Singapore Property Insurance Guide 2026: Fire, MRTA, HPS & Contents Cover Decoded

Property insurance in Singapore is one of those topics most homeowners discover only when something goes wrong — a kitchen fire, a burst pipe, a borrower’s sudden death. By then it is too late to negotiate a better policy. This 2026 guide walks you through every layer of cover a Singapore property owner can buy: HDB Fire Insurance, the Home Protection Scheme (HPS), private Mortgage Reducing Term Assurance (MRTA), Home Contents Insurance, and the building cover that sits inside your condo’s management corporation budget. Premiums, what each policy actually pays for, common gaps, and the cheapest legitimate way to cover yourself in 2026 — it is all here.

Quick Answer — what every Singapore homeowner should hold

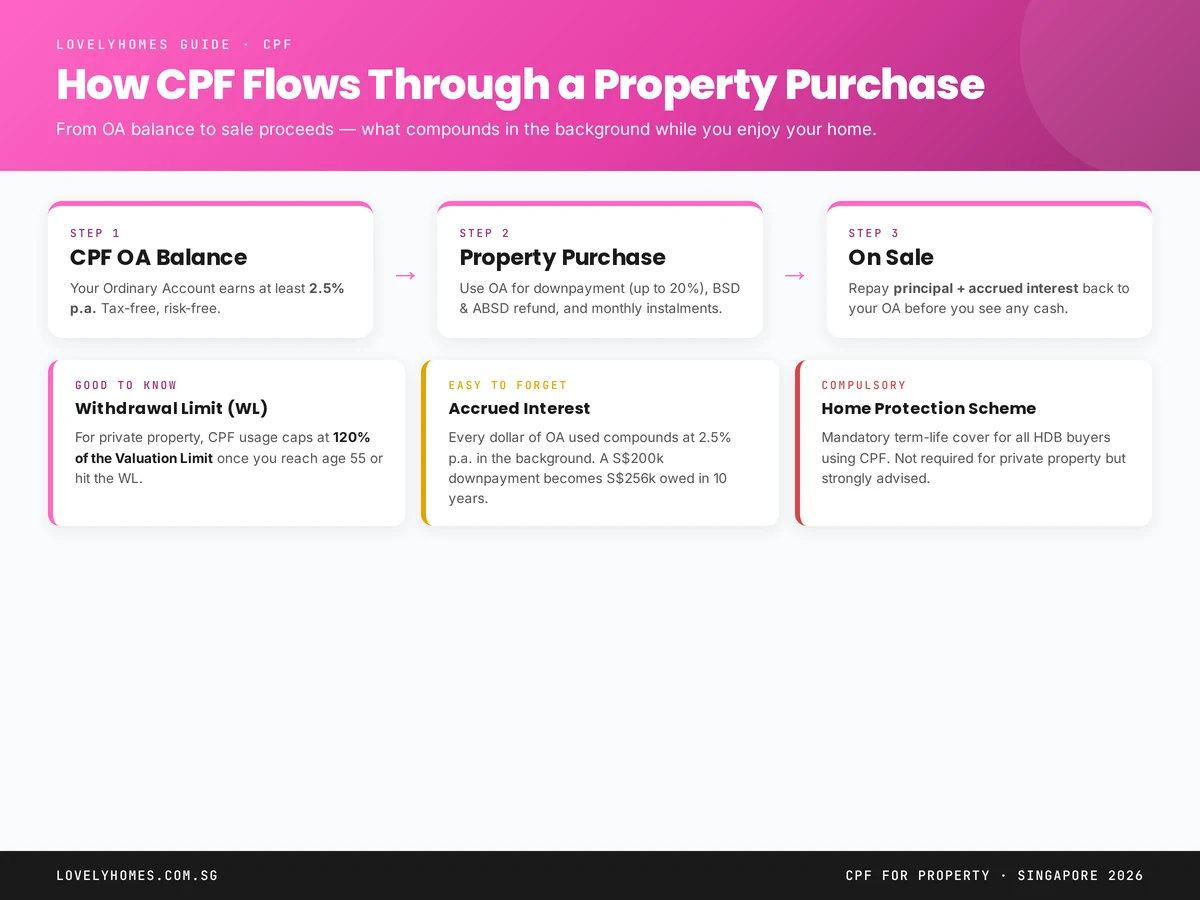

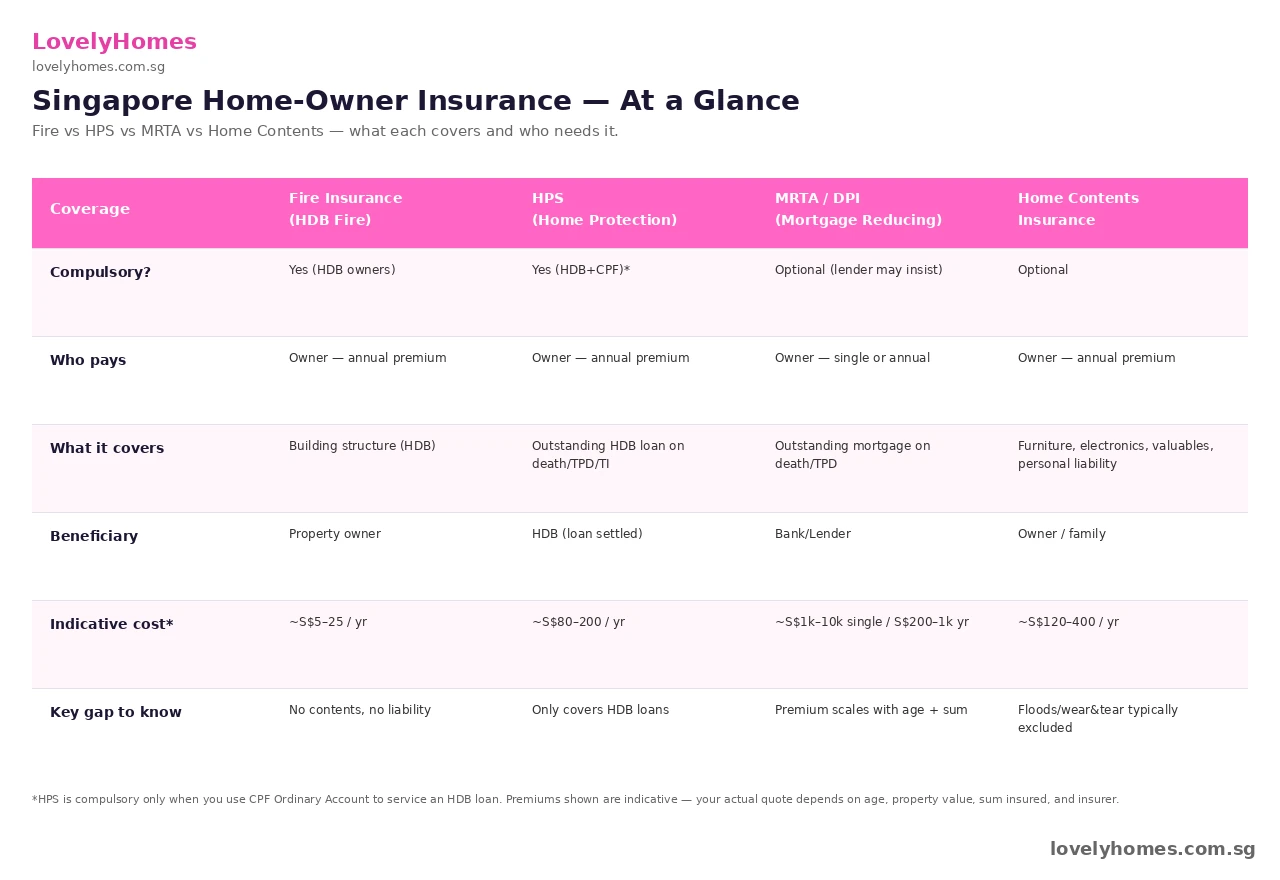

- HDB owners: Fire Insurance is compulsory. If you use CPF Ordinary Account to service your HDB loan, the Home Protection Scheme (HPS) is also auto-enrolled.

