Quick Answer — Toa Payoh at a Glance

- One of Singapore’s oldest and most established HDB towns, founded in 1966 and now home to approximately 100,000 residents in the Central Region.

- HDB resale prices range from S$450,000 for a 3-room flat to S$950,000+ for an EA/jumbo, with private condominiums trading at S$1.5M–S$1.8M and above.

- Served by Toa Payoh MRT and Braddell MRT on the North-South Line (NSL), with the Cross Island Line (CRL) Phase 2 expected around 2031 to further boost connectivity.

- Home to the HDB headquarters (HDB Hub), Toa Payoh Central, Toa Payoh Town Park, and a dense network of schools including CHIJ Primary (Toa Payoh) and Catholic High Primary (Bishan, adjacent).

- Gross rental yields range from 3.5–4.1% for HDB flats, while 3-year capital growth for HDB has tracked 7–9% — strong for a mature central estate.

- Most HDB flats in Toa Payoh are classified as Standard under the new HDB flat classification system, with a 5-year Minimum Occupation Period (MOP), though some newer BTOs in the Bidadari edge are Plus.

- Additional Buyer’s Stamp Duty (ABSD): Singapore Citizens buying their first residential property pay 0% ABSD; 20% applies on a second property.

Why Toa Payoh Remains One of Singapore’s Most Sought-After Mature Estates

Toa Payoh holds a special place in Singapore’s housing story. Developed from 1966 onwards as one of the Housing and Development Board’s (HDB) earliest planned new towns, it was purpose-built to rehouse residents cleared from kampungs (traditional villages) and fringe urban settlements. More than five decades later, Toa Payoh is not a relic — it is one of the most consistently in-demand estates on the HDB resale market, valued by Singaporeans for its central location, mature infrastructure, and exceptional school choices.

The estate sits in the Central Region of Singapore, bounded broadly by Novena (District 11) to the west, Bishan to the north, Potong Pasir to the east, and Kallang to the south. Its location inside the mature Central Region means demand from buyers willing to pay a premium for proximity to the city centre, and supply that is naturally constrained because no new large-scale HDB development is possible within the existing town footprint.

