Singapore CCR RCR OCR Property Guide 2026: Three Regions, Their Differences and Which Suits You

- CCR (Core Central Region) — Districts 1–4, 9, 10, 11 plus parts of D7, D8, D15. Singapore’s prime residential belt: Orchard, Marina Bay, Sentosa, Holland, Newton, Novena.

- RCR (Rest of Central Region) — City-fringe zones just outside the CCR. Includes Queenstown, Toa Payoh, Bukit Merah, Bishan, Geylang, Katong and Clementi.

- OCR (Outside Central Region) — All other districts. Mass-market heartlands: Tampines, Sengkang, Punggol, Jurong West, Woodlands, Yishun and Sembawang.

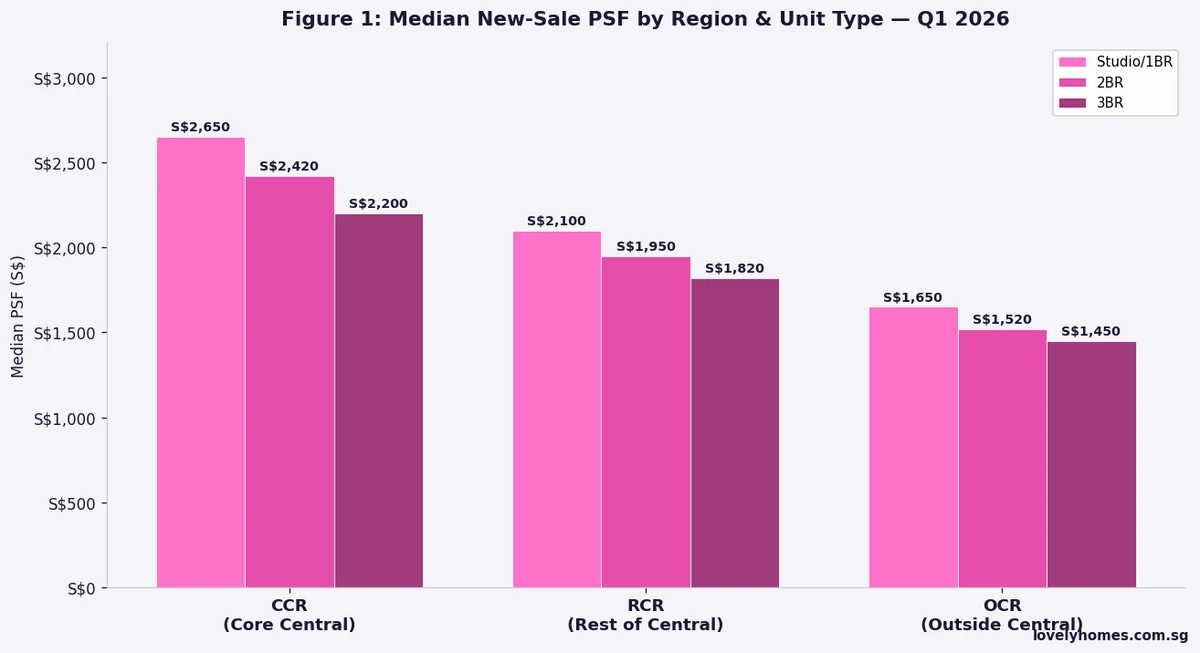

- Price gap (Q1 2026): CCR median PSF ≈ S$2,420 (2BR); RCR ≈ S$1,950; OCR ≈ S$1,520 — roughly a 30–60% price premium in CCR over OCR.

