Singapore Stamp Duty Remission Guide 2026: ABSD Upgrader Refunds, Married Couple Exemptions and How to Apply

Stamp duty in Singapore is not one-size-fits-all. The government has deliberately built a system of remissions and exemptions that recognise legitimate circumstances — the upgrading family, the divorcing couple, the deceased estate, the registered charity — and provides a mechanism to recover the stamp duty paid, or to pay a lower rate in the first place. Understanding these remissions is not an advanced topic for lawyers; it is practical knowledge that can save a Singapore family anywhere from S$40,000 to well over S$1,000,000 in upfront costs.

This guide explains every major stamp duty remission available in Singapore in 2026 — who qualifies, how much is refunded, how to apply, and what the key deadlines are. The framework is administered by the Inland Revenue Authority of Singapore (IRAS) under the Stamp Duties Act (Cap 312). All rates reflect the 27 April 2023 cooling measures, which remain in force.

Quick Answer — Stamp Duty Remissions at a Glance

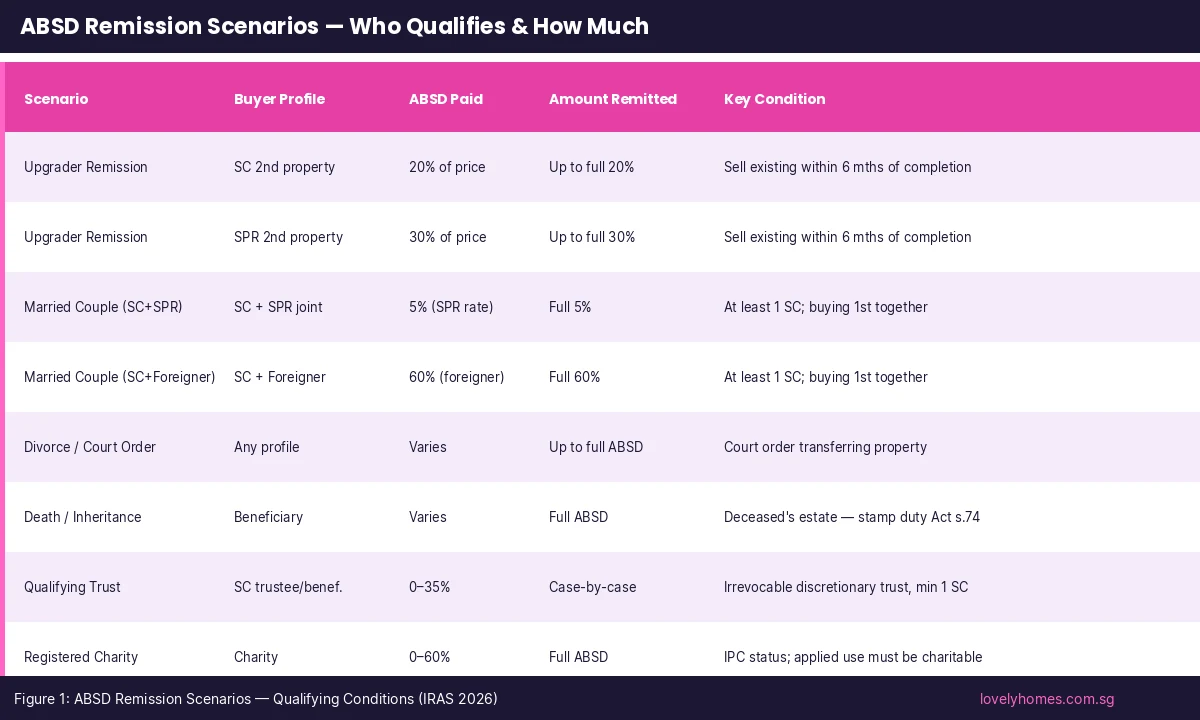

- ABSD Upgrader Remission: SC and SPR second-property buyers who sell their existing home within 6 months of completion can reclaim the full ABSD paid (20% for SC; 30% for SPR).

- Married Couple Remission: Couples where at least one party is a Singapore Citizen buying their first joint residential property together pay 0% ABSD regardless of the other party’s nationality (subject to conditions).

- Divorce / Court Order: A court-ordered transfer of property between divorcing spouses may attract an ABSD remission or BSD exemption on a case-by-case basis.

- Death and Inheritance: Properties transferred from a deceased estate to beneficiaries are exempt from ABSD under s.74 of the Stamp Duties Act.

- SSD Exemptions: Properties sold under en-bloc, compulsory acquisition, court order (divorce/death), or gifted to lineal descendants are exempt from Seller’s Stamp Duty.

- BSD Remissions: Rare — mainly for government bodies, charities, and certain trust arrangements. Most individual buyers do not qualify for BSD remission.

- All remission claims are filed at myTax Portal → Stamp Duty → Apply for Remission. ABSD remissions for upgraders require documentary proof of the sale of the existing property.

- The key upgrader deadline is 6 months from completion of the new purchase to sell the existing property. Miss this window and the ABSD paid is forfeited.

What Is Stamp Duty Remission?

