Inheriting Property in Singapore 2026: Probate, Stamp Duty & Estate Planning Essentials

Inheriting property in Singapore is one of those events most families confront only once or twice in a lifetime. The legal mechanics are forgiving compared with the United Kingdom or the United States — Singapore has no estate duty, no inheritance tax, and no capital-gains tax on residential property — but the process is still demanding. The deceased’s estate must clear probate, the heir must understand how the property fits into their existing ABSD count, and several stamp-duty deadlines run from the date of death rather than the date of transfer. Get any of these wrong and you can either lose months of clear title or unwittingly trigger ABSD on a future purchase.

This 2026 guide walks the entire journey end to end — what happens whether or not the deceased left a Will, the statutory shares set by the Intestate Succession Act, the typical costs of probate, the stamp-duty position on transfer to the heir, and the all-important interaction with ABSD on the heir’s next property purchase. All figures and rules below reflect Singapore’s position as of 29 April 2026. For the live position, always check Family Justice Courts, the Intestate Succession Act, and IRAS Stamp Duty.

Quick Answer — inheriting property in Singapore

- Singapore abolished estate duty for deaths from 15 February 2008. There is no longer an inheritance tax.

- The deceased’s estate goes through probate (with a Will) or Letters of Administration (without one).

- Without a Will, the Intestate Succession Act (ISA) sets statutory shares between spouse, children and parents.

- Transfer of property to the heir is a transmission, not a sale — no BSD or ABSD on that transfer.

- BUT — the inherited property counts toward the heir’s property tally for ABSD on their next purchase.

- Joint-tenancy property passes automatically by survivorship — outside the Will or ISA.

- HDB flats follow extra rules — only Singapore Citizen/PR family members who meet eligibility can inherit and remain in occupation.

