HDB 2-Room Flexi for Seniors Singapore 2026: Short Lease, Silver Housing Bonus and Lease Buyback Explained

Singapore’s HDB system includes a category of flat specifically designed for seniors and older singles who want to right-size, reduce their mortgage burden, or access their housing equity without leaving public housing. The HDB 2-Room Flexi flat — and its cousin, the Studio Apartment — give buyers aged 55 and above a route to a smaller, more manageable home, often with significant grant support on top. If you are approaching retirement and wondering what to do with a large, nearly-paid-off flat, this guide explains every option available to you in 2026.

Quick Answer — HDB 2-Room Flexi for Seniors 2026

- Who can buy: Singles aged 35+; couples where at least one party is 55+ (for Short Lease option)

- Short Lease option: 15, 20, 25, 30, or 35 years — choose a lease matching your remaining life expectancy

- Studio Apartments: Available at Selective En-bloc Redevelopment Scheme (SERS) sites; 30-year lease; for buyers 55+

- Silver Housing Bonus (SHB): Up to S$30,000 cash when right-sizing from a larger flat

- Lease Buyback Scheme (LBS): Sell part of your remaining HDB lease back to HDB; proceeds top up your CPF Retirement Account

- CPF use: Proportional for short leases — you can only use CPF savings up to the value of the remaining lease

- No resale market for Studio Apartments; 2-Room Flexi 99-year units can be resold after 5-year MOP

What Is a HDB 2-Room Flexi Flat?

The 2-Room Flexi flat is a Build-To-Order (BTO) flat type rolled out by HDB in 2015 to replace the discontinued Studio Apartment in new BTO exercises. It comes in two variants. The first is the Short Lease option, designed specifically for seniors aged 55 and above and singles aged 35 and above, with a lease of 15 to 35 years (in five-year increments) chosen at the point of application. The second is the Standard 99-Year Lease option, available to singles aged 35 and above and to families. Floor area is modest by design: Type 1 units are 36 sqm and Type 2 units are 45 sqm. Both include a living/dining area, one bedroom, one bathroom, a kitchen, and a service yard.

Short Lease vs 99-Year: Which Should Seniors Choose?

The Short Lease variant is usually the financially smarter choice for buyers who are primarily right-sizing for comfort, not investment. By choosing a shorter lease — say, 25 years for a buyer aged 65 — you pay a significantly lower price for the flat. The sale proceeds from your current, larger flat are then available for other needs. CPF use on a short-lease flat is proportional: the CPF Board limits your Ordinary Account (OA) withdrawal to a fraction of the flat’s valuation based on the ratio of the chosen lease relative to 65 years. In practice, buyers on a 20-year short lease will use mostly cash and have less CPF deployed in the flat, leaving more CPF savings liquid for drawdown in retirement.

The 99-Year Lease option makes more sense for younger singles in their 30s or early 40s who want a small flat as a starter or long-term home with full resale flexibility. After the 5-year MOP, the unit can be sold on the open market.

Studio Apartments — The Legacy Option

Studio Apartments were HDB’s original senior-friendly product, built from the 1990s. They are no longer built in new BTO exercises (replaced by the 2-Room Flexi from 2015), but existing units occasionally come up through SERS (Selective En-bloc Redevelopment Scheme) rehousing exercises. Studio Apartments are typically 35–45 sqm, carry a 30-year lease from the date of offer, and are sold to buyers aged 55 and above. There is no open-market resale — you can only surrender the flat back to HDB if you need to leave.

