Kovan Neighbourhood Guide Singapore 2026: HDB Prices, Condos & Investment Outlook

Quick Answer — Kovan / D19 at a Glance

- District: D19 (Hougang, Kovan, Serangoon North); served by North East Line (NEL) at Kovan (NE13) and Hougang (NE14) stations.

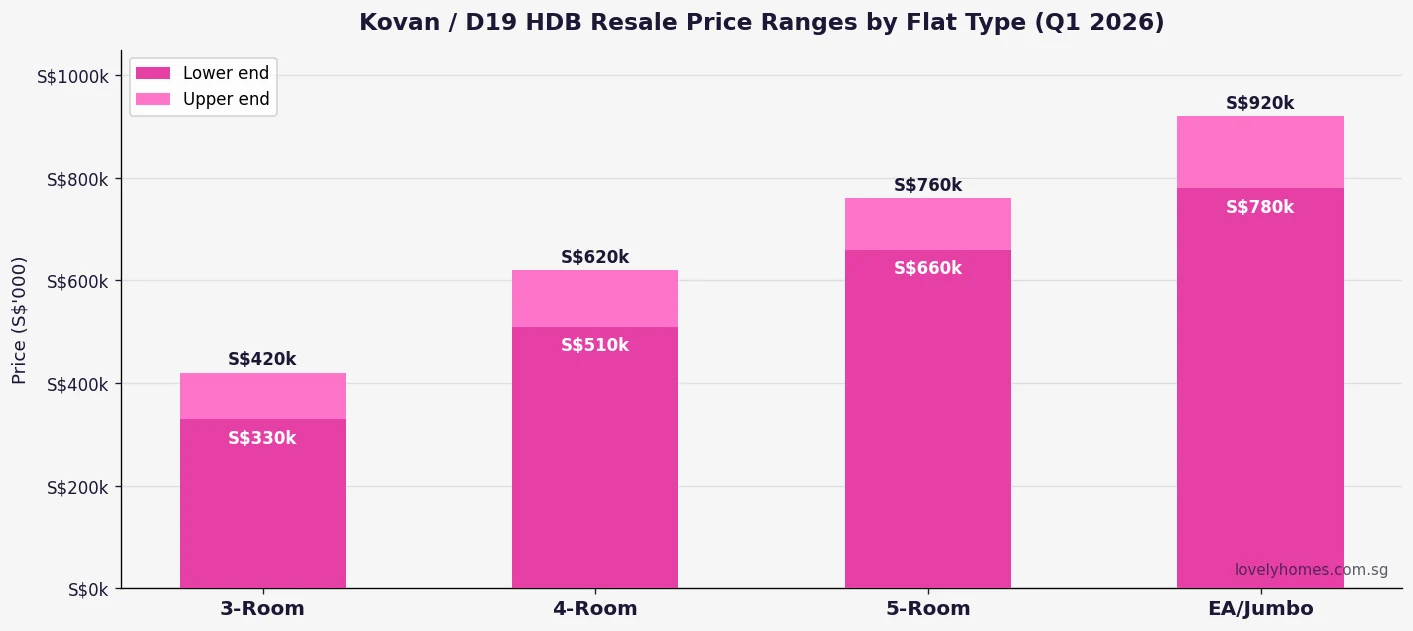

- HDB resale: 4-room flats range from S$510,000–S$620,000; 5-room from S$660,000–S$760,000 (Q1 2026).