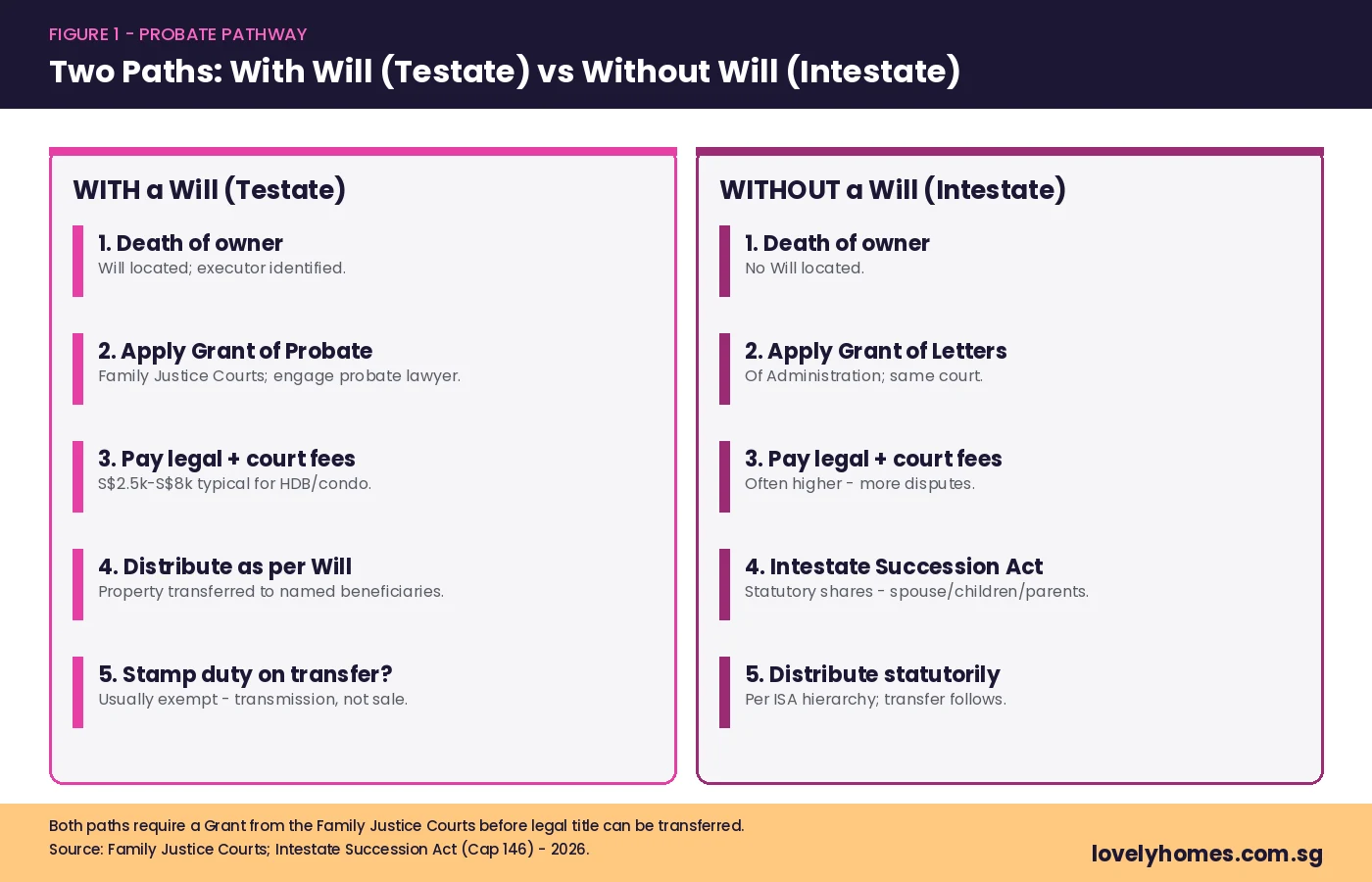

The Two Pathways: With a Will and Without

The first question after a death is the same one solicitors ask: was there a Will? The answer determines which application the executors or family must make to the Family Justice Courts, who has standing to administer the estate, and how the property is ultimately divided.

With a Will (Testate Succession)

If the deceased left a valid Will, the named executor applies to the Family Justice Courts for a Grant of Probate. The Will dictates who inherits the property — the executor’s job is to carry out those instructions after settling the estate’s debts. For a clean estate (no caveats, no contests, full documentation), a Grant of Probate is typically issued within 4–8 weeks. Probate fees range roughly S$3,000 to S$8,000 in legal costs for a single residential property, plus court filing fees of a few hundred dollars.

Without a Will (Intestate Succession)

Where there is no Will, the next-of-kin applies for a Grant of Letters of Administration. The applicant administers the estate and distributes it according to the statutory shares set out in the Intestate Succession Act (ISA). Letters of Administration take longer than probate — typically 8–16 weeks — because the Court must satisfy itself who is entitled to apply, what the estate consists of, and that no contest exists. Where the estate is over S$5 million or contains foreign assets, the timeline extends materially.

Joint-Tenancy — The Quiet Third Path

For property held by spouses as joint tenants, the surviving spouse takes the deceased’s share automatically by survivorship — outside the Will, outside the ISA, and outside probate altogether. The surviving spouse simply lodges a Notice of Death with the Singapore Land Authority (SLA) along with the death certificate, and the title is updated. This is the cleanest of the three pathways. By contrast, tenancy-in-common property passes through the Will or the ISA like any other estate asset. For the difference, see our Joint Tenancy vs Tenancy in Common Singapore 2026 guide.

