Buying your first home in Singapore is the single largest financial decision most people ever make. It has regulatory gates (HFE, TDSR, MSR), financial gates (downpayment, stamp duty, renovation), and procedural gates (OTP, resale application, completion). This 2026 walkthrough moves through all eight gates in the order you will actually encounter them.

If you are still deciding between flat types, read our comparison of BTO, resale and EC first. This article assumes you know roughly what you want to buy, and are ready to work out how.

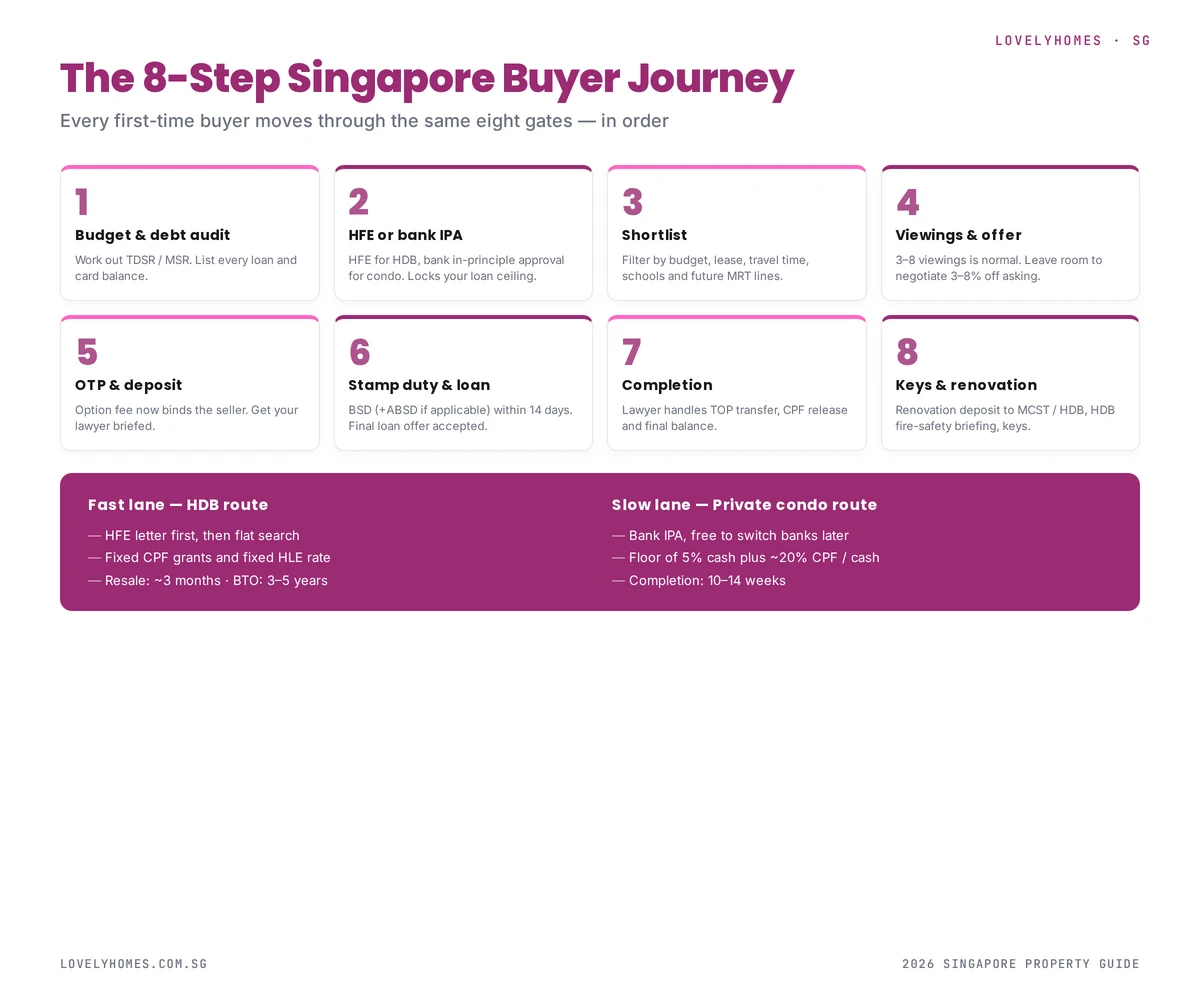

Quick Answer — The 8 Gates

Budget and debt audit — work out TDSR and MSR.

HFE letter or bank IPA — locks your loan ceiling.

Shortlist and compare — narrow to 3–5 options.

Viewings and offer — expect 3–8 viewings before firming.

OTP and option fee — commits both parties.