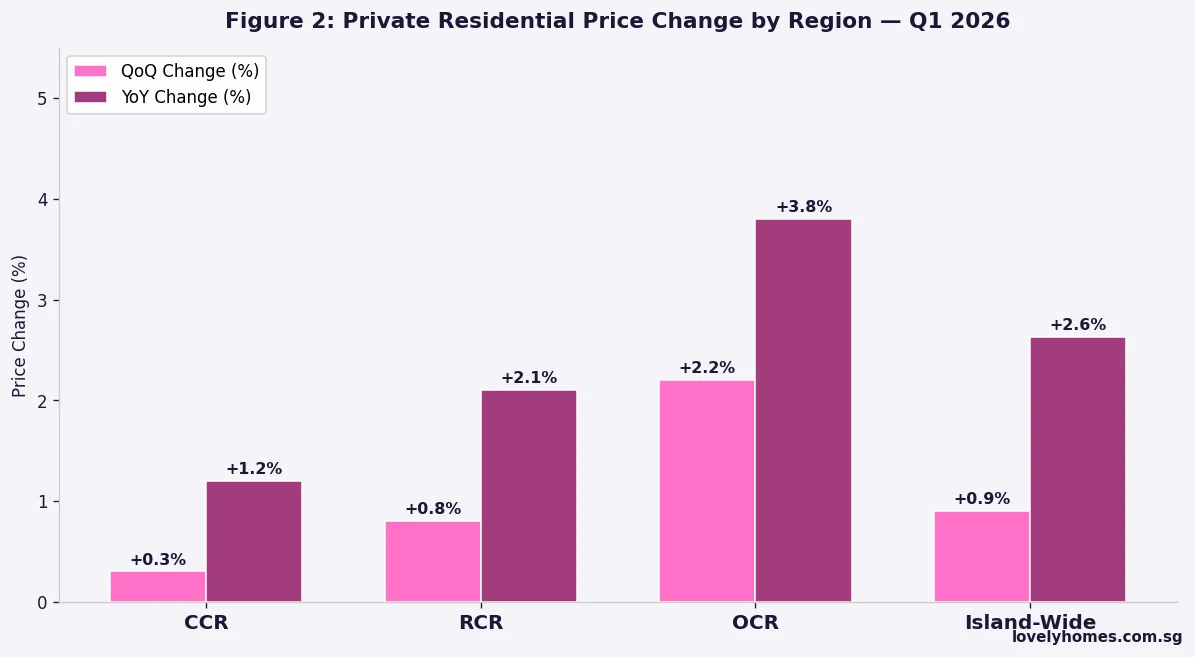

- Growth trend: OCR led price gains in Q1 2026 (+2.2% QoQ, +3.8% YoY); CCR grew more modestly (+0.3% QoQ, +1.2% YoY).

- ABSD applies uniformly — no region-based concessions; the same buyer-profile rates apply across CCR, RCR and OCR.

