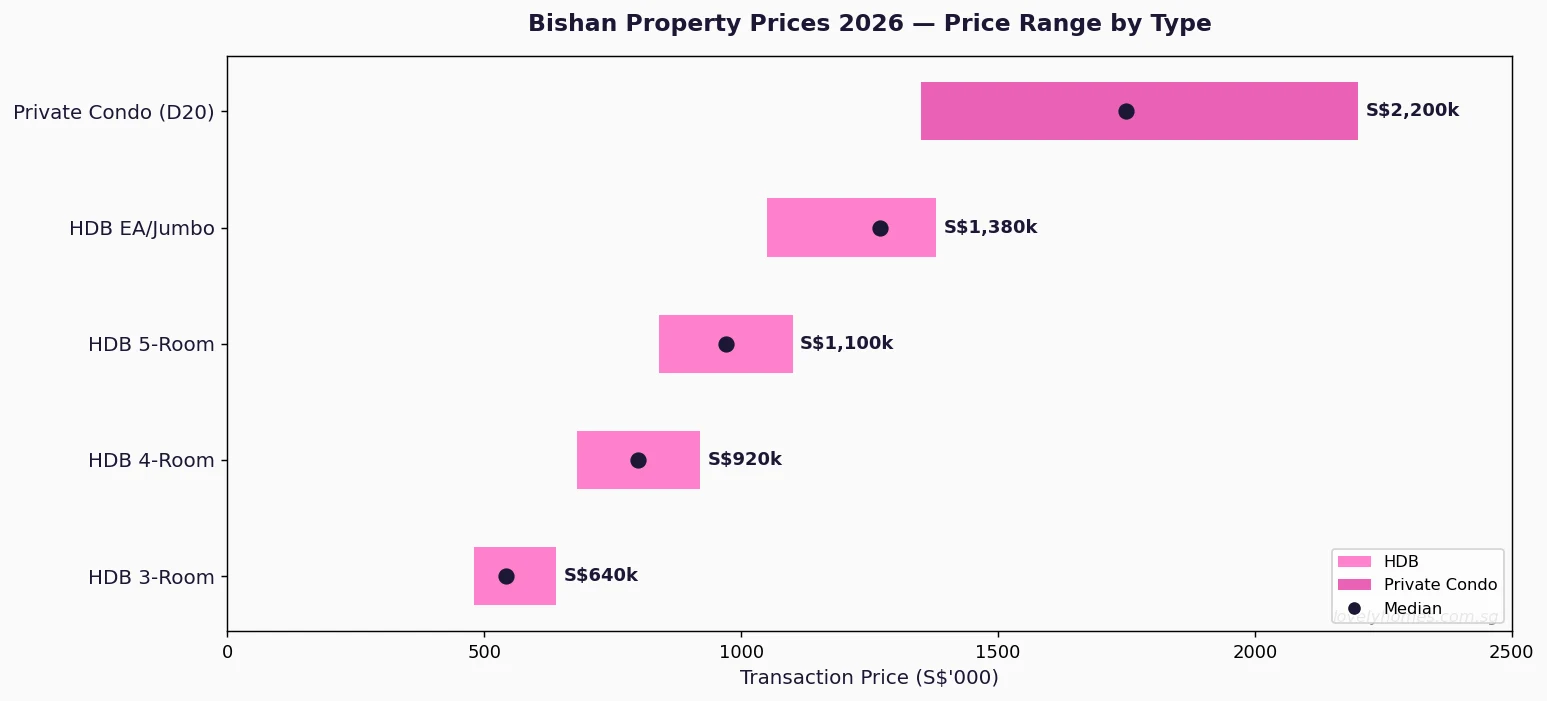

- HDB resale prices (2026): 3-room S$480k–S$640k | 4-room S$680k–S$920k (median S$800k) | 5-room S$840k–S$1.1M — among Singapore’s most premium HDB estates.

- Private condo (District 20): S$1.35M–S$2.2M for freehold and 99-year leasehold units in a supply-constrained market with no major new launches since 2021.