- Condo owners: Building cover is paid through your monthly maintenance fees (MCST policy). You still need Home Contents and a private MRTA if you have a bank loan.

- MRTA protects your family from a forced sale by repaying the outstanding mortgage on death, terminal illness, or total & permanent disability.

- Home Contents covers furniture, electronics, jewellery, and personal liability — items the building policy excludes.

- Indicative annual outlay for a S$1.5M condo with a S$1.05M loan: ~S$1,000–1,200 across MRTA + Contents + topped-up Fire cover.

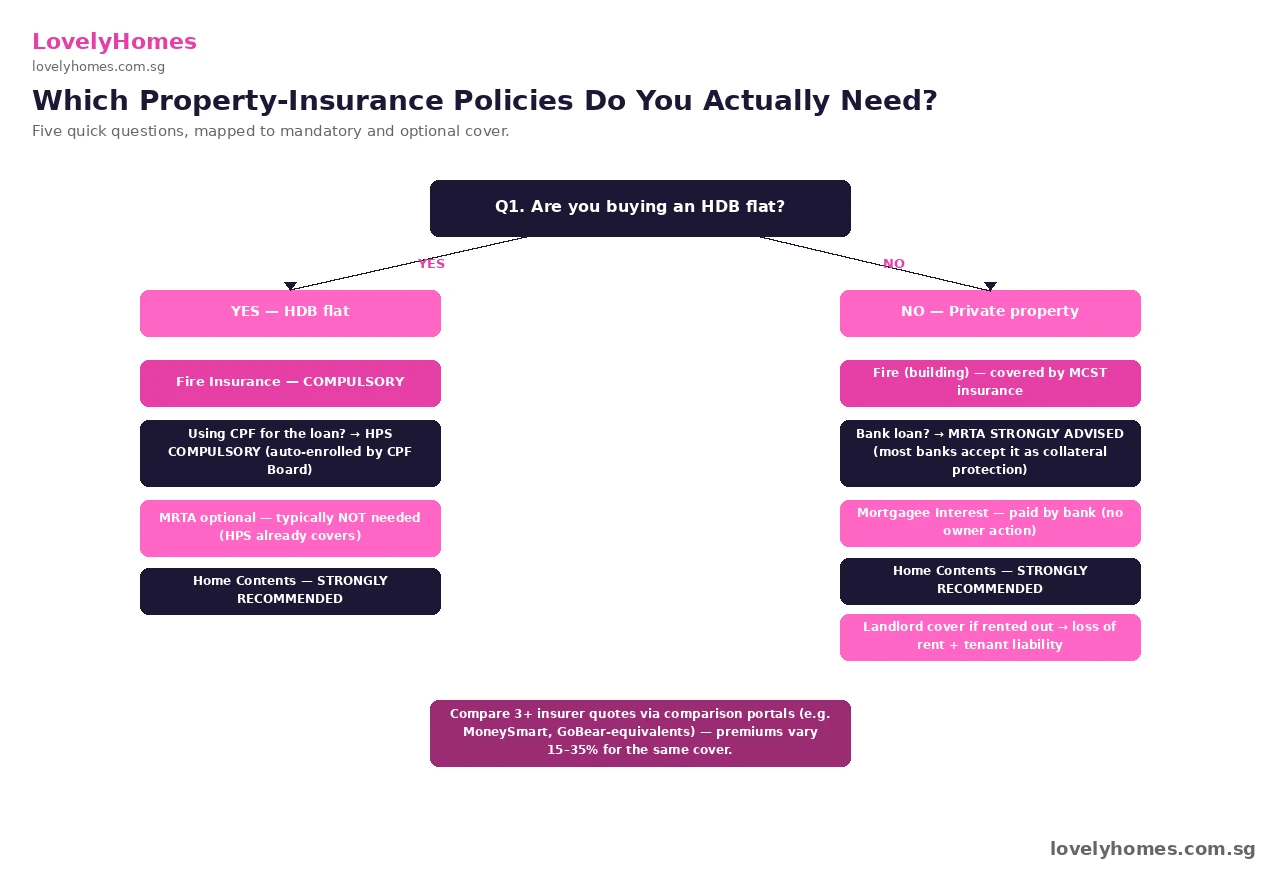

- Premiums vary 15–35% between insurers for identical cover — always compare 3+ quotes.

What “Property Insurance” Actually Means in Singapore

The phrase “property insurance” covers four distinct policies in the Singapore context, and the rules around each one differ by housing type. Understanding which is mandatory, which your bank insists on, and which you can safely skip is the difference between an over-insured budget and a real protection plan.

The four pillars are:

- Fire Insurance — covers the building structure (walls, floors, ceilings, fixed fittings). Compulsory for HDB flat owners; built into the maintenance fees of every condominium via the Management Corporation Strata Title (MCST).

- Home Protection Scheme (HPS) — a CPF-administered group term assurance that pays off your outstanding HDB loan if you die, become totally and permanently disabled, or are diagnosed with a terminal illness. Compulsory for HDB owners using CPF Ordinary Account funds to service the loan.

- Mortgage Reducing Term Assurance (MRTA) — the private-sector equivalent of HPS, sold by life insurers. Most banks strongly recommend (and some require) MRTA for private property loans.

- Home Contents Insurance — covers everything inside the four walls: furniture, white goods, electronics, jewellery, watches, plus personal liability if a guest is injured at your home.

Fire Insurance — Compulsory for HDB, Bundled for Condos

