QUICK ANSWER: Singapore Sellers’ Stamp Duty (SSD) 2026

- SSD applies for the first 3 years after you purchase a residential property in Singapore — the rate drops by year and reaches zero in year 4.

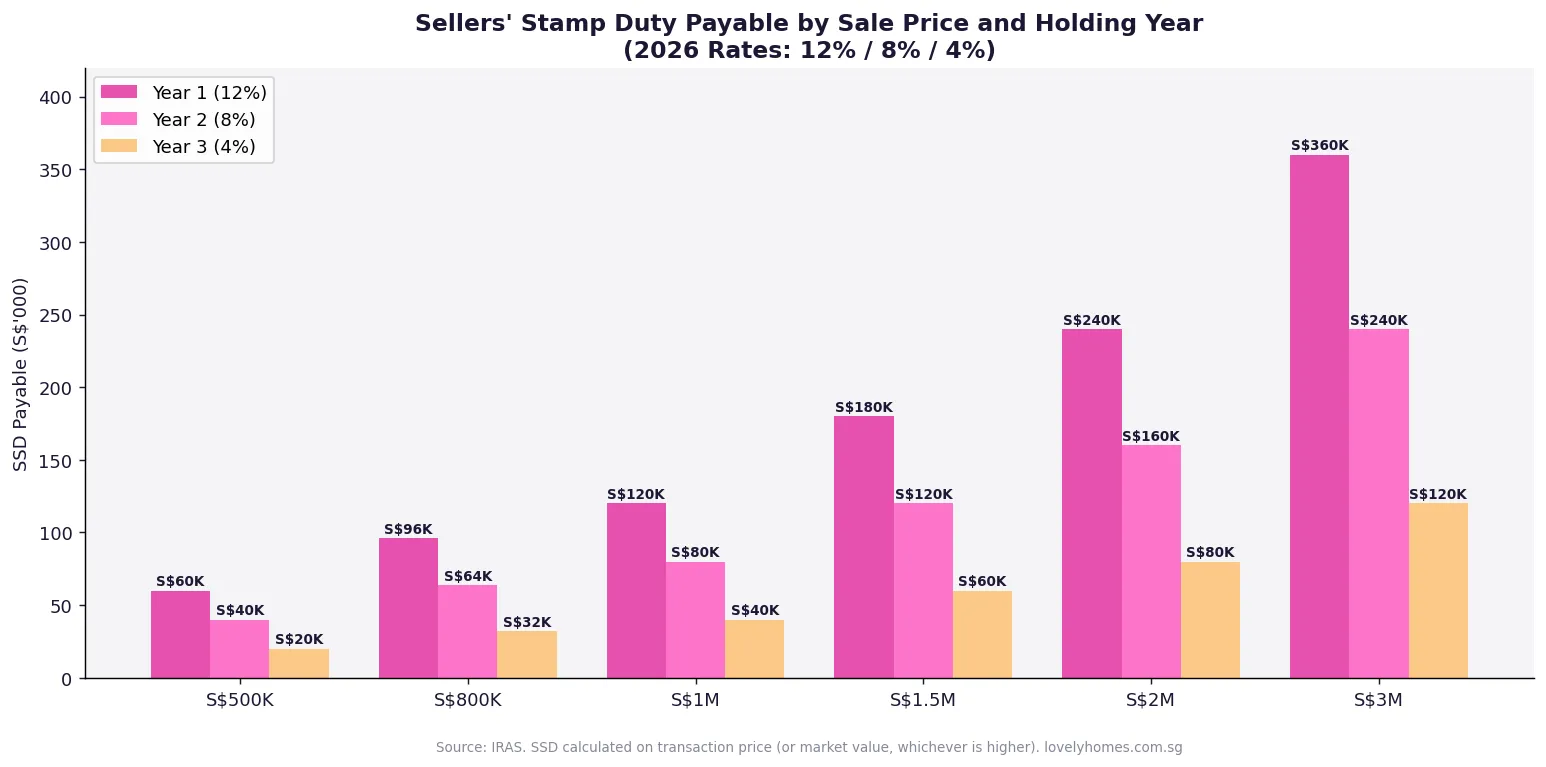

- Current rates: 12% (Year 1), 8% (Year 2), 4% (Year 3), 0% (Year 4 onwards).