A remission is a partial or full waiver of stamp duty that would otherwise be payable. Unlike an exemption (which means the duty was never due), a remission often means the duty is paid upfront and then refunded once the qualifying conditions are met. The Ministry of Finance (MOF) and IRAS administer Singapore’s remission framework under Part IV of the Stamp Duties Act. The rationale is to avoid distorting legitimate property transactions — particularly family upgrading, matrimonial transfers, and estate administration — while still collecting duty on speculative purchases.

There are three types of stamp duty in Singapore where remissions may arise:

- Additional Buyer’s Stamp Duty (ABSD): The most significant remissions. ABSD can be 0–65% of purchase price depending on buyer profile. Remissions here can be worth hundreds of thousands of dollars.

- Buyer’s Stamp Duty (BSD): Remissions are rare and mainly apply to non-individual entities (charities, government bodies). Most homebuyers do not benefit from BSD remission.

- Seller’s Stamp Duty (SSD): Certain exit scenarios — en-bloc, compulsory acquisition, divorce, death — are exempt from SSD even within the 4-year holding period.

ABSD Upgrader Remission — The Most Common Remission in Singapore

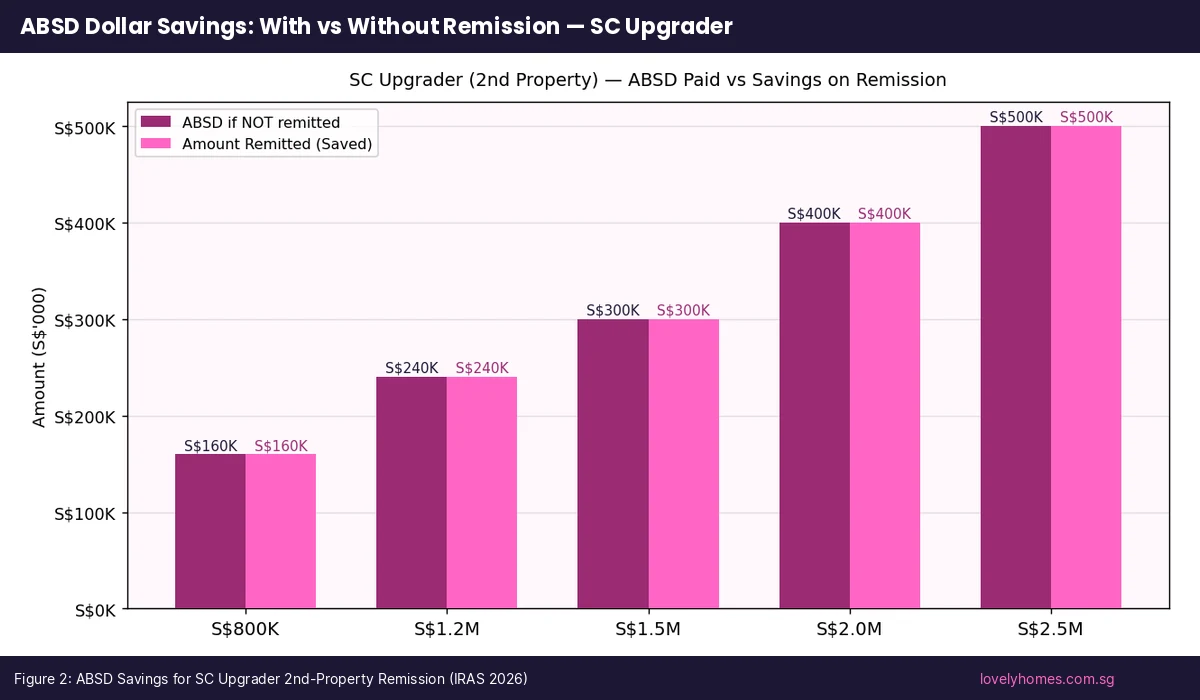

The ABSD Upgrader Remission is the single most commonly used remission in Singapore and affects tens of thousands of families each year. It applies when a Singapore Citizen or Singapore Permanent Resident purchases a second residential property while still owning an existing one, intending to sell the existing property after moving into the new one.

How It Works

Under the current rules, a Singapore Citizen purchasing a second residential property must pay ABSD at 20% of the purchase price at the point of signing the Option to Purchase (OTP) or Sale and Purchase (S&P) Agreement — within 14 days. The duty is paid first; the remission is claimed after the fact. If the buyer subsequently sells the existing property within 6 months of completing the new purchase, they may apply to IRAS for a full refund of the ABSD paid. The same mechanism applies to Singapore PRs purchasing a second property at the 30% ABSD rate.

| Buyer Profile | ABSD Rate | Remission Available? | Key Condition |

|---|---|---|---|

| SC buying 2nd property | 20% | Yes — full 20% refund | Sell existing within 6 mths of completion |

| SPR buying 2nd property | 30% | Yes — full 30% refund | Sell existing within 6 mths of completion |

| SC buying 3rd+ property | 30% | No — not eligible | Must only hold one other property for remission to apply |

| Foreigner buying any property | 60% | No (except FTA nationals on 1st property) | No upgrader remission for foreigners |

| Entity (company/trust) | 65% | Case-by-case only | Qualifying trust structures may apply — see IRAS guidelines |

The Critical 6-Month Deadline

The 6-month window runs from the date of completion of the new purchase — not from the date you sign the OTP. For a new launch condominium, completion (when the keys are handed over) may be 3 to 5 years after you sign the OTP. This means upgraders buying off-plan have a generous window: the clock only starts ticking when TOP is obtained and legal completion occurs. For resale properties, completion is typically 8 to 12 weeks after signing the OTP, so the window is tighter in practice.

