Upgrading from HDB to Private Property Singapore 2026: Step-by-Step Guide, Costs and Timing

Upgrading from an HDB flat to a private condominium is the most common property-wealth move in Singapore — and the most misunderstood. This guide walks you through every stage, every cost and every timing trap.

Quick Answer

- You must fulfil the Minimum Occupation Period (MOP) — 5 years for standard HDB flats, 10 years for Plus or Prime classification flats — before selling and upgrading. The 5-year clock starts from the date of key collection, not the BTO application.

- Upgrading while retaining the HDB flat triggers 20% ABSD on the private property (SC buying second residential property). Selling the HDB first and then buying private means you pay 0% ABSD as a first-time private buyer — but you face a timing gap.

- CPF Ordinary Account funds used for the HDB must be refunded with accrued interest (2.5% p.a.) upon sale. This is not a penalty — it is your own money going back to your CPF — but it reduces the cash proceeds from the HDB sale.

- Most upgraders secure an in-principle approval (IPA) from a bank before listing their HDB, to confirm their private-property borrowing capacity.

- The typical timeline from HDB listing to moving into the private property is 9–12 months. A decoupling strategy can shorten this but adds complexity and legal costs.

- For a S$1.35M OCR condo purchase (SC selling HDB and buying private): expect total cash outflow of S$340,000–S$380,000 (25% downpayment + BSD ~S$38,600 + legal fees) if CPF is used for the remainder of the downpayment.

Why Upgrading Is Such a Defining Decision in Singapore

For most Singapore families, the HDB flat is the largest asset they own — and the only asset from which they can extract equity to fund the next step in their property journey. Unlike in most developed economies, Singapore’s public housing system is tightly regulated: the MOP, resale levy rules, and eligibility restrictions mean that the upgrade from HDB to private property is not simply a matter of listing one property and buying another. It is a sequenced, rules-bound process that requires careful planning of CPF, ABSD, TDSR and timing.

In 2026, this upgrade pathway has become more complex following the 8 May 2026 measures by the Ministry of National Development, which doubled the MOP for new Executive Condominiums to 10 years. While this does not directly affect standard HDB upgraders, it has recalibrated expectations about holding periods across the market.

Step 1 — Confirm You Have Cleared the MOP

The Minimum Occupation Period is enforced by HDB under the Housing and Development Act (Cap. 129). For BTO, DBSS and most resale flats purchased under HDB schemes, the MOP is 5 years from the date of keys collection. For Plus classification flats (transitional zone — introduced under the October 2024 BTO reclassification) and Prime classification flats (central/mature areas under the PLH model), the MOP is 10 years.

During the MOP, you may not sell, sublet the entire flat, or purchase another private residential property. Breach of MOP is a serious offence — HDB may require compulsory acquisition at below-market rates. You can verify your MOP completion date via the HDB Portal (my.hdb.gov.sg).

Step 2 — The ABSD Decision: Sell First or Buy First?

This is the central financial decision of any HDB upgrade. Two paths exist:

| Strategy | ABSD | Risk | Best for |

|---|---|---|---|

| Sell HDB first, then buy private | 0% (first private property) | Timing gap — may need bridging loan or temporary rental | Cost-conscious upgraders; those with flexible timeline |

| Buy private first, then sell HDB | 20% (SC 2nd residential) | 20% ABSD payable immediately; can claim remission if HDB sold within 6 months of private completion | Those who need continuity; if new launch with long wait |

| Decoupling (married couple) | One spouse buys private as first-timer: 0% ABSD | Stamp duty + legal costs on decoupling; ABSD remission rules complex | Married couples; wealth-splitting strategy |

ABSD remission for the second-purchase strategy: If you purchase the private property first, you pay 20% ABSD upfront. However, if you sell your HDB flat within 6 months of the private property’s completion (for completed property) or within 6 months of the private property’s Temporary Occupation Permit (TOP) (for new launch under construction), you may apply to IRAS for a partial ABSD remission. The remission is not automatic — it requires a formal application and supporting documents confirming the HDB was sold within the stipulated period.

Step 3 — CPF Accrued Interest: The Hidden Cost of Upgrading

Every dollar withdrawn from your CPF Ordinary Account for the HDB purchase — whether for the downpayment or monthly mortgage instalments — accrues interest at 2.5% per annum from the date of withdrawal. When you sell the HDB flat, this full amount plus accrued interest must be refunded to your CPF OA before any cash proceeds are released to you.

