Quick Answer: En Bloc Singapore 2026 — Key Facts at a Glance

- What is en bloc? A collective sale where the majority of owners in a strata development agree to sell the entire site to a single buyer — typically a property developer.

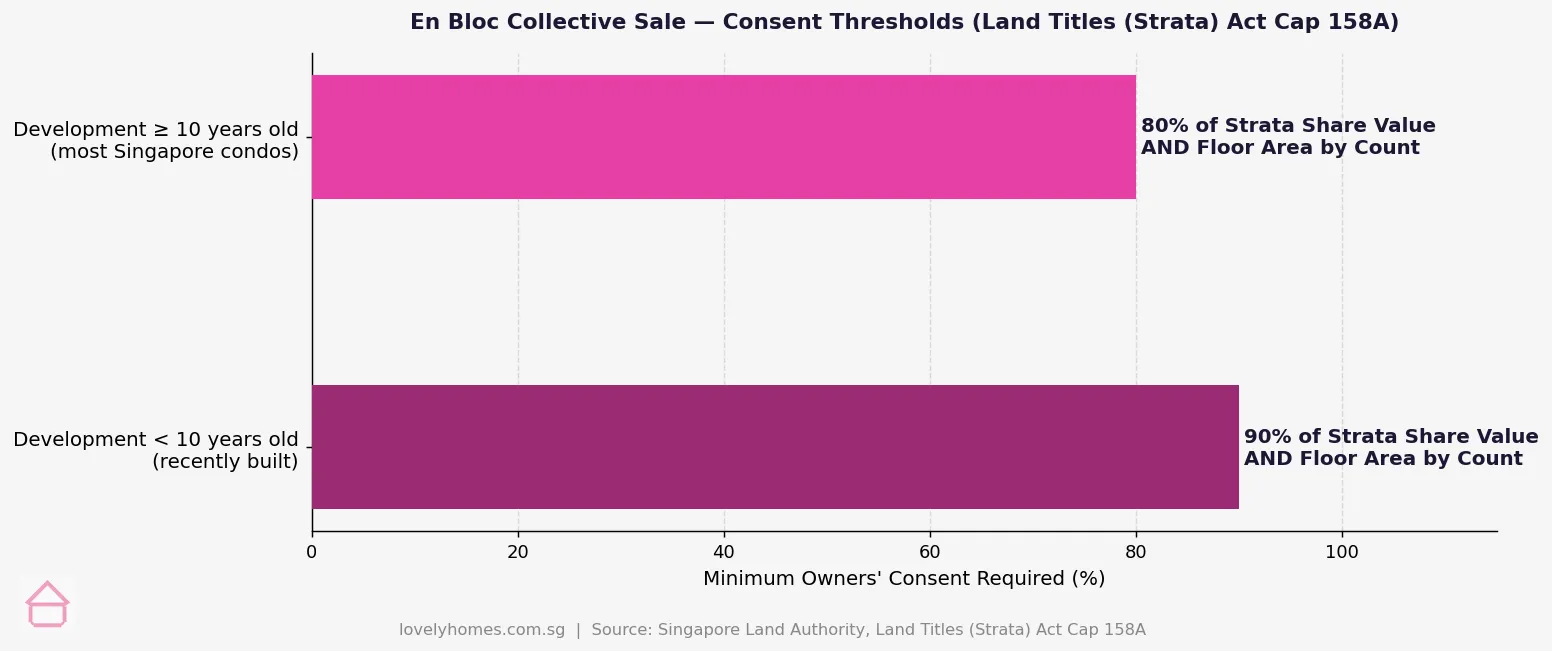

- Consent threshold: 80% (development ≥ 10 years old) or 90% (younger than 10 years) — measured by strata share value AND floor area simultaneously.

- Legal framework: Land Titles (Strata) Act (Cap 158A), administered by the Singapore Land Authority (SLA).

- Minority protection: Dissenting owners may object to the Strata Titles Board (STB); the STB may still approve if the sale is not prejudicial to the minority.