Stamp duty and loan drawdown — the money phase.

Completion — legal transfer and final balance.

Keys and renovation — you own a home.

Every Singapore first-time buyer moves through the same eight gates — in order.

Gate 1: Budget and Debt Audit

Before you look at a single listing, sit down with your household income and debt obligations. Two ratios govern what banks will lend you:

TDSR 55%: All monthly debts (existing loans, minimum credit-card payments, new home loan) must be at or below 55% of gross income.

MSR 30%: For HDB and EC buyers only — home loan alone is capped at 30% of gross income.

With the maths squared away, you need a financing lock:

HDB route: Apply for an HFE letter via the HDB Flat Portal. Takes ~2 weeks. Valid 6 months.

Private condo route: Apply for Bank IPA (in-principle approval). Typically 3–5 working days. Valid 30 days.

An HFE or IPA is the document a seller or developer will ask to see before engaging seriously. It also tells you how much you can actually borrow, which constrains your flat search.

Gate 3: Shortlist and Compare

Use the HDB Resale Portal (for HDB), 99.co, PropertyGuru, and our own LovelyHomes listings (for private) to narrow a shortlist. Criteria that matter:

Transport: Walking distance to MRT, commute to work, future Cross Island Line / Jurong Region Line stations.

Schools: 1km and 2km catchment for primary schools if you have young children.

Remaining lease (HDB): Affects loan tenure and CPF usage.

Maintenance fees (private): Check the strata table for the monthly MCST fee.

Gate 4: Viewings and Offer

Expect 3–8 viewings before you firm on a unit. At each viewing, check:

Water pressure and drainage (run taps, flush toilets)

Ceiling for water staining (upstairs leaks)

Door frames for termite damage

Window seals for water ingress

Electrical outlet locations and DB box condition

Noise during the day and evening

When you are ready to offer, recognise that asking prices are typically 3–8% above the agreed-on transaction price for HDB resale, and 5–10% for private condos. Start below asking.

Gate 5: OTP and Option Fee

Once price is agreed, the seller issues the Option to Purchase:

HDB resale: S$1,000 option fee (fixed by HDB). 21 days to exercise.

Private resale: 1% of purchase price. 14 days to exercise.

New launch condo: 5% on booking, then S&P Agreement within 8 weeks.

This is the commitment point. Engage a conveyancing lawyer during this window, and if buying private with a bank loan, lock the loan offer now.

Gate 6: Stamp Duty and Loan Drawdown

Within 14 days of OTP exercise, you must pay Buyer Stamp Duty via IRAS. If ABSD applies (second or subsequent property, PR, or foreigner), it is due at the same time. Your lawyer will handle the filing and remittance.

Your bank will now process the loan in earnest. They will send a valuer to the property, finalise the loan offer, and coordinate with your lawyer for completion.

Gate 7: Completion

For HDB, completion happens at the HDB Hub, typically 8–12 weeks after the resale application. For private, it happens at your lawyer’s office, typically 8–12 weeks after OTP exercise. At completion:

You pay the final cash balance

Your CPF is debited for the CPF portion

Your bank disburses the loan

The seller receives the proceeds

Legal title transfers to you

You receive the keys

Gate 8: Keys and Renovation

Congratulations — you own a home. From this point:

Apply for HDB renovation permit if structural changes (hacking, plumbing relocation).

Attend fire-safety briefing (HDB only) before renovation begins.

Budget realistically: 4-room HDB renovation runs S$50,000–S$80,000 on average in 2026.

MOP clock starts (HDB and EC) from the completion date.

Worked Example: S$780,000 BTO Flat, First-Timer Couple

A married couple, both SCs, combined monthly income S$9,500, buying a 4-room BTO in Tengah at S$380,000 (Standard flat):

Component

Amount

Purchase price

S$380,000

CPF Housing Grant (EHG)

S$55,000

Effective price

S$325,000

HDB loan @ 75%

S$244,000

Downpayment (cash + CPF)

S$81,000

Of which minimum cash

S$16,300 (5%)

Buyer Stamp Duty

S$5,700

Legal fees

~S$500

Minimum cash upfront

~S$23,000

Monthly HDB loan (25 yr, 2.6%)

~S$1,108

Against a household income of S$9,500, this represents an MSR of 11.7% — well inside the 30% limit. TDSR is also comfortable if there are no other debts.

Common Mistakes First-Timers Make

Viewing first, financing second. Without an HFE or IPA, you cannot make a binding offer.

Forgetting renovation cost. Budget S$50k–S$100k. It is often the second-largest cost after the downpayment.

