Singapore levies an annual property tax on all property owners — whether you live in your home or rent it out as an investment. Administered by the Inland Revenue Authority of Singapore (IRAS), property tax is calculated on the Annual Value (AV) of the property, not its market price. If you are an owner-occupier of a modest HDB flat, your annual property tax bill may be just a few hundred dollars. If you hold a prime-district investment condo with a high AV, that bill can run into five figures. Understanding the system — and the difference between owner-occupier rates and non-owner-occupier rates — can make a meaningful difference to your annual holding costs.

- Property tax is based on Annual Value (AV) — the estimated annual rent if the property were let.

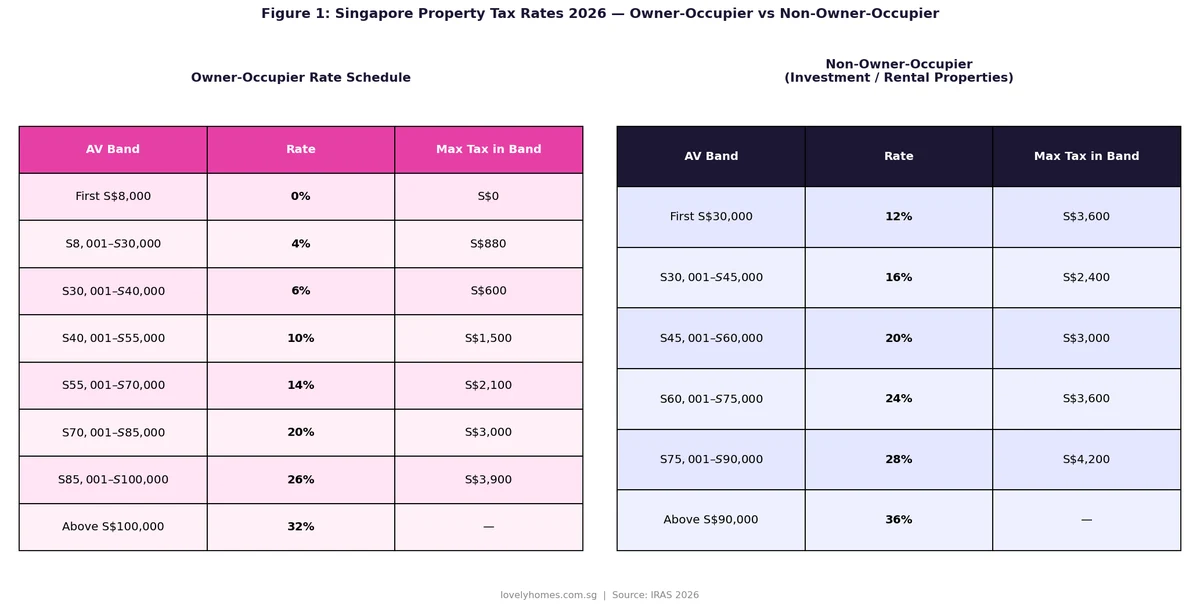

- Owner-occupier rates are progressive from 0% to 32%; the first S$8,000 AV is tax-free.

- Non-owner-occupier rates (investment/rental properties) are higher: 12% to 36%.

- IRAS reviews AV periodically; owners can file a Notice of Objection within 30 days of an AV revision.

- Property tax is payable by 31 January each year; GIRO instalments are available.

- Investment-property owners may deduct property tax as an allowable expense against rental income.

- Rates were last overhauled in Budget 2022, with further adjustments in Budget 2023 effective 2024.

What Is Property Tax and Who Administers It?

Property tax in Singapore is a wealth tax on property ownership, levied annually by IRAS under the Property Tax Act 1960. It is distinct from the Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD) — those are one-time transaction taxes paid at purchase. Property tax is a recurring annual cost borne by every property owner in Singapore, regardless of whether the property is occupied, vacant, or rented out.

The tax is assessed on the Annual Value (AV) of the property — IRAS’s estimate of the annual rent the property would fetch on the open market if let on a tenancy that excludes furniture, furnishings, and maintenance. For most HDB flats, IRAS derives the AV from comparable transaction rents in the same block and vicinity. For private residential properties, IRAS draws on URA rental data and its own valuation database.