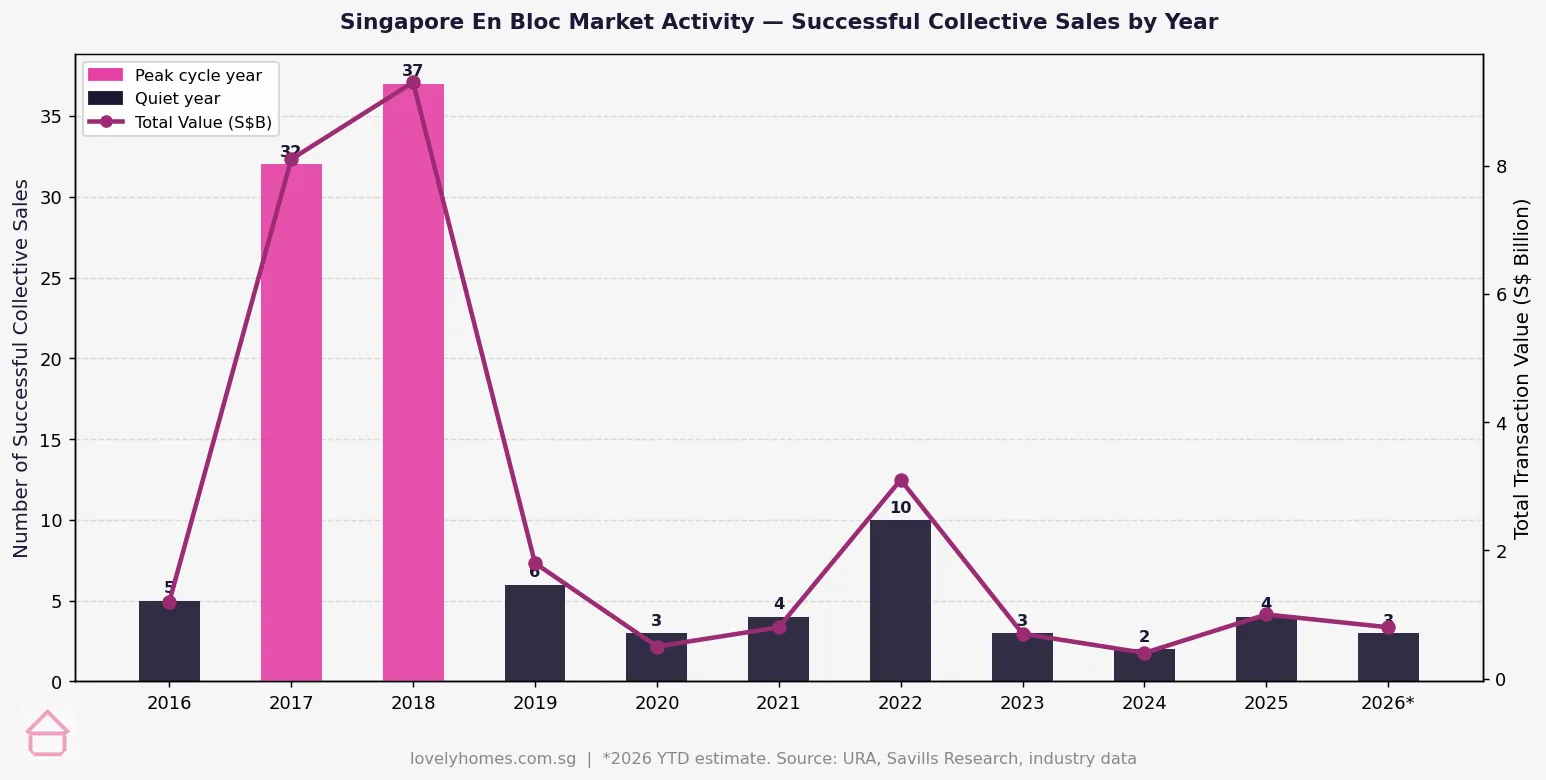

- Market cycle: Peak was 2017–2018 (~S$8–9 billion/year). Subdued since: 2–10 completions a year from 2019 to 2026.

- Owner proceeds: Generally capital in nature and not subject to income tax. Seller’s Stamp Duty (SSD) applies if sold within 3 years of purchase.

- Developer ABSD: 35% entity rate; conditional 30% remission if all units sold within 5 years of the collective sale order.

- Timeline: Typically 18–30 months from Collective Sale Committee formation to completion.

What Is an En Bloc Sale and Why Does It Happen?

