Singapore Property Market Mid-Year Outlook 2026: Prices, Trends and What the Second Half Holds

Quick Answer: Singapore Property Market Mid-Year 2026

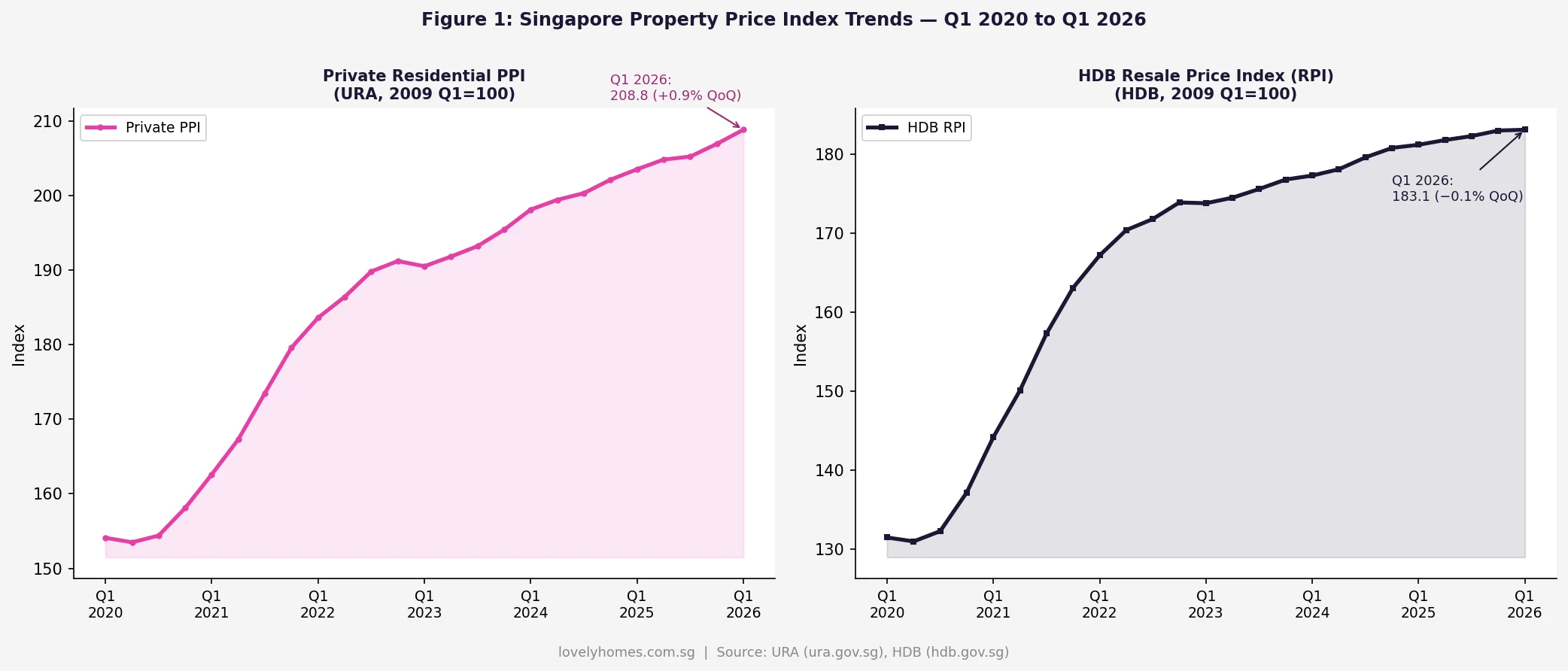

- Private residential prices rose 0.9% in Q1 2026 — the sixth consecutive quarter of increase, with the price index reaching 208.8 (2009 Q1 = 100).

- HDB resale prices edged down 0.1% in Q1 2026 — the first quarterly decline since Q1 2023, though the Resale Price Index remains at a historically elevated 183.1.