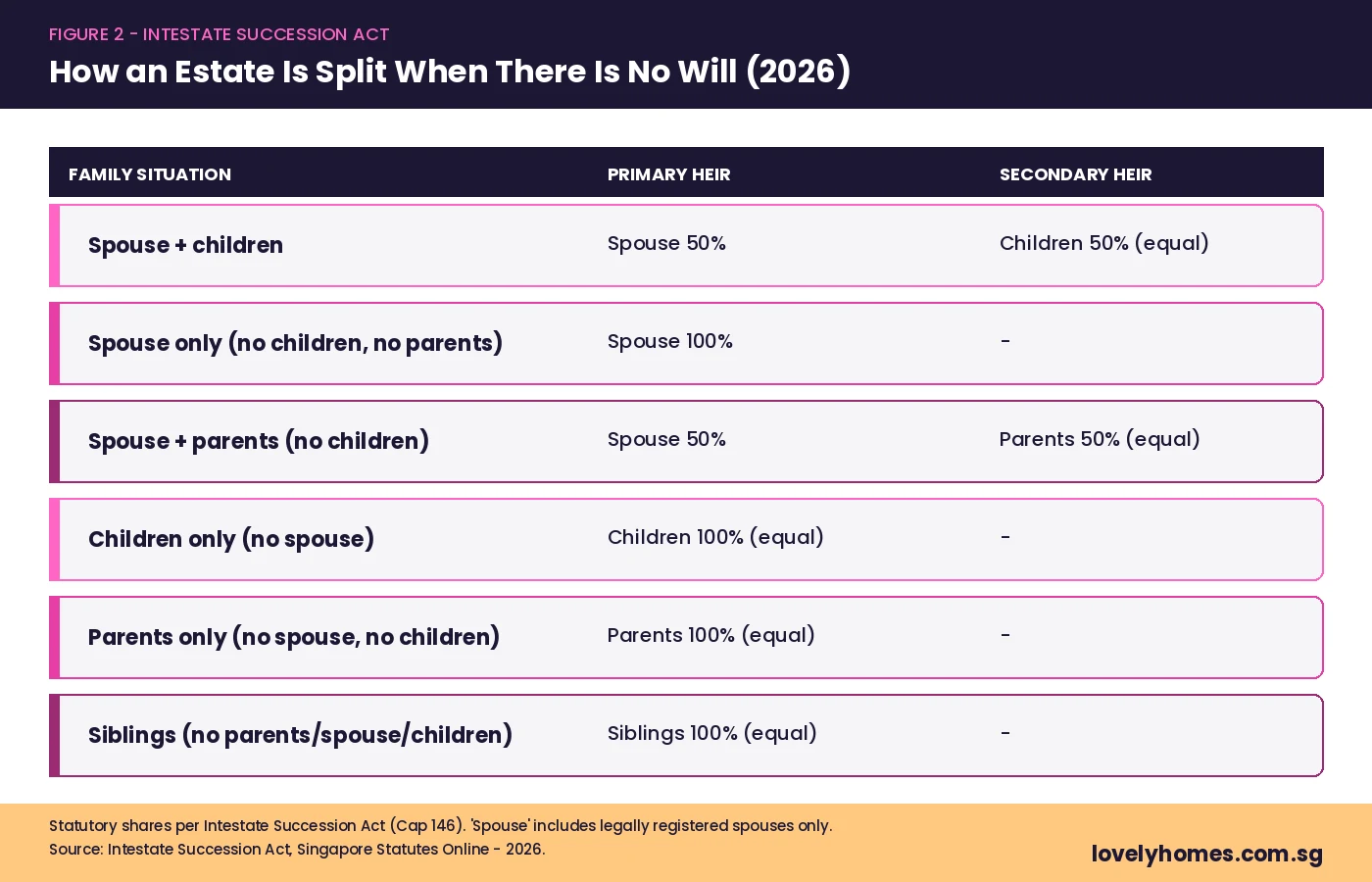

The Intestate Succession Act — How an Estate Without a Will Is Split

If you die intestate (without a Will) and you are domiciled in Singapore, the Intestate Succession Act (Cap 146) determines exactly who gets what. The Act is gender-neutral but assumes a fairly traditional family structure — spouse, children, parents, siblings — in that order of priority.

| Family Situation | Statutory Distribution |

|---|---|

| Spouse + children | Spouse 50%; children 50% (split equally between children) |

| Spouse only (no children, no parents) | Spouse takes 100% |

| Spouse + parents (no children) | Spouse 50%; parents 50% (equally) |

| Children only (no spouse) | Children 100% (equal shares per stirpes) |

| Parents only (no spouse, no children) | Parents 100% (equally) |

| Siblings (no parents, no spouse, no children) | Siblings 100% (equally) |

| No surviving immediate or extended family | Estate goes to the Singapore Government (bona vacantia) |

Two practical points worth highlighting. First, “spouse” in the Act means a legally registered spouse only — long-term partners, fiancés, and ex-spouses are excluded, no matter how long the relationship. Second, step-children are not statutory heirs unless legally adopted. If you have a blended family, you almost certainly need a Will — the ISA will not deliver the outcome most blended families assume.