Every HDB flat owner is required by law to maintain a Fire Insurance policy on the structure of the flat. The Housing & Development Board has appointed a single insurer (currently FWD Singapore) to underwrite a basic policy with a uniform 5-year premium of around S$5.30 to S$25.40 depending on flat type. The cover sum is set to rebuild the structure, not the contents — if you assume your renovation, kitchen cabinets, or solid-timber flooring is included, you are mistaken. Most HDB owners then top up with a Home Contents policy from a private insurer.

For private condominium owners, fire insurance for the building is paid for collectively by the MCST and recovered through monthly management fees. The MCST policy is typically a Comprehensive HOOIS (Home Owner’s Outline Insurance Schedule) covering the structure, common property, and original developer fittings. What it excludes: any owner-installed renovation upgrades, fitted furniture beyond the original handover spec, and contents. If your condo unit has been substantially renovated, you should buy a top-up renovation cover — insurers will assess your defects-handover-to-current condition and quote accordingly.

For landed property owners, building fire insurance is bought directly from a general insurer. Sums insured are based on the rebuilding cost (excluding land value) rather than market price, which is why a S$10M Good Class Bungalow on a 15,000 sq ft plot may insure for only S$2.5M of structure.

Home Protection Scheme (HPS) — HDB’s Built-In Mortgage Cover

The Home Protection Scheme is a mortgage-reducing term assurance plan administered by the CPF Board for HDB flat buyers. It is compulsory for any flat owner using their CPF Ordinary Account to service their HDB loan, and is auto-enrolled at the point you commit to using CPF for the monthly instalment. The premium is paid annually from your CPF OA — typically S$80 to S$200 per year for a healthy 30-something with an outstanding loan in the S$300,000–500,000 range.

