Singapore’s property auction market is small but consistent. Roughly 150–200 properties are publicly auctioned every year, mostly mortgagee sales arising from borrower default, with a smaller flow of owner sales and a handful of sheriff (court-ordered) sales. For prepared buyers, auctions can deliver a 5–15% discount to recent comparables, and on rare occasions deeper. For unprepared buyers, they are an efficient way to lose a 5% deposit. This guide explains how the three auction types work, what to do on the day, the full cost stack including ABSD, and the legal traps that catch first-time bidders.

All references to amounts and rates reflect the position in April 2026 and the cooling-measures regime in force since 27 April 2023. Cross-check the IRAS stamp-duty page, Singapore Land Authority and your appointed conveyancing lawyer before bidding.

Quick Answer — auction buying at a glance

- Three public auction types operate in Singapore: mortgagee, owner and sheriff sales.

- Mortgagee sales (lender-driven) account for roughly two-thirds of public listings.

- The winning bidder pays a 5% deposit at the fall of the hammer (cashier’s order).

- Stamp duty (BSD + ABSD if applicable) is due within 14 days of the auction date.

- Completion is typically within 60–90 days of the auction.

- Properties are sold “as-is, where-is” with very limited vendor warranties.

- A 5–15% discount is realistic; deeper discounts come with more risk, not less.

- A bidder without an in-principle approval (IPA) and a cashier’s order at the auction is gambling.

Why Singapore property auctions matter

Public auctions sit at the margin of the Singapore market — the secondary market clears the vast majority of resale transactions through private treaty. But the auction floor is interesting for two reasons.

First, mortgagee sales are distressed sales by definition. The bank is enforcing under the mortgage deed and wants to clear the asset off the balance sheet at fair value within the calendar year. Where the property is unusual (unique strata mix, awkward layout, sub-12-month tenancy, dated condition), the auction route signals that. Buyers willing to accept the unusual feature typically capture a real discount.

Second, auctions are price discovery in public. Every reserve, every withdrawn lot, every successful bid is reported. In a quiet quarter for new launches, watching the auction order book gives you a real-time read on what the market thinks a CCR three-bedder or an OCR resale flat is genuinely worth. We track auction prints alongside private-treaty data in our Transaction News section.