In Singapore, an en bloc sale — formally a collective sale — occurs when the majority of owners in a strata-titled development agree to sell the entire site to a single buyer, usually a property developer intending to demolish the existing buildings and redevelop the land. Singapore’s Land Titles (Strata) Act (Cap 158A) allows a supermajority of owners to proceed over minority objections, provided the statutory criteria are met and, where necessary, the Strata Titles Board (STB) approves the application. The economic driver is land scarcity: ageing private estates on prime sites with low plot ratios relative to current URA Master Plan permissions present lucrative redevelopment opportunities, and owners can achieve premiums over individual market value that would be impossible through a solo sale.

Legal Framework: The Land Titles (Strata) Act

The Land Titles (Strata) Act (Cap 158A) (LTSA), administered by the SLA and the STB, is the primary legislation governing collective sales. Key amendments in 1999, 2007, and 2010 progressively strengthened minority-owner protections — including requirements for independent financial advice for elderly or low-income owners, stricter disclosure obligations, and clearer rules on how proceeds must be distributed. Under the LTSA, every collective sale must satisfy two tests: the consent threshold (required supermajority by strata share value and floor area) and the good faith test (the sale must be conducted fairly, taking into account sale price, distribution method, and any relationships between the purchaser and CSC members).

How Consent Is Measured: Strata Share Value and Floor Area

The threshold must be met on two dimensions simultaneously: by strata share value (a weighting assigned to each unit at strata subdivision) and by floor area (the actual area of each unit in square metres). A development where 82% of owners by strata share value have signed the Collective Sale Agreement (CSA), but only 78% by floor area, has not yet met the 80% bar. This dual requirement protects against situations where a few large-unit owners could dominate the value calculation while a majority of smaller-unit owners might not support the sale.