If you miss the 6-month deadline, IRAS will not extend it except in very exceptional circumstances (documented illness, death in the immediate family, force majeure). Do not rely on an extension being granted.

Worked Example — The SC Upgrader

Mr & Mrs Tan are Singapore Citizens who own a Tampines 5-room HDB flat purchased in 2019. In March 2026, they sign an OTP for an Orchard Rd 2BR condominium at S$2,200,000. Within 14 days, they pay:

- BSD: S$79,600 (progressive: 1% on first S$180,000 + 2% on next S$180,000 + 3% on next S$640,000 + 4% on next S$500,000 + 5% on next S$700,000)

- ABSD at 20%: S$440,000

- Total stamp duties upfront: S$519,600

They list their HDB flat and complete the sale in August 2026 — 5 months after the new condominium’s completion date in July 2026. They then apply to IRAS for the ABSD remission. IRAS processes the claim and refunds S$440,000 within approximately 4 to 6 weeks. The Tan family’s net stamp duty cost is thus S$79,600 (BSD only) — exactly the same as a first-time buyer at the same purchase price.

Married Couple Remission — Buying Your First Home Together

The Married Couple Remission (formally the “remission for married couple purchasing first residential property together”) addresses a common scenario: a Singapore Citizen marrying a foreigner or a Permanent Resident, where the couple’s combined nationalities would otherwise attract a higher ABSD rate.

Who Qualifies

The conditions are strict. At the time of purchase, the couple must be legally married (not merely cohabiting). At least one party must be a Singapore Citizen. The property must be their first jointly-owned residential property in Singapore — neither party may own any other residential property in Singapore at the time of purchase. If either party already owns a property, the remission does not apply.

| Couple Profile | Rate Without Remission | Rate With Remission | Saving at S$1.5M |

|---|---|---|---|

| SC + SC (both first property) | 0% | 0% | Nil (no ABSD to begin with) |

| SC + SPR (first joint purchase) | 5% (SPR 1st rate) | 0% | S$75,000 |

| SC + Foreigner (first joint purchase) | 60% (foreigner rate) | 0% | S$900,000 |

| SC (existing property) + SPR | 20% (SC 2nd) or 5% (SPR 1st) | Not eligible — SC already owns property | No remission |

The most significant application is the SC + Foreigner couple. Without the remission, buying a S$2,000,000 condominium would attract ABSD of S$1,200,000 (foreigner rate of 60%). With the Married Couple Remission, ABSD falls to nil — a saving of S$1,200,000 at that price point. This is why the remission is one of the most financially impactful pieces of property law for internationally mixed families in Singapore.

It is important to note that the remission applies at the time of purchase — the couple does not pay ABSD first and then reclaim it. The conveyancing solicitor applies for the remission before e-Stamping the instrument of transfer, and if approved, the stamp duty assessed is nil ABSD from the outset.

Divorce and Court-Ordered Transfers

When a court orders a matrimonial property to be transferred between spouses as part of a divorce settlement, the question of stamp duty arises. Singapore law provides relief in two forms. First, BSD may be remitted on a court-ordered transfer of a matrimonial home between divorcing spouses — the instrument of transfer lodged pursuant to a court order is submitted to IRAS with the order attached, and IRAS will assess whether BSD is payable. Second, an ABSD remission may be available where the transfer results in one party holding the property as their sole property (so the ABSD for a second property would not apply after the divorce).

These cases are assessed on the specific facts by IRAS. Engage a conveyancing solicitor with experience in divorce property transfers to ensure the application is properly structured and timed. The Stamp Duties Act s.15 provides the general power for IRAS to remit duty; ministerial notifications specify which scenarios qualify.

Deceased Estates and Inheritance

When a property owner dies, the transmission of their property to their beneficiaries under a will or intestacy is not an arm’s length commercial transaction. Singapore law accordingly exempts transfers by way of transmission on death from ABSD (Stamp Duties Act s.74). BSD may still be payable on the transmission instrument, but IRAS has published guidance noting that the transmission of property from a deceased to a beneficiary under an approved will or intestacy is generally exempt from stamp duty provided it is not a sale. Families dealing with an estate should confirm the exact position with their estate lawyer, as the specific structure of the transfer (assent, deed of family arrangement, court order of distribution) affects the stamp duty treatment.

Qualifying Remissions for Trusts

Trusts are a more complex area. IRAS has issued guidelines on ABSD for trust arrangements. Generally, where a residential property is transferred into a trust, ABSD is chargeable at 65% — the rate for entities — unless specific conditions are met. The main qualifying condition for a lower ABSD rate (or nil ABSD) is that the trust is an irrevocable discretionary trust whose beneficiaries are all Singapore Citizens. The ABSD is then assessed at the applicable individual rate for the beneficiaries’ profile rather than the entity rate. This area is highly technical and requires legal and tax advice before any trust structure is implemented.

