HDB Million-Dollar Flats Singapore 2026: Where, Why, and Whether One Is Worth Buying

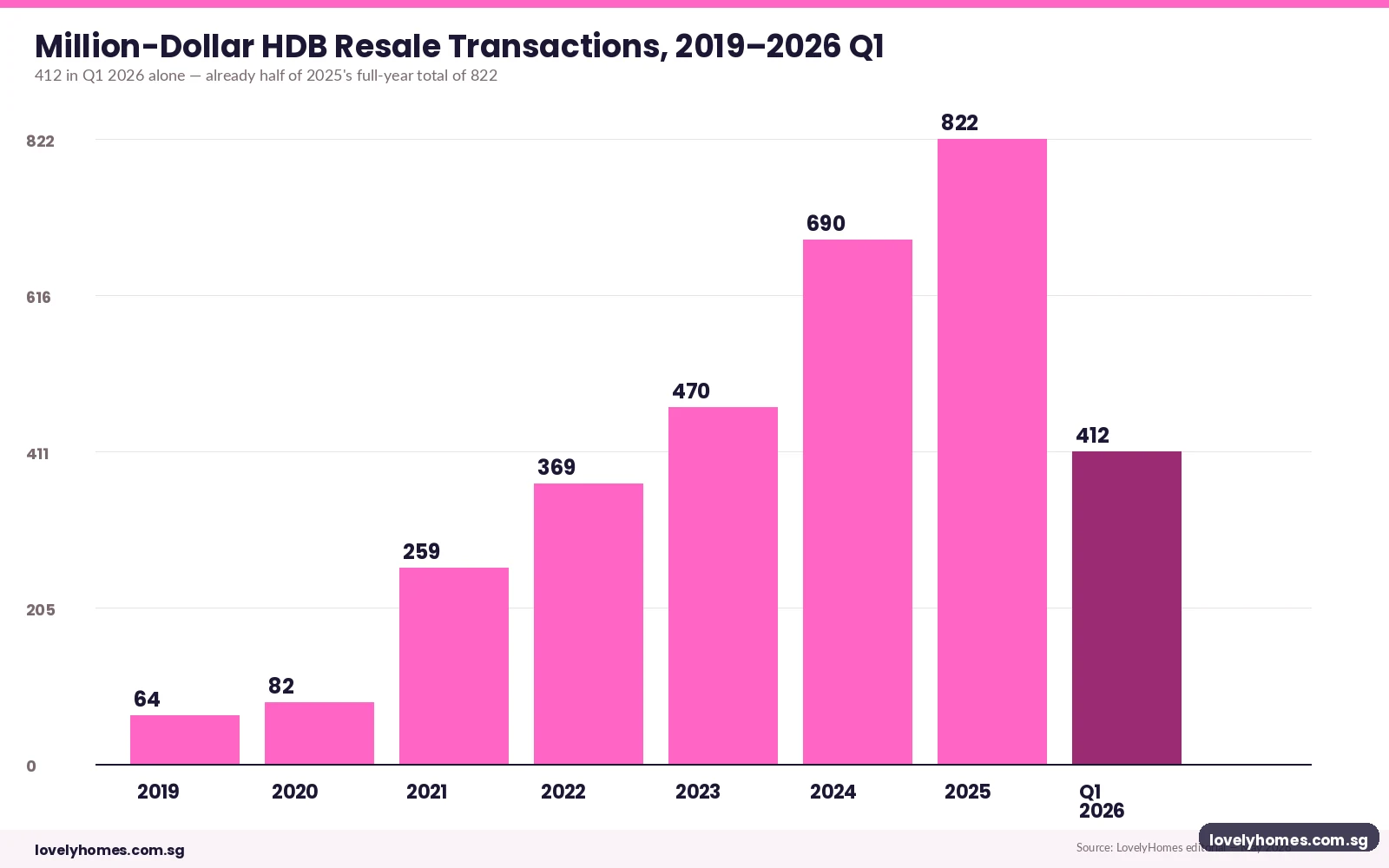

Million-dollar HDB flats are no longer the freak occurrence they once were. In the first quarter of 2026, 412 HDB resale transactions crossed the S$1,000,000 line — a single-quarter record, and already roughly half of the 822 logged across the whole of 2025. Bukit Merah, Toa Payoh, Queenstown, Bishan, and Kallang/Whampoa do most of the heavy lifting, but flats in Tampines, Sengkang and even outer-ring towns are now occasionally clearing the bar.