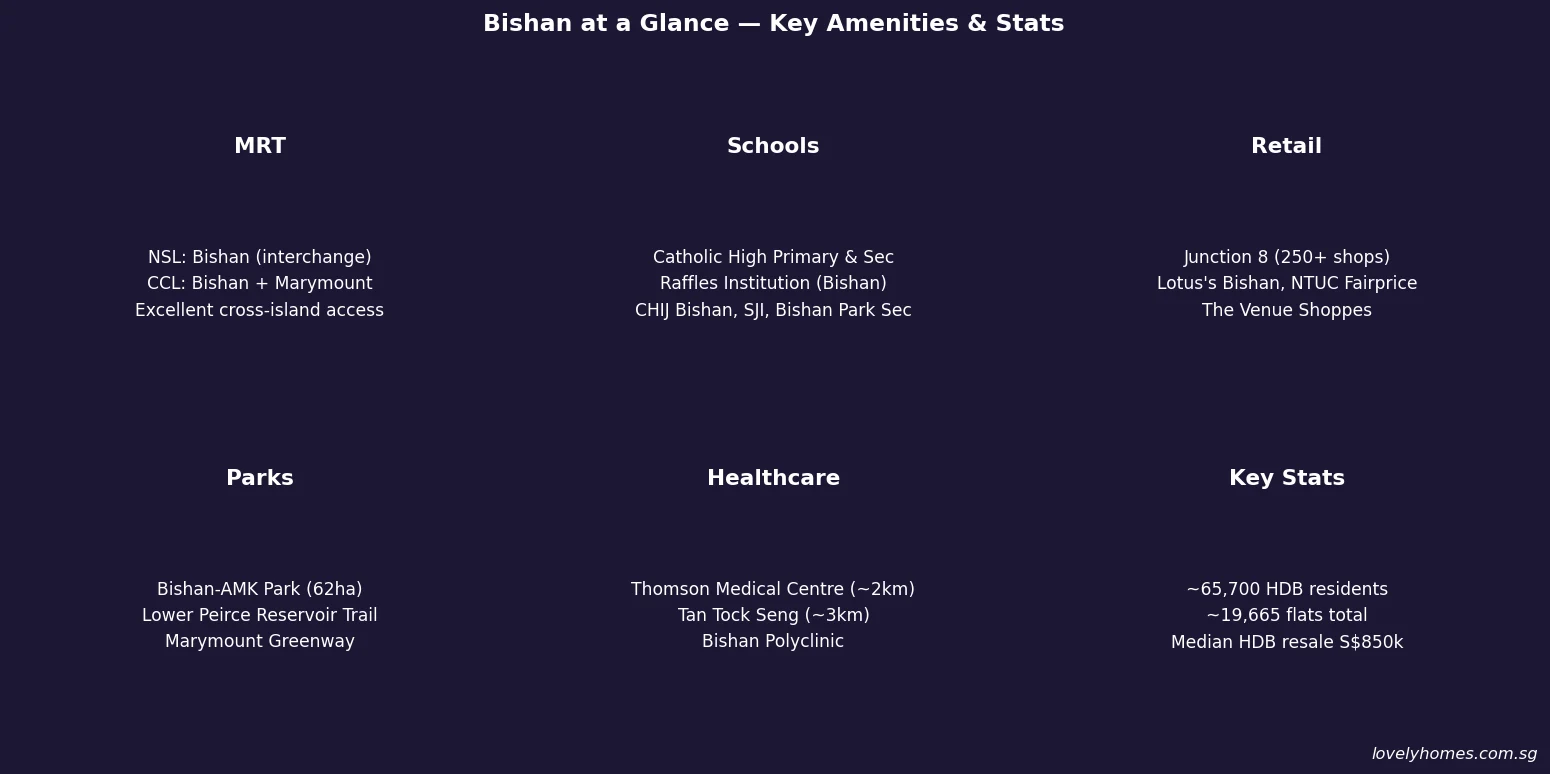

- MRT: North–South Line and Circle Line both pass through Bishan station (double interchange); Marymount (CCL) also serves the estate — exceptional cross-island access.

- Schools: Raffles Institution (Bishan campus), Catholic High Primary & Secondary, CHIJ Bishan — one of Singapore’s top school corridors, rivalling Queenstown and Toa Payoh.