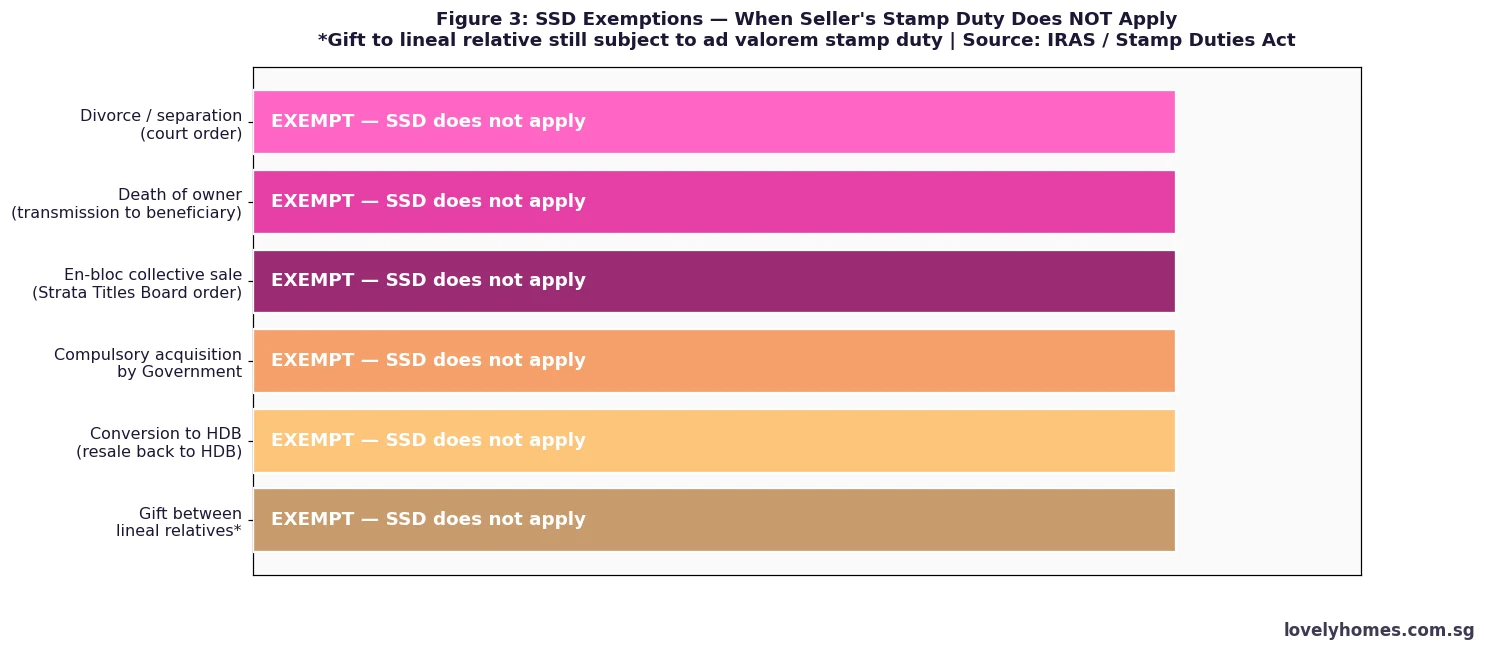

Seller’s Stamp Duty (SSD) Exemptions

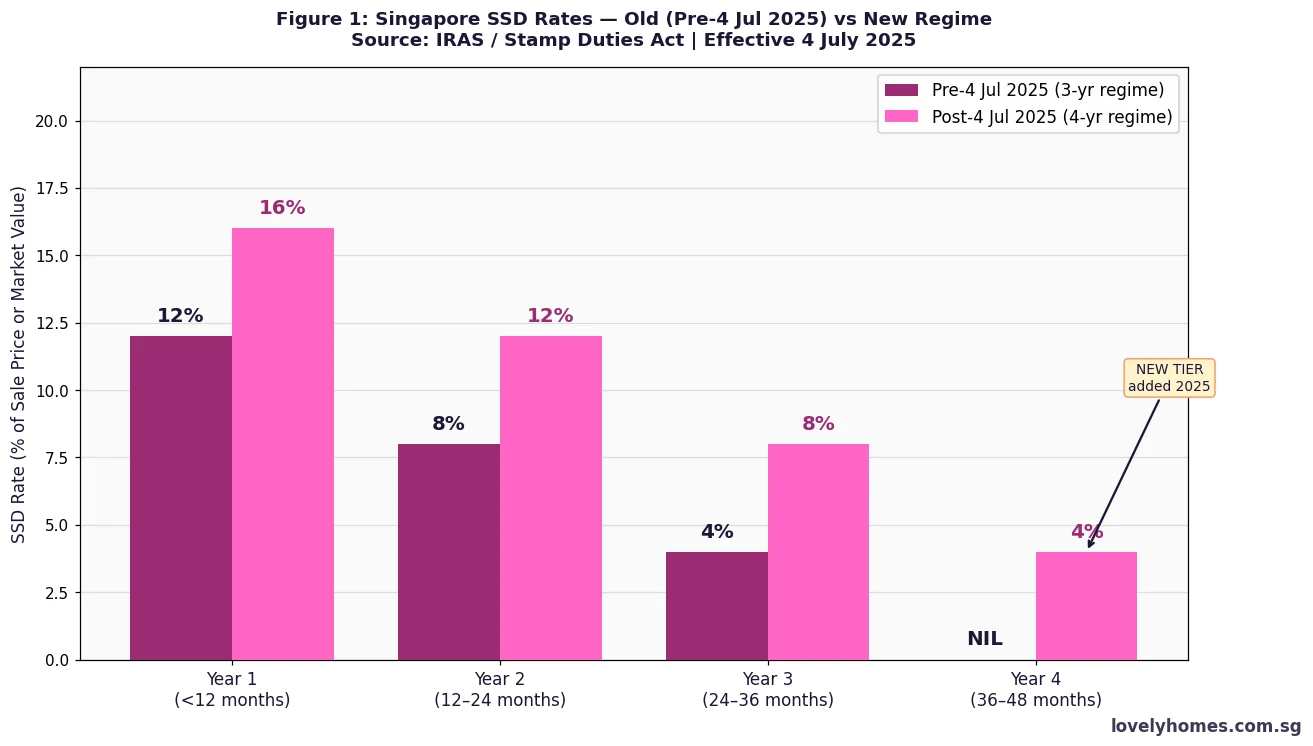

The SSD exemptions are discrete scenarios where the duty simply does not arise, even within the 4-year holding period introduced on 4 July 2025 (rates: 16% / 12% / 8% / 4% in Years 1–4). The following transactions are exempt from SSD:

- En-bloc (collective sale): A property sold as part of a collective sale under the Land Titles (Strata) Act is exempt from SSD regardless of how recently the individual unit was purchased. This is a significant carve-out for owners whose development is acquired en-bloc within their first 4 years of ownership.

- Compulsory acquisition by the State: Where Singaporean authorities acquire a property under the Land Acquisition Act, SSD is not payable.

