The Dunearn Road Government Land Sales (GLS) tender closed on 28 April 2026 with the Wing Tai Holdings and Metro Holdings joint venture submitting the top bid of S$533 million — equivalent to S$1,625 per square foot per plot ratio (psf ppr). Six developer bids contested the site, signalling sustained appetite for prime District 11 freehold-equivalent precincts despite the wider market’s cautious tone.

The result extends the steady price discovery in Bukit Timah Turf City — a precinct URA has signalled as a long-term residential growth area, anchored by Sixth Avenue MRT, the Bukit Timah Nature Reserve, and the Bukit Timah Plaza retail district. For buyers tracking the next CCR new launch, this tender frames the indicative pricing band for what is likely to launch in late 2027.

Quick Answer — Dunearn Road GLS at a glance

- Tender closed: 28 April 2026

- Top bid: S$533 million by Wing Tai Holdings + Metro Holdings JV

- Land rate: S$1,625 psf ppr

- Number of bids: 6 — strongest contest in the precinct so far

- Site size: 19,042 sqm; ~330 residential units + 1,400 sqm commercial

- Tenure: 99-year leasehold

- Implied breakeven: ~S$2,650 psf; indicative launch psf above S$3,000

- Expected launch: late 2027, subject to URA approval

What Happened — A Six-Bid Contest in District 11

URA released the Dunearn Road site on the 1H 2026 GLS Confirmed List in December 2025, with the tender closing on 28 April 2026. The site sits within the Bukit Timah Turf City precinct — a long-tail residential growth area that the Master Plan rezoned from racing-club use to mixed residential several years ago.

Six developer groups bid for the parcel. The Wing Tai Holdings and Metro Holdings joint venture — bidding through Winrich Investment Pte Ltd and Metrobilt Construction Pte Ltd — clinched the site with a S$533 million top bid, equivalent to S$1,625 psf ppr on the maximum allowable gross floor area. The runner-up bid is understood to have come within roughly 6% of the top, indicating a tightly contested tender rather than a one-developer outlier.

