The HDB Lease Buyback Scheme (LBS) lets older Singaporean households unlock the value of their flat’s tail-end lease without moving out. In exchange for selling the back end of the lease to HDB, eligible owners aged 65 and above receive a top-up to their CPF Retirement Accounts, a fixed cash bonus, and any remaining proceeds in cash — while continuing to live in the flat for the rest of the retained lease. For seniors who own a flat outright but feel cash-poor, LBS is the most direct lever the Government provides to convert bricks into retirement income.

This guide walks through the 2026 LBS framework end-to-end — eligibility, how the retained-lease calculation works, the cash bonus tiers across flat types, a worked example, and how LBS compares against Right-Sizing (selling the existing flat to buy a smaller one) and the Silver Housing Bonus. All figures and rules below reflect HDB’s current published scheme. For the latest position, always check the HDB Lease Buyback Scheme page.

Quick Answer — LBS at a glance

- Owners must be Singapore Citizens, aged 65 or older, with at least one SC member in the household.

- Household income ceiling: S$14,000 per month.

- Sells the tail end of the flat’s lease to HDB; retain enough lease to cover the youngest owner up to age 95.

- Net proceeds first go to top up the CPF Retirement Account — balance paid as cash.

- Cash bonus of S$30,000 (3-room or smaller), S$15,000 (4-room), or S$7,500 (5-room+).

- You continue to live in the flat for the entire retained lease — no need to move.

- Cannot rent out the whole flat once you have sold the tail-end lease (bedroom rental is allowed).

What is the HDB Lease Buyback Scheme?

Most HDB flats are leased on a 99-year tenure. By the time owners reach their 60s and 70s, only part of that lease is left, and the practical value of the remaining decades is substantially more than the lifespan of the owner. The Government introduced LBS in 2009 (initially for 3-room and smaller flats; extended to 4-room flats in 2013 and to 5-room and larger flats in 2015) to let seniors monetise the portion of the lease they will not personally use, while staying in their home until the end of the retained lease.

The mechanism is simple in concept: HDB buys back the “tail end” of the lease at an HDB-determined valuation; the owner keeps a shorter, fully paid-up lease that is calibrated to last beyond the youngest owner’s age 95. The proceeds first plug any shortfall in the owner’s CPF Retirement Account up to the prevailing Full Retirement Sum (or Basic Retirement Sum for couples, depending on cohort rules), then the remainder is paid out as cash.

Crucially, LBS is a retirement-income scheme, not a property cash-out scheme. The CPF top-up flows through to monthly CPF LIFE payouts for life — that is what makes LBS valuable. If the goal is purely to free up a lump sum, Right-Sizing or selling on the open market is usually the better route, which we cover later. For the retirement-income angle, see our CPF for Property Purchase guide and Singapore Property Tax 2026 guide.

Who Is Eligible for LBS in 2026?

Six tests determine LBS eligibility. All six must be satisfied for the application to proceed:

- Citizenship: at least one owner must be a Singapore Citizen.

- Age: all owners must be aged 65 years or older at the point of application. (CPF Retirement Age is currently 65.)

- Flat type: all HDB flat types are eligible — 2-room flexi, 3-room, 4-room, 5-room, executive, and 3Gen flats.

- Ownership: the flat must not be subject to an existing mortgage that exceeds the proceeds — LBS proceeds will first redeem any outstanding HDB or bank loan.

- Income: household income must not exceed S$14,000 per month (gross). Pension and CPF LIFE payouts count as income.

- Single property: the household must own only one property — the HDB flat in question. Owners of any other private residential or overseas property are not eligible.

If your situation is borderline on age or income, HDB’s Flat Portal provides an indicative LBS calculator. Note that the income test looks at average monthly household income over the prior 12 months, so a recent windfall or bonus does not immediately disqualify a household.