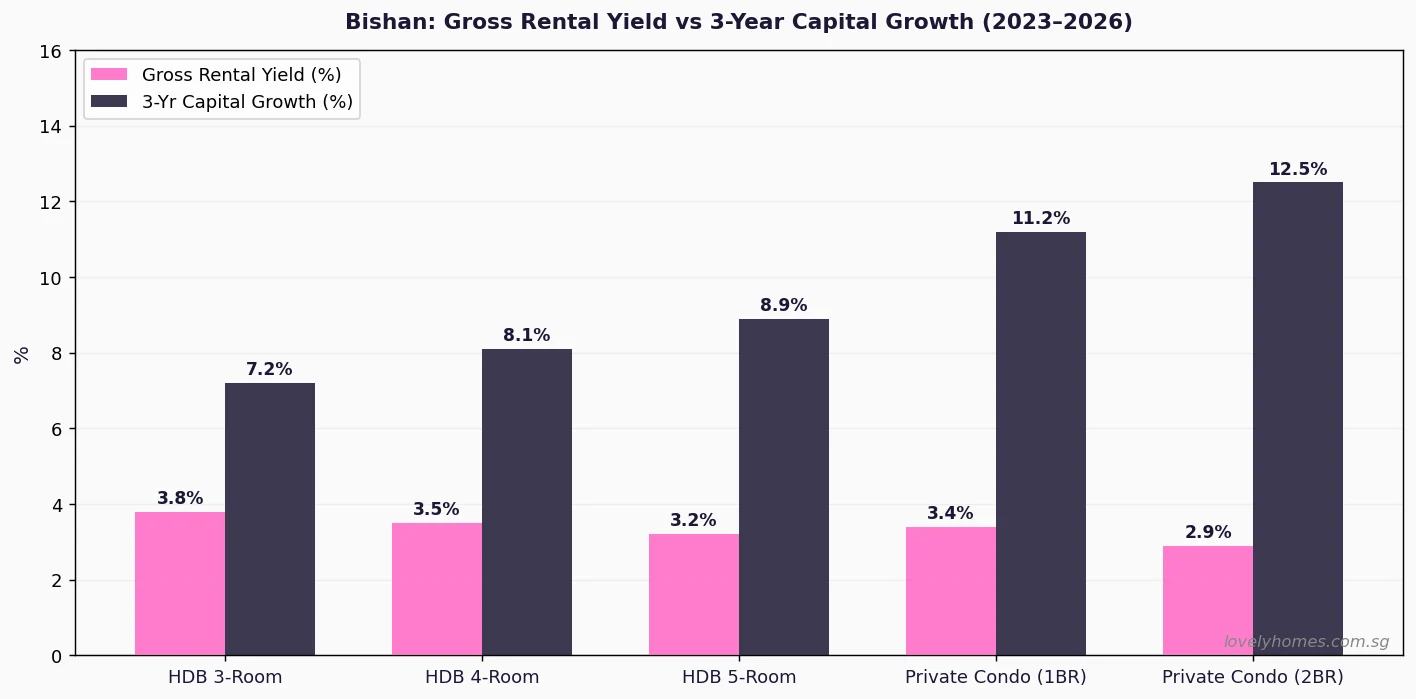

- Gross rental yield: HDB 3-room 3.8% | private condo 2.9–3.4% — lower than OCR averages, reflecting Bishan’s capital appreciation premium.

- 3-year capital growth (2023–2026): HDB 5-room +8.9% | private condo (2BR) +12.5% — outperforming the national average.

- June 2026 BTO: HDB will offer new flats in Bishan as part of the June 2026 exercise — likely Plus or Prime classification given the mature estate status and MRT proximity.

- Supply scarcity: Bishan has approximately 19,665 HDB flats and virtually no land for new private residential GLS — a structural supply constraint that supports long-term price stability.

Introduction: Bishan’s Enduring Premium in Singapore’s Property Market

Bishan is one of Singapore’s most sought-after HDB towns — and arguably the one that most consistently defies the public-housing price ceiling. With a median HDB resale price of approximately S$850,000 across 411 transactions in the first four months of 2026 — including executive and multi-generation flats commanding S$1.27M–S$1.39M — Bishan sits in a property tier that bridges the gap between HDB and private condominium ownership in a way that few other towns manage.