How the Land Rate Compares

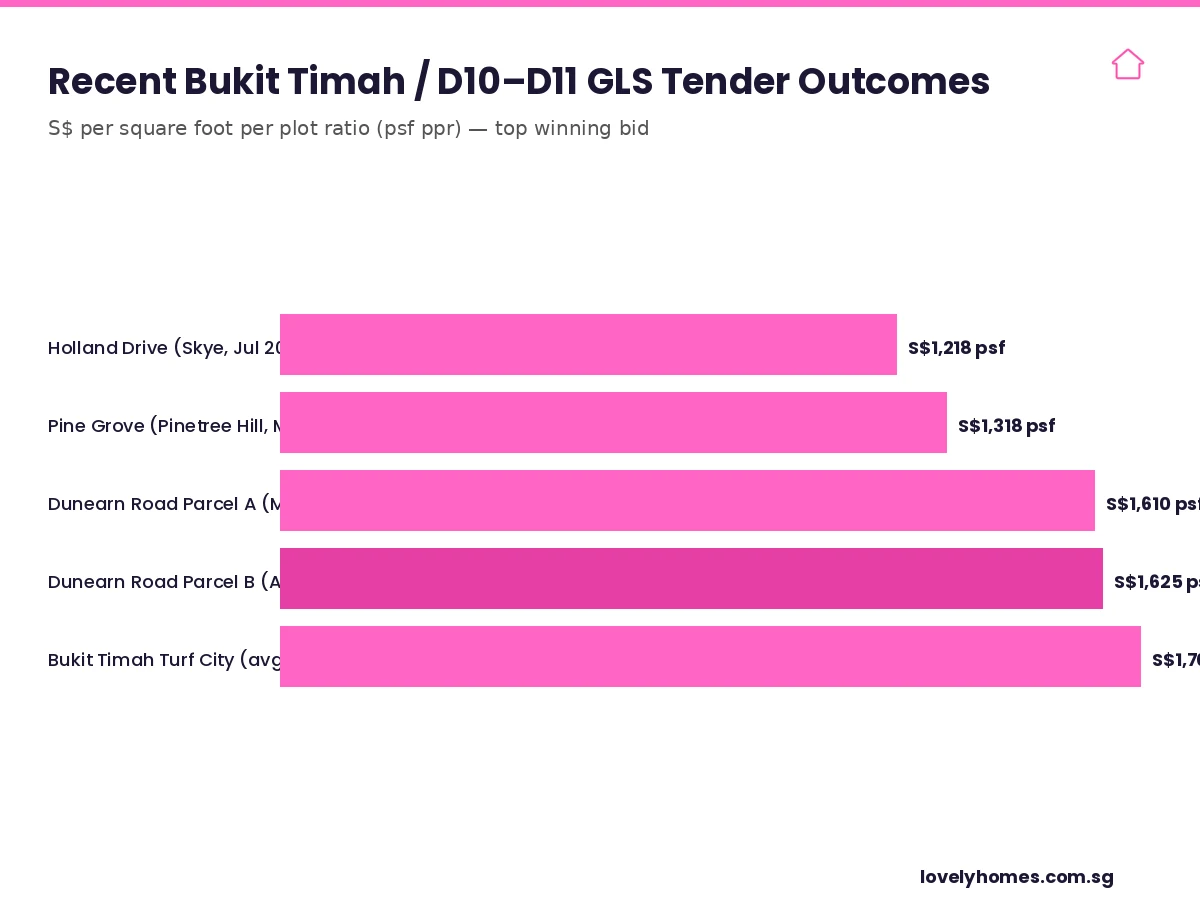

The S$1,625 psf ppr land rate sits right at the top of the recent Bukit Timah / D10–D11 GLS comparable set, narrowly above the S$1,610 psf ppr that Dunearn Road Parcel A cleared in March 2025. Both Dunearn Road parcels now anchor the precinct’s pricing.

| Metric | Reading | What it means |

|---|---|---|

| 6 bids on a CCR site | Strong contest | Refutes the “CCR is dead” narrative; ABSD-resilient buyer pool still exists for prime D11 |

| S$1,625 psf ppr | Top of band | Sets the new floor for D11 precinct land rates; future tenders likely to anchor here |

| ~330 units | Mid-sized | Manageable absorption profile; not a 1,000-unit mega-launch |

| Implied breakeven ~S$2,650 psf | Premium pricing | Launch psf above S$3,000 likely needed for healthy developer margins |

| 99-year tenure | Standard | No freehold premium baked in — Bala’s Curve applies in the long run |

Why District 11 Is Pulling Bids

The Dunearn Road tender outcome cuts against the broader CCR softness narrative in three ways:

- Bukit Timah Turf City master plan upside. URA has flagged the precinct as a major long-term residential growth area, with planned road and MRT enhancements funnelling traffic away from the existing Bukit Timah Road bottleneck. Future-precinct optionality — in particular the eventual mixed-use redevelopment of the surrounding Bukit Timah Plaza area — gives the Dunearn Road parcels a longer-tail upside than a typical CCR infill site.

- Sixth Avenue MRT proximity. The site sits within walking distance of Sixth Avenue MRT (Downtown Line). The recent re-rating of MRT-adjacent properties post-Cross Island Line announcement has lifted the implicit transit premium for sites in the Bukit Timah corridor.

- School catchment. The site falls within the catchment of several top primary schools — the perennial demand engine for District 11 family buyers, where ABSD is largely an irrelevance because the buyers are SC families on first-home purchases.

Indicative Launch Pricing — A Worked Example

Working backwards from the S$1,625 psf ppr land rate, industry figures typically estimate breakeven and indicative launch psf as follows. Worked Example: a developer paying S$1,625 psf for the land typically adds construction (~S$520–600 psf), professional fees and finance costs (~S$120–160 psf), and a margin and contingency layer (~S$280–320 psf), bringing all-in breakeven to roughly S$2,545–2,705 psf. Adding a healthy launch margin pushes indicative launch psf into the S$3,000–3,300 band. That places the new launch in the same general band as recent CCR new launches like 19 Nassim and the upper end of Watten Estate redevelopments.

| Cost Component | Indicative psf (S$) |

|---|---|

| Land cost | 1,625 |

| Construction | 560 |

| Professional fees + finance | 140 |

| Margin + contingency | 300 |

| Indicative breakeven | ~2,625 |

| Launch margin | ~400 |

| Indicative launch psf | ~3,025 |

Per-unit prices for typical 3-bedroom (~1,000 sqft) units would therefore range S$3.0–3.3 million at launch. For 2-bedroom units (~700 sqft) a launch range of S$2.1–2.3 million is plausible. The actual pricing will depend on launch-window comparables, prevailing financing rates, and any cooling-measures recalibration in the meantime.