- Court order (divorce): A property transferred pursuant to a divorce court order is exempt from SSD.

- Death: Transmission of a property on the death of the owner is exempt from SSD.

- Gift to lineal descendants: A property gifted (not sold) to a child, grandchild, or other lineal descendant is exempt from SSD, provided the gift is not commercially motivated and no consideration passes.

- Industrial SSD exemptions: Industrial properties have their own regime (15%/10%/5% over 3 years). The same categories of exemption — compulsory acquisition, death, court orders — apply.

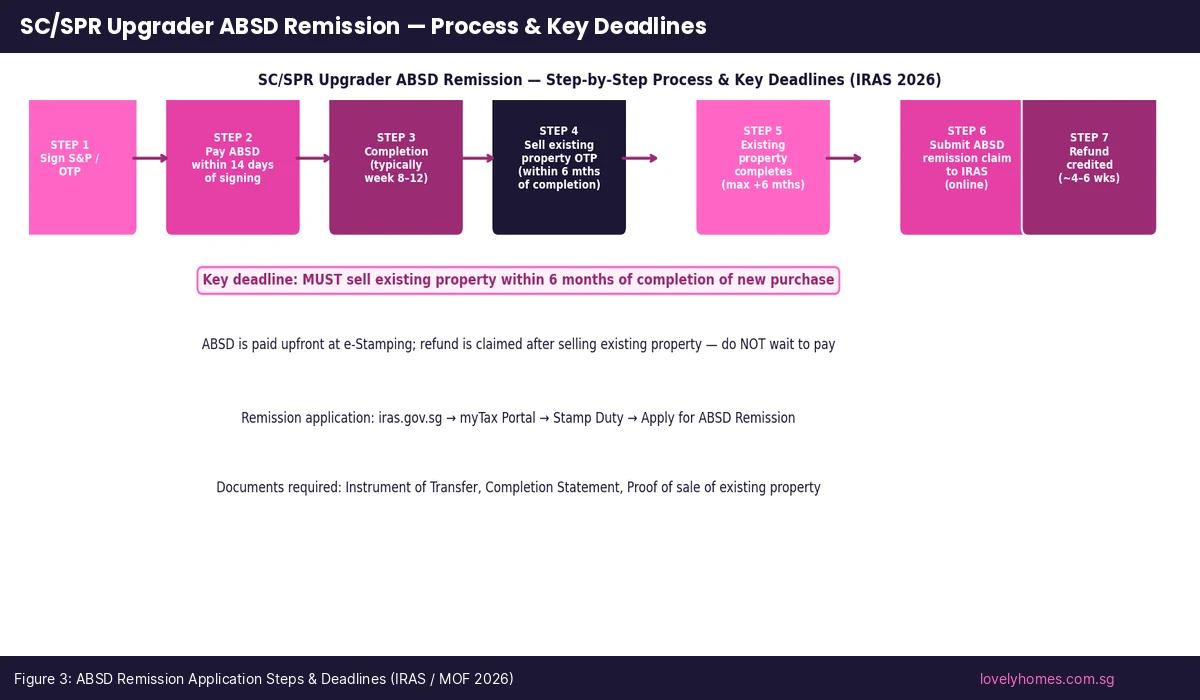

How to Apply for an ABSD Remission — Step by Step

The process for claiming an ABSD remission for upgraders is well-defined. Your conveyancing solicitor will typically guide you through it, but understanding the steps independently protects you from missing a critical deadline.