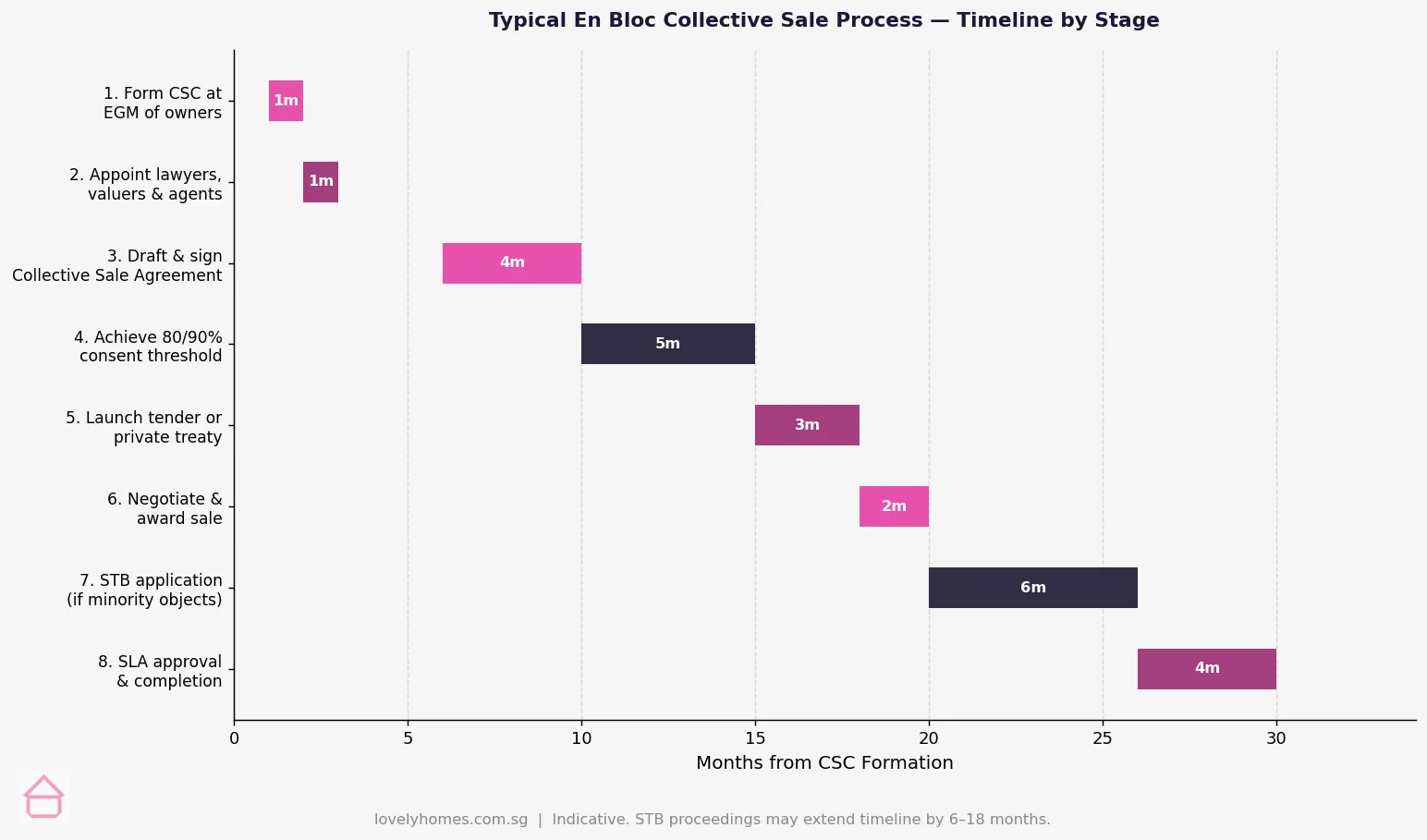

The En Bloc Process: Stage by Stage

A collective sale follows a defined statutory sequence. The timeline below is typical, though individual developments vary in complexity and duration.

Stage 1 — Forming the Collective Sale Committee (CSC)

At least 20% of subsidiary proprietors by share value must requisition an Extraordinary General Meeting (EGM). At the EGM, owners vote to form a CSC — typically 3 to 14 elected owner-members — who manage the sale process on behalf of all owners. The CSC owes statutory duties of care to all owners, including those who oppose the en bloc.

Stage 2 — Appointing Professional Advisers

The CSC appoints a solicitor, an independent valuer (to establish the reserve price and market value), and a marketing agent. LTSA conflict-of-interest rules require that all three be independent — no relationship may exist between these advisers, the CSC, and the prospective purchaser.

Stage 3 — Drafting and Signing the Collective Sale Agreement

The CSA specifies the reserve price, distribution method, marketing approach, and conditions of sale. It must be made available for inspection by all owners before signatures are collected. The LTSA imposes a 12-month window to achieve the required threshold — if the deadline lapses without success, the process must restart from the EGM stage.

Stage 4 — Public Tender or Private Treaty

Once the threshold is met, the site is marketed via a minimum 10-week public tender. If the tender produces no acceptable bid, the CSC may pursue private treaty negotiations for up to 10 months. Any bid at or above the reserve price may be accepted by the CSC.

Stage 5 — STB Application (If Required)

Non-signing owners have 21 days after notification of the sale to file objections with the STB. If objections are raised, the CSC applies to the STB for approval. The STB holds hearings and may approve the sale if satisfied it was conducted in good faith and is not genuinely prejudicial to the minority objectors. Where no objections are filed, the sale proceeds directly to SLA without STB involvement.

Stage 6 — SLA Completion

The SLA processes the legal title transfer. The developer pays the agreed price; all owners receive their allocated proceeds per the CSA distribution formula. The development is then vacated, demolished, and redeveloped.

Singapore En Bloc Market: History and Current Activity

Singapore’s en bloc market moves in cycles driven by land prices, developer appetite, cooling measures, and interest rates. The 2017–2018 boom was fuelled by a prolonged low-interest-rate environment and strong developer land-banking demand following the 2013–2016 property price trough. The Government responded decisively in July 2018: developer ABSD was raised from 15% to 25%, effectively pricing many en bloc deals out of developer feasibility. Since 2019, annual completions have ranged from just 2 to 10, versus more than 30 at the peak.

In 2026, the market remains quiet. Developer ABSD is now 35% for entities, with a conditional 30% remission if all units are completed and sold within 5 years of the collective sale order — still a significant carrying-cost burden. Rising construction costs (up approximately 20–30% since 2020) further compress developer margins. Industry analysts note that a meaningful revival requires either a reduction in developer ABSD or a significant moderation in owner price expectations — or both.

