Freehold or 99-year leasehold? It is the single most-asked question on every Singapore condo viewing — and the most-misunderstood. The freehold premium is real but smaller than most buyers think. Lease decay is real but slower in the early years than buyers fear. Whether the freehold premium is worth paying depends almost entirely on your holding period, not your gut feeling.

This guide unpacks how Singapore property tenure actually works in 2026 — the four tenure types you will encounter, the maths behind Bala’s Curve (the lease-relativity table the Singapore Land Authority uses internally), the financing and CPF rules that bite as a lease shortens, and a worked 20-year hold comparison on a S$1.8 million condo in the same district. Where useful, we cross-link to the underlying frameworks at IRAS and CPF.

Quick Answer — Freehold vs 99-Year Leasehold at a glance

Freehold premium in comparable locations: typically 10–20% over 99-year leasehold

Bala’s Curve sets leasehold value at ~74.7% of freehold at 50 years remaining; ~60% at 30 years; ~49% at 20 years

CPF restrictions kick in when remaining lease is below 60 years; cannot use CPF at all if lease falls below 30 years for the next buyer

Bank financing tightens when remaining lease is below 40 years

Lease must cover the youngest applicant’s age + 95 for full CPF usage

Most new-launch condos and ECs are 99-year leasehold; freehold supply is fixed at ~5% of Singapore’s land area

For holding periods under 20 years in good locations, leasehold often outperforms freehold on a return-on-capital basis

For multi-generational holds (40+ years), the freehold premium pays for itself

What Are You Actually Buying? The Four Tenure Types

Singapore property comes with four main tenure types — and the difference between them is more legal than emotional. Tenure determines how long the State (or your descendants) recognises your interest in the land beneath your unit. Strata-Title in your condo gives you ownership of your apartment and a share in the land — for as long as the land tenure runs.

Figure 1: The four tenure types you will encounter in Singapore.

Freehold (Estate in Fee Simple)

You own the land in perpetuity, with the right to sell, lease or pass it to heirs without time limit. About 5% of Singapore’s land area is freehold — concentrated in the prime districts (D9, D10, D11) and pockets of D15. The State has not generally released new freehold land since 1965; almost all freehold supply today is from pre-1965 grants. This is why freehold supply is functionally fixed and cannot be created.

999-Year Leasehold

Issued mostly under pre-1900 colonial grants. Functionally identical to freehold for any sensible holding period — banks and valuers treat 999-year as a freehold equivalent. About 1% of Singapore’s land area sits on 999-year tenure. When you read a marketing brochure that says “freehold equivalent”, this is what is meant.

99-Year Leasehold

By far the most common tenure for new condos, Executive Condominiums, HDB flats, and almost every site released through the Government Land Sales (GLS) programme. The lease starts running on the date of issuance — which for a new launch is typically 1–2 years before TOP. Land reverts to the State at the end of the 99 years, with the building demolished or redeveloped. Subject to Bala’s Curve depreciation, which we cover next.

60-Year and 30-Year Leases

Unusual outside specific commercial or industrial sites. Some HDB shophouses sit on 60-year leases; certain industrial GLS plots are 30-year. CPF, bank-financing and resale rules are sharply restricted on these — not the tenure for a typical residential buyer.

