When you buy a condo or strata-titled property, you own your unit plus a proportionate share of the common property (pools, corridors, lifts, roofs).

The Management Corporation (MCST) is the statutory body comprising all unit owners. It is responsible for maintaining common property.

Maintenance fees are split between the Management Fund (day-to-day running costs) and the Sinking Fund (long-term capital works). The sinking fund must receive at least 10% of total levies.

Your share value (SV) determines how much you pay and how many votes you hold at general meetings.

The Annual General Meeting (AGM) must be held within 15 months of the previous one. Owners can vote on budgets, elect council members, and pass resolutions.

Disputes go to the Strata Titles Board (STB), a quasi-judicial tribunal under the Building and Construction Authority (BCA).

What Is Strata Title?

In Singapore, most private residential properties sold in multi-unit developments — condominiums, apartments, cluster housing, and some mixed-use commercial buildings — are sold under strata title. Strata title is a form of property ownership that allows a developer to subdivide a building into individual lots (units) and a common property lot, with each unit owner holding title to their own lot while all owners collectively share ownership of the common property.

The legal framework governing strata title in Singapore is the Land Titles (Strata) Act (LTSA) and, for the management obligations, the Building Maintenance and Strata Management Act (BMSMA) administered by the Building and Construction Authority (BCA). Together these two statutes define what you own, how common property is managed, what fees you must pay, and how disputes are resolved.

Understanding strata title matters practically because it determines your rights and obligations from the day you collect keys. Maintenance fees are a legal obligation — not a voluntary contribution. By-laws govern what you can and cannot do within your unit and the common areas. The financial health of the MCST directly affects the value of your property.

The MCST — What It Is and How It Works

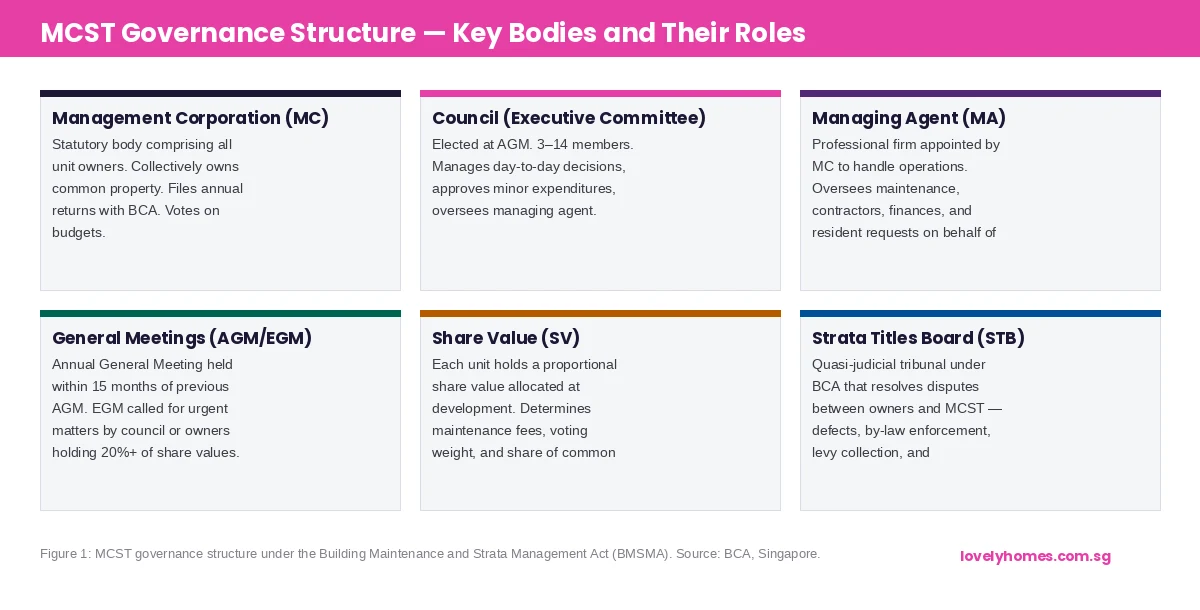

Figure 1: MCST governance structure under the Building Maintenance and Strata Management Act (BMSMA). Source: BCA.

The Management Corporation Strata Title (MCST) comes into legal existence automatically when the first unit in a strata development is sold. Every unit owner is automatically a member of the MCST — there is no opt-out. The MCST number (e.g. MCST 1234) is printed on the strata certificate of title and is registered with the Singapore Land Authority (SLA).

The MCST has a council — sometimes called the executive committee — of 3 to 14 elected members who are responsible for day-to-day management between general meetings. Council members are volunteers elected by other owners at the AGM. For large developments (above 100 units), managing the MCST professionally is a significant undertaking, which is why most developments appoint a managing agent (MA) — a licensed professional firm (regulated by BCA under the BMSMA) — to handle operations.

The managing agent is an agent of the MCST, not an independent principal. Their scope of authority is defined in the MA agreement and must be approved by the council. A managing agent can be replaced at the AGM by an ordinary resolution. Disputes about managing agent performance are common triggers for EGMs (Extraordinary General Meetings).

Management Fund vs Sinking Fund

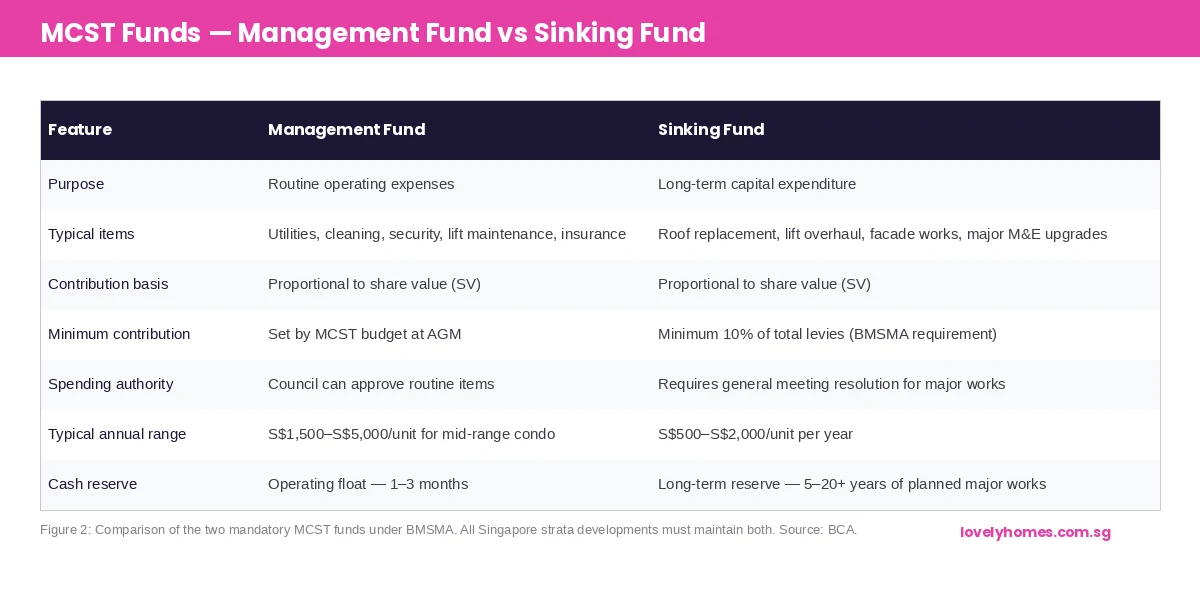

Figure 2: The two mandatory MCST funds — management fund for operations, sinking fund for capital works. Source: BCA, BMSMA.

The BMSMA requires every MCST to maintain two separate funds. Understanding their purpose helps you evaluate the financial health of a development before you buy, and interpret the financial statements tabled at each AGM.

The Management Fund covers the day-to-day running costs of the development: electricity and water for common areas, cleaning contracts, security personnel, lift maintenance contracts, swimming pool chemicals and attendants, building insurance, and the managing agent’s fees. It operates like an operating budget. The council proposes the annual budget, and owners vote on it at the AGM. Contributions are collected monthly or quarterly as maintenance levies.

The Sinking Fund is reserved for major cyclical expenditure: repainting the facade, replacing lifts (typically required every 25 years), reroofing, upgrading fire-suppression systems, and replacing aged mechanical-electrical (M&E) equipment. By law, the sinking fund must receive a minimum of 10% of the total levies collected. A healthy sinking fund is one of the strongest indicators of a well-managed development — a depleted sinking fund often signals years of underfunding, leading to either special levies or deferred maintenance that depresses property values.

When evaluating a resale condo for purchase, always request the MCST’s most recent annual financial statements (obtainable from the managing agent or the outgoing owner) and check the sinking fund balance per unit relative to the age and planned major works cycle of the development.

Maintenance Levies — How Much and How Calculated

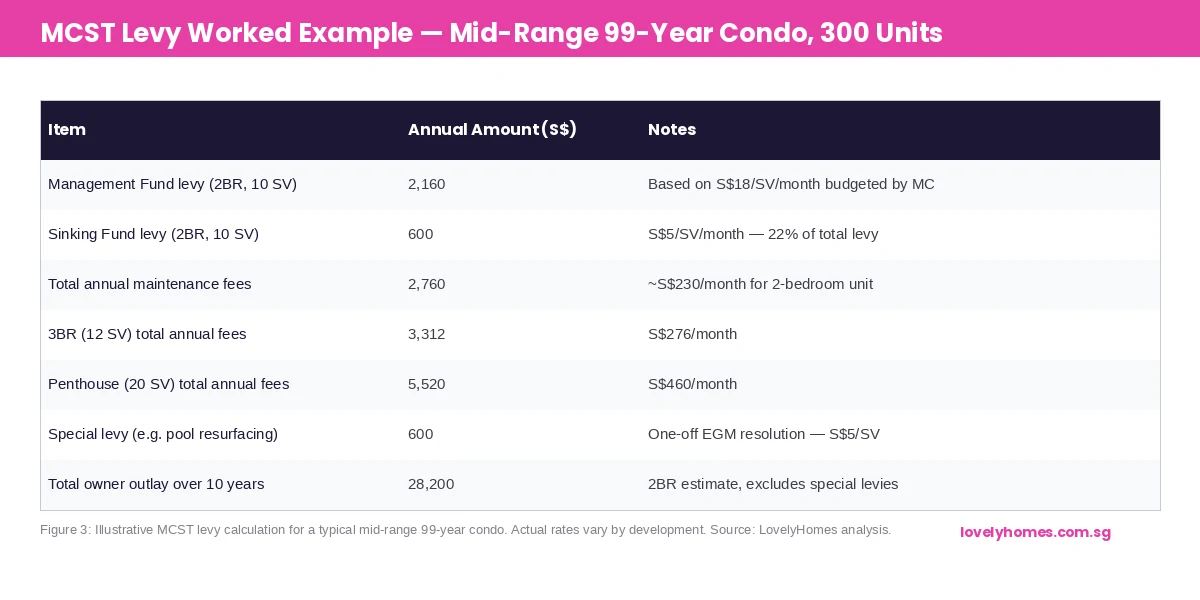

Figure 3: Illustrative MCST levy for a 300-unit mid-range 99-year leasehold condo. Actual rates vary by development size and facilities. Source: LovelyHomes analysis.

Maintenance levies are calculated based on your unit’s share value (SV). Share values are fixed at the time the strata development is registered with SLA and are proportional to the floor area of each unit (with some adjustments for exclusive use areas, car parks, and other factors). A 2-bedroom unit typically carries 10 share values; a 3-bedroom 12; a penthouse 20 or more.

The formula is simple: Monthly levy = SV × (Rate per SV per month approved at AGM). In a mid-range 300-unit development in 2026, a management fund rate of S$18 per SV per month and a sinking fund rate of S$5 per SV per month is typical. For a 2-bedroom with 10 SV, that is S$230 per month or S$2,760 per year.