The estate was gazetted in the 1980s on land previously used as the Peck Shan Theng cemetery, and its development was carefully planned around three anchors that have proven durable: first-class MRT connectivity (it hosts one of only four NSL–CCL interchanges in Singapore), a concentrated school corridor anchored by Raffles Institution and Catholic High, and the 62-hectare Bishan–Ang Mo Kio Park — one of Singapore’s largest urban nature parks. These structural advantages have made Bishan one of the most defensible property markets on the island, capable of holding value even during market corrections.

In 2026, three dynamics are shaping Bishan’s market: the continued migration of HDB upgraders from surrounding estates seeking established schools and park proximity; the resurgence of private condo interest in a supply-constrained district where no major new launch has occurred since 2021; and the announcement of the June 2026 BTO exercise, which will add new flats likely classified as Plus under HDB’s new framework — carrying a 10-year MOP and subsidy clawback provisions that will moderate resale supply for a decade.

Property Market Overview: HDB Resale Prices in Bishan 2026

Bishan’s HDB resale market is characterised by premium pricing relative to most OCR and even many RCR estates, underpinned by genuine demand from school-corridor buyers and MRT interchange seekers. Price growth over the past three years has been moderate but consistent — approximately 7–9% for 4-room and 5-room flats — without the sharp corrections seen in Queenstown (which experienced cooling-measure headwinds in 2023).

Three-room flats, representing an older and less actively traded segment in Bishan, transact at S$480,000–S$640,000, with a median of approximately S$542,000. Four-room flats — the estate’s most traded category with 199 transactions in the first four months of 2026 — record a median of S$800,000 and a range of S$680,000–S$920,000. Five-room units, popular with larger families and CPF-flush upgraders, command S$840,000–S$1.1M. Executive Apartments and multi-generation units, found in blocks like Bishan Street 22 and Street 24, are transacting at S$1.05M–S$1.38M — firmly within the million-dollar flat segment.

On the private residential side, District 20 condominiums including Clover by the Park, Bishan 8, and the freehold Thomson Three have seen prices range from S$1.35M (smaller 1-bedroom units) to S$2.2M (3-bedroom). The median private transacted price is approximately S$1,750 per square foot, reflecting the district’s premium over OCR benchmarks of S$1,100–S$1,400 psf.

Bishan’s Three Subzones: Where Within the Estate Matters

Bishan is divided into three primary subzones: Bishan East, Upper Thomson, and Marymount, each with a distinct character and proximity profile.

Bishan East is the commercial and transport core, centred on Bishan MRT station (NSL and CCL interchange) and Junction 8 shopping mall. Flats in Bishan East command the highest premiums within the estate, typically 8–12% above the town average for equivalent flat types, owing to walkability to the MRT interchange and the concentration of retail, F&B, and services at Junction 8. This subzone is the preferred choice for transport-prioritising buyers and rental investors targeting working professionals.

Upper Thomson spans the northern portion of the estate bordering Marymount Road and Lower Peirce Reservoir. This is Bishan’s most park-proximate subzone, with cycling access to the Lower Peirce Reservoir Trail and a quieter, residential character. Older private condominiums in Upper Thomson — a few are freehold — attract long-term owner-occupiers who value the green-belt surroundings. The Thomson–East Coast Line (TEL) Caldecott station, while technically in Toa Payoh, is a short bus ride from Upper Thomson, providing an additional connectivity layer.

Marymount is served by Marymount MRT (CCL) and is characterised by a mix of relatively newer HDB blocks (1990s–2000s build) and private landed properties along Marymount Lane and Marymount Terrace. Proximity to Thomson Medical Centre and the Catholic High campus makes Marymount a particularly attractive subzone for young families and medical professionals.

