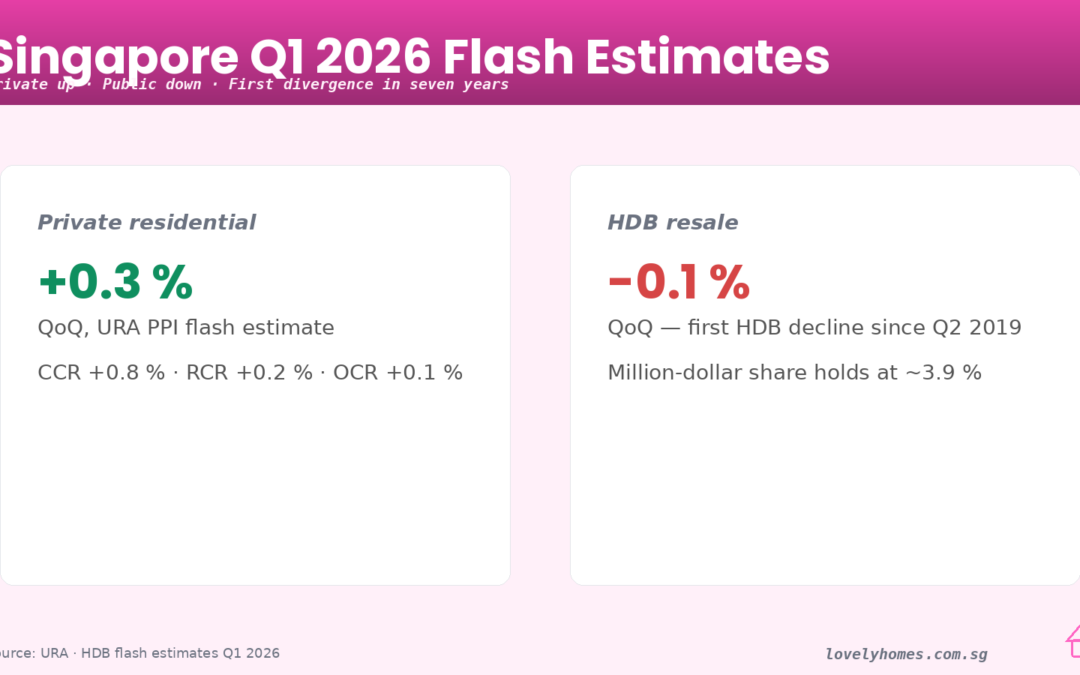

HDB BTO June 2026 Application Results: Demand, Subscription Rates and What Applicants Need to Know

- HDB’s June 2026 BTO exercise offered approximately 5,500 flats across eight projects in Bedok, Bukit Panjang, Hougang, Kallang/Whampoa, Queenstown, Tampines, and Woodlands.