If you own one of these flats, you are sitting on a paper windfall that the rest of the market can only watch. If you are thinking about buying one, the question is harder: are you paying for a real long-run asset, or for a short-lived premium that will reset the moment supply normalises? This guide walks through the data, the geography, the buyer profile, and the upgrade math — with worked numbers in Singapore dollars.

For the full quarterly market context, see our companion piece on the HDB resale price decline in Q1 2026, the earlier flash-estimate analysis, and the URA private-market Q1 final figures.

Quick Answer — Million-Dollar HDB at a glance

- 412 transactions crossed S$1,000,000 in Q1 2026 alone — a record quarter.

- 2025 full-year total: 822, up from 690 in 2024 and 470 in 2023.

- Top five towns: Bukit Merah, Toa Payoh, Queenstown, Kallang/Whampoa, Bishan — all mature, rail-served estates.

- Typical winning unit: 4-room or 5-room flat, high floor, walking distance to MRT, with most lease years remaining.

- Highest single sale on record: S$1.7 million at Dawson Road (5-room, Q1 2026).

- For owners, the headline is paper wealth; the cash you walk away with after CPF refund + accrued interest is much smaller.

- For buyers, factor MOP (5 years), the LTV cap on subsequent property, and the limited resale liquidity above S$1.2 million.

How Common Are Million-Dollar HDB Flats Now?

Think of it as a slow build, then a sharp acceleration. Pre-pandemic Singapore saw fewer than a hundred million-dollar HDB transactions a year, almost all of them at Pinnacle@Duxton or other iconic central blocks. From 2021 onwards, two things changed: the COVID-era price surge in resale lifted everything by about 30%, and a steady drip of well-located DBSS / SBF estates hit their MOP and entered the resale market. The result is the curve in Figure 1.

The Q1 2026 number deserves its own line. At 412 it is roughly half a normal full-year total compressed into 12 weeks. It is also doing this while the broader HDB Resale Price Index fell 0.1% quarter-on-quarter for the first time since the second quarter of 2019. Two things are going on at once: the average flat is finally cooling after 25 consecutive quarters of growth, while the top end keeps climbing because demand for irreplaceable mature-estate stock has not budged.