Unlike income tax, property tax does not depend on whether you actually earn any rental income. A vacant investment condo is still taxed at non-owner-occupier rates. The practical implication is that vacancy periods hurt landlords twice: no rental income, and a continuing property-tax bill at the higher NOO rate.

Property Tax Rates in Singapore (2026)

Singapore uses two separate progressive rate schedules — one for owner-occupiers, one for all other uses. The schedules below reflect the rates introduced by Budget 2023, effective from 1 January 2024, and remain in force for the 2025 and 2026 assessment years.

The key structural difference: the owner-occupier schedule starts at 0% on the first S$8,000 of AV, rising to 32% above S$100,000. The non-owner-occupier schedule starts at 12% on every dollar of AV — there is no zero-rate band. An investment property with an AV of S$30,000 pays S$3,600 in property tax annually; an owner-occupier home with the same AV pays only S$1,040.

The rates were raised in two stages as part of the Government’s effort to make the property tax system more progressive and to moderate speculative demand. The Budget 2022 changes (effective 2023) increased rates at the upper AV bands; the Budget 2023 changes (effective 2024) extended the progressivity further, reducing the width of the lower bands at the NOO schedule so that mid-value investment properties bear a meaningfully higher tax.

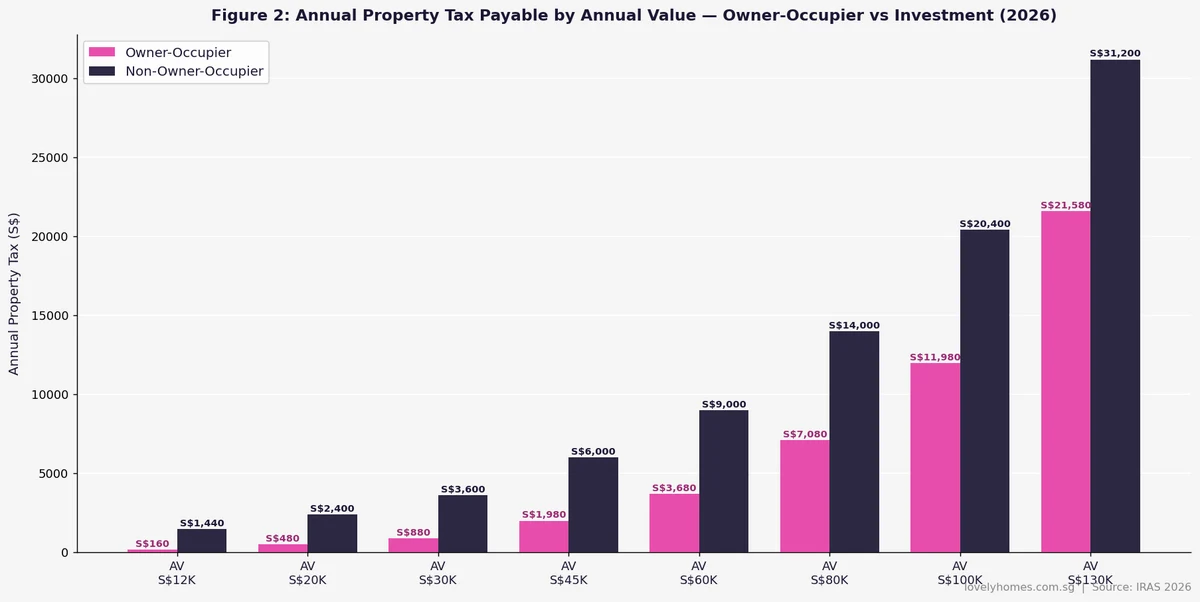

Annual Tax Payable at Different Annual Values

The chart below shows exactly how much property tax you pay at various AV levels under both schedules. The gap between the owner-occupier and non-owner-occupier bills widens sharply above S$30,000 AV — the point where NOO rates jump from 12% to 16% and beyond, while OO rates are still rising gently.

What Is Annual Value and How Does IRAS Set It?

The Annual Value (AV) is IRAS’s estimate of the gross annual rent that a property would fetch if let unfurnished. It is important to understand that AV is not based on what you actually receive in rent — it is a notional figure set by IRAS using comparable market rents in the same area and property type. Key points:

- HDB flats: AV is derived from the HDB’s published rental data for comparable flat types and locations.