- SSD is charged on the higher of the transaction price or the property’s market value — and must be paid by the seller within 14 days of the sale.

- For a S$1.5M property sold in Year 1, the SSD charge is S$180,000 — enough to wipe out or reverse most short-term capital gains.

- SSD applies to all residential property: private condominiums, landed homes, and HDB resale flats.

- The 3-year SSD window starts from the date the Option to Purchase (OTP) was exercised, not from the legal completion date.

- SSD is administered by the Inland Revenue Authority of Singapore (IRAS) under the Stamp Duties Act (Cap 312).

- Exemptions exist for specific circumstances: inherited property, court-ordered divorce transfers, and certain government acquisition scenarios.

What Is Sellers’ Stamp Duty in Singapore?

Sellers’ Stamp Duty (SSD) is a tax levied on the seller of a residential property in Singapore when the property is sold within three years of its purchase. It was introduced by the government in February 2010 as part of a package of property cooling measures designed to discourage short-term speculative buying — the practice of purchasing property with the primary intent to sell quickly for a profit, rather than to occupy or hold as a long-term investment.

IRAS administers SSD under the Stamp Duties Act (Cap 312). The duty is based on the higher of the sale price or the property’s open market value, and must be remitted by the seller within 14 days of the disposal date. Unlike Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD) — which are buyer obligations — SSD is unambiguously the seller’s responsibility, regardless of any contractual arrangement between buyer and seller.

The current SSD rate schedule has been in place since January 2012, when the government recalibrated the rates following earlier rounds of adjustment in February 2010 and January 2011. The 2012 schedule — 12%, 8%, 4% for years one, two, three respectively — has remained unchanged, serving as a stable deterrent against rapid property trading.

SSD Rates: The Holding Period Framework

The SSD rate schedule is straightforward in structure but consequential in impact. A property sold within the first 12 months of purchase attracts SSD at 12% of the higher of the transaction price or market value. Selling in the second year (months 13 to 24) attracts 8%, and in the third year (months 25 to 36) attracts 4%. From month 37 onwards — the fourth year — SSD falls to zero and there is no longer any tax consequence to selling.

The “year” here is based on 12-month periods from the relevant acquisition date, not calendar years. The relevant date is defined as the date the buyer exercised the Option to Purchase (OTP), or the date of the Sale and Purchase Agreement if no OTP was involved. This is not the date of legal completion — a distinction that sometimes catches sellers off guard, particularly for new launch properties where completion may be two to three years after OTP exercise.

On a S$2 million property sold in Year 1, SSD would be 12% of S$2M = S$240,000. On a S$1.5M property sold in Year 3, SSD is 4% of S$1.5M = S$60,000. These are substantial sums that can eliminate or reverse what appeared to be a profitable transaction on paper.

Which Properties Are Subject to SSD?

SSD applies broadly to all residential property in Singapore: private condominiums, executive condominiums (during the period they are treated as private residential property — i.e., after the 5-year Minimum Occupation Period), landed homes (terraced houses, semi-detached, bungalows, good class bungalows), and HDB resale flats.

Critically, SSD does not apply to commercial property, industrial property, or shophouses where the entire floor area is zoned for commercial use. This distinction makes commercial and industrial properties attractive to investors seeking to trade without a 3-year holding constraint — though these assets carry different yield profiles, CPF eligibility rules, and liquidity characteristics.