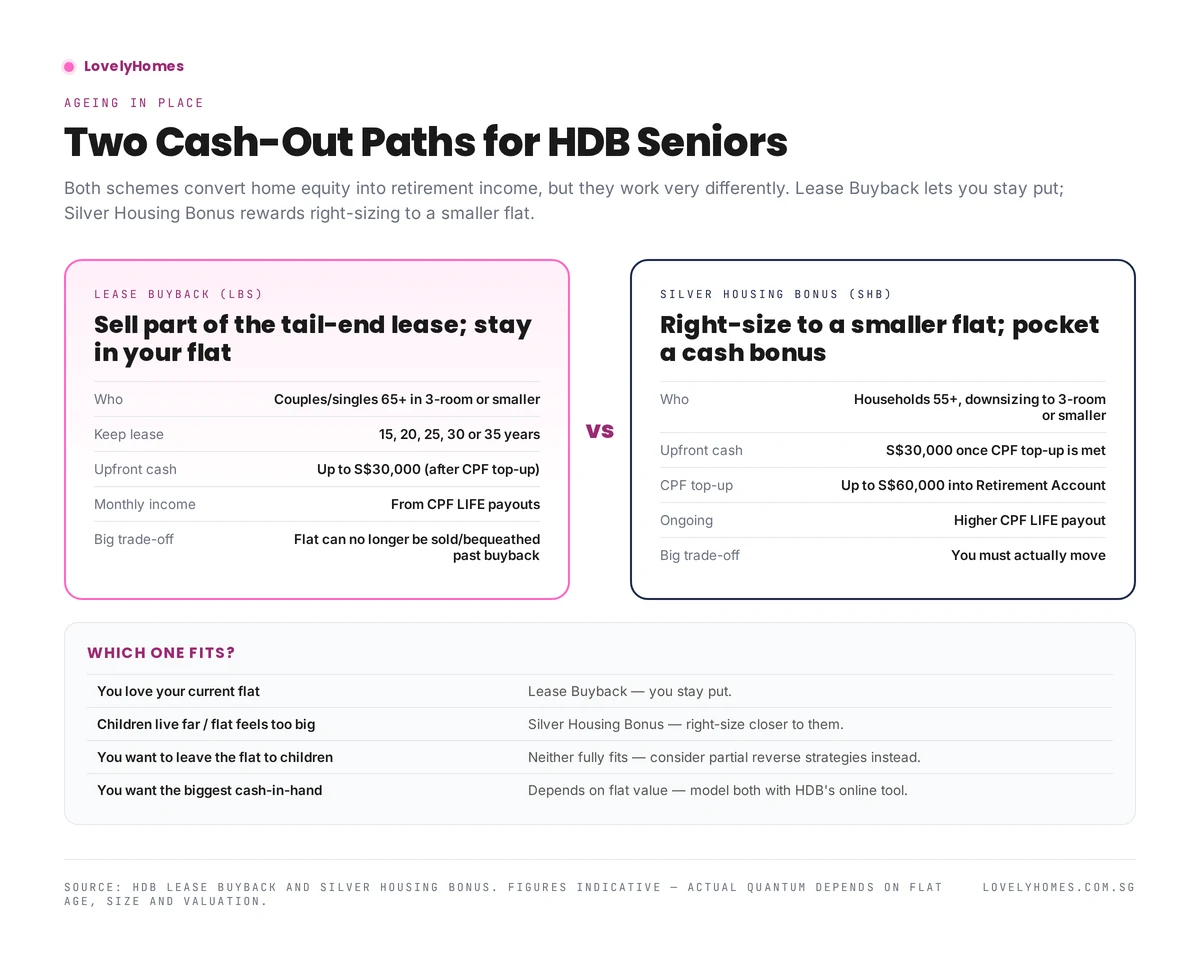

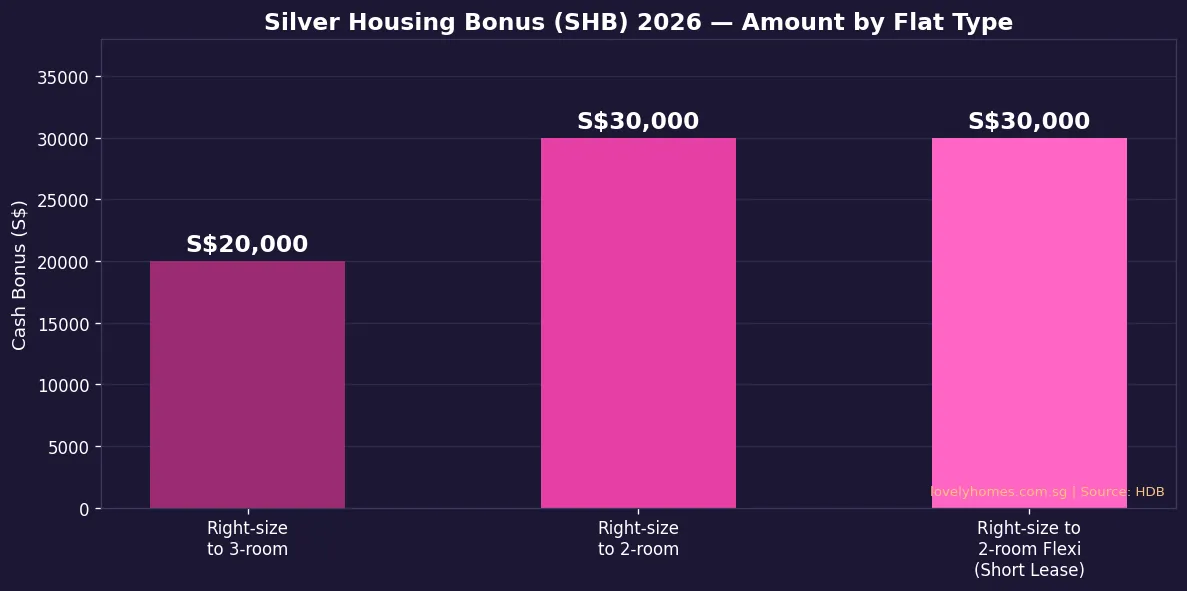

Silver Housing Bonus — Up to S$30,000 in Cash

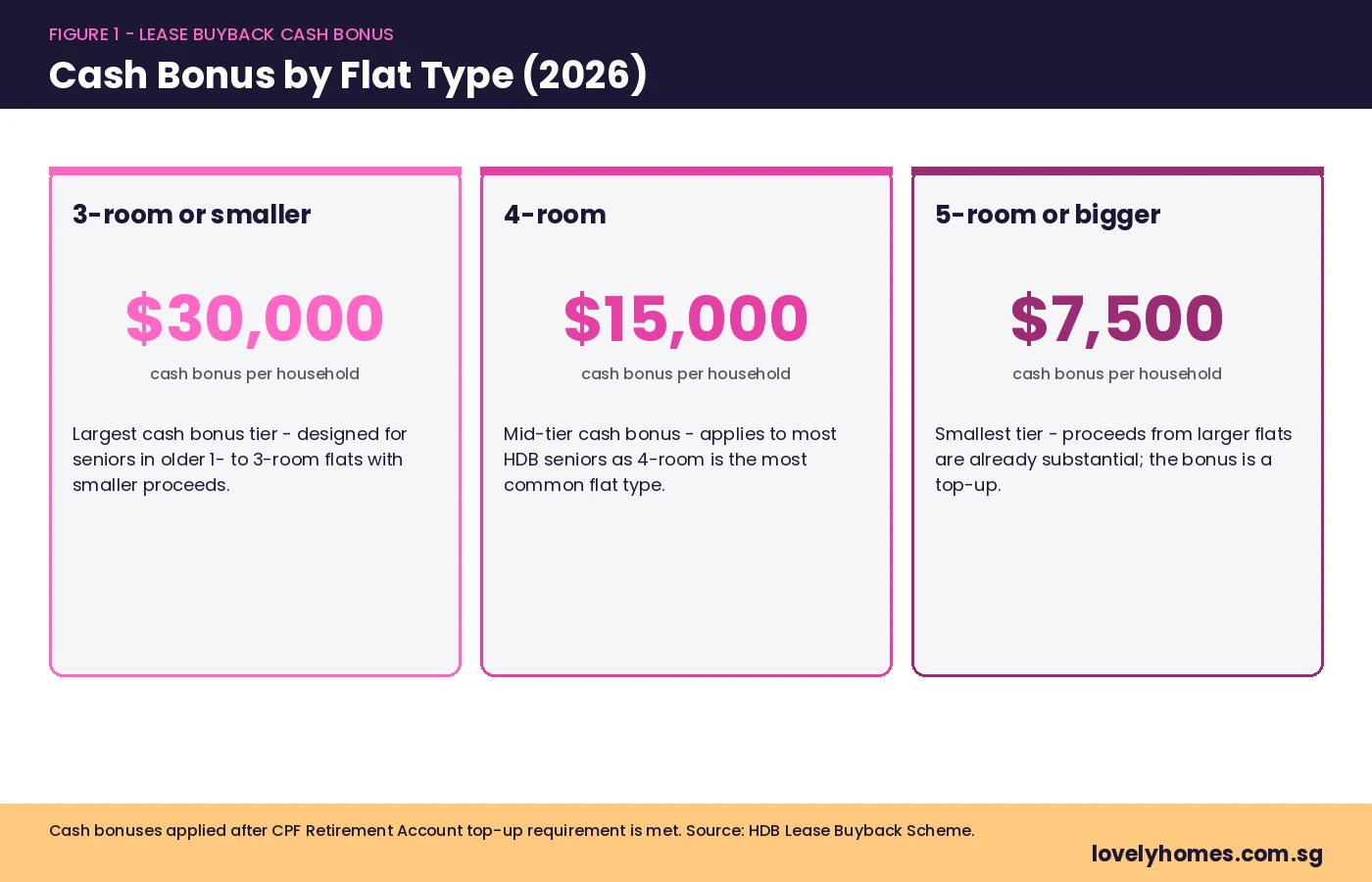

The Silver Housing Bonus (SHB), administered by the CPF Board and HDB, provides eligible seniors with a cash bonus of up to S$30,000 when they right-size to a smaller flat. Eligibility: At least one flat owner must be a Singapore Citizen aged 55 or above. The seller must use the net sale proceeds of their current flat to top up their CPF Retirement Account (RA) up to the current Enhanced Retirement Sum (ERS). For right-sizing to a 2-room or 2-Room Flexi flat (Short Lease), the maximum bonus is S$30,000. For right-sizing to a 3-room flat, the bonus is S$20,000.

