Quick answer — S-REITs in 30 seconds

- A Singapore Real Estate Investment Trust (S-REIT) is an SGX-listed vehicle that owns income-producing real estate and is required by law to distribute at least 90% of its taxable income to unit holders.

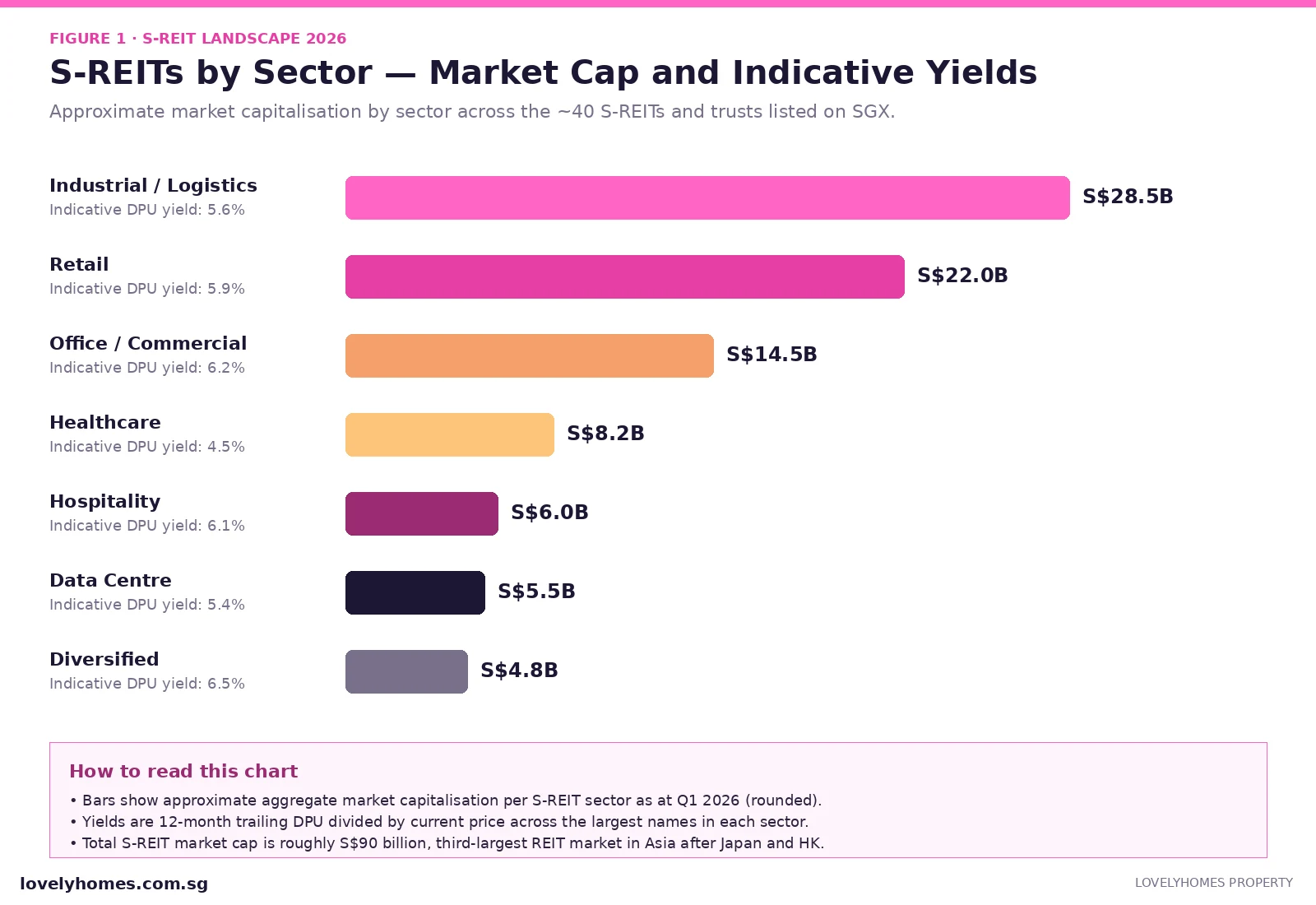

- Around 40 S-REITs and stapled trusts are listed on the Singapore Exchange, with combined market cap roughly S$90 billion — the third-largest REIT market in Asia.

