Holland Plain GLS 2026: Sim Lian Wins at S$1,491 psf ppr — D10 CCR Pricing, Investment Outlook and Buyer Analysis

- Sim Lian Group won the Holland Plain GLS tender on 12 May 2026 as the sole bidder at S$454 million — translating to S$1,491 psf ppr.

- The 99-year leasehold site in District 10 (CCR) spans 15,717 sq m with a max GFA of 28,291 sq m and an estimated yield of ~280 residential units.

- Building height is capped at 6 to 8 storeys, pointing to a low-rise boutique development — a rare product type in the Holland Road / Farrer Road corridor.

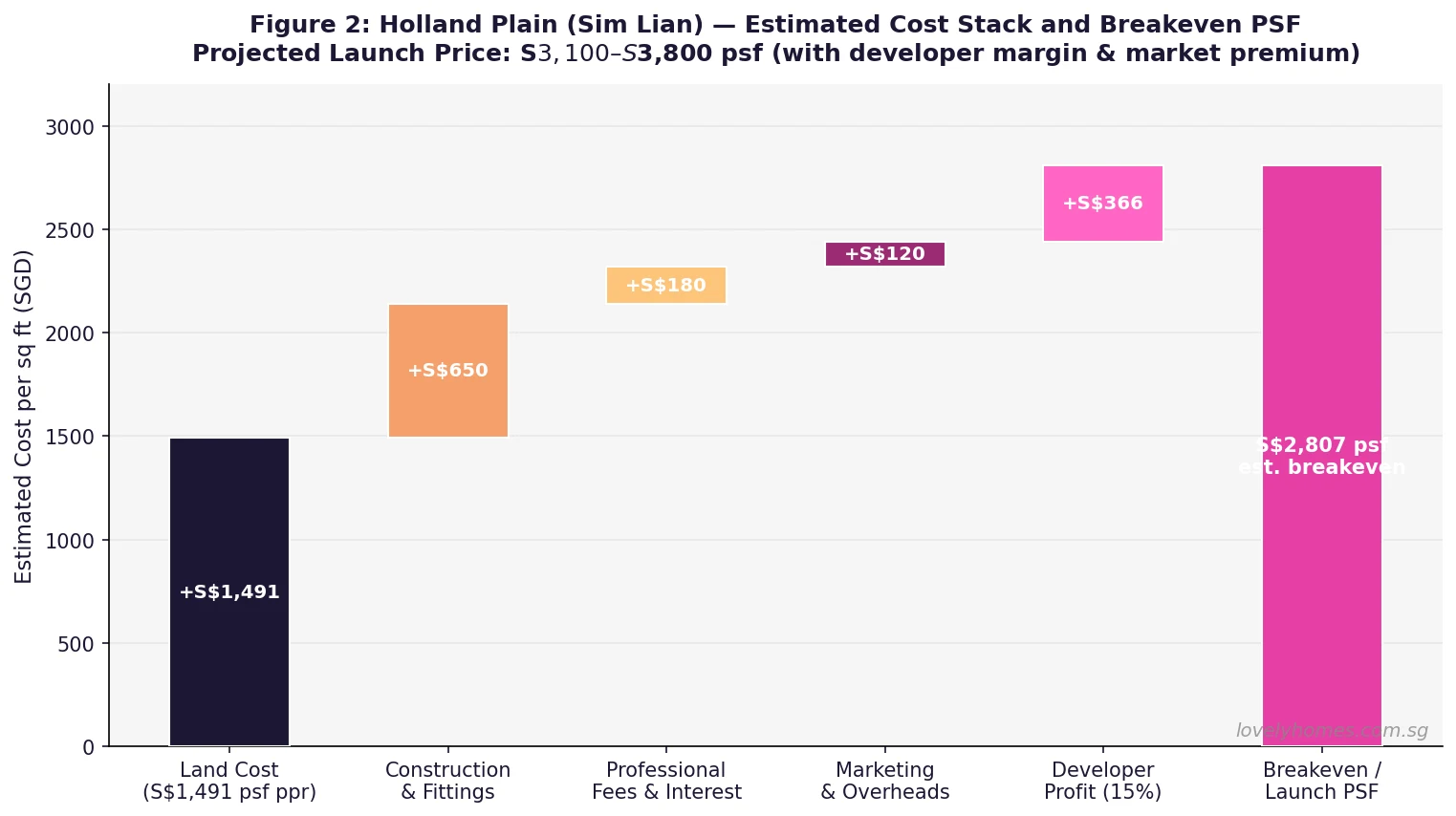

- Estimated launch price: S$3,100–S$3,800 psf, based on the S$1,491 psf ppr land cost plus construction, financing, and a market premium over One Holland Village Residences resale benchmarks.

- Preview is likely in Q3–Q4 2027 at the earliest, given the 18–24 month planning and construction mobilisation window typical of CCR boutique sites.

- The sole-bid outcome reflects cautious developer sentiment in the CCR at current interest rates, but Sim Lian’s calculated entry represents a significant up-market pivot for the group.

- For SC buyers, no ABSD on a first property purchase. Foreigners face a 65% ABSD surcharge — materially reducing demand from the international pool that traditionally drives CCR volumes.

Holland Plain GLS Awarded to Sim Lian — The Deal Breakdown

On 12 May 2026, the Urban Redevelopment Authority (URA) announced the award of the Government Land Sales (GLS) site at Holland Plain, District 10, to Sim Lian Group — Singapore’s only bidder. The developer tendered S$454,110,000 for the 99-year leasehold parcel, equivalent to approximately S$1,491 per square foot per plot ratio (psf ppr).