- Sign OTP or S&P Agreement on the new property. This triggers the 14-day deadline to pay stamp duties (BSD + ABSD).

- Pay BSD and ABSD within 14 days via IRAS e-Stamping or through your solicitor. Note: you must pay ABSD upfront even if you intend to claim a remission. Failure to pay by the deadline incurs penalties.

- Complete the new property purchase. For resale, this is typically 8–12 weeks after OTP. For new launches, this is when TOP is issued and legal completion occurs (potentially years later).

- Sell your existing property within 6 months of the completion date of the new purchase. Sign the OTP, exercise it, and complete the sale — all within the 6-month window.

- File the remission claim at IRAS. Go to myTax Portal → Stamp Duty → Apply for Remission. You must file the claim within 6 months of completing the sale of your existing property (i.e., there are two successive 6-month windows).

- Submit supporting documents: Completion Statement for the new property, Option to Purchase and Sale & Purchase Agreement for the existing property, Completion Statement confirming the sale of the existing property, and your identity documents.

- Receive the refund. IRAS typically processes approved claims within 4 to 6 weeks and credits the refund to the bank account or solicitor’s account you specify.

For married couple remissions, the process is different: your solicitor applies before stamping, submitting the marriage certificate and statutory declarations confirming neither party owns other Singapore residential property. If approved, the instrument is stamped at nil ABSD from the outset.

Common Mistakes and Pitfalls

The most frequent error is missing the 6-month sale deadline. This can happen when sellers are over-confident about finding a buyer, or when the sale falls through at the last minute and the window cannot be recovered. A second common error is assuming the remission applies when one spouse already owns a property — the Married Couple Remission requires both parties to have no existing residential property in Singapore. A third pitfall is failing to maintain the marriage: if a couple applies for the Married Couple Remission and subsequently divorces or annuls the marriage, IRAS may claw back the remission.

Tax professionals also warn against structuring a trust to access lower ABSD rates without proper advice. IRAS scrutinises trust arrangements and applies a facts-and-circumstances test. An arrangement that appears primarily tax-motivated rather than genuinely estate-planning-driven risks being disregarded, with ABSD assessed at the 65% entity rate.

What This Means for You

Singapore’s stamp duty remission framework is materially generous for families following the conventional housing ladder: HDB flat → private property, with a short overlap period. A Singapore Citizen couple upgrading from their HDB flat to a S$1,800,000 condominium will pay S$360,000 in ABSD upfront, but recover every dollar of it within 6 months if they sell the HDB flat on schedule. The net stamp duty cost is simply BSD — S$56,600 at that price, equivalent to 3.1% of the purchase price.

The framework is less generous for those who want to hold multiple properties simultaneously. There is no remission for a Singapore Citizen buying a third property; the 30% ABSD is final. For SPRs and foreigners, the investment calculus must factor in the full ABSD cost as a permanent drag on returns.

The one area where policy may evolve is the trust ABSD regime. The government has signalled that it will continue to monitor whether trust structures are being used to circumvent the cooling measures, and further tightening cannot be ruled out.

Frequently Asked Questions

Can I claim the ABSD upgrader remission if I buy a new launch before my HDB MOP expires?

No. If your HDB flat is still within its Minimum Occupation Period (MOP) — typically 5 years for standard BTO flats, 10 years for Plus/Prime location flats — you are prohibited from privately listing or selling it. This means you cannot sell your HDB flat within the required 6-month window after completing the new purchase. You would therefore be unable to claim the ABSD remission, and the 20% (SC) or 30% (SPR) ABSD paid on the new purchase would be forfeited. Wait until your MOP is completed before purchasing a second property if you intend to rely on the upgrader remission.

What documents does IRAS require for an ABSD remission claim?

You will need: (1) the Instrument of Transfer (stamp certificate) for the new property showing the ABSD paid; (2) the Completion Statement for the new property purchase; (3) the executed Option to Purchase and Sale & Purchase Agreement for the existing property sold; (4) the Completion Statement for the sale of the existing property confirming completion date and proceeds; (5) NRIC / passport copies of the purchasers; and (6) if applicable, proof of marriage (for Married Couple Remission). Your conveyancing solicitor will typically compile this package. IRAS may request additional documents and will reject incomplete applications.

If I paid ABSD on a new launch in 2023 and the TOP is only in 2027, when does the 6-month window start?

The 6-month window starts from the date of legal completion of your new property purchase. For new launch condominiums, this is the date when the developer issues the Certificate of Statutory Completion (CSC), the TOP is obtained, and legal completion takes place — not the date you signed the OTP. So if you signed the OTP in 2023 and TOP/completion is in 2027, you have until approximately 6 months after the 2027 completion date to sell your existing property and file the remission claim. This gives upgraders buying off-plan a significantly longer window than resale purchasers.