MRT Connectivity: The Double-Interchange Advantage

Bishan station is one of the most connected interchange stations on the Singapore MRT network. As an NSL–CCL interchange, it provides direct access to the North–South Corridor (Orchard in 15 minutes, City Hall in 21 minutes) and the Circle Line (one-stop to Braddell and Marymount; direct to one-north, Harbourfront, and Dhoby Ghaut via the CCL loop). The addition of Marymount station, a further CCL stop within the estate, means Bishan has effectively three MRT access points — a density matched only by estates like Queenstown and Outram.

For buyers evaluating Bishan against comparable mature estates like Toa Payoh (NSL only) or Serangoon (NEL and CCL, but no NSL), the double-interchange MRT profile is a structural differentiator that justifies the Bishan price premium. Commute times to major employment nodes — Raffles Place (24 min), one-north (25 min via CCL), Marina Bay (28 min) — are competitive with several RCR estates at substantially higher prices.

School Corridor: One of Singapore’s Most Concentrated

Bishan’s school corridor is one of the most concentrated in Singapore. Within the estate or within a 1-kilometre radius of the HDB heartland, buyers can access Catholic High Primary School (PSLE-top-stream feeder to Catholic High Secondary, which offers the Integrated Programme to Raffles Institution); CHIJ Our Lady of the Nativity (Primary); Raffles Institution (Secondary, Bishan campus — one of the two RI campuses); Bishan Park Secondary; and St Joseph’s Institution (SJI), accessible via the CCL from Bishan station in two stops.

For families who run their housing search on school proximity, the 1-kilometre priority registration boundary around Catholic High Primary or Raffles Institution alone can justify a S$50,000–S$100,000 price premium on Bishan flats over equivalent flat types in neighbouring Ang Mo Kio. The Ministry of Education administers school registration via Phase 2A and Phase 2B ballots, and school proximity continues to be a documented driver of HDB resale premiums in established educational corridors.

Summary Table: Bishan Property at a Glance

| Property Type | Price Range (2026) | Median Price | Gross Rental Yield | Notes |

|---|---|---|---|---|

| HDB 3-Room | S$480k – S$640k | S$542k | ~3.8% | Older stock; limited supply in Bishan East |

| HDB 4-Room | S$680k – S$920k | S$800k | ~3.5% | Most actively traded (199 txns Q1 2026); strong upgrader demand |

| HDB 5-Room | S$840k – S$1.1M | S$970k | ~3.2% | Near MRT commands top of range; 10-yr MOP for new BTO Plus flats |

| HDB EA / Multi-Gen | S$1.05M – S$1.39M | S$1.27M | ~2.8% | Million-dollar category; limited supply; high demand from multi-gen families |

| Private Condo (D20) | S$1.35M – S$2.2M | ~S$1.75M | ~2.9–3.4% | Freehold premium at Upper Thomson; 99-yr at Bishan East; supply-constrained |

Rental Market and Investment Yield

Bishan’s rental market is smaller and more selective than Sengkang or Woodlands, reflecting the estate’s owner-occupier character. However, demand is consistent from two distinct renter pools: professionals and expat families drawn by the school corridor (who are often willing to pay a premium for proximity to Raffles Institution and Catholic High), and working professionals who prioritise the MRT interchange commute access.

Three-room flats achieve S$2,800–S$3,200 per month; four-room S$3,200–S$3,800; five-room S$3,800–S$4,500. Private condominiums achieve S$3,800–S$5,200 for one-bedroom units and S$5,000–S$7,200 for two-bedroom units. Gross yields, at 2.9–3.8%, are below OCR averages — but this reflects the capitally appreciated base price, not weak rental demand. The trade-off is capital appreciation: Bishan private condos have delivered approximately 12.5% three-year capital growth, meaningfully above the OCR average of 9.5–10%.

Worked Example: Mr & Mrs Ng — SC Couple Buying First Private Property in Bishan (D20)

Mr and Mrs Ng are Singapore Citizens. They have sold their Bishan HDB flat (MOP cleared) at S$870,000, netting approximately S$620,000 after repaying HDB loan and CPF accrued interest. They plan to purchase a 2-bedroom 99-year leasehold condo in Bishan East at S$1.48M.