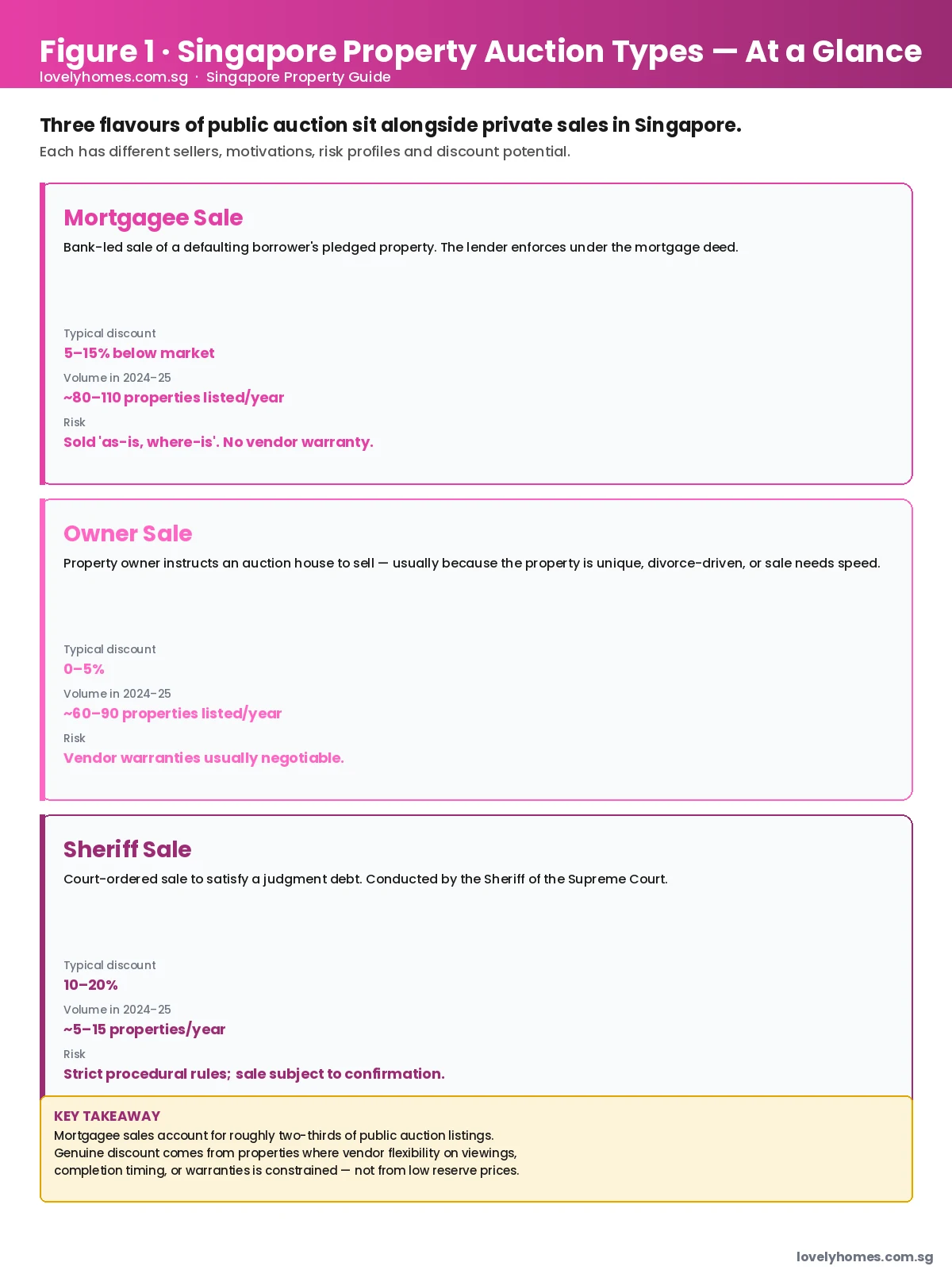

The three auction types — mortgagee, owner, sheriff

Mortgagee sale

A mortgagee sale is a forced sale by a mortgagee (typically a bank or financial institution) to recover an outstanding loan. The mortgagor (borrower) has defaulted; the lender has issued and exhausted statutory notices; and the property is being sold under the power of sale in the mortgage deed. The sale is conducted by a licensed auctioneer instructed by the lender. The lender does not warrant title quality, vacant possession, or condition — the buyer takes the property as it stands.

Mortgagee sales are the bulk of the public auction calendar. In 2024–25 around 80–110 mortgagee listings reached the auction floor each year, with 50–60% selling in the room, the rest withdrawn or rolled to the next sale. Discount versus comparable resale typically runs 5–15%, with deeper discounts available where the property is occupied by a holdover tenant or has known disputes attached to it.

Owner sale

An owner sale is a sale instructed by the registered owner, usually because the property is unique (a high-floor penthouse with no comparable benchmark), the timeline is short (divorce, estate distribution), or the owner wants the auction transparency. Volume is similar to mortgagee sales. Discounts are smaller — often 0–5% — but vendor warranties on title and vacant possession are usually negotiable, narrowing the risk gap.

Sheriff sale

A sheriff sale is a court-ordered sale by the Sheriff of the Supreme Court, conducted to satisfy a judgment debt. Volumes are tiny — perhaps 5–15 a year — and the procedure is rigid: the sale price must be confirmed by the court, and the buyer takes title only on confirmation, which can take weeks. Discounts of 10–20% are common but the procedural fragility means many bidders avoid sheriff sales unless the discount is large enough to compensate.

The bidder’s timeline — from catalogue to completion

The full sequence is mechanical and unforgiving on dates:

- T-21 days — spot the listing. Public auction catalogues are issued roughly three weeks ahead of each sale. The major Singapore auctioneers publish digital catalogues with property details, reserves and conditions of sale. URA Realis (the URA’s title and tenure portal) is the authoritative cross-check on tenure, plot ratio and outstanding charges.

- T-14 days — site inspection. Inspect the property with the auction-house contact. Mortgagee sales are usually delivered with vacant possession; owner sales sometimes come with sitting tenants whose tenancies survive the sale. Check the tenancy status and any holdover risk before bidding.

- T-10 days — lawyer and valuation. Engage a conveyancing lawyer to read the conditions of sale (these are non-negotiable on the day) and identify any unusual covenants, head-leases or maintenance disputes. If you intend to finance, instruct a bank-panel valuation report so the lender can issue an IPA quickly.