For luxury condos with extensive facilities (full-size Olympic pool, tennis courts, concierge, gym, multiple function rooms), rates of S$50–S$80 per SV per month are common, translating to S$6,000–S$12,000 per year for a mid-sized unit. Before buying, always verify the current maintenance fee from the MCST financial statements — the amount stated in the OTP or by the agent may be out of date if the AGM has recently approved a rate increase.

Development Type

Indicative Monthly Fee Range

Key Cost Driver

Mass-market condo (no full facilities)

S$150–S$250/month

Lower facilities overhead

Mid-range condo (pool, gym, BBQ)

S$200–S$400/month

Typical 2BR in 300-unit development

Luxury condo (full concierge, courts)

S$500–S$1,200/month

Staffing and high-spec M&E

Older development (>25 years)

Higher sinking fund component

Lift, roof and M&E replacement cycle

Small boutique development (<50 units)

Higher per-unit cost

Fixed overhead spread over fewer owners

By-Laws — What You Can and Cannot Do

Every MCST operates under two layers of by-laws: the default by-laws prescribed in the Second Schedule to the BMSMA, which apply to all strata developments unless expressly amended, and any additional by-laws passed by the MCST at a general meeting by special resolution (75% of votes by share value).

The default by-laws cover a wide range of matters that affect daily condo living, including:

Noise and nuisance. The by-laws prohibit activities that cause unreasonable noise or nuisance to other residents, particularly between 10:30pm and 7:00am. This includes power tools, loud music, and guests in common areas.

Alterations and renovations. Any renovation works that affect common property or structural elements require written approval from the MCST before commencement. This includes hacking or coring through floor slabs, installation of air-conditioner ledges, and changes to external facades. Works that do not affect common property (internal non-structural reconfigurations) require only compliance with URA/BCA requirements and notification to the MCST — not approval. See our Renovation Loan guide for the financing angle.

Pets. The default by-laws do not prohibit pets, but many MCSTs pass specific by-laws restricting pets to dogs under 10kg or prohibiting them altogether in common lifts or areas. Check the development’s specific by-laws before buying if pet ownership is important to you.

Parking. Car park lots in most condos are either strata-titled (you own the lot) or allocated by the MCST. The MCST sets the rules for allocation, usage, and visitor parking. Unauthorised parking in common lots may result in vehicles being towed at the owner’s expense.

Your Rights as an Owner — General Meetings and Voting

As a unit owner, you are automatically a member of the MCST with enforceable rights. The most important of these is your right to attend and vote at general meetings. Votes are weighted by share value — the more SV you hold, the more voting power you have. However, for most ordinary resolutions, a simple majority by share value suffices, and the practical reality is that small-unit owners collectively hold the majority of share values in most developments.

Key resolutions and their required majority:

Ordinary resolution (simple majority by SV): annual budget approval, election of council, appointment of managing agent, minor by-law amendments.

90% resolution: improvements or alterations to common property that disproportionately benefit some owners over others.

Special resolution (75% by SV with 14 days’ notice): new or amended by-laws, significant improvements to common property, major expenditure from sinking fund.

Unanimous resolution: changes that affect only certain strata lots, or that extinguish exclusive use rights.

If you believe the council has acted improperly or the MCST is not fulfilling its statutory obligations, you can requisition an EGM (with 20% of SV supporting the requisition), file a complaint with BCA, or bring a dispute to the Strata Titles Board.

Strata Titles Board — Dispute Resolution

The Strata Titles Board (STB) is a quasi-judicial tribunal established under the LTSA. It has jurisdiction over disputes between unit owners and MCSTs in three main areas:

Management disputes. Failure by the MCST to carry out its maintenance obligations, disputes over levy computation or enforcement, unauthorised alterations to common property, and by-law enforcement disputes.

Financial disputes. Recovery of unpaid levies by the MCST against defaulting owners, disputes over the validity of resolutions passed at general meetings, and challenges to special levies.

Collective sale (en-bloc). When an en-bloc sale reaches 80% owner consent by share value and floor area, the sale committee applies to the STB for an order to sell. The STB hears objections from dissenting owners and decides whether the collective sale is just and equitable. See our En-Bloc Collective Sale guide for the full process.

STB proceedings are less formal than court but legally binding. For monetary disputes, the STB can award damages and costs. For en-bloc applications, the STB’s order is final subject only to High Court appeal on points of law.

What to Check Before Buying a Strata-Titled Property

Savvy buyers treat MCST financial health as a material factor in pricing a strata purchase. Key due-diligence checks:

1. Request the MCST financial statements for the last 2–3 years. Look at the sinking fund balance per unit against the age of the development and scheduled major works. A 15-year-old condo with a sinking fund of only S$500,000 for 200 units (S$2,500 per unit) is likely underfunded for an imminent lift replacement costing S$3–5M.

2. Check for pending special levies or litigation. Ask the managing agent directly whether there are any planned or approved special levies for major works, or any STB proceedings pending. These will become your obligation after purchase.

3. Review the by-laws for specific restrictions. Pet policies, AirBnB/short-term rental prohibitions, parking allocation rules, and guest policies vary significantly between developments.

4. Note the MCSTs arrear rate. A high arrears rate on maintenance levies signals owner financial stress or poor management — both are red flags for collective governance.

What Might Come Next

BCA is actively reviewing the BMSMA framework in 2026, with a public consultation on several proposed amendments including mandatory mediation before STB proceedings, enhanced disclosure requirements for MCSTs on major works timelines, and possible standardisation of sinking fund contribution rates linked to development age rather than purely to AGM approval. These reforms, if enacted, would increase transparency for buyers and reduce the risk of discovering an underfunded sinking fund post-purchase. Buyers of resale condos in particular stand to benefit from enhanced mandatory disclosure.

FAQ 1: Can the MCST prevent me from renting out my unit on Airbnb or short-term lets?

Yes. Under the BMSMA, an MCST can pass a by-law (by special resolution — 75% of share values) prohibiting short-term rentals of fewer than a specified minimum period. Many condos have enacted such by-laws following the Urban Redevelopment Authority’s position that residential units must not be used for short-term accommodation of fewer than 3 consecutive months without URA approval. Even if your MCST has not passed a specific by-law, short-term rentals below 3 months in a private residential property require URA planning approval, which is rarely granted. Always check both URA rules and the development’s by-laws before letting on short-term platforms.

FAQ 2: What happens if I don’t pay my maintenance fees?

Non-payment of MCST levies is a serious legal matter. The MCST is entitled to pursue unpaid levies through the courts or STB without notice and can register a charge on your unit title for the amount owed. The charge is enforceable and would have to be discharged before you can sell or mortgage the property. In persistent cases, the MCST may apply to court to have the charge enforced by sale of the unit. Practical consequences include denial of access to clubhouse facilities (permissible under by-laws), legal costs being added to the debt, and — ultimately — STB proceedings.

FAQ 3: Can I vote at the AGM if I have not paid my maintenance fees?

Under the BMSMA, an owner who is in arrears of levies for more than 30 days at the time of the general meeting is not entitled to vote. The right to vote is reinstated once arrears are cleared. The right to attend and speak at the meeting is not affected by arrears status — only the voting right is suspended.

FAQ 4: My condo’s council wants to spend S$2M on a new gymnasium. Can they do this without my approval?

No. Expenditure of that scale from the sinking fund for capital improvements (as opposed to like-for-like replacements) requires a special resolution at a general meeting, which needs 75% of share values voting in favour with 14 days’ notice. The council cannot unilaterally authorise major capital expenditure beyond the limits set in the by-laws and the annual budget. Ordinary council spending limits are typically set at S$500–S$1,000 per occasion without general meeting approval — well below S$2M.

FAQ 5: What is a special levy and is it common?

A special levy is a one-off charge raised by the MCST above and beyond the regular maintenance fee, approved by special resolution at a general meeting. It is used when a major unplanned repair or improvement cannot be funded from the sinking fund alone — for example, emergency waterproofing after a roof failure, or an unplanned full lift replacement. Special levies are common in older developments (25+ years) where the sinking fund was historically underfunded. They are payable within the timeframe stipulated in the resolution and carry the same legal enforcement mechanism as regular levies.

FAQ 6: Can I stand for election to the council?

Yes, any subsidiary proprietor (unit owner) who is at least 21 years of age and is not an undischarged bankrupt may stand for election to the council at the AGM. You do not need any professional qualifications. Council membership is unpaid but carries legal responsibilities — council members must act in good faith and in the interests of the MCST. A council member who acts in their own interest to the detriment of the MCST can be removed by ordinary resolution at a general meeting and may be liable for any losses caused.

FAQ 7: What is the difference between MCST and TOP?

TOP (Temporary Occupation Permit) is the certificate issued by BCA that allows units in a new development to be occupied. It is issued to the developer, not the MCST. The MCST is formed separately — it comes into legal existence when the first unit is sold. In new developments, between TOP issuance and the formation of a functioning elected council (which happens at the inaugural general meeting, typically within one year of TOP), the developer or a developer-appointed managing agent manages the development. New owners in this period should attend the inaugural AGM and review the initial MCST budget and accounts carefully, as the transition from developer management to owner-managed MCST can involve significant financial decisions.

Disclaimer: This article is for general information only and does not constitute legal or financial advice. MCST obligations, by-laws, and the BMSMA framework are subject to change. Always obtain the relevant MCST financial statements and by-laws before any property purchase, and engage a licensed conveyancing lawyer for transaction-specific advice. For official MCST and strata management guidance, visit the BCA Strata Management page.

What is it? An unsecured personal loan offered by licensed financial institutions to finance home renovation works.

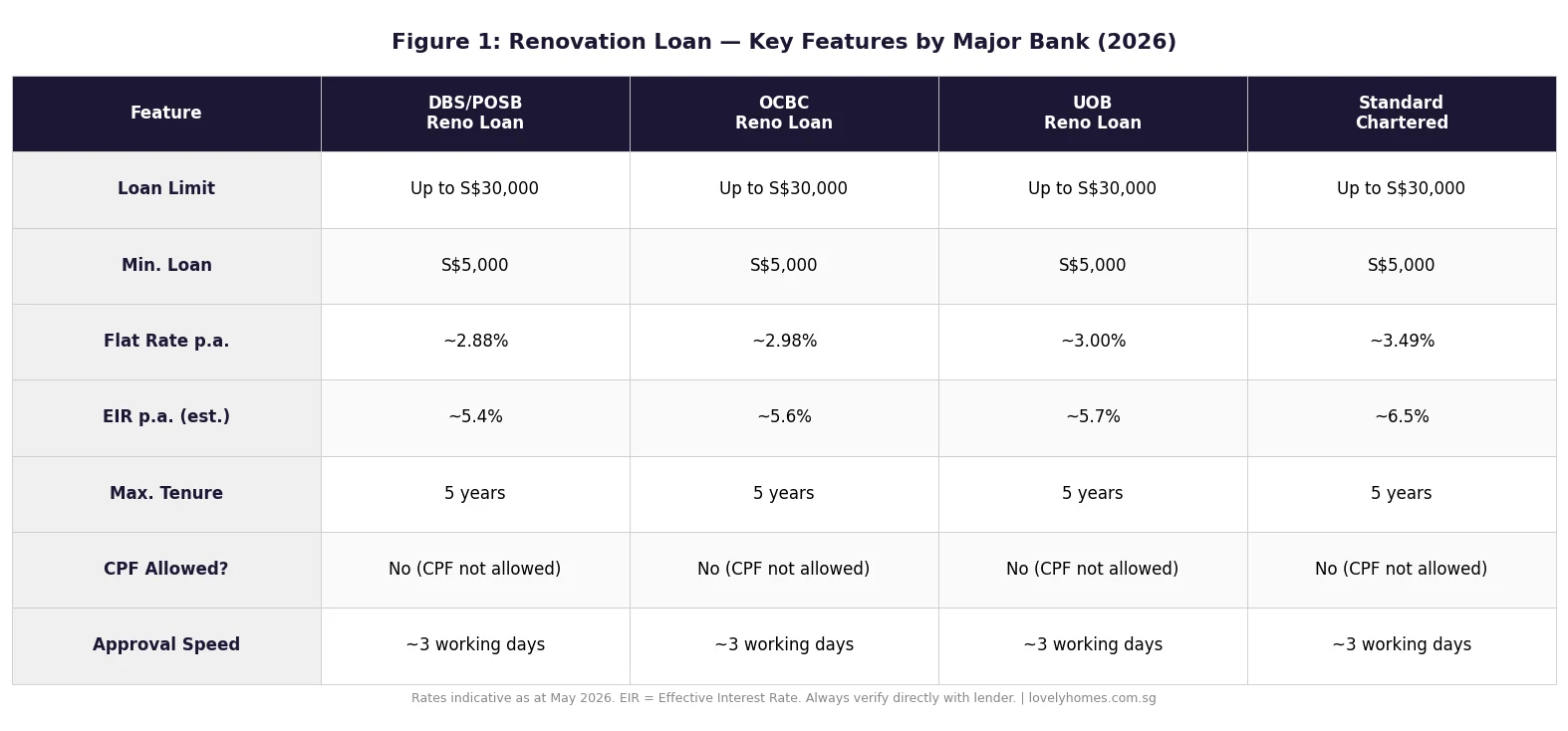

Loan limit: Typically up to S$30,000 or 6× your monthly income, whichever is lower.