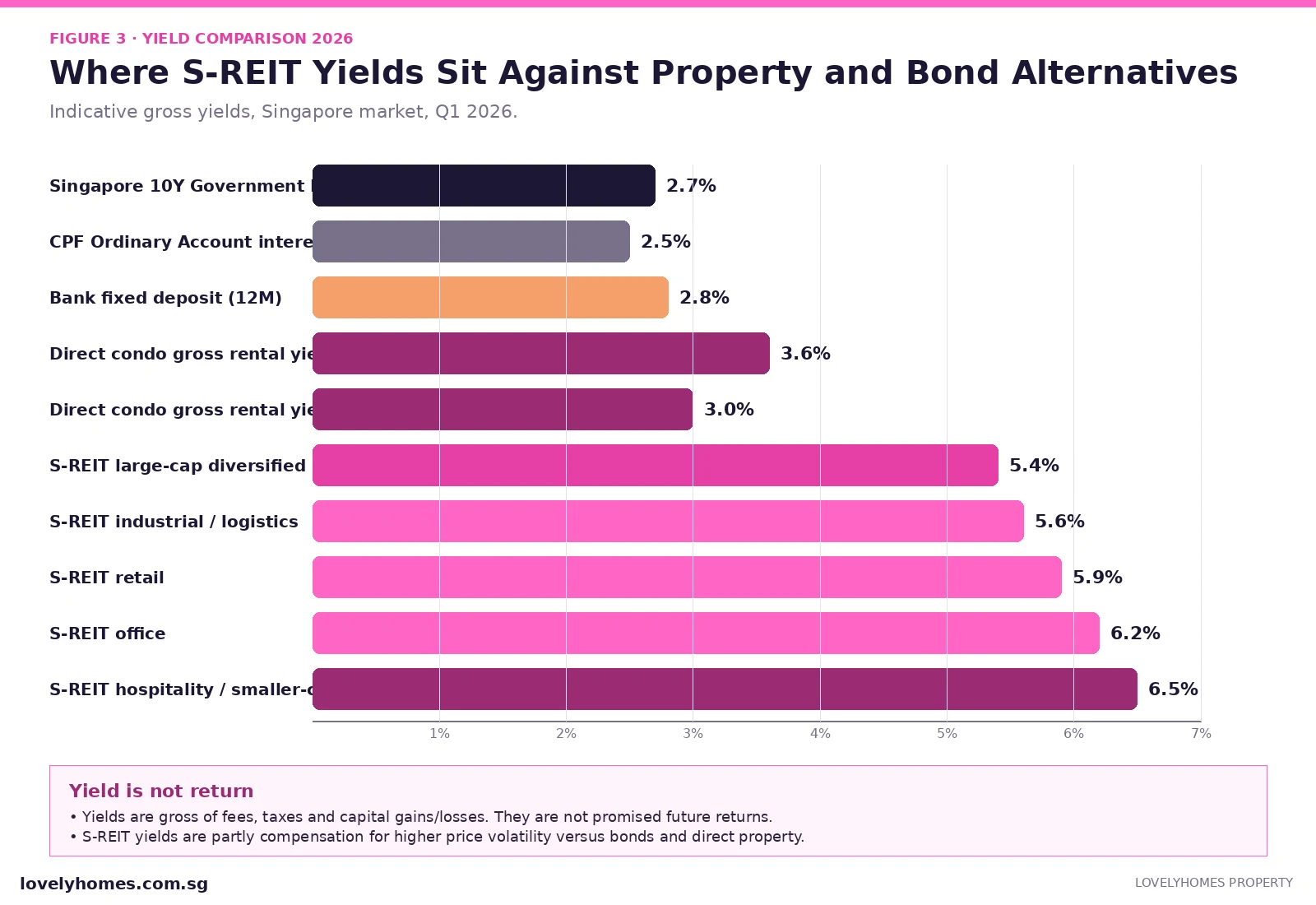

- Indicative distribution per unit (DPU) yields sit at 5–6.5% across most S-REITs in 2026, against ~3.0–3.8% gross rental yields on direct condos.