- T-7 days — bank IPA. Get the IPA in writing. Banks treat auction purchases as standard property loans — LTV up to 75% for first-property residents, lower for foreign buyers (50–55%). The IPA is honoured for 30–60 days and gives the bidder confidence to commit. See our Singapore Home Loan Guide 2026 for the LTV and stress-test framework.

- T-1 day — funds in hand. Issue the cashier’s order for 5% of your maximum bid (yes — you may bid below it; no — you cannot bid above it without further funds). Earmark cash and CPF for ABSD/BSD due within 14 days.

- Day 0 — the auction. Register at the door; receive a paddle. Bids open at the auctioneer’s call. The reserve is rarely declared in advance; watch the room. The winning bid above reserve is final on the fall of the hammer. The buyer signs the Memorandum of Sale immediately and hands over the deposit.

- Day +14 — stamp duty. BSD and ABSD (if applicable) are paid via IRAS e-stamping within 14 days of the auction date. Late payment attracts penalties at IRAS’s stated rate. Refer to the BSD guide and ABSD guide for the calculation.

- Day +60 to +90 — completion. The balance 95% is paid; the transfer is registered with SLA; the buyer receives the keys. Mortgagee sales typically complete within 60–90 days. Sheriff sales need court confirmation and may stretch to 120 days.