BSD on S$1.48M: First S$180,000 × 1% = S$1,800 | Next S$180,000 × 2% = S$3,600 | Next S$640,000 × 3% = S$19,200 | Remaining S$480,000 × 4% = S$19,200 | Total BSD = S$43,800

ABSD: Nil — SC couple purchasing their first private property; no ABSD applies to Singapore Citizens on their first residential property purchase under the Stamp Duties Act (Cap. 312).

Bank Loan (75% LTV): S$1,110,000 at 1.80% fixed (2-year) → estimated monthly instalment S$4,603. Total Debt Servicing Ratio (TDSR): assuming household income S$14,000/month → TDSR = 32.9% (within the 55% cap, but approaching the prudent 40% threshold).

Cash outlay: 5% cash down S$74,000 + BSD S$43,800 + legal/conveyancing S$5,500 = approximately S$123,300 cash. Remaining 20% down (S$296,000) via CPF OA from sale proceeds.

Capital growth scenario: At a conservative 8% three-year growth rate (below Bishan’s 2023–2026 actual of 12.5%), the property would be worth approximately S$1.6M by 2029, a paper gain of S$120,000. Gross yield at S$6,200/month rent (market rate) = 5.02% on current price — though net yield after BSD amortisation, maintenance, and tax would be approximately 3.2%.

Why Bishan Commands a Premium: The Scarcity Equation

Bishan’s premium over comparable OCR markets is not simply a function of present amenities — it is a function of structural supply scarcity compounded by high-quality demand anchors. Unlike Tengah, Punggol North, or Woodlands Regional Centre, where URA’s Master Plan has allocated substantial new land for development, Bishan has effectively no large vacant parcels. The estate’s GLS pipeline for private residential under the 1H 2026 Confirmed List does not include any Bishan sites — nor has any Bishan private residential site appeared on the reserve list since 2022.

This supply constraint, when combined with consistently high demand from school-corridor buyers, MRT-interchange seekers, and portfolio investors who appreciate the defensive characteristics of the estate, creates a price floor that has proven resilient across multiple cooling-measure cycles. Bishan HDB resale prices fell by less than 3% during the 2023 policy tightening (15-month wait-out period for private downgraders), compared with declines of 5–8% in Tampines and Pasir Ris.

For investors, the implication is clear: Bishan is not a high-yield market, but it is arguably the most capital-efficient defensive hold in Singapore’s public-housing sector. The combination of school corridor premium, MRT interchange access, park proximity, and supply scarcity makes Bishan uniquely resistant to the demand shocks that afflict more peripheral estates.

What Might Come Next: Bishan in 2027–2030

This section is forward-looking speculation and should not be taken as a guarantee of future performance.

The June 2026 BTO exercise will add new Bishan flats, likely classified as Plus under HDB’s Standard–Plus–Prime framework given the estate’s mature status and proximity to Bishan MRT interchange. Plus classification implies a 10-year MOP and a subsidy clawback on resale for the first eligible buyer — provisions that will suppress the resale supply of these new flats until approximately 2036. In the near term (2026–2031), this means resale supply remains tight, supporting existing Bishan HDB resale prices.

The Thomson–East Coast Line (TEL) is already operational at Caldecott (one stop north of Bishan on the CCL), connecting Bishan to the Orchard–Marina Bay–East Coast corridor without transfers. As TEL’s full extension to Changi Airport East completes by 2027, the indirect accessibility uplift for Bishan buyers will be material — TEL has already catalysed price premiums at stations along the Caldecott–Napier corridor.

On the private market, any new GLS announcement for Bishan — however unlikely — would create a supply shock. The more probable scenario is continued price appreciation of 5–9% over 2026–2028 driven by scarcity and school corridor demand, potentially pushing the median Bishan private condo above S$2,000 psf by 2028.

Is Bishan a good place to buy property in Singapore?

Bishan is one of Singapore’s strongest all-round property estates. It offers premium school corridor access (Raffles Institution, Catholic High), exceptional MRT connectivity (NSL–CCL double interchange), park-proximate living (Bishan–AMK Park), and supply scarcity that underpins long-term price stability. The primary trade-off is price: HDB 4-room flats median at S$800,000 and private condos well above S$1.35M, making Bishan one of the most expensive HDB estates in Singapore. For buyers who can afford entry, the defensive capital appreciation characteristics are arguably unmatched outside the CCR.