HDB Inheritance — Special Rules That Override the General Position

HDB flats are not just real estate — they are part of Singapore’s public housing system, with eligibility rules that override the general law of succession. When a HDB owner dies, the flat does not simply transfer to the heir named in the Will or the ISA share — HDB still has to approve who can inherit and remain in the flat. The rules are roughly:

- The heir must be Singapore Citizen or PR. Foreigner heirs cannot inherit and remain on title for an HDB flat.

- The heir must satisfy HDB’s family-nucleus or single-buyer eligibility. A 28-year-old single child cannot inherit the flat outright until age 35 under the Single Singapore Citizen Scheme — the flat is held in trust until then or sold on the open market.

- Existing property by the heir matters. If the heir already owns a private residential property, HDB’s ownership rules require the heir to dispose of the private property within 6 months of the inheritance to retain the HDB flat, or vice versa.

- The flat’s remaining MOP and SC quota apply. Inheritance does not reset the Minimum Occupation Period or trigger any quota issues, but the heir must continue to comply with rental, sublet, and EIP/SPR quota rules.

For a HDB-specific deep-dive, our How to Sell an HDB Flat 2026 guide covers the complications when an inherited HDB flat must be sold to fund the estate or to free the heir to remain on private property. The HDB section of the official HDB site sets out the live position.