- S-REIT distributions to retail Singapore investors are tax-exempt at the investor level, and there is no BSD or ABSD on REIT unit purchases.

- Minimum entry can be as low as one board lot (typically S$1,000–2,500), versus ~S$200,000 cash + CPF for a S$1M condo.

- S-REITs trade like shares — settlement T+2, daily liquidity — so the lock-in risk of direct property does not apply.

- You don’t choose the tenants, the manager does. You also don’t get the leverage of a 75% mortgage on a personal balance sheet.

- Risks include sector concentration, refinancing risk on REIT debt, and price volatility driven by SGS yields and the SORA curve.

What is an S-REIT, exactly?

An S-REIT is a pooled investment vehicle, structured as a unit trust, that owns and manages a portfolio of income-producing real estate — shopping malls, office towers, logistics warehouses, hotels, hospitals, data centres, or a mix of these. The trust is listed on the Singapore Exchange (SGX) and trades just like a share. When you buy a unit of an S-REIT, you buy a slice of the underlying portfolio’s rental income and net asset value.

The key feature that distinguishes a REIT from a property holding company is the tax pass-through: as long as the trust distributes at least 90% of its taxable income to unit holders, that income is exempt from corporate tax at the trust level. The Inland Revenue Authority of Singapore (IRAS) further exempts these distributions from personal income tax for individual Singapore investors. The result is yield that flows from rents into your bank account with no tax leakage along the way — provided you remain an individual retail investor (different rules apply for institutions and non-residents).

S-REITs were introduced in Singapore in 2002, when the Monetary Authority of Singapore (MAS) and SGX rolled out the regulatory framework. The first listing — CapitaLand Mall Trust, now CapitaLand Integrated Commercial Trust — set a template that has been replicated 40-plus times since. Today the universe spans purely domestic plays (Frasers Centrepoint Trust, Suntec REIT) all the way to globally diversified industrial and data-centre REITs (Mapletree Industrial Trust, Keppel DC REIT) sponsored by listed Singapore developers.

How S-REITs make money (and how you make money from them)

An S-REIT generates revenue almost entirely from rents and service charges on the buildings it owns. Operating costs — property management fees, marketing, repairs, utilities recovered from tenants, the REIT manager’s base + performance fees — are deducted to get to net property income. Interest on the REIT’s debt is then paid; what remains is distributable income. Unit holders are paid out quarterly or semi-annually, depending on the trust.

Total return for a unit holder therefore has two components. The first is the distribution yield (the DPU divided by your purchase price), which is the income piece. The second is capital appreciation or depreciation of the units themselves, which moves with the trust’s net asset value (NAV) per unit and broader interest-rate sentiment. Over long holding periods, total returns are anchored to the underlying real estate’s rental growth and the discipline of the REIT manager. Over shorter periods, S-REIT prices can swing meaningfully on every change in SORA and SGS yields, which is the price volatility you accept in exchange for the liquidity advantage.

S-REIT vs direct Singapore condo — a side-by-side

The cleanest way to think about S-REITs is as a competing route into Singapore property exposure. Most retail buyers default to a single-unit private condo because it is the path of least resistance — the developer markets it, you sign for it, you collect rent. The S-REIT route requires opening a brokerage account and buying units, but eliminates a long list of frictions.