Interest rates: Flat rates of approximately 2.88%–3.49% p.a. (Effective Interest Rate 5.4%–6.5% p.a.).

Tenure: Up to 5 years (most banks offer 1–5 years).

CPF not allowed: You cannot use your CPF Ordinary Account for renovation — cash or loan only.

Who qualifies: Singapore Citizens, Permanent Residents, and eligible Employment Pass holders aged 21+.

HDB flats: Structural and civil works require prior approval from HDB before renovation begins.

GST applies: As of 1 January 2024, GST is 9% on all renovation contractor invoices.

What Is a Renovation Loan in Singapore?

A renovation loan is a purpose-bound unsecured loan offered by Monetary Authority of Singapore (MAS)-regulated banks and licensed financial institutions. Unlike a home loan — which is secured against your property — a renovation loan is a personal credit facility ring-fenced for approved home improvement works. It is administered separately from your mortgage and does not require additional collateral.

The objective is straightforward: to help Singaporean homeowners spread the cost of renovating a newly purchased HDB flat, executive condominium, or private property over manageable monthly instalments, rather than drawing down lump-sum savings in one hit.

In 2026, renovation costs in Singapore have continued to climb, driven by higher material costs, post-pandemic labour tightness, and the mandatory 9% GST applied since January 2024. A typical 4-room HDB flat renovation now costs between S$35,000 and S$60,000 for a full-gut-and-rebuild scope, making the renovation loan a meaningful financing tool for most first-time buyers.

Figure 1: Key renovation loan features across major Singapore banks, May 2026. Rates indicative — verify directly with each lender before applying.

Who Administers Renovation Loans?

Renovation loans are offered exclusively by MAS-licensed banks and finance companies. They are not government-subsidised products, unlike the CPF Housing Grant or the HDB Concessionary Loan. The key lenders as at 2026 include DBS/POSB, OCBC, UOB, Standard Chartered, Citibank, and several others. Each sets its own flat rate, effective interest rate, minimum loan amount, and processing fee structure — which is why comparing offers before committing is essential.

The Moneylenders Act (Cap. 188) prohibits licensed moneylenders from marketing loans specifically labelled as “renovation loans” to unsecured personal credit borrowers, though some borrowers do turn to licensed moneylenders for shortfall amounts; rates there are materially higher (up to 4% per month on outstanding balances) and should be approached with extreme caution.

Eligibility: Who Can Apply?

Bank renovation loan eligibility criteria are broadly consistent across lenders, though specific income thresholds vary:

Criterion

Typical Requirement

Notes

Age

Minimum 21 years old

Some banks cap at 65 at loan maturity

Citizenship

SC, PR, or EP/S-Pass holder

Non-residents may face stricter income requirements

Minimum Income

S$24,000–S$30,000 per annum

Loan limit = lower of S$30,000 or 6× monthly income

Credit History

Good CBS credit grade (AA–BB preferred)

Checked via Credit Bureau Singapore at application

Property Ownership

Must be owner/co-owner of property to be renovated

Proof via HDB/URA records or title deed

Renovation Quotes

Contractor invoices or at least 1 quotation required

Loan disbursed to contractor, not directly to borrower

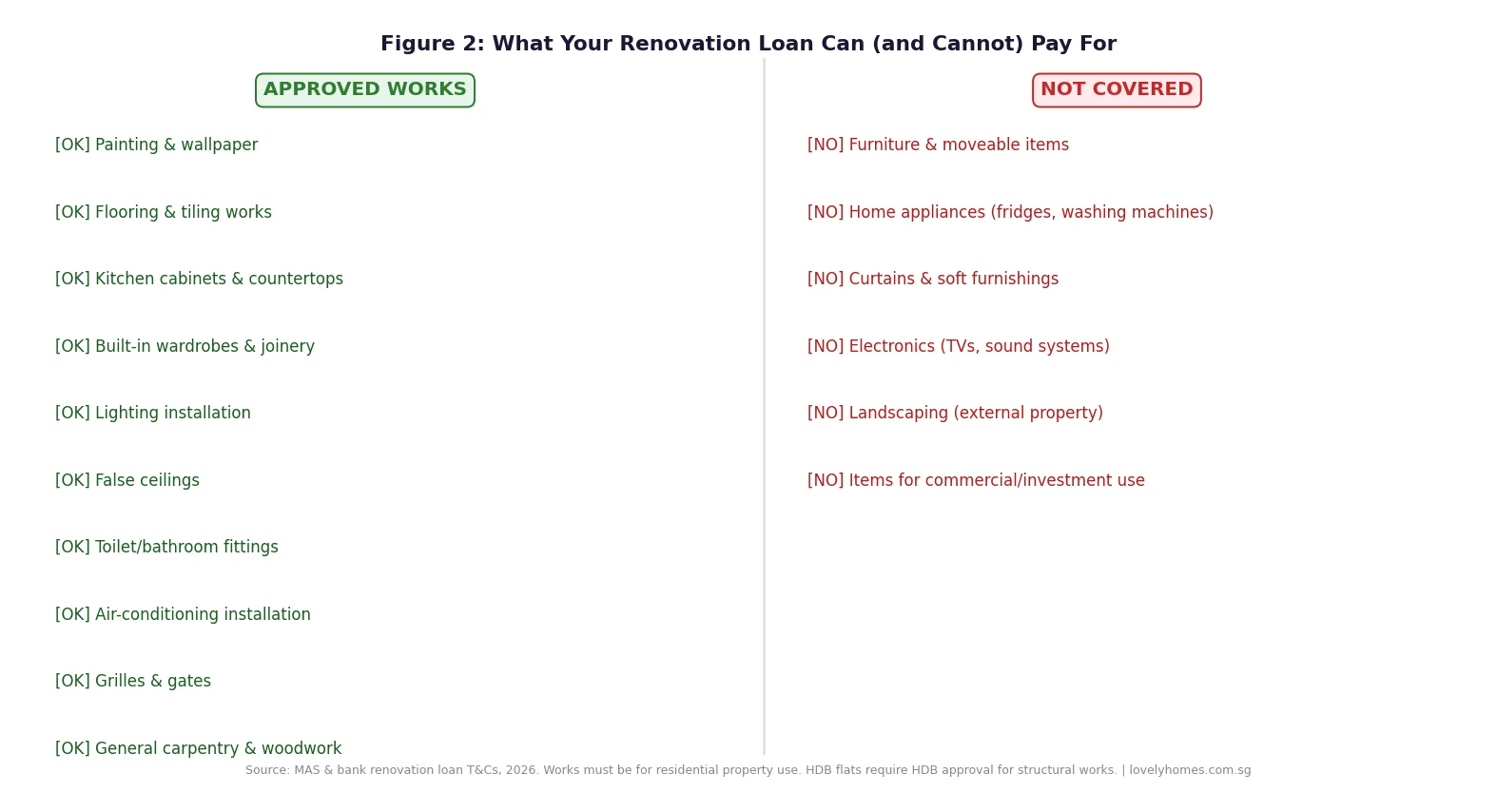

Approved Renovation Works — What the Loan Covers

The defining feature of a renovation loan — as distinct from a general personal loan — is that it can only be used for approved renovation or improvement works. Banks require contractors’ invoices as proof, and funds are typically disbursed directly to the contractor. This protects lenders from the loan being diverted to non-renovation spending.

Figure 2: Works covered and excluded under Singapore bank renovation loans, 2026. Always confirm with your lender before signing the contractor agreement.

For HDB flat owners, an additional layer of approval applies. Under HDB’s Renovation Guidelines, certain works — including demolishing non-structural walls, hacking floor tiles, installing heavy feature walls, and any works affecting the building’s structural integrity — require prior written approval from HDB before work can commence. Failure to obtain this approval can result in a Rectification Order, fines, and in severe cases, compulsory reinstatement at the owner’s cost.

HDB’s e-Service portal allows flat owners to apply for Renovation Permits online; most approvals for standard works are granted within three to five working days. Your bank does not liaise with HDB on your behalf — this is entirely your responsibility as the flat owner.

Interest Rates, Loan Limits and Repayment

Understanding the difference between a flat interest rate and an Effective Interest Rate (EIR) is critical when comparing renovation loans. Banks advertise the flat rate because it sounds lower, but the EIR — which accounts for the reducing loan balance over time — is the true cost of borrowing.

For example, a 2.88% flat rate on a 5-year, S$30,000 loan translates to an EIR of approximately 5.4% per annum. On a monthly repayment basis, that works out to roughly S$565 per month across 60 months, with total interest paid of approximately S$3,900 — a meaningful but manageable premium for spreading renovation costs over five years.

The MAS-mandated borrowing limit cap means that if your gross monthly income is S$4,000, your maximum renovation loan is S$24,000 (6× S$4,000), even if the bank’s product ceiling is S$30,000. This aggregate unsecured credit limit (across all unsecured credit facilities) is capped at 12× monthly income for borrowers with annual income below S$120,000.

Can You Use CPF for Renovation?

No. The CPF Board explicitly prohibits the use of CPF Ordinary Account (OA) savings for home renovation. Your CPF OA may only be used for the purchase of an approved HDB flat, executive condominium, or private residential property, and for the repayment of an approved housing loan. Renovation is not an approved purpose under the CPF Act (Cap. 36).

This means that regardless of how much you have accumulated in your CPF OA, every dollar of your renovation must be funded either from cash savings or a renovation loan. This is a common misconception among first-time buyers who assume that CPF — having covered the down payment — can also cover the renovation tab.