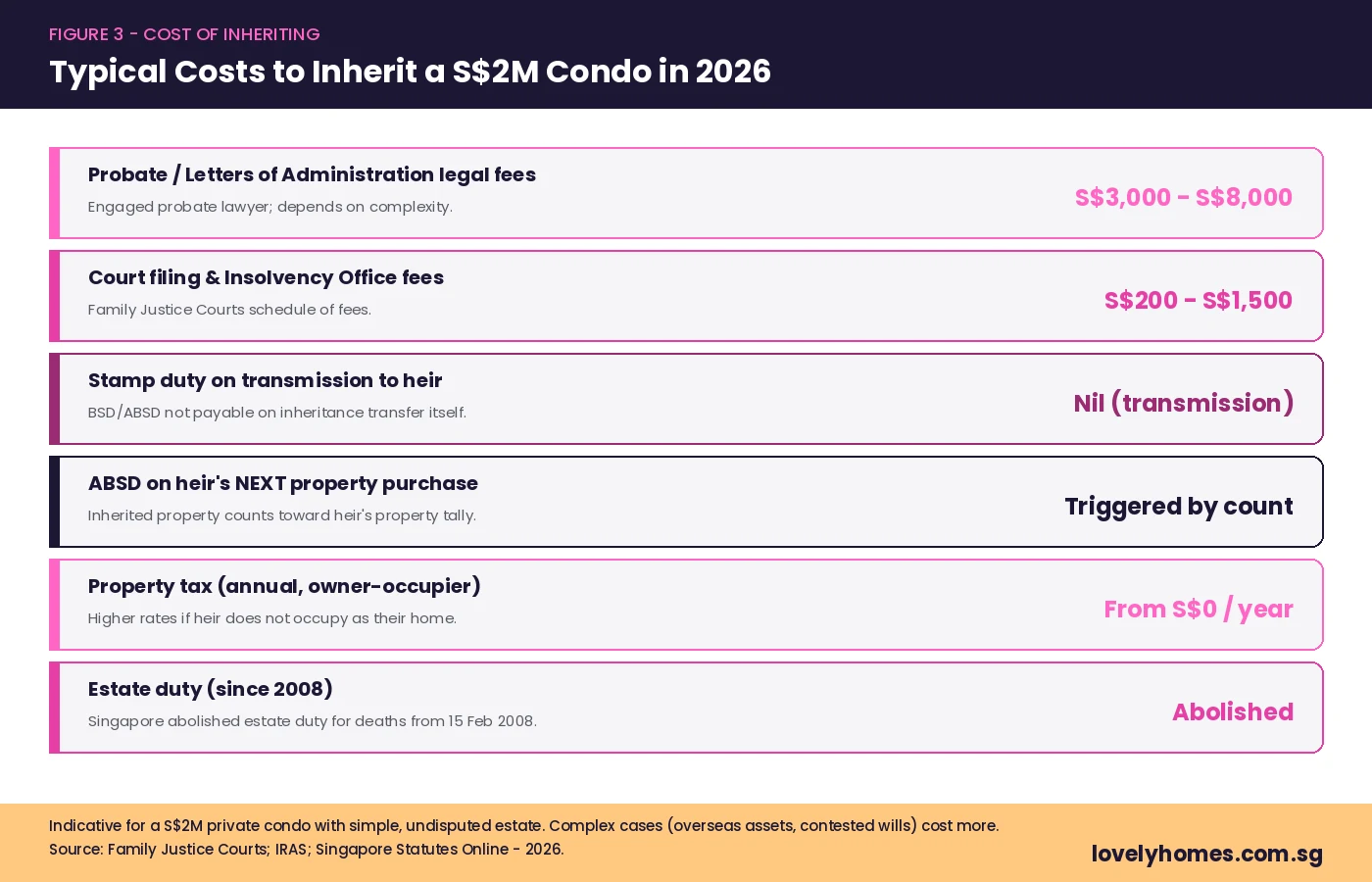

Stamp Duty on the Inheritance — What You Actually Pay

Singapore’s tax position on inheritance is unusually generous compared with major Western jurisdictions:

1. No estate duty since 15 February 2008

Singapore abolished estate duty for deaths occurring on or after 15 February 2008. There is no “death tax”, no “inheritance tax”, and no “estate tax” on the value of the property at the date of death. This is a major reason why Singapore is favoured by family-office structures over the UK (40% inheritance tax) or the US federal estate tax.

2. No BSD or ABSD on transmission

The transfer of the property from the deceased’s estate to the heir is a transmission — not a sale — and therefore not subject to Buyer’s Stamp Duty (BSD) or Additional Buyer’s Stamp Duty (ABSD). This is consistent with IRAS’s position that ABSD only applies on a purchase. Inheriting your parent’s flat does not, in itself, trigger any stamp-duty bill.

3. BUT — ABSD count is affected for the heir’s next purchase

Here is the trap. While the inheritance itself attracts no ABSD, the inherited property counts toward the heir’s property tally for any future purchase. A Singapore Citizen who inherits their parent’s HDB flat now owns one residential property — their next purchase will be an SC-2nd at 20% ABSD, not the SC-1st at 0%.

Heirs who are mid-purchase when the inheritance arrives need to plan carefully. A common workaround is to renounce the inherited interest in favour of another beneficiary — legally permissible under the Probate & Administration Act, provided the renunciation is done before the heir takes any benefit from the property. We strongly recommend speaking to a probate lawyer before renouncing because the implications are irreversible. For broader context on ABSD, see our ABSD Singapore Complete Guide 2026.

4. Property tax continues, billed to the new owner

The annual property tax obligation passes to the heir on transmission. If the heir occupies the property as their home, owner-occupier rates (lowest band) apply. If the heir already has another home and rents the inherited property out, IRAS will apply the higher non-owner-occupier rates. See our Singapore Property Tax 2026 guide for current rates and bands.

CPF Refund — The Easily-Missed Step

If the deceased used CPF to fund the property, the principal sum used plus accrued interest must be refunded to their CPF account on transfer. The CPF refund is paid to the deceased’s estate (effectively to the named CPF nominees, if any, or otherwise distributed by the executor). This is not a tax — it is the final clearing of the deceased’s CPF position. The figure can be substantial: a 4-room HDB flat that was funded with S$200,000 of CPF in 2000 might owe over S$400,000 of principal-plus-accrued-interest in 2026.