How HDB Calculates the Retained Lease

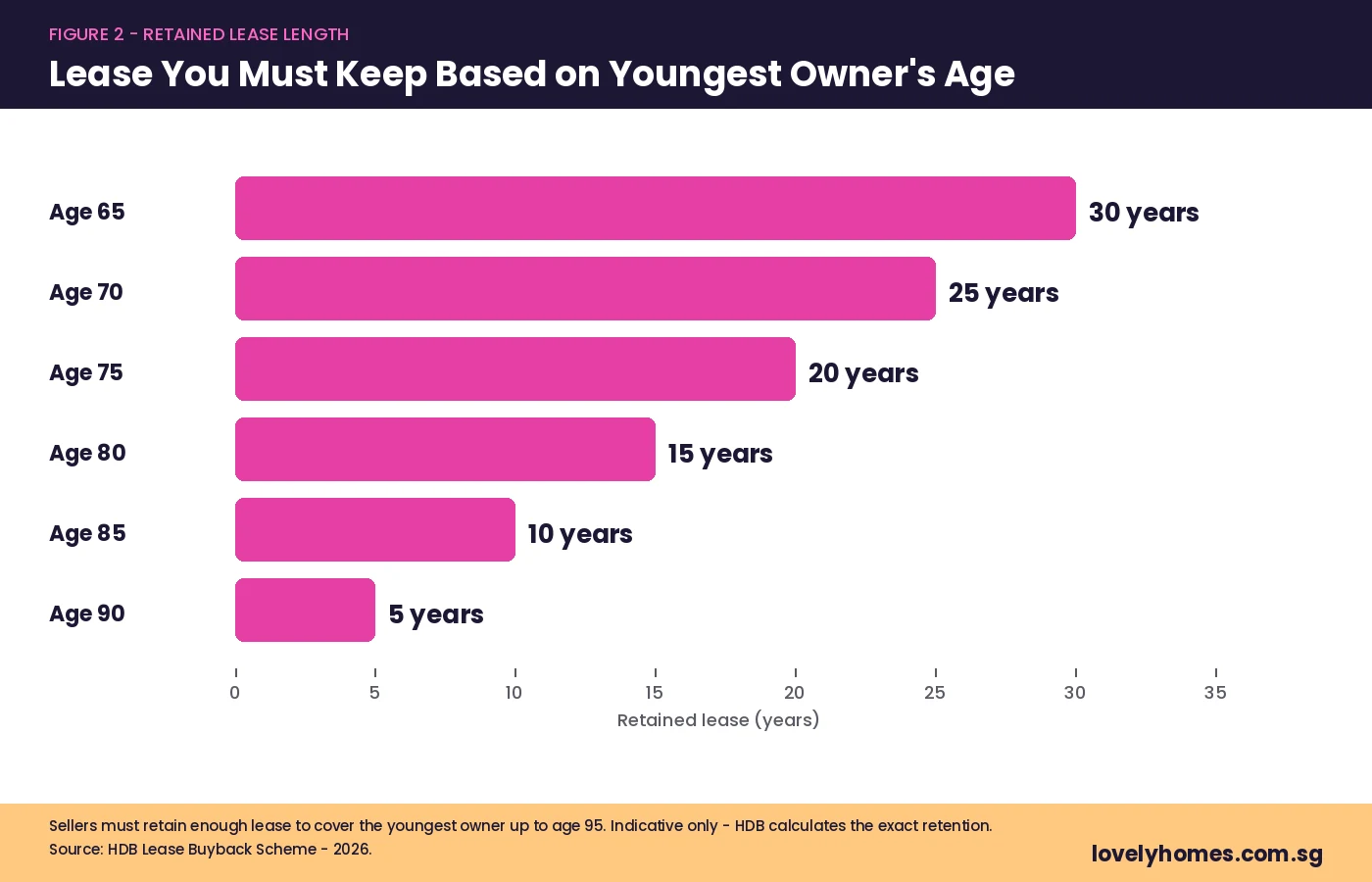

The single most important number in any LBS application is the retained lease. HDB sets it so that the youngest owner is covered up to age 95. In practical terms this means the older the youngest owner, the shorter the retained lease and the more lease you sell back to HDB. The figure below shows the typical retention by age for the youngest owner of the household.