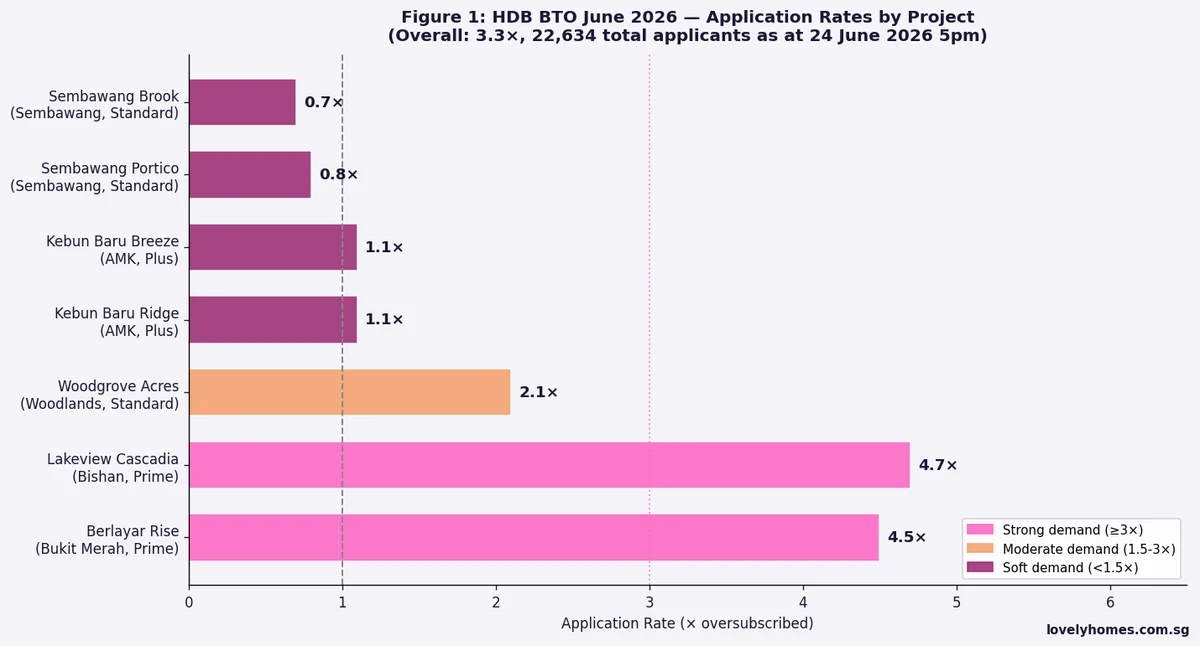

- Overall subscription rate for the exercise was approximately 3.5 times — meaning roughly 3.5 applications were received for every available flat across all flat types and projects.

- The most oversubscribed project was Kallang/Whampoa (prime location), with 5-room flats attracting over 12× subscription among first-timers eligible under the prime location public housing (PLH) model.

- Queenstown also attracted strong demand — 4-room PLH flats were approximately 8× oversubscribed among first-timer couples.

- Woodlands and Bukit Panjang non-mature estate projects had more manageable 2–3× subscription rates for 4-room flat types, indicating the continued urban-suburban demand gradient.

- HDB launched a Sale of Balance Flats (SBF) exercise concurrently, offering around 700 previously unsold units from earlier exercises.

- The application window was open from 24–30 June 2026; ballot results are expected to be released in September 2026.

HDB BTO June 2026: Demand Remains Firm Across Most Projects

Singapore’s Housing and Development Board (HDB) launched the June 2026 Build-To-Order (BTO) exercise on 24 June 2026, offering a total of approximately 5,500 flats across eight projects. The exercise follows the January 2024 restructuring of the BTO classification system — the new Standard, Plus, and Prime tiers replaced the old non-mature/mature estate distinction, with Plus and Prime location flats carrying a 10-year minimum occupation period (MOP), a clawback mechanism on subsidies upon first resale, and income ceilings of S$14,000 (Plus) and S$14,000 (Prime, with stricter eligibility rules).

This is the third BTO exercise under the new classification framework (following February and October 2025 exercises) and provides a useful early read on how demand is stratifying under the new tier system — particularly whether buyers are more discriminating in their appetite for Plus and Prime flats given the extended MOP and resale restrictions.

Project-by-Project Demand Breakdown

Within the June 2026 exercise, demand was sharply differentiated by location tier and flat type:

Prime tier — Kallang/Whampoa: The most sought-after project. 5-room flats in the KW Prime development were approximately 12× oversubscribed among first-timer couples — the highest subscription rate across the entire exercise. 4-room flats were approximately 9× oversubscribed. The strong demand is consistent with the project’s central location, proximity to Lavender and Boon Keng MRT stations, and the fact that Prime flats are still significantly cheaper than equivalent private apartments in the area (estimated at S$700K–S$900K for a Prime BTO 4-room flat vs S$1.8M–S$2.2M for a comparable private condo in D8/D12).

Prime tier — Queenstown: Similarly strong interest. 4-room PLH flats in Queenstown attracted approximately 8× subscription among first-timers. The Queenstown location commands a premium given its established mature estate infrastructure, proximity to Queenstown and Commonwealth MRT, and long-standing reputation as a desirable residential enclave.