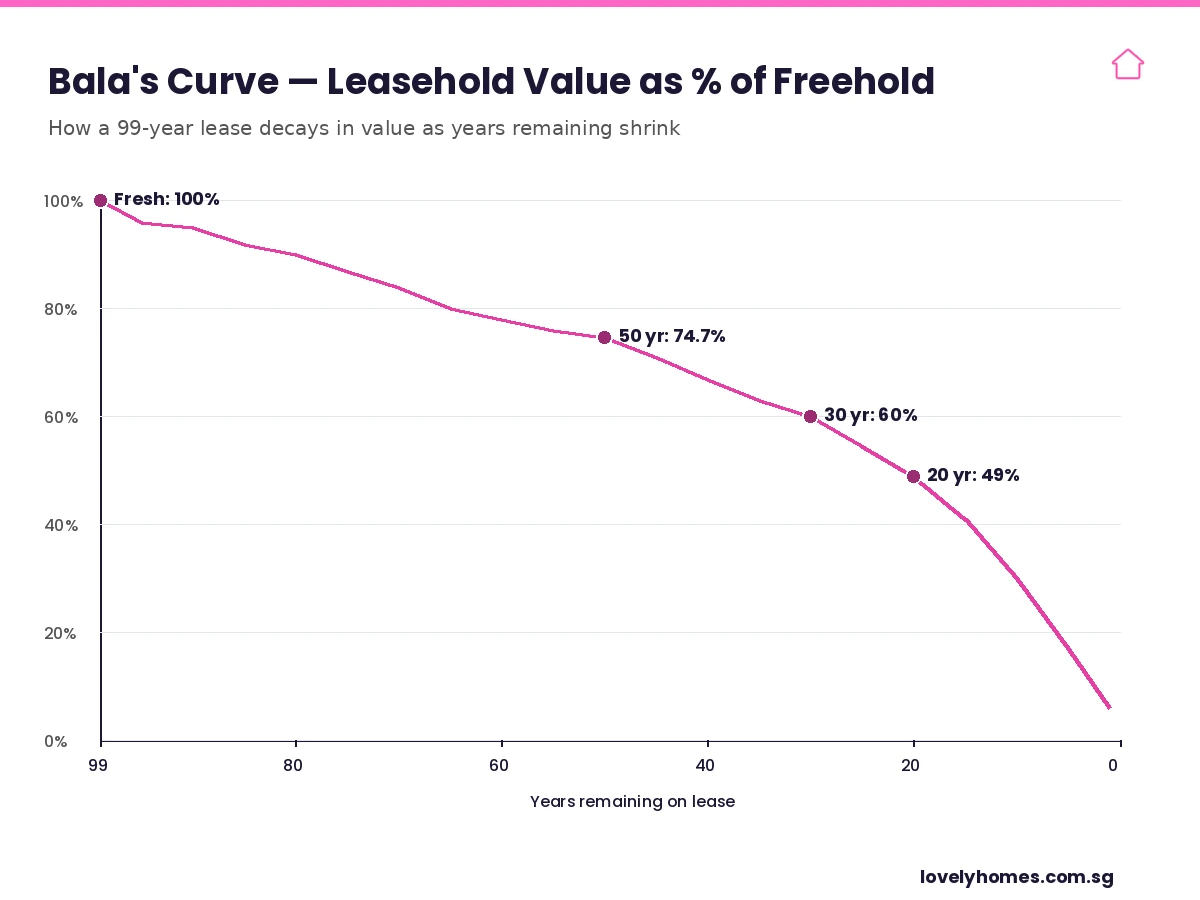

Bala’s Curve — The Maths Behind Lease Decay

The single most important framework for understanding 99-year leasehold pricing is Bala’s Table (sometimes called Bala’s Curve, after Mr V K Balasubramaniam who developed it for the Singapore Land Authority in the 1990s). Bala’s Table sets out the value of a leasehold property as a percentage of its equivalent freehold value, indexed to the years remaining on the lease.

Figure 2: Bala’s Curve — non-linear lease decay across the 99-year lease. Steepest depreciation falls in the final 30 years.

Two features of the curve matter most:

The depreciation is non-linear. A fresh 99-year lease is worth roughly the same as freehold — the curve sits at 100%. After 50 years remaining (i.e. ~half-life), value is still ~74.7% of freehold — a far gentler decay than the simple linear “halfway = 50%” intuition. The steep portion of the curve falls in the last 30 years, when value drops from ~60% (30 years remaining) to ~17% (5 years remaining).

Bala’s Table is the floor, not the market. Real-world transactions rarely match the table exactly. Local demand, building condition, en-bloc potential, and lease topping-up rumours can push prices well above (or below) the Bala line. The table is what SLA uses to price lease top-ups and to convert tenure for tax purposes — not what the open market necessarily pays.

For a buyer, the practical implication is that the first 30–40 years of a 99-year lease behave very like freehold. A 99-year condo at TOP today is essentially “freehold for two generations”. The depreciation problem is real for buyers planning to hold past Year 60 or thinking about en-bloc redevelopment as the exit strategy.

The CPF and Financing Cliffs — When Lease Decay Starts to Bite

Bala’s Curve is the underlying valuation framework, but two regulatory cliffs determine when lease decay actually starts to hurt resale liquidity:

The CPF Usage Rules

CPF can be used in full only if the remaining lease covers the youngest buyer’s age plus 95 years. For a 35-year-old buying a property today, the remaining lease must be at least 60 years for full CPF use; otherwise CPF usage is pro-rated and capped. If the remaining lease is below 30 years, CPF cannot be used at all by your next buyer — which collapses the buyer pool to cash buyers only.