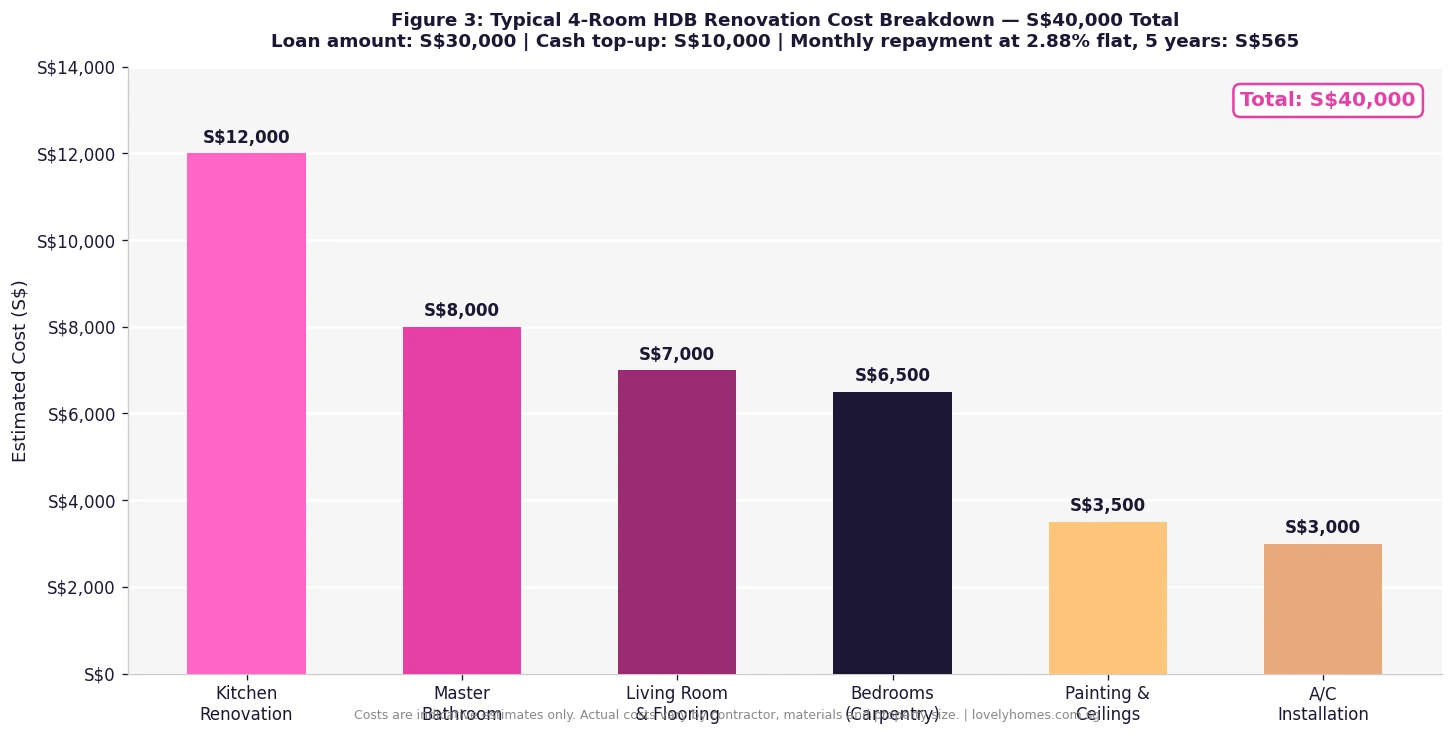

Figure 3: Indicative 4-room HDB renovation cost breakdown, 2026. Total S$40,000: loan covers S$30,000; S$10,000 self-funded. Monthly repayment at 2.88% flat over 5 years: ~S$565.

Worked Example: The Tan Family’s S$40,000 HDB Renovation

Mr and Mrs Tan, both Singapore Citizens aged 32 and 30, have just collected keys to their 4-room BTO flat in Tengah. They received keys in March 2026. Their combined gross monthly income is S$9,500. After accounting for their home loan, their existing monthly financial commitments are modest. They plan a full renovation costing approximately S$40,000.

Step 1 — CPF check: They confirm they cannot use CPF for renovation. Their CPF OA savings remain untouched for future home-loan instalments.

Step 2 — Loan limit: 6 × S$9,500 = S$57,000. The bank product ceiling is S$30,000. Their loan is capped at S$30,000.

Step 3 — Cash shortfall: S$40,000 total cost − S$30,000 loan = S$10,000 cash top-up from savings.

Step 4 — Repayment at 2.88% flat rate, 5-year tenure:

Item

Amount

Loan amount

S$30,000

Monthly repayment (60 months)

~S$565

Total interest paid (5 years)

~S$3,900

Cash top-up (out of pocket)

S$10,000

Total renovation outlay (cash + interest)

S$13,900

The Tans’ TDSR is unaffected in terms of their home loan (renovation loans, being unsecured credit, count towards the MAS aggregate unsecured credit limit rather than the TDSR property-loan computation). Their S$565 monthly renovation repayment does, however, reduce disposable income for the duration of the loan — a practical cash-flow consideration when budgeting for the first five years in their new flat.

What This Means for Singapore Homebuyers in 2026

With renovation costs continuing to rise — industry data points to a 15–20% increase in contractor rates between 2021 and 2026 — the renovation loan has become a near-universal fixture in a first-time buyer’s financial plan. The important discipline is to draw only what is needed: a maxed-out S$30,000 loan taken simply because it is available creates an unnecessary debt burden on top of your mortgage.

Experienced buyers typically adopt a phased renovation strategy: loan the absolute essentials (kitchen, bathrooms, flooring) in Phase 1, then fund discretionary aesthetics (feature walls, bespoke carpentry, statement lighting) from savings in Phase 2, twelve to twenty-four months later when cash flow has normalised.

What Might Come Next

There is no current signal from MAS that renovation loan limits will be increased. Some financial observers have called for the S$30,000 ceiling — last reviewed several years ago — to be revised upward to reflect inflation in renovation costs. Whether MAS acts on this in its next review of unsecured credit guidelines remains to be seen. Separately, should Singapore’s interest rate environment continue to normalise post-2026, bank flat rates on renovation loans may ease modestly, improving affordability.

Frequently Asked Questions

Can I apply for a renovation loan before I collect my flat keys?

Most banks require you to have already collected the keys to your property before disbursing a renovation loan, as they will ask for proof of ownership (e.g., HDB acknowledgement or title deed). Some banks allow you to apply up to three months before key collection, but disbursement is only triggered upon confirmation of ownership. Check with your specific lender on their pre-key-collection policy.

Does a renovation loan affect my home loan TDSR?

Not directly. Renovation loans are classified as unsecured credit under MAS guidelines, not as property loans. They do not form part of the Total Debt Servicing Ratio (TDSR) computation for your home loan. However, they do count toward your aggregate unsecured credit limit (capped at 12× monthly income). If you are applying for a renovation loan shortly after taking a home loan, the bank will assess your credit capacity on a consolidated basis.

What happens if my renovation costs exceed S$30,000?

You will need to fund the excess from personal savings, or consider taking a personal loan (which may carry a higher interest rate than a dedicated renovation loan). Some homeowners choose to phase renovations — borrowing the maximum S$30,000 for the initial works, repaying part of the loan over one to two years, then applying for a top-up or second loan for subsequent phases. It is generally inadvisable to combine renovation loan funds with high-interest credit card debt to bridge a shortfall.

Can I claim renovation costs as a tax deduction?

No, if the property is owner-occupied and not generating rental income. You cannot claim renovation costs against personal income tax for your primary residence. If you are renting out a room or the entire unit, renovation costs may be deductible as allowable expenses against your rental income — but only for the income-producing portion and only for works that are not of a capital improvement nature. Consult IRAS guidelines or a tax adviser for your specific situation.

Do I need HDB approval before I start renovation on my flat?

Yes, for certain categories of work. HDB requires prior written approval for structural changes, hacking of floor tiles, installation of heavy feature walls, and any modifications to the flat’s structural elements. Cosmetic works such as painting, installing blinds, and placing furniture do not require HDB approval. You can apply for an HDB Renovation Permit through the HDB e-Service portal. Works commenced without required approval can result in Rectification Orders and fines.

How long does renovation loan approval take?

Most major banks in Singapore process renovation loan applications within two to five working days. Approval in principle can sometimes be obtained on the same day for existing bank customers with a good credit profile. Full disbursement to your contractor typically follows within three to seven working days of loan approval, depending on the bank’s internal processes and the verification of contractor invoices.

Is there a penalty for early repayment of a renovation loan?

This varies by lender. Some banks impose an early repayment fee of one to two months’ interest if you settle the loan before the agreed tenure ends. Others, especially those competing aggressively for market share, have removed early repayment penalties. Always read the Loan Agreement carefully before signing. If you expect a lump sum (e.g., year-end bonus, CPF refund from property sale) that would let you repay early, factor the penalty into your net savings calculation.

Disclaimer: This article is intended for general informational purposes only and does not constitute financial, legal, or banking advice. Renovation loan rates, limits, and terms are subject to change at any time by individual lenders and are not guaranteed. Readers should verify current product terms directly with their chosen bank and consult a licensed financial adviser for personalised guidance. For official information on CPF usage rules, visit www.cpf.gov.sg. For MAS regulations on unsecured credit, refer to www.mas.gov.sg. For HDB Renovation Permits, visit www.hdb.gov.sg.

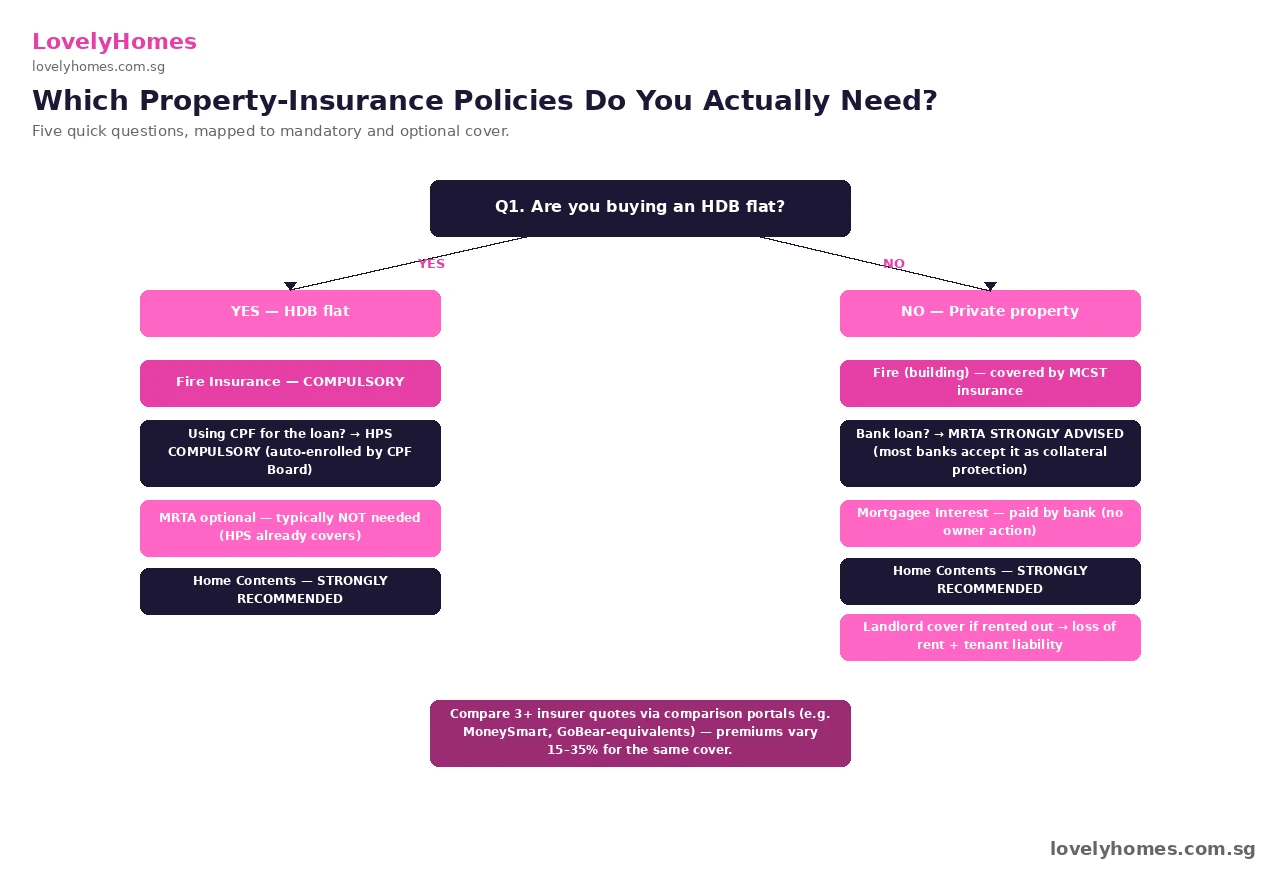

Property insurance in Singapore is one of those topics most homeowners discover only when something goes wrong — a kitchen fire, a burst pipe, a borrower’s sudden death. By then it is too late to negotiate a better policy. This 2026 guide walks you through every layer of cover a Singapore property owner can buy: HDB Fire Insurance, the Home Protection Scheme (HPS), private Mortgage Reducing Term Assurance (MRTA), Home Contents Insurance, and the building cover that sits inside your condo’s management corporation budget. Premiums, what each policy actually pays for, common gaps, and the cheapest legitimate way to cover yourself in 2026 — it is all here.