For new launch private condominiums where a buyer exercises an OTP at the sales gallery — for example, exercising an OTP on 15 March 2024 for a property that achieves TOP in July 2026 — the SSD clock starts from 15 March 2024, not from the TOP date or keys collection date. A seller who sells in August 2024 (5 months after OTP exercise) would still be liable for 12% SSD even though they have not yet received the keys.

| Property Type | SSD Applies? | Start Date for SSD Clock | Notes |

|---|---|---|---|

| Private condo (resale) | Yes | OTP exercise date | Standard SSD 12%/8%/4% |

| New launch condo (BUC) | Yes | OTP exercise date (not TOP) | SSD clock runs during construction |

| HDB resale flat | Yes | OTP exercise / HDB resale application date | Distinct from 5-year MOP requirement |

| Landed property | Yes | OTP exercise date | GCB and all landed categories |

| EC (during privatisation) | After MOP (Year 5+) | Original purchase date from developer | SSD window typically expires well before 5-yr MOP |

| Commercial / industrial | No | N/A | Different stamp duty regime applies |

How SSD Is Calculated: Key Rules

SSD is computed on the higher of (a) the actual sale price and (b) the market value at the date of disposal. IRAS may obtain an independent valuation if it believes the stated sale price does not reflect market value. This rule prevents arrangements where a seller agrees with a buyer to understate the purchase price to reduce SSD — any such arrangement is ineffective against IRAS and may additionally attract scrutiny for tax evasion.

The seller is responsible for paying SSD regardless of what has been agreed in the sale contract. If a buyer and seller have contractually agreed that the buyer will “absorb” the SSD (sometimes seen in developer sales of completed units), this is a private contractual arrangement that does not alter the legal liability: IRAS will pursue the seller, and the seller must then seek recourse from the buyer under contract law. Stamp duty is a statutory obligation, not a negotiable commercial term from IRAS’s perspective.

SSD payments are due within 14 days of the date of disposal. Late payment attracts a 5% per annum surcharge and IRAS may impose additional penalties for substantial delay. SSD paid is not tax-deductible against rental income or capital gains (Singapore does not tax capital gains on property for individuals).

SSD Exemptions: When You Do Not Pay

IRAS provides for specific exemptions where SSD is not payable even if the disposal occurs within three years. These include: transfers pursuant to a divorce court order (the court order must specifically direct the transfer); inheritance by beneficiaries where the property is acquired by gift or succession (the SSD clock resets for the beneficiary from the date of inheritance); compulsory government acquisition under the Land Acquisition Act (where the government exercises its statutory power); and certain court-sanctioned insolvency disposals.

There is no exemption based on financial hardship, job loss, or personal circumstances — if the property is sold within the SSD window for any reason not covered by the statutory exemptions, SSD is payable. Sellers who need to sell urgently within three years (relocation, divorce settlement outside of court order, financial difficulty) should budget for the SSD liability as an unavoidable cost of early exit.

