Singapore New Home Sales April 2026: URA Data Released as Q2 Rebound Gets Under Way

Quick Answer — Singapore Developer Sales April 2026

- URA released April 2026 monthly developer sales data on 15 May 2026.

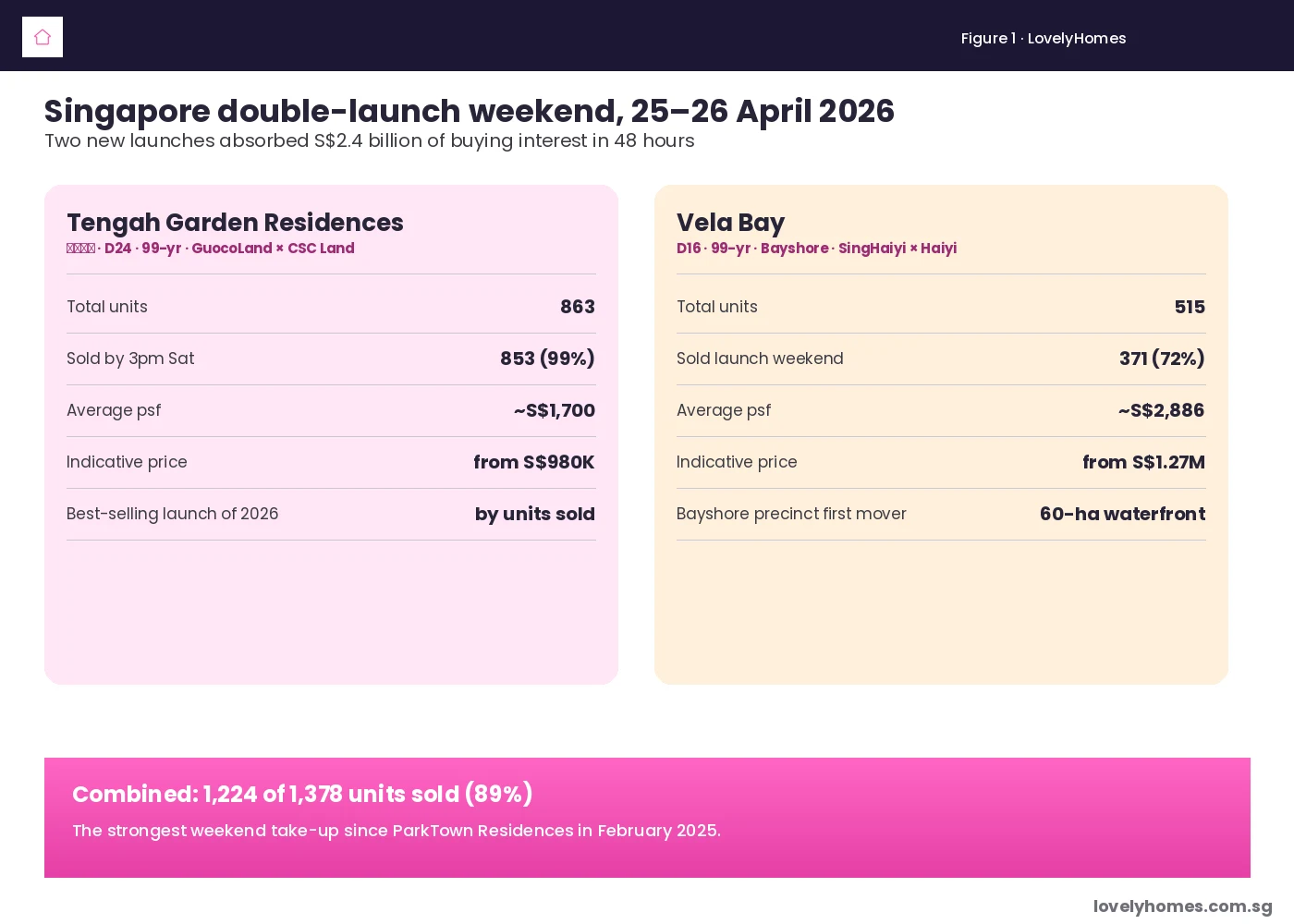

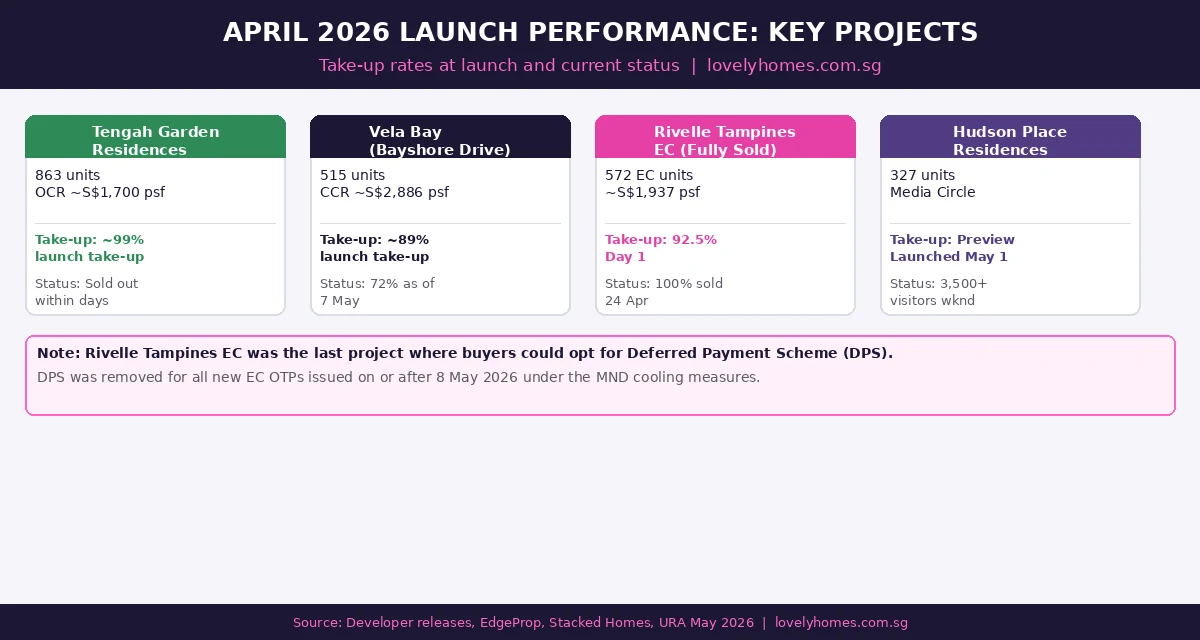

- April was driven by two blockbuster late-month launches: Tengah Garden Residences (~863 units, OCR, ~S$1,700 psf) and Vela Bay (515 units, CCR, ~S$2,886 psf), which together cleared approximately 1,224 units in a single 48-hour launch weekend.

- Rivelle Tampines EC (572 units) was fully sold out in April — the last EC project in 2026 where buyers could use the Deferred Payment Scheme (DPS) before it was removed on 8 May 2026.

- Q2 2026 has begun with stronger momentum than Q1 2026’s 1,294-unit total (which was weaker due to a light launch calendar).

- The declining SORA rate (now ~1.20%, down from peak 3.68%) is improving affordability for new home buyers on floating-rate loans.

- Key Q2 pipeline still to launch: Lentor Gardens Residences (499 units), and further OCR projects as GLS sites progress.