What It Means for Buyers and Investors

For owner-occupiers in the District 11 catchment:

- Existing comparable resale stock in Bukit Timah Estate (e.g. Trevista, Cluny Park, Eng Neo Avenue) becomes a reference for upgrader value. Resale at S$2,400–2,600 psf for relatively new freehold stock starts looking competitive against an S$3,000+ psf new-launch.

- The 99-year tenure is a structural disadvantage relative to the freehold stock surrounding it. See our Freehold vs 99-Year Leasehold guide for the holding-period maths.

For investors:

- The implied breakeven sits well above the rental-yield supportable level. Net yields at S$3,000+ psf launch in District 11 typically come in at 2.0–2.5% — a yield-vs-capital-appreciation trade-off the buyer must accept upfront.

- For ABSD-resilient buyers (SCs on first home, FTA-exempted nationals), the entry calculus is dominated by capital appreciation expectations. For ABSD-paying buyers (foreigners at 60%, entities at 65%), the entry math is far harder.

What Comes Next

The 1H 2026 GLS programme has several more tenders ahead. The Holland Plain site closes on 7 May 2026 — another D10 / Bukit Timah-adjacent parcel that will set the next price benchmark. Beyond that, the remaining 1H 2026 sites include Bayshore Drive (a major mixed-use parcel closing 15 July 2026) and EC sites at Sembawang Drive and Canberra Drive that will affect the EC pipeline rather than the prime CCR narrative.

For Dunearn Road Parcel B specifically, the next milestones are the developer’s formal site mobilisation, the URA development application, and the pre-launch marketing window — all typically running 12–18 months from tender award. A late-2027 launch window is the practical expectation.

Frequently Asked Questions

When will the Dunearn Road condo launch?

Likely late 2027. Tender awards typically take 12–18 months to translate into a formal launch, depending on URA development-application turnaround, design finalisation, and pre-launch marketing setup. Earlier launches are possible if the developer fast-tracks the design, but the late-2027 to early-2028 window is the realistic baseline.

What is the expected launch psf for Dunearn Road?

Working from the S$1,625 psf ppr land rate, indicative breakeven is S$2,500–2,700 psf and an indicative launch range of S$3,000–3,300 psf is plausible. Final pricing will reflect launch-window comparables, financing rates, and any future cooling-measure recalibration.

Is the Dunearn Road site freehold or leasehold?

99-year leasehold — the standard tenure for Singapore GLS sites. The 99-year clock starts from issuance, typically 1–2 years before TOP. By the time buyers move in around 2030, the remaining lease will likely be 96–97 years.

How does this tender compare with the Tanjong Rhu GLS?

The Tanjong Rhu (River Modern) GLS site cleared at S$709 million in March 2025 — a larger project on a Riverfront RCR site. Dunearn Road Parcel B at S$533 million is a different scale and a different micro-market. Both are signals of sustained developer appetite for well-located GLS sites despite cooling-measure pressure.

What other 1H 2026 GLS tenders should I track?

Holland Plain (closing 7 May 2026) is the next D10-adjacent site. Bayshore Drive (closing 15 July 2026) is the major mixed-use parcel for the new Bayshore precinct. Sembawang Drive and Canberra Drive are EC sites that will affect the 2027–2028 EC pipeline. Each tender result becomes a fresh data point for pricing the surrounding resale and new-launch markets.

Are there alternatives in the same area for buyers who do not want to wait?

Existing freehold or 999-year leasehold stock in Bukit Timah Estate is the immediate resale alternative. Newer 99-year leasehold stock at Watten Estate, Sixth Avenue, and Coronation Road can be compared on a like-for-like psf basis. Pinetree Hill in the Pine Grove precinct remains the recent benchmark for Dunearn-adjacent leasehold new launches.

Related Articles

- Freehold vs 99-Year Leasehold Singapore 2026

- Executive Condominium Singapore 2026: Complete Guide

- URA Q1 2026 Private Home Prices Rise 0.9%

- Singapore Private Property Q1 2026 Full Statistics

- Frasers + Mitsubishi Win Kallang Close GLS

- ABSD Singapore 2026: Complete Guide

Disclaimer: This article is for general information only and does not constitute legal, tax, or financial advice. Tender outcomes, launch pricing and indicative breakeven figures are based on publicly disclosed URA tender data and industry-standard estimation conventions. Always verify current GLS data with the URA Land Sales page and consult a licensed property professional or financial adviser before acting on any property purchase.

0 Comments