For couples, the youngest owner’s age is what counts — even if one spouse is 80 and the other is 67, the household must retain at least 28 years of lease (covering the 67-year-old to age 95). Singles retain only enough lease for their own coverage to age 95, so they generally sell back more lease and receive larger proceeds.

The retained lease is non-negotiable: HDB will not allow households to retain less than the age-95 buffer, even if the household elects a shorter retention to receive more cash. This is by design — the policy intent is to ensure no senior runs out of housing tenure during their lifetime.

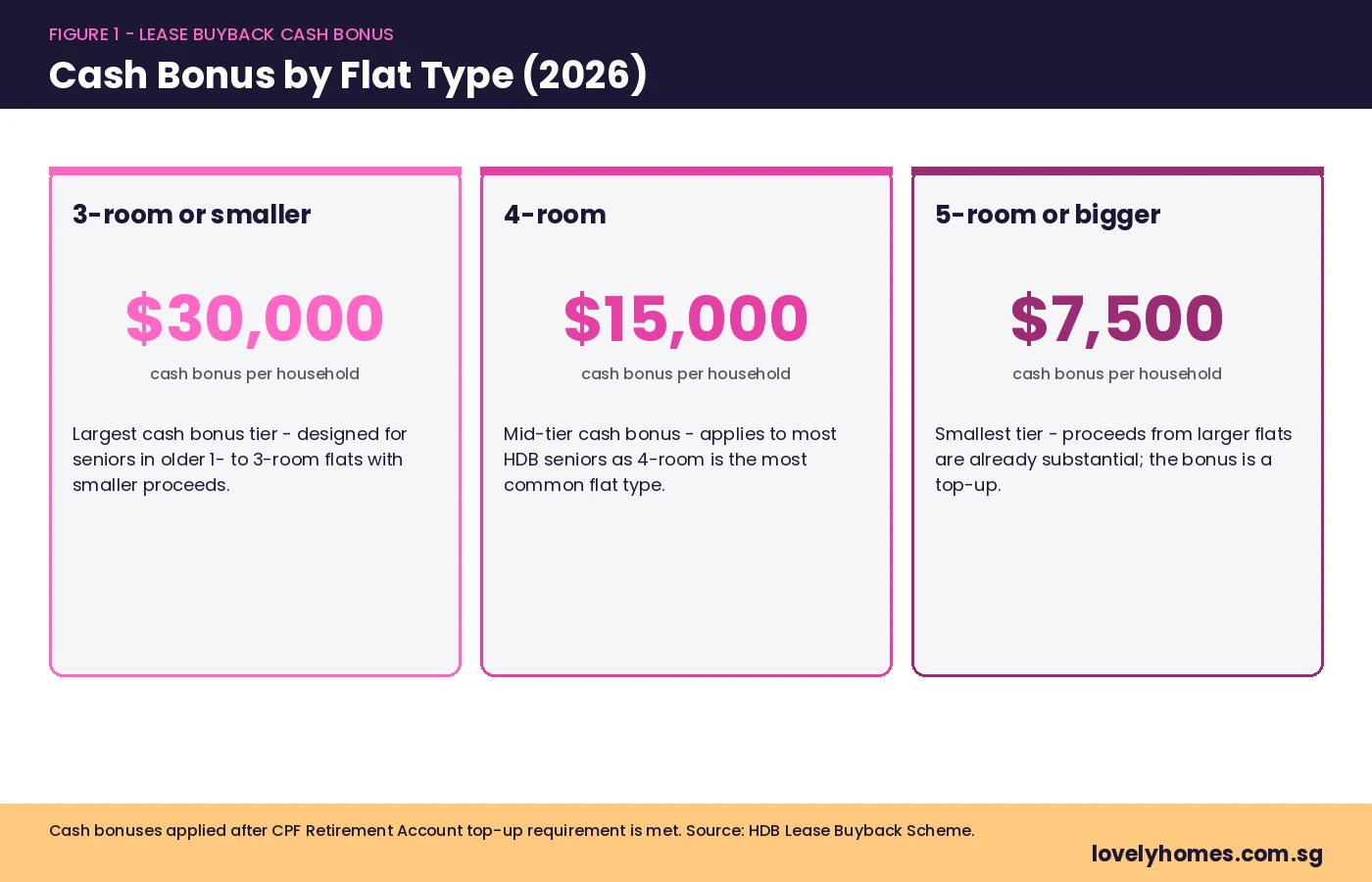

Cash Bonus Tiers by Flat Type

Once the household has met the CPF Retirement Account top-up requirement (more on this below), HDB pays a fixed cash bonus. The bonus tiers are deliberately weighted toward smaller flats — seniors in 1-, 2-, and 3-room flats receive a much larger bonus relative to their proceeds than seniors in 5-room or executive flats, where the proceeds are already substantial.

| Flat Type | Cash Bonus | Why Set This Way |

|---|---|---|

| 3-room or smaller (1- to 3-room, 2-room flexi) | S$30,000 | Tail-end-lease proceeds tend to be modest; a higher absolute bonus tilts the scheme toward lower-income retirees. |

| 4-room | S$15,000 | The most common HDB flat type and where most LBS applicants sit. Proceeds are substantial; bonus is mid-tier. |

| 5-room or bigger (5-room, executive, 3Gen) | S$7,500 | Proceeds are already largest in this tier — the bonus is more of a courtesy top-up. |

The bonus is paid only after the CPF Retirement Account top-up has been done. If the household has already met the prevailing retirement sum, the cash bonus is paid out fully and immediately along with any residual cash. If the proceeds are insufficient to meet both the CPF top-up and the bonus, HDB will still pay out the cash bonus — provided the senior has met the required retirement sum either through LBS proceeds alone or in combination with their existing CPF balance.