Ignoring CPF accrued interest. The CPF you use will need to be returned with ~2.5% annual compounding when you sell. See our CPF guide.

Choosing HDB Legal for complex cases. HDB Legal is great for straightforward cases but offers no flexibility if your situation has quirks (trust ownership, divorce partial transfer, etc).

Maxing the loan tenure. The longest tenure minimises instalments but means vastly more interest over time.

FAQ — First-Time Buyer 2026

How long does the whole process take from first viewing to keys?

For HDB resale: 4–6 months. For private condo: 3–5 months. For BTO: add the 3–5 year build wait after selection.

Can I use my parents’ CPF to buy?

Yes, if they are named as co-applicants or under the Essential Occupier scheme. Their contribution becomes a charge on the flat like any other CPF usage.

Should I choose HDB loan or bank loan?

HDB loan: fixed 2.6% rate, forgiving on TDSR stress test, flexible on prepayment. Bank loan: potentially lower floating rates but exposed to SORA volatility. See our fixed vs floating guide.

Do I need a lawyer for my first home purchase?

Yes. For HDB, the HDB Legal service is low-cost. For private, you will need an external conveyancing firm. Expect to pay S$2,000–S$3,500 including disbursements.

What grants am I eligible for as a first-timer?

CPF Housing Grant (up to S$80k for families depending on income), Enhanced CPF Housing Grant, and Proximity Housing Grant if living near or with parents. Your HFE letter will compute your exact entitlement.

Disclaimer: Regulations, rates and grants change over time. Verify current rules with HDB, your bank, and IRAS before committing. Consider engaging a qualified financial advisor for tax and CPF planning on large purchases.