Heirs sometimes mistake this CPF refund for a charge that they have to pay personally. They do not — the refund comes out of the estate’s share of any sale proceeds, or, if the property is being retained, the estate must arrange for the refund from cash assets. The refund is a precondition for clear title and cannot be deferred.

How Long Does the Whole Process Take?

For a simple estate — one residential property, undisputed Will or clean intestacy, one or two heirs, no overseas assets — the typical journey looks like this:

| Stage | Typical Timeline | Who Drives It |

|---|---|---|

| Locate Will & gather documents | 1–2 weeks | Family |

| Engage probate lawyer | 1 week | Family |

| File Grant application (probate or LA) | 2–4 weeks | Lawyer |

| Court issues Grant | 2–6 weeks for probate; 8–16 for LA | Court |

| Lodge Grant + Notice of Death with SLA | 1–2 weeks | Lawyer |

| CPF refund & outstanding loan settlement | 2–4 weeks | Lawyer / family |

| Title transmitted to heir | 2–3 weeks after CPF/loan clearance | SLA |

| Total simple estate | ~3–4 months testate; ~5–7 months intestate | — |

Contested estates, estates over S$5 million, estates with overseas immovable property, or estates where the deceased’s domicile is uncertain all add months to the timeline. Engaging an experienced probate solicitor early is the single most important action a family can take to keep the timeline on track.

A Worked Example — What Mr Tan’s Family Actually Pays

Mr Tan, a Singapore Citizen aged 78, dies in March 2026. He leaves behind:

- A 4-room HDB flat in Bedok (held in his sole name), valued at S$650,000.

- A S$2 million private condominium in District 15 (held jointly with his wife as joint tenants).

- A simple Will leaving the HDB flat equally to his two adult children, both Singapore Citizens.

The flow:

- Condo — immediate transfer. The District 15 condominium passes automatically to Mrs Tan by survivorship. No probate, no Will, no ISA. Mrs Tan lodges the death certificate with SLA. Cost: roughly S$300 in lodgement fees.

- HDB flat — through probate. The executor (eldest son) applies for a Grant of Probate. Court issues the Grant in five weeks. Probate legal fees: ~S$4,500. The HDB flat is then transmitted equally to the two children. Both children are Singapore Citizens, but each already owns a private condo — under HDB rules, they cannot retain the inherited HDB flat and must dispose of either the HDB or the private property within six months. Family decides to sell the flat on the open market.

- CPF refund. Mr Tan had used S$280,000 of CPF (principal + accrued interest) on the HDB flat. The refund flows from sale proceeds to his CPF account, then to nominees.

- Sale proceeds distributed. Net of the CPF refund and S$8,000 selling costs, the remaining S$362,000 is divided equally between the two children (S$181,000 each).

- ABSD impact for the children. Because each child took beneficial ownership of the HDB flat before selling it, each had two residential properties on title for that brief window. Their next condo purchase will be an SC-3rd-property at 30% ABSD — not 0%. The family should have spoken to a probate lawyer about renouncing in favour of the surviving spouse, or selling the flat directly out of the estate without taking transmission.

This is the textbook example of why estate planning matters. With one Will revision — leaving the HDB flat to Mrs Tan instead — the entire ABSD complication for the children would have been avoided.

How Estate Planning Works in Singapore (Briefly)

Three estate-planning instruments do most of the heavy lifting:

- A valid Will. Drafted, signed, and witnessed per the Wills Act. Costs from S$300 (simple Will at a high-street firm) up to several thousand for a complex estate. The single highest-leverage action any property-owning Singaporean can take.

- CPF nominations. CPF moneys do not pass through the Will or the ISA — they go to nominees. Without a CPF nomination, balances go to the Public Trustee for distribution per ISA. Update CPF nominations whenever there is a major life event.

- Manner of co-ownership. Married couples buying property together should consciously choose between joint tenancy (survivorship transfers automatically) and tenancy in common (each owner’s share passes through their estate). The choice has profound implications for inheritance, divorce, and ABSD planning.