Worked Example: Mr Tan’s Investment Property Sale

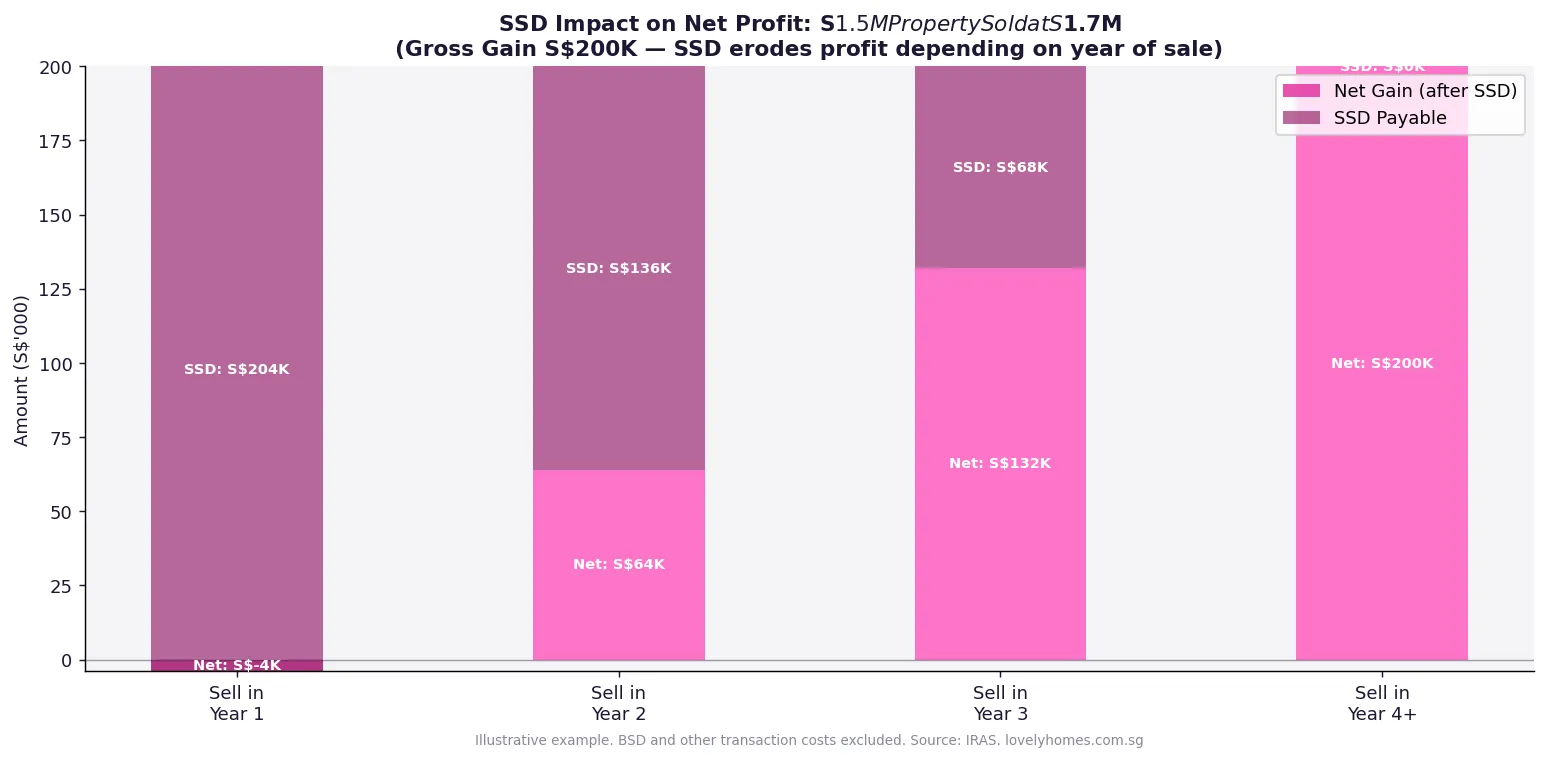

Mr Tan, a Singapore Citizen, purchased a two-bedroom condominium in the Rest of Central Region (RCR) in September 2023 for S$1.5 million. He received keys upon TOP in March 2026 and began receiving rental income of S$3,800 per month. In June 2026, his employer offers him a long-term posting in London. He needs to assess his options:

Option A — Sell immediately (June 2026 = 33 months from OTP):

Sale price: S$1.65 million (S$150,000 gross appreciation)

SSD rate: 4% (Year 3, month 33) on S$1.65M = S$66,000

Agent commission: 1% of S$1.65M = S$16,500

Net gain after SSD and agent: S$150,000 − S$66,000 − S$16,500 = S$67,500

Option B — Wait until October 2026 (37 months from OTP — SSD window expires):

Sale price assuming S$1.7M by October 2026 (further appreciation)

SSD: S$0 (past 36-month SSD window)

Agent commission: 1% of S$1.7M = S$17,000

Net gain: S$200,000 − S$0 − S$17,000 = S$183,000

Option C — Rent out the property while overseas:

Gross rental yield at S$3,800/mth on S$1.65M asset = 2.76% p.a.