- Private condos and landed properties: IRAS uses URA rental transaction data and its own database of rental agreements.

- Commercial shophouses: AV is based on commercial rental comparables; commercial property tax uses a flat 10% rate (not the residential schedules above).

- AV reviews: IRAS revises AV annually at the start of each calendar year. Rapid changes in market rents — as seen in 2022–2023 when Singapore rents spiked — can translate into significant AV increases and higher property tax bills.

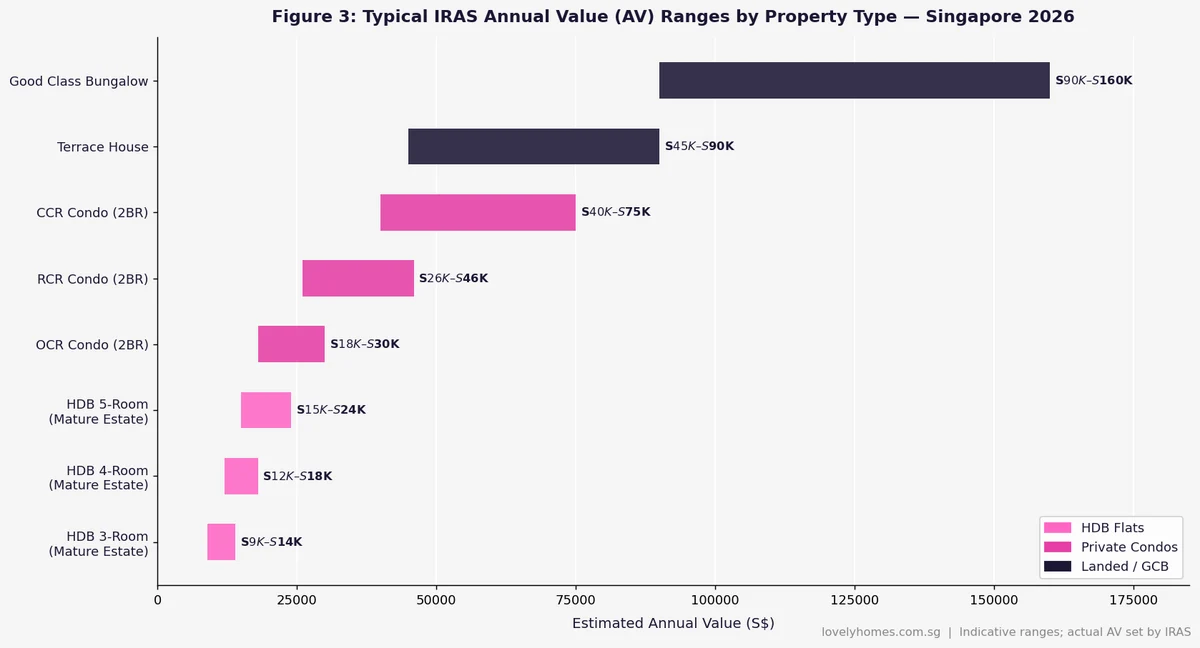

Typical Annual Values by Property Type

As the chart shows, HDB AVs typically sit between S$9,000 and S$24,000 — well within the lower-rate bands of both schedules. Private condo AVs in the OCR start around S$18,000–S$30,000; CCR condos can reach S$40,000–S$75,000, where NOO rates become materially higher. Good Class Bungalows with AVs above S$90,000 incur property tax at the 36% NOO rate on a large portion of their AV.

Worked Example — Property Tax Calculation

Example A: Mr Lim — HDB Owner-Occupier

Mr Lim owns and lives in a 4-room HDB flat in Bishan. IRAS sets the AV at S$16,000 for YA 2026.

| AV Band | Rate | Tax |

|---|---|---|

| First S$8,000 | 0% | S$0 |

| Next S$8,000 (to S$16,000) | 4% | S$320 |

| Total Annual Property Tax | S$320 |

At S$320 per year, Mr Lim’s property tax is a minimal cost — less than a single month’s utilities. The owner-occupier zero-rate band and the low initial rate mean most HDB owner-occupiers pay very little in property tax.