The sole-bid outcome drew immediate attention from industry observers. In previous cycles, prime CCR confirmed-list sites in District 10 attracted three to six bidders. The absence of competing bids from large listed developers such as City Developments, CapitaLand Development, UOL Group, or Frasers Property points to a recalibration of risk appetite in the Core Central Region, where the 65% Additional Buyer’s Stamp Duty on foreigners has significantly dampened the international buyer pool that historically underpinned CCR price discovery.

That Sim Lian Group — better known for large-scale Outside Central Region projects such as Treasure at Tampines (2,203 units) and Parc Clematis (1,468 units) — stepped into this site alone is a notable strategic shift for the developer. It signals confidence in the long-term premium of the District 10 address book and suggests Sim Lian has modelled a profitable outcome at launch prices that may be more measured than the aspirational pricing sometimes associated with CCR boutique developers.

Site Specifications — A Boutique Low-Rise in the Heart of D10

| Parameter | Details |

|---|---|

| Location | Holland Plain, District 10 (CCR), Singapore |

| Tenure | 99-year leasehold from 12 May 2026 |

| Site Area | 15,716.9 sq m (approximately 169,148 sq ft) |

| Max Gross Floor Area | 28,291 sq m (approx. 304,590 sq ft) |

| Gross Plot Ratio | 1.8 |

| Permitted Building Height | 6 to 8 storeys |

| Estimated Residential Units | ~280 units |

| Land Use | Residential (private condominium) |

| Developer | Sim Lian Group |

| Award Price | S$454,110,000 (S$1,491 psf ppr) |

| Tender Closed | 7 May 2026 |

| Award Date | 12 May 2026 |

The six-to-eight storey height cap is significant. In the Holland Plain and Farrer Road precinct, most condominium developments are low-to-mid-rise, and the Master Plan’s height guidance for this parcel maintains the neighbourhood’s established residential character. Sim Lian is unlikely to build a high-density tower; buyers can expect a product more akin to Cluny Park Residences or Gallop Green — intimate, well-appointed, and positioned for owner-occupier and high-net-worth tenant demand from the nearby international schools.