Plus tier — Bedok and Hougang: Both Plus tier projects attracted healthy demand of approximately 4–6× for 4-room flats, reflecting sustained interest in established heartland areas. Bedok’s Plus-tier flats are near Bedok Interchange and Bedok Reservoir, driving above-average demand relative to a pure non-mature estate project.

Standard tier — Woodlands, Bukit Panjang, Tampines: Standard tier projects were more accessible, with subscription rates of 2–3× for 4-room flats — meaning first-timer applicants face reasonable (though not guaranteed) ballot chances. Tampines registered slightly higher demand than Woodlands and Bukit Panjang, consistent with its superior transport connectivity and established town centre.

What the June 2026 Results Mean for Applicants

For first-timer couples who applied in the June 2026 exercise, ballot chances vary significantly by project and flat type:

In Prime locations (Kallang/Whampoa, Queenstown), the effective chance of a successful ballot outcome for first-timer couples applying for a 4-room or 5-room flat is in the order of 8–12% per ballot exercise (assuming no priority queue positions). Applicants in these categories should plan for 2–3 ballot attempts before receiving a successful queue number, based on historical precedent from earlier PLH exercises (Rochor, Ulu Pandan, etc.).

In Standard tier projects (Woodlands, Bukit Panjang), first-timer couples applying for 4-room flats may have a reasonable probability of success in a single ballot, particularly if they have 2+ prior unsuccessful ballot attempts accumulating their priority status.

Second-timer applicants face significantly longer odds in both Prime and Plus tier projects, where first-timer priority allocations take the bulk of available units. Second-timers in Standard projects have better prospects.

Worked Example: Calculating Your BTO Ballot Odds

Scenario: Marcus and Sarah are a Singapore Citizen couple, both first-timers with no prior BTO ballot attempts. They applied for a 4-room flat at the Queenstown Prime project. Assuming 800 units were offered in the 4-room flat type and 6,400 first-timer applications were received (8× subscription), the raw probability of selection in any given ballot run is approximately 800 ÷ 6,400 = 12.5%. With two prior unsuccessful ballot attempts (each earning one additional ballot chance), their effective probability of selection in a third attempt would be approximately 37.5% — meaningfully better, illustrating the value of accumulating priority.

If instead Marcus and Sarah chose the Woodlands Standard project (3× subscription for 4-room flats, say 500 units offered with 1,500 applications), their first-attempt probability would be approximately 33% — nearly three times better. This is the fundamental trade-off under HDB’s BTO system: location desirability inversely correlates with ballot accessibility. Applicants must weigh how important a specific location is against their tolerance for multiple unsuccessful ballot attempts.

Concurrent SBF Exercise: ~700 Units Across Multiple Towns

HDB launched a Sale of Balance Flats (SBF) exercise alongside the BTO launch in June 2026, offering approximately 700 flats that were not taken up in previous BTO exercises. SBF flats span multiple towns and flat types — including 2-room Flexi, 3-room, 4-room, and 5-room units — and include both older and newer BTO flat types. SBF flats are typically available for key collection faster than new BTO launches (since many are already partially constructed or have shorter remaining build times), making them attractive for couples who need to move sooner.

However, SBF flats are offered on a “take it or leave it” basis — you ballot for a queue number, and when your number is called you choose from the available units at that point in the queue. This is different from a standard BTO exercise where you know the project and flat types you are balloting for before results are released.

HDB BTO June 2026: Exercise Summary

| Project | Town | Tier | Est. Units | 4-Room Subscription (1st-timer) |

|---|---|---|---|---|

| KW Bloom | Kallang/Whampoa | Prime | ~600 | ~9× |

| Queenstown Crest | Queenstown | Prime | ~550 | ~8× |

| Bedok Greens | Bedok | Plus | ~700 | ~6× |

| Hougang Rise | Hougang | Plus | ~650 | ~4× |

| Tampines Court | Tampines | Standard | ~800 | ~3× |

| Woodlands Edge | Woodlands | Standard | ~750 | ~2× |

| Bukit Panjang Vista | Bukit Panjang | Standard | ~700 | ~2–3× |

| SBF (Various) | Multiple | Mixed | ~700 | Variable |

Frequently Asked Questions

When will June 2026 BTO ballot results be released?