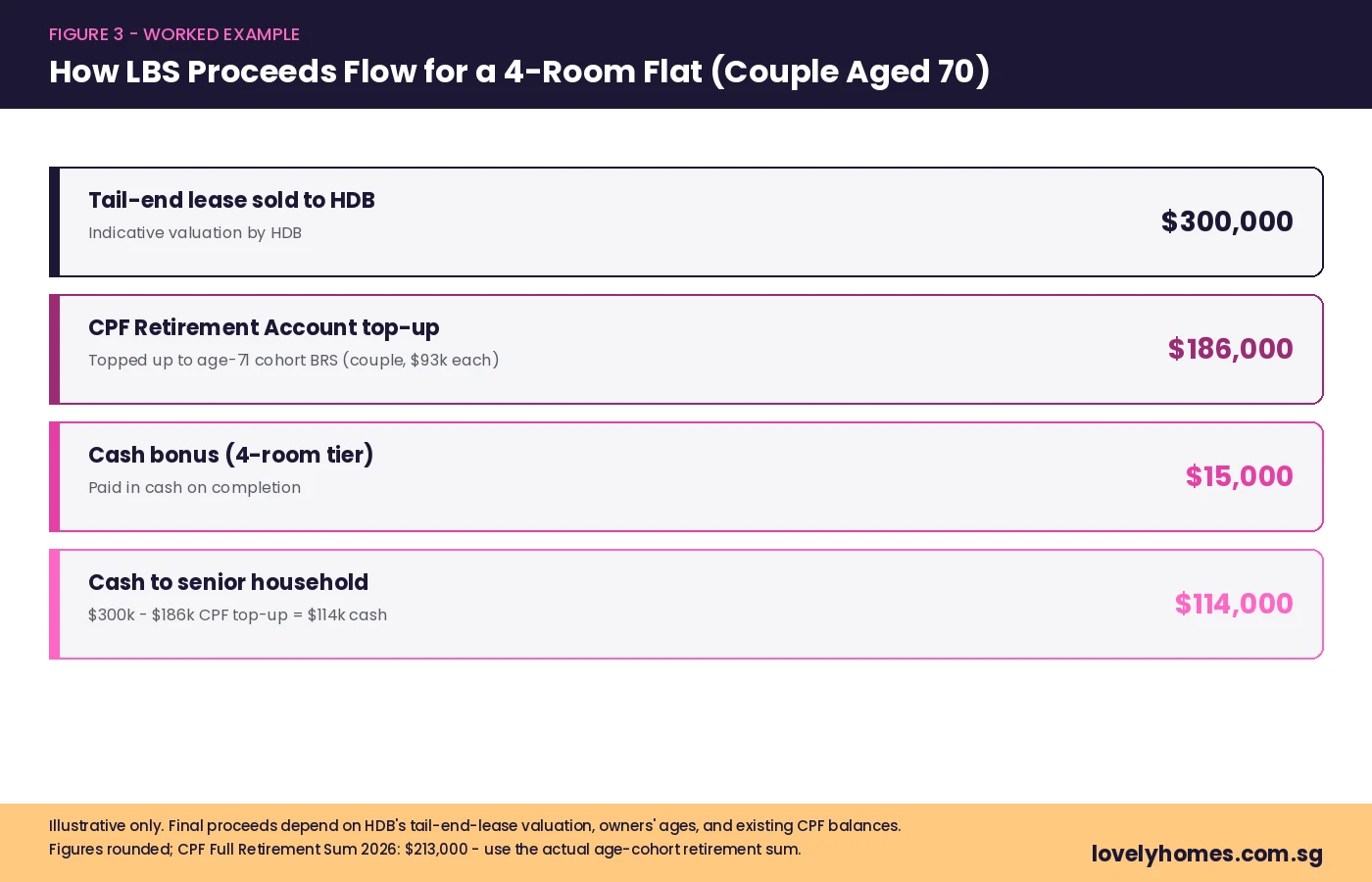

How Proceeds Flow — A Worked Example

The cleanest way to understand LBS is to walk a sample household through it. Take a Singaporean couple, both aged 70, living in a 4-room flat in Tampines bought in 1995. The flat’s remaining lease is roughly 68 years. HDB’s indicative valuation of the tail-end lease they will sell back is S$300,000.

Here is the cascade in plain English:

- Tail-end lease sold to HDB: S$300,000.

- CPF Retirement Account top-up: the couple must each be topped up to the prevailing retirement sum for their age cohort. In this example, that is roughly S$93,000 each, or S$186,000 in total.

- Cash bonus (4-room tier): S$15,000 paid in cash on completion.

- Cash payout: the residual after the CPF top-up is paid out as cash — here, S$300,000 − S$186,000 = S$114,000.

The total received by the couple is therefore approximately S$315,000 — S$186,000 of which goes into a CPF LIFE annuity that will pay them roughly S$1,200 to S$1,400 a month for life (depending on plan), and S$129,000 of which is in cash they can deploy as they wish (medical reserves, family support, simple savings). They keep living in the flat for the retained lease.

If the household’s existing CPF Retirement Account balances were already at or above the prevailing retirement sum at the point of application, the entire S$300,000 (less any compulsory CPF refund on the original purchase) would be paid as cash plus the S$15,000 bonus.

LBS vs Right-Sizing — Which Path Makes More Sense?

LBS is one of three main “monetisation paths” for senior HDB owners. The other two are Right-Sizing (selling the current flat and buying a smaller one, often qualifying for the Silver Housing Bonus) and a straight open-market sale (selling the flat outright and renting or moving in with family). Each has different tax, CPF refund, and lifestyle consequences.