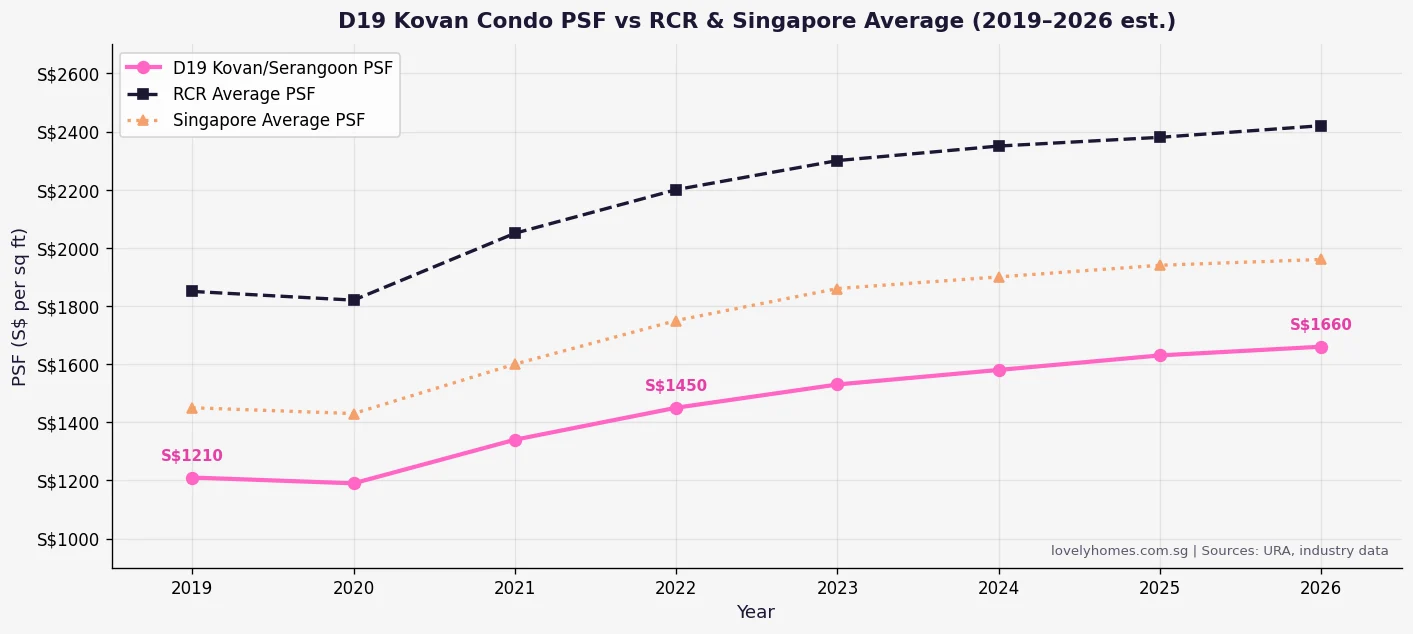

- Condos: Non-landed private homes trade at S$1,450–S$1,700 psf, a meaningful 25–30% discount to RCR average.

- Rental yield: Approximately 3.3–3.6% for Kovan-area condos; strong tenant demand from families and young professionals.

- Schools: Maris Stella High School, CHIJ St Joseph’s Convent, Kovan Primary School and Montfort Secondary within close reach.

- Investment catalyst: The Cross Island Line (CRL) Serangoon North station (Phase 1, 2030) will add a second MRT line to the broader D19 corridor.

- Upcoming supply: Limited new-launch condo pipeline in the immediate Kovan/Hougang precinct keeps resale values supported.

- Buyer profile: HDB upgraders, families seeking mature estate amenities, and investors targeting OCR rental demand.

- BSD: On a S$1.5M condo, Buyer’s Stamp Duty totals S$44,600; ABSD is S$0 for Singapore Citizens buying their first property.

- Next step: Apply for HDB Loan Eligibility (HLE) or bank pre-approval; engage a CEA-registered agent to access HDB resale portal.

What Is the Kovan / D19 Neighbourhood?

Kovan is a mature residential precinct in District 19, nestled in the north-eastern quadrant of Singapore between the more bustling Serangoon and the HDB heartlands of Hougang. Administered by the Hougang–Punggol Town Council (under the broader Aljunied GRC and Hougang SMC divisions), D19 spans Hougang, Kovan, Serangoon North and parts of Upper Serangoon — a broad swathe of land that mixes older public housing, low-density walk-up apartments, newer private condominiums and some semi-detached and terrace houses.

The estate gained a reputation for quiet, laid-back living: tree-lined streets, local coffeeshops, community markets and the charming Kovan F&B hub along Upper Serangoon Road. Unlike the more commercially dense Serangoon or Toa Payoh, Kovan retains a neighbourhood feel, making it a consistent favourite among families who want amenity access without city-centre noise and pricing.

The North East Line (NEL) has anchored the estate’s connectivity since 2003. Kovan MRT (NE13) sits roughly in the centre of the precinct, while Hougang MRT (NE14) serves the broader HDB heartland to the north. The upcoming Cross Island Line (CRL) — with a Serangoon North station planned under Phase 1 (expected 2030) — will add a second MRT line to the broader D19 corridor, strengthening connectivity to Pasir Ris, Jurong and the city core.