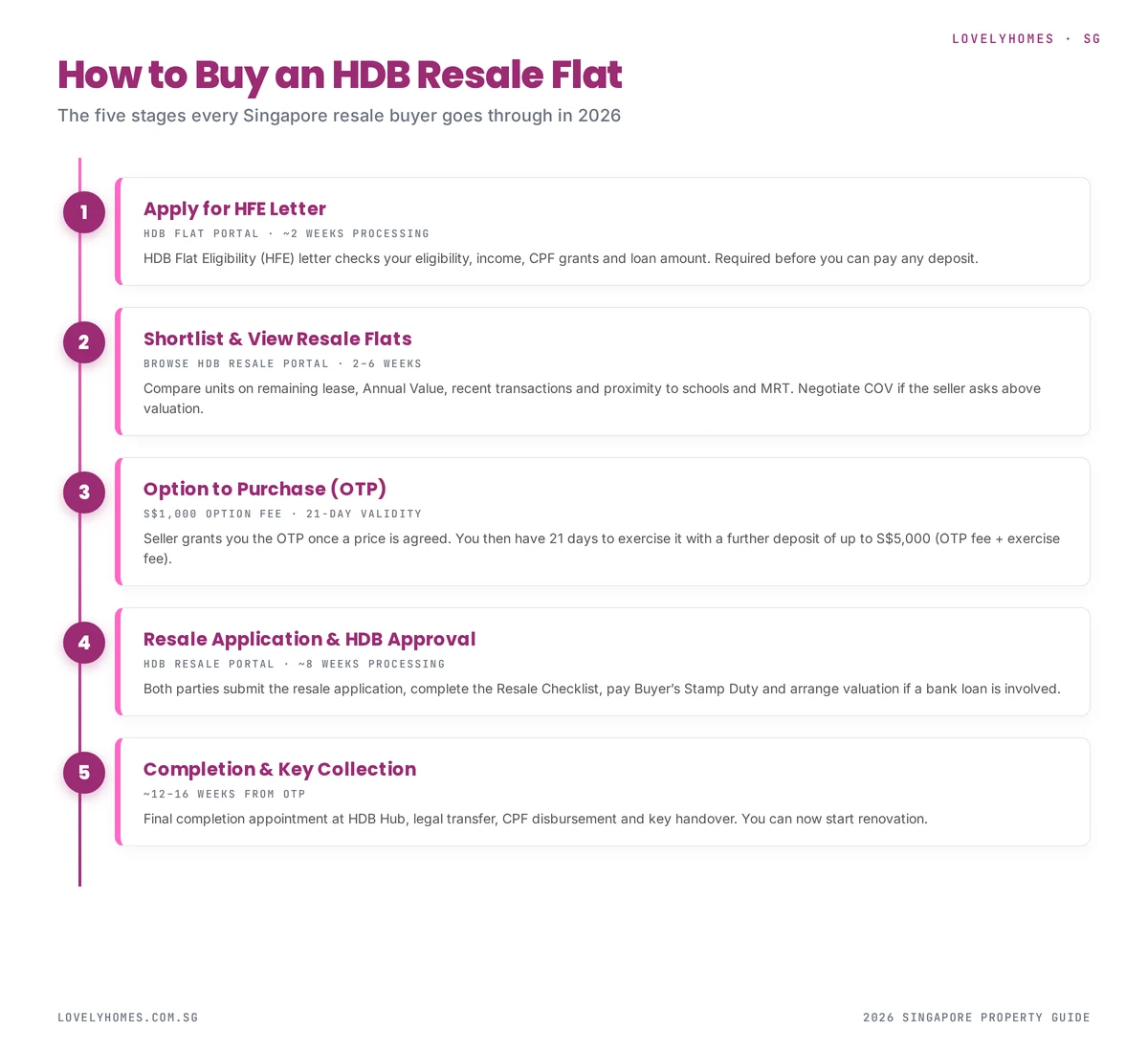

Buying an HDB resale flat in Singapore in 2026 is a process with clear, legally-defined stages. Miss one, and the deal either stalls or collapses entirely. This guide walks you through every step in the exact order you will actually encounter it — from securing your HDB Flat Eligibility (HFE) letter to collecting the keys.

For the official rules, refer to the HDB Resale Buying page. This article explains what those rules mean in practice and how the numbers add up for a typical 2026 buyer.

Quick Answer — The HDB Resale Buying Process

Apply for HFE letter on the HDB Flat Portal (~2 weeks processing).

Shortlist and view flats (typically 2–6 weeks).

Negotiate, then receive the OTP from the seller (S$1,000 option fee).

Exercise the OTP within 21 days with the exercise fee (up to S$4,000 more).

Submit the resale application on the HDB Resale Portal.

Complete the purchase at the HDB Hub appointment and collect keys.

Total elapsed time: typically 12–16 weeks from OTP to keys.

The five stages of buying an HDB resale flat, from HFE letter to keys.

Step 1: Apply for Your HFE Letter

The HDB Flat Eligibility (HFE) letter is the gating document for any HDB purchase. It confirms three things in a single statement: whether you are eligible to buy, how much CPF housing grant you qualify for, and the maximum HDB loan you can take.

You apply through the HDB Flat Portal using Singpass. The portal will check your household income, ages, citizenship, and existing property holdings. Processing usually takes around two weeks — but longer if HDB needs clarification on income or existing flat ownership.

The HFE letter is valid for six months, and you cannot exercise any OTP without one. Budget for your HFE to be ready before you start serious viewings — you will see sellers, and agents expect you to have it lined up.

What the HFE letter tells you

Whether your household meets the eligibility conditions (at least one SC, under the S$14,000 monthly household income ceiling, no overlapping private-property ownership).

The exact CPF Housing Grants you qualify for (CPF Housing Grant, Enhanced CPF Housing Grant, Proximity Housing Grant).

The maximum HDB Concessionary Loan you can take, based on TDSR and MSR.

The minimum cash required at OTP and exercise stages.

Step 2: Shortlist Flats and Conduct Viewings

Once you have your HFE letter in hand, you can begin serious viewings. The HDB Resale Portal and third-party sites (PropertyGuru, 99.co, ourselves at LovelyHomes) let you filter by town, flat type, remaining lease and recent transacted price.

What to actually evaluate at a viewing

Remaining lease: Directly affects your maximum loan tenure and CPF usage. Anything under 60 years of remaining lease starts restricting grants and CPF usage significantly.

Condition of the flat: Look past the paint. Check ceilings for water marks (upstairs leaks), windows for water ingress, and door frames for termite damage.

Ethnic quota status: Your ethnic group must be under the block-level EIP cap. Ask the agent if the block is “open” for your group.

Noise and dust: Traffic, MRT, and construction noise. Visit twice — once at peak hour, once in the evening.

Ownership history: The agent should be able to confirm the number of previous owners and whether any structural alterations were made without HDB approval.

Step 3: Negotiate the Price and Receive the OTP

Once you and the seller agree on a price, the seller grants you the Option to Purchase (OTP). The option fee is fixed by HDB at S$1,000, paid on the spot. This buys you the exclusive right to purchase that flat at the agreed price for 21 calendar days.

The OTP is a legally binding document for the seller during those 21 days — they cannot sell to anyone else. But you, the buyer, can walk away by simply not exercising the option. You forfeit the S$1,000 but have no further obligation.

Cash-Over-Valuation (COV) in 2026

If the agreed price exceeds HDB’s official valuation, the gap must be paid in cash — never from CPF or loan. This is Cash-Over-Valuation, and it is firmly back on the table in 2026’s tight resale market. Budget for it if you are bidding on a popular estate or a high-floor unit. See our full COV guide for negotiation tactics.