Net yield after IRAS-deductible expenses (mortgage interest, property tax, agent fee, maintenance) ≈ 1.8–2.0% p.a.

By waiting until October 2026, Mr Tan collects approximately 4 months of additional rent (S$15,200) and avoids S$66,000 SSD, while benefiting from continued capital appreciation. The 4-month wait is clearly superior financially if his overseas posting allows for remote property management.

Key insight: The SSD framework is highly effective at aligning incentives towards longer holding periods. Even a 4-month difference between Options A and B changes the outcome by nearly S$115,500 (S$183,000 vs S$67,500) — a dramatic illustration of why informed investors track their SSD clock carefully from the OTP exercise date.

Why SSD Matters for Singapore’s Property Market

SSD’s primary economic function is to lengthen the average holding period across the residential property market, thereby dampening transaction volume during upswings and reducing the role of speculative “hot money” in price formation. Academic and policy research consistently finds that short-term speculative transactions — where buyers have no intention of occupying or holding the property — amplify price volatility. By making early exit financially costly, SSD encourages buyers to base their purchase decisions on fundamental value rather than anticipated short-term price movements.

Singapore’s SSD framework is also notable for its stability. Unlike ABSD — which has been revised multiple times, most recently in April 2023 — the SSD rate schedule has remained unchanged since January 2012. This consistency provides predictability for genuine long-term investors and reduces policy uncertainty in medium-term investment planning. Buyers who understand the 3-year SSD window at the point of purchase can factor it into their investment thesis without fear of mid-holding-period rule changes.

Internationally, comparable anti-speculation duties exist in Hong Kong (Special Stamp Duty, up to 20% within 36 months), Canada (various provincial measures), and New Zealand (previously the “bright-line test”). Singapore’s SSD is broadly in line with international practice, though the combination of SSD with the ABSD framework makes the overall speculative cost substantially higher than in most comparable markets.

What Might Change for SSD?

The SSD framework is rarely the subject of policy discussion compared with ABSD. Its unchanged rate structure since 2012 reflects broad political consensus that 3 years is an appropriate minimum holding period to distinguish genuine investors from speculators. The rates themselves — 12%, 8%, 4% — are seen as calibrated to the typical profit margin from short-term flipping: at 12%, any investment yield below 12% of purchase price in year one produces a net loss for a flipper, effectively eliminating the financial rationale for early exit.

Any future relaxation of SSD is most likely to come via a shortening of the window (from 3 years to 2 years) rather than rate changes — similar to what was done when the government reduced the SSD window from 4 years to 3 years in January 2012. An extension of the SSD window beyond 3 years appears unlikely given that most genuine investors plan to hold longer than 3 years anyway. As with all cooling measures, changes would be announced by the Ministry of Finance and MAS, effective immediately upon announcement to prevent front-running.

Frequently Asked Questions

Does SSD apply if I sell my HDB flat within 3 years of purchase?

Yes, SSD technically applies to HDB resale flat purchases if the flat is sold within 3 years. However, in practice, HDB’s Minimum Occupation Period (MOP) — which requires the owner to physically occupy the flat for at least 5 years before selling on the open market — is the more binding constraint. Since 5 years is longer than the 3-year SSD window, HDB flat owners will never actually trigger SSD liability when they eventually sell their flat after satisfying the MOP (because by then, the SSD clock has long expired). The SSD risk for HDB is theoretical rather than practical under normal ownership circumstances.

Is SSD based on the date I bought the property or the date I TOP (Temporary Occupation Permit)?

SSD is based on the date you legally acquired the property — specifically, the date you exercised the Option to Purchase (OTP) or entered into a Sale and Purchase Agreement (S&P), whichever is earlier. For new launch properties, this is the date you signed documents at the sales gallery, which can be 2 to 4 years before TOP. This means that by the time a new launch property receives TOP and you collect your keys, the SSD window may already be partially or fully expired. For example, if you exercised your OTP in January 2022, your SSD window expired in January 2025 — well before a property with a 2025 or 2026 TOP date would be ready for sale.