For a household that bought a 4-room BTO for S$350,000 in 2017, used S$90,000 CPF for the downpayment and S$30,000 in CPF for monthly instalments over 9 years: the accrued interest can easily reach S$28,000–S$35,000. This sum reduces the net cash-in-hand from the HDB sale, though it is returned to CPF and can be re-deployed for the private property purchase.

Step 4 — Finance Check: TDSR, LTV and Bank IPA

Before listing your HDB, obtain an In-Principle Approval (IPA) from a bank. This confirms your maximum loan quantum for the private property. Key constraints:

- LTV (Loan-to-Value): 75% of the lower of purchase price or valuation for a first private property (no outstanding housing loan). If you still have an HDB concessionary loan at time of private purchase — i.e., you are buying private before selling HDB — LTV drops to 45%.

- TDSR (Total Debt Servicing Ratio): Monthly mortgage obligations must not exceed 55% of gross monthly income, stress-tested at 4.0% per annum (or the contracted rate + 2.0%, whichever is higher). At a 30-year loan tenure, a combined household income of S$12,000/month supports a maximum loan of approximately S$1.6M at a 3.8% actual rate — but the stress test at 4.0% (or effective 5.8%+) may reduce this.

- MSR (Mortgage Servicing Ratio): The 30% MSR applies only to HDB loans and EC purchases; it does NOT apply to private condominium purchases. However, banks apply internal stress tests that are effectively similar.

Step 5 — The HDB Resale Levy: When It Applies

The HDB Resale Levy is payable if you have previously enjoyed a housing subsidy from HDB — typically from purchasing a new BTO or SERS flat at subsidised rates — and then purchase another subsidised HDB flat (BTO or DBSS) or an EC at the subsidised price. The levy ranges from S$15,000 (2-room flat) to S$50,000 (5-room flat and above).

Importantly, the resale levy is NOT payable if you are upgrading directly to a private condominium. It only applies when you move from a subsidised HDB flat to another subsidised HDB or EC. For the typical HDB-to-private upgrade journey, the resale levy is irrelevant — but it becomes relevant if, later in life, you sell the private condo and wish to purchase a subsidised flat again.

Worked Example: The Lim Family’s Upgrade

Mr and Mrs Lim — both Singapore Citizens, combined gross income S$13,500/month — own a 4-room BTO in Sengkang purchased in 2019 at S$420,000. They collected keys in December 2019 and have cleared their 5-year MOP as of December 2024. They aim to upgrade to a 3BR OCR condo in Tampines priced at S$1,350,000, using the sell-first strategy.

HDB sale side:

- Estimated resale value (2026): S$550,000

- CPF principal withdrawn (downpayment + 5 years of instalments): S$130,000

- CPF accrued interest (2.5% p.a. × ~6 years average): ~S$24,500

- Total CPF refund required: S$154,500 → returns to OA

- Outstanding HDB loan (HDB concessionary at 2.6%, 25-year, ~5 years elapsed): ~S$268,000

- Agent fees + legal: ~S$14,000

- Net cash from sale: S$550,000 − S$154,500 − S$268,000 − S$14,000 = S$113,500 cash + S$154,500 to CPF OA

Private purchase side (S$1.35M OCR condo, first private property — 0% ABSD):

- BSD: S$38,600

- Downpayment (25%): S$337,500 — covered by CPF OA S$154,500 + additional CPF savings S$80,000 + cash S$103,000

- Bank loan (75% LTV): S$1,012,500

- Legal + stamp duties: ~S$5,000

- Monthly instalment at 3.8% for 25 years: ~S$5,260/month (TDSR at S$13,500: ratio = 39% — within 55% limit)

The Lims transition from a paid-down HDB flat (equity ~S$282,000 post-CPF-refund) to a S$1.35M private condo with a S$1.01M loan. Their monthly outgoing rises from ~S$1,400 (HDB loan) to ~S$5,260 (bank loan) — a significant lifestyle adjustment that underpins why financial planning before committing to the OTP is essential.

Decoupling: A Strategy for Married Couples

Decoupling refers to the transfer of one spouse’s share of the HDB flat to the other, so that the first spouse becomes a private-property first-timer with no existing residential property — thereby buying the condo at 0% ABSD. This is a legitimate strategy permitted under Singapore law but involves several costs: Buyer’s Stamp Duty on the share transfer (at prevailing BSD rates), legal fees (~S$3,000–S$5,000), and CPF accrued interest implications if the receiving spouse uses CPF to buy out the transferring spouse’s equity.