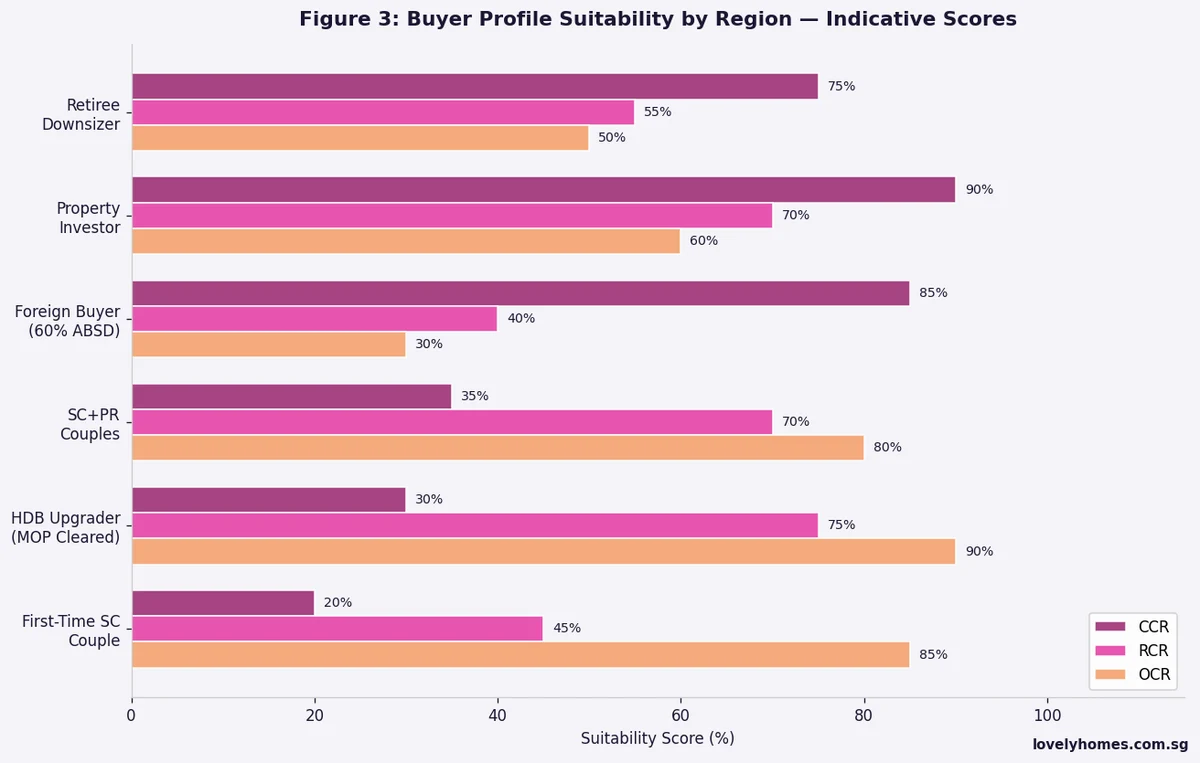

- Foreign buyers (60% ABSD) concentrate primarily in CCR; HDB upgraders and families dominate OCR demand.

- URA uses these three classifications to publish its official Private Residential Property Price Index (PPI) every quarter.

What CCR, RCR and OCR Mean — and Why They Matter

Whenever a bank economist says “CCR prices rose 0.3% this quarter” or a developer advertises a “city-fringe RCR address”, they are using a classification system maintained by the Urban Redevelopment Authority (URA) since the early 2000s. Understanding these three zones is not just academic: they directly influence which grants you qualify for, how much ABSD you pay, which mortgage LTV ratios apply, and — most critically — how much you will pay per square foot for an otherwise identical apartment.

Singapore’s 28 postal districts are grouped into three residential planning regions. The URA publishes a quarterly Private Residential Property Price Index (PPI) broken down by these regions, forming the primary benchmark for analysts, investors and homebuyers tracking where the market is heading. The HDB Resale Price Index (RPI) is a separate measure that covers public housing and does not map onto CCR/RCR/OCR.

This guide explains each region in precise terms, shows the price differentials backed by Q1 2026 URA data, maps which districts sit where, and helps you decide which region best fits your buyer profile and budget.

CCR — Core Central Region: Singapore’s Prime Residential Belt

The Core Central Region encompasses the districts that form Singapore’s historic and financial core: Districts 1–4 (Marina Bay, Tanjong Pagar, Shenton Way, Sentosa), District 9 (Orchard Road, River Valley), District 10 (Tanglin, Holland Village, Bukit Timah), and District 11 (Newton, Novena, Thomson). Parts of Districts 7 (Beach Road/Bugis), 8 (Little India/Farrer Park) and 15 (East Coast/Katong) that fall within the Central Planning Area are also classified as CCR.

The CCR is where Singapore’s most exclusive condominiums, Good Class Bungalows and ultra-luxury developments are concentrated. Transactions at Nassim Road, Ardmore Park and Marina Bay Suites set national PSF records regularly. For non-landed private property, CCR typically commands median new-sale PSFs of S$2,200–S$2,650 depending on unit type and specific district, based on Q1 2026 caveats lodged with the Singapore Land Authority (SLA).

CCR demand is driven by high-net-worth Singapore Citizens (SCs), Permanent Residents (PRs) and foreign buyers — particularly those from Indonesia, mainland China, India and Malaysia — though the 60% ABSD levied on foreigners since April 2023 has significantly curtailed international volumes. Developer launches in CCR typically feature lower unit counts, higher finishes, and more bespoke services than OCR mass-market projects.