For an even more direct approach, large families with significant property holdings sometimes use private trusts — though Singapore’s ABSD-on-trustees position (65% on the trustee’s entity rate) means trust structures need careful structuring to avoid triggering punitive ABSD. This is well outside the scope of a general guide and demands specialist trust counsel.

What Might Come Next

Two areas to watch. First, Singapore’s policy stance on intergenerational transfer is generally favourable, but the ABSD position on inherited property has been quietly tightening since 2018. Expect IRAS to continue scrutinising arrangements where inheritance is structured to avoid ABSD — in particular “in-life gifts” and trust structures that benefit a Singapore property owner’s children. Second, the Family Justice Courts have signalled that they may digitise more of the probate process by 2027, which should compress the testate timeline below 4 weeks for simple estates. None of this is policy yet, and these paragraphs are editorial speculation only.

Frequently Asked Questions

Do I have to pay any tax when I inherit property in Singapore?

No tax is payable on the transmission itself — Singapore abolished estate duty for deaths from 15 February 2008, and no BSD or ABSD applies on a transfer that is not a sale. You will, however, pick up the annual property-tax obligation from the date of transmission, and any future purchase you make will count the inherited property toward your ABSD tally.

My parent died without a Will. Can I just sign over my share to my sibling?

Yes — this is called a Deed of Family Arrangement, signed after the Grant of Letters of Administration is issued. All ISA-statutory heirs must agree, and the deed is filed with the Court. It allows the family to redirect the estate without having to go to a full reapplication. Engage a probate solicitor to draft the deed and ensure stamp duty implications are covered.

Can I refuse the inheritance?

Yes. A beneficiary can renounce their interest under the Probate & Administration Act before taking any benefit from the property. The renunciation must be in writing and is irrevocable. Heirs sometimes do this to avoid the ABSD-count consequence of inheriting, channelling the property to a sibling who would not be affected.

What happens to the deceased’s outstanding mortgage on the property?

Most Singaporean homeowners carry Mortgage Reducing Term Assurance (MRTA) or the Home Protection Scheme (HPS) for HDB. Either policy pays off the outstanding loan on death — the heir takes the property unencumbered. If no MRTA/HPS exists, the mortgage continues and the heir must either continue servicing it (if eligible to take over the loan) or sell the property to discharge it.

If I am a Singapore Citizen and inherit a Malaysian property, do I need to declare it in Singapore?

Yes. Even though no Singapore tax is due on the inheritance itself, you must declare any overseas residential property you own when applying for ABSD remission, HDB schemes, or LBS — the Singapore Government counts overseas residential property toward eligibility tests. You will also have Malaysian filing obligations, including the Real Property Gains Tax position on any future disposal.

Can a foreigner inherit a Singapore property?

Yes for private property — foreigners can inherit and own non-restricted private residential property in Singapore, subject to the Residential Property Act for landed homes. For HDB flats, foreigners cannot inherit the flat directly — the HDB flat must be sold and the proceeds distributed instead. Engage a Singapore lawyer who deals with cross-border probate.

How much do probate lawyers cost in 2026?

For a simple estate with one residential property and no contests, expect around S$3,000–S$8,000 in legal fees (with a Will) or S$4,000–S$10,000 (without a Will, since Letters of Administration take longer and require a personal-representative bond). Court filing fees are typically a few hundred dollars more.

Related Articles

- ABSD Singapore Complete Guide 2026

- Joint Tenancy vs Tenancy in Common Singapore 2026

- Decoupling for Married Couples Singapore 2026

- Singapore Property Tax 2026: Owner-Occupier vs Investor Rates

- CPF for Property Purchase Singapore 2026

- How to Sell Your HDB Flat Singapore 2026 Timeline

- Property Conveyancing Guide Singapore 2026

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. Probate, succession, stamp duty, and HDB inheritance rules change over time and depend on individual circumstances. Always verify the live position with the Family Justice Courts, the Intestate Succession Act, the HDB website, and IRAS, and consult a Singapore-qualified probate solicitor before acting on any estate matter.