Summary Table: Key En Bloc Parameters

| Parameter | Detail | Source / Reference |

|---|---|---|

| Consent threshold (≥ 10 years) | 80% by strata share value AND floor area | LTSA Cap 158A s. 84A |

| Consent threshold (< 10 years) | 90% by strata share value AND floor area | LTSA Cap 158A s. 84A |

| CSA signing window | 12 months to achieve the threshold | SLA guidelines |

| Public tender period | Minimum 10 weeks | LTSA s. 84C |

| Private treaty (post-failed tender) | Up to 10 months | SLA guidelines |

| Objection window | 21 days after owners are notified of the sale | LTSA, STB Rules |

| STB process duration | Typically 6–18 additional months | STB, SLA data |

| SSD for individual owners | 12%/8%/4% if sold within 1/2/3 years of purchase | IRAS Stamp Duties Act Cap 312 |

| BSD for developer (entity) | Progressive 1–6% on purchase price | IRAS |

| ABSD for developer (entity) | 35%; conditional 30% remission if all units sold within 5 years | IRAS, Ministry of Finance |

Worked Example: What Owners Receive in an En Bloc Sale

Case Study: Hillview Gardens Collective Sale (Illustrative Example)

Background: Hillview Gardens is a fictional 1995-built condominium of 120 units in District 23 (Bukit Timah area). At 31 years old, the 80% consent threshold applies. Land area approximately 7,800 sqm; URA Master Plan plot ratio 2.1; estimated redevelopment GFA approximately 16,380 sqm (176,250 sq ft).

Reserve price: S$220 million (~S$1,249 psf ppr). Tender result: A developer bids S$238 million (~S$1,351 psf ppr), above the reserve.

Indicative owner proceeds (blended strata share value + floor area formula):

- 2-bedroom owner (86 sqm, share value 12): approximately S$1.62M

- 3-bedroom owner (126 sqm, share value 18): approximately S$2.45M

- Penthouse owner (248 sqm, share value 35): approximately S$4.87M

SSD consideration: The 2BR owner who purchased in October 2024 at S$1.05M and receives S$1.62M triggers SSD at 4% (sold in year 2 of ownership after purchase) — approximately S$64,800 payable to IRAS before netting out proceeds.

Developer cost summary: S$238M land + BSD approximately S$8.8M + ABSD 35% = S$83.3M ABSD upfront (S$71.4M conditionally remitted if 5-year sell-down target met, leaving net S$11.9M non-remittable ABSD). Construction estimated at S$97–115M for approximately 200 new 99-year leasehold units. Total development outlay approximately S$350–370M.

Why This Matters for Singapore Homeowners and Investors

En bloc optionality — the possibility of a collective sale at a significant premium over individual market value — is a genuine pricing factor in Singapore’s property market. Buyers of units in ageing estates with favourable plot ratios and URA Master Plan zoning frequently factor this in. Understanding the en bloc process allows owners to participate meaningfully in CSC elections, evaluate distribution formulas, and make informed decisions about whether to sign the CSA or exercise their statutory rights as minority objectors. For property investors, en bloc adds a second return pathway alongside rental yield and capital appreciation — albeit a probabilistic one, since the majority of developments never complete a collective sale.

What Might Come Next: En Bloc Outlook for 2026–2028

A revival in Singapore’s en bloc market depends primarily on developer ABSD and construction-cost trajectories. At the current 35% rate (net effective approximately 5% after conditional remission), most en bloc pricing equations remain tight for developers. Any easing of the developer ABSD rate — which requires a Ministry of Finance decision — would likely unlock significant pent-up activity. Many developments formed between 2007 and 2015 have already crossed the 10-year threshold (allowing the lower 80% consent bar) and are candidates for future en bloc bids. Industry analysts place the probability of a new en bloc mini-cycle at moderate-to-high by 2028–2030, contingent on interest-rate normalisation and government policy direction. Separately, the Government’s Voluntary Early Redevelopment Scheme (VERS) — a public-sector counterpart for ageing HDB estates — continues in pilot stage, signalling the Government’s long-term commitment to estate renewal beyond the private sector alone.

Frequently Asked Questions

Can I be forced to sell my property in an en bloc even if I did not sign the CSA?

Yes. Once the consent threshold has been met and either no objections are filed within 21 days or the STB approves the application despite minority objections, the collective sale order is legally binding on all subsidiary proprietors — including those who did not sign the CSA. The STB will deny an application only where the sale was not conducted in good faith or where it finds the transaction to be genuinely prejudicial to the minority. In practice, the STB approves the overwhelming majority of collective sale applications brought before it. This binding mechanism is a deliberate feature of Singapore’s regime, designed to enable urban renewal without individual vetoes indefinitely blocking community-level redevelopment decisions.