Three differences stand out. First, stamp duty: a Singapore Citizen buying a S$1M condo as a second property pays roughly S$24,600 in BSD plus S$200,000 in ABSD — over a fifth of the purchase price walks out the door before they have collected a single dollar of rent. The S-REIT investor pays roughly 0.20% in SGX clearing/transfer charges and the broker’s commission. Second, liquidity: a condo takes months to list, market, exercise OTP, and complete; S-REIT units settle T+2 on SGX. Third, diversification: a single condo is one tenant’s whim away from zero rent for three months; a typical industrial S-REIT owns 100+ buildings across multiple geographies.

The case for direct property has not gone away. Direct property gives you control of the asset, lets you draw 75% bank leverage at your personal credit, lets you live in the asset rent-free, and historically has tracked Singapore’s housing-market price index quite closely. The case for the S-REIT is that, for the same dollar of equity, you typically get higher cash-on-cash income, daily liquidity, and zero stamp-duty drag.

The S-REIT yield story versus alternatives

Yield is the headline reason most investors look at S-REITs. In a world where the Singapore 10-year government bond pays around 2.7% and a CPF Ordinary Account compounds at 2.5%, an S-REIT yield in the 5.5–6.5% range looks attractive. The right way to read these numbers is as yield premium — the spread above the risk-free rate that compensates you for taking equity-like risk.

Three caveats are worth holding in mind. The 5–6.5% headline yield is gross of price volatility — S-REIT unit prices can fall 15–25% in a year of rising rates, which means the cash-on-cash yield on your purchase price can be very different from the yield-on-paper an investor sees if they buy mid-correction. Yields are also not promised future returns; managers can cut DPU when occupancy or rental reversion turns negative, as several office and hospitality REITs did during 2020–2021. Finally, the headline yield does not include broker commissions, withholding tax for non-residents, or the bid-ask spread on smaller-cap names.

How to buy S-REITs — practical mechanics

The mechanics in 2026 are simple but worth getting right. You need three things: a Central Depository (CDP) account with SGX (free to open, requires NRIC/FIN, takes a few business days), a brokerage account (DBS Vickers, OCBC Securities, UOB Kay Hian, Tiger, Moomoo, IBKR all offer SGX access), and a Singapore-dollar settlement account at your bank. Once those are in place, you log into the broker, search for the REIT’s stock code, and place a buy order — limit orders are recommended over market orders for less-liquid names.

Most S-REITs trade in board lots of 100 units. With unit prices typically in the S$0.80–S$3.50 range, that puts the practical entry at around S$80–S$350 per board lot. There is no minimum to start; you can buy a single board lot of one REIT and add to it monthly. Many investors use a dollar-cost averaging approach — fixed monthly contributions into a small basket of REITs — which smooths the price-volatility risk over time.

The four real risks to underwrite

Before deploying capital, walk through four specific risks each REIT faces, and check the latest annual report or quarterly disclosure to see how the manager is positioned.

1. Interest-rate / refinancing risk

S-REITs are leveraged vehicles. The MAS caps aggregate leverage at 50% of total assets (raised from 45% in 2020 and made permanent in 2022). That debt has to be rolled. When SORA spikes, refinancing the next tranche of expiring debt costs more, and DPU compresses. The cleanest way to read this is to check weighted average debt cost, weighted average debt maturity, and the fixed-rate coverage in the latest results presentation — well-managed REITs disclose all three.

2. Sector / geography concentration

A retail REIT owning only Singapore suburban malls is fine in normal times and very exposed during a tourism collapse. A logistics REIT with US warehouses is fine in normal times and exposed to USD/SGD currency moves. Diversifying across at least three S-REIT sub-sectors (typically industrial + retail + office or data centre) is a practical hedge against single-sector shocks.

3. Manager incentive risk

The REIT manager is paid a base fee on assets under management plus a performance fee linked to DPU growth. This is well-aligned in good times and can become misaligned if managers push for acquisitions just to grow AUM. Look for managers with internal ownership, transparent unit-issuance discipline, and a track record of value-accretive acquisitions rather than dilutive ones.