HPS pays off the outstanding HDB loan in three scenarios: death, total and permanent disability (TPD), or terminal illness. The flat then passes to the surviving co-owners or beneficiaries free of mortgage debt. There is no payout to the family beyond clearing the loan — if you want a cash sum on top, HPS will not deliver it. For that you need a separate term-life policy.

You may apply to opt out of HPS only if you already hold an equivalent or better term-assurance policy — a deliberate carve-out designed to prevent over-insurance. The CPF Board reviews your alternative policy against minimum sum-assured and tenure benchmarks before granting the exemption.

Mortgage Reducing Term Assurance (MRTA) — The Private-Sector Equivalent

MRTA, also marketed as Decreasing Term Assurance (DTA) or Mortgage Insurance, performs the same function as HPS but for buyers of private properties or those servicing their HDB loan entirely in cash. It is sold by every major life insurer in Singapore and underwritten as a single-premium or annual-premium policy whose sum assured tracks the falling balance of your mortgage as you pay down principal.

Premiums depend on age, gender, smoking status, sum assured, and tenure. As a rough guide, a 35-year-old non-smoker buying MRTA on a S$1,050,000 25-year loan will see single-premium quotes of S$15,000–22,000, equivalent to about S$600–900 per year if paid annually. Many buyers fund the single premium from their CPF OA at the point of property completion — CPF rules permit this provided the policy is assigned to the property.

If you are buying a condo on a bank loan and your mortgage is your largest financial liability, MRTA is the single most cost-effective protection product available. A S$700/year MRTA premium pays off in any month you are unable to work, where the alternative (a forced sale into a falling market) destroys decades of equity.

Home Contents Insurance — The Most Underbought Policy

Home Contents Insurance is the most commonly skipped policy and, statistically, the one that pays out most often. It covers the loose property inside the four walls of your home: furniture, white goods, televisions, computers, kitchen appliances, jewellery, watches, art, musical instruments, and (within sub-limits) cash. It also covers personal liability — the legal cost if your child accidentally injures a visitor on your premises, or if water damage from your unit affects the unit below.

Premiums are remarkably affordable. A standard policy with S$30,000 contents cover and S$500,000 personal liability costs around S$120–220 per year at major insurers (NTUC Income, Etiqa, FWD, Tokio Marine, MSIG). Higher contents sums, jewellery riders, or all-risks cover for valuables sit at S$300–500 per year.

What is typically excluded: gradual wear and tear, mould, vermin damage, intentional damage by a household member, cosmetic damage, and items left in common corridors. Read the schedule carefully — the differences between insurers on what counts as “valuables” (above S$2,500 per article) and which valuables need declaration are material.

Which Policies Do You Actually Need?

The right insurance stack depends on whether you live in HDB or private property, how the property is financed, and whether you intend to rent it out. The flowchart below traces the decisions.

Summary — Indicative Annual Premiums by Property Profile

| Profile | Fire / Building | HPS / MRTA | Contents | Total / Year |

|---|---|---|---|---|

| 4-rm HDB owner-occupier (CPF loan) | ~S$5 (5-yr premium) | ~S$120 HPS | ~S$140 | ~S$265 |

| 5-rm HDB owner-occupier (cash loan) | ~S$25 (5-yr premium) | ~S$650 MRTA | ~S$160 | ~S$835 |