What if I want to give the property to a family member — is that a disposal subject to SSD?

Transferring a property as a gift to a family member — for example, transferring a property from parent to child — is treated as a disposal by IRAS. SSD is payable if the gift occurs within 3 years of the transferor’s acquisition date. The SSD is calculated on the market value of the property at the date of transfer (since the “transaction price” is effectively zero for a gift). This rule prevents SSD avoidance through gifting arrangements. The only exempt transfers are those ordered by a court (e.g., in divorce proceedings) or arising from inheritance upon death.

Does selling a property at a loss exempt me from SSD?

No. SSD is calculated on the sale price or market value — not on profit. A seller who purchased at S$2M and is forced to sell at S$1.8M in Year 2 (a loss of S$200,000) is still liable for SSD of 8% on S$1.8M = S$144,000, compounding the loss. Singapore does not provide SSD relief for distressed sales, negative equity situations, or circumstances where the seller makes no profit. This underscores the importance of understanding the SSD obligation before purchasing any residential property with a short intended holding horizon.

Does SSD apply to property inherited from a deceased estate?

When a beneficiary inherits a property through a will or intestate succession, the SSD clock resets — it starts from the date the property is legally transferred into the beneficiary’s name, not from the original purchase date by the deceased. So if the deceased bought the property in 2020 and passes away in 2026, the beneficiary inherits the property with a fresh SSD clock from 2026. If the beneficiary sells immediately after inheritance, no SSD is payable (as the clock just started and the acquisition cost for SSD purposes is the inherited value, not the original purchase price). This fresh-start treatment for inherited property is distinct from a gift during the original owner’s lifetime, which does not reset the clock.

Can I avoid SSD by putting the property in a company or trust?

Disposing of a beneficial interest in a residential property — including through a company structure or a trust — is treated as a disposal for SSD purposes. IRAS has specific anti-avoidance provisions that look through corporate and trust structures to identify the underlying beneficial owner and the effective date of disposal. A sale of shares in a company that holds residential property as its primary asset may be treated as a disposal of the property itself if the primary purpose of the structure is to circumvent stamp duty obligations. Additionally, entity purchases of residential property already attract the 65% ABSD rate, making corporate structures extremely costly for residential property holding even apart from SSD considerations.

How does SSD interact with the property’s rental income tax treatment?

SSD and rental income tax are entirely separate obligations. A seller who incurs SSD when selling a rented property cannot deduct the SSD from their taxable rental income — SSD is a transaction tax, not a revenue expense in IRAS’s framework. Rental income is taxed on a net basis after allowable deductions (mortgage interest, property tax, agent fees, repairs, depreciation of furniture under IRAS-approved rates). Since Singapore does not impose capital gains tax on individuals’ property disposals, the capital gain itself (sale price minus purchase price) is not taxed at all — leaving SSD as the only significant tax consequence of selling within 3 years of purchase.

Related Articles

- Singapore Property Cooling Measures Guide 2026: ABSD, TDSR, LTV and SSD Explained

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Private Property Buying Costs 2026: Complete All-In Cost Guide

- Singapore Property Decoupling Guide 2026: How to Save ABSD by Transferring Ownership

- Singapore En Bloc Sellers’ Guide 2026: Collective Sale Process and Proceeds

- Singapore Home Loan Refinancing Guide 2026: When to Switch and How Much You Save

- Singapore Property Portfolio Guide 2026: ABSD, Yields and Strategy

- Singapore Annual Property Tax Guide 2026: Annual Value, IRAS Rates Explained

Disclaimer

This article provides general educational information about Singapore’s Sellers’ Stamp Duty framework and does not constitute financial, legal, or tax advice. SSD rules are administered by IRAS and are subject to change. Always verify current rates, exemptions, and deadlines at iras.gov.sg and consult a licensed property agent, qualified conveyancing lawyer, and tax adviser before any property transaction. LovelyHomes does not provide personalised investment or legal advice.

0 Comments