The Bank Financing Rules

Bank loan tenure cannot exceed (lease remaining minus a buffer; typically 5 years). If the remaining lease is below 40 years, banks will quote shorter loan tenures, lower LTVs, and higher rates — and some banks will decline outright. When this happens, your effective buyer pool narrows further.

Together, these two cliffs mean that the Bala’s Curve depreciation is amplified in the secondary market by liquidity contraction. A 40-year-remaining lease may be worth 67% of freehold in pure Bala terms, but the smaller buyer pool means actual transactions can clear at a steeper discount. This is why the “sweet spot” for selling a 99-year leasehold is usually before Year 50, not after.

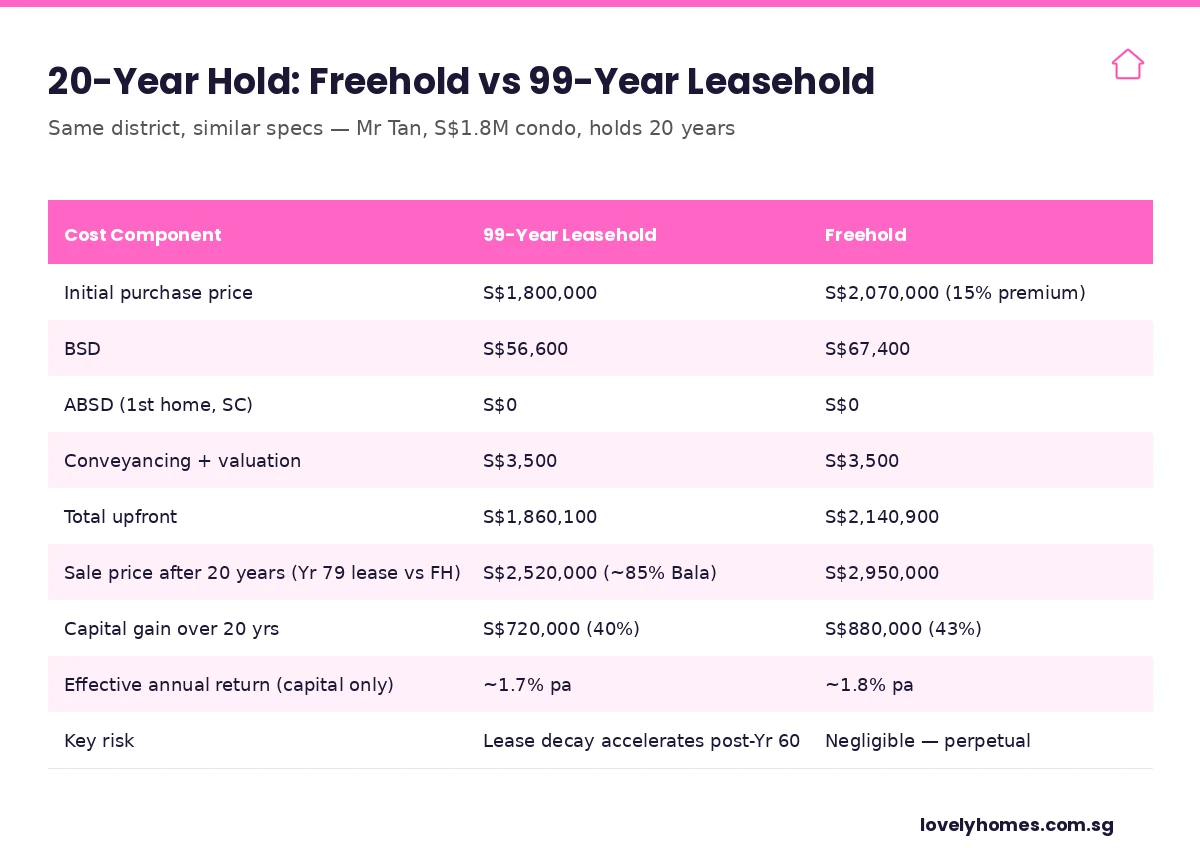

Worked Example — 20-Year Hold, Same District, Same Specs

Let’s strip out emotion and compare on the maths. Mr Tan is 40, a Singapore Citizen first-time buyer. He is choosing between two condos in the same District 15 micro-market: a brand-new 99-year leasehold at S$1,800,000 and a 999-year (freehold-equivalent) unit at S$2,070,000 — a 15% freehold premium, which is roughly the historic norm. He plans to hold 20 years.