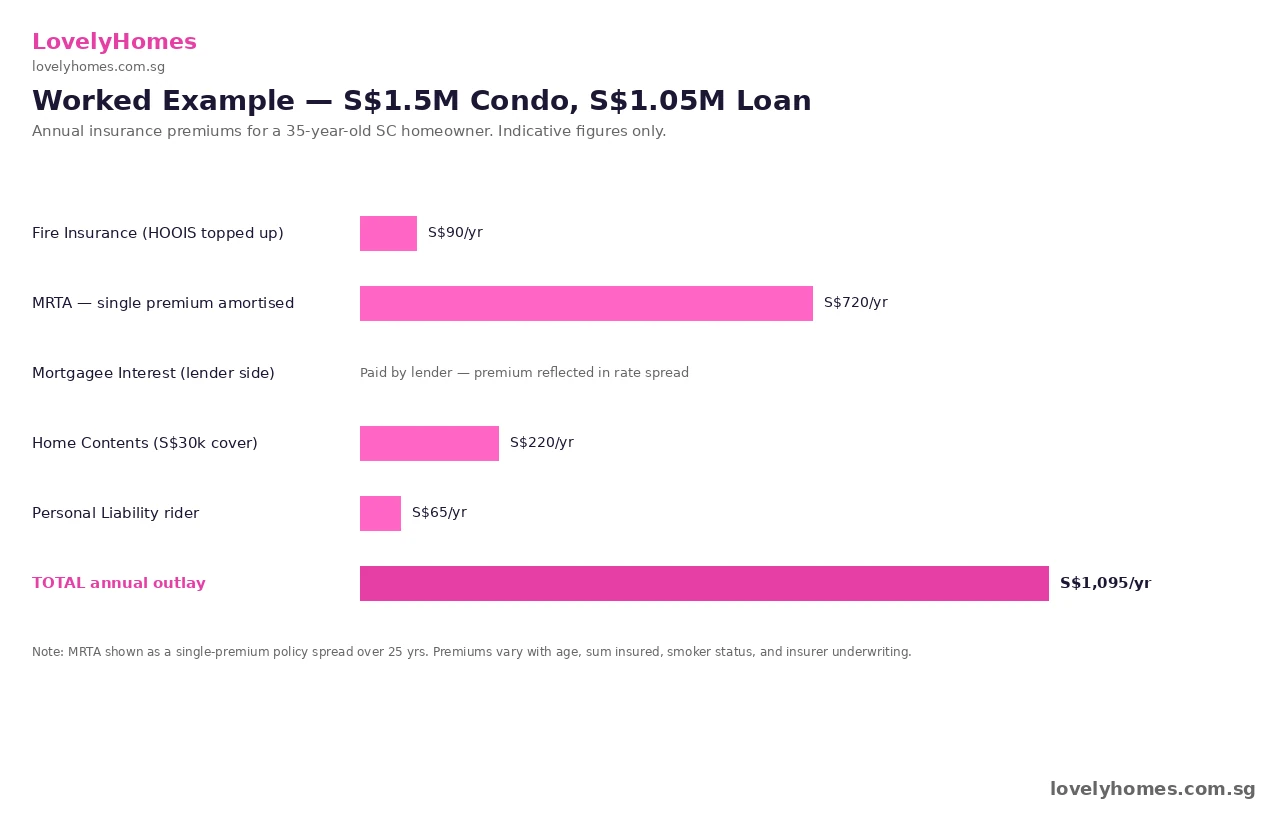

| S$1.5M condo owner-occupier (bank loan) | MCST top-up ~S$90 | ~S$720 MRTA | ~S$220 | ~S$1,030 |

| S$2.5M condo investor (rented out) | MCST top-up ~S$140 | ~S$1,200 MRTA | Landlord cover ~S$420 | ~S$1,760 |

| Landed property (S$5M, owner-occupier) | ~S$650 fire | ~S$2,400 MRTA | ~S$520 | ~S$3,570 |

Worked Example — The Tan Family, S$1.5M Condo Buyer

Mr Tan (35, SC, non-smoker) and his wife (33, SC, non-smoker) have just collected keys to a S$1.5M condo in District 19. Their bank loan is S$1,050,000 over 25 years at a SORA-pegged rate currently at about 3.7%. They have no children but plan to start a family within two years. Here is how their insurance stack lines up.

- Fire / Building cover: Provided through the MCST policy — included in their monthly S$420 maintenance fee. They top up with a S$50,000 renovation cover at S$90/year, since their renovation upgrades (kitchen cabinetry, full marble flooring) are not part of the original developer handover.

