Cash-Over-Valuation (COV) in Singapore HDB Resale: 2026 Guide

Cash-Over-Valuation — COV — is the gap between the price a Singapore HDB resale buyer agrees to pay and the official valuation HDB assigns to the flat. That gap is paid entirely in cash, on top of the 5% deposit and any loan shortfall. For the first time since 2014, COV is measurably back in Singapore’s hotter resale estates — and most buyers have no mental model for it.

This 2026 guide explains exactly how COV arises, why HDB redesigned the valuation process to kill it in 2014, why it came back, and how to negotiate it down when you are sitting across the table from a seller’s agent. For the official valuation process, see the HDB resale valuation page.

Quick Answer — COV at a glance

- COV = offer price − HDB valuation. If positive, the difference is payable in cash only.

- No CPF allowed. You cannot draw CPF OA to pay COV.

- No loan allowed. Banks and HDB cap their loans at LTV applied to valuation, not to price.

- On top of: 5% cash deposit, any BSD and ABSD, and any shortfall between loan quantum and valuation.

- Typical 2026 COV in hot estates: S$20,000–S$80,000 in Queenstown, Bukit Merah, Tiong Bahru.

How COV Arises

HDB resale purchases follow a fixed sequence: buyer and seller agree on a price; buyer pays a S$1,000 Option Fee; HDB conducts its valuation; buyer exercises the OTP within 21 days with a further 4% cash Option Exercise Fee. The valuation comes after the price agreement.

If the agreed price is higher than HDB’s valuation, the buyer has a choice: abandon the option (losing S$1,000) or proceed and pay the gap in cash. That gap is COV.

A Worked Example

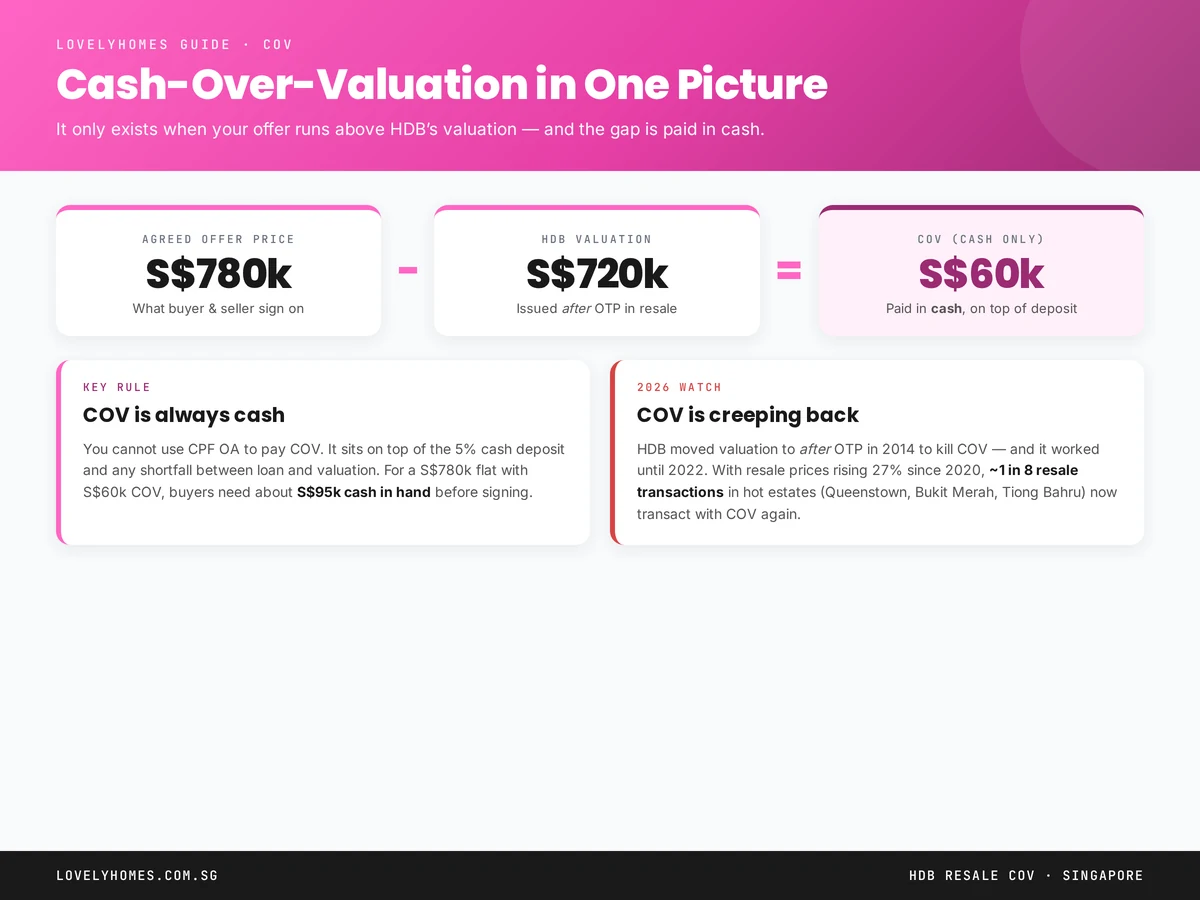

A couple agrees to buy a 4-room flat in Queenstown for S$780,000. HDB valuation comes back at S$720,000.

