Quick Answer: URA 2H2026 GLS Programme — Key Headlines

- Announced: 3 June 2026 by the Urban Redevelopment Authority (URA) and Ministry of National Development.

- Total supply (2H2026): 9,200 private residential units, 188,100 sqm GFA of commercial space, and 970 hotel rooms across all Confirmed and Reserve List sites.

- Confirmed List: 9 sites — 8 private residential (including 1 EC site) and 1 white site — yielding approximately 4,745 residential units and 83,350 sqm GFA of commercial space.

- Jurong Lake District white site: To be launched for tender in July 2026; up to 1,200 private residential units, minimum 40,000 sqm office space, and 44,000 sqm complementary uses.

- Pipeline total: With the 2H2026 injection, the overall private residential (including EC) supply pipeline rises to approximately 61,000 units from approximately 57,000 units.

- Market signal: The Government signals continued commitment to sustaining adequate private housing supply and accelerating the development of Jurong Lake District as Singapore’s second CBD.

URA Releases 2H2026 GLS Programme: What It Means for Singapore Property

The Urban Redevelopment Authority (URA) announced Singapore’s Government Land Sales (GLS) programme for the second half of 2026 on 3 June 2026, releasing nine sites on the Confirmed List and thirteen sites on the Reserve List. The announcement is a significant policy signal, sustaining a high level of private housing supply while accelerating one of Singapore’s most ambitious urban development projects — the Jurong Lake District (JLD) transformation.

GLS programmes are released twice yearly (for 1H and 2H) and represent the Government’s primary tool for regulating private housing land supply. Sites on the Confirmed List are released for tender regardless of market conditions; those on the Reserve List are launched only when a developer submits an acceptable bid, providing a buffer of supply that can be activated when demand warrants.