Post-8 May 2026, decoupling strategies for Executive Condominiums are more complex given the extended 10-year MOP, but for standard HDB flats the fundamentals are unchanged. Note that a decoupling exercise does not reset the MOP clock — both spouses must still fulfil the residual MOP on the existing flat before selling it.

What Might Come Next

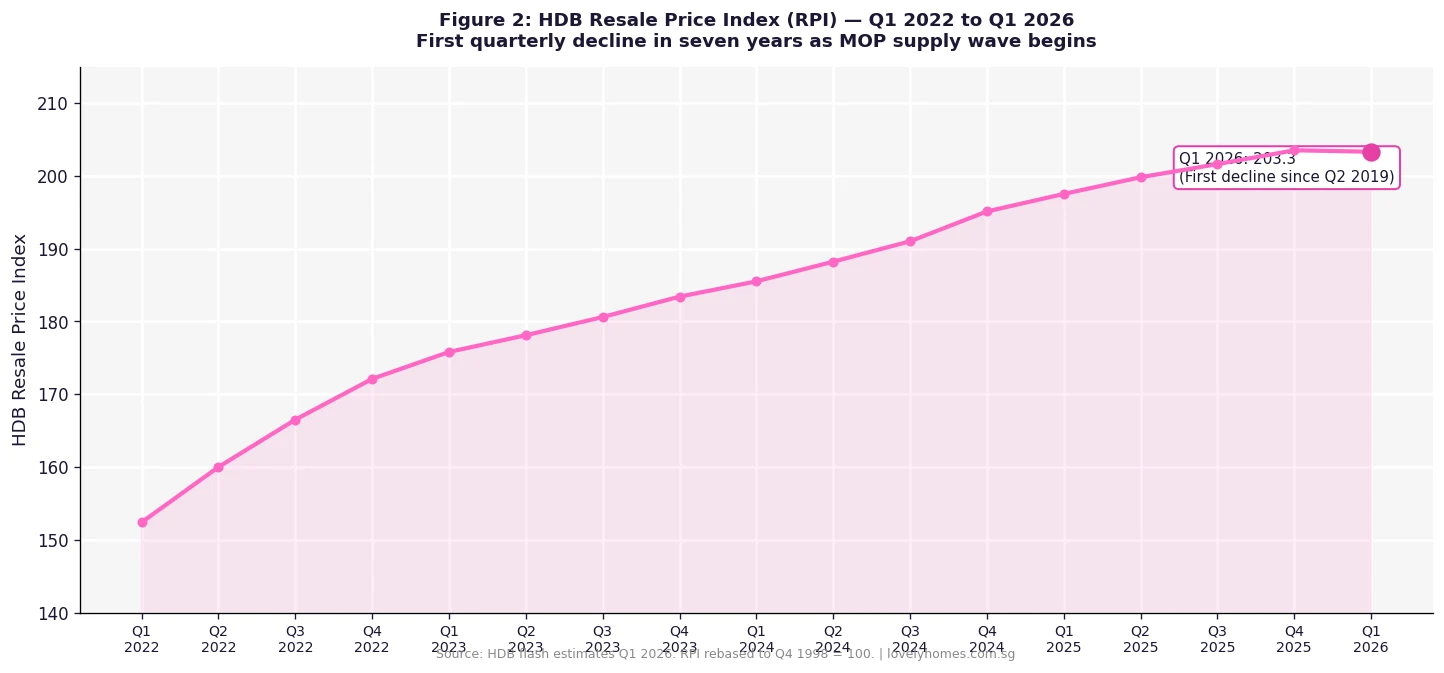

The upgrader market in Singapore is highly sensitive to HDB resale prices, private condo prices and the ABSD quantum. With the HDB Resale Price Index posting its first quarterly decline since Q2 2019 in Q1 2026, upgraders who have waited now face a window where HDB proceeds are softening — but private prices in the OCR have remained resilient (+1.3% in Q1 2026 per URA flash estimates). If HDB prices soften further while OCR condo prices hold, the upgrade gap widens, potentially tempering upgrader demand. Conversely, a release of the ABSD remission ceiling — which has been discussed informally in policy circles but not announced — could re-energise the buy-first strategy.

Frequently Asked Questions

Can I buy a private property before my HDB MOP is up?

No. HDB rules explicitly prohibit the purchase of any private residential property — whether in Singapore or overseas — during the MOP. This restriction applies to both spouses if the HDB flat is held jointly. Violation is treated as a breach of HDB terms and can result in compulsory acquisition of the HDB flat. The HDB actively cross-checks URA caveats and IRAS stamp duty records to detect such breaches. Once MOP is cleared (confirmed via the HDB Portal), you are free to purchase private property — though ABSD implications depend on whether you retain or sell the HDB.