Step 4: Exercise the OTP

Within the 21-day window, you exercise the OTP by paying the exercise fee. The option fee plus exercise fee cannot exceed S$5,000 combined — typically structured as S$1,000 option + S$4,000 exercise. At this point the sale becomes unconditional.

In the same 21 days, you should:

Engage a conveyancing lawyer (HDB’s in-house Legal & Claims Registry is a low-cost option for straightforward cases).

If taking a bank loan, finalise your loan offer and submit it for valuation.

Prepare the Buyer’s Stamp Duty (BSD) — due within 14 days of OTP exercise.

Step 5: Submit the Resale Application

Once the OTP is exercised, both parties log into the HDB Resale Portal and submit the resale application jointly. The portal walks you through the Resale Checklist, financial plan, and any declarations.

You will pay stamp duty, agree on the completion timeline, and nominate your solicitor. Your CPF refund to the seller, the loan disbursement and the final cash shortfall are all calculated at this point. HDB aims to process the resale application within eight weeks.

Typical fees at application stage

Resale application fee: S$80 (1-room / 2-room flats) or S$120 (3-room and above).

Buyer Stamp Duty (BSD): Graduated — 1% on first S$180k, 2% on next S$180k, 3% on next S$640k, 4% thereafter. On a S$600k resale, BSD comes to S$12,600. See our BSD guide for the full maths.

Legal fees: S$350–S$600 via HDB Legal, S$1,800–S$3,000 via a private conveyancing firm.

Step 6: Completion and Key Collection

About twelve to sixteen weeks after you first exercised the OTP, you will attend the completion appointment at HDB Hub. Both parties sign the legal transfer documents, CPF disbursements are triggered, your bank or HDB loan is drawn down, and you receive the keys.

From this moment, the flat is legally yours. Your MOP clock starts ticking from this date — see our MOP guide for what that means going forward.

Worked Example: Buying a S$620,000 4-Room Resale Flat

Let’s walk through a realistic 2026 purchase. A young couple, both Singapore Citizens and first-time buyers, buy a 4-room resale flat in Sengkang at S$620,000 — S$30,000 above HDB’s valuation of S$590,000.

Component

Amount

Purchase price

S$620,000

HDB valuation

S$590,000

COV (cash)

S$30,000

HDB loan @ 75% of valuation

S$442,500

Cash + CPF downpayment (25% of valuation)

S$147,500

Buyer Stamp Duty

S$13,200

Legal fees (HDB route)

~S$500

Minimum cash needed upfront

~S$60,000

The couple might qualify for an Enhanced CPF Housing Grant of up to S$80,000 depending on their combined income, which offsets a large chunk of the downpayment. See our CPF for property guide for how the grants flow into the purchase.

Common Mistakes That Delay or Kill the Deal

No HFE letter in hand: You cannot exercise an OTP without one. Plan at least three weeks of buffer before you start offering.

Underestimating COV: It has to come from cash savings, not CPF. Many deals collapse at OTP because buyers find their cash short.

Ignoring the ethnic quota: Your offer can be accepted, only to have HDB reject the resale application because the block is full for your group.

Not checking structural alterations: Unauthorised renovations (load-bearing wall removal, unpermitted window grilles) are the buyer’s problem after completion.

Valuation shock: If the valuation comes in below the purchase price, the cash shortfall must be covered by you — not CPF.

FAQ — HDB Resale Buying 2026

How long does the entire HDB resale process take?

Typically 12–16 weeks from OTP exercise to keys. Add another 2–6 weeks for your flat search, and 2 weeks for the HFE letter.

Can I use CPF to pay the option fee?

No. The S$1,000 option fee and the up-to-S$4,000 exercise fee both come from cash. CPF Ordinary Account funds only flow in at the resale-application stage.

What happens if I cannot exercise the OTP in time?

You forfeit the S$1,000 option fee. The seller is then free to grant the OTP to someone else.

Do I need a property agent to buy HDB resale?

No. HDB’s Resale Portal is designed to let buyers and sellers complete the process without an agent, though you are welcome to use one. Total agent commission on the buyer side is typically 1% of the purchase price.

Can I back out after I exercise the OTP?

Only with the seller’s agreement, and you would likely forfeit both the option and exercise fees (up to S$5,000). HDB does not have a “cooling-off” period for resale buyers once OTP is exercised.

Disclaimer: This is general guidance, not legal advice. Rules, fees and grant amounts change periodically — always verify with HDB directly before committing. Consult a qualified conveyancing lawyer for your specific purchase.