How is my individual share of the en bloc proceeds calculated?

The distribution method must be specified in the Collective Sale Agreement and disclosed to all owners before they are invited to sign. The three most common methods are: distribution by strata share value (the weighting assigned at the time of strata subdivision), by floor area (the actual size of each unit), or a blended formula combining both in agreed proportions. Disputes over the distribution formula are one of the most common reasons en bloc attempts fail to reach the consent threshold — owners of larger units generally favour floor-area distribution, while those with relatively high strata share values may prefer the share-value method.

Is profit from an en bloc sale subject to income tax in Singapore?

For most individual property owners, proceeds from an en bloc sale are treated as capital gains and are therefore not subject to income tax — Singapore does not impose a general capital gains tax on real property. However, Seller’s Stamp Duty (SSD) applies if the property was acquired within the 3 years prior to the collective sale: 12% in the first year, 8% in the second year, and 4% in the third year (calculated on the higher of sale price or market value). Owners who hold the property for more than 3 years pay no SSD. Property traders or those who purchased specifically for resale may be taxed differently by IRAS. Consult a qualified tax adviser if your circumstances are complex.

What happens to tenants when an en bloc sale completes?

Tenants have no legal right to block or delay a collective sale. Existing tenancy agreements remain binding on the owner (and, during the transition, on the developer-purchaser) until legal completion. Once completion occurs, the developer takes vacant possession and all tenancies must end. Landlords are generally obliged to give reasonable notice and return security deposits. Tenants should review their tenancy agreements carefully — en bloc completion is a termination event typically outside the landlord’s direct control, and some agreements include specific clauses addressing this scenario.

How does developer ABSD affect the en bloc price owners receive?

Developer ABSD is currently 35% of the land purchase price for entities, with a conditional 30 percentage-point remission if the developer completes the project and sells all units within 5 years — leaving a non-remittable 5% ABSD minimum. On a S$300M en bloc transaction, this means S$105M in upfront ABSD, of which S$90M may eventually be remitted, but S$15M is permanently sunk. This significantly raises the bar for developer feasibility and directly depresses the price developers will bid for en bloc sites. The higher the developer ABSD, the wider the gap between owner expectations and developer bids — which is why the rate has been the primary dampener on en bloc activity since the July 2018 cooling measures.

What is the difference between an en bloc and a Government Land Sales (GLS) site?

A Government Land Sales (GLS) site is released directly by the Government — typically through the URA or the HDB — via public tender to developers. GLS sites are usually vacant or cleared land with no existing private owners to compensate. An en bloc site is privately held: the developer must negotiate with existing owners, obtain a collective sale order, and pay a premium above individual resale values. GLS is faster, more predictable, and more transparent in timeline; en bloc offers locations in established neighbourhoods that the Government does not hold land to release, and can provide superior amenity and locational attributes for certain buyers. Developers typically pursue both channels simultaneously as part of their land-banking strategies.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Complete Guide 2026: BSD, ABSD, SSD and ACD Explained

- Singapore Property Selling Guide 2026: Step-by-Step Guide for HDB, Condo and Landed

- Singapore Property Inheritance Guide 2026: Wills, CPF Nominations and Stamp Duty

- Singapore CPF Property Withdrawal Limits 2026: OA Valuation and Withdrawal Limits Explained

- Singapore Bridging Loan Guide 2026: Bridge the Gap Between Selling and Buying Property

Disclaimer

This article is for general informational and educational purposes only and does not constitute legal, tax, or financial advice. En bloc collective sale laws, ABSD rates, Strata Titles Board procedures, and Seller’s Stamp Duty rules are subject to change by the Singapore Government. Owners and investors considering participation in a collective sale should engage a Singapore-qualified solicitor experienced in collective sales, an independent valuer registered with IRAS, and a licensed property agent registered with the Council for Estate Agencies (CEA). For the most current legal requirements, refer to the Singapore Land Authority (sla.gov.sg), IRAS (iras.gov.sg), the Strata Titles Board (stratatitlesboard.gov.sg), and the Urban Redevelopment Authority (ura.gov.sg).

0 Comments