Quick Answer — what every Singapore homeowner should hold

HDB owners: Fire Insurance is compulsory. If you use CPF Ordinary Account to service your HDB loan, the Home Protection Scheme (HPS) is also auto-enrolled.

Condo owners: Building cover is paid through your monthly maintenance fees (MCST policy). You still need Home Contents and a private MRTA if you have a bank loan.

MRTA protects your family from a forced sale by repaying the outstanding mortgage on death, terminal illness, or total & permanent disability.

Home Contents covers furniture, electronics, jewellery, and personal liability — items the building policy excludes.

Indicative annual outlay for a S$1.5M condo with a S$1.05M loan: ~S$1,000–1,200 across MRTA + Contents + topped-up Fire cover.

Premiums vary 15–35% between insurers for identical cover — always compare 3+ quotes.

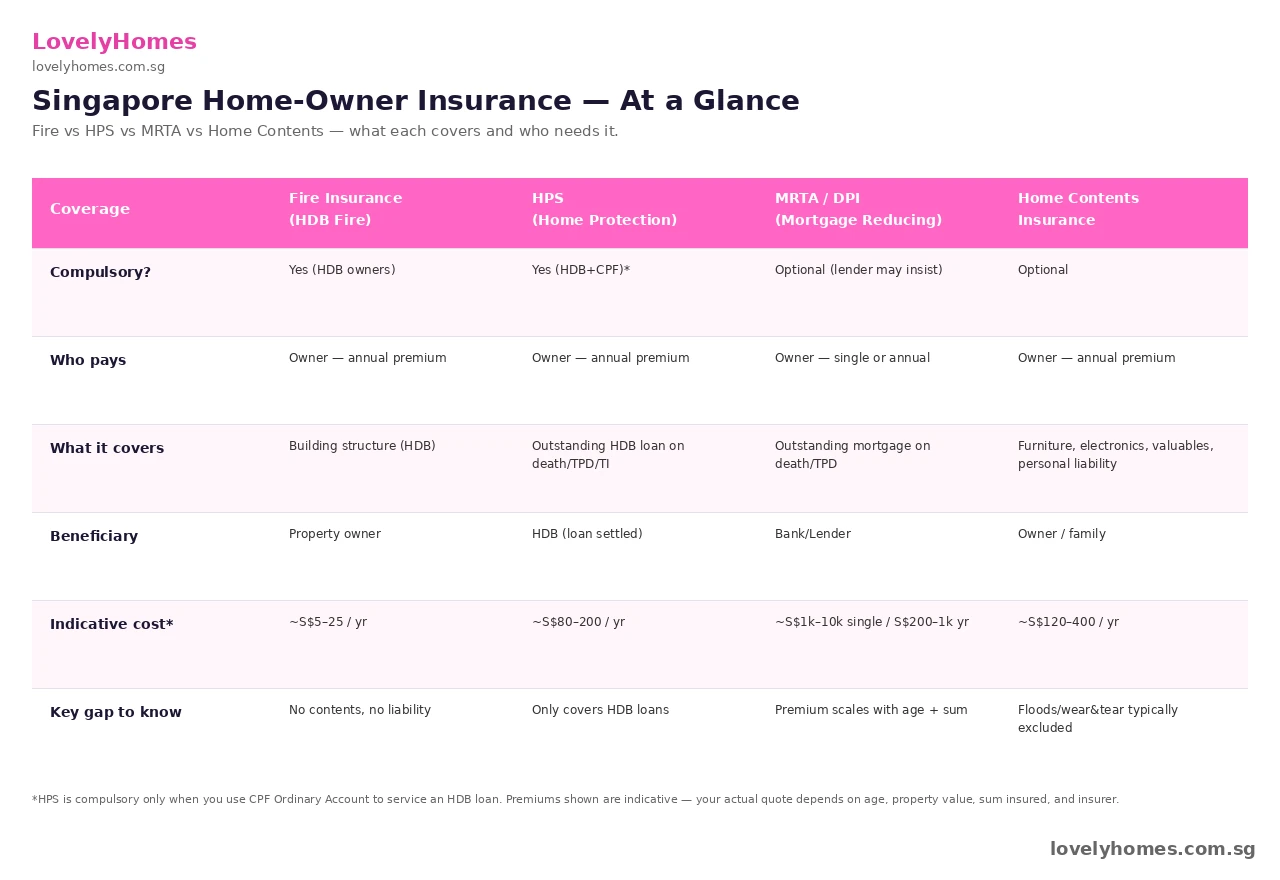

What “Property Insurance” Actually Means in Singapore

The phrase “property insurance” covers four distinct policies in the Singapore context, and the rules around each one differ by housing type. Understanding which is mandatory, which your bank insists on, and which you can safely skip is the difference between an over-insured budget and a real protection plan.

The four pillars are:

Fire Insurance — covers the building structure (walls, floors, ceilings, fixed fittings). Compulsory for HDB flat owners; built into the maintenance fees of every condominium via the Management Corporation Strata Title (MCST).

Home Protection Scheme (HPS) — a CPF-administered group term assurance that pays off your outstanding HDB loan if you die, become totally and permanently disabled, or are diagnosed with a terminal illness. Compulsory for HDB owners using CPF Ordinary Account funds to service the loan.

Mortgage Reducing Term Assurance (MRTA) — the private-sector equivalent of HPS, sold by life insurers. Most banks strongly recommend (and some require) MRTA for private property loans.

Home Contents Insurance — covers everything inside the four walls: furniture, white goods, electronics, jewellery, watches, plus personal liability if a guest is injured at your home.

Figure 1: At-a-glance comparison of the four core property-insurance pillars in Singapore.

Fire Insurance — Compulsory for HDB, Bundled for Condos

Every HDB flat owner is required by law to maintain a Fire Insurance policy on the structure of the flat. The Housing & Development Board has appointed a single insurer (currently FWD Singapore) to underwrite a basic policy with a uniform 5-year premium of around S$5.30 to S$25.40 depending on flat type. The cover sum is set to rebuild the structure, not the contents — if you assume your renovation, kitchen cabinets, or solid-timber flooring is included, you are mistaken. Most HDB owners then top up with a Home Contents policy from a private insurer.

For private condominium owners, fire insurance for the building is paid for collectively by the MCST and recovered through monthly management fees. The MCST policy is typically a Comprehensive HOOIS (Home Owner’s Outline Insurance Schedule) covering the structure, common property, and original developer fittings. What it excludes: any owner-installed renovation upgrades, fitted furniture beyond the original handover spec, and contents. If your condo unit has been substantially renovated, you should buy a top-up renovation cover — insurers will assess your defects-handover-to-current condition and quote accordingly.

For landed property owners, building fire insurance is bought directly from a general insurer. Sums insured are based on the rebuilding cost (excluding land value) rather than market price, which is why a S$10M Good Class Bungalow on a 15,000 sq ft plot may insure for only S$2.5M of structure.

Home Protection Scheme (HPS) — HDB’s Built-In Mortgage Cover

The Home Protection Scheme is a mortgage-reducing term assurance plan administered by the CPF Board for HDB flat buyers. It is compulsory for any flat owner using their CPF Ordinary Account to service their HDB loan, and is auto-enrolled at the point you commit to using CPF for the monthly instalment. The premium is paid annually from your CPF OA — typically S$80 to S$200 per year for a healthy 30-something with an outstanding loan in the S$300,000–500,000 range.

HPS pays off the outstanding HDB loan in three scenarios: death, total and permanent disability (TPD), or terminal illness. The flat then passes to the surviving co-owners or beneficiaries free of mortgage debt. There is no payout to the family beyond clearing the loan — if you want a cash sum on top, HPS will not deliver it. For that you need a separate term-life policy.

You may apply to opt out of HPS only if you already hold an equivalent or better term-assurance policy — a deliberate carve-out designed to prevent over-insurance. The CPF Board reviews your alternative policy against minimum sum-assured and tenure benchmarks before granting the exemption.

Mortgage Reducing Term Assurance (MRTA) — The Private-Sector Equivalent

MRTA, also marketed as Decreasing Term Assurance (DTA) or Mortgage Insurance, performs the same function as HPS but for buyers of private properties or those servicing their HDB loan entirely in cash. It is sold by every major life insurer in Singapore and underwritten as a single-premium or annual-premium policy whose sum assured tracks the falling balance of your mortgage as you pay down principal.

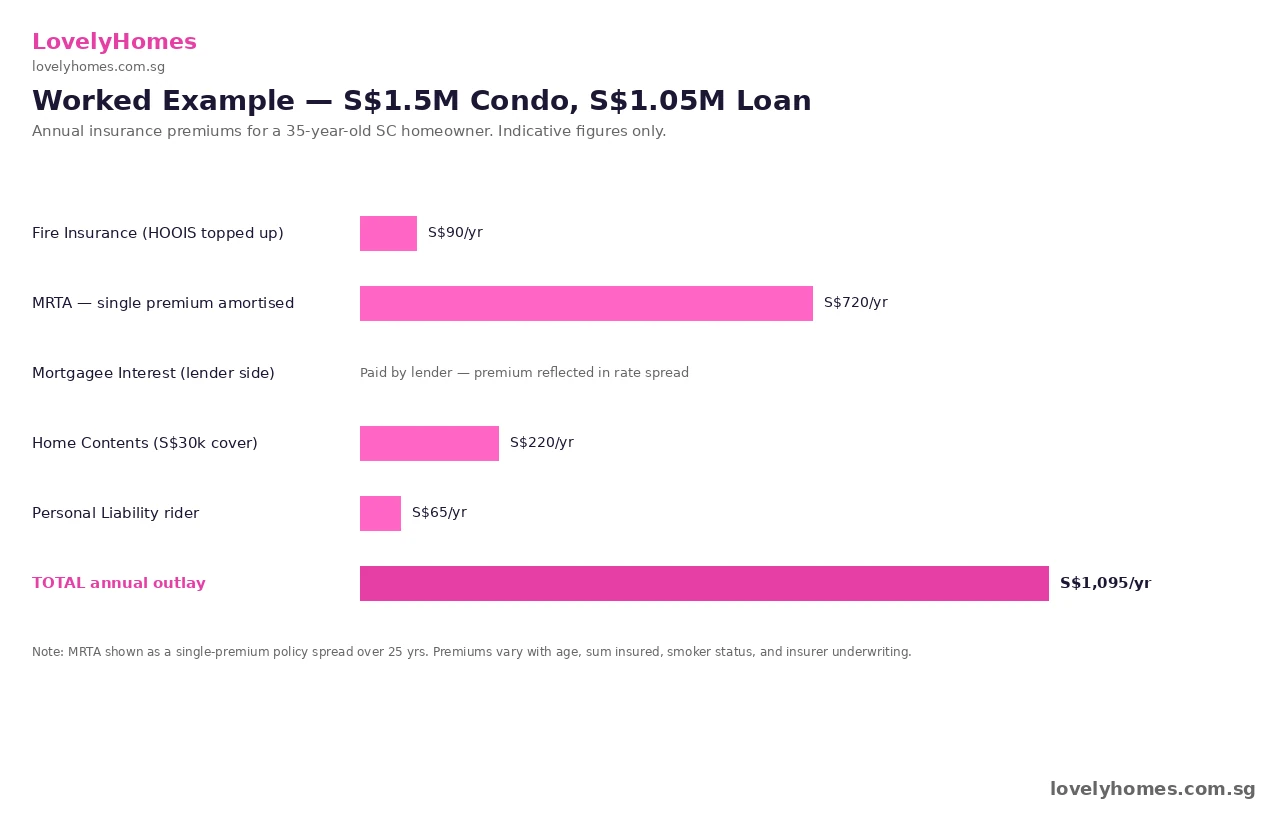

Premiums depend on age, gender, smoking status, sum assured, and tenure. As a rough guide, a 35-year-old non-smoker buying MRTA on a S$1,050,000 25-year loan will see single-premium quotes of S$15,000–22,000, equivalent to about S$600–900 per year if paid annually. Many buyers fund the single premium from their CPF OA at the point of property completion — CPF rules permit this provided the policy is assigned to the property.