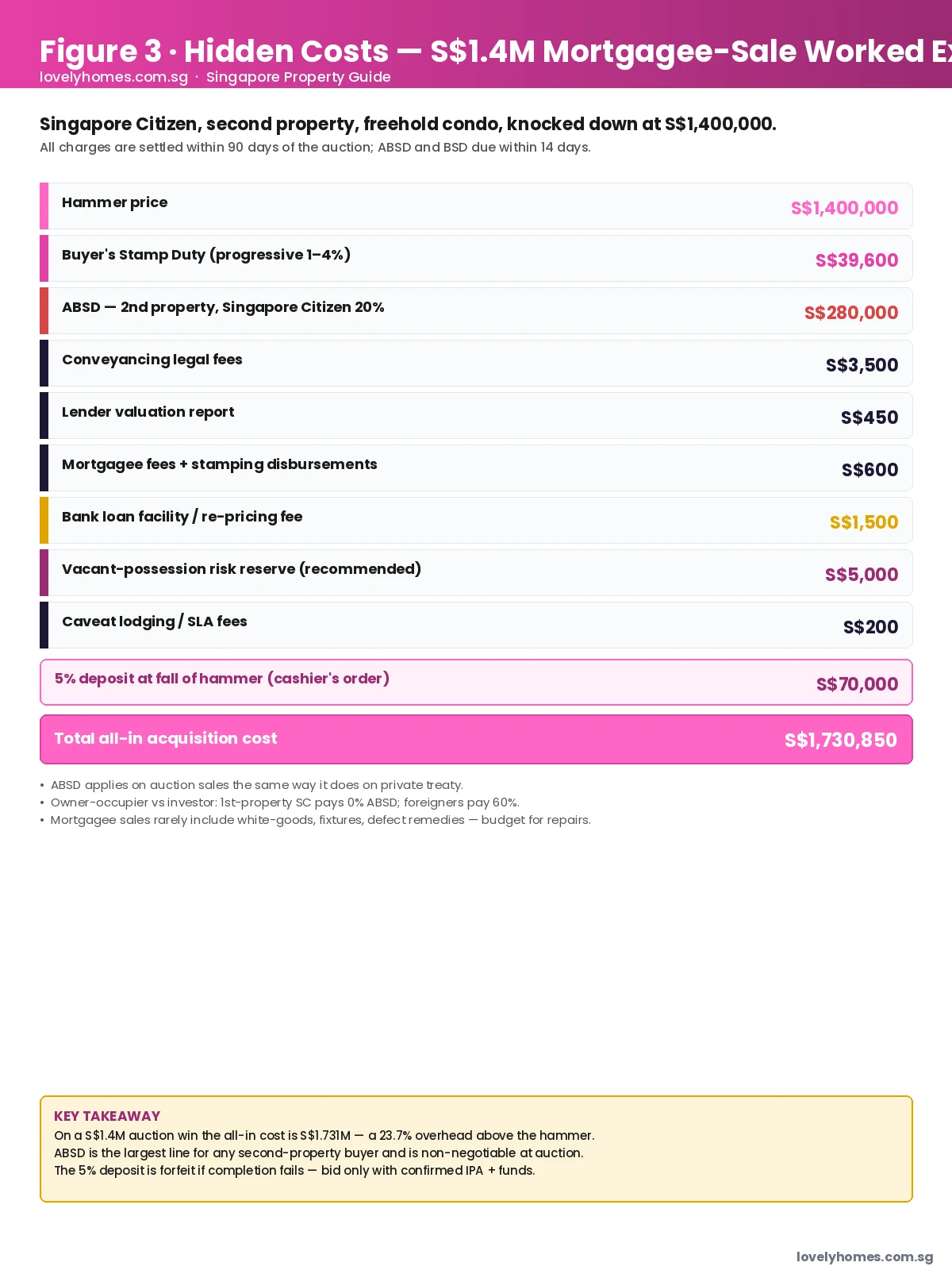

What you actually pay — full cost stack on a S$1.4M win

Take a Singapore Citizen second-property buyer who wins a freehold two-bedroom condominium at a mortgagee auction with a hammer price of S$1,400,000. The full cost stack — including everything most first-time bidders forget — looks like this:

- Hammer price: S$1,400,000;

- 5% deposit at the fall of the hammer: S$70,000 (cashier’s order);

- BSD: S$39,600;

- ABSD at SC second-property 20%: S$280,000;

- Conveyancing legal fees: ~S$3,500;

- Lender valuation, mortgagee fees, SLA fees: ~S$1,250;

- Bank loan facility / re-pricing fee: ~S$1,500;

- Vacant-possession reserve (recommended): S$5,000.

Total all-in cost: roughly S$1,731,250 — about 23.7% above the hammer. A bidder who treats the hammer as the “real” price and budgets only for it will be cash-short by Day 14. ABSD is the largest single line and applies on auction sales the same way it does on private treaty.

Legal traps that catch first-time bidders

Auction is a public-law procedure with much sharper edges than private treaty. The five most common traps:

- “As-is, where-is” condition. Mortgagee sale Conditions of Sale typically exclude all warranties on physical condition. The buyer takes the property exactly as it is on auction day — defects, illegal renovations, encroachments, pest damage, leaks. Always inspect personally.

- Holdover tenants. A mortgagor may, at the time of auction, still have a tenancy agreement in place. The mortgagee sale extinguishes some tenancies but not all — tenancies with a registered head lease can survive the sale. Read the tenancy documents before bidding.

- Outstanding maintenance and management corporation arrears. The MCST may have a charge over the property for unpaid maintenance and sinking-fund contributions; these can attach to the new owner. Auction-house fact sheets often disclose, but not always.

- Caveats and CPF charges. Where the previous owner used CPF for the purchase, the CPF Board’s charge must be discharged at completion. Where there are private caveats, your lawyer must lift them before transfer.

- Failure to complete. If you fail to pay the 95% balance by the completion date, the vendor (or mortgagee) may rescind, retain the 5% deposit and re-auction. The original buyer has no claim back. This is the most common reason auction buyers lose substantial sums — it is almost always avoidable with a confirmed IPA before bidding.

Summary table — auction snapshot 2026

| Item | Position at Singapore property auction |

|---|---|

| Deposit at hammer | 5% of hammer price (cashier’s order) |

| Stamp-duty deadline | 14 days from auction date |

| Completion window | 60–90 days (sheriff sales: up to 120) |

| Vendor warranties | Minimal. Usually none on condition. |

| Typical discount band | Mortgagee 5–15%; sheriff 10–20%; owner 0–5% |

| ABSD payable | Yes — same as private treaty |

| Buyer’s Stamp Duty | Yes — 1–6% progressive |

| Bank financing | Yes — IPA from at least one bank required |

| CPF use | Yes for SCs/PRs (subject to OA balance) |

| Cooling-off period | None — bid is final on fall of hammer |

Why this matters — how auction discounts compare to private treaty

Auction is sometimes positioned as a high-discount route to Singapore property. The reality is more nuanced. URA caveat data suggests that average mortgagee-sale prints land at roughly 92–95% of comparable private-treaty values for the same building, with deeper discounts only where the property is unusual or distressed. Net of the buyer-side legal and vacant-possession risk reserve, the realised discount is typically 5–10 percentage points — meaningful, but not transformative.