HDB Resale Market in Kovan and Hougang

The bulk of public housing in D19 is concentrated in Hougang estate, one of Singapore’s largest and most established HDB towns. Hougang Central and Hougang Street areas contain mostly 3-room to executive apartment blocks built in the 1980s and 1990s, with a smaller supply of newer 4-room and 5-room flats dating from the 2000s. Kovan itself has limited HDB stock — the precinct is dominated more by walk-up apartments and private condominiums — but buyers seeking HDB ownership in D19 typically look at Hougang Ave 2, Hougang Ave 8, Upper Serangoon Road and the Hougang Central cluster.

As at Q1 2026, median transacted prices in D19 for HDB resale flats are as follows: 3-room flats range between S$330,000 and S$420,000 depending on floor level, facing and lease remaining; 4-room flats fall in the S$510,000–S$620,000 band, with prime upper-floor units in sought-after blocks pushing past S$600,000; 5-room flats and executive apartments trade between S$660,000 and S$760,000, and the very best executive apartments (rare in D19) have tested S$920,000.

The HDB resale market in D19 has been steady rather than spectacular. The estate does not attract the speculative frenzy of D3 (Tiong Bahru) or D10 (Bukit Timah), but precisely this stability makes it appealing to genuine owner-occupiers. Resale flat buyers should note that all purchases are subject to the HDB Ethnic Integration Policy (EIP) and the Singapore Permanent Resident (SPR) quota, both of which limit supply in individual blocks and neighbourhoods and can affect resale timing.

Private Condominiums in Kovan D19

The private residential market in Kovan is anchored by a cluster of well-regarded condominiums, most built in the 2000s to mid-2010s. Key developments include:

- The Minton (Hougang St 11, 1,145 units, TOP 2013) — one of the largest private developments in D19; swimming pools, recreational facilities; 4–5 min walk to Hougang MRT.

- Kovan Melody (Kovan Road, 778 units, TOP 2007) — established estate, good rental demand; 6 min walk to Kovan MRT.

- Kovan Residences (Upper Serangoon Road, 393 units, TOP 2013) — freehold tenure; one of the area’s premium addresses.

- The Scala (Serangoon Ave 3, 468 units, TOP 2013) — adjacent to NEX mall and Serangoon MRT interchange; technically D19/D13 border.

Transacted PSF across these developments ranges from S$1,450 to S$1,700 in Q1 2026, with freehold units (notably Kovan Residences) commanding a 12–15% premium over leasehold stock. This represents a roughly 25–30% discount to the RCR average (approximately S$2,300–S$2,500 psf) — a meaningful value proposition for buyers who want private housing without paying CCR or RCR prices.

Rental demand is supported by the estate’s family-friendly character, school proximity and NEL connectivity. A 3-bedroom unit at The Minton or Kovan Melody typically commands S$4,200–S$5,200/mth in 2026, translating to gross rental yields of approximately 3.3–3.6%. These are modest by CCR standards but comparable to other OCR-fringe estates.

Schools and Education

D19’s school roster is one of its strongest selling points for family buyers. Within the 1km registration radius of Kovan MRT or Hougang Central, buyers can access:

| School | Type | Distance from Kovan MRT | Notable |

|---|---|---|---|

| Kovan Primary School | Primary | ~600m | SAP school; bilingual programme |

| Xinghua Primary School | Primary | ~900m | Established, strong CCA programme |

| CHIJ St Joseph’s Convent | Girls’ Primary (mission) | ~1.2km | MOE school, strong pastoral tradition |

| Maris Stella High School | Independent (boys) | ~1.1km | Consistently top-ranked independent school |

| Montfort Secondary School | Secondary | ~1.4km | SAP school; strong performing arts |

| Serangoon Garden Secondary | Secondary | ~2km | Near Serangoon Gardens precinct |

Maris Stella High School in particular has long driven family buyer demand in the Kovan precinct. As an independent all-boys school with direct-admission and talent programmes, it consistently attracts families who prioritise secondary school options at point of primary registration. The 1km radius around Kovan MRT encompasses Maris Stella’s registration zone, making addresses near Upper Serangoon Road and Kovan Road especially sought-after for family buyers.