Figure 3: 20-year hold — freehold vs 99-year leasehold, identical-district worked example.

Cost / Outcome

99-Year Leasehold

Freehold

Year 0 purchase price

S$1,800,000

S$2,070,000

Year 0 BSD

S$56,600

S$67,400

Year 0 ABSD (1st home, SC)

S$0

S$0

Year 0 conveyancing

S$3,500

S$3,500

Total upfront outlay

S$1,860,100

S$2,140,900

Year 20 sale price (assume 2.0% pa district appreciation, freehold; leasehold capped at Yr 79 Bala factor ~92% of freehold)

S$2,520,000

S$2,950,000

Capital gain

S$720,000 (40%)

S$880,000 (43%)

Effective annual return (capital only)

~1.7% pa

~1.8% pa

Return on incremental S$280,800

~3.4% pa — the marginal freehold premium implies a ~3.4% annualised return on the extra capital tied up

The headline finding: in this worked example, the freehold buyer earns a ~3.4% annualised return on the extra S$280,800 tied up in the freehold premium — modest, and below typical bond returns. For a 20-year hold, the leasehold often comes out marginally ahead on a return-on-capital basis, especially if the freed-up capital can earn 4–5% in conservative investments.

Where the maths flips is at longer holding periods. Repeat the calculation across 40 years — with the leasehold now at Yr 59 remaining (~78% Bala) versus a still-perpetual freehold — and the freehold premium starts compounding strongly. By Year 50 of holding, the freehold has typically earned a meaningful spread.

When Freehold Wins, When Leasehold Wins

The framework most experienced Singapore buyers use is to match tenure to holding period and exit strategy:

Hold under 15 years: 99-year leasehold typically wins on return-on-capital. Lease decay is too gentle in this window to matter, and the freed-up capital can earn elsewhere. This is the typical short-to-medium hold investor case.

Hold 15–30 years: A toss-up. Outcome turns on (a) the actual freehold premium paid and (b) the district’s underlying appreciation rate. In high-growth districts, leasehold often wins; in slow-growth districts, the freehold premium does its job.

Hold 30+ years or multi-generational: Freehold wins. Lease decay enters its accelerating zone, and the freehold becomes a meaningfully stronger compounding asset. This is the family-legacy or trust-held case.

Buying for own-stay, expecting to en-bloc: Leasehold can win if the project has clear redevelopment upside (high plot ratio uplift, supportive URA zoning, agreeable owner mix). The collective sale becomes the “lease top-up” you couldn’t buy directly.

Buying for rental yield: Leasehold typically yields more — lower entry price for the same rent. Yield-focused investors generally prefer leasehold.

Owners and developers occasionally apply to SLA to top up a depleting lease — restoring it to a fresh 99 years for a payment based on the difference between the current and the topped-up value. The cost is calculated against Bala’s Table. In practice, lease top-ups are most often initiated as part of an en-bloc / collective sale, where the developer negotiates the top-up alongside the redevelopment approval.

An individual owner cannot reliably plan for a private top-up. The Government’s VERS (Voluntary Early Redevelopment Scheme), announced in 2018 for selected HDB precincts, is a separate framework from private leasehold top-ups and applies only to public-housing estates. There is no equivalent statutory framework for private leasehold properties — which means private leasehold owners cannot count on lease top-ups as part of their long-term plan.

What This Means for You

If you take only five things away from this guide, take these:

Match tenure to holding period. Under 15 years, leasehold typically wins. Over 30 years, freehold typically wins. In between, run the maths on the actual freehold premium versus the capital-cost spread.

Don’t pay more than ~15–20% premium for freehold. Above this, the maths almost never works for typical holding periods. Some new-launch freehold projects have asked for 25–30% premiums — treat those with caution.

Watch the lease-remaining number when buying resale. 60 years is the CPF cliff for buyers in their late 30s. Below that, you start losing CPF eligibility for your next buyer — which compresses your exit price more than Bala’s Table would suggest.

Check the lease commencement date carefully. A new-launch 99-year condo often has a lease that started 1–2 years before TOP, so a buyer at TOP only gets ~97–98 years remaining, not 99.