Key CCR planning districts and landmark projects: Orchard/Scotts area (D9): One Draycott, Klimt Cairnhill. Holland/Tanglin (D10): The Crest, Leedon Residence, 15 Holland Hill. Newton/Novena (D11): 19 Nassim, Pullman Residences. Marina Bay/Tanjong Pagar (D1–4): Marina One Residences, V on Shenton, Wallich Residence.

RCR — Rest of Central Region: The City-Fringe Sweet Spot

The Rest of Central Region occupies the transitional band between the prime CCR and the mass-market OCR. It covers key mature estates: Queenstown (D3), Pasir Panjang/West Coast (D5), Beach Road/Kampong Glam (D7 outside CCR-classified areas), Little India (D8 outside CCR), Toa Payoh/Balestier (D12), MacPherson/Potong Pasir (D13), Geylang (D14), and much of East Coast/Katong/Mountbatten (D15) and Bedok South/Upper East Coast (D16, in part).

RCR properties typically offer city-fringe convenience — short MRT commutes to the CBD, established amenities, and mature town infrastructure — at a meaningful discount to CCR. Median new-sale PSFs in Q1 2026 ranged from roughly S$1,820 to S$2,100 depending on location and unit size. Districts 3, 5 and 15 command the highest RCR premiums, owing to their proximity to the Central Business District, the upcoming Greater Southern Waterfront transformation, and East Coast’s enduring lifestyle appeal.

RCR has historically been the favoured zone for HDB upgraders who want proximity to the city without CCR prices, and for dual-income professional couples who prioritise commute times over absolute affordability. New RCR launches like those in Bukit Merah (Prime, Plus BTO classification for HDB counterparts) and Queenstown have attracted strong ballot demand in both the public and private housing markets.

OCR — Outside Central Region: Singapore’s Mass-Market Heartland

The Outside Central Region covers everything outside the Central Planning Area: the eastern districts (D16 Bedok, D17 Loyang/Changi, D18 Tampines/Pasir Ris), the north-east (D19 Serangoon/Sengkang, D20 Bishan/AMK, D28 Seletar), the north (D25 Kranji/Woodlands, D26 Upper Thomson, D27 Sembawang/Yishun), the west (D21 Clementi/Upper Bukit Timah, D22 Boon Lay/Jurong, D23 Choa Chu Kang/Bukit Panjang, D24 Lim Chu Kang), and Tengah, the newest district currently under development.

OCR dominates Singapore’s private residential volume. The majority of HDB upgraders, young families, and first-time private property buyers target OCR, where new-launch condo pricing (for 2BRs) typically ranges from S$1,400–S$1,700 PSF as at Q1 2026. OCR properties tend to carry longer commutes to the CBD but offer larger unit sizes, lower quantum, and better access to green spaces, schools and suburban amenities.

OCR saw the strongest price appreciation in Q1 2026: +2.2% quarter-on-quarter and +3.8% year-on-year — outpacing both CCR (+0.3% QoQ, +1.2% YoY) and RCR (+0.8% QoQ, +2.1% YoY). This outperformance reflects robust HDB upgrader demand, lower entry quantum making properties accessible to a wider buyer pool, and a pipeline of GLS projects in growth corridors such as Tampines, Tengah, Jurong Lake District, and the Lentor precinct in AMK.