Amenities and Lifestyle

Kovan’s retail scene is deliberately low-key. The area’s character is defined by its Kovan food enclave — a cluster of independent F&B outlets, local eateries, cafés and neighbourhood shops along Kovan Road and Upper Serangoon Road, stretching roughly between Kovan MRT and Hougang MRT. This strip has gentrified quietly over the past decade and now includes artisan coffee shops, Japanese restaurants, local hawker favourites and weekend farmers’ market pop-ups.

For larger retail needs, residents have quick access to:

- Heartland Mall Kovan — a medium-sized suburban mall at Kovan MRT, anchored by Fairprice and a mix of F&B and services.

- Hougang Mall — near Hougang MRT; NTUC FairPrice anchor, cinema and family dining.

- NEX Mall Serangoon — two stops away on the NEL; one of the largest suburban malls in Singapore with 580,000 sq ft of retail, a rooftop pet pool and family entertainment.

Parks and green spaces include Hougang Stadium, the tree-lined corridors of Kovan Road and the Serangoon Park Connector, which connects to the broader round-island park connector network. The Punggol Waterway is one NEL stop further and provides a riverside recreational option that many D19 residents treat as their extended backyard.

Connectivity: NEL and the Coming CRL Uplift

The North East Line (NEL) is D19’s primary rail artery. From Kovan MRT (NE13), the NEL runs direct to:

- Serangoon interchange (NE12) — 1 stop, connection to CCL and Bishan

- Dhoby Ghaut (NE6) — 6 stops, interchange with NSL and CCL (city centre)

- Outram Park (NE3) — 9 stops, connection to EWL and TEL (city fringe)

Journey time from Kovan to Raffles Place is approximately 25–30 minutes by train — competitive with many CCR and RCR addresses when accounting for door-to-door travel. The NEL’s operational frequency of approximately 2.5 minutes during peak hours makes it one of the more reliable commuter lines.

The transformative catalyst for D19’s medium-term investment story is the Cross Island Line (CRL). CRL Phase 1, currently under construction, includes a Serangoon North station that will sit approximately 1.5km west of Kovan MRT, within the broader D19 corridor. When completed (expected around 2030), this station will offer a direct cross-island rail connection from Hougang / Serangoon North through Punggol, Ang Mo Kio, Bright Hill, Clementi, West Coast and on to Changi — dramatically reducing transfer requirements for residents who currently commute to the north-west or south-west.

Research by the Urban Redevelopment Authority (URA) and independent property analysts consistently shows MRT proximity within 500m commands a 5–12% price premium for private residential properties. The CRL effect, though not yet priced in for Kovan proper (Kovan MRT is NEL, not CRL), is expected to lift values in Serangoon North sub-zones within D19 over the 2027–2032 period as construction activity and station footprints become visible.

Investment Outlook for Kovan D19

From a property investment standpoint, D19 sits in a compelling mid-tier position: established enough to have deep rental demand and school-driven owner-occupier interest, but not yet priced to perfection in the way that D11 (Novena) or D9 (Orchard) are. The PSF discount to RCR (~25–30%) and to CCR (~40–45%) creates a valuation buffer that appeals to value-oriented investors.

The supply picture is favourable. There are no major new-launch condominium sites in the immediate Kovan/Hougang precinct in URA’s 2H 2026 GLS Confirmed List. The most proximate recent supply came from Kovan Jewel and a handful of boutique freehold developments. This supply scarcity, combined with steady rental demand (especially from families with children at Maris Stella and Kovan Primary), supports occupancy rates of 92–95% in well-managed D19 condominiums.

Risks to monitor include: broader Singapore macro headwinds (higher-for-longer interest rates compressing buyer affordability); the ABSD regime (which makes multiple-property investment expensive for Singapore Citizens and essentially prohibitive for Singapore Permanent Residents and foreigners); and the five-year Seller’s Stamp Duty (SSD) holding-period requirement, which locks in investors for a minimum period before tax-free disposal is possible. Buyers should also note that ABSD for a Singapore Citizen’s second property is 20%, significantly raising the cost of entry for investors who already own one property.

Worked Example: Buying a 4-Room HDB Resale Flat in Hougang

Case Study — Lim Couple (SC/SC), First HDB Resale Purchase

Profile: Mr and Mrs Lim, Singapore Citizens, both aged 33, combined gross household income S$7,200/mth, no existing property ownership.

Target: 4-room HDB resale flat, Hougang Ave 8, Blk 418C (5th floor), 92 sqm, lease commencing 1993 (72 years remaining).

