Singapore’s ageing population has turned HDB equity into a retirement-planning question. Two schemes let seniors tap that equity, and they work in almost opposite ways. The right choice depends less on the numbers and more on whether you are ready to move.

Lease Buyback Scheme (LBS)

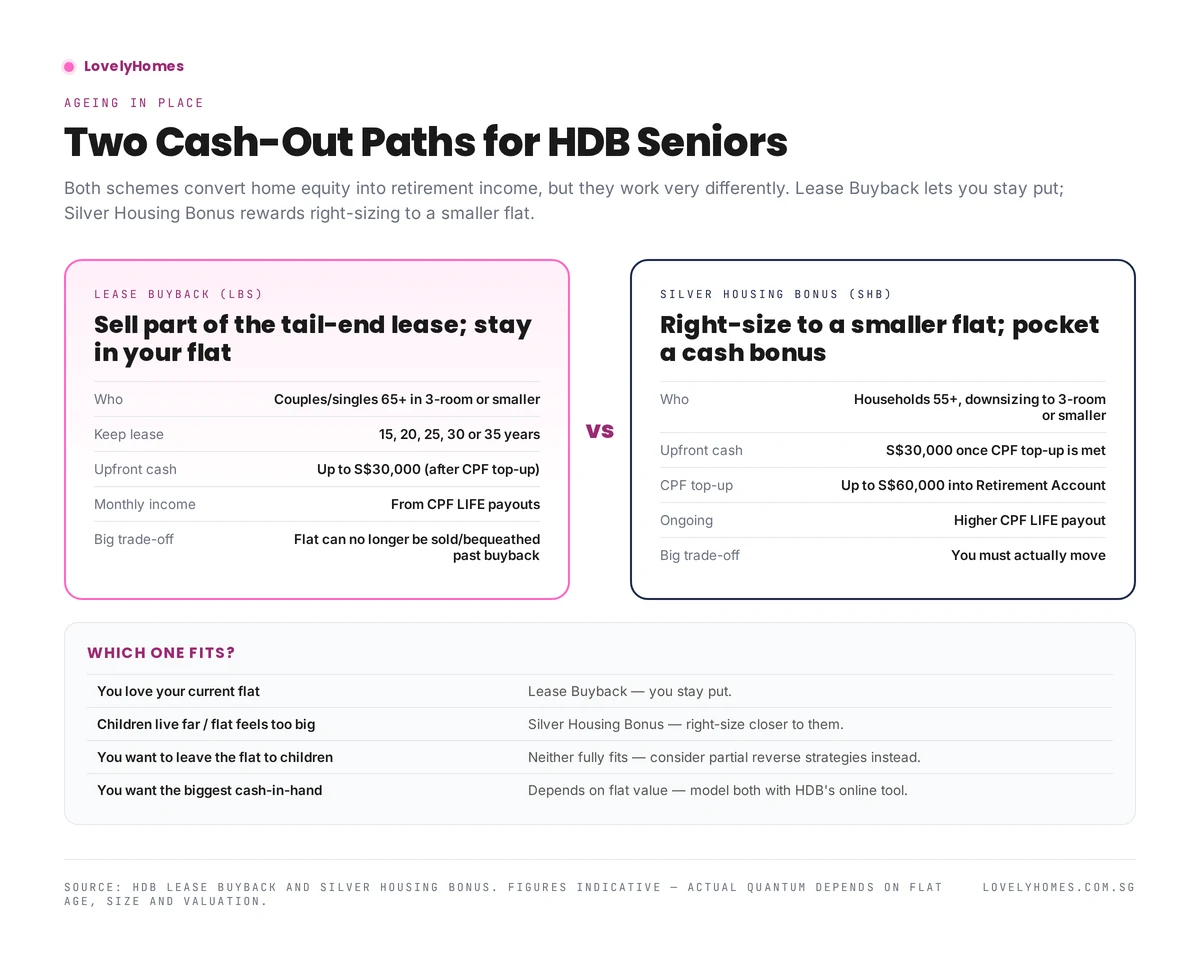

Lease Buyback lets a household aged 65+ in a 3-room or smaller HDB flat sell the tail end of their 99-year lease to HDB, keeping a shorter lease (15, 20, 25, 30 or 35 years depending on age and need). The sale proceeds are used to top up your CPF Retirement Account; the first portion of that top-up goes into CPF LIFE to generate monthly lifetime payouts, and any excess over statutory caps comes back as cash — up to S$30,000 on the standard scheme.