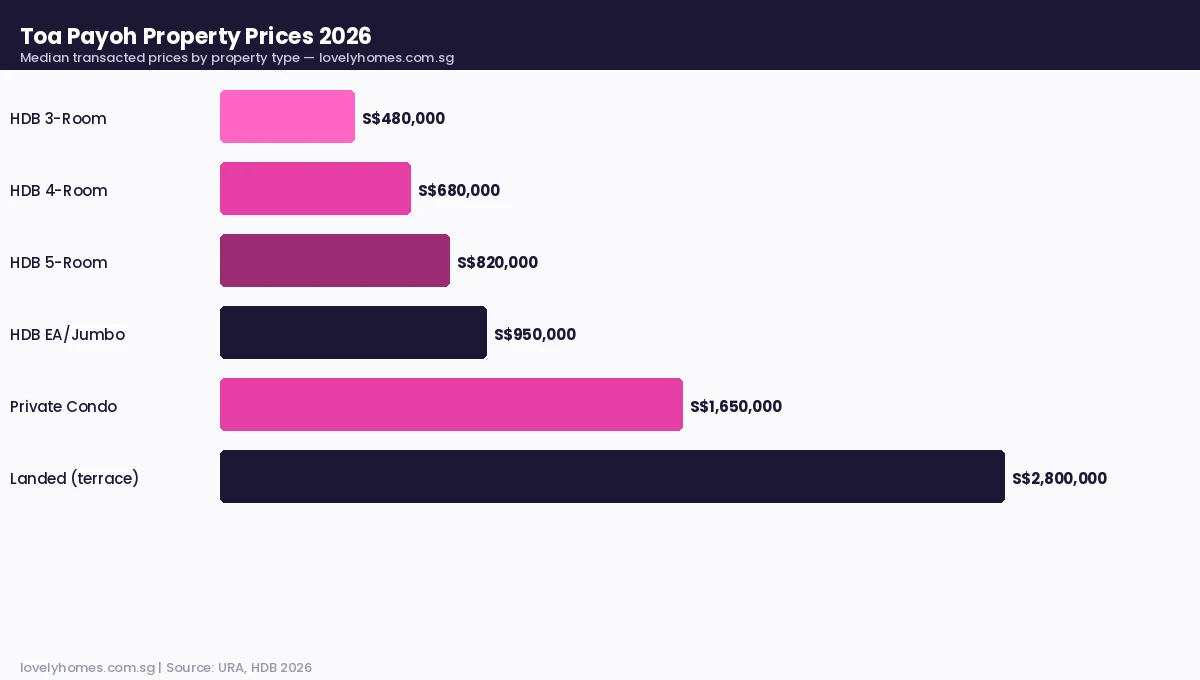

Property Prices in Toa Payoh — What You Can Expect to Pay in 2026

Toa Payoh commands a meaningful premium over most OCR (Outside Central Region) estates, reflecting its central location and the scarcity of supply in a fully built-out town. Based on URA and HDB transaction data through Q1 2026, the following price benchmarks apply.

| Property Type | Price Range (2026) | Median / Typical | Notes |

|---|---|---|---|

| HDB 3-Room | S$430,000 – S$560,000 | ~S$480,000 | Older blocks near Toa Payoh Central; high floor commands premium |

| HDB 4-Room | S$600,000 – S$800,000 | ~S$680,000 | Most common transaction type; blocks near HDB Hub attract strong demand |

| HDB 5-Room | S$720,000 – S$960,000 | ~S$820,000 | Large flats on upper floors can approach or exceed S$1M |

| HDB EA / Jumbo | S$880,000 – S$1,100,000 | ~S$950,000 | Limited supply; these trade well above median given scarcity |

| Private Condominium | S$1,400,000 – S$2,100,000 | ~S$1,650,000 | Gem Residences (2019 TOP) and legacy condos in D12/D20 |

| Landed (Terrace) | S$2,400,000 – S$3,500,000 | ~S$2,800,000 | Mainly inter-terrace units along Toa Payoh fringe streets |

A particular feature of Toa Payoh’s resale market is that record transactions regularly break the S$1 million mark for 5-room and EA flats. In Q1 2026, at least two 5-room units transacted above S$950,000, reflecting continued appetite from buyers who want central living without private-property stamp duty exposure. The MOP wave releasing approximately 1,200 Toa Payoh-adjacent flats in 2026 is expected to add transactional volume but not necessarily to dampen prices, given the persistent supply deficit in this mature zone.

MRT Connectivity and Getting Around Toa Payoh

Toa Payoh’s primary transport backbone is the North-South Line (NSL), with two stations serving the estate: Toa Payoh MRT (NS19) and Braddell MRT (NS18). Toa Payoh MRT sits directly at the heart of the town’s commercial hub, making it one of the most walkable MRT-to-estate combinations in Singapore. Travel time to Raffles Place is approximately 16 minutes; to Orchard, about 10 minutes.

Beyond the NSL, residents benefit from an extensive network of feeder buses connecting to Bishan (NS-CCL interchange), Novena, and Potong Pasir (NEL). The Land Transport Authority (LTA) has confirmed that Cross Island Line (CRL) Phase 2, expected around 2031, will include a station in the Hougang-Toa Payoh corridor, which analysts at CBRE Research project will add a further 5–8% price uplift to properties within a 500-metre radius of any new CRL station.

Schools in Toa Payoh — One of Singapore’s Premier School Corridors

School proximity is a major driver of buyer demand in Toa Payoh. The estate and its immediate neighbours contain an unusually high concentration of well-regarded primary and secondary schools, including several that are highly sought-after for Primary 1 registration purposes.

Within and directly adjacent to Toa Payoh, families benefit from access to CHIJ Primary (Toa Payoh) — one of Singapore’s most popular girls’ primary schools — as well as Kheng Cheng School, Pei Chun Public School, and Marymount Convent Primary. Secondary options in the vicinity include CHIJ Secondary (Toa Payoh), Catholic High School (Bishan, Phase 2B priority for Toa Payoh addresses), and, at the junior college level, several JCs reachable within 15–20 minutes by MRT.