Can both the BSD and the ABSD be refunded via remission?

BSD and ABSD are treated separately. The ABSD upgrader remission refunds only the ABSD — not the BSD. BSD is considered a fundamental transaction tax on the acquisition of property and is not remitted for individual buyers under the upgrader framework. The Married Couple Remission also applies only to ABSD (bringing it to nil), not to BSD. BSD remains payable in all standard purchases regardless of remission status. The only scenarios where BSD may be waived are very narrow: government-linked acquisitions, certain approved charities, and specific statutory transfers.

What happens if I cannot sell my existing property within 6 months?

If you miss the 6-month deadline, you lose the right to claim the ABSD remission and the amount paid (20% or 30% of the purchase price) is forfeited. IRAS does not routinely grant extensions. In exceptional cases — certified medical incapacitation of the owner, death of an immediate family member, or an Act of God materially preventing the sale — IRAS may consider an appeal with supporting documentation, but this is discretionary and not guaranteed. Property market conditions (“I could not find a buyer at the price I wanted”) are not accepted as grounds for extension. Plan your sale timeline carefully and engage a property agent well in advance of the deadline.

Does the ABSD upgrader remission apply to the purchase of a commercial or industrial property?

No. The ABSD upgrader remission applies exclusively to the purchase of residential properties (landed houses, apartments, condominiums, executive condominiums before privatisation). Commercial properties (shophouses, offices, retail units) and industrial properties (factories, warehouses) do not attract ABSD in the first place — they are subject only to BSD. There is no equivalent upgrader remission mechanism for commercial or industrial property. The SSD industrial exemptions discussed above are separate and concern selling, not buying.