Agreed price: S$578,000.

CPF Housing Grants available:

- Enhanced Housing Grant (EHG): S$30,000 (income S$7,200/mth, both first-timers)

- Family Grant (resale, SC/SC): S$50,000

- Total grants: S$80,000

Financing (HDB loan):

- Purchase price: S$578,000

- Less grants: S$80,000

- Net purchase price: S$498,000

- HDB loan (80% LTV): S$462,400 @ 2.60% p.a. over 25 years

- Monthly repayment: approximately S$2,099/mth

- MSR check: S$2,099 / S$7,200 = 29.2% — PASS (must be ≤30%)

Stamp duty:

- BSD on S$578,000: 1% × S$180k + 2% × S$180k + 3% × S$218k = S$1,800 + S$3,600 + S$6,540 = S$11,940

- ABSD: S$0 (SC, first property)

Upfront cash required:

- 20% downpayment (cash + CPF): S$115,600; CPF OA (assumed S$60,000 each) covers S$80,000 → cash S$35,600

- BSD in cash: S$11,940

- Legal and admin fees: ~S$2,500

- Total cash outlay: approximately S$50,040

Note: Actual grant amounts depend on household income, citizenship status and eligibility checks by HDB at point of application. TDSR and MSR calculations are indicative; engage an HDB officer or licensed mortgage broker for a precise assessment.

What the Numbers Mean for Buyers

Kovan / D19 offers a rare combination in Singapore’s property market: school-belt proximity, mature estate amenities, NEL connectivity and pricing that remains accessible to HDB upgraders and first-time private property buyers alike. The Lim couple’s example illustrates how an S$578,000 4-room resale flat — with maximum grants reducing the effective loan to S$462,400 — delivers an MSR of 29.2% at a S$7,200/mth combined income, leaving meaningful financial headroom for living expenses, savings and future property goals.

For investors, the S$1,450–S$1,700 psf price band for Kovan condominiums compares favourably to equivalent-quality stock in D13 (Serangoon) or D14 (Geylang/Eunos), while offering better school catchment and a quieter living environment. The CRL uplift story — though not yet a reality — gives D19 a medium-term catalyst that many other mature OCR estates lack.

What might come next for Kovan? URA’s long-term planning maps indicate densification of the Upper Serangoon Road corridor, with some existing industrial and mixed-use sites potentially rezoned for residential or mixed-development use over the next decade. Any rezoning announcements would act as material catalysts for land value and, consequently, resale prices in the immediate vicinity.

Frequently Asked Questions

Is Kovan a good area to live in Singapore?

Yes, Kovan is consistently rated as one of Singapore’s most liveable mature OCR estates. Its combination of North East Line connectivity, reputable schools (Maris Stella High, Kovan Primary), a vibrant independent F&B scene, low-density residential character and competitive property prices make it particularly popular with families. It lacks the commercial density of Toa Payoh or Tampines but offers a quieter, more residential lifestyle that many owner-occupiers prefer. The upcoming Cross Island Line Serangoon North station (Phase 1, ~2030) will further strengthen its connectivity case.

What are HDB resale flat prices in Hougang / Kovan 2026?

As at Q1 2026, 4-room HDB resale flats in the Hougang / Kovan D19 area are transacting in the range of S$510,000–S$620,000. 5-room flats and executive apartments fetch S$660,000–S$760,000. 3-room flats — increasingly limited in supply — range from S$330,000 to S$420,000. Premium units with long remaining leases (70+ years), high floors or desirable block facings tend to transact at the upper end or occasionally above the range. All HDB resale transactions require an Option to Purchase (OTP) and are subject to EIP and SPR quota restrictions.

Can foreigners buy property in Kovan / D19?

Foreigners (non-Singapore Citizens and non-Permanent Residents) are prohibited from purchasing HDB flats under any circumstances. For private condominiums in D19 — such as The Minton, Kovan Melody or Kovan Residences — foreigners may purchase subject to paying Additional Buyer’s Stamp Duty (ABSD) of 60% of the purchase price (as at January 2024, per IRAS). This is in addition to Buyer’s Stamp Duty (BSD) of approximately S$43,800–S$54,600 on a S$1.5M unit. Singapore Permanent Residents buying their first property pay 5% ABSD. The cost burden makes foreign investment in private condominiums in D19 generally marginal on a yield basis, though some investors still proceed for capital appreciation or estate-planning reasons.