- COV: S$780,000 − S$720,000 = S$60,000 cash.

- 5% cash deposit (1% Option Fee + 4% Exercise Fee on purchase price): 5% × S$780,000 = S$39,000.

- Loan ceiling: HDB loan at 75% LTV on valuation = 75% × S$720,000 = S$540,000.

- Downpayment (25%) on valuation: 25% × S$720,000 = S$180,000 from CPF or cash.

- Loan shortfall: loan only covers S$540,000; purchase price is S$780,000 — shortfall of S$240,000 covered by downpayment (S$180,000) + COV (S$60,000).

Total cash required (excluding stamp duty): 5% deposit + COV = S$39,000 + S$60,000 = S$99,000. BSD of about S$17,400 must also be paid (reimbursable from CPF OA).

Why COV Was “Killed” in 2014

From 1994 to 2014, HDB valuations were issued before buyers made offers. Agents advertised a flat with both the valuation and the asking COV — e.g. “valued at S$500k, asking S$550k (S$50k COV).” This framing normalised COV as a negotiated headline number and fed a runaway COV culture.

In March 2014, HDB reversed the sequence: buyers agree a price first, then HDB values the flat. With buyers no longer able to advertise or openly negotiate COV, the market default moved to “price at valuation” and COV collapsed to zero on most transactions for nearly a decade.

Why COV Is Back in 2026

Resale prices rose 27% between 2020 and 2025 on the HDB Resale Price Index. HDB’s own valuations are based on a 6-month trailing transaction window — which means when prices rise fast, valuations lag the market. In a hot estate, an agent can credibly point to last-week comparables at S$800k while HDB’s valuation, anchored to six-month-old evidence, comes in at S$740k.

The structural ingredients for COV are back:

- Supply constraint: MOP release volumes below long-term averages.

- Premium locations: mature estates near MRT and international schools see thinner supply and bigger price-to-valuation gaps.

- Cash-heavy buyer pools: multi-generational households and HDB upgraders returning to buy smaller units have cash on hand to pay COV.

In Q4 2025, HDB data showed roughly 1 in 8 resale transactions with measurable COV, concentrated in Queenstown, Bukit Merah, Tiong Bahru, Toa Payoh, and Kallang/Whampoa. Two years earlier the number was closer to 1 in 30.

How to Negotiate COV Down

Sellers asking for COV have real competition. Use these levers:

- Pull recent transaction comparables. HDB Resale Portal publishes all resale transactions with price, flat type, floor range and storey. If the asking price is above the 90th percentile for comparable flats in the same block, push back with evidence.

- Request HDB valuation before exercise. The valuation is issued to you after the OTP is granted. If the gap is unacceptable, you have 21 days to walk away and lose only the S$1,000 Option Fee.

- Time your viewing. Sellers under pressure (downgrading, emigrating, selling to fund a BTO completion) drop COV asks fastest. Ask the agent what the seller’s next move is.

- Offer a smooth completion. Sellers often trade COV against completion certainty — pre-approved loan, short exercise window, willingness to extend for them to buy their next place.

- Walk away. On 2 of every 3 COV asks in 2026, the next buyer in the pipeline pays less or at valuation. Patience is priced.

When COV Is Actually Worth Paying

COV is not always irrational. Sometimes it reflects real scarcity that will not reverse:

- Rare floor plate. A high-floor corner unit with panoramic view and cross-ventilation in a mature estate.

- Zero-renovation condition. Move-in-ready flats save S$40k–S$80k in renovation and 3–6 months of rent elsewhere.

- Family proximity. Living near parents for childcare or caregiving has a legitimate non-market value.

The rule of thumb: if the COV is less than 2% of the purchase price and the trade-offs are non-replicable, paying is defensible. Above 5% COV is rarely justified.

Frequently Asked Questions

Is COV allowed for BTO or EC purchases?

No. COV only appears in HDB resale transactions where a valuation is issued separately from the price. BTO flats are priced directly by HDB; ECs are priced by developers. Both settle on price and never encounter a valuation gap.

Can the seller accept my offer at or below valuation?

Yes. Many transactions settle at valuation with zero COV. The seller’s agent may push back, but the buyer ultimately chooses whether to pay COV.

What happens if HDB undervalues the flat and I walk away?

You forfeit the S$1,000 Option Fee and the 21-day exercise window lapses. No other penalty.

Can I request a second valuation?

HDB valuations are final for the purpose of that transaction. You cannot appeal or request a second opinion — you must walk away and try a different flat.

Does the seller benefit from a higher COV?

Yes, directly. Every dollar of COV goes to the seller in cash at completion. This is why agents representing sellers push for higher COV asks in a tight market.

What to Do Next

- HDB Buying Guide — the full resale process end to end.

- TDSR & MSR 2026 — because MSR, not LTV, is usually the binding loan limit for HDB buyers.

- BSD Singapore 2026 — stamp duty on the purchase price, including any COV component.

Disclaimer: This guide is general information, not financial advice. HDB rules and valuation practice are subject to change. Verify current rules at hdb.gov.sg.