Price Differentials: What the PSF Gap Means in Dollar Terms

Understanding PSF differences in isolation can be abstract. A concrete comparison brings the gap to life. Consider a 700 sqft (65 sqm) 2-bedroom unit — a common floor plan across all three regions:

| Region | Median PSF (Q1 2026) | Total Price (700 sqft) | BSD (SC) | ABSD (SC, 1st Property) |

|---|---|---|---|---|

| CCR | S$2,420 | S$1,694,000 | S$43,120 | S$0 |

| RCR | S$1,950 | S$1,365,000 | S$27,300 | S$0 |

| OCR | S$1,520 | S$1,064,000 | S$18,280 | S$0 |

The CCR-to-OCR price differential for this hypothetical 700 sqft unit is approximately S$630,000 — nearly 60%. That gap widens significantly for second-property buyers adding 20% ABSD (S$338,800 for CCR vs S$212,800 for OCR), and for foreign buyers at 60% ABSD (S$1,016,400 for CCR vs S$638,400 for OCR). Lifestyle and investment considerations aside, region choice has a material, immediate impact on stamp duty outlay.

Lifestyle and Practical Trade-offs by Region

Beyond price, each region offers a distinct living experience. CCR residents enjoy the most concentrated mix of international restaurants, luxury retail, premium healthcare (Gleneagles, Mount Elizabeth, Farrer Park Hospital), and cultural infrastructure (National Gallery, Singapore Art Museum). However, CCR neighbourhoods tend to be denser and offer less green-space per resident than suburban OCR estates.

RCR offers arguably the strongest lifestyle-value balance: city-fringe convenience, established hawker infrastructure, proximity to parks (Queenstown Park, Potong Pasir Community Club) and access to well-served MRT lines, at 20–40% lower PSF than CCR equivalents. The ongoing Greater Southern Waterfront development, which will transform the former Keppel Club site and Alexandra corridor, is expected to further raise RCR’s profile over the coming decade.

OCR living emphasises community and family infrastructure: larger void decks, PAP community centres, proximity to Primary 1 Registration schools (important for families planning early enrolment), HDB town malls, and, increasingly, direct MRT connections through expanding TEL and CRL lines. Commute times to the CBD can range from 30 to 60 minutes depending on the district.

Which Region Suits Which Buyer?

The chart above summarises indicative suitability, but a few buyer groups merit deeper explanation. HDB upgraders who have cleared their 5-year MOP and hold meaningful CPF balances typically have loan eligibility of S$800K–S$1.4M, making OCR new launches their most accessible private market entry point. RCR remains an upgrade stretch for higher-income upgraders, but typical CCR quanta are prohibitive unless significant cash savings or investments exist outside CPF.

SC+PR couples with combined incomes above S$12,000/month often target RCR for its balance of price and location, but should note that a PR spouse is subject to a 5% ABSD on a first jointly-purchased property (SC gets 0%, but the higher of the two rates applies to the purchase). This effectively adds S$68,250 to a S$1.365M RCR unit — worth factoring into region comparison.

Foreign buyers (60% ABSD since April 2023) almost exclusively target CCR when investing in Singapore, given that the rental yield differential versus OCR rarely justifies the higher entry price at non-CCR locations. CCR’s international tenant base — expatriate professionals, corporate HQs — provides a liquidity premium that partially offsets the ABSD load.

CCR vs RCR vs OCR: Complete Comparison Table

| Factor | CCR | RCR | OCR |

|---|---|---|---|

| Key Districts | D1-4, D9, D10, D11 | D3, D5, D7–8, D12–15 | D16–28 |

| Median 2BR PSF (Q1 2026) | S$2,420 | S$1,950 | S$1,520 |

| Q1 2026 QoQ | +0.3% | +0.8% | +2.2% |

| Q1 2026 YoY | +1.2% | +2.1% | +3.8% |

| Typical Tenure | Mix of FH, 999yr, 99yr | Mostly 99yr, some FH | Predominantly 99yr |

| Primary Buyer Profiles | HNW, foreign, SC investor | Upgrader, professional | Family, first-time, HDB upgrader |

| Gross Rental Yield (est.) | 2.5–3.2% | 3.0–3.8% | 3.5–4.2% |

| CBD Commute (MRT) | 0–15 mins | 10–25 mins | 25–50 mins |

| Foreign Buyer ABSD | 60% (applies equally) | 60% (applies equally) | 60% (applies equally) |

| Landed Property Available? | Yes (GCB in D10–11) | Limited | Yes (most landed housing) |

Worked Example: The Tan Family’s Region Decision

The Tan family — a Singapore Citizen couple, both aged 35, combined monthly income of S$14,000, CPF Ordinary Account balance of S$210,000 combined — are upgrading from their Tampines 4-room HDB (MOP cleared, estimated market value S$600,000, outstanding HDB loan S$120,000).