The Ministry of Education’s (MOE) school registration framework means that within 1 km of a school, Phase 2A and 2B registration confers significant advantage in ballot. Families purchasing specifically for school access should verify school registration zones each year, as boundaries are subject to MOE review.

Retail, Food, and Daily Living in Toa Payoh

Toa Payoh Central is one of the best-served HDB town centres in Singapore. HDB Hub, the Housing and Development Board’s own headquarters, sits at the heart of the estate and anchors a retail podium — Toa Payoh Mall — that includes a Cold Storage supermarket, food court, and dozens of specialty retailers. The adjoining Toa Payoh Town Park provides approximately 6.5 hectares of green recreational space within easy reach of most flats, while the Toa Payoh Sports Hub (formerly Toa Payoh Stadium) services community sports needs.

Food options are outstanding: the wet market and hawker centres at Toa Payoh Lorong 1, Lorong 4, and Lorong 7 are among the most established in central Singapore. Residents are also a short bus or MRT ride from the Novena cluster (for major medical facilities and premium retail) and Bishan Junction 8.

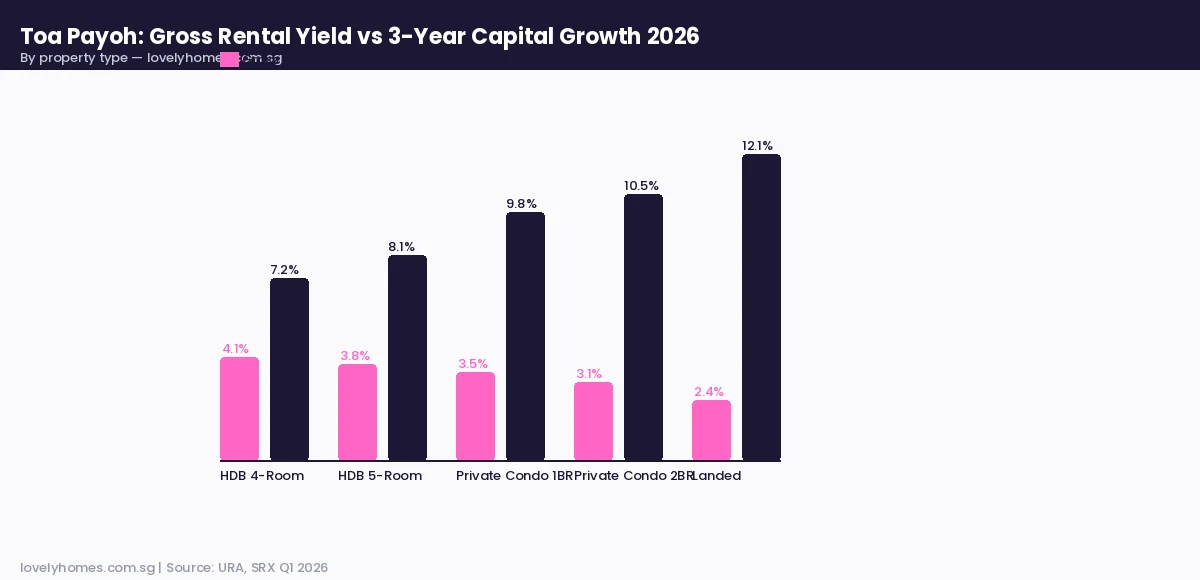

Investment Analysis — Rental Yields and Capital Growth Outlook for 2026

For investors evaluating Toa Payoh, the key question is whether the premium entry cost is justified by rental income and capital appreciation. On both counts, the data is broadly supportive, though buyers should manage expectations on yield given the higher entry price.

HDB 4-room flats in Toa Payoh command gross rents of approximately S$2,200–S$2,600 per month in 2026, translating to a gross rental yield of around 3.8–4.1% on a median acquisition cost of S$680,000. This compares favourably with OCR estates like Tampines or Pasir Ris, where similar-sized flats yield 3.5–3.8% on higher transacted prices. Private condominiums in the Toa Payoh catchment typically yield 3.2–3.5%, with 1-bedroom units (S$1.4M–S$1.6M) offering the best yield-to-capital ratio.