| Dimension | Lease Buyback (LBS) | Right-Sizing (with SHB) | Open-Market Sale |

|---|---|---|---|

| Stay in current flat? | Yes — same flat, same neighbourhood | No — move to a smaller flat | No |

| Cash to household | Modest after CPF top-up; +S$7.5k–S$30k bonus | Larger lump sum + S$30k Silver Housing Bonus (subject to top-up) | Largest lump sum; subject to CPF refund + accrued interest |

| CPF LIFE income | Top-up to retirement sum boosts payouts | Top-up to retirement sum boosts payouts | No automatic top-up; voluntary deposit possible |

| Future bequest | Limited — lease ends with you; estate may receive only un-used lease balance value | Smaller flat passes to estate, subject to its remaining lease | Cash held in estate; flat is gone |

| Lifestyle disruption | None | Significant move — downsize and pack | Major — new home/lifestyle entirely |

| Renting permitted | Bedrooms only — not the whole flat | Subject to MOP rules on the new flat | No flat to rent |

For households that want to stay in the same neighbourhood, LBS is almost always the right answer. For households happy to move to a smaller flat (especially in a different town with lower prices), Right-Sizing typically yields more cash and a fully owned smaller flat that can be passed on to children. For broader monetisation strategy, see our How to Sell an HDB Flat 2026 and CPF Housing Grants 2026 guides.

Interaction with Other Senior Schemes

LBS does not exist in isolation. Three other schemes interact with it — and each has its own rules:

1. Silver Housing Bonus (SHB)

The Silver Housing Bonus pays seniors a cash bonus of up to S$30,000 for selling their existing property and buying a smaller one (3-room flat or smaller from HDB or resale). SHB is the Right-Sizing counterpart to LBS — you cannot claim both for the same flat in the same transaction. If the household uses LBS, they may still apply for SHB later if they subsequently move to a smaller flat (subject to the household’s eligibility at the time).

2. CPF LIFE Annuity

The proceeds from LBS that go into the CPF Retirement Account flow into the household’s CPF LIFE annuity. CPF LIFE pays a guaranteed monthly income for life, and is the lifetime-income engine that LBS feeds. Couples can choose Standard, Basic, or Escalating Plans — the choice affects the size and trajectory of monthly payouts, but does not change LBS proceeds.

3. ElderShield / CareShield Life

LBS does not interact with CareShield Life premiums directly, but the cash portion of LBS proceeds is sometimes used by seniors to pre-pay several years of CareShield Life or to fund integrated shield plan riders for hospital coverage. This is a sensible use of the cash portion for seniors without dependants.

How to Apply — Step by Step

- Use the HDB online calculator (HDB Flat Portal) to get an indicative quote of your proceeds, retained lease, and bonus.

- Attend an LBS information session at a HDB Branch or online. Counselling is mandatory before formal application.

- Submit the formal application via the HDB Flat Portal with the required documents (NRIC, marriage certificate, latest CPF Retirement Account statement, and proof of income).

- HDB issues a Letter of Offer with the final retained-lease length, CPF top-up amount, cash bonus, and cash payout figure.

- Sign the Lease Buyback Agreement — once signed, HDB administers the CPF top-up and pays the cash bonus + cash payout.

- Continue living in the flat for the retained lease. You remain responsible for service & conservancy charges, utilities, and property tax.

The full application typically takes 2–4 months from submission to completion. During the application period, you cannot transact the flat (sell, sublet whole, or remortgage) and HDB will hold your title until completion.

What Happens at the End of the Retained Lease?

If the youngest owner outlives the retained lease (i.e. lives past 95), the household must vacate. HDB has flexibility to assist genuine cases — in practice this is rare because the retained-lease formula is conservative (covers to age 95 from current age, then HDB has discretionary buffer). Where surviving spouses or family members continue occupying the flat past the retained lease, HDB has supported temporary accommodation arrangements on a case-by-case basis, including a short Top-Up Lease for households who genuinely need to extend.

If both owners pass away before the retained lease ends, the unused lease balance has residual value that can pass to the estate — HDB will repurchase it from the estate at a HDB-determined value. This is one of the under-appreciated aspects of LBS: it is not pure forfeiture, just sale of the portion you do not need.