Option A — OCR (Tampines/Sengkang area): S$1.25M 3BR condo

BSD: S$24,100 payable via CPF. ABSD: S$0 (1st private property, SC). Bank loan: 75% LTV = S$937,500, at 3.0% fixed for 2 years / 25-year tenure = S$4,439/month. TDSR: 4,439 / 14,000 = 31.7% — PASS (below 55%). Cash upfront: 5% = S$62,500, plus BSD from CPF. HDB proceeds (≈S$480K after loan) fund CPF top-up and furnishing. Assessment: comfortable, achievable, long commute from current neighbourhood.

Option B — RCR (Queenstown/Bishan area): S$1.65M 3BR condo

BSD: S$47,600 via CPF. ABSD: S$0 (1st private property, SC). Bank loan: 75% LTV = S$1,237,500, at 3.0% / 25 years = S$5,867/month. TDSR: 5,867 / 14,000 = 41.9% — PASS. Cash upfront: 5% = S$82,500, plus BSD. After HDB proceeds the family has adequate liquidity but modest buffer. Assessment: viable, tighter cash flow, better city access and rental potential.

Verdict: On income of S$14,000/month, both options are TDSR-compliant, but Option A leaves a far more comfortable monthly buffer (≈S$9,561 vs ≈S$8,133). The family’s decision ultimately hinges on commute preference, proximity to school zones, and whether they intend to rent the property out within the first few years. Many families in this profile choose RCR as a one-step upgrade recognising they can access the city fringe without stretching to CCR prices.

Why the CCR/RCR/OCR Framework Matters for Buyers in 2026

The three-region framework shapes far more than quarterly URA statistics. Banks use it when calibrating their internal risk pricing; developers use it to position their projects and set launch prices; mortgage brokers use it when stress-testing TDSR across different loan sizes. For buyers, the most practical use is benchmarking: if a developer quotes S$1,800 PSF for a suburban project claiming it’s “competitively priced”, you can immediately check whether it is an OCR (where the median is S$1,520 PSF) or RCR (where S$1,800 PSF sits around the 50th percentile) project, and calibrate your offer accordingly.

The OCR’s recent outperformance is also a structural signal. Singapore’s ongoing MRT expansion — the Cross Island Line (CRL), the Thomson-East Coast Line (TEL) Stage 5, and future Jurong Region Line (JRL) extensions — is closing the commute-time gap between OCR and the CBD. As connectivity improves, OCR locations that once seemed remote are being repriced toward RCR norms, a trend that has been visible in Tampines, Pasir Ris and the Lentor precinct over the past three years.

What Might Come Next

Speculation: The CCR premium is unlikely to narrow significantly as long as the 60% ABSD on foreign buyers remains in place — these buyers were a key source of CCR liquidity, and their reduced participation has suppressed CCR transaction volumes even as prices held. If cooling measures are selectively eased for permanent residents or certain investment categories (which analysts do not expect before 2027 at the earliest), CCR could see a sharp repricing upward.

OCR, meanwhile, faces a pipeline risk: the 2H2026 Government Land Sales (GLS) Confirmed List offers 4,745 units including sites at Tampines, Bayshore Road and Lentor Gardens, which will add meaningful new OCR and OCR-adjacent supply over 2028–2030. Buyers targeting OCR investments with a 5–7 year exit horizon should model potential competition from these incoming projects when estimating resale premiums.

Frequently Asked Questions

Is CCR always more expensive than OCR?