4. Property-specific risk

A REIT’s biggest tenant going bankrupt, a major asset failing the BCA’s Green Mark recertification, or a leasehold running down without a top-up — all of these are real, individual-property risks that can hit DPU faster than macro factors. Mitigate by owning diversified REITs (no single tenant > 5–10% of rents) and check that lease expiry profiles are well staggered.

S-REIT taxation for Singapore investors

Tax treatment is a quiet but meaningful part of the S-REIT case. For an individual Singapore tax resident:

- Distributions are tax-exempt at the unit-holder level — no personal income tax to declare.

- Capital gains on unit sales are not taxed — Singapore has no capital gains tax, and S-REIT units are treated like other listed securities.

- No GST on unit purchases or sales.

- No property tax — that is paid by the REIT at the asset level and already reflected in the distributable income figure.

- No ABSD or BSD, since unit ownership is not direct real-estate ownership.

For a Singapore corporate investor, distributions are subject to corporate tax. For a non-resident individual, distributions attract a 10% withholding tax under MAS’s 2026 framework, which is a meaningful drag versus the resident treatment. Tax rules can change; always verify with IRAS or a qualified tax adviser before sizing a position.

Worked example — building a S$200,000 S-REIT portfolio

Take a Singapore Citizen with S$200,000 of investible savings (separate from emergency fund, separate from CPF Ordinary Account property allocation). They want Singapore property exposure but cannot stomach the ABSD on a second condo.

| Allocation | Sector | S$ amount | Indicative yield | Annual DPU |

|---|---|---|---|---|

| Industrial / logistics REIT (large-cap) | Logistics warehousing | S$60,000 | 5.6% | S$3,360 |

| Retail REIT (Singapore-focused) | Suburban malls | S$50,000 | 5.9% | S$2,950 |

| Office REIT (Grade A CBD) | Singapore offices | S$40,000 | 6.2% | S$2,480 |

| Data centre REIT (global) | Data centres | S$30,000 | 5.4% | S$1,620 |

| Healthcare REIT (defensive) | Hospitals | S$20,000 | 4.5% | S$900 |

| Total portfolio | 5 sectors | S$200,000 | 5.65% | S$11,310 |

That portfolio yields roughly S$11,310 a year in tax-free DPU, paid quarterly or semi-annually depending on the manager. Compare with the same S$200,000 deployed as the down-payment on an S$800,000 OCR condo with a 75% mortgage: ~S$24,000 in BSD plus, if it is a second property, S$160,000 in ABSD — meaning you would only have S$16,000 left of the S$200,000 to cover legal fees, valuation, and the cash portion of the down-payment. The condo path requires another S$140,000+ in cash to actually transact.

What this means for you

For most Singapore retail investors, S-REITs are not a substitute for a primary residence — that home should still be your first property and your primary anchor in Singapore real estate. But for the second dollar of property exposure, S-REITs are usually the more efficient route. The stamp-duty drag on a second condo is so heavy that it takes years of rental income to recoup; an S-REIT portfolio compounds from day one. The trade-off is that S-REIT prices move daily — you have to be psychologically comfortable watching unit prices drop 10–15% in a tightening cycle without panic selling.

A reasonable rule of thumb: keep your primary residence as the base, then consider S-REITs (rather than a second condo) for the next S$100,000–S$500,000 of property allocation. Above that level, the case for direct property — leverage, control, the ability to live in or rent out a unit — starts to compete more strongly with the S-REIT route. Decoupling and ABSD-avoidance strategies have their place, but most households arrive at the S-REIT route via simple arithmetic.

What might come next

Three structural shifts are worth tracking through 2026 and beyond. The MAS leverage cap (50%) and minimum interest coverage ratio (1.5x) are set to be reviewed periodically; any tightening would compress acquisition pipelines, while any easing would increase DPU growth optionality. The data-centre sub-sector continues to attract sponsor interest as AI compute demand reshapes industrial real estate; expect more S-REITs to lean toward this segment. And the Singapore office market is in the middle of a quiet repricing as hybrid work patterns stabilise — Grade A CBD assets remain bid, but secondary office is under structural pressure that should show up in DPU revisions.