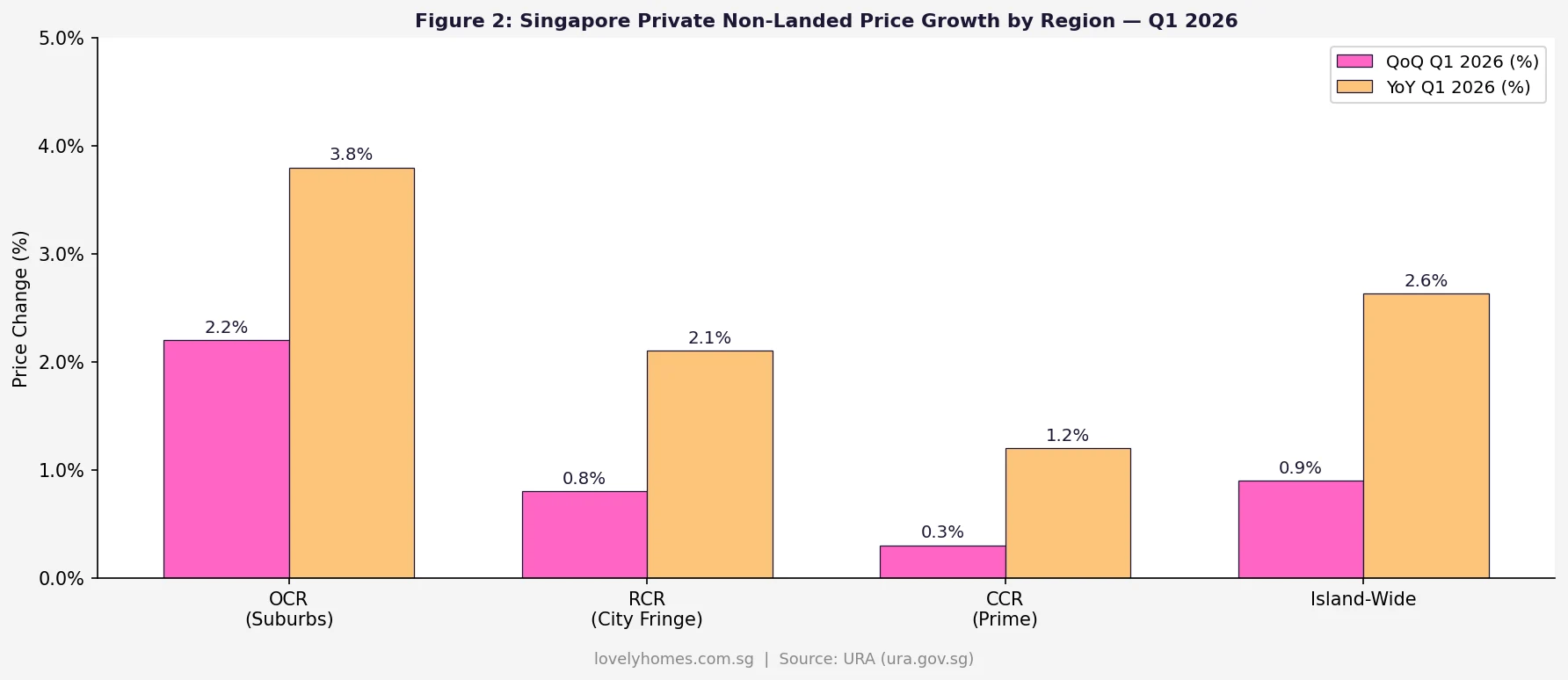

- Suburbs (OCR) led price gains at 2.2% QoQ, outpacing the city fringe (RCR) at 0.8% and prime districts (CCR) at 0.3%.

- 42,561 private units in the pipeline as at Q1 2026, with 17,032 remaining unsold — adequate supply is expected to keep price growth measured in 2H 2026.

- Full-year 2026 forecast: industry research desks project approximately 3% private residential price growth, with suburban condominiums and mid-market segments continuing to outperform.

- River Valley Green (Parcel C) tender closed today (18 June 2026) — award expected in approximately four weeks; signals continued institutional appetite for prime residential land.

Singapore’s property market enters the second half of 2026 in a state of cautious optimism. Prices are rising, but at a measured pace that reflects both MAS cooling measures and tighter buyer affordability. Transaction volumes have moderated, yet well-located new launches continue to see strong take-up at launch weekends. This mid-year analysis draws on URA and HDB Q1 2026 data — the most current available — to assess where the market stands and what the second half may hold.