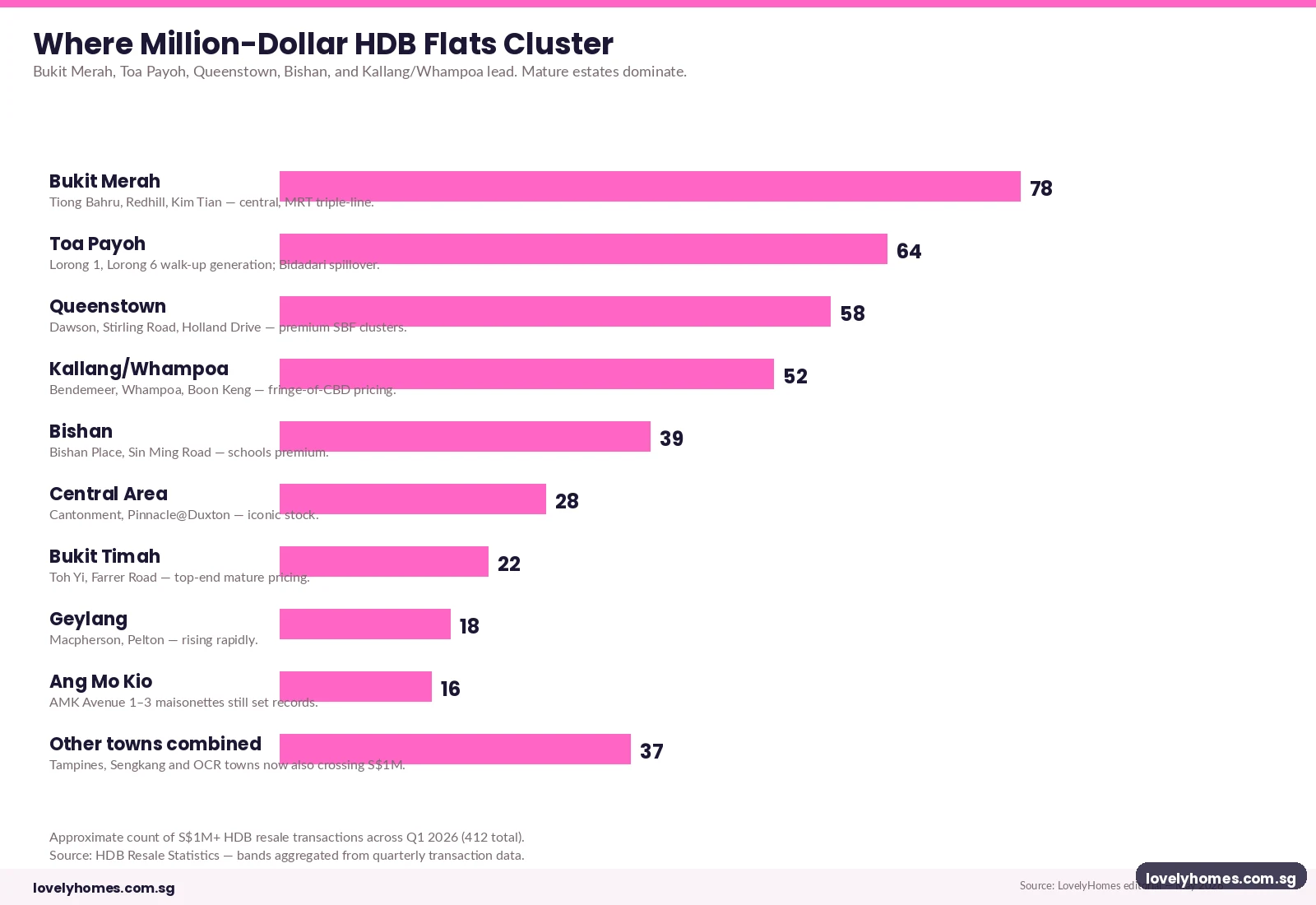

Where Million-Dollar HDB Flats Cluster

Geography is the single biggest determinant of whether a flat will sell above the million-dollar mark. The flats that clear the bar share three traits almost without exception: a mature estate within ten kilometres of the central business district, direct rail connectivity (preferably to two or three lines), and most of the 99-year lease still intact. Figure 2 maps the leading towns for Q1 2026.

Bukit Merah alone accounts for nearly one in five million-dollar transactions, anchored by Tiong Bahru, Redhill, and the Kim Tian / Bukit Ho Swee corridor. The pattern repeats: high-floor 4 and 5-room flats from the early 2010s build cycle, ten minutes by walking link to two MRT lines, with views over the city. Toa Payoh and Queenstown sit just behind — the Dawson and Stirling Road clusters in particular have produced multiple S$1.4–1.7 million sales over the past 18 months.

The pattern starts to break down further out. Tampines, Sengkang and Punggol flats now occasionally cross S$1 million, but they tend to be flagship corner units, executive maisonettes from the 1990s, or DBSS sales like the Pinnacle-style towers. They do not yet form a stable resale pool above the bar in the way that the central towns do. For broader town-level pricing context, see our HDB resale flat buying guide.

Why Million-Dollar HDB Pricing Holds Up

Three structural forces keep the top end of the HDB resale market firm even as the overall index turns:

- Supply is genuinely scarce. Most million-dollar flats are 4 or 5-room units in mature estates with high floors and short walks to MRT. HDB does not build new flats with those characteristics any more — central-area BTO supply has shifted to smaller 3 and 4-room units in tower blocks at higher densities.

- Demand is mostly cash-rich upgraders and second-time buyers. First-time buyers cannot compete here. The market for million-dollar flats is dominated by households trading down from a private property to a centrally-located HDB, or by Singapore Citizens cycling out of an executive condo and buying back into HDB before applying for a Build-To-Order replacement.

- Private-condo prices have set the ceiling. When a freehold city-fringe condo trades at S$2,400 per square foot, a 1,200 sq ft 5-room HDB at S$1,400,000 is still S$1,166 per sq ft — less than half. Buyers see relative value, not absolute expense.

That last point matters for the path ahead. As long as the gap between mature-estate HDB and city-fringe condos remains north of 50%, the top end of HDB pricing has a floor. The risk is a meaningful condo correction or a sustained leasehold-decay narrative shift — either of which would pull the ceiling lower.

Summary Table — Profile of Q1 2026 Million-Dollar Sales

| Metric | Q1 2026 | 2025 Full Year | 2024 Full Year |

|---|---|---|---|

| Million-dollar transactions | 412 | 822 | 690 |

| Share of total HDB resale | ~5.4% | ~3.1% | ~2.3% |

| Highest sale | S$1.70m (Dawson, 5-room) | S$1.65m (Dawson, 5-room) | S$1.58m (Pinnacle, 5-room) |

| Most common flat type | 5-room | 5-room | Executive / 5-room |

| Top town | Bukit Merah | Bukit Merah | Queenstown |

Indicative figures cross-referenced from HDB’s quarterly resale statistics and SRX/EdgeProp reporting; minor variances arise from cut-off dates.