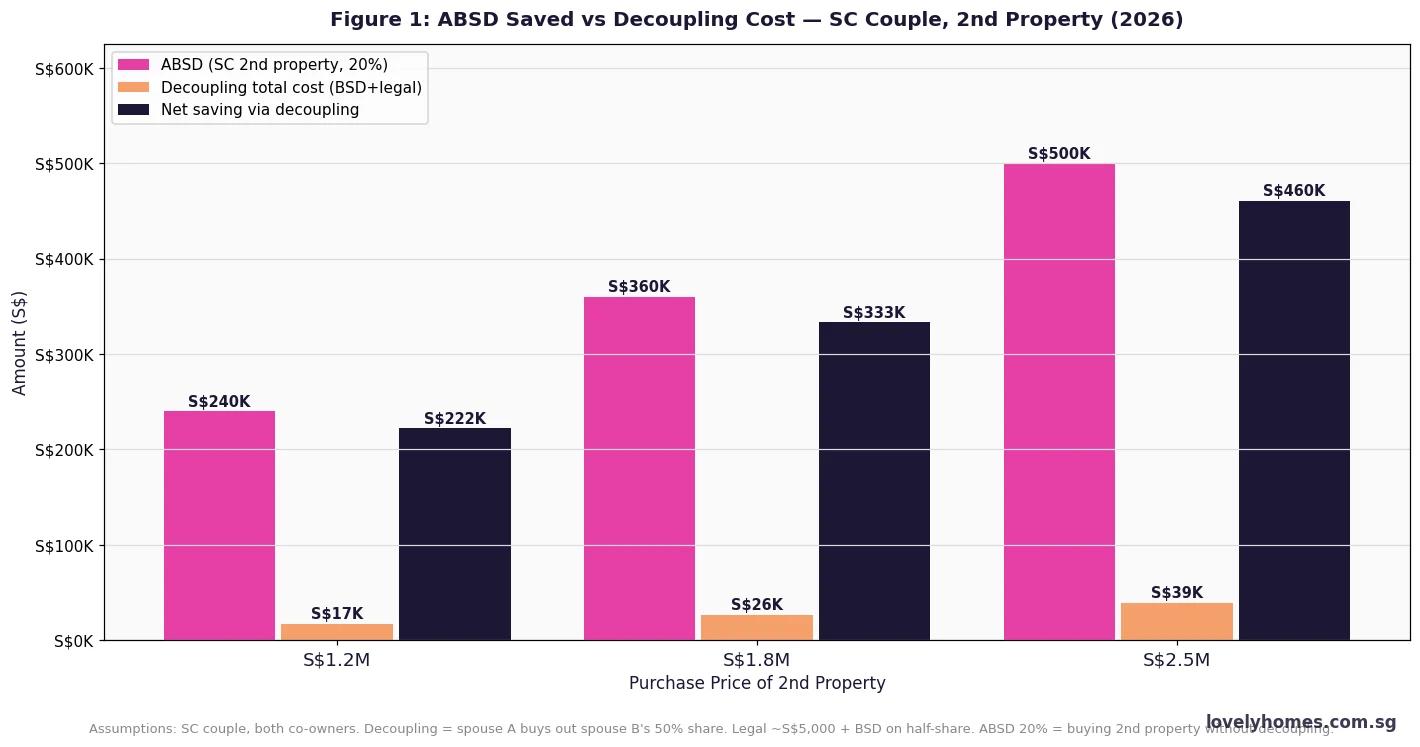

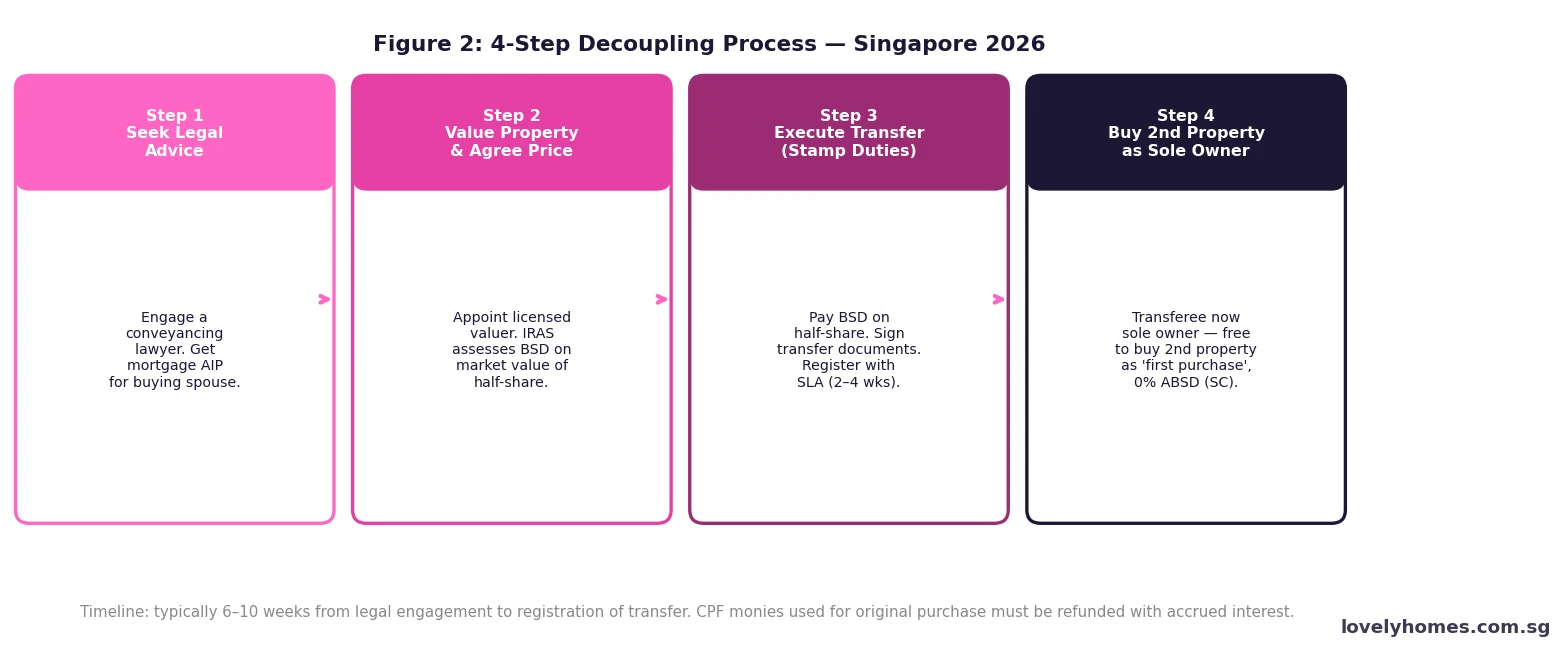

Is there a remission if my spouse and I decouple ownership of our property?

Decoupling — where one co-owner transfers their share to the other so that the transferee becomes the sole owner and the transferor becomes a “first-time buyer” for ABSD purposes on a future purchase — is a legal strategy but does not enjoy a special remission. BSD is payable by the transferee on the share acquired (at the standard progressive rates). There is no BSD or ABSD remission specifically for decoupling transfers. The tax cost of the decoupling (BSD on the transferred share plus legal and valuation fees) must be weighed against the ABSD saving on the future purchase. IRAS treats the transfer at market value and will assess BSD on the higher of the consideration paid or the market value.

Related Articles

- ABSD Singapore 2026 — Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Buyer’s Stamp Duty (BSD) 2026: Rates, Calculations and Worked Examples

- Singapore Seller’s Stamp Duty (SSD) 2026: New 4-Year Holding Period and Rates

- Singapore Property Decoupling Guide 2026: Save ABSD, Costs and Process

- Singapore HDB Upgrading Guide 2026: Costs, ABSD and Step-by-Step Process

- Buying a Condo in Singapore 2026: Complete Guide to Costs and Process

- Singapore Property Investment Guide 2026: How to Buy, Rent and Build Wealth

Disclaimer

This article is published for general informational purposes only and does not constitute legal, tax, or financial advice. Stamp duty rates, remission conditions, and application procedures are subject to change by the Ministry of Finance and IRAS. Always refer to the IRAS Stamp Duty website and the Stamp Duties Act (Cap 312) on Singapore Statutes Online for the authoritative and current position. Seek independent legal and tax advice from a qualified Singapore solicitor or tax practitioner before making property decisions. LovelyHomes does not accept liability for any decisions made in reliance on this article.