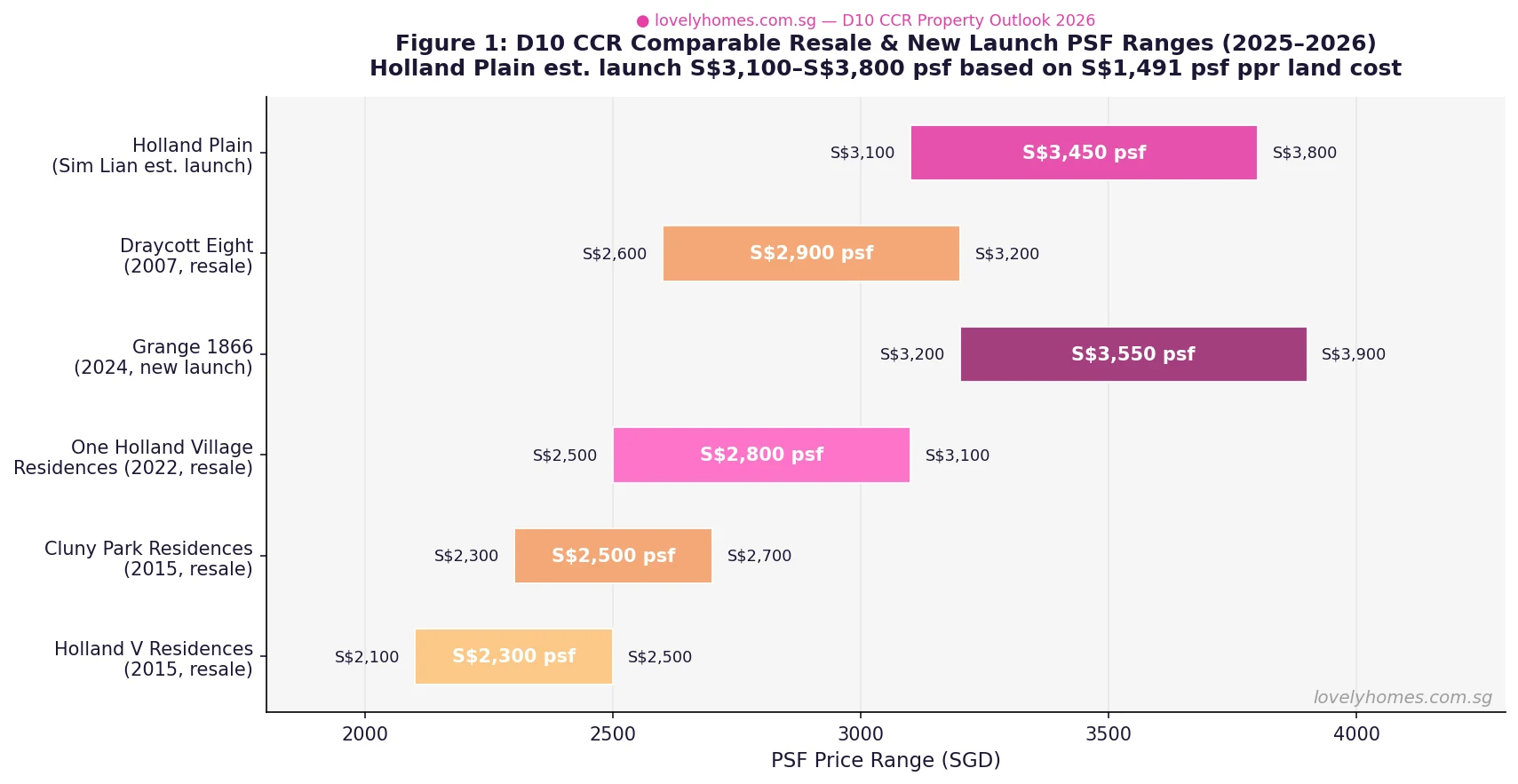

D10 Comparable PSF — Where Holland Plain Fits

The chart above places Holland Plain’s estimated launch price alongside established D10 benchmarks. One Holland Village Residences — the most proximate recent comparable, launched in 2022 and developed by Far East Organization — traded at roughly S$2,800–S$3,000 psf on launch and currently resells at S$2,500–S$3,100 psf depending on floor level and facing. Grange 1866 in D9 launched in 2024 at S$3,200–S$3,900 psf. Draycott Eight — an older freehold project in D10 — commands S$2,600–S$3,200 psf on resale despite its 2007 completion date, underlining the sustained value of CCR addresses.