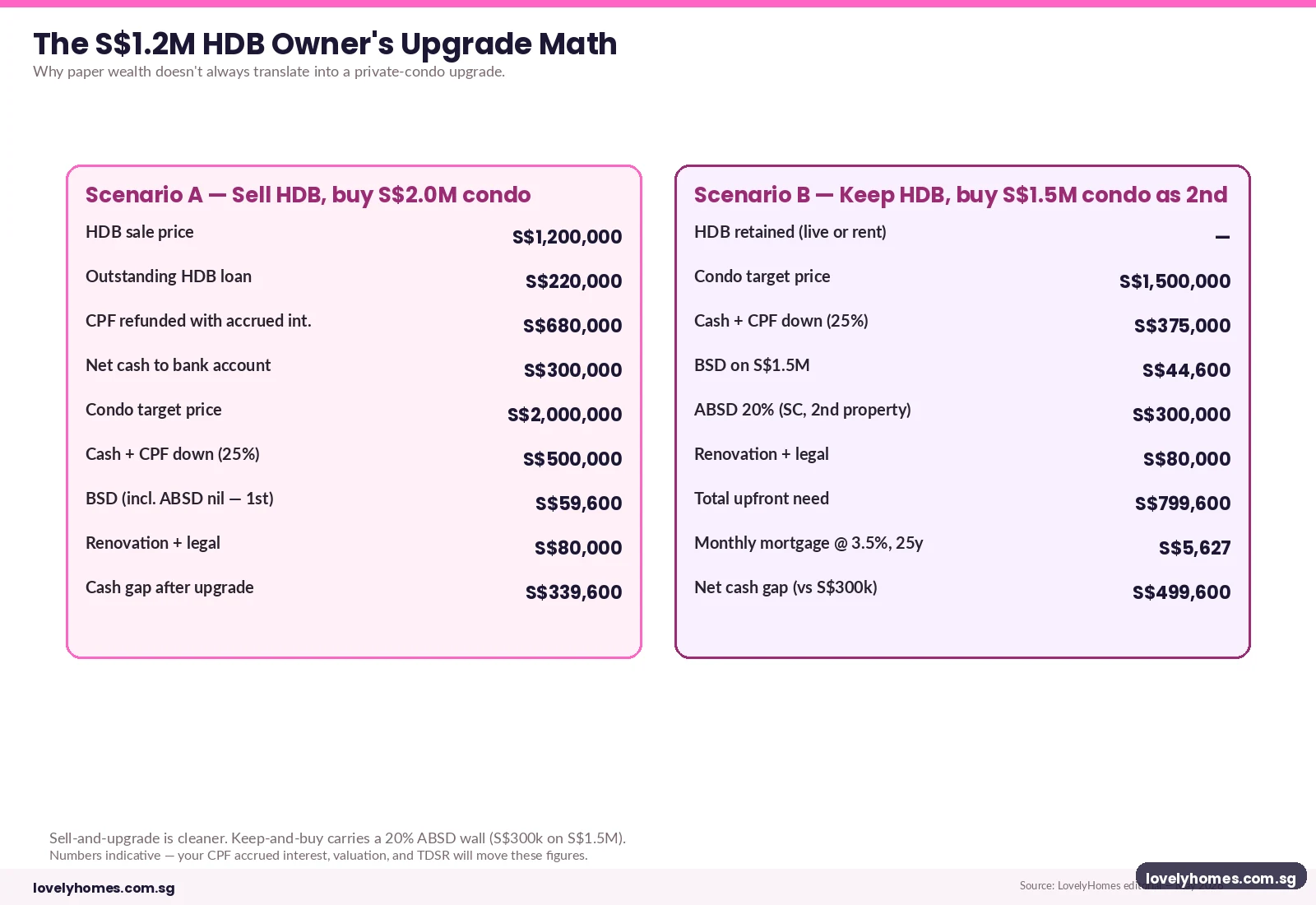

Worked Example — What S$1.2 Million Actually Looks Like in Cash

Let’s anchor on a realistic scenario. A Singapore Citizen couple, both 42, own a 5-room flat in Bukit Merah bought new from HDB in 2010 for S$520,000. Their outstanding HDB Concessionary Loan balance is S$220,000. They have used a combined S$420,000 of CPF Ordinary Account funds across the holding period, and CPF accrued interest has compounded to S$260,000. They list the flat and accept an offer at S$1,200,000.