Private Residential Market: Six Quarters of Unbroken Growth

The URA Private Residential Property Price Index reached 208.8 in Q1 2026, up 0.9% from Q4 2025’s 206.9. This marks six consecutive quarters of positive growth — a run that began after the brief pause in Q1 2023 following the April 2023 cooling measure increase. The cumulative gain since Q1 2023 (190.5) stands at 9.6%, equivalent to a modest but consistent appreciation trajectory.

The trajectory in Figure 1 reveals a key structural shift: the steep post-2021 rise has moderated into a gentle upward slope, suggesting that the market has absorbed the 2023 cooling measures and found a new equilibrium. Critically, prices have not corrected significantly — the cooling measures slowed momentum rather than reversed it.

OCR Leads: Suburban Condominiums Driving Growth

Not all segments of the private market moved equally in Q1 2026. The Outside Central Region (OCR) — encompassing HDB upgrader demand in the suburbs — recorded the strongest growth at 2.2% QoQ, against the Rest of Central Region (RCR) at 0.8% and the Core Central Region (CCR) at 0.3%. This pattern has been consistent since 2023 and reflects a structural demand driver: the large cohort of HDB flat owners whose Minimum Occupation Periods are maturing, giving them access to their CPF proceeds and equity to fund private property purchases.

The year-on-year (YoY) figures reinforce the OCR leadership: at 3.8% YoY, suburban condominiums have outperformed the island-wide average of 2.63%. For buyers targeting long-term capital appreciation, the data continues to favour well-located OCR projects near MRT stations in growth corridors such as Punggol Digital District, Jurong Lake District, and Woodlands Regional Centre.

HDB Resale: The First Dip in Three Years

The HDB Resale Price Index registered a marginal -0.1% in Q1 2026 — the first quarterly decline since Q1 2023. This does not signal a market downturn; at 183.1, the RPI remains close to its all-time high (183.1 in Q4 2025) and the volume of million-dollar HDB transactions remained elevated in early 2026. Rather, the mild softening reflects a combination of factors: the additional 30-month wait for buyers with prior private property experience, the expanded HDB BTO supply pipeline, and general affordability pressure at the upper end of the HDB resale market.

For HDB upgraders, the moderation in resale prices may actually be beneficial — it reduces the risk of overpaying for an HDB flat just before a condo purchase, as the HDB asset they are selling remains close to peak value whilst the risk of further HDB price acceleration is tempered. Read our HDB Resale Flat Prices Guide 2026 for detailed data by flat type and town.

Supply: 42,561 Units in the Pipeline

As at Q1 2026, URA reports 42,561 private residential units (including Executive Condominiums) with planning approval, of which 17,032 remain unsold by developers. This inventory level is above the recent 5-year average of approximately 14,000 unsold units, providing a meaningful supply buffer against price spikes in 2H 2026 and into 2027.

| Market Segment | Q1 2026 Price Change (QoQ) | YoY Change | 2H 2026 View |

|---|---|---|---|

| Private Non-Landed (OCR) | +2.2% | +3.8% | Continued support from HDB upgrader demand |

| Private Non-Landed (RCR) | +0.8% | +2.1% | Selective strength; site-specific |

| Private Non-Landed (CCR) | +0.3% | +1.2% | Muted; foreign buyer ABSD effect persists |

| Landed Residential | +0.5% | +1.8% | Constrained supply; stable demand |

| HDB Resale (RPI) | −0.1% | +1.5% | Mild moderation; supported by BTO delays |

GLS Market: River Valley Green Parcel C Closes Today

The Government Land Sales (GLS) market provided a timely data point today (18 June 2026) as the tender for River Valley Green (Parcel C) closed at noon. This 11,516 sqm site next to Great World City MRT station — the last undeveloped plot in the River Valley Green enclave — is expected to yield approximately 470 residential units. The adjacent Parcel B attracted five bids when it closed in February 2025 at a land rate of $1,420 per square foot per plot ratio (psf ppr).

The tender award (expected in approximately 4 weeks) will be a closely watched indicator of developer confidence in the prime residential segment. A land rate above $1,500 psf ppr would signal continued appetite for CCR sites despite the 60% ABSD on foreign buyers. The 2H 2026 GLS programme, which HDB and URA released in June, continues to inject supply — particularly in the suburban corridors.

What Might Come Next: Second Half 2026 Outlook

The following is forward-looking analysis, not a price forecast or investment advice.