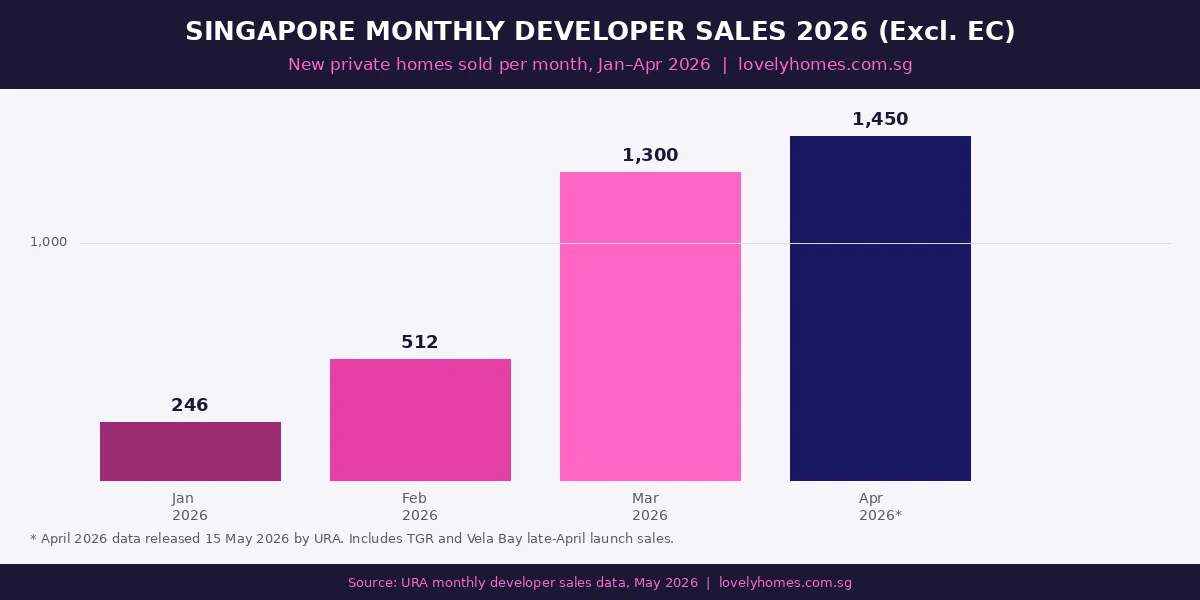

Singapore’s Urban Redevelopment Authority (URA) released its monthly developer sales statistics for April 2026 on 15 May 2026, and the headline picture is a significant rebound from Q1 2026’s subdued volumes. After a first quarter that recorded just 1,294 new private homes sold excluding executive condominiums — a figure depressed by a deliberately thin launch calendar — April’s late-month double launch of Tengah Garden Residences and Vela Bay changed the narrative.

For buyers, developers, and investors watching Singapore’s new launch market, April 2026 provides several important data points. This article breaks down what the monthly figures show, which projects drove the numbers, what the fully-sold Rivelle Tampines EC tells us about post-cooling-measures demand, and what to expect through the rest of Q2 2026.

1. Q1 2026 in Context: A Quiet Quarter by Design

Before analysing April, it is important to understand why Q1 2026 was so subdued. The 1,294 new private homes sold (excluding ECs) across January to March represented a 60% quarter-on-quarter fall from Q4 2025’s elevated volumes. This was not demand weakness — it reflected a deliberately compressed launch pipeline.