- MRTA: Mr Tan is the sole borrower for tax-deduction reasons. They take a single-premium MRTA of S$17,500 funded from his CPF OA — equivalent to about S$700/year over the 25-year tenure. Sum assured starts at S$1,050,000 and decreases linearly with the loan balance.

- Home Contents: S$50,000 contents sum + S$1M personal liability + jewellery rider for Mrs Tan’s heirloom pieces. Annual premium: S$285.

- Mortgagee Interest: The bank carries this internally — Mr Tan does not pay separately, but it is one reason the bank’s spread sits at +0.75% over SORA rather than +0.5%.

Total annual outlay: ~S$1,075, or about S$90 a month. Against a household income of S$15,000/month, the protection is rounding error — but it is the difference between Mrs Tan keeping the home if Mr Tan dies, and being forced into a distressed sale.

Insurance Riders Worth Considering

Beyond the four core pillars, riders address specific risk pockets that many homeowners discover only after a claim:

- Renovation cover — tops up the MCST policy to include your renovation upgrades. Premium scales with renovation spend; rule of thumb is 0.1–0.2% of renovation value per year.

- Domestic helper liability — covers the legal liability of accidents your foreign domestic helper causes inside or outside your home. ~S$50–120/year, often bundled with helper accident insurance.

- Loss of rent cover — for landlords. Pays a defined monthly rent if the property becomes uninhabitable due to an insured peril (e.g. fire). ~S$80–200/year on a Home Contents Landlord policy.

- All-risks worldwide for valuables — covers jewellery, watches, art whether at home or away. Stacks cleanly on top of Home Contents.

- Public-liability extension — raises personal liability cover from the standard S$500K up to S$2M, useful for landed property owners and high-rise condo owners on upper floors where falling object claims can be material.

Common Mistakes Singapore Owners Make

Because property insurance is dull and the worst-case scenarios feel remote, most owners default to the cheapest single-quote option and discover the gaps when a claim is denied. The five most common mistakes:

- Assuming HDB Fire Insurance covers contents — it does not. The FWD/HDB policy covers structure only.

- Letting MRTA lapse after refinancing — if you refinance to a different bank, you must re-assign your MRTA policy or switch to a fresh one. A surprising number of owners hold an MRTA policy that no longer points to their current lender.

- Not declaring jewellery and valuables — high-value items above S$2,500 each must be specified separately. Otherwise, the Home Contents policy caps any single-item claim at the unspecified-items sub-limit (typically S$5,000–10,000).

- Renovating extensively without telling the insurer — if a fire or flood damages your premium kitchen, the MCST policy will only restore the original developer spec. Without your own renovation cover, you self-fund the gap.

- Trusting bank-bundled policies — banks earn referral fees on bundled MRTAs and contents policies. Compare independently against direct insurer quotes; you will routinely save 10–25%.

What This Means for You

Insurance is the cheapest part of homeownership and the part with the lowest psychological return until something happens. The exercise to do today, regardless of how long you have owned your home, is simple: list every policy you currently hold, the sum insured, the renewal date, and the bank or insurer you bought it from. If you cannot complete that list in fifteen minutes, you almost certainly have a gap or a duplication. The total cost of being properly covered — even on a S$2.5M condo — rarely exceeds S$2,000 a year, less than a single mortgage instalment for most owners.

What Might Come Next

The Monetary Authority of Singapore has signalled interest in reforming retail insurance disclosure under its Financial Advisers Act review. Expect to see standardised “policy summary” documents for MRTA and Home Contents in 2027, similar to the Product Highlights Sheet for unit trusts. CPF Board has also been studying whether HPS should be extended to cover serious-illness scenarios beyond the current TPD definition; any such expansion would materially raise HPS premiums but reduce the case for private MRTA on top.

Frequently Asked Questions

Is HDB Fire Insurance enough on its own?