If en-bloc is your exit strategy, leasehold can win. The collective-sale premium effectively converts the 99-year lease into a one-time cash payout that bypasses Bala’s Curve. But en-bloc success rates vary — do not assume your project will get there.

What Might Come Next

Three policy and market variables to watch in 2026–2027:

Bala’s Table revision. SLA last refreshed Bala’s Table several years ago. A revision — especially one that flattens the curve or pushes the steep zone closer to lease end — would mark up secondary leasehold values across the board. There is no current signal of revision in 2026.

Freehold premium compression. Several recent freehold launches have struggled to clear meaningful premiums over comparable leasehold launches in the same district. If this trend continues, the structural freehold premium may compress towards the 5–10% range, weakening the case for paying up.

VERS or analogous private-lease scheme. If the Government extends a VERS-style framework to private leaseholds (an idea floated occasionally by industry figures), the long-tail risk of holding past Year 60 reduces sharply — and the freehold premium loses some of its insurance value.

Frequently Asked Questions

Is freehold always better than leasehold?

No. Freehold is structurally lower-risk for very long holds (30+ years) and multi-generational holds. For shorter holds (under 15 years), the capital tied up in the freehold premium often earns a lower return than the same capital deployed elsewhere. The right answer depends entirely on your holding period.

What happens at the end of a 99-year lease?

The land reverts to the State. Owners typically receive no compensation unless a private collective-sale or a public scheme (e.g. VERS for HDB) intervenes earlier. In practice, almost every 99-year property in Singapore exits via en-bloc or major redevelopment well before the lease expires — full lease expiry is rare for residential land.

Can CPF be used for any leasehold property?

Only if the remaining lease covers the youngest applicant’s age plus 95. For full CPF withdrawal limits to apply, the lease must run at least to that age. Where the lease is shorter, CPF usage is pro-rated. Below 30 years remaining, CPF cannot be used at all by the next buyer.

How is Bala’s Curve different from straight-line depreciation?

Straight-line depreciation would assume the leasehold loses 1/99 of its value every year. Bala’s Curve recognises that the early years of a long lease have negligible depreciation (because the buyer pool is large and time-to-expiry is far away), while the final 20–30 years see steep depreciation (because financing and CPF rules compress the buyer pool sharply). Bala’s Table is non-linear and far more accurate for real-world pricing.

Are HDB flats freehold or leasehold?

All HDB flats are 99-year leasehold. The lease starts when the block is completed and the title issued. By the time most BTO buyers move in, the lease typically has between 96 and 99 years remaining. HDB resale flats from the 1970s and 1980s have far less remaining lease — some now under 60 years — which is why CPF eligibility for older HDB resale is increasingly tight.

Does freehold matter for rental yield?

Not really. Tenants pay for liveability, location and amenities — not for tenure. Rental yield is therefore a function of the lower entry price, which favours leasehold. Yield-focused investors typically prefer leasehold because the same rent against a lower entry price gives a higher gross yield.

Can I top up a 99-year lease privately?

An individual owner cannot reliably do so. SLA does process lease top-up applications, but they are typically in the context of an en-bloc / collective sale where the developer pays for the top-up as part of the redevelopment approval. A private owner asking SLA to extend their personal 99-year lease should not assume approval — nor should they assume the cost would be commercially reasonable.

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. Bala’s Table and CPF / financing rules are administered by the Singapore Land Authority, the Central Provident Fund Board, and the Monetary Authority of Singapore respectively, and may be revised from time to time. Always verify the current position with the Singapore Land Authority, the CPF Board, and a licensed conveyancing lawyer before signing any Option to Purchase.

Freehold or 99-year leasehold? This is one of the most consequential questions a Singapore buyer faces — and one of the most commonly misunderstood. Freehold stock in Singapore typically commands a 10–20% premium over an otherwise identical 99-year leasehold, but the price spread varies wildly by district, by remaining lease, and by the buyer’s hold horizon. This 2026 guide walks you through how lease decay actually works, how the price spread behaves across the ownership decades, and when the freehold premium is worth paying.

Quick Answer

Freehold grants ownership in perpetuity. 99-year leasehold grants ownership for a fixed term, after which the land reverts to the State.

Freehold stock in Singapore typically prices at a 10–20% premium over comparable 99-year leasehold stock — the spread widens sharply as remaining lease falls below 60 years.

Only roughly 3% of all residential stock in Singapore is freehold, concentrated in D9, D10, D11 and parts of D15.