Example B: Mrs Chen — Investment Condo (Non-Owner-Occupier)

Mrs Chen owns a 2-bedroom investment condo in Tanjong Pagar (RCR). IRAS sets the AV at S$42,000 for YA 2026. She rents it out at S$3,800/month.

| AV Band | Rate | Tax |

|---|---|---|

| First S$30,000 | 12% | S$3,600 |

| Next S$12,000 (to S$42,000) | 16% | S$1,920 |

| Total Annual Property Tax | S$5,520 |

At S$5,520 per year, property tax represents approximately 1.2% of Mrs Chen’s annual rental income (S$45,600/year), or S$460/month. The good news: this S$5,520 is deductible as an allowable expense when Mrs Chen files her income tax return — offsetting part of her rental income. For details, see our Rental Income Tax Singapore 2026 guide.

Owner-Occupier Status — How to Qualify

To benefit from the lower owner-occupier rates, at least one owner must use the property as their principal place of residence. The owner-occupier concession is not automatic — you must apply to IRAS. Key rules:

- Only one property per individual can receive the owner-occupier concession at any time.

- If you move out, you must notify IRAS — failure to do so and receiving an undeserved concession is an offence.

- If you are a Singapore Citizen or PR renting out one or more rooms in your HDB flat while still living there, you retain the owner-occupier concession for your HDB (since you are still in residence).

- If you own two private properties and move into the second, you must surrender the owner-occupier concession on the first and apply for it on the second.

How to Pay and When

IRAS issues property tax bills in January each year, for the full calendar year (January to December). Payment is due by 31 January. Options include:

- GIRO (General Interbank Recurring Order) — the most convenient; IRAS offers monthly GIRO instalments spreading the payment across 12 months.

- Internet banking, AXS, or SAM kiosks — pay in a single lump sum.

- PayNow or e-Pay — supported via the myTax Portal.

Late payment attracts a 5% penalty on the outstanding amount, with further penalties if not paid within 60 days. There is no CPF offset available — property tax must be paid in cash.

Appealing Your Annual Value

If you believe IRAS has overestimated the AV of your property, you have the right to object. The process:

- File a Notice of Objection within 30 days of the AV revision notice (or the annual property tax notice) via myTax Portal.

- State the grounds: typically, you provide comparable rental evidence showing that similar properties in your area fetch lower rents.

- IRAS reviews and may adjust the AV, reject the objection, or propose a revised AV for agreement.

- If unresolved, the matter proceeds to the Valuation Review Board (VRB).

Successful appeals — particularly in periods when market rents have fallen sharply after a spike — can meaningfully reduce your annual property tax bill. During the post-2023 rental normalisation period, some landlords saw AV reductions of 10–20% after objecting.

Property Tax as an Investment Metric

For investors, property tax is a recurring carrying cost that directly affects net yield. At a gross rental yield of 3.5% on a S$1.5M condo, the annual gross rental income is S$52,500. If the AV is set at S$46,000 and the NOO rate applies:

- Property tax = S$30,000 × 12% + S$15,000 × 16% + S$1,000 × 20% = S$3,600 + S$2,400 + S$200 = S$6,200

- Property tax as % of gross income: 11.8%

- After property tax, other costs (mortgage, management, maintenance), net yield compresses to around 2.0–2.5%.

This calculation underscores why investors in higher-AV properties — particularly CCR condos and landed homes — need to model property tax carefully as part of total ownership cost. The NOO schedule’s progressivity means the tax burden climbs quickly above S$60,000 AV. For a comprehensive holding-cost analysis, see our Singapore Rental Yield Guide 2026.

Summary Table — Property Tax Key Facts

| Parameter | Owner-Occupier | Non-Owner-Occupier |

|---|---|---|

| Tax Base | Annual Value (AV) — IRAS’s estimated annual rent | |

| Rate Range | 0% – 32% | 12% – 36% |

| Zero-Rate Band | First S$8,000 AV | None — 12% from first dollar |

| Application | Must apply to IRAS; one property per owner | Applies automatically to all other properties |

| Payment Due | 31 January each year (GIRO available) | |

| Deductibility | Not deductible (no rental income) | Deductible against rental income (IRAS) |

| AV Review Period | Annual (1 January); objection window 30 days | |

| Rates Last Revised | Budget 2022 (effective YA 2023); Budget 2023 (effective YA 2024) | |

Frequently Asked Questions

Is property tax the same as income tax on rental income?