On capital growth, URA and SRX data show that HDB resale prices in mature central estates like Toa Payoh appreciated approximately 7.2–8.5% over the three years to Q1 2026, outperforming the national HDB resale index (which rose approximately 5.8% over the same period). Private condo capital growth in the D12/D20 catchment has been stronger, at approximately 9–11%, on the back of limited new supply and persistent upgrader demand.

What This Means for Buyers — Toa Payoh as a Long-Term Hold

Toa Payoh is not a speculative play — it is a quality-of-life and long-term capital preservation story. The estate’s age means most HDB flats have a remaining lease of 50–65 years, which has implications for CPF usage (subject to the CPF board’s Lease Buyback rules and pro-rated OA withdrawal cap) and for eventual en-bloc potential in the private residential pockets. Buyers considering HDB should verify the remaining lease and applicable CPF withdrawal limits before budgeting.

For Singapore Citizens using HDB as a stepping-stone — buy a resale flat, benefit from the School Proximity advantage, and then upgrade when ready — Toa Payoh offers a credible path. The estate’s consistent demand means resale liquidity is strong, and the likely CRL Phase 2 uplift adds a forward-looking catalyst.

What Might Come Next — Toa Payoh in 2027 and Beyond

Singapore’s Urban Redevelopment Authority (URA) has not announced major new development plans specific to Toa Payoh in the 2025 Master Plan cycle, which is unsurprising given that it is already a fully built-out mature estate. However, several factors bear watching. First, the CRL Phase 2 alignment and exact station locations will, when confirmed, reprice properties within walking distance of new stations — likely in the 2028–2030 timeframe ahead of actual completion. Second, the broader national trend of HDB flat upgrading — facilitated by the progressive privatisation of Singapore’s housing market — means the pool of buyers willing to pay S$800,000+ for a 5-room flat continues to deepen. Third, the ageing HDB stock in Toa Payoh raises the speculative (but unconfirmed) possibility of Selective En-Bloc Redevelopment Scheme (SERS) designations over the medium term, which would provide a government-administered exit at fair value for affected flat owners.

Worked Example — Mr & Mrs Ong: HDB Upgrader Buying a Toa Payoh 5-Room Resale

Mr & Mrs Ong are a Singapore Citizen couple. They sold their Ang Mo Kio 4-room HDB flat in February 2026 for S$780,000 and are now buying a Toa Payoh 5-room resale flat at S$870,000. Because they sold their first property before completing the purchase, they are buying their new flat as their only property — ABSD = 0%.

- Purchase price: S$870,000

- BSD (progressive on S$870k): S$3,600 + S$4,500 + S$15,600 = S$23,700

- ABSD: S$0 (SC, 1st property at point of purchase)

- HDB loan (up to 80% of purchase price): S$696,000 at 2.6% p.a.

- Monthly instalment (25-year loan): approximately S$3,160

- MSR check (must not exceed 30% of gross monthly income): requires household income of at least S$10,533 — well within the S$14,000 ceiling for 5-room resale

- Cash needed upfront: BSD S$23,700 + 5% cash downpayment S$43,500 = S$67,200; balance S$130,500 downpayment can come from CPF OA

- CPF OA balance available from AMK sale: estimated S$280,000 (post-refund, net of original principal)

Verdict: Feasible for a dual-income household earning S$11,000–S$14,000/month. The upgrade from a 4-room AMK flat to a 5-room Toa Payoh flat costs a net outlay of approximately S$90,000 (after CPF proceeds) but gives school-corridor access and improved central connectivity.

Frequently Asked Questions about Toa Payoh Property

Is Toa Payoh a good place to buy property in 2026?

Yes, for most buyer profiles who value central location, school access, and strong resale liquidity. Toa Payoh consistently ranks among the top HDB estates by transaction volume and median price per square foot. The main caveat is the ageing lease profile of older HDB blocks — buyers should check the remaining lease and confirm CPF withdrawal eligibility before committing. For private property investors, the limited supply of condominiums in the estate means capital values are well-supported but entry prices are high.

Which MRT stations serve Toa Payoh?