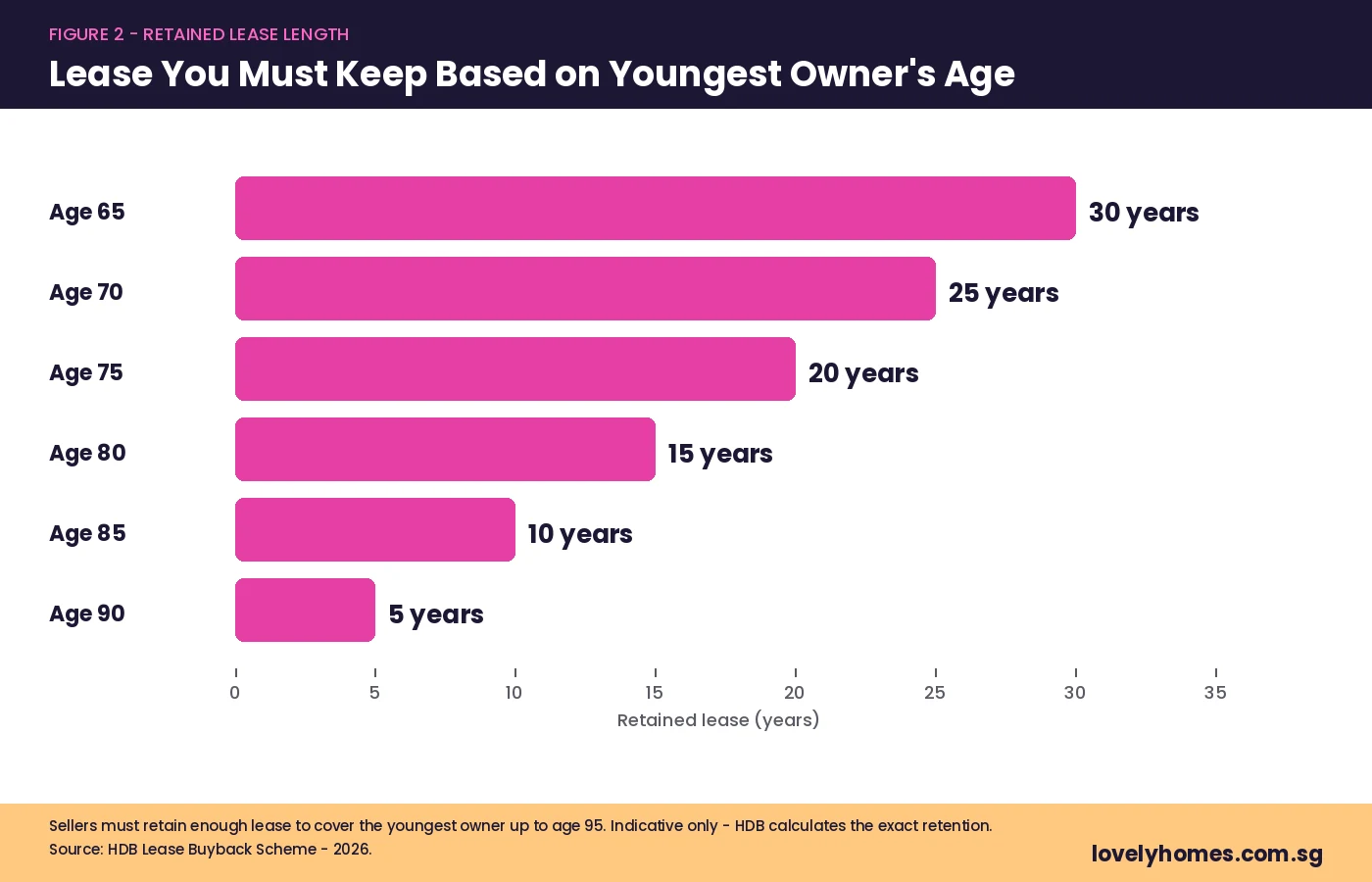

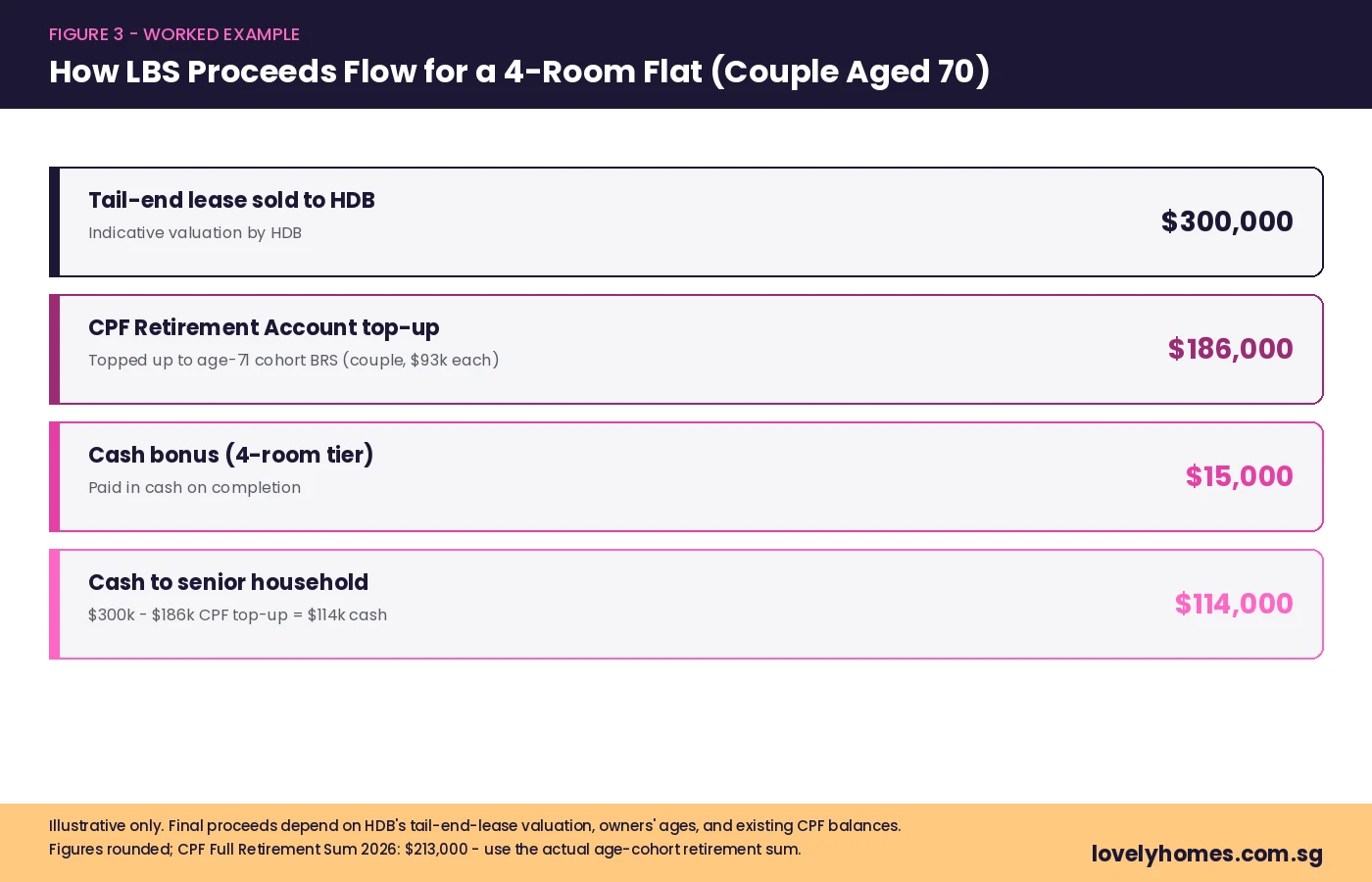

Lease Buyback Scheme — Converting Your Flat’s Value to Retirement Income

The Lease Buyback Scheme (LBS) allows eligible seniors to sell part of their flat’s remaining lease to HDB for a lump sum, which is used to top up their CPF Retirement Account. The retained lease must be at least 20 years and cover the youngest owner to age 95. HDB buys the tail end of the lease at assessed market value of that lease proportion, with proceeds going into the owner’s CPF RA to meet the Full Retirement Sum (FRS) or Basic Retirement Sum (BRS) — excess is paid in cash. The couple continues living in the flat under the retained lease and receives monthly CPF LIFE payouts from the topped-up RA.

LBS is not available for 2-Room Flexi Short Lease flats because the chosen lease is already short by design. It is available for 2-Room Flexi 99-Year flats and for larger flats (3-room and above).

Summary: HDB Senior Housing Options at a Glance

| Scheme | Who Qualifies | Key Benefit | Amount / Price Range |

|---|---|---|---|