If you are buying a condo on a bank loan and your mortgage is your largest financial liability, MRTA is the single most cost-effective protection product available. A S$700/year MRTA premium pays off in any month you are unable to work, where the alternative (a forced sale into a falling market) destroys decades of equity.

Figure 2: Indicative annual premium outlay for a 35-year-old SC homeowner with a S$1.5M condo and S$1.05M loan.

Home Contents Insurance — The Most Underbought Policy

Home Contents Insurance is the most commonly skipped policy and, statistically, the one that pays out most often. It covers the loose property inside the four walls of your home: furniture, white goods, televisions, computers, kitchen appliances, jewellery, watches, art, musical instruments, and (within sub-limits) cash. It also covers personal liability — the legal cost if your child accidentally injures a visitor on your premises, or if water damage from your unit affects the unit below.

Premiums are remarkably affordable. A standard policy with S$30,000 contents cover and S$500,000 personal liability costs around S$120–220 per year at major insurers (NTUC Income, Etiqa, FWD, Tokio Marine, MSIG). Higher contents sums, jewellery riders, or all-risks cover for valuables sit at S$300–500 per year.

What is typically excluded: gradual wear and tear, mould, vermin damage, intentional damage by a household member, cosmetic damage, and items left in common corridors. Read the schedule carefully — the differences between insurers on what counts as “valuables” (above S$2,500 per article) and which valuables need declaration are material.

Which Policies Do You Actually Need?

The right insurance stack depends on whether you live in HDB or private property, how the property is financed, and whether you intend to rent it out. The flowchart below traces the decisions.

Figure 3: Five-question decision flow mapping owner profile to mandatory and recommended policies.

Summary — Indicative Annual Premiums by Property Profile

Profile

Fire / Building

HPS / MRTA

Contents

Total / Year

4-rm HDB owner-occupier (CPF loan)

~S$5 (5-yr premium)

~S$120 HPS

~S$140

~S$265

5-rm HDB owner-occupier (cash loan)

~S$25 (5-yr premium)

~S$650 MRTA

~S$160

~S$835

S$1.5M condo owner-occupier (bank loan)

MCST top-up ~S$90

~S$720 MRTA

~S$220

~S$1,030

S$2.5M condo investor (rented out)

MCST top-up ~S$140

~S$1,200 MRTA

Landlord cover ~S$420

~S$1,760

Landed property (S$5M, owner-occupier)

~S$650 fire

~S$2,400 MRTA

~S$520

~S$3,570

Worked Example — The Tan Family, S$1.5M Condo Buyer

Mr Tan (35, SC, non-smoker) and his wife (33, SC, non-smoker) have just collected keys to a S$1.5M condo in District 19. Their bank loan is S$1,050,000 over 25 years at a SORA-pegged rate currently at about 3.7%. They have no children but plan to start a family within two years. Here is how their insurance stack lines up.

Fire / Building cover: Provided through the MCST policy — included in their monthly S$420 maintenance fee. They top up with a S$50,000 renovation cover at S$90/year, since their renovation upgrades (kitchen cabinetry, full marble flooring) are not part of the original developer handover.

MRTA: Mr Tan is the sole borrower for tax-deduction reasons. They take a single-premium MRTA of S$17,500 funded from his CPF OA — equivalent to about S$700/year over the 25-year tenure. Sum assured starts at S$1,050,000 and decreases linearly with the loan balance.

Home Contents: S$50,000 contents sum + S$1M personal liability + jewellery rider for Mrs Tan’s heirloom pieces. Annual premium: S$285.

Mortgagee Interest: The bank carries this internally — Mr Tan does not pay separately, but it is one reason the bank’s spread sits at +0.75% over SORA rather than +0.5%.

Total annual outlay: ~S$1,075, or about S$90 a month. Against a household income of S$15,000/month, the protection is rounding error — but it is the difference between Mrs Tan keeping the home if Mr Tan dies, and being forced into a distressed sale.

Insurance Riders Worth Considering

Beyond the four core pillars, riders address specific risk pockets that many homeowners discover only after a claim:

Renovation cover — tops up the MCST policy to include your renovation upgrades. Premium scales with renovation spend; rule of thumb is 0.1–0.2% of renovation value per year.

Domestic helper liability — covers the legal liability of accidents your foreign domestic helper causes inside or outside your home. ~S$50–120/year, often bundled with helper accident insurance.

Loss of rent cover — for landlords. Pays a defined monthly rent if the property becomes uninhabitable due to an insured peril (e.g. fire). ~S$80–200/year on a Home Contents Landlord policy.

All-risks worldwide for valuables — covers jewellery, watches, art whether at home or away. Stacks cleanly on top of Home Contents.

Public-liability extension — raises personal liability cover from the standard S$500K up to S$2M, useful for landed property owners and high-rise condo owners on upper floors where falling object claims can be material.

Common Mistakes Singapore Owners Make

Because property insurance is dull and the worst-case scenarios feel remote, most owners default to the cheapest single-quote option and discover the gaps when a claim is denied. The five most common mistakes:

Assuming HDB Fire Insurance covers contents — it does not. The FWD/HDB policy covers structure only.

Letting MRTA lapse after refinancing — if you refinance to a different bank, you must re-assign your MRTA policy or switch to a fresh one. A surprising number of owners hold an MRTA policy that no longer points to their current lender.

Not declaring jewellery and valuables — high-value items above S$2,500 each must be specified separately. Otherwise, the Home Contents policy caps any single-item claim at the unspecified-items sub-limit (typically S$5,000–10,000).

Renovating extensively without telling the insurer — if a fire or flood damages your premium kitchen, the MCST policy will only restore the original developer spec. Without your own renovation cover, you self-fund the gap.

Trusting bank-bundled policies — banks earn referral fees on bundled MRTAs and contents policies. Compare independently against direct insurer quotes; you will routinely save 10–25%.

What This Means for You

Insurance is the cheapest part of homeownership and the part with the lowest psychological return until something happens. The exercise to do today, regardless of how long you have owned your home, is simple: list every policy you currently hold, the sum insured, the renewal date, and the bank or insurer you bought it from. If you cannot complete that list in fifteen minutes, you almost certainly have a gap or a duplication. The total cost of being properly covered — even on a S$2.5M condo — rarely exceeds S$2,000 a year, less than a single mortgage instalment for most owners.

What Might Come Next

The Monetary Authority of Singapore has signalled interest in reforming retail insurance disclosure under its Financial Advisers Act review. Expect to see standardised “policy summary” documents for MRTA and Home Contents in 2027, similar to the Product Highlights Sheet for unit trusts. CPF Board has also been studying whether HPS should be extended to cover serious-illness scenarios beyond the current TPD definition; any such expansion would materially raise HPS premiums but reduce the case for private MRTA on top.

Frequently Asked Questions

Is HDB Fire Insurance enough on its own?

No. HDB Fire Insurance covers only the structure of the flat — the walls, floor slab, ceiling, and original developer-fitted items. It does not cover renovations, furniture, electronics, or any of your possessions. Owner-occupiers should pair it with Home Contents Insurance, which is sold separately by every major insurer for around S$120–220 per year.

Can I opt out of HPS if I have a private term-life policy?

Yes — the CPF Board permits HPS exemption if you can demonstrate an equivalent or better term-assurance policy is in force. The alternative policy must cover at least the outstanding HDB loan amount and run for the remaining loan tenure. Apply online via the CPF website with the policy schedule and a recent statement; approval typically takes 2–3 weeks. If the alternative policy lapses, HPS auto-resumes.

Should I buy single-premium or annual-premium MRTA?

Single-premium gives you a fixed cost upfront, payable from CPF OA, and locks in your insurability based on today’s health profile. Annual-premium spreads the cost but is repriced if you ever change tenure or sum assured. For most buyers under 40 in good health, single-premium delivers a 10–15% lifetime saving once you account for the CPF interest you forgo, but the convenience of paying from CPF rather than cash is significant. Annual-premium suits buyers who want the flexibility to switch insurers later.

Does my MCST condo policy cover my renovations?

Generally no. The Management Corporation Strata Title (MCST) policy covers the building structure and the original developer fittings — the kitchen and bathroom finishes that came with the unit at handover. Any subsequent renovation work, custom carpentry, designer fittings, or upgraded flooring is your responsibility. Buy a renovation cover or top-up through your home contents policy, sized to your actual renovation spend.

Will Home Contents Insurance pay out for a stolen Rolex?

Only if you specified it. Most policies treat any single article above S$2,500 as a “valuable” that must be individually declared on the schedule. Watches, jewellery, art, and rare collectibles fall into this category. If you have not declared a S$25,000 Rolex and it is stolen, the insurer pays the unspecified-items sub-limit (typically S$5,000–10,000), not the full value. Add a jewellery and watches rider for an extra S$50–120 per year per S$10,000 of declared value.

What happens to MRTA when I refinance?

The policy is assigned to a specific lender as collateral. When you refinance to a new bank, the policy must either be reassigned to the new lender or be replaced with a fresh policy. If you do nothing, the original MRTA may continue paying out to the old lender (now without a loan to settle), which means your family may eventually receive the residual but only after a contested administration process. Always notify your insurer the day you complete a refinance.

Does Home Contents cover my domestic helper’s belongings?

Most do not. The standard contents policy covers items belonging to the policyholder and household members — helpers are typically excluded. If you want to protect their personal items, look for a domestic-helper extension or take out a separate helper insurance policy (most foreign-domestic-helper insurance plans bundle a small personal effects cover at no extra cost).

This guide is for general information only and does not constitute financial, insurance, or legal advice. Premiums, sum-insured guidelines, scheme rules, and exemption criteria are illustrative as at April 2026 and subject to change at the discretion of the CPF Board, the Housing & Development Board, the Monetary Authority of Singapore, and individual insurers. Always verify the latest figures with primary sources — the CPF Board HPS page, the HDB Fire Insurance page, the Monetary Authority of Singapore, and the Inland Revenue Authority of Singapore — and consult a licensed financial adviser before purchasing or replacing any policy.

The day your condo developer hands over the keys is the single most important inspection day in the 25-year life of your home. It is also, for most buyers, the least rehearsed. This 2026 guide walks through exactly what the Temporary Occupation Permit (TOP) legally means, how the Defects Liability Period (DLP) works under the Housing Developers (Control and Licensing) Act, what a professional defects inspection looks like room-by-room, and how to escalate if a defect is not rectified within the statutory window.