Which condos are near Kovan MRT?

The closest condominiums to Kovan MRT (NE13) include Heartland Mall Kovan (retail, not residential), Kovan Melody (~650m, 778 units, leasehold 99yr, TOP 2007), Kovan Residences (~800m, 393 units, freehold, TOP 2013) and The Scala (~1.2km towards Serangoon). Further along Hougang Ave, The Minton (1,145 units, leasehold, TOP 2013) is approximately 1km from Hougang MRT. There are no major new-launch condominiums currently available for purchase in the immediate Kovan/Hougang precinct as at July 2026; the nearest new-launch pipeline is in Tampines North and the Greater Plantation Loop.

How does the CRL Serangoon North station affect D19 property values?

The Cross Island Line (CRL) Phase 1 Serangoon North station is expected to open around 2030 and will sit approximately 1.5km from Kovan MRT within the broader D19 corridor. Property research consistently shows that MRT stations within 500m of a development command a 5–12% premium over comparable properties without such proximity. Properties directly adjacent to the Serangoon North station box (likely between Upper Serangoon Road and Ang Mo Kio Ave 3) stand to benefit most. Kovan proper (served by the existing NEL) is less directly exposed, but improved network connectivity across D19 broadly supports price floors and rental demand. Buyers who can identify future station catchment areas ahead of station opening often capture the best appreciation.

What CPF Housing Grants are available for HDB resale in D19?

First-timer Singapore Citizens buying an HDB resale flat in D19 may be eligible for the Enhanced Housing Grant (EHG) — up to S$80,000 for individuals or S$160,000 for families depending on household income — and the Family Grant of up to S$50,000 (SC/SC couple) or S$40,000 (SC/SPR couple). The Proximity Housing Grant (PHG) of up to S$30,000 is available when buying within 4km of parents or children. Grants are administered by HDB and disbursed directly against the purchase price or loan. Full details on eligibility conditions, income ceilings and grant stacking rules are covered in our HDB CPF Housing Grant Guide 2026.

What is the Minimum Occupation Period (MOP) for Kovan HDB flats?

All HDB flats in D19 — whether Standard, Plus or Prime classification — are subject to a Minimum Occupation Period (MOP) before the flat can be sold on the open resale market or rented out entirely. For Standard flats in Hougang / Kovan, the MOP is 5 years from date of key collection (or from the date the last occupier moves in, if applicable). Plus flats (a newer classification introduced in August 2024) carry a 10-year MOP. Prime flats have a 10-year MOP with a subsidy clawback on resale. The HDB does not classify existing Hougang and Kovan flats as Prime; they are generally Standard or Plus depending on specific project and location. Full MOP rules are detailed in our HDB MOP Complete Guide 2026.

Related Articles

- Novena Neighbourhood Guide Singapore 2026: D11 Medical Hub, Prices & Investment Outlook

- East Coast Neighbourhood Guide Singapore 2026: D15 Prices, TEL Impact & Investment Outlook

- Hougang Neighbourhood Guide Singapore 2026

- Kallang Neighbourhood Guide Singapore 2026: HDB, Condos & the Kallang Alive Opportunity

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- HDB CPF Housing Grant Guide 2026: EHG, Family Grant, PHG and Singles Grant Explained

- Buyer’s Stamp Duty Singapore 2026: Complete Guide to BSD Rates and Calculation

- HDB Ethnic Integration Policy (EIP) Singapore 2026: Quotas, Eligibility and What Buyers Must Know

Disclaimer

The information in this article is provided for general informational purposes only as at July 2026 and does not constitute financial, legal or property investment advice. Property prices, HDB resale figures, PSF data and grant amounts are indicative based on available URA, HDB and industry transaction data and may differ from actual conditions at time of purchase. All property transactions in Singapore are subject to prevailing stamp duty rates (ABSD, BSD, SSD), HDB eligibility rules, CPF Board regulations and financial institution lending criteria. Readers should consult a CEA-registered property agent, a licensed mortgage adviser and where appropriate a qualified lawyer before making any property purchase decision. For authoritative information, refer to the Urban Redevelopment Authority (ura.gov.sg), Housing & Development Board (hdb.gov.sg), Inland Revenue Authority of Singapore (iras.gov.sg) and the Monetary Authority of Singapore (mas.gov.sg).

Click anywhere or press Esc to close