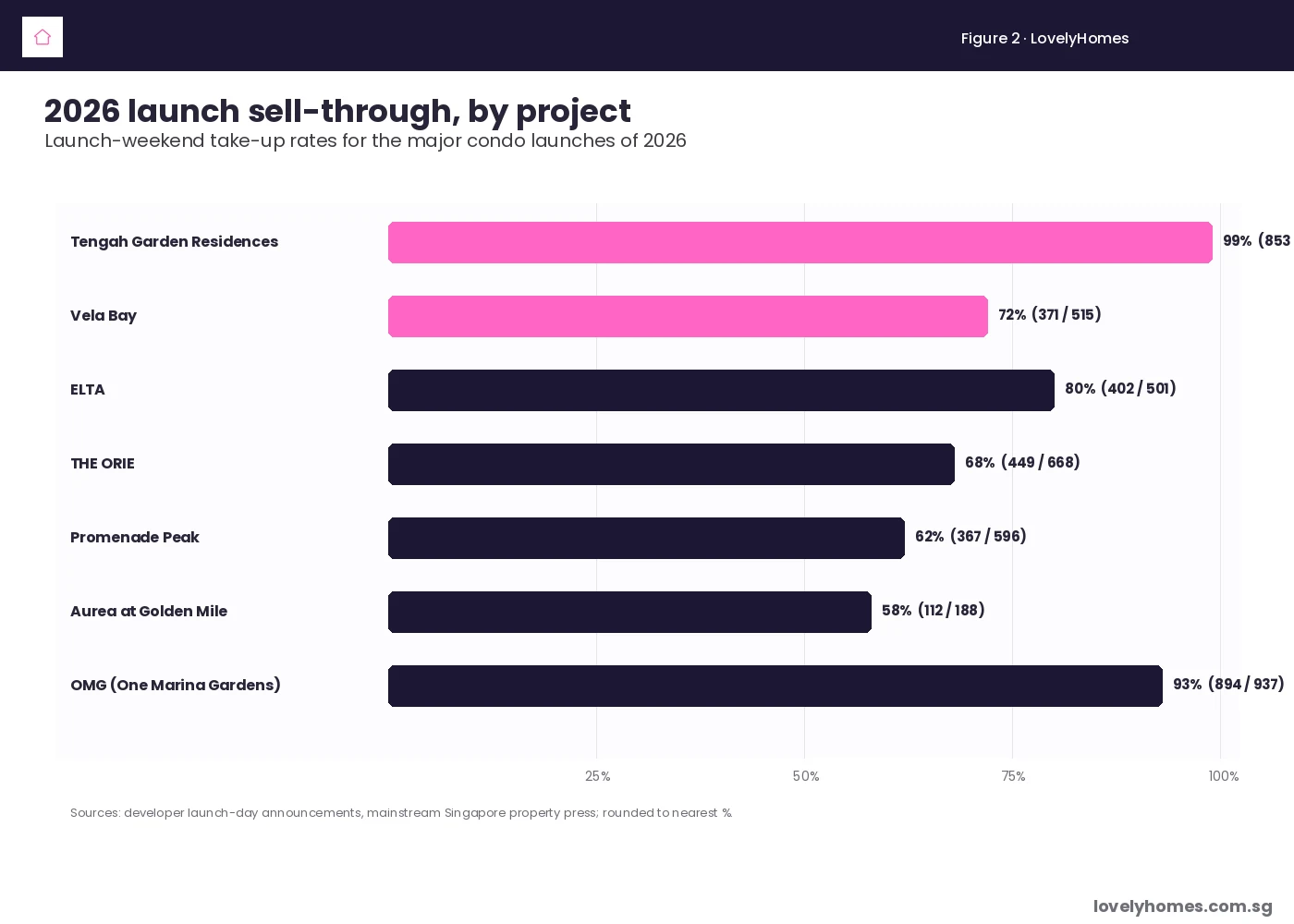

Developers held back launches in early 2026 after the strong 2H 2025 absorption. January saw just 246 units transacted and February approximately 512, both reflecting Lunar New Year seasonality and minimal new launches. March rebounded sharply when Pinery Residences (588 units, 92.3% sold) launched, driving March’s total to approximately 1,300 units — the busiest month of the quarter.

2. April’s Headline: The Double Launch Weekend

The defining event of April 2026 was a single late-month launch weekend where two major projects went on sale simultaneously — Tengah Garden Residences (TGR) in the Outside Central Region (OCR) and Vela Bay in Bayshore, Core Central Region (CCR). Together, these two projects accounted for approximately 1,378 units and achieved combined take-up of around 89% in 48 hours, representing roughly 1,224 units sold over one weekend.

The performance of these two launches illustrates a key dynamic in Singapore’s 2026 market: quality supply at the right pricing attracts immediate buyer conviction, even at very different price points. TGR’s OCR pricing (~S$1,700 psf) targets HDB upgraders and first-time private buyers; Vela Bay’s CCR pricing (~S$2,886 psf) targets investment-grade buyers, permanent residents, and high-net-worth individuals comfortable with Singapore’s ABSD framework.

3. Rivelle Tampines EC: The Last DPS Sale of 2026

Rivelle Tampines, the 572-unit executive condominium at Tampines Street 95 developed by Sim Lian Group, completed its sell-out in April 2026. The project had launched on 21 March 2026 with a spectacular 92.5% Day 1 take-up at a median price of S$1,937 psf — the best EC launch since Hundred Palms Residences in 2017. The remaining units were fully taken up during the second ballot on 24 April 2026.

What makes Rivelle Tampines historically significant is that 87.9% of its buyers opted for the Deferred Payment Scheme (DPS) — and all of those OTPs were issued before 8 May 2026, the date on which the Ministry of National Development announced the removal of DPS for new ECs as part of the EC cooling package.

Under DPS, EC buyers need only pay the down payment and service the loan when they collect their keys (typically 3–4 years later), rather than making progressive payments during construction. The scheme was popular among buyers with existing home loans who did not want to service two mortgages simultaneously. With DPS now gone for all new EC OTPs from 8 May 2026 onwards, Rivelle Tampines buyers were effectively the last cohort to benefit.

For more on the broader EC rule changes that took effect in May 2026, including the doubled Minimum Occupation Period (10 years) and the 90% first-timer allocation, see our Singapore EC Cooling Measures May 2026 guide.

4. What This Means for Q2 2026

April’s data, when viewed alongside March’s strength and the EC sell-out, points to an active Q2 2026 for Singapore’s new launch market. Several observations:

Pricing resilience: The fact that both a S$1,700 psf OCR project and a S$2,886 psf CCR project achieved near-90% launch take-up confirms that buyers across different budgets remain engaged when product quality is there. Singapore’s private home price index rose 0.9% in Q1 2026 (revised up from the initial flash estimate of 0.3%) and the pipeline suggests continued modest appreciation.

EC supply adjustment: With DPS removed and MOP doubled to 10 years, the EC buyer calculus has changed. First-timers still benefit from income-ceiling eligibility and lower entry prices than private condos, but the investment horizon is longer and the payment obligation is heavier without DPS. Near-term EC launches (watch for Canberra Drive and Senja Close tenders when awarded) will test this new demand profile.