Holland Plain’s 99-year leasehold tenure will attract a discount versus freehold and 999-year leasehold projects in the same district. Buyers accustomed to Cluny Park Residences or Good Class Bungalow (GCB) adjacency-premium projects will note that freehold equivalents in the Farrer Road–Grange Road belt command a 10–15% premium over comparable 99-year leasehold product. This suggests the achievable PSF at Holland Plain may cluster towards S$3,100–S$3,500 psf for the majority of units, with penthouses and premium stacks potentially touching S$3,800 psf.

Estimated Launch Pricing and Unit Mix

With 280 units across ~304,590 sq ft of GFA, the average unit will be approximately 1,088 sq ft — consistent with a mix weighted towards 2- and 3-bedroom configurations appropriate for the family-oriented D10 demographic. LovelyHomes estimates the following indicative pricing grid, based on a blended average launch PSF of S$3,300:

| Unit Type | Est. Size (sq ft) | Indicative Price Range |

|---|---|---|

| 1-Bedroom | 450–550 | S$1.40M – S$2.09M |

| 2-Bedroom | 700–900 | S$2.17M – S$3.42M |

| 3-Bedroom | 1,000–1,300 | S$3.10M – S$4.94M |

| 4-Bedroom / Penthouse | 1,500–2,000 | S$4.65M – S$7.60M+ |

Indicative only. Actual pricing will depend on Sim Lian’s unit mix strategy, prevailing SORA rates at the time of launch, and market conditions in 2027–2028. Consult a licensed property professional before making any commitment.