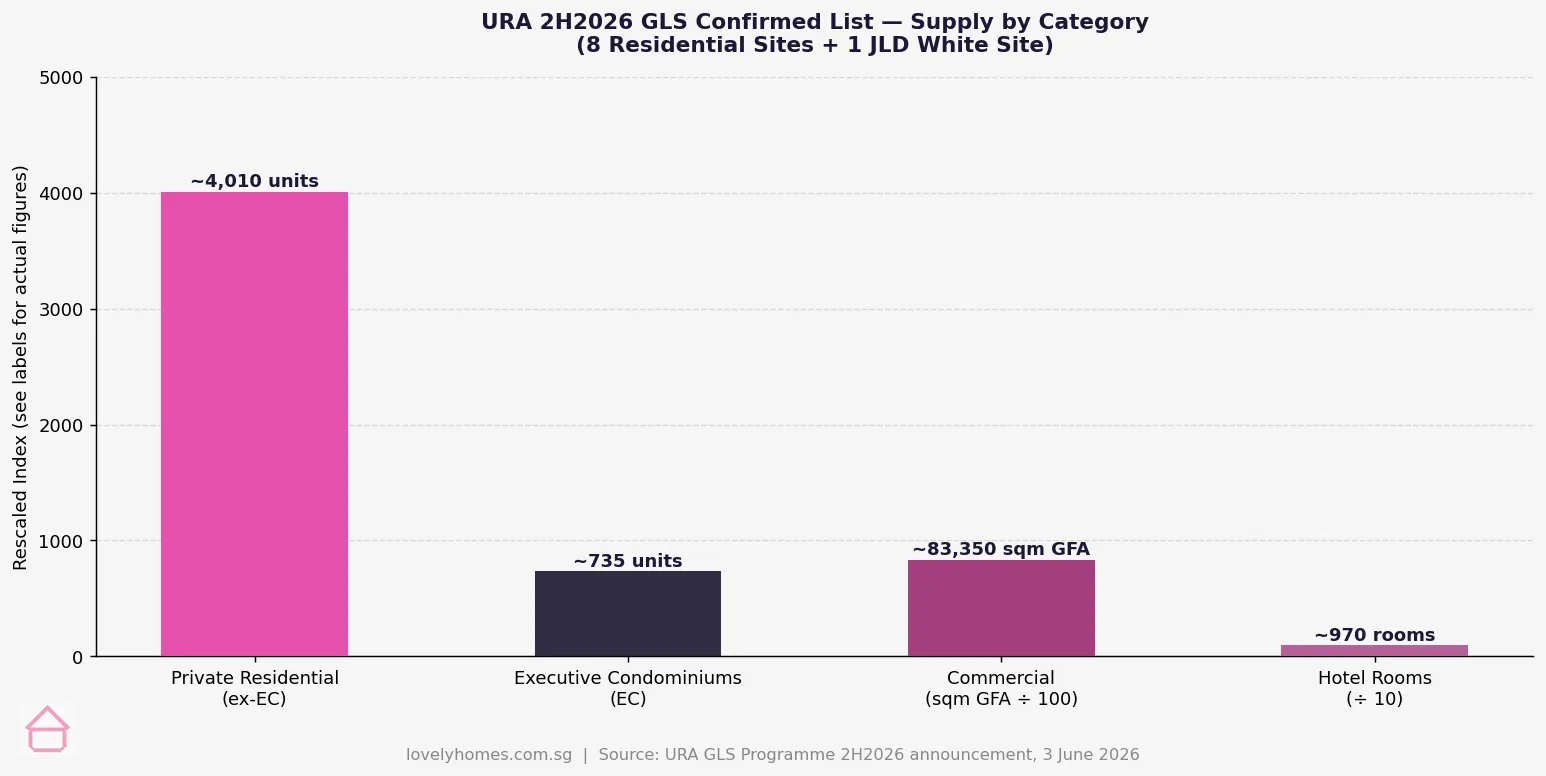

2H2026 Confirmed List: Nine Sites, 4,745 Units

The nine Confirmed List sites announced for 2H2026 can collectively yield approximately 4,745 private residential units (including 735 executive condominium units) and 83,350 sqm GFA of commercial space. The eight private residential sites include a mix of Outside Central Region (OCR), Rest of Central Region (RCR), and Core Central Region (CCR) locations, sustaining the supply diversity that has characterised recent GLS programmes. A single executive condominium (EC) site is included — responding to persistent demand for the EC tenure from HDB upgraders priced out of the full private market.

Taken together with the thirteen Reserve List sites — which can yield an additional approximately 4,455 residential units, 104,750 sqm of commercial GFA, and 970 hotel rooms if triggered by developer demand — the 2H2026 programme adds meaningful supply headroom to Singapore’s already robust private housing pipeline.

The Jurong Lake District White Site: Singapore’s Second CBD Moves Forward

The centrepiece of the 2H2026 programme is the Jurong Lake District (JLD) white site, scheduled for tender launch in July 2026. The JLD white site is a large, mixed-use parcel with a total development potential of approximately 186,000 sqm GFA, comprising:

- A minimum of 40,000 sqm of office space (Grade A commercial)

- Up to 1,200 private residential units

- Approximately 44,000 sqm GFA of complementary uses (retail, hospitality, or civic)

The Government has invested heavily in JLD infrastructure ahead of this white site release — the revitalised 90-hectare Jurong Lake Gardens, the new Science Centre at Jurong Lake, the Jurong Gateway Hub, and two new MRT lines: the Jurong Region Line (JRL), opening in stages from approximately mid-2028, and the Cross Island Line (CRL) Phase 2, expected approximately 2032. These infrastructure investments significantly enhance the district’s attractiveness to both commercial occupiers and residential buyers, and represent the Government’s long-term commitment to decentralising Singapore’s economic activity away from the Raffles Place/Marina Bay corridor.

For property investors, the JLD white site is a landmark tender — likely to attract significant interest from Singapore’s major listed developers and potentially joint ventures with international capital partners. The development, once built, is expected to set a new benchmark for integrated mixed-use development outside the CCR and will meaningfully reshape the Jurong Lake corridor pricing landscape.