In median PSF terms, yes — CCR has consistently traded at a significant premium to OCR since URA began publishing regional data. However, there are exceptions: a large OCR penthouse in a boutique freehold development can exceed the quantum of a small CCR studio. PSF is the more relevant metric when comparing like-for-like unit types. The median CCR 2BR PSF in Q1 2026 was approximately S$2,420, versus S$1,520 in OCR — a 59% gap.

Do cooling measures (ABSD, LTV, TDSR) apply differently across regions?

No. All cooling measures administered by the Ministry of Finance (MOF), MAS, and IRAS apply uniformly regardless of whether a property is in CCR, RCR or OCR. The ABSD rate is determined by your citizenship/residency status and the number of residential properties you own — not by the location of the property being purchased.

Can I use CPF to buy in any region?

Yes. CPF Ordinary Account (OA) funds can be used for the purchase of any private residential property in Singapore regardless of region, subject to the standard CPF withdrawal limits tied to the property’s Valuation Limit (VL) and any applicable Basic Retirement Sum top-up requirement. The same CPF rules apply in CCR, RCR and OCR.

Are HDB flats classified under CCR/RCR/OCR?

HDB flats use a separate classification system: Standard, Plus and Prime (introduced in October 2024 under the new BTO framework). HDB does not use CCR/RCR/OCR as official categories, though analysts often informally apply the same geographic boundaries to HDB data. The HDB Resale Price Index (RPI) covers all HDB flats islandwide and is published separately from URA’s PPI.

Which region has the best rental yield?

OCR generally offers the highest gross rental yields (estimated 3.5–4.2% for non-landed as at Q1 2026), followed by RCR (3.0–3.8%) and CCR (2.5–3.2%). The CCR’s higher entry prices compress yield percentages even though absolute rents are higher. Investors targeting yield over capital appreciation are often better served by OCR or RCR properties with strong MRT access, where tenant demand from Singapore’s large pool of mid-range expatriates and local professionals is robust.

What determines if a specific development is CCR or RCR?

The URA classifies developments based on their postal district and planning area boundaries. Specifically, a development is CCR if it falls within the defined Central Area boundary (which includes the downtown core, Marina Bay, Sentosa and selected planning areas) or within the Orchard, Newton, Buona Vista or Tanglin planning areas. Developments in planning areas like Queenstown, Toa Payoh or Geylang — which are geographically close to the city centre but outside these defined zones — are classified as RCR. You can verify a specific development’s classification using URA’s online planning maps at the URA Space portal.

Does the region affect my eligibility for grants or CPF schemes?

For private residential property purchases, no CPF housing grants are available — grants (EHG, Family Grant, PHG) are exclusively for HDB flat purchases. The CPF withdrawal rules and TDSR requirements are the same regardless of region. However, for HDB buyers using the new BTO classification framework, the type of grant available is influenced by whether the flat is classified as Standard, Plus or Prime — a parallel but separate system to CCR/RCR/OCR.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Cooling Measures Guide 2026: ABSD, TDSR, LTV and SSD Explained

- Singapore Property Financing Guide 2026: LTV, TDSR, MSR and HDB vs Bank Loan

- Singapore Property Market Mid-Year Review 2026: H1 Results, Price Trends and 2H Outlook

- Singapore 2H2026 GLS Programme Guide: 9 Sites, 4,745 Units and What It Means for Buyers

- Singapore First-Time Buyer Guide 2026: HDB, Resale or New Launch?

Disclaimer: This article is for general informational purposes only and does not constitute financial, legal or tax advice. PSF figures and price statistics are derived from URA real estate statistics (Q1 2026), SLA caveats and industry estimates. Property prices can fall as well as rise. Before making any property purchase decision, readers should consult a licensed property agent, qualified mortgage broker and independent legal counsel. Stamp duty obligations should be verified with the Inland Revenue Authority of Singapore (IRAS). CPF withdrawal eligibility should be confirmed with the Central Provident Fund Board. Grant eligibility should be checked directly with the Housing and Development Board (HDB). Cooling measure rules are subject to change by the Ministry of Finance and MAS.