For CPF usage and home-loan tenure, a leasehold property with less than 60 years remaining triggers pro-rated financing caps.

The right choice depends on your hold horizon, financing strategy and whether you are optimising for inheritance or capital appreciation.

What is freehold property in Singapore?

Freehold tenure — technically called estate in fee simple in Singapore land law — grants ownership rights in perpetuity. The owner holds the land indefinitely and passes title to heirs without any lease-decay consideration. Most freehold private residential stock in Singapore was originally granted in the 19th century through Crown grants, with title now consolidated into the Singapore Land Authority registered land system.

A small portion of private residential stock is held on tenures longer than 999 years — technically leasehold but functionally indistinguishable from freehold. Banks, conveyancing lawyers and CPF generally treat 999-year leasehold and freehold identically for financing and valuation purposes, and we do the same in this guide.

What is 99-year leasehold property?

Leasehold tenure grants ownership for a fixed term, after which the land and everything built on it reverts to the State. Most modern private condominium sites and virtually all HDB flats are 99-year leaseholds. A handful of developments are on shorter 60- or 99-year leasehold with renewal options, but these are uncommon in the private market.

The 99-year clock does not start on your purchase date. It starts on the date the State granted the lease to the original developer, which may have been 3 years ago or 30 years ago. Always check the remaining lease at the time of purchase, not the original tenure length. For HDB resale flats, this is published on the HDB Resale Flat Prices portal; for private condominiums, it appears on the title deed and in the caveat.

Key distinction

‘99-year’ is a description of the original tenure. ‘Remaining lease’ is what you actually buy. A 2014-developer-TOP 99-year condo sold in 2026 has 87 years remaining, not 99.

How much does freehold cost over leasehold in Singapore?

The data pattern is consistent: the freehold premium starts at around 10–15% at new launch, holds roughly flat for the first two decades of the lease, widens modestly in decades three and four, and widens sharply once remaining lease drops below 60 years. That non-linearity is not speculation — it is a mechanical consequence of how CPF usage and bank financing caps step down as remaining lease falls.

The Bala’s Table — how leasehold value decays

The Bala’s Table, first published by Professor P. Balasubramanian in the 1960s, remains the rule-of-thumb discount applied by the Singapore Land Authority when assessing lease top-up premiums. It approximates how leasehold value falls as remaining lease decreases. The table is not used for open-market pricing today — banks and valuers have largely replaced it with transaction-based regression — but it still frames the direction and rough magnitude of decay.

Two things to notice. First, the curve is gently sloped for the first 25 years of decay — a 99-year lease with 75 years remaining is still worth 90% of freehold. Second, the curve steepens sharply after the 60-year remaining-lease mark. That steepening is why CPF and banks step down their financing caps precisely there.

CPF and financing caps tied to remaining lease

CPF Ordinary Account funds and bank home loans can be used on leasehold property, but both taper once the remaining lease falls below a threshold. The 2026 framework is summarised below.

The pro-rated formula for CPF usage on a leasehold with remaining lease below 60 years is roughly: CPF usage cap = Valuation Limit × (remaining lease at end of ownership) / (minimum 20 years). This mechanic ties your exit horizon to your entry, and is one of the main reasons resale HDB flats with remaining lease in the 40–60 year band have seen price pressure over the last three years.

What this means for HDB buyers

If you buy a 50-year-old resale HDB (49 years remaining) at age 40 and expect to hold 25 years, you will still meet the 60-year threshold at entry. But if you buy at age 55 and expect to hold to age 85, you are in the 30–59 year remaining-lease band at entry — CPF pro-rated usage applies.

Worked example — the 30-year hold

Consider two identical units — same floor, same stack, same facing — in the D15 East Coast pocket. Unit A is freehold priced at S$2,800 psf; Unit B is 99-year leasehold priced at S$2,450 psf. Both are 1,076 sqft three-bedroom.

Purchase economics — 2026 launch

Unit A (freehold): 1,076 sqft × S$2,800 psf = S$3,012,800

Unit B (99-year): 1,076 sqft × S$2,450 psf = S$2,635,200

Absolute spread: S$377,600 (+14.3%)

BSD on A: S$ 128,064

BSD on B: S$ 108,182

BSD spread: S$ 19,882

Total upfront spread: S$397,482

Now fast-forward 30 years. Unit A is still freehold. Unit B has 69 years remaining — Bala’s Table places that at roughly 87% of freehold. If market values for comparable freehold have grown at 3% compound annually, freehold Unit A is worth roughly S$7.3 million. Leasehold Unit B, on the same curve, adjusted for the 87% remaining-lease coefficient, is worth roughly S$6.35 million. The spread at sale is S$950,000 — materially wider than the S$397,000 spread at purchase.