Two regulatory tweaks under discussion at MAS — both flagged in industry consultation papers but not yet enacted as of April 2026 — could reshape the asset class. One is a possible adjustment to the 90% distribution requirement to give managers more flexibility on retention for AEI (asset enhancement initiative) capex. The other is a potential review of REIT manager fee structures to better align with unit-holder outcomes. Both would be modestly positive for long-term unit holders if implemented thoughtfully.

Frequently asked questions

Are S-REIT distributions really tax-free for Singapore investors?

For Singapore tax-resident individual investors holding S-REIT units in a personal capacity, distributions are exempt from personal income tax under IRAS rules. This does not apply to Singapore companies, partnerships, or non-residents (who face withholding tax). Always confirm the current IRAS guidance for your specific tax-residency status.

How do S-REITs differ from REIT ETFs?

An S-REIT is an individual trust that owns specific buildings. A REIT ETF (e.g. listed Lion-Phillip S-REIT ETF, NikkoAM-StraitsTrading Asia ex-Japan REIT ETF) holds a basket of REITs and rebalances on a defined index. ETFs trade lower yields after fees but offer one-ticker diversification. New investors often start with a REIT ETF and migrate to direct REIT picks once they’re comfortable reading the financials.

Can I use my CPF Ordinary Account to buy S-REITs?

S-REITs listed on SGX are eligible under the CPF Investment Scheme (CPFIS-OA), subject to the 35% stocks limit. Distributions paid into your CPFIS account are credited back to OA and continue to earn the OA floor rate. Note that capital losses from CPFIS are not tax-deductible the way personal cash investments would be in some other markets — Singapore has no capital gains tax in either case.

What yield should I aim for when buying S-REITs?

Yield is a function of price; a higher yield often signals higher perceived risk. A reasonable target band in 2026 is 5.5–6.5% for diversified large-cap S-REITs. Yields above 8% are usually a warning sign — the market is pricing in a DPU cut. Yields below 4.5% are typically defensive, low-volatility names where investors are paying up for stability.

What happens to my S-REIT units if the REIT manager is removed?

Unit holders have the right under the trust deed to vote out a manager (typically with a supermajority). The asset portfolio is owned by the trust itself, not the manager — so a change of manager is messy but does not zero out the unit value. This protection is one reason MAS regulates REIT managers heavily; the framework is designed to keep unit-holder interests primary.

Should I buy individual S-REITs or a REIT ETF first?

If you have time to read 2–3 annual reports per quarter, individual S-REITs let you tailor sector exposure and earn a slightly higher yield after fees. If you want a low-maintenance core position, a REIT ETF is a sensible starting point — you get instant diversification across 20–30 names with one trade.

How do S-REITs perform in a recession?

It depends heavily on sector. Industrial and healthcare REITs tend to be defensive (long leases, essential tenants). Hospitality and retail REITs tend to be cyclical (tourism, discretionary spend). In the 2020 COVID drawdown, the FTSE Straits Times REIT Index fell roughly 30% peak-to-trough before recovering most losses by mid-2021. Holding period and sector mix matter more than market timing.

Disclaimer: This article is general information only, not personalised investment advice. S-REITs carry market risk, sector concentration risk, and refinancing risk; unit prices can fall meaningfully and DPU is not guaranteed. Yields and market-cap figures are indicative as at Q1 2026 and will move; always verify current data on the relevant SGX disclosure pages and the Monetary Authority of Singapore (MAS) at mas.gov.sg. Tax treatment depends on your residency and circumstances — consult IRAS at iras.gov.sg or a licensed financial adviser. SingStat at singstat.gov.sg publishes housing-market and macro data referenced in this article. This article does not endorse any specific REIT or fund.

0 Comments