Quick Answer — condo handover in Singapore

TOP (Temporary Occupation Permit) is granted by the Building & Construction Authority (BCA) when the building is safe to occupy. It is not the legal completion of your purchase.

Defects Liability Period is 12 months from Notice of Vacant Possession, statutorily enshrined in the standard-form Sale & Purchase Agreement (Schedule 2 of the Housing Developers Rules).

Inspection day: walk every room with a checklist. Typical defects count on a 3-bedroom unit: 40-120 items.

Log defects in the developer’s defect-management portal (often handed over with keys) or by signed Defect List; keep dated photos and timestamps.

Developer must rectify within a reasonable time. Escalation path: BCA → Consumers Association of Singapore (CASE) → Strata Titles Board → Small Claims Tribunal or High Court.

What TOP actually means — and does not mean

A Temporary Occupation Permit is issued by the BCA under the Building Control Act when the development has met minimum safety, structural and sanitary standards and is fit for temporary occupation. In plain English: the building is safe to live in, but regulatory sign-off is still in progress.

TOP is followed some months later by the Certificate of Statutory Completion (CSC), which is the final regulatory approval once all architectural, M&E, landscape and external works are closed out.

For the buyer, TOP triggers three commercial events under the standard-form SPA:

Event

What it means

Notice of Vacant Possession (NVP)

The developer notifies you the unit is ready. You have 14 days to pay the TOP progress instalment (typically 25% of price under progressive payment).

Defects Liability Period starts

12 months from NVP. Any defect discovered in this window must be rectified by the developer at their cost.

Maintenance obligations start

You begin paying maintenance charges to the Managing Agent from NVP onward (pro-rated from the NVP date).

The Defects Liability Period in detail

Under Schedule 2 of the Housing Developers Rules (the standard SPA clauses prescribed by the Controller of Housing), the developer is required to make good, at their own cost, any defect, shrinkage or fault in the Building Unit caused by defective workmanship or materials or by the unit not being constructed in accordance with the approved plans. The obligation runs for 12 months from the date of Notice of Vacant Possession.

Key practical points:

Notify the developer in writing (email counts) of any defect within the DLP. Verbal notifications are unenforceable.

If the developer does not commence rectification within one month of written notice, you may engage your own contractor to rectify and deduct the cost from the developer — provided you give 14 days’ written notice of intention first.

The DLP does not cover wear-and-tear, misuse, or alterations you have made to the unit.

Major structural defects (beams, columns, slab) have a separate 15-year limitation period under the Building Control Act.

Inspection day — a room-by-room walk-through

Give yourself two hours minimum. Take: a spirit level, a measuring tape, a torch, a power-point tester (available for around S$15), a roll of masking tape, a marker, a sheet of printer paper, and a smartphone with a full battery. Many buyers also engage a professional defect inspector for a fee of around S$400-800 per unit depending on size — a worthwhile investment on a S$1.5m-plus purchase.

Living / dining

Walk the entire floor. Tap tiles with a coin — a hollow sound indicates a poor screed bond.

Run a marble or spirit level across the floor; a fall of more than 3 mm over 2 m should be flagged.

Check ceiling for hairline cracks, particularly at beam/slab junctions.

Open and close every sliding door 3-5 times — listen for grinding, sticky runners, mis-aligned handles.

Check air-conditioning: run each fan coil unit for 10 minutes on cool and on dry, listen for gurgling, check drip-tray drainage.

Bedrooms

Open every wardrobe door, test soft-close hinges, check shelf alignment.

Check skirting along all walls — gaps more than 2 mm are defects.

Test every power-point with the tester (live / neutral / earth indicator).

Close the door fully — check for light gaps around frame, check door-closer speed.

Check window seals by spraying a fine mist on the outside (many buyers do this during the first rain).

Kitchen

Turn every tap fully open for 60 seconds; test mixer hot/cold blend; check for slow drainage.

Run dishwasher cycle (if provided), oven at 200°C for 15 minutes, hob on high.

Open every cabinet and drawer; test soft-close; check that runners do not bind.

Check for silicone gaps at counter-splashback junction — should be continuous and flush.

Test extractor hood fan on all settings; confirm exhaust flap opens.

Bathrooms

Shower test: run at full flow for 5 minutes, verify floor drainage (no ponding beyond 24 hours is the industry benchmark).

Check mirror-cabinet doors, shelves; test backlit LED strip if provided.

Tap every tile with a coin; flag hollow sounds.

Run hot water for 2 minutes at both basin and shower; check instant-heater / storage heater cycling.

Balcony / yard

Check tile falls toward drains; no ponding.

Verify balcony screen glass is fully seated; safety tape or sticker removed.

Yard tap should run at full pressure; washing machine standpipe drains cleanly.

M&E and overall

Test the main DB (distribution board): flip each MCB individually and identify which circuit it protects.

Test the audio/video intercom to guardhouse.

Test smart-home panel if provided; check Wi-Fi signal in every room.

Check the unit handover pack: as-built drawings, appliance warranties, maintenance schedules, keys count.

How to log defects properly

Most developers now run a defect-management portal or a QR-code driven mobile form. If yours does, use it — it creates an auditable log with timestamps. If not, draft a signed Defect List, sign two copies, and ask the handover officer to counter-sign with a date. Each defect entry should include:

Field

Example

Location

Master bedroom, north wall near cornice

Item

Wall paint — 40 cm horizontal hairline crack

Photo (timestamped)

IMG_20260421_1445.jpg

Requested rectification

Cut and re-plaster, repaint to match

Date logged

21 April 2026

Worked example — the timeline of a typical handover

Illustrative timeline for a 2026 condo buyer:

Day 0: Developer issues Notice of Vacant Possession.

Day 14: 25% TOP progress instalment due; your solicitor completes the transfer of keys.

Day 15-21: You schedule the keys-collection + inspection appointment.

Day 22 (inspection day): Walk the unit with a checklist. Log all defects in the developer’s portal.

Day 22-60: Developer schedules rectification visits. Typical turnaround: 2-6 weeks per batch.

Day 60 onward: You move in, continue to log new defects discovered in live-in use.

Day 365 (end of DLP): Submit a final consolidated list of any outstanding defects; developer remains liable until they are closed out even if the DLP end-date passes.

Years 1-15: Structural-defect window under the Building Control Act.

Common defects ranked by frequency

Wall / ceiling hairline cracks (shrinkage-related, usually stabilises after 6 months).

Floor-tile hollowness.

Door alignment and soft-close.

Silicone gaps at wet-area junctions.

Paint drips, roller marks, colour mismatches on patches.

Plumbing: leaks under basins, slow drainage, inconsistent water pressure.

Balcony ponding.

If the developer does not rectify — escalation path

Serve a formal 14-day notice citing the standard-form SPA clause, threatening to engage your own contractor and deduct costs.

Report to the Controller of Housing (BCA): the Housing Developers (Control and Licensing) Act empowers the Controller to take administrative action against developers in breach. Use the BCA feedback portal.

Consumers Association of Singapore (CASE): CASE mediates consumer disputes and can help facilitate settlement, particularly for finishes-quality issues.

Strata Titles Board (STB): for disputes that involve common property or the Building Maintenance and Strata Management Act.

Small Claims Tribunal: for money claims up to S$20,000 (S$30,000 with parties’ consent).

High Court civil action: for larger, structural, or complex disputes — typically after engaging a surveyor or architect to prepare a quantified report.

Key takeaway. Your handover day is the only time the developer is legally obligated to make good defects at their cost — use it. Walk every room with a checklist, log everything in writing, keep timestamped photos, and do not sign an “acceptance” form without an addendum listing the outstanding defects. The 12-month DLP is the most valuable warranty in Singapore property, and structural cover under the Building Control Act runs 15 years. Budget two hours for inspection day and consider a professional inspector on any purchase above S$1.5m.

Frequently asked questions

When does the Defects Liability Period start?

From the date of the developer’s Notice of Vacant Possession. The statutory 12-month period is prescribed in Schedule 2 of the Housing Developers Rules.

Do I need to be physically present at handover?

Yes. Your identity documents and the original keys-collection letter must be presented. If you cannot attend, grant a notarised Power of Attorney to a trusted representative.

Can I engage a professional defect inspector?

Yes. Independent defect-inspection firms typically charge S$400-800 per unit depending on size. They bring calibrated instruments (moisture meters, infra-red cameras, spirit levels) and a standardised report, which strengthens your claim if disputes arise.

What if I only discover a defect after moving in?

Report it within the 12-month DLP in writing. The developer remains liable for any defect arising from defective workmanship, materials, or non-compliance with approved plans during this period.

What about major structural defects?

The Building Control Act imposes a 15-year limitation period for structural defects. Structural claims are rare but serious — engage a Professional Engineer to inspect if you suspect one.

Does the DLP cover wear-and-tear?

No. Normal use, wear-and-tear, and any alterations you have made to the unit are excluded.

Can the developer refuse to rectify on grounds of “cosmetic issue”?

Only if the “defect” is genuinely cosmetic wear. Shrinkage cracks, paint drips, silicone gaps and poor workmanship are rectifiable defects under the SPA, not cosmetic issues. If the developer refuses, escalate to BCA.

What counts as a defect — is a small hairline crack a defect?

Shrinkage cracks up to 0.3 mm wide are generally considered within industry tolerance for a plastered wall, but wider cracks or any crack on a tile, ceiling or beam is a defect. Photograph, measure with a crack gauge, and log.

Who is the “Managing Agent” and when do I start paying?

The Managing Agent is the professional property-management firm appointed by the developer to run the MCST (Management Corporation Strata Title) until the first AGM, after which the MCST Council may retain or change the agent. Maintenance charges run from NVP.

What if I find a defect on the last day of DLP?

Notify in writing immediately. As long as the defect was reported within the 12-month window, the developer remains liable to rectify even if rectification work itself extends beyond the DLP end-date.

Can I claim compensation for delayed handover?

Yes. The standard SPA provides for Liquidated Damages if the developer fails to deliver vacant possession by the contracted date (typically 3 years from the date of the Sale & Purchase Agreement). LD is calculated at 10% per annum (on purchase price) for each day of delay, pro-rated.

What happens at the end of the DLP?

The Managing Agent typically schedules a formal “end-of-DLP” inspection of common property (lobbies, lifts, facilities). For your own unit, you bear responsibility for any new defects after DLP end-date, except for latent defects discovered within the 15-year structural window.

Building & Construction Authority (BCA) — Building Control Act and TOP / CSC administration.

Urban Redevelopment Authority (URA) — Approved plans and subsidiary proprietor records.

Controller of Housing — Housing Developers (Control and Licensing) Act; Housing Developers Rules Schedule 2 (standard-form SPA).

Strata Titles Board (STB) — Building Maintenance and Strata Management Act 2004 and subsidiary regulations.

Consumers Association of Singapore (CASE) — dispute-mediation framework.

Disclaimer: This guide is a general overview of Singapore’s condo handover and defects-rectification framework, not legal advice. The standard-form Sale & Purchase Agreement and Defects Liability Period terms are prescribed by the Controller of Housing under the Housing Developers Rules; always refer to the actual SPA you have signed for the binding terms of your purchase. Structural claims, complex rectification disputes, and any escalation beyond the Small Claims Tribunal should involve a qualified solicitor and, where appropriate, a Professional Engineer or Quantity Surveyor.

Quick Answer — what every first-time landlord must do

Check you can rent — MOP (if HDB), mortgage terms, condominium MCST by-laws, and URA’s minimum rental tenure (3 months private; 6 months HDB).

Price your unit using URA rental caveats plus a realistic weighted-average of last 6-month comparables — not wishful-thinking anchor listings.