Exit economics — 30 years later (illustrative, 3% CAGR)

Unit A freehold value: ~S$7,305,000

Unit B leasehold value: ~S$6,354,000 (87% of freehold at 69 yrs remaining)

Absolute exit spread: ~S$950,000 (+15.0%)

Spread growth vs entry: S$950K − S$397K = S$553K

The take-away: for a 30-year-plus hold, the freehold premium you pay at entry is typically more than recovered through compounding plus the widening Bala’s Table spread. For a 5-to-10-year hold horizon, the lease-decay math barely moves, and the freehold premium behaves like a pure capital outlay.

Worked example — the 10-year flip

Now take the opposite end. Same two units, sold after 10 years — a typical trade-up horizon.

Exit economics — 10 years later (3% CAGR)

Unit A freehold value: ~S$4,050,000

Unit B leasehold value: ~S$3,472,000 (93% of freehold at 89 yrs remaining)

Absolute exit spread: ~S$578,000 (+16.6%)

Spread growth vs entry: S$578K − S$397K = S$181K

Over a 10-year hold, the widening spread contributes roughly S$181,000 of additional capital to the freehold holder — a modest outperformance but far less dramatic than the 30-year case. For shorter horizons, the leasehold route usually wins on a pure return-on-capital basis, because the upfront capital commitment is lower and the lease-decay spread has not yet materialised.

When freehold is worth the premium

Five situations where paying the freehold premium is typically justifiable:

One, you plan a 25-year-plus hold or intend to leave the property to the next generation. Inheritance planning works cleanly on freehold title and becomes messy on a leasehold property with 40 years remaining.

Two, you are in a prime district pocket where freehold is structurally scarce. In D11 Bukit Timah, D9 River Valley and D10 Holland-Bukit Timah, freehold parcels effectively cannot be reassembled; scarcity protects the freehold premium.

Three, you are buying a landed property. Landed freehold and landed 99-year leasehold trade at a wider spread than non-landed because the scarcity effect is stronger and inheritability carries more weight.

Four, you want optionality on future en-bloc redevelopment. Freehold sites are easier to redevelop at full-density economics; 99-year sites require a top-up premium to the State to refresh the lease, which taxes the redevelopment math.

Five, you are comparing freehold at a 12–14% premium. The 10–15% range is the sweet spot where long-hold math pencils out; spreads above 20% require a scenario-specific justification.

When leasehold is the smarter buy

Four situations where leasehold is typically the better economic choice:

One, you are a short-to-medium hold buyer (under 10 years). The lease-decay spread has not materialised yet; the freehold premium behaves like a pure cost.

Two, you are optimising for rental yield. 99-year stock typically yields 30–50 bps higher than comparable freehold stock, because tenants do not price in lease decay at all — they price on the monthly-rent market rate.

Three, you are a first-time buyer with a constrained deposit. The lower capital outlay on the 99-year option improves your free-cash-flow runway and leaves room to add a second property earlier in the hold cycle.

Four, you are buying in a district where the freehold premium is trading at 20%+. Over-paid freehold premiums tend to compress in the first half of the hold cycle.

Landed freehold vs non-landed freehold — a crucial distinction

The freehold premium behaves very differently in the landed market. Landed freehold properties in District 10 typically trade at 30–40% premium to comparable landed 99-year stock — more than double the non-landed spread. Three factors drive the widening. First, landed freehold land is a finite resource in a functionally-finished supply pipeline. Second, the redevelopment case on landed freehold is cleaner — a single-lot freehold landed plot can be rebuilt without lease top-up negotiations. Third, inheritance preferences in the landed buyer cohort skew strongly toward freehold.

The ‘999-year’ question

A small population of developments are held on 999-year leases. Functionally, 999-year is indistinguishable from freehold for any buyer under 70 years old. The original grants are 19th-century Crown leases, most now registered under the SLA title system. Banks, conveyancers, CPF and valuers treat 999-year and freehold identically for all practical purposes. If you see a 999-year property marketed at a discount to comparable freehold, it is usually mis-priced.