No — they are entirely separate taxes. Property tax is levied by IRAS on the Annual Value of the property and is payable regardless of whether you earn any rental income. Rental income tax is part of personal income tax, assessed on your net rental income after deductible expenses. An investor pays both property tax (annually, to IRAS) and rental income tax (via the annual tax return). Crucially, the property tax you paid in the year is deductible as an expense against your rental income, reducing your rental income tax bill.

I live in my condo — do I pay owner-occupier rates on my HDB flat too?

No. The owner-occupier concession applies to only one property at a time — the one you use as your principal residence. If you live in your condo, your HDB flat is taxed at non-owner-occupier rates (12–36%), even if it is empty. If you move back into the HDB flat and surrender the condo’s OO status, the concession switches. This is a common overlooked cost for property investors who hold both HDB and private residential property simultaneously — note that SCs who retain an HDB flat while owning a private property do so subject to HDB rules on subletting and must pay the full NOO property tax on whichever property they do not live in.

Can I use CPF to pay property tax?

No. Unlike mortgage instalments and BSD, property tax cannot be paid from CPF. It is a cash obligation payable directly to IRAS by 31 January each year. However, you can spread the payment using GIRO into 12 monthly instalments, which many property owners find more manageable. Setting up GIRO through the myTax Portal typically takes about two weeks to process.

What happens if the market rent for my area falls but IRAS doesn’t revise my AV?

You can file a Notice of Objection via myTax Portal within 30 days of the annual property tax notice. You will need to provide evidence that comparable properties in your area fetch lower rents than IRAS’s estimate — for example, URA rental transaction records (available on the URA website), your own tenancy agreement, or comparable listings. IRAS reviews the evidence and may revise the AV. If accepted, the revised AV applies for the current and sometimes preceding year, with a refund of overpaid tax. If rejected, you may escalate to the Valuation Review Board (VRB) — a quasi-judicial body that hears property valuation disputes.

Does a newly bought property attract property tax immediately?

Yes — property tax runs from the date you become the legal owner (the date of completion/transfer of title). IRAS will issue a property tax notice shortly after the transfer is registered. For new launch condominiums, property tax kicks in from the date of Temporary Occupation Permit (TOP) or, in some cases, from completion date. Before TOP, the developer typically pays the property tax on the land/building under construction. After TOP, individual purchasers begin receiving property tax notices for their units. Make sure to factor property tax into your cash-flow planning from TOP onwards, particularly if you are holding the unit vacant while planning a renovation before rental.

Is commercial shophouse property taxed the same way?

No. Commercial property in Singapore — including the ground-floor commercial units of conservation shophouses — is taxed under a flat 10% property tax rate, not the progressive residential schedules. The AV for commercial property is similarly based on comparable commercial rents. Mixed-use shophouses (residential upper floors, commercial ground floor) may have their AV apportioned, with the commercial portion taxed at 10% and the residential portion at the applicable residential NOO rate. This is one reason investors find shophouses attractive — the commercial-floor tax burden is relatively modest compared with residential NOO rates.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty Singapore 2026: Rates, Calculation and Worked Examples

- Rental Income Tax Singapore 2026: Complete IRAS Guide for Landlords

- Rental Yield Singapore 2026: District-by-District Guide for Property Investors

- Seller’s Stamp Duty Singapore 2026: Rates, Holding Periods and Exemptions

- Singapore Property Buying Checklist 2026: 12 Steps from IPA to Key Collection

- Singapore Landed Property Buying Guide 2026: Terrace, Semi-D, Bungalow and GCB

Disclaimer: This article is for general information only and does not constitute tax, legal, or financial advice. Property tax rates, Annual Value assessments, and IRAS procedures are subject to change. Always verify the current position with the IRAS Property Tax page and consult a qualified tax professional or licensed property consultant before making decisions based on property tax calculations. IRAS’s AV assessment is the authoritative figure for any given property and may differ from indicative ranges shown in this guide.

Click anywhere outside to close

0 Comments