| 2-Room Flexi Short Lease | Singles 35+; couples with one 55+ | Smaller, cheaper flat; choose lease | ~S$90k–S$200k |

| 2-Room Flexi 99-Year | Singles 35+; families | Full resale rights after MOP | ~S$180k–S$350k |

| Studio Apartment | Buyers 55+ (SERS estates) | Below-market; 30-yr lease | ~S$80k–S$150k |

| Silver Housing Bonus | SC 55+, right-sizing from larger flat | Cash bonus | S$20k (3-rm) / S$30k (2-rm) |

| Lease Buyback Scheme | SC/SPR 65+, own 3-room or larger HDB | Convert lease equity to CPF LIFE | Lump sum into RA; monthly payout |

| Proximity Housing Grant | Buyers near parents/children | Grant on resale purchase | S$20k (1km) / S$30k (same estate) |

Worked Example — The Lim Couple Right-Sizes at 68

Mr and Mrs Lim, both aged 68, Singapore Citizens, live in a 5-room HDB flat in Bishan with 55 years of lease remaining. Their children have moved out. They right-size to a 2-Room Flexi, Short Lease (25 years) in the same estate.

- Sale proceeds from the 5-room flat: S$650,000 (after refunding CPF + accrued interest of S$220,000)

- Purchase price of 2-Room Flexi (25-year short lease): S$145,000

- CPF use for purchase: proportional to 25/65 years ≈ 38% of flat value → S$55,000 from OA (if available)

- Cash needed: S$145,000 − S$55,000 = S$90,000 cash

- Silver Housing Bonus: S$30,000 cash (right-sizing to 2-room)

- CPF RA top-up from sale proceeds to meet ERS (say S$190,000 per person)

- Net free cash in hand after purchase, SHB, and CPF RA top-up: approximately S$235,000

- Monthly CPF LIFE payout after RA top-up (ERS scheme): approximately S$2,200–S$2,500 per person

Why This Matters — Housing as a Retirement Asset

A very large proportion of household wealth in Singapore is locked inside HDB flats. The 2-Room Flexi, SHB, and LBS framework is the Government’s systematic answer: offering seniors structured, HDB-administered routes to convert housing equity into retirement cash flow without moving out of public housing. The 2026 environment makes right-sizing particularly attractive — HDB resale prices remain elevated after years of growth, while 2-Room Flexi Short Lease prices remain relatively modest, offering a significant arbitrage between what seniors receive for their existing flat and what they pay for the right-sized replacement.