Draft a tenancy agreement with a compliant Diplomatic Clause, Minor Repairs Clause (typically S$150–S$250 cap), and Tenant-Pays-Utilities clause.

Stamp the lease with IRAS within 14 days of signing — via e-Stamping Portal. Rental stamp duty is ~0.4% of total rent for leases up to 4 years.

Declare rental income in your annual tax return — net of allowable deductions, or the 15% deemed-expense route.

Why this checklist exists

Renting out a Singapore condo for the first time is deceptively simple in concept and unexpectedly intricate in execution. The number of moving parts — URA minimum-stay rules, the Income Tax Act, IRAS e-Stamping, MCST by-laws, your own bank’s covenants, the Residential Property Act, the Immigration & Checkpoints Authority’s occupancy checks — is the real source of first-year landlord mistakes. This checklist walks you through the end-to-end process in the order a first-time landlord actually encounters each task.

The framing throughout is practical. We are not going to rehearse abstract property law. We will assume you own a private condominium in Singapore, you are considering renting it out, and you need a dependable sequence from “should I do this?” to “my tenant has handed back the keys”.

Step 1 — Check you can legally rent out your unit

Five checks come before anything else. Skip any one and you risk a voided tenancy, a penalty from IRAS, or a breach of your mortgage.

MCST by-laws. Your condominium’s Management Corporation Strata Title (MCST) may have short-tenancy restrictions, pet rules, or fit-out limits. Request a copy of the current by-laws and confirm they permit a lease of the intended length.

URA minimum rental tenure. For private residential property, URA mandates a minimum continuous stay of 3 months per tenancy. Anything shorter (short-term / holiday / Airbnb-style) is illegal and subject to a fine of up to S$200,000 under the Planning Act. For HDB flats, the minimum is 6 months and subletting rules are stricter.

Mortgage covenants. Most bank mortgages allow owner-occupation and arm’s-length tenancy without objection, but some lower-rate promotional home loans require owner-occupation as a condition. Check your Letter of Offer.

HDB MOP. If the unit is an Executive Condominium within 5 years of TOP, or an HDB flat within the 5-year Minimum Occupation Period, renting out the entire unit is prohibited. Room rental is permitted for HDB after certain thresholds.

Residential Property Act. Foreign buyers of landed property must have URA approval. For condos, this matters less for leasing purposes but still shapes the tenant pool (e.g. corporate leases often require company-to-company contracts).

Step 2 — Decide your target tenant profile

The rental market in 2026 is fragmented across tenant archetypes, each with different lease length, rent ceiling, and fit-out expectations.

Tenant archetype

Typical lease

Sensitivities

Corporate expat (regional HQ)

2 years with Diplomatic Clause after year 1

Fully furnished; near international schools; building quality

Near NUS / NTU / SMU / international school; broadband; parental guarantor

Choose the archetype first, then calibrate the asking rent, fit-out, and marketing channel accordingly. A corporate-expat lease on a D10 condo targets a different price ceiling than a tech-couple lease on a D3 condo, even when gross psf rent is similar.

Step 3 — Price the unit correctly

The single most common first-time landlord mistake is pricing the unit from the highest asking listings in the building. Landlords who do this leave their unit vacant for 6–10 weeks and then let it on the original fair-market rent anyway.

Use URA’s Rental Contracts Data (updated monthly on the URA eservice portal) to extract the last six months’ rental contracts for your exact project. Calculate a weighted-average psf monthly rent; weigh larger units more heavily; discount short-lease and unfurnished contracts to a like-for-like basis. Aim your asking rent at 2%–5% above the weighted average to leave negotiating headroom.

If you are within 500 metres of an MRT and the building has functioning pool/gym/BBQ amenity, you can price at the upper end. If your unit faces a noisy road, is low-floor, or has a cramped layout, price at or below the median.

Worked example — 2BR at a D3 condo

Your project’s last 6 months showed 8 rental contracts for 2BR units ranging from S$4,200 to S$5,300 monthly, weighted average S$4,750. Your unit is mid-floor, fully furnished, south-facing.

Minimum accept: S$4,700 (just below weighted average) if you want to lease within 3 weeks.

Target lease: 2 years with Diplomatic Clause at year 1 exit — stabilises cash flow.

Step 4 — Prepare the unit for marketing

A well-prepared unit typically lets 30%–50% faster than a “lived-in” unit at the same asking rent. Before photographs, complete:

Deep clean. Pay for a professional clean — kitchen extractor, bathroom grout, washing machine filter, air-con servicing with gas top-up.

Repaint. Freshly painted white walls read as new on listing photos. Budget S$1,500–S$3,500 for a 2BR condo depending on size.

Small repairs. Silicone re-beading in bathrooms, replace chipped grout, re-polish wood flooring, replace yellowed power sockets and light switches.

Furnish correctly for archetype. For corporate expat, the unit must be fully furnished including crockery, washing machine, and curtains. For local family, a part-furnished option (white goods + curtains only) is often welcomed.

Photographs. Commission a professional property photographer — S$200–S$400 for a 2BR shoot. Wide-angle lenses, white balance, twilight shots. Professional photos translate directly into listing click-through.

Step 5 — Engage help (or go solo)

You have three routes:

Engage an exclusive salesperson. A registered salesperson under the Council for Estate Agencies can market the unit across their channels, screen tenants, draft the tenancy agreement, and manage the handover. Commission is typically half a month’s rent for a one-year lease, one month for two-year. Pay only on successful tenancy.

List yourself on property portals. Free or low-cost direct listing on the major Singapore property portals. You handle enquiries, showings, draft the tenancy agreement, and carry all the risk of under-pricing or picking the wrong tenant. Best for landlords with time and prior experience.

Use a corporate-relocation broker. For premium addresses, dedicated corporate-relocation specialists can introduce multi-national company tenants directly. Fees are higher but tenants are pre-vetted and leases are longer.

Whichever route, insist that any salesperson you engage is registered and CEA-accredited — verify on the CEA Public Register.

Step 6 — Screen the tenant

Screening protects you from the most expensive landlord mistake: the non-paying or damaging tenant. At minimum, collect:

Copy of NRIC / passport + visa / Work Pass.

Latest 3 months’ payslips or bank statements.

Employment letter confirming role, start date, and notice period.

Reference from previous landlord (ask for a WhatsApp call).

For corporate tenants: letter of employment from the corporate HR, plus the corporate tenancy agreement signatory authority.

Ask directly about number of occupants and relationship. Under ICA rules, only permitted occupants may live at the address, and their names and identification documents must be on file.

Step 7 — Issue the Letter of Intent and collect the booking deposit

The tenant typically signs a Letter of Intent (LOI) and pays a 1-month booking deposit (also called the “good faith deposit”). The LOI sets out key terms: rent amount, lease period, commencement date, Diplomatic Clause presence, and any special conditions. On signing the tenancy agreement, the booking deposit converts into the first month’s rent or security deposit per the LOI terms.

Step 8 — Draft and sign the tenancy agreement

A compliant Singapore residential tenancy agreement should contain:

Parties — landlord(s) and tenant(s), full legal names and NRIC/passport numbers.

Demise — unit address, inclusive items (furniture inventory attached as Schedule).

Governing law and dispute resolution — Singapore law, Singapore courts.

Attach a detailed inventory Schedule with photographs of every furniture item and appliance, timestamped.

Step 9 — Stamp the tenancy agreement with IRAS

All residential tenancies must be stamped via the IRAS e-Stamping Portal within 14 days of signing. Rental stamp duty rates:

Lease length

Stamp duty rate

Up to 4 years

0.4% on total rent over the lease term

Over 4 years

0.4% on four times the Average Annual Rent (AAR) for the period

Typically either party can pay; custom is for the tenant to pay. Keep the stamp certificate — you will need it for any dispute and for IRAS tax returns.

Step 10 — Handover the unit

On commencement day, meet the tenant at the unit. Walk through the inventory Schedule together and sign a handover checklist. Photograph meters (water, electricity, gas) and log them on the checklist. Hand over keys, access cards, season parking labels, fob keys and remote controls. Confirm the forwarding address for bills and the tenant’s emergency contact.

If utilities are not already transferred, go through the SP Group transfer together on the spot. For condos, file the tenant’s details with the MCST so the security office admits the tenant and guests.

Step 11 — Manage the tenancy

During the lease:

Collect rent on the agreed day. Set up a GIRO standing instruction or a calendar reminder.

Log repair requests via email, not WhatsApp voice — you want a paper trail.

Conduct annual inspection (often in month 6) on 14 days’ written notice, during reasonable daylight hours.

Service air-conditioners quarterly — tenant responsibility under standard TA, but landlord should confirm it happens.

Step 12 — Declare rental income

IRAS requires all rental income to be reported in your annual tax return, even if you made a cash-flow loss. Two routes are possible:

Route A — actual deductions. Deduct property tax, bank mortgage interest, MCST fees, condo maintenance charges, agent commission, insurance, and allowable repairs. Keep all invoices and receipts for 5 years.

Route B — 15% deemed-expense option. Take a flat 15% of gross rent as a deemed allowance for expenses, plus the actual property-tax paid and actual mortgage interest separately. Simpler, but worse outcome if your actual expenses exceed 15%.

Compute both routes each tax year; pick the higher deduction. IRAS provides worksheets on its website.

Key takeaway

First-time landlord success is 80% process and 20% market. Follow the checklist: clear the legal checks, price against URA caveats (not aspiration), prepare the unit properly, screen rigorously, stamp within 14 days, and document everything. Landlords who short-cut the checklist typically pay for it at lease end — disputes over the security deposit, unpaid minor repairs, or tax penalty letters. Landlords who run the checklist end the first tenancy profitably and with a confident call on whether to renew, re-let, or sell.

Step 13 — Renew, re-let, or end the tenancy

In month 9 of a 12-month lease (or month 21 of a 24-month lease), open the renewal conversation. Market rent has moved; your existing tenant’s departure is your blank canvas to re-price. Three outcomes are common:

Renew at a new rent. Market has risen; propose a 3%–8% increase. Tenant accepts — draft a renewal tenancy agreement and re-stamp.

Tenant gives notice. Serve the standard handover notice. Conduct the exit inspection against the original inventory Schedule. Refund the security deposit minus damages within 7–14 days.

Re-market. If no renewal and no replacement via the outgoing tenant, restart from Step 3. The second lease typically signs faster because you already have fresh photos, inventory, and process.

Frequently asked questions

Can I rent out my HDB flat as a first-time landlord? Only after the 5-year Minimum Occupation Period. Rules for HDB whole-unit rental differ from room rental and are stricter than private condo rental.

How long is the minimum tenancy? 3 months for private residential (URA), 6 months for HDB.

Is Airbnb or short-term rental allowed? No. Short-term rentals under 3 months for private residential are illegal and carry fines up to S$200,000.

How much is the security deposit? 1 month for a 12-month lease; 2 months for a 24-month lease is market standard, though parties can negotiate.

Who pays stamp duty? Custom: tenant. Legal position: either party, but standard template puts it on the tenant.

What is a Diplomatic Clause? A clause allowing expat tenants to terminate the lease after the minimum 12 months with 2 months’ notice if transferred or repatriated by the employer. Applies only to holders of Employment Pass or equivalent.

Must I use an agent? No. You can self-manage, but many first-time landlords benefit from the risk management an experienced salesperson provides.

Can I disallow pets? Yes — put a “no pets” clause in the tenancy agreement. Some condominiums have MCST-level pet restrictions independent of your lease.

Do I pay GST on residential rent? No. Residential leasing is exempt from GST.

What if the tenant damages the unit? The inventory Schedule, entry-day photos and exit inspection are your evidence. Deduct repair cost from the security deposit. If damages exceed the deposit, send a formal demand letter; escalate via Small Claims Tribunal for claims up to S$30,000.