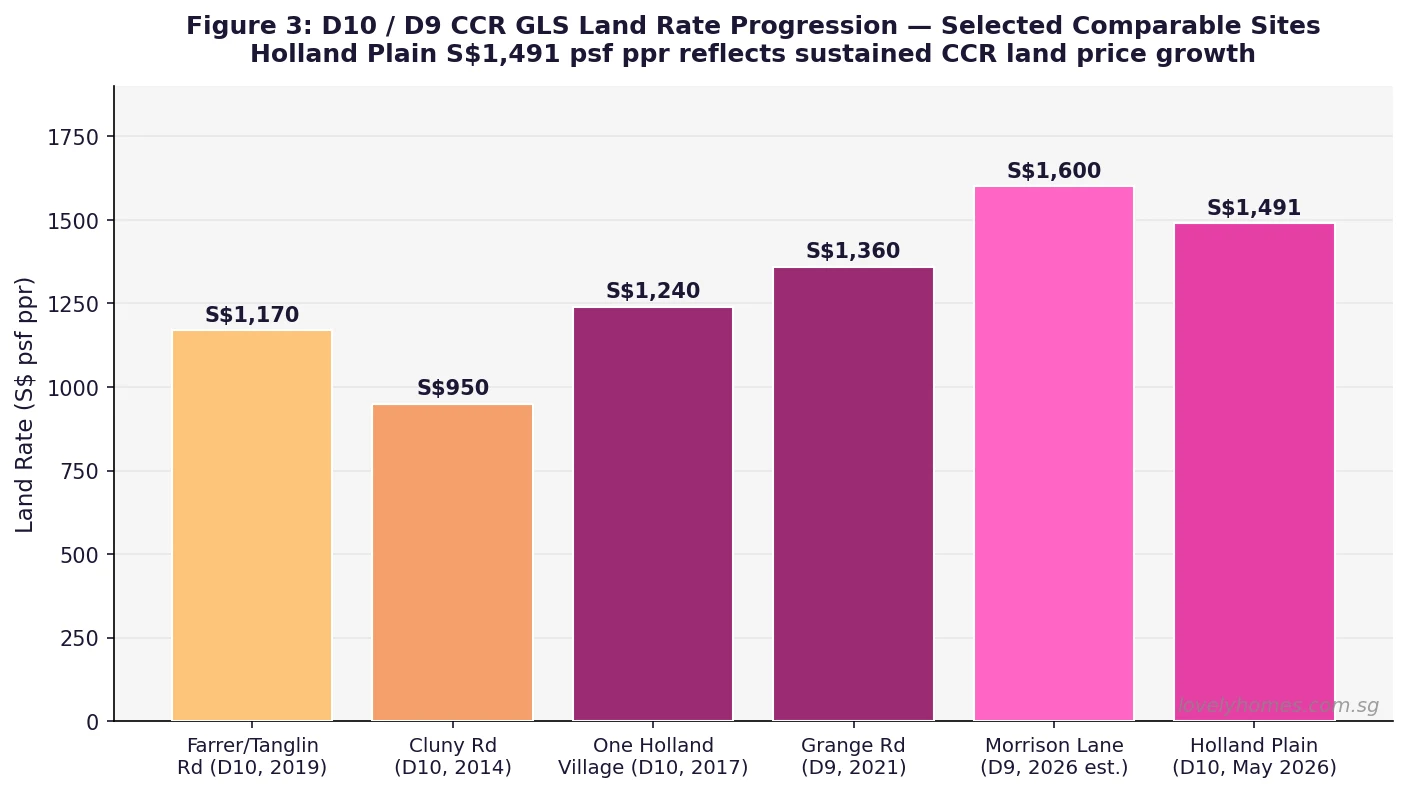

D10 GLS Land Rate Progression — Context

Holland Plain’s S$1,491 psf ppr land rate is notable for what it is not: a record. In the pre-cooling-measure era, CCR land bids regularly pushed past S$2,000 psf ppr. The 60% Additional Buyer’s Stamp Duty on foreigners (raised to 65% in April 2023) has structurally redirected international capital away from the new-launch CCR pipeline, removing the speculative demand layer that previously compressed developer margins and pushed bids skyward. What remains is the durable owner-occupier and long-term investment demand from Singapore Citizens and Permanent Residents, which is more price-sensitive and longer in decision horizon.

Sim Lian’s S$1,491 psf ppr bid is broadly consistent with a financially disciplined modelling exercise rather than a prestige land-banking move. The developer is betting on a specific thesis: that D10 boutique, low-rise product at 280 units will sell through comfortably to local families and returning expatriates, even at S$3,100–S$3,500 psf, given the paucity of new launch supply in the Holland Road–Farrer Road corridor since 2022.

Who Will Buy Holland Plain — The Target Buyer Profile

Several distinct buyer archetypes are likely to drive take-up at Holland Plain:

SC upgraders from the OCR. With OCR private condo prices rising 2.2% in Q1 2026 and MOP waves releasing large numbers of resale HDB flats into the market, a cohort of Singapore Citizens who purchased OCR condominiums or HDB flats in 2018–2021 are now sitting on significant capital gains. For couples with household incomes of S$20,000–S$30,000 per month, a 3-bedroom unit at Holland Plain at S$3.5M–S$4.5M represents an aspirational CCR upgrade with no ABSD on a first private property purchase.

D10 residents downsizing or lateral moving. Freehold condominium owners in the Farrer Road, Grange Road, and Tanglin Road precinct who seek newer infrastructure, modern facilities, and professional property management without leaving the district will look seriously at Holland Plain, even with the 99-year leasehold caveat.