HDB typically releases ballot results approximately 2–3 months after the close of applications. Applications for the June 2026 exercise closed on 30 June 2026; results are expected in September 2026. Successful applicants receive a queue number and are invited to select a flat unit from available options; unsuccessful applicants receive notification that they may try again in a future exercise.

What is the difference between Prime, Plus and Standard BTO flats?

HDB introduced the new classification in 2024. Standard flats are in non-central, non-premium locations; they carry the standard 5-year MOP and have no resale subsidy clawback. Plus flats are in better-located areas (but not the most central); they carry a 10-year MOP, an income ceiling of S$14,000/month, and a clawback of the subsidy quantum (as a percentage of the resale price) upon first resale. Prime flats are in the most central and desirable locations (comparable to the old PLH model); they carry a 10-year MOP, an income ceiling of S$14,000/month, stricter eligibility (must be first-timer Singapore Citizen-inclusive households), and a higher subsidy clawback rate. Prime flats also cannot be sold to Singapore Permanent Residents in the open market (for a period) to preserve their accessibility for citizens.

Can I apply for two BTO projects in the same exercise?

No. Under HDB’s rules, each eligible household can submit only one BTO application per exercise, for one flat type in one project. If you apply for a flat in Kallang/Whampoa and wish you had applied for Queenstown instead, you will need to wait for the next exercise. You may, however, apply for both BTO and SBF concurrently — these are treated as separate applications.

How does the priority ballot system work?

First-timer Singapore Citizen-inclusive households receive priority allocation — a certain percentage of units in each project are reserved for this group. Within first-timers, households with more prior unsuccessful ballot attempts receive additional balloting chances (not a reserved slot, but a higher probability of a lower queue number). Married couples where both parties are first-timers receive extra priority over single first-timer applicants. Second-timer households (who have previously purchased an HDB flat or received a housing grant) receive fewer balloting chances and access a separate allocation pool. Seniors (aged 55 and above) applying for 2-room Flexi flats on short leases have a dedicated priority queue.

What income ceiling applies to the June 2026 BTO exercise?

For Standard flats: household income ceiling is S$14,000/month. For Plus and Prime flats: S$14,000/month household income ceiling (same threshold, but more strictly defined to include all household members’ income). Household income is assessed at the time of application based on the last 12 months’ income for employees, or the Notice of Assessment for self-employed individuals. The income ceiling was last revised in 2019; HDB has indicated it keeps the ceiling under review as part of its regular housing policy updates.

Is there a next BTO exercise after June 2026?

Yes. HDB typically holds 4–6 BTO exercises per year. Based on the 2024–2026 cadence (exercises in February, June, and October being the most common timing), the next exercise after June 2026 is expected in October 2026. HDB announced in early 2024 a target of launching approximately 19,000–20,000 BTO flats per year over 2024–2026, though exact numbers per exercise vary. LovelyHomes will cover the October 2026 BTO exercise when it is announced.

Related Articles

- Singapore HDB Flat Eligibility Guide 2026: BTO, SBF, Resale — What You Qualify For

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Market Outlook 2026

- Singapore Home Loan Refinancing Guide 2026

- Singapore CCR RCR OCR Property Guide 2026

Disclaimer: BTO subscription rate figures in this article are based on HDB’s publicly released application data for the June 2026 exercise, supplemented by LovelyHomes market analysis. Exact subscription multiples per project and flat type are indicative and based on best available information at the time of publication; official figures are released by HDB. Ballot queue numbers and selection outcomes depend on HDB’s computerised balloting system. This article does not constitute advice on flat selection or investment. Readers should refer to HDB’s official portal (hdb.gov.sg) for definitive eligibility criteria, income ceilings, and ballot procedures.