Toa Payoh is served by two North-South Line (NSL) stations: Toa Payoh MRT (NS19) and Braddell MRT (NS18). Toa Payoh MRT is integrated with the HDB Hub and town centre, making it exceptionally walkable. The Land Transport Authority (LTA) has confirmed Cross Island Line (CRL) Phase 2 for completion around 2031, which will add a new interchange point in the broader corridor. For CCL connectivity, the Bishan interchange is accessible via a short bus ride.

What are HDB resale prices in Toa Payoh in 2026?

Based on URA and HDB Q1 2026 data, typical resale prices are: 3-room S$430,000–S$560,000; 4-room S$600,000–S$800,000; 5-room S$720,000–S$960,000; EA/jumbo S$880,000–S$1,100,000. High-floor, centrally located units in sought-after blocks (particularly near Toa Payoh Central and the HDB Hub) can exceed the upper end of these ranges. The S$1 million threshold for HDB 5-rooms in Toa Payoh has been crossed multiple times in 2025–2026.

How does Toa Payoh compare with Bishan and Ang Mo Kio?

All three are mature central estates, but Toa Payoh commands slightly higher HDB prices than Ang Mo Kio for equivalent flat types, reflecting its proximity to the city core and its school corridor premium. Bishan is broadly comparable to Toa Payoh in pricing and also benefits from the NSL-CCL interchange. Ang Mo Kio prices are typically 8–15% lower than Toa Payoh for equivalent flat sizes, with the gap reflecting the latter’s greater walkability to the CBD. For private condos, the difference is more pronounced: Bishan Sky Habitat-level stock is priced similarly to Toa Payoh private condos, while AMK condos typically trade at a slight discount.

Can foreigners or PRs buy HDB resale flats in Toa Payoh?

Singapore Permanent Residents (SPRs) may purchase HDB resale flats, subject to forming an eligible family nucleus (for example, an SPR married to another SPR, or an SPR with SPR children). However, SPRs must pay 5% ABSD on their first Singapore residential property and cannot apply for CPF Housing Grants on the resale market. Foreigners (non-PRs) are not eligible to purchase HDB flats under any circumstances. For private condominiums in the area, foreigners pay 60% ABSD under the April 2023 cooling measures regime.

Are there any new BTO launches planned for Toa Payoh?

As a fully built-out mature estate, Toa Payoh has very limited capacity for new BTO projects. HDB launches new flats in Toa Payoh only when sites are freed up through redevelopment of existing stock. The most recent HDB BTO in the Toa Payoh area was a small Plus-classified project at the Bidadari boundary in 2025. Buyers interested in new HDB flats in the Central Region should monitor the HDB website for BTO launch announcements, as central-region BTOs are typically heavily oversubscribed.

Is the lease decay a concern for Toa Payoh HDB flats?

Yes, and buyers should take this seriously. Many of Toa Payoh’s HDB blocks were built in the late 1960s and 1970s, meaning remaining leases of 45–60 years as of 2026. Flats with fewer than 60 years remaining are subject to a pro-rated CPF withdrawal cap under the CPF Board’s rules, and banks may apply stricter loan-to-value limits. For older flats (built before 1985), buyers should model their maximum CPF drawdown carefully before signing any OTP, and consult a licensed conveyancing lawyer on the financing structure. The government has introduced several programmes (including the Lease Buyback Scheme and VERS — though VERS details remain under study) to address lease decay in older flats.

Related Articles

- Bishan Neighbourhood Guide Singapore 2026

- Ang Mo Kio Neighbourhood Guide Singapore 2026

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Stamp Duty Calculator Singapore 2026: Complete BSD and ABSD Guide

- First-Time Property Buyer Checklist Singapore 2026

- HDB Flat Subletting Singapore 2026: Complete Guide

- Home Insurance Singapore 2026: Complete Guide

Disclaimer: This guide is for general information only and does not constitute legal, financial, or property advice. Property prices, stamp duty rates, CPF rules, and HDB policies change over time. Always verify current prices through the URA Real Estate Information System (REALIS) and HDB’s official website, and consult a licensed conveyancing lawyer or financial adviser before entering any property transaction.

Click image or press Esc to close

0 Comments