Expat tenants’ employers and parents. The international schools immediately adjacent — United World College of South East Asia (Dover campus), the Australian International School, the German European School — generate sustained demand for family-sized rental units in D10. Investor-buyers who target the expat tenant pool will find Holland Plain’s 3-bedroom stock particularly compelling, especially given one-north and the Buona Vista biomedical employment cluster’s continued expansion driving corporate housing budgets.

High-net-worth Singaporeans for own stay. At six to eight storeys in a low-density neighbourhood, Holland Plain will offer a level of privacy and exclusivity rarely available in new launches. The limited unit count of ~280 means the development will feel intimate — a selling point for buyers accustomed to landed living who want managed-property convenience.

ABSD Implications — The Foreigner Market Is Largely Sidelined

The 65% Additional Buyer’s Stamp Duty on foreign buyers, in force since 27 April 2023, means that any foreigner purchasing a S$2M 2-bedroom unit at Holland Plain would face an ABSD bill of S$1.3 million — on top of BSD of approximately S$57,600. Total acquisition cost before loan: over S$3.35M. This is not a purchase case that works for most foreign nationals who do not have deep Singapore roots or a specific business reason to own in the CCR.

The practical implication: Holland Plain will be absorbed almost entirely by Singapore Citizens and Permanent Residents. SPR buyers pay 5% ABSD on a first property — manageable at S$100,000–S$180,000 on a typical unit — and a meaningful segment of the take-up will come from this pool. SC buyers on a first property pay zero ABSD. SC buyers on a second or subsequent property pay 20% ABSD — a S$640,000 bill on a S$3.2M unit — which remains a significant friction, though less prohibitive for high-net-worth upgraders than the foreigner rate.

For more on ABSD rates by buyer profile, see our ABSD Singapore 2026 complete guide.

Worked Example — Mr & Mrs Chua: SC Upgraders Buying a 3-Bedroom at Holland Plain

Mr & Mrs Chua are Singapore Citizens in their early 40s. They sold their OCR condominium in Tampines in late 2025 for S$1.55M (purchased in 2019 for S$1.1M), banking approximately S$350,000 in net cash after paying off the outstanding mortgage. They are now renting in D10 and plan to purchase a 3-bedroom unit at Holland Plain when it launches, estimated at approximately S$4.1M.

ABSD: As SC buyers on their second private residential property (they now own zero properties — the Tampines unit was sold), they are effectively first-time owners at point of purchase. Zero ABSD applies. ✓

BSD on S$4.1M: 1% × S$180k = S$1,800; 2% × S$180k = S$3,600; 3% × S$640k = S$19,200; 4% × S$500k = S$20,000; 5% × S$1.1M = S$55,000; 6% × S$1M = S$60,000. Wait — let me apply the correct BSD tiers. On S$4.1M: 1%×180k + 2%×180k + 3%×640k + 4%×500k + 5%×2.6M. Actually: First S$180k at 1% = S$1,800; next S$180k at 2% = S$3,600; next S$640k at 3% = S$19,200; next S$500k at 4% = S$20,000; above S$1.5M: next S$1.5M at 5% = S$75,000; above S$3M: remaining S$1.1M at 6% = S$66,000. Total BSD = S$185,600.

Financing: At a blended bank fixed rate of approximately 2.0% per annum (estimated for 2027), the Chua couple borrows 75% of the S$4.1M purchase price = S$3,075,000. Monthly instalment over 25 years ≈ S$13,020. TDSR check: assuming joint gross income S$35,000/mth — TDSR = 37.2% (below 55% cap). ✓

Down payment and cash needed: 25% down = S$1,025,000 (can be funded from CPF OA and cash); BSD S$185,600 in cash. Using S$350,000 cash from the Tampines sale and drawing S$675,000 from CPF OA, the couple meets both the down payment and stamp duty requirements with ~S$164,000 CPF OA remaining as a buffer.