How do I compute the CPF accrued interest I need to refund?

The CPF Board applies 2.5% per annum compounded on each CPF OA withdrawal from the date of that withdrawal. The total CPF refund = sum of all withdrawals × compounded interest from withdrawal date to sale completion date. You can get an exact figure by logging into the CPF website (cpf.gov.sg) under “My Home” → “Property Withdrawal Details”. The computation is provided automatically based on your withdrawal records. Accrued interest on CPF used for private property follows a similar principle but uses the OA interest rate applicable to each year (2.5% p.a. currently).

If I sell HDB first and the market rises before I buy private, am I stuck?

Yes, this is the primary risk of the sell-first strategy: the private property market may move against you between HDB sale completion and private purchase completion. Most upgraders mitigate this by either (a) securing the OTP on the private property before accepting the HDB offer, relying on the ~10-week HDB completion timeline; or (b) renting temporarily (typically 3–6 months) while searching for the right private unit. Some banks offer a bridging loan to cover the gap between HDB sale and private purchase completion, though interest rates on bridging loans (typically prime + 1–2%) can be costly if the gap extends beyond 3–6 months.

What happens to my HDB loan when I upgrade?

The outstanding HDB concessionary loan balance must be fully repaid from the HDB sale proceeds. HDB does not allow you to maintain an HDB loan on a flat you no longer occupy. Once the loan is discharged at completion, the CPF charge and bank caveat (if any) on the HDB flat are also withdrawn. If you had taken a bank loan (not HDB loan) for the flat, the bank will be repaid from sale proceeds in the same way. Note that having previously taken an HDB concessionary loan means you will not be eligible for a future HDB concessionary loan — you will need a bank loan for any future HDB purchase.

Can I use CPF savings to pay for the private property?

Yes — CPF OA savings can be used for the downpayment and monthly mortgage instalments on a private residential property purchased with a bank loan (not HDB loan). The funds returned to your CPF OA from the HDB sale (principal + accrued interest) are immediately available for the private purchase. There is a Valuation Limit (VL) — you may withdraw up to the lower of purchase price or valuation — and a Withdrawal Limit (WL) at 120% of the VL for properties with remaining lease below certain thresholds. For a new private condo with a 99-year lease, the VL and WL are unlikely to be the binding constraint for most upgraders.

What is the typical timeline for the HDB-to-private upgrade?

For a sell-first strategy: HDB Option-to-Purchase exercise → HDB resale registration with HDB → 8-week HDB flat completion → gap period (1–12 weeks) → private OTP exercise → 10–12 weeks to private completion (for resale condo). Total: approximately 5–9 months. For a new launch with progressive payment scheme, the private purchase is effectively a commitment today for a TOP 2–4 years away, during which time you can sell the HDB (and potentially claim ABSD remission). This is the most common “buy-first” timing for upgraders targeting new launches.

Is there a grants programme to help first-time private buyers?

No — CPF Housing Grants (EHG, CPF Housing Grant, Proximity Grant) apply only to HDB flat purchases, not private properties. Once you upgrade to a private condo, you lose access to these grant programmes for that purchase. However, the CPF OA funds returned from your HDB sale (including accrued interest) are your own funds and can be redeployed freely for the private purchase within CPF rules. Some banks offer preferential mortgage rates or fee waivers for existing mortgage customers upgrading — it is worth requesting a private banking review if your combined assets are above S$1M.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Minimum Occupation Period (MOP) Singapore 2026

- HDB Resale Procedure Singapore 2026

- TDSR Singapore 2026: How the 55% Cap Decides Your Home Loan

- Buyer’s Stamp Duty (BSD) Singapore 2026

- HDB Grants Singapore 2026: EHG, CPF Housing Grant and More

- Rental Yield Singapore 2026: Gross, Net and Location-Adjusted Yields

- Decoupling for Married Couples Singapore 2026

Disclaimer: This article is for general information purposes only and does not constitute legal, financial or tax advice. Stamp duty rates, CPF rules, HDB eligibility criteria and MAS lending regulations are subject to change — always verify with official sources including the HDB Portal (hdb.gov.sg), CPF Board (cpf.gov.sg), IRAS (iras.gov.sg), MAS (mas.gov.sg) and the URA (ura.gov.sg). Consult a licensed conveyancing solicitor, a MAS-regulated financial adviser and a CPF-accredited mortgage specialist before making any property decision.