What This Means for Property Buyers and Investors

| Stakeholder | Key Implication | Timing |

|---|---|---|

| Private property buyers | Confirmed List sites will produce new launches over 2027–2028. Buyers should monitor tender awards and expected launch timelines for preferred locations. | Tender launches from July 2026 |

| HDB upgraders (EC buyers) | One EC site on the Confirmed List suggests a new EC project for 2027 application. Income ceiling remains S$16,000/month. | EC launch approximately 2027 |

| Jurong/JLD investors | JLD white site signals the next phase of JLD development. Properties in Jurong (D22) may see re-rating as the master plan becomes reality. | JLD white site tender July 2026 |

| Commercial space occupiers | 83,350 sqm of new commercial GFA in confirmed sites (plus JLD 40,000 sqm office minimum). Grade A office supply will expand from approximately 2028. | Construction 2026–2028 |

| Developers | High confirmed supply indicates Government policy intent to keep private housing prices in check. Competitive land pricing likely to remain disciplined. | Ongoing |

Context: Overall Supply Pipeline Reaches 61,000 Units

With the 2H2026 programme confirmed, the total supply of private residential units (including ECs) in Singapore’s overall development pipeline rises to approximately 61,000 units — up from approximately 57,000 units before the announcement. This pipeline encompasses units under construction, those with planning approvals, and those with awarded GLS or en bloc land but not yet commenced. The Government considers a pipeline of approximately 60,000–65,000 units to be consistent with market balance given Singapore’s typical absorption rate of 8,000–12,000 units per year in private completions and sales.

The sustained high supply — following similarly large GLS programmes in 1H2026, 2H2025, and 1H2025 — reflects the Government’s ongoing commitment to ensuring that private housing price growth remains moderate and accessible. Property analysts note that the 2H2026 programme, while substantial, is not materially larger than recent halves — suggesting a deliberate policy of continuity rather than a supply shock or withdrawal.

Frequently Asked Questions

What is a GLS Confirmed List site and how is it different from a Reserve List site?

A Confirmed List site is released for public tender by the Government at a predetermined date, regardless of prevailing market conditions. This ensures a baseline level of private housing land supply even during market downturns. A Reserve List site, by contrast, is only placed on the market if a developer submits an application to tender the site at a price that meets the Government’s minimum threshold — effectively providing an on-demand supply buffer that is activated by real developer appetite. Reserve List sites give the Government flexibility to release additional supply quickly when demand is strong without committing to an inflexible fixed programme.

When will the Jurong Lake District white site tender close and who will likely bid?

The JLD white site is scheduled to be launched for tender in July 2026. Tender close dates for major white sites are typically set 10–14 weeks after launch, suggesting a likely close in September or October 2026. Given the scale and complexity of the site — mixed-use with mandatory minimum office space — bidders are likely to be Singapore’s largest listed developers (CapitaLand Development, City Developments, UOL Group, GuocoLand) potentially in joint venture with institutional capital partners. International consortia have bid on previous JLD sites. The winning bid will set a new benchmark land rate for the JLD corridor and signal developer confidence in Singapore’s Grade A office and premium residential demand.

How does the 2H2026 GLS programme affect private property prices?

The release of a large GLS Confirmed List — 4,745 units in addition to the existing pipeline — is generally a moderating influence on private property price growth, as it ensures developers have sufficient access to land without excessive competition for a scarce resource. However, the near-term effect on prices is limited: GLS land requires 2–4 years from tender award to new-launch sales, so 2H2026 sites will contribute to supply primarily in 2028–2030. More immediately, the JLD white site signals long-term confidence in Singapore’s property market fundamentals and the Jurong corridor specifically, which is likely to be read positively by investors already holding or considering D22 assets.

Related Articles

- Jurong West Neighbourhood Guide Singapore 2026: Property Prices, Schools and JRL MRT

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Complete Guide 2026: BSD, ABSD, SSD and ACD Explained

- Singapore Property Investment Guide 2026

- HDB BTO June 2026 Application Guide: 6,900 Flats Across AMK, Bishan, Bukit Merah, Sembawang and Woodlands

Disclaimer

This article is for general informational and editorial purposes only. GLS programme details, site specifications, tender timelines, and supply figures are based on URA announcements as at 3 June 2026 and are subject to revision. Property buyers and investors should conduct independent due diligence and consult licensed property advisers and financial professionals before making property decisions. For official GLS information, refer to the Urban Redevelopment Authority at ura.gov.sg.

0 Comments