What are HDB resale prices in Bishan in 2026?

Based on HDB Resale Portal caveats through April 2026, Bishan HDB resale prices are approximately: 3-room S$480,000–S$640,000 (median S$542,000); 4-room S$680,000–S$920,000 (median S$800,000); 5-room S$840,000–S$1.1M (median S$970,000); EA/Multi-Gen S$1.05M–S$1.39M (median S$1.27M). The overall estate median across all flat types is approximately S$850,000 — placing Bishan among the top five most expensive HDB estates in Singapore alongside Queenstown, Toa Payoh, Clementi, and Buona Vista.

How does Bishan compare to Ang Mo Kio and Toa Payoh for property investment?

All three are mature, centrally located NSL estates with strong amenity profiles. Bishan commands the highest prices due to its CCL interchange and superior school corridor. Ang Mo Kio (median 4-room ~S$650k) offers better affordability with strong amenities and CRL Phase 2 upside (~2031); Toa Payoh (median 4-room ~S$720k) has the added advantage of TEL Caldecott access and proximity to the city fringe. For yield-focused investors, Ang Mo Kio typically offers slightly better gross yields (3.8–4.2% for 4-room) than Bishan (3.5%); for capital appreciation and defensive holding, Bishan’s supply scarcity and demand anchors make it the preferred choice.

Which schools are near Bishan HDB flats?

Within or immediately adjacent to Bishan estate: Catholic High Primary School (Phase 2A feeder to Catholic High Secondary and Raffles Institution IP); CHIJ Our Lady of the Nativity (Primary); Raffles Institution (Secondary, Bishan campus — IP programme, no O-Level); Bishan Park Secondary School. Within a 2-kilometre radius: Marymount Convent School, St Gabriel’s Primary and Secondary, Peirce Secondary. At the junior college level, Raffles Institution’s Year 5–6 (JC equivalent) is on the same campus. Families prioritising Catholic High Primary should note that Priority Phase 2A admission is conditional on a sibling or parent who is an alumnus or active church member of the affiliated parishes.

Will the June 2026 BTO flats in Bishan be classified as Plus or Prime?

HDB has not yet published the June 2026 BTO flat type classifications at the time of this article’s publication (May 2026). However, based on URA’s Master Plan zoning and HDB’s stated criteria — which factor in MRT proximity, amenity density, and mature estate status — Bishan flats near Bishan MRT interchange are likely candidates for Plus classification (10-year MOP, subsidy clawback on resale to eligible buyers) rather than Standard (5-year MOP). Buyers should check HDB’s official BTO portal (homes.hdb.gov.sg) once the exercise launches for confirmed classification. A Plus classification does not affect the flat’s capital appreciation potential but does restrict near-term resale flexibility.

Can foreigners or PRs buy HDB flats in Bishan?

Permanent Residents (PRs) may purchase HDB resale flats in Bishan subject to the standard eligibility conditions: a minimum 3-year PR status, formation of a family nucleus with at least one Singapore Citizen or another PR, and no concurrent ownership of private property. PRs are not eligible to purchase new BTO flats. Foreigners (non-PRs) cannot purchase HDB flats under the Housing and Development Act. Foreigners may purchase private condominiums in Bishan (District 20) subject to 65% ABSD administered by IRAS. There are no additional restrictions specific to Bishan beyond the standard national eligibility framework.

What is Bishan-AMK Park and how does it affect property values?

Bishan–Ang Mo Kio Park is a 62-hectare urban park jointly developed by NParks and the Public Utilities Board (PUB) as part of the Active, Beautiful, Clean Waters (ABC Waters) programme. The park features a naturalised river channel, extensive green space, wetland habitats, and recreational facilities including a swimming complex and multiple playgrounds. Research by academics at the National University of Singapore has documented a statistically significant price premium of 3–6% for HDB flats within 500 metres of Bishan–AMK Park, relative to equivalent flats further from the park boundary. This proximity premium is one of several quantifiable amenity factors that support Bishan’s above-market HDB resale valuations.

0 Comments