No. HDB Fire Insurance covers only the structure of the flat — the walls, floor slab, ceiling, and original developer-fitted items. It does not cover renovations, furniture, electronics, or any of your possessions. Owner-occupiers should pair it with Home Contents Insurance, which is sold separately by every major insurer for around S$120–220 per year.

Can I opt out of HPS if I have a private term-life policy?

Yes — the CPF Board permits HPS exemption if you can demonstrate an equivalent or better term-assurance policy is in force. The alternative policy must cover at least the outstanding HDB loan amount and run for the remaining loan tenure. Apply online via the CPF website with the policy schedule and a recent statement; approval typically takes 2–3 weeks. If the alternative policy lapses, HPS auto-resumes.

Should I buy single-premium or annual-premium MRTA?

Single-premium gives you a fixed cost upfront, payable from CPF OA, and locks in your insurability based on today’s health profile. Annual-premium spreads the cost but is repriced if you ever change tenure or sum assured. For most buyers under 40 in good health, single-premium delivers a 10–15% lifetime saving once you account for the CPF interest you forgo, but the convenience of paying from CPF rather than cash is significant. Annual-premium suits buyers who want the flexibility to switch insurers later.

Does my MCST condo policy cover my renovations?

Generally no. The Management Corporation Strata Title (MCST) policy covers the building structure and the original developer fittings — the kitchen and bathroom finishes that came with the unit at handover. Any subsequent renovation work, custom carpentry, designer fittings, or upgraded flooring is your responsibility. Buy a renovation cover or top-up through your home contents policy, sized to your actual renovation spend.

Will Home Contents Insurance pay out for a stolen Rolex?

Only if you specified it. Most policies treat any single article above S$2,500 as a “valuable” that must be individually declared on the schedule. Watches, jewellery, art, and rare collectibles fall into this category. If you have not declared a S$25,000 Rolex and it is stolen, the insurer pays the unspecified-items sub-limit (typically S$5,000–10,000), not the full value. Add a jewellery and watches rider for an extra S$50–120 per year per S$10,000 of declared value.

What happens to MRTA when I refinance?

The policy is assigned to a specific lender as collateral. When you refinance to a new bank, the policy must either be reassigned to the new lender or be replaced with a fresh policy. If you do nothing, the original MRTA may continue paying out to the old lender (now without a loan to settle), which means your family may eventually receive the residual but only after a contested administration process. Always notify your insurer the day you complete a refinance.

Does Home Contents cover my domestic helper’s belongings?

Most do not. The standard contents policy covers items belonging to the policyholder and household members — helpers are typically excluded. If you want to protect their personal items, look for a domestic-helper extension or take out a separate helper insurance policy (most foreign-domestic-helper insurance plans bundle a small personal effects cover at no extra cost).

Related Articles

- CPF for Property Purchase Singapore 2026 — how CPF OA funds your HPS premium and MRTA single-premium.

- Property Conveyancing Guide Singapore 2026 — where insurance assignment fits into the completion timeline.

- Singapore Home Loan Guide 2026 — understand the loan that MRTA is designed to discharge.

- CPF Housing Grant Singapore 2026 — first-time HDB buyers should stack grants before worrying about insurance.

- HDB Resale Flat Buying Guide 2026 — resale buyers face the same Fire and HPS rules as BTO buyers.

- Freehold vs 99-Year Leasehold Singapore 2026 — tenure affects sum-insured and rebuild assumptions.

Disclaimer

This guide is for general information only and does not constitute financial, insurance, or legal advice. Premiums, sum-insured guidelines, scheme rules, and exemption criteria are illustrative as at April 2026 and subject to change at the discretion of the CPF Board, the Housing & Development Board, the Monetary Authority of Singapore, and individual insurers. Always verify the latest figures with primary sources — the CPF Board HPS page, the HDB Fire Insurance page, the Monetary Authority of Singapore, and the Inland Revenue Authority of Singapore — and consult a licensed financial adviser before purchasing or replacing any policy.