You keep living in the same flat. The downside: once the shorter lease you retain runs out, the flat returns to HDB. You cannot sell the flat on the open market after the buyback. Bequeathing the flat to children is effectively off the table.

Silver Housing Bonus (SHB)

SHB rewards households aged 55+ for right-sizing to a smaller flat (3-room or smaller for SHB purposes). You sell your existing flat on the open market, buy the smaller one, and top up your CPF Retirement Account with a portion of the sale proceeds. HDB then pays a S$30,000 cash bonus once the top-up target (up to S$60,000 into CPF RA) is met.

You must actually move — this is the whole point. The new smaller flat does not need to be in the same estate; many seniors use the chance to move closer to adult children or to ground-floor units.

Side-by-side comparison

| Aspect | Lease Buyback (LBS) | Silver Housing Bonus (SHB) |

|---|---|---|

| Age threshold | 65+ | 55+ |

| Must move? | No — you stay | Yes — right-size to 3-room or smaller |

| Upfront cash | Up to S$30,000 (after CPF top-up) | S$30,000 (after CPF top-up) |

| CPF top-up | Funded by lease sale proceeds | Up to S$60,000 into CPF RA |

| Monthly income | CPF LIFE payouts from RA | Higher CPF LIFE payouts from top-up |

| Flat bequest | Not really — flat returns to HDB at end of shorter lease | You still own the (smaller) flat |

| MOP on new flat | N/A | 5 years |

A when-to-pick framework

| Situation | Scheme that usually fits |

|---|---|

| “This flat is home, we’re not moving.” | Lease Buyback |

| “The 4-room is too big, kids have moved out.” | Silver Housing Bonus |

| “We want to leave the flat to our children.” | Neither — consider partial-equity or rent-out-a-room strategies |

| “We want the biggest CPF LIFE stream possible.” | SHB (higher top-up ceiling) |

| “We’re in a 4-room and want to stay.” | LBS not available (3-room or smaller only); consider renting out rooms or a 2-room Flexi purchase |

Worked example — 3-room flat in Ang Mo Kio

Mr and Mrs Chong are 70, in a 3-room HDB with 50 years of lease left. Flat valuation is roughly S$500,000. Under LBS, selling 30 of the remaining 50 years to HDB might net ~S$150,000, of which most tops up their Retirement Accounts to the Basic Retirement Sum and the residual ~S$30,000 comes as cash. They keep a 20-year retained lease — long enough for most seniors’ horizon — and stay in the same flat.

Under SHB, they sell the 3-room, buy a 2-room Flexi on a shorter new lease in the same estate for ~S$250,000, top up their CPF RAs by up to S$60,000, and receive S$30,000 in cash. They now own a smaller flat outright, with no mortgage, and have a higher CPF LIFE payout.

Frequently asked questions

Can I do both?

Not at the same time on the same flat. Seniors sometimes SHB into a smaller flat, then LBS again later in life.

Is CPF LIFE automatic after the top-up?

If you are already on CPF LIFE, the top-up simply raises your payouts. If you are not yet on a plan, the top-up is held in your RA and annuitised when you join CPF LIFE.

Are the cash amounts taxable?

No. The S$30,000 bonuses and the retained cash from LBS are not taxable.

Can I rent out rooms under LBS?

Yes, subject to standard HDB room-rental rules — one of the common ways LBS seniors supplement income without moving.

Related guides

- MOP rules — including rules on renting out rooms vs the whole flat.

- How to sell an HDB flat.

- Category: Home Ownership & Living.

This guide is for general information only and is accurate as of April 2026. CPF grants, scheme quantum and eligibility rules are set by HDB / the Ministry of National Development and can change. Always confirm current rules on the HDB Flat Portal or with an HDB officer before committing. We are not a financial or legal advisor.

0 Comments