What hits the bank account? Sale price S$1,200,000, less HDB loan repayment S$220,000, less CPF refund S$420,000 + S$260,000 accrued interest = S$680,000 returned to CPF (not cash), less legal and agent costs of around S$30,000. Net cash to the seller: S$270,000. Net CPF balance: S$680,000 (which can be redeployed for a next property purchase). The headline million-dollar print is real, but it travels in two channels — cash and CPF — and most of it is not cash.

Now layer on the upgrade decision. Scenario A — sell HDB and buy a S$2.0M condo: the couple uses S$500,000 down payment (cash + CPF mix), pays Buyer’s Stamp Duty of about S$59,600, no ABSD (it is a first private property after disposing of the HDB), and a S$1.5M loan at around S$7,520 per month over 25 years at 3.5%. Scenario B — keep the HDB, buy a S$1.5M condo as a second property: they need S$375,000 down, pay BSD of S$44,600, and an additional 20% ABSD on the S$1.5M = S$300,000. The ABSD wall changes the maths fundamentally; total upfront need is S$799,600. For most upgraders, scenario A wins for cash flow; scenario B wins only if the rental yield on the retained HDB is meaningfully positive after MSR and HDB sub-letting rules are factored in.

For the full mechanics on the second-property tax, see our ABSD complete guide.

Why This Matters for Buyers, Sellers, and Upgraders

If you are a seller sitting on a likely million-dollar flat: the asset is real, but realise that less than 30% of it lands as cash if you have used CPF heavily across the holding period. Run the cash-out arithmetic before listing — especially if you intend to fund a private upgrade. The CPF for Property Purchase guide walks through the refund and accrued-interest mechanics in detail.

If you are a buyer considering a million-dollar HDB: be honest about exit liquidity. Above S$1.2M the resale buyer pool is thin and dominated by HDB-eligible, MOP-cleared upgraders trading sideways; foreign demand and PR demand are zero by regulation. Hold periods of less than seven to eight years can leave you exposed to a price reset if the index turns and the cash-rich upgrader cohort sits out a cycle.

If you are an upgrader: the S$1M HDB and the S$2M condo are not the same dollar. The HDB is mostly CPF; the condo down payment must be cash + CPF in regulated proportion, and the ABSD wall sits between you and a second property. For the full upgrade decision tree, see our HDB-to-condo upgrade guide.

How Singapore Compares

Comparing public-housing premium pricing across cities is messy — few jurisdictions have a system as institutionalised as HDB. The Hong Kong public estate market trades at very different scarcity premiums. Sydney’s former public-housing stock at Waterloo and Glebe has occasional A$1m+ trades, but those are usually privatised dwellings in markets with no income-cap rules. The closest comparable framework is South Korea’s LH-built apartments at high floors in Seoul, where the cap-relaxation cycles drive episodic premium pricing. Against those benchmarks, HDB’s top-end resale market is unusually deep, unusually well-policed for ownership, and unusually liquid.

What Might Come Next

Forward-looking commentary — clearly speculative. Three scenarios bear watching over the rest of 2026 and into 2027:

- Continued top-end strength even as the index falls. The most plausible scenario. Mature-estate scarcity is structural; the top end carries on as the broader resale market cools through fresh BTO supply (around 13,000 flats expected in 2026, roughly double 2025).

- Targeted cooling. If the Government feels the optics of S$1.7M HDB sales are inconsistent with public-housing affordability messaging, a targeted measure — expanded Prime / Plus restrictions on high-priced resale, or a longer MOP — is possible. None has been signalled, but the policy lever is real.

- Material condo correction pulling the HDB ceiling down. The least likely in the near term but the most disruptive: a 10–15% private-condo correction would compress the relative-value gap and remove the implicit ceiling on million-dollar HDB pricing.

None of these scenarios changes the basic logic for owners or considered buyers. Million-dollar HDB pricing is geographic, structural, and slow-moving. Trying to time it is a poor use of attention; understanding what you actually own (or are buying) is the better use.

Frequently Asked Questions

What is the highest price ever paid for an HDB resale flat?