The genuine edge for an auction buyer comes elsewhere: access to atypical inventory (high-floor penthouses, partial-strata bungalows, en-bloc-pending units that owners want to clear before the SoR vote), and certainty of timing. If you must complete by a fixed date, an auction commitment with confirmed IPA delivers that certainty in a way that a 14-day OTP private-treaty negotiation often cannot.

What might come next

Two trends in 2026 are worth watching:

- Volume sensitivity to the rate cycle. Mortgagee sale volumes have a clear correlation with mortgage stress. With 3-month compounded SORA having stabilised in the 2.7–3.0% band through 2025–26, mortgage default volumes have eased back to roughly 80–100 mortgagee listings a year. A renewed rate spike could push that materially higher; a sharper Singapore Dollar rate cut would reduce supply further.

- Online auction normalisation. Singapore’s main auction houses moved to hybrid online + in-room formats from 2021. Online registration, livestream bidding and digital paddle systems are now standard. The risks of remote bidding (fat-finger entries, latency on accelerating bid books) are real and a reason to keep your maximum bid documented in writing before you log in.

Frequently Asked Questions

Can I view the property before bidding?

Yes. Auction houses arrange supervised viewings during the 7–10 days before the auction. Mortgagee-sale viewings are usually empty units; owner-sale viewings may have furniture or sitting occupants. Always personally inspect — the photographs in the auction catalogue are not warranted.

Do auction buyers pay ABSD on the same basis as private-treaty buyers?

Yes. ABSD is administered by IRAS based on the Buyer Profile and the property count at the time of the document attracting duty (the Memorandum of Sale on auction day). The 60% foreigner rate, 20%/30% SC rates and 30%/35% PR rates all apply unchanged. See our ABSD complete guide.

What happens if the property fails to sell at auction?

The lot is “withdrawn”, and the auctioneer typically invites private-treaty offers above the reserve. Many auction-floor failures sell within four weeks at or near the reserve, with the same conditions of sale. This is a useful route for bidders who attended the auction and watched the bidding stall just below their valuation.

Can I bid by proxy or remotely?

Yes. Most major Singapore auction houses accept written or telephone proxy bids and offer hybrid online bidding portals. The proxy form must be signed and lodged before the auction; the highest authorised proxy bid will be entered automatically when called. Confirm IT and identification requirements with the specific auction house.

Do I lose the deposit if my bank withdraws financing after I win?

Yes — if you cannot complete by the contractual completion date, the vendor (mortgagee) may rescind and retain the 5% deposit. This is why a pre-auction IPA is non-negotiable. Banks do not usually pull a written IPA without good reason, but if your circumstances change between IPA and completion (job loss, a second mortgage commitment), the IPA can be withdrawn.

Can I use CPF for an auction purchase?

Yes, on the same basis as a private-treaty purchase. CPF Ordinary Account funds may be used for the down payment (subject to the OA balance), and CPF can service monthly mortgage instalments after completion. CPF cannot, however, be used for the 5% deposit at the fall of the hammer — that must be a cashier’s order from a Singapore bank account.

Are auction prices visible in URA caveat data?

Yes. Auction completions are lodged as caveats with SLA in the same way as private-treaty completions, and they appear in URA Realis, IRAS Property Tax records, and downstream property data feeds. Look at the caveat date vs auction date to spot mortgagee transactions — auction closes typically lag 60–90 days behind the auction date.

Related reading on LovelyHomes

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty Singapore 2026: Rates, Worked Examples & How to Calculate

- Property Conveyancing Guide Singapore 2026

- Singapore Home Loan Guide 2026: LTV, TDSR, Fixed vs SORA

- Singapore Property Valuation 2026: How Banks Decide Your Home’s Worth

- Seller’s Stamp Duty Singapore 2026

- CPF for Property Purchase Singapore 2026

- Foreign Buyer Guide Singapore 2026

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. Auction Conditions of Sale, ABSD remissions and bank-lending caps are fact-specific and change over time. Always verify the current position with the IRAS Stamp Duty page, the Singapore Land Authority, and a licensed Singapore conveyancing lawyer before signing any Memorandum of Sale.

0 Comments