Summary for Mr & Mrs Chua: S$4.1M Holland Plain 3-bedroom → ABSD nil → BSD S$185,600 → bank loan S$3.075M @ 2.0% for 25yr → monthly S$13,020 → TDSR 37.2% → cash outlay S$535,600 (cash from Tampines proceeds + stamp duty) + CPF drawdown S$675,000.

Development Timeline and What to Watch

Following the tender award on 12 May 2026, Sim Lian will enter the planning and approvals phase with URA. A provisional building plan is typically submitted within six months of award, with a building plan approval following three to six months later. Construction commencement generally occurs 18–24 months post-award for CCR boutique sites. Based on this trajectory, the likely public preview window is Q3–Q4 2027, with expected project completion (Temporary Occupation Permit) in 2030–2031.

Watch for: Sim Lian’s project name announcement (likely within six months), architectural rendering release, showflat construction in the Holland Plain vicinity, and any pre-indication of pricing through EdgeProp or Stacked Homes developer briefings approximately 60–90 days before the official launch date.

What This Means for D10 Buyers and the Broader CCR

The Holland Plain award is a data point in a larger story about CCR supply discipline. With the 65% foreigner ABSD in place and a generation of Singaporean private property owners sitting on significant unrealised equity from 2019–2024 price appreciation, the CCR market in 2026–2028 will be one where supply is lean, developer caution is visible (sole bids, measured land rates), and local buyers — particularly SC upgraders — will find themselves as the dominant demand driver for the first time in decades.

For buyers considering Holland Plain, the opportunity is clear: a boutique, low-rise D10 CCR address in a school belt with strong expat tenant demand, delivered by a developer with an established sales track record, at land rates that suggest a measured (rather than euphoric) launch PSF. The risk factors are the 99-year leasehold tenure, the reliance on local SC/SPR demand, and the long wait time (2027–2028 launch, 2030–2031 completion) during which market conditions may shift.

What Might Come Next — GLS Pipeline and CCR Outlook

This is speculative. The remaining 1H 2026 GLS confirmed list site — River Valley Green Parcel C — closes for tender on 18 June 2026 and is expected to attract two to four bidders given its smaller site area. If it also draws a sole bid at conservative land rates, it would confirm a broader pattern of developer restraint in the CCR. The URA may respond to this signal when compiling the 2H 2026 GLS programme (expected announcement December 2026) by adjusting the CCR mix on the confirmed list, potentially holding back sites to avoid depressing land values further or to allow existing pipeline to absorb before adding new confirmed-list supply.

Watch also for any policy review of the 65% foreigner ABSD. If global capital flows to Singapore property are assessed to have become too restricted and if housing prices stabilise, there is a non-trivial possibility of a partial relaxation (e.g., from 65% to 30–45% for longer-term PRs or certain FTA-holder nationalities) in the 2026–2027 National Day Rally or Budget cycle. Any such relaxation would immediately revive international demand at D10 project launches and push achievable PSF upwards — a significant upside scenario for early Holland Plain buyers.

FAQ: Holland Plain GLS 2026 — Sim Lian Award

Why did only one developer bid for Holland Plain?

The sole-bid outcome reflects a combination of factors: the 65% Additional Buyer’s Stamp Duty on foreigners has substantially reduced the addressable buyer pool for CCR new launches, narrowing the demand basis that developers model when deciding how aggressively to bid. Many larger listed developers were also managing existing CCR inventory — including ongoing projects in D9 (Peck Hay Road, River Valley) — and may have chosen to preserve capital rather than pursue a concurrent D10 commitment. Sim Lian’s willingness to bid alone at S$1,491 psf ppr suggests the group has a specific product and pricing thesis that pencils out within that land cost, without requiring the foreign buyer premium that other developers may have deemed necessary to justify a higher bid.

Is Holland Plain’s 99-year leasehold a concern for long-term value?