SORA tailwind: The 1-month SORA rate’s continued decline to approximately 1.20% (from its 3.68% peak in 2023) means floating-rate home loan payments have fallen meaningfully. A buyer with a S$900,000 floating-rate loan at SORA + 0.80% now pays approximately S$3,960/month versus approximately S$5,300/month at peak SORA — a difference of over S$1,300/month. This affordability improvement is supporting buyer confidence across the market. See our home loan comparison guide for the full 2026 rate picture.

Q2 launch pipeline: Several significant projects remain to launch through June 2026. Lentor Gardens Residences (499 units, RCR) is expected to test OCR/RCR crossover pricing. For a broader view of what is coming in 2026’s new launch pipeline, see our New Launch Condo Pipeline article.

Summary Table: Q1–Q2 2026 Developer Sales at a Glance

| Period | New Private Homes Sold (excl. EC) | Key Driver | Context |

|---|---|---|---|

| Jan 2026 | ~246 | No major launches; LNY season | Quiet start to year |

| Feb 2026 | ~512 | Pent-up demand, small projects | Pre-EC announcement |

| Mar 2026 | ~1,300 | Pinery Residences (92.3% Day 1) | Strongest Q1 month |

| Apr 2026 | ~1,450* | TGR + Vela Bay double launch weekend; Rivelle EC cleared | Q2 rebound begins |

| Q1 2026 Total | 1,294 (as at 26 Mar caveat data) | Limited launch calendar | Down 60% q-o-q; set to revise up with full Mar caveats |

* April 2026 figure estimated. Official URA data released 15 May 2026; includes late-April TGR and Vela Bay launch sales.

FAQ: Singapore April 2026 Developer Sales

When does URA release monthly developer sales data?

URA releases monthly developer sales statistics on the 15th of the following month. April 2026 data was therefore published on 15 May 2026. The data includes the number of units launched, sold, and unsold for each development, with prices and units based on Options to Purchase (OTPs) issued by developers. The URA e-Service portal (eservice.ura.gov.sg) provides the full data table.

Why was Q1 2026 new home sales so low?

Q1 2026’s 1,294 new private homes sold (excluding ECs) represented a 60% fall from Q4 2025’s elevated levels, but this primarily reflected a thin launch calendar rather than a demand collapse. Developers launched fewer developments in Q1 2026, with only six projects (including two ECs) coming to market. When projects did launch — particularly Pinery Residences in March — they achieved very high take-up rates (92.3% for Pinery), confirming strong underlying buyer demand.

What is Tengah Garden Residences and who is it for?

Tengah Garden Residences (TGR) is an OCR condominium in Tengah, Singapore’s newest housing district in the western region. The project offers approximately 863 units at an indicative price of around S$1,700 psf — competitive for a new OCR launch with direct access to the Tengah Town Centre MRT (Jurong Regional Line) when completed. TGR targets HDB upgraders, first-time private property buyers, and investors seeking yield at OCR price points. It is NOT an EC, so Singapore PRs and foreigners are also eligible to purchase (subject to ABSD).

Can Rivelle Tampines EC buyers still use DPS?

Yes — buyers who received their OTP from Rivelle Tampines before 8 May 2026 are entitled to retain the Deferred Payment Scheme (DPS) arrangements they agreed to. The MND’s announcement removing DPS for ECs applies only to OTPs issued on or after 8 May 2026. Since all Rivelle Tampines units had OTPs issued before that date (the last units were sold on 24 April), those buyers are grandfathered under the old rules.

What EC projects are coming next after Rivelle Tampines?

Singapore’s EC pipeline for the remainder of 2026 and into 2027 includes sites that have been tendered or are awaiting tender under the 1H 2026 GLS programme. Key upcoming EC sites include Canberra Drive and Senja Close. These projects will launch under the new EC framework (10-year MOP, 90% first-timer allocation, no DPS), so their sales performance will be the first real-world test of buyer appetite for the revised rules.

Related Articles

- Singapore EC Cooling Measures May 2026: 10-Year MOP, 90% First-Timer Quota and End of DPS

- Minimum Occupation Period Singapore 2026: HDB, EC and Private Property Rules

- Singapore New Launch Condo Pipeline May 2026: 17 Projects, OCR-Heavy

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Home Loan Comparison Singapore 2026: HDB Loan, Fixed vs Floating and SORA

Disclaimer

This article is based on URA monthly developer sales data released on 15 May 2026, supplementary reporting from industry sources, and developer announcements. Sales figures for April 2026 include estimates and approximations where official caveat data may not yet be fully lodged. Always verify the most current figures at the URA Property Market Information portal. This is not investment advice. Consult a licensed financial adviser or property consultant before making any property purchase decision.