What Might Come Next

HDB has been gradually expanding 2-Room Flexi supply in mature and prime estates. The Government may introduce enhancements to the Silver Housing Bonus quantum or Lease Buyback Scheme proceeds as Singapore’s population continues to age. Monitor the annual MND Budget statement, National Day Rally, and the HDB website for the latest BTO schedule and grant amounts before committing to any right-sizing decision.

Frequently Asked Questions

Can a single person buy a 2-Room Flexi short-lease flat?

Yes. Singapore Citizens and Permanent Residents aged 35 and above who are singles can apply for a 2-Room Flexi flat — both the 99-year and Short Lease variants. For the Short Lease, HDB targets it at buyers aged 55 and above, but the formal eligibility lower bound is 35. Singles are not eligible for most family-tier HDB grants, but may qualify for the Silver Housing Bonus if they are at least 55 and right-sizing from a larger flat.

What happens when the short-lease flat’s chosen tenure expires?

When the lease expires, the flat reverts to HDB with no residual value or compensation. This is by design — the flat’s utility is fully consumed during the chosen lease period. Buyers should choose a lease length covering at least to age 95 per CPF Board guidelines. If the owner passes away before expiry, the remaining lease value may be passed to eligible family members under HDB estate transmission rules.

Can I use CPF OA to buy a 2-Room Flexi Short Lease flat?

Yes, but proportionally. The CPF Board allows OA use up to the value corresponding to the lease coverage from your youngest owner’s age to 95. For a 25-year lease chosen by a 65-year-old (covering to age 90), the CPF-usable proportion is roughly 25/65 ≈ 38% of assessed value. A significant portion must therefore be paid in cash. This is intentional — it preserves CPF savings for retirement income rather than locking them into housing.

How do I apply for the Silver Housing Bonus?

The Silver Housing Bonus is administered jointly by HDB and the CPF Board. You apply at the point of booking your new (smaller) flat or during the resale application process. HDB assesses eligibility and the bonus amount based on the size of your current flat, your new flat, and whether you meet the RA top-up requirement from sale proceeds. The cash bonus is paid directly to you — not into CPF — once the transaction is completed. Check HDB’s 2-Room Flexi page for current SHB quantum and conditions.

Does the Lease Buyback Scheme work with a 2-Room Flexi flat?

LBS is available for 3-room and larger HDB flats and for Studio Apartments in SERS estates. It is not available for 2-Room Flexi Short Lease flats because the chosen lease is already short. For 2-Room Flexi 99-year flats, LBS is in principle available but less commonly used, since most LBS participants hold larger flats with more lease equity to monetise. Contact HDB directly to assess eligibility for your specific lease position.

Can I rent out my 2-Room Flexi flat?

You may rent out individual bedrooms after satisfying the MOP (5 years for the 99-year variant). HDB generally does not approve whole-unit rentals for short-lease 2-Room Flexi flats. Renting a bedroom is subject to HDB’s standard subletting approval process and tenant nationality quotas. You may not rent out the entire flat while listed as the owner-occupier.

What is the difference between the 2-Room Flexi and the old Studio Apartment?

Studio Apartments (1990s–2000s) are no longer available in new BTO exercises — replaced by the 2-Room Flexi from 2015. Studio Apartments carry a 30-year lease and are offered at SERS estates to sitting residents. The 2-Room Flexi offers greater flexibility: choice of lease from 15–35 years or a full 99-year lease, two floor-area variants, and (for the 99-year unit) open-market resale rights after MOP. Studio Apartments have no resale market. For most seniors today, the 2-Room Flexi is the primary option.

Related Articles