Leasehold tenure is always a consideration in the CCR, where freehold and 999-year projects exist as alternatives. A 99-year leasehold in D10 will typically trade at a 10–15% discount to a freehold equivalent on a like-for-like basis. However, for buyers with a 10–20 year investment horizon, the leasehold discount at point of purchase can represent a compelling entry point, particularly if the area’s rental demand and capital growth story remain intact. The critical factor is the remaining lease at the point of future sale: a buyer who purchases a 99-year leasehold unit in 2028 and sells in 2043 will be transacting a unit with approximately 84 years remaining — still well above the HDB housing grant lease-coverage threshold and broadly financeable for the next generation of buyers.

When is the expected launch date for Sim Lian’s Holland Plain project?

Based on the typical CCR boutique development timeline — URA planning approvals (6–12 months), building plan submission and approval (3–6 months), showflat construction and marketing preparation (3–6 months) — the most likely preview window is Q3 to Q4 2027. Construction commencement would follow in late 2027 or early 2028, with a Temporary Occupation Permit (TOP) date of approximately 2030–2031. This is an estimate based on typical timelines; Sim Lian has not publicly confirmed any milestones.

What is the nearest MRT station to Holland Plain?

The Holland Plain site is located approximately 700 metres to 1 kilometre from Holland Village MRT station (Circle Line CC21 and Thomson-East Coast Line TE17). The dual-line interchange at Holland Village provides excellent connectivity to Botanic Gardens (CC19/DT9), Buona Vista (CC22/EWL), and Marina Bay (TE20/CC29/NS27/CE1). The Thomson-East Coast Line also connects northward to Caldecott (TE9/CC17) and southward through the city to Bayshore. For commuters working in the CBD or Orchard, Holland Village MRT offers a one- to two-interchange journey of approximately 20–30 minutes.

What schools are near Holland Plain?

The Holland Plain site benefits from proximity to some of Singapore’s most sought-after schools. Henry Park Primary School is located within approximately 1 kilometre, making the project eligible for Phase 2B HDB priority balloting for future owners with children. Nanyang Primary School in Buona Vista is another highly-regarded option within approximately 2 km. For international school demand — which drives a significant portion of D10 rental volumes — United World College of South East Asia (Dover campus), the Australian International School, and the German European School Singapore are all within a 3–4 km radius. This cluster is a major driver of family tenant demand at S$5,000–S$9,000 per month for 3- to 4-bedroom units.

Should I register interest now to buy Holland Plain?

Sim Lian has not opened any registration of interest (ROI) process as at 22 May 2026. The project has not been named, priced, or publicly marketed. It is premature to commit funds or make any financial arrangement based solely on this GLS award. LovelyHomes recommends monitoring Sim Lian’s official announcements, EdgeProp project launch alerts, and URA’s building plan approvals database for planning-permission milestones, which will give approximately 60–90 days’ advance notice before a formal marketing launch. Do not rely on unofficial registration lists maintained by individual marketing agents, as these carry no legal weight and may involve data privacy risks.

Related Articles

- URA 1H 2026 GLS Programme Analysis: All 9 Confirmed List Sites

- Bayshore Drive GLS Tender 2026: Singapore’s Largest Integrated Site

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Stamp Duty Calculator Singapore 2026: BSD and ABSD Guide

- Jurong Lake District Property Outlook 2026: Prices and Investment Potential

- Singapore New Home Sales April 2026: Q2 Rebound Under Way

Disclaimer: This article contains LovelyHomes’ independent analysis and projections based on publicly available URA GLS data, industry cost benchmarks, and comparable transaction information. Projected launch prices, unit mixes, timelines, and investment outcomes are estimates only and do not constitute financial advice, a solicitation to purchase, or a guarantee of any outcome. The Singapore property market is subject to government policy changes, interest rate movements, and macroeconomic conditions that may materially alter outcomes. Always consult a licensed real estate agent, licensed financial adviser, and qualified conveyancing solicitor before making any property purchase decision. Source data: URA GLS programme 1H 2026, URA REALIS, MND, CPF Board.

Click anywhere to close