The consensus view from industry research desks points to full-year 2026 private residential price growth of approximately 3%, with OCR non-landed leading and CCR lagging. Three factors could alter this trajectory in either direction:

- MAS interest rate environment: SORA-linked floating rates remain at approximately 3.0–3.4% as at June 2026. Any reduction in US Federal Reserve rates — expected by some analysts in late 2026 — would ease SORA and reduce effective mortgage costs for Singapore borrowers, potentially stimulating upgrader activity in Q4 2026 and Q1 2027.

- ABSD policy review: The government has signalled no near-term review of ABSD rates. Any reduction of the SC second-property rate (currently 20%) would significantly unlock pent-up HDB upgrader demand. Conversely, any further increase would weigh on the OCR segment that has been the market’s growth engine.

- New launch pipeline quality: Several large-scale OCR new launches are expected in 2H 2026 from GLS sites awarded in 2024–2025. Strong opening weekends at these launches would validate the upgrader demand thesis; weak take-up would signal affordability limits have been reached at current price points.

What This Means for Buyers in Mid-2026

For first-time buyers: the market is not cheap, but it is not in a speculative bubble either. Price growth is moderate, supply is adequate, and interest rates — whilst elevated versus 2021 — are stable. If your financial position qualifies you for a bank loan and your timeline is 5 years or longer, the current environment does not present an extraordinary risk of a sharp near-term correction.

For HDB upgraders: the HDB-to-private upgrade window remains open. HDB resale values are near peak, giving you maximum equity to deploy. The OCR condo segment continues to see the strongest demand from buyers in similar circumstances to yours — buy into quality, not just momentum. See our HDB Upgrader Condo Buying Guide 2026 for a full financial roadmap.

For investors: the rental market remained resilient through early 2026 despite earlier forecasts of rental corrections. Gross yields for well-located OCR condos are approximately 3.0–3.8%, providing a positive carry on leveraged purchases at current bank rates. Rental income is taxable — see our Singapore Property Rental Income Tax Guide 2026 for the full IRAS framework.

Frequently Asked Questions

Where can I find official Singapore property price data?

URA publishes quarterly private residential price statistics at ura.gov.sg. The Urban Redevelopment Authority releases flash estimates in the first week of each new quarter, followed by full statistics approximately 4–5 weeks later. HDB publishes its Resale Price Index and transaction data at hdb.gov.sg. Both datasets are freely available and updated quarterly.

What is the difference between the PPI and individual condo prices?

The URA Private Property Price Index (PPI) is a volume-weighted aggregate index of all private residential transactions island-wide. Individual condo prices can diverge significantly from the PPI — a new launch in a prime location may appreciate 10% in a year whilst the PPI rises 2%. Use the PPI as a broad directional indicator, but base purchase and sale decisions on comparable transaction (caveats) data for the specific development or district you are evaluating.

Will the River Valley Green Parcel C award affect condo prices in the area?

GLS land awards typically influence pricing in the surrounding micro-market. A high land rate at River Valley Green Parcel C would signal developer confidence in the Great World City / River Valley corridor and may support asking prices at nearby resale condos (including the completed Parcel A and Parcel B projects). However, new launch pricing from the awarded parcel is unlikely to enter the market for 3–4 years (construction to TOP), so the near-term impact on existing resale condos is mostly psychological.

Has the 30-month wait for private property sellers affected the resale market?

Yes. The 30-month wait — introduced in September 2022 — requires sellers of private residential properties to wait 30 months before they can purchase an HDB resale flat (if they intend to downgrade). This has reduced the supply of private resale properties from buyers who might otherwise have sold to downgrade into an HDB flat. The effect has been most visible in reducing transaction volume at the lower end of the condo market (1-bedroom to 2-bedroom units in the OCR priced below $1.5M), where owner-occupiers seeking to downgrade to HDB have been deterred from selling.

When will URA release Q2 2026 flash estimates?

URA typically releases quarterly flash estimates in the first week of the following quarter. Q2 2026 flash estimates are expected in the first week of July 2026, with full Q2 2026 statistics released approximately 4–5 weeks thereafter (likely early-to-mid August 2026). LovelyHomes will publish a full analysis immediately upon release — bookmark our Q2 2026 URA Flash Estimates page for that update.

Related LovelyHomes Guides

Click anywhere or press Esc to close