Summary — how to decide

Frequently asked questions

1. Is freehold always worth more than leasehold?

On an absolute-price basis, yes — at any given moment, comparable freehold stock prices higher than leasehold. On a total-return basis, whether the premium is worth paying depends on your hold horizon. For a 25-year-plus hold, freehold typically outperforms; for a 5-to-10-year hold, 99-year leasehold often wins on a return-on-capital basis.

2. What happens to a 99-year leasehold property when the lease runs out?

The land, and any structure on it, reverts to the State of Singapore. The owner at the moment of expiry receives no compensation. This is the default legal outcome under Singapore leasehold law. In practice, collective-sale en-bloc transactions almost always occur long before lease expiry for well-located sites.

3. Can I top up the lease on a 99-year leasehold property?

For private leasehold, lease top-ups to restore the tenure to 99 years require an application to the Singapore Land Authority and the payment of a lease top-up premium, which is assessed using the Bala’s Table methodology. Approval is not guaranteed. For HDB flats, the Voluntary Early Redevelopment Scheme (VERS) and the Selective En bloc Redevelopment Scheme (SERS) are the two mechanisms HDB uses to refresh ageing leasehold stock, but both are government-led — a flat owner cannot unilaterally top up the lease.

4. Does remaining lease affect my home loan?

Yes. Banks cap home-loan tenure such that the loan must be fully repaid by the borrower’s 75th birthday under TDSR rules, and no later than the borrower’s 95th birthday on the remaining lease. CPF usage is pro-rated below a 60-year remaining lease. Both caps become binding together on older leasehold stock.

5. Are freehold properties in Singapore rare?

Yes. Freehold stock accounts for roughly 3% of all residential property in Singapore, concentrated in D9, D10, D11 and the older pockets of D15, D20 and D21. The scarcity is structural: Singapore stopped granting new freehold titles in the 1960s, so freehold supply grows only through subdivision — slowly.

6. Can foreigners buy freehold landed property?

Foreigners cannot buy landed freehold property in Singapore without specific approval from the Land Dealings (Approval) Unit. Sentosa Cove is the main exception — the island allows foreign ownership of landed property subject to MAS disclosure rules. Non-landed freehold (condominium apartments) is unrestricted for foreign buyers, subject to ABSD.

7. Is a 999-year leasehold the same as freehold?

For practical financing, valuation, CPF and tax purposes, yes. A 999-year lease effectively outlasts any human lifetime and multiple generations, and banks treat 999-year and freehold identically. Legally, 999-year is still a lease, but the difference is operationally immaterial.

8. Which districts have the most freehold stock?

D9 (Orchard, River Valley), D10 (Holland, Tanglin, Bukit Timah), D11 (Newton, Novena), D15 (Katong, Marine Parade), D20 (Upper Thomson) and D21 (Clementi, Upper Bukit Timah) have the highest freehold density. D1, D2, D7 and D8 are almost entirely 99-year or shorter.

9. Does freehold guarantee a profit?

No. Freehold buys you duration, not direction. A freehold property can still fall in value if the market broadly corrects or the specific micro-market de-rates. What freehold protects against is time-based lease decay, not price risk.

10. Should I pay a 20% premium for freehold over leasehold?

In most micro-markets, 20% is at the high end of the historically-supported spread. Spreads above 20% are typically observed only in luxury D9/D10/D11 pockets where freehold is structurally scarce. For mid-tier outside-central-region stock, a 20%+ spread is a yellow flag that the freehold unit may be over-priced.

11. How do I find the remaining lease of a property?

For HDB, the remaining lease is published on the HDB Resale Flat Prices portal and on the Form A issued at purchase. For private property, it appears on the title deed and can be extracted from the caveat record on URA’s property information portal. For condominiums, the developer’s factsheet states the TOP date, from which the remaining lease at any future date can be calculated.

12. Does HDB offer freehold flats?

No. All HDB flats — BTO, Sale-of-Balance, resale, DBSS, Premium, Prime Location Housing — are 99-year leasehold from the date of the original lease grant to HDB.

Disclaimer. This article is for general information only and does not constitute legal, financial or tax advice. Figures referenced reflect the position as at 23 April 2026 and are subject to change without notice. Always verify the latest rates and policies with the official authority — IRAS, HDB, URA, CPF or MAS — before making any property decision. Consult a qualified lawyer, mortgage broker or accountant for advice specific to your circumstances.