As at Q1 2026, the published record sits at S$1.70 million for a 5-room SBF flat at Dawson Road in Queenstown. Prior records included a S$1.65 million Dawson sale in 2025 and a S$1.58 million Pinnacle@Duxton sale in 2024. HDB and SRX publish resale transaction records monthly; record-breakers are usually high-floor 5-room or executive flats in central, MRT-served estates.

Why are million-dollar HDB flats clustering in Bukit Merah and Queenstown?

Three reasons: most of the high-floor 4 and 5-room SBF flats from the 2010–2014 build cycle are now MOP-cleared and entering the resale market; the central location supports very high relative-value pricing against private condos; and the rail connectivity (Tiong Bahru / Redhill / Queenstown / Commonwealth on the East-West Line) means buyers are paying for both location and convenience. Toa Payoh and Bishan show similar patterns on the North-South Line corridor.

Can foreigners or PRs buy million-dollar HDB resale flats?

Foreigners cannot buy any HDB resale flat. Permanent Residents can, but only as part of a family nucleus where the eligibility scheme is met (PR Quota for the block applies, and the standard SPR holding rules), and never as a sole household. The buyer pool above S$1 million is therefore entirely Singapore Citizen + PR family nuclei — this is one of the structural reasons the market behaves differently from private resale.

Should I buy a million-dollar HDB or a similarly-priced city-fringe condo?

The honest answer depends on horizon and household composition. The HDB delivers more living space, better proximity to schools and transport in the affected estates, and lower maintenance fees, but it locks you into the public-housing rule set (MOP, ethnic quota, no rental until MOP, restrictions on second-property ownership). The condo trades floor space for asset class flexibility — you can rent it, sell it without MOP, and own it alongside other properties (subject to ABSD). Many buyers find the HDB the better lifestyle choice and the condo the better balance-sheet choice; very few buyers should pretend the two are equivalent.

How much cash will I actually walk away with from a S$1.2 million HDB sale?

Less than the headline. From a typical S$1.2M sale you must repay the outstanding HDB or bank loan, then refund used CPF principal plus accrued interest at 2.5% per annum into your CPF account, then pay legal and agent fees. In a representative scenario with S$220k loan outstanding, S$420k of OA used over 14 years, S$260k accrued interest and S$30k transaction costs, the seller receives roughly S$270k as cash to the bank account and S$680k restored to CPF. The CPF portion can fund a next purchase but is not free cash. See our CPF for Property Purchase guide for the mechanics.

Will the price falls in Q1 2026 reach the million-dollar segment?

The Q1 2026 HDB Resale Price Index fell 0.1% — the first quarterly decline since Q2 2019 — while million-dollar transactions hit a record. The two facts coexist because the broader index is moved by the volume centre of the market (3 and 4-room flats in non-mature towns), while the million-dollar segment depends on the supply of mature-estate, rail-served, larger flats. The mechanisms that have lifted the top end (scarcity, relative value vs condos) are not the mechanisms cooling the broader index (fresh BTO supply, transactional fatigue). The two segments can diverge for an extended period.

What should I do if I bought my flat for S$400,000 and it’s now worth S$1.2 million?

First, separate the unrealised gain from your decision: the windfall does not change whether your home suits your household. Second, if you intend to monetise, run the cash-out + CPF refund maths before listing — many sellers find their actual cash-in-hand is far less than expected. Third, if you intend to upgrade to a private property, model both the “sell + upgrade” path and the “keep + buy second” path with full ABSD; the answer is rarely obvious. Fourth, engage a conveyancing solicitor and (where relevant) a CPF-aware financial planner before signing any OTP. The numbers are too large for shortcuts.

Related Articles

- HDB Resale Prices First Decline Since 2019 — Q1 2026 Final Stats

- HDB Resale Flat Buying Guide Singapore 2026

- HDB to Condo Upgrade Guide Singapore 2026

- CPF for Property Purchase Singapore 2026

- ABSD Singapore 2026 — Complete Guide

- Seller’s Stamp Duty Singapore 2026

- LTV Limits Singapore 2026

Disclaimer

This article is general information about HDB resale pricing in Singapore as at May 2026 and does not constitute financial, tax, or legal advice. Transaction figures are aggregated from HDB’s published resale statistics, with cross-reference from URA, MAS, IRAS and CPF Board guidance where applicable. Individual transaction values, CPF balances, and accrued interest computations vary materially by household; for a transaction of this size always engage a licensed Singapore conveyancing solicitor, a CPF-aware financial adviser, and (if upgrading) a chartered tax practitioner before signing any Option to Purchase or Sale & Purchase agreement.