Pros and Cons of LBS

| Advantages | Disadvantages |

|---|---|

| No need to move — same flat, same neighbourhood, same neighbours | Most proceeds go to CPF top-up — less liquid cash than open-market sale |

| Boosts CPF LIFE monthly payouts for life | Reduces estate value — tail-end lease no longer yours |

| Cash bonus on top of proceeds (S$7.5k–S$30k) | Cannot rent out the whole flat post-LBS (bedroom rental allowed) |

| No selling costs, no commission, no agent fees | Income ceiling and single-property test exclude wealthier seniors |

| Counselling is mandatory — reduces poor decisions | If you outlive the retained lease, you may need to vacate |

What Might Come Next

Two policy directions are worth watching. First, with Singapore’s rapidly ageing population — one in four residents will be aged 65 and above by 2030 — expect HDB to keep the LBS framework generous and to consider further age tier adjustments. There has been quiet discussion in policy circles about lowering the LBS minimum age below 65 in step with future CPF reforms, though no announcement has been made.

Second, the income ceiling of S$14,000 per month has remained unchanged for several years. As wages have risen, an increasing share of HDB seniors have been priced out by the income test. A future tweak that lifts the ceiling or moves to a means-test on assets rather than income would broaden LBS reach. None of this is policy as of 29 April 2026 — it is editorial speculation only. Always check the HDB LBS page for the live position.

Frequently Asked Questions

Can I apply for LBS if I still have a mortgage on the flat?

Yes. The LBS proceeds will first redeem the outstanding mortgage (HDB or bank). The remainder then flows through the standard CPF top-up and cash payout cascade. If the proceeds are not enough to redeem the mortgage in full, HDB will not approve the LBS application — the household must first reduce or pay off the mortgage from other sources.

Can I rent out the whole flat after LBS?

No. Renting out the whole flat is not allowed because the policy intent of LBS is for the senior owner to continue living there. You may rent out individual bedrooms while continuing to occupy the flat as your principal residence, subject to the standard HDB subletting rules — see our Tenancy Agreement Singapore 2026 guide.

What happens if both my spouse and I outlive the retained lease?

The retained-lease formula is calibrated to cover the youngest owner up to age 95, so this is a rare scenario. Where it does occur, HDB has historically supported case-by-case extensions and rehousing assistance. Engage HDB well before the retained lease ends to discuss options.

Is LBS reversible? Can I cancel after signing?

No. Once the Lease Buyback Agreement is signed and proceeds are disbursed, the transaction is final. This is why HDB requires mandatory counselling and an information session before applying — to ensure households make an informed decision.

Can I use LBS if I own a holiday home overseas?

No. The single-property test counts overseas residential property too. You must dispose of any other residential property (in Singapore or abroad) before applying for LBS.

How does LBS affect property tax on the flat?

You remain the registered owner of the flat for the retained lease, so property tax continues to be billed to you under owner-occupier rates (HDB flats benefit from very low or zero owner-occupier annual property tax). See our Singapore Property Tax 2026 guide for details.

If my children move in to take care of me, do they have any rights?

No. The retained lease belongs to the original owners. Children moving in to care for the senior do not acquire title or lease rights. After the retained lease ends, they would not be entitled to remain in the flat. Households where this is a likely scenario should consider Right-Sizing instead, as the smaller resale flat passes to the estate.

Related Articles

- CPF Housing Grants Singapore 2026: The Complete Guide

- CPF Housing Grant Singapore 2026: EHG, Family Grant & Proximity Grant

- CPF for Property Purchase Singapore 2026

- How to Sell Your HDB Flat Singapore 2026 Timeline

- Singapore Property Tax 2026: Owner-Occupier vs Investor Rates

- Tenancy Agreement Singapore 2026: Landlord & Tenant Guide

- HDB Resale Levy Singapore 2026

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. HDB Lease Buyback Scheme rules, retirement sums, and CPF LIFE payout structures change over time. Always verify the live position on the HDB Lease Buyback Scheme page, the CPF Board, and consult a HDB Branch counsellor or licensed financial adviser before making a decision. Sources